Sample Category Title

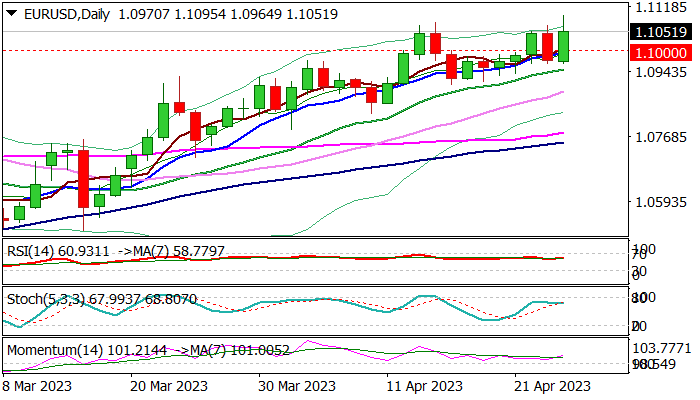

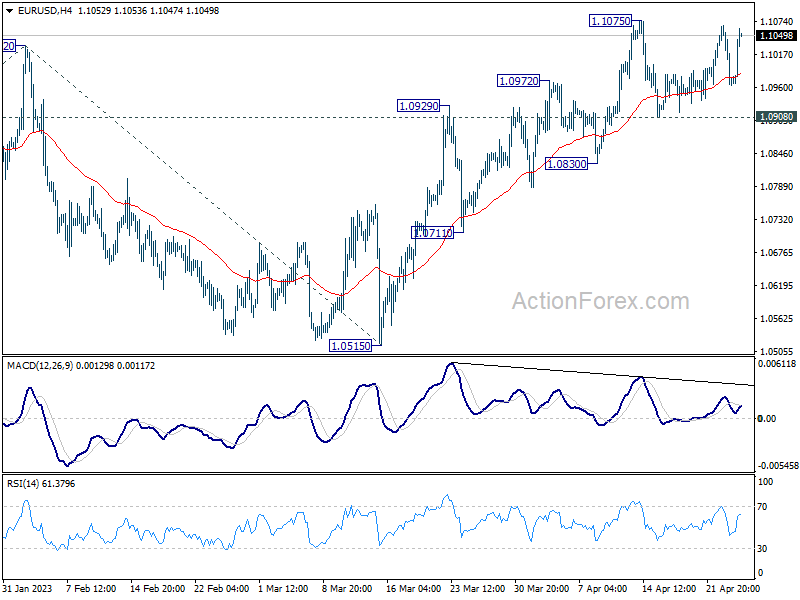

EUR/USD: Bulls Return to Play and Hit New 2023 High

The Euro was sharply up on Wednesday, advancing over 1% until early US session, on weaker dollar and better than expected German economic data, which so far offset fragile risk sentiment on renewed concerns about the US banking sector, after shares of troubled First Republic Bank extended sharp fall into second consecutive day.

Fresh rally returned above 1.10 level and hit new 2023 high today (1.1095), reversing a negative signal from Tuesday’s bearish engulfing, into bullish signal, as bulls fully reversed previous day’s nearly 0.7% drop and on track to form bullish engulfing candlestick pattern today.

Bullish technical studies contribute to brightening near-term outlook, though sustained break above former top at 1.1075 (Apr 14) is needed to signal bullish continuation.

Dips on partial profit-taking after today’s strong bullish acceleration, should stay above psychological 1.10 support (reinforced by rising daily Tenkan-sen) to keep bulls in play.

Break of 1.1075/95 tops would open way for extension of the second leg of larger uptrend from 0.9535 (2022 low) and expose targets at 1.1184 (31 Mar 2022 top) and 1.1223 (Fibo 61.8% of 1.2266/0.9535 downtrend.

Res: 1.1075; 1.1095; 1.1184; 1.1223

Sup: 1.1000; 1.0964; 1.0950; 1.0909

Sunset Market Commentary

Markets

European bond markets started the day still on a solid footing (gap open), betting we’ll see a continuation of yesterday’s trends even as overnight news flow was extremely thin. They soon lost dash though, morphing into sideways trading afterwards. German yield currently lose 6.5 (bps) at the front end and gain slightly at the very long end. US yields are 1.6 bps (30-yr) to 3.1 bps (3-yr) lower. Main European stock markets cede up to 1%, but are also off worst intraday levels. Key US indices are back in positive territory following yesterday short-lived First Republic scare. EUR/USD resumed its uptrend with the pair in a technical acceleration moving beyond the YTD highs in the 1.1070/75 area. First resistance stands at 1.1274 (62% retracement on drop between early 2021 and September 2022). Less liquid crosses like EUR/AUD, EUR/NZD and EUR/CAD are showing similar technical accelerations. EUR/GBP gains are more contained with the pair rising from 0.8842 to 0.8872. Eco data were few and failed to give any meaningful direction. Headline US durable goods orders rose more than expected in March (3.2% M/M) but were diluted by non-defense aircraft orders. Capital goods shipments non-defense ex-aircraft (proxy for investments in GDP calculations) fell 0.4% M/M following a downwardly revised -0.4% M/M in February. German May consumer confidence unexpectedly increased from -29.3 to -25.7 (vs -28 expected), the highest level since April 2022. The German government raised its 2023 GDP forecast from 0.2% in January (and -0.4% in October) to 0.4%. Next year, the government expects growth to accelerate to 1.6%, economy minister Habeck said (from 1.8% in January). Inflation forecasts stand at 5.9% this year (from 6.9% in 2022) and 2.7% in 2024.

Focus now turns to GDP and inflation numbers to released tomorrow and especially on Friday. Tomorrow we’ll see Belgian inflation and US Q1 GDP figures. Friday starts with April Tokyo inflation and the Bank of Japan policy meeting, but the focal point will be French/Spanish/German inflation numbers and to a lesser extent EMU Q1 GDP. The US eco calendar contains March PCE deflators, Q1 employment cost index and Chicago PMI. The data won’t derail Fed plans to lift policy rates by 25 bps next week, but could make or break our base case for a 50 bps ECB hike.

News & Views

Sweden’s central bank jacked up rates by 50 bps to 3.5% today. The increase was necessary to bring back inflation back to the 2% target. Both headline and underlying price pressures eased in March but did so (much) less than the Riksbank anticipated in its February Monetary Policy report. Inflation forecasts as a result were revised upwards, from 5.5% to 5.9% this year and from 1.9% to 2.3% in 2024. Growth this year should be less worse than previously thought (-0.7% vs -1.1%) but 2024 growth momentum was reduced to 0.2% (vs 0.9%). The Riksbank projected another 25 bps rate hike in either June or September to 3.75%. The Swedish krone was disappointed. It hoped for something more, if only because the weak currency (officially) became matter of concern to the central bank since February. It barely left the multiyear lows since then. The fact that two members out of six voted for a smaller hike and a shallower rate path didn’t help either. EUR/SEK retested the 2020/2023 highs around 10.40 after the decision. Swedish swap yields, already down going into the policy outcome, extended declines to almost 15 bps at the front end of the curve.

The European Commission today unveiled proposals to revise the current rules on public spending. These have been suspended in the wake of the Covid and then energy crisis but are set to return next year. Deficit and public-debt limits remain at the familiar 3% and 60% of GDP but individual member states are given greater ownership of their debt-reduction plans. They are required to set out plans with fiscal targets, measures to address imbalances, priority reforms and investments over at least four years. Debt burdens of countries in excess of the 60% threshold will have to be lower by the end of the plan period than at the start while excessive deficits should be reduced at a minimum pace of 0.5% of GDP annually. Some elements of the plan require unanimous member state approval, meaning negotiations could last for months. Germany already expressed concerns about “debt reduction à la carte”.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8878; (P) 0.8903; (R1) 0.8945; More...

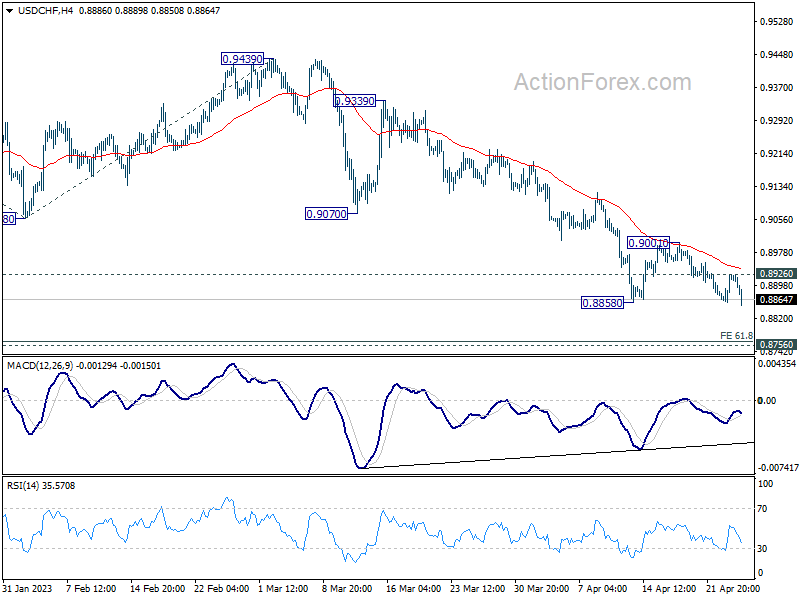

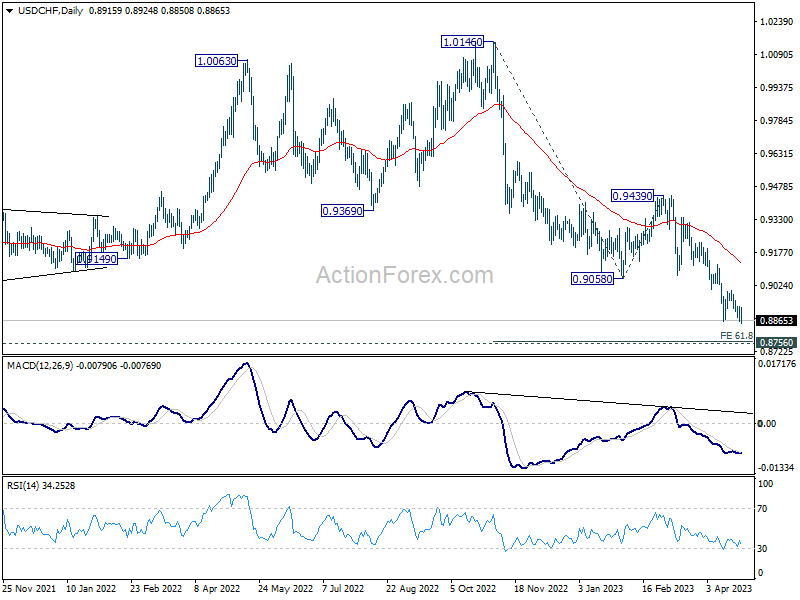

Breach of 0.8858 support indicates resumption of recent down trend in USD/CHF. Intraday bias is back on the downside. Current fall from 1.0146 should target 1.0146 to 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support. Strong support is expected there to bring rebound, at least on first attempt. On the upside, above 0.8926 minor resistance will turn intraday bias neutral first. Further break of 0.9001 should confirm short term bottoming.

In the bigger picture, fall from 1.1046 (2022 high) is in progress for 0.8756 support (2021 low). But overall, this fall is still seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

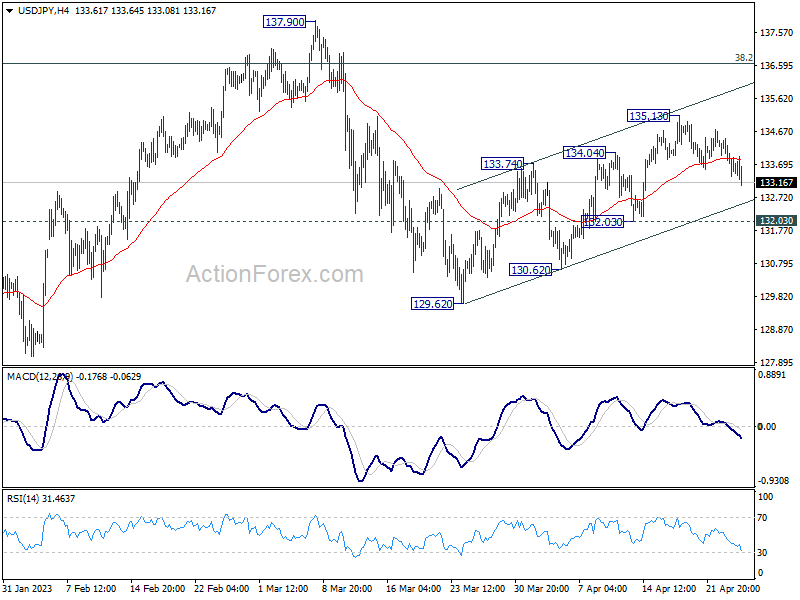

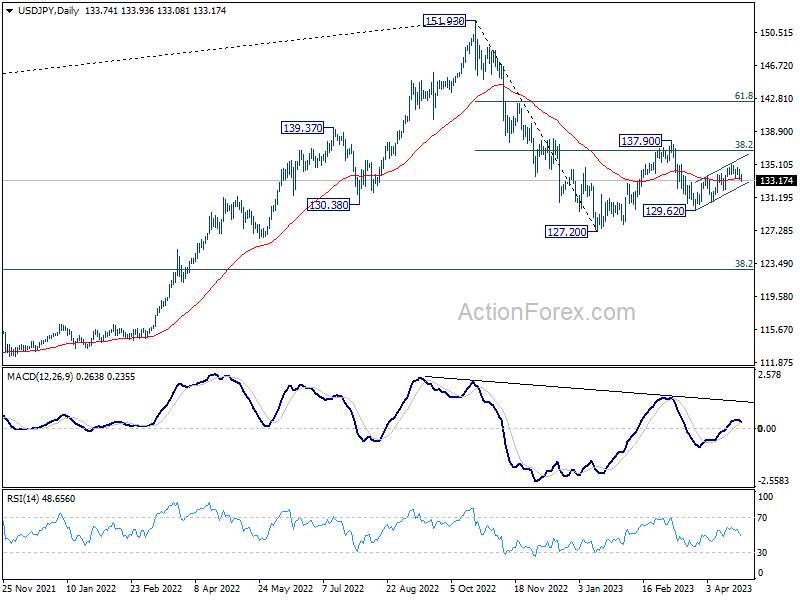

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 133.24; (P) 133.85; (R1) 134.33; More...

USD/JPY's pull back from 135.13 extends lower today, but stays well above 132.03 support. Intraday bias remains neutral first. Further rally is expected as long as 132.03 support holds. On the upside, break of 135.13 will resume the choppy rebound from 129.62 towards 137.90 resistance next. However, break of 132.03 will argue that the rebound has completed already and turn bias back to the downside for 129.62 and below.

In the bigger picture, corrective pattern from 127.20 might be extending. But after all, down trend from 151.93 is expected to resume at a later stage. Break of 127.20 will resume this down trend and target 61.8% projection of 151.93 to 127.20 from 137.90 at 122.61. This will now be the favored case as long as 137.90 resistance holds.

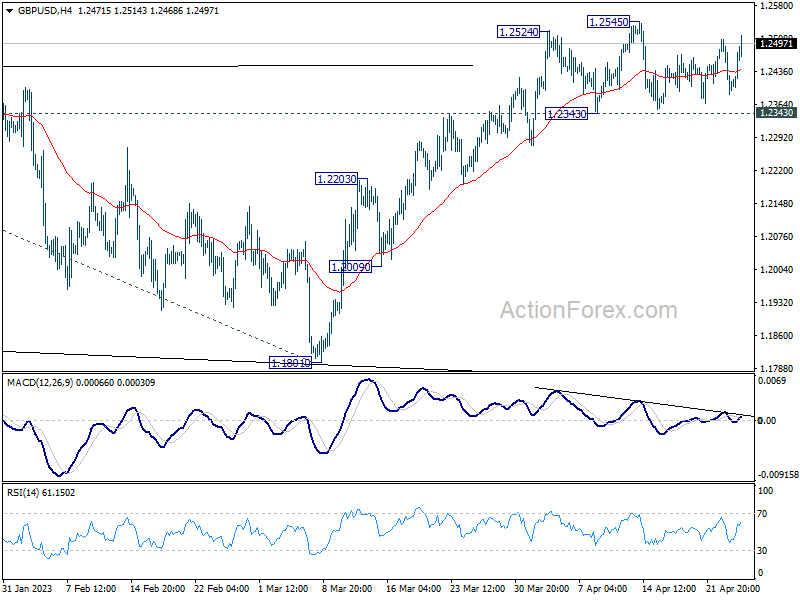

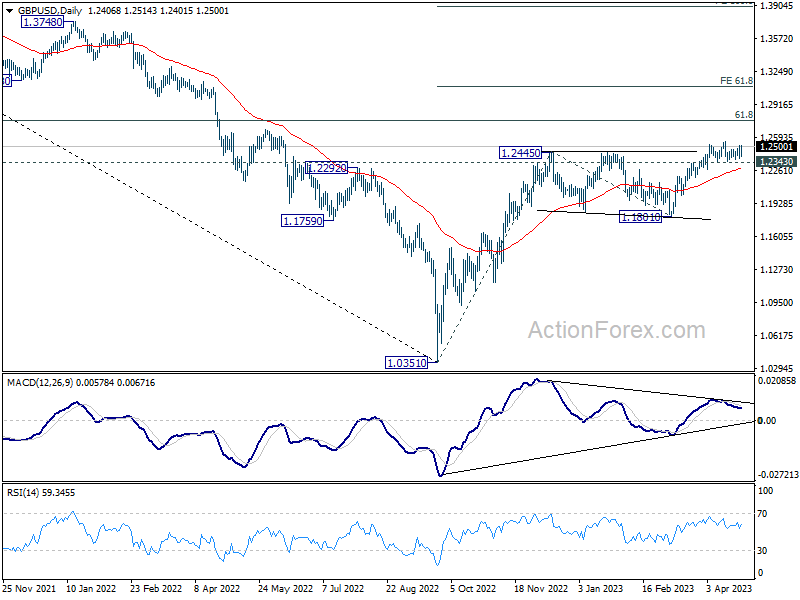

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2362; (P) 1.2435; (R1) 1.2482; More...

While GBP/USD's is still bounded in range below 1.2545 resistance, outlook stays bullish with 1.2343 support intact. On the upside, above 1.2545 will target 1.2759 fibonacci level first. Firm break there will target 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095. However, considering bearish divergence condition in 4H MACD, firm break of 1.2343 will confirm short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, the rise from 1.0351 medium term term bottom (2022 low) is in progress for 61.8% retracement of 1.4248 (2021 high) to 1.0351 at 1.2759. Sustained break there will add to the case of long term bullish trend reversal. Further break of 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095 could prompt upside acceleration to 100% projection at 1.3895. For now, this will remain the favored case as long as 1.1801 support holds, even in case of deep pull back.

Nasdaq (NQ) Buyers Can Appear Soon According to Elliott Wave

Short Term Elliott Wave in Nasdaq (NQ) suggests the Index is cycle from 3.13.2023 low ended in wave ((1)) at 13349.37 as the 1 hour chart below shows. Wave ((ii)) pullback is currently in progress to correct cycle from 3.13.2023 low. Internal subdivision of wave ((ii)) is unfolding as a double three Elliott Wave structure.

Down from wave ((i)), wave a ended at 12953.25 and wave b ended at 13241.75. Wave c lower ended at 12925.50 which completed wave (a) in higher degree. Wave (b) rally ended at 13298.75 with internal subdivision as a zigzag. Up from wave (a), wave a ended at 13255 and dips in wave b ended at 13160.25. Wave c ended at 13297.75 which completed wave (b). Wave (c) lower is in progress as 5 waves. Down from wave (b), wave i ended at 13065 and rally in wave ii ended at 13226.75. Wave iii ended at 12800. Expect wave iv to end soon and Index to turn lower in wave v to complete wave (c) of ((ii)). Potential target for wave (c) of ((ii)) is 100% – 161.8% Fibonacci extension of wave (a) which comes at 12614.1 – 12876.5.

NQ 60 Minute Elliott Wave Chart

Nasdaq Elliott Wave Video

https://www.youtube.com/watch?v=aJVUCAKTqEY

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0936; (P) 1.1002; (R1) 1.1039; More...

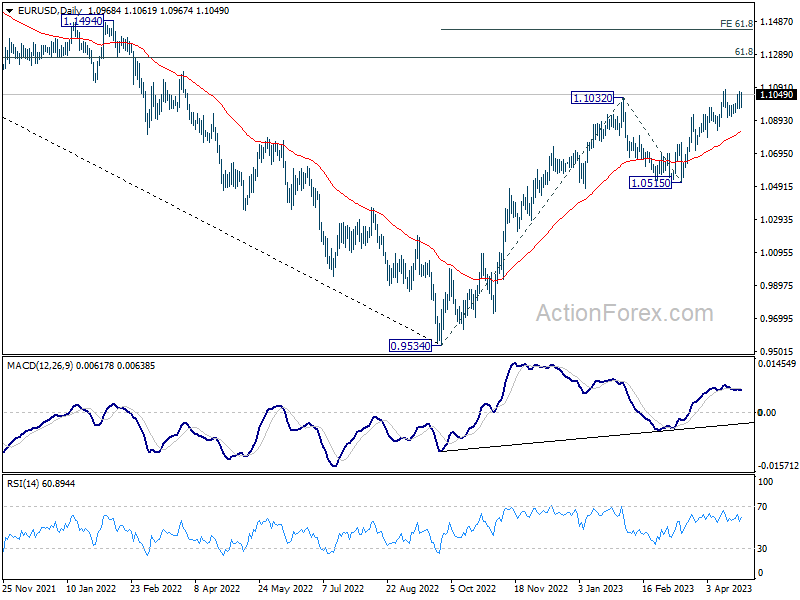

Immediate focus is back on 1.1075 resistance with today's rebound in EUR/USD. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441. Meanwhile, outlook will remain bullish as long as 1.0908 support holds, in case of another retreat.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

Euro Leads European Higher Amid Improving German Consumer Sentiment and US Regional Bank Worries

Euro is leading European majors higher today, with a little boost from improving consumer sentiment in Germany. However, it is likely that the rise is more due to concerns over regional bank woes in the US, which are triggering some risk-off sentiment. Australian Dollar is the worst performer for the day, with selloffs deepening, followed by New Zealand and Canadian Dollars. Meanwhile, Dollar is mixed for now, along with Yen. The relative performance of the US and Japanese currencies will largely depend on whether this week's decline in US treasury yields extends.

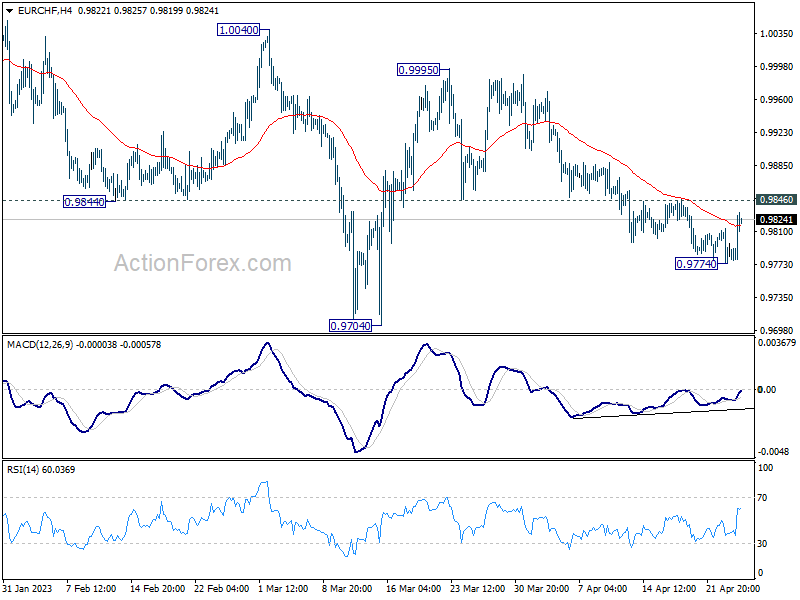

Technically, the main focuses for the US session today will be on 1.1075 resistance in EUR/USD, 0.8858 support in USD/CHF, and to a lesser extent, 1.2545 resistance in GBP/USD. Decisive breaks of these levels will confirm resumption of recent downtrend of Dollar against Europeans. Another focus is the 0.9846 minor resistance in EUR/CHF. A firm break there will confirm short-term bottoming at 0.9774 and bring a stronger rebound. This could help push EUR/USD through the mentioned 1.1075 resistance and possibly prompt upside acceleration above that level.

In Europe, at the time of writing, FTSE is down -0.27%. DAX is down -0.58%. CAC is down -0.95%. Germany 10-year yield is up 0.0022 at 2.387. Earlier in Asia, Nikkei dropped -0.71%. Hong Kong HSI rose 0.71%. China Shanghai SSE dropped -0.02%. Singapore Strait Times dropped -0.08%. Japan 10-year JGB yield dropped -0.0170 to 0.463.

US durable goods orders rose 3.2% mom in Mar, ex-transport orders up 0.3% mom

US durable goods orders rose 3.2% mom to USD 276.4B in March, well above expectation of 0.8% mom. Ex-transport orders rose 0.3% mom to USD 179.0B, above expectation of -0.2% mom. Ex-defense orders rose 3.5% mom to USD 259.3B. Transportation equipment rose 9.1% mom to USD 97.4B.

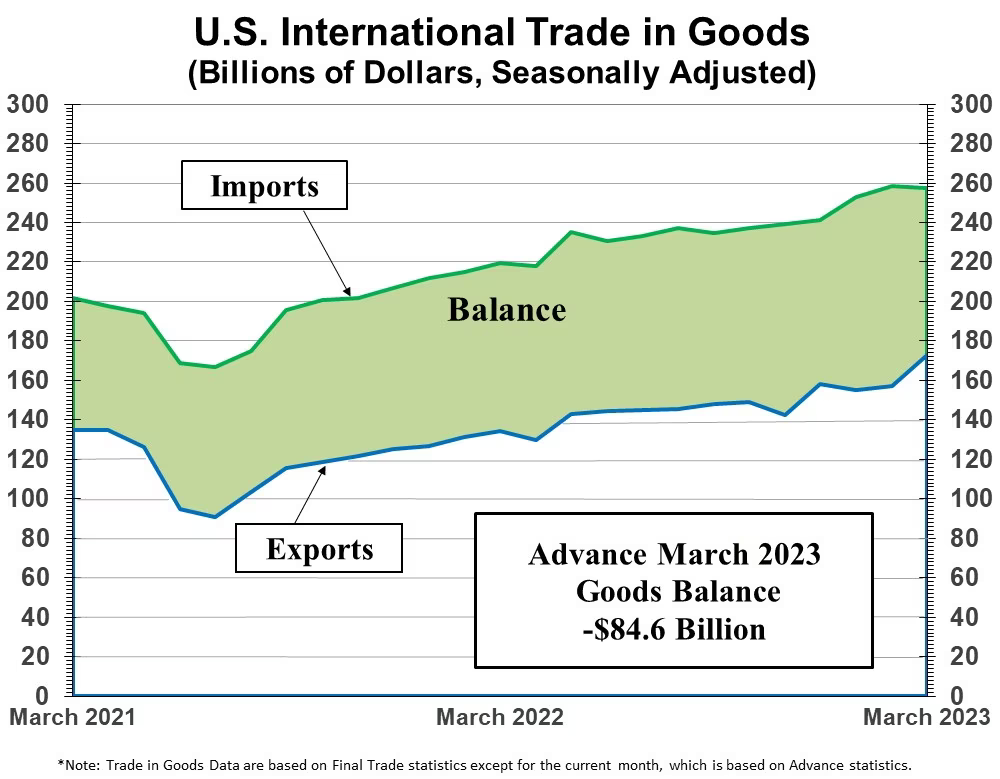

US goods trade deficit narrowed to USD -84.6B in Mar

US goods exports rose USD 4.9B to USD 172.7B in March. Goods imports dropped USD -2.5B to 257.3B. Trade deficit came in at USD -84.6B, smaller than expectation of USD -89.8B.

Wholesale inventories rose 0.1% mom to USD 919.9B. Retail inventories rose 0.7% mom to USD 773.4B.

Germany Gfk consumer sentiment rose to -25.7, improved economic and income expectations

Germany Gfk Consumer Sentiment for May improved from -29.3 to -25.7, above expectation of -27.5. In April, Economic Expectations rose sharply from 3.7 to 14.3. Income Expectations rose from -24.3 to -10.7. Propensity to Buy rose from -17.0 to -13.1.

The seventh increase in a row indicates that consumer sentiment is gathering momentum. "Following a rather small increase in the previous month, consumer sentiment is showing clear signs of an upswing this month," explains Rolf Bürkl, GfK consumer expert.

"However, the value still remains below pre-pandemic levels of around three years ago. On another positive note, income expectations have risen for the seventh time in a row, returning to the level prior to the start of the war in Ukraine for the first time."

Australia CPI down to 7.0% yoy in Q1, 6.3% yoy in Mar

Australia CPI slowed from 7.8% yoy to 7.0% yoy in Q1, slightly above expectation of 6.9% yoy. For the quarter, CPI rose 1.4% qoq, down from prior 1.9% qoq, below expectation of 1.3% qoq. Trimmed mean CPI rose 1.2% qoq, 6.6% yoy while weighted median CPI rose 1.2% qoq, 5.8% yoy.

Michelle Marquardt, ABS head of prices statistics, said "CPI inflation slowed in the March quarter, with the quarterly rise being the lowest since December 2021. While prices continued to rise for most goods and services, many of these increases were smaller than they have been in recent quarters."

Monthly CPI slowed from 6.8% yoy to 6.3% yoy in March, below expectation of 6.5% yoy. Excluding volatile items (Fruit and vegetables and Automotive fuel) CPI, rose from 6.8% yoy to 6.9% yoy.

NZ imports surged 10% yoy, export rose 0.6% yoy in Mar

New Zealand goods exports rose 0.6% yoy or NZD 40m to NZD 6.5B in March. Imports rose 10% yoy or NZD 719m to NZD 7.8B. Monthly trade balance recorded a deficit of NZD -1.3B, larger than expectation of NZD -0.5B.

Australia contributed the most to the growth in monthly exports, with a 30% rise. Goods exports to the US was up 4.1%, EU up 28%, but down -9.6% to Japan and down -5.7% to China.

On the other hand, imports from the US leads the monthly rise, up 39%. Imports from EU and South Korea grew 24% and 20% respectively. On the other hand, imports from China was down -13%, Australia down -4.0%.

BoJ Ueda: Dealing with cost-push inflation is very difficult

In an address to parliament today, BoJ Governor Kazuo Ueda highlighted the difficulties central banks face when dealing with cost-push inflation.

Ueda explained, "In general, dealing with cost-push inflation is very difficult for central banks. On the one hand, you'd like to curb inflation. On the other hand, you don't want to tighten monetary policy knowing that cost-push inflation will cool the economy."

The governor emphasized the importance of striking the right balance, which he said, "depends on economic developments at the time, including where inflation stood at the outset."

Ueda also noted that cost-push inflation in Japan is likely to ease as prices of imported raw materials have probably peaked.

These comments come ahead of BoJ's two-day policy meeting starting on Thursday, during which the central bank is widely anticipated to maintain its ultra-loose monetary policy.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0936; (P) 1.1002; (R1) 1.1039; More...

Immediate focus is back on 1.1075 resistance with today's rebound in EUR/USD. Decisive break there will resume larger up trend from 0.9534 to 1.1273 fibonacci level. Break there will target 61.8% projection of 0.9534 to 1.1032 from 1.0515 at 1.1441. Meanwhile, outlook will remain bullish as long as 1.0908 support holds, in case of another retreat.

In the bigger picture, rise from 0.9534 (2022 low) is in progress for 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidify the case of bullish trend reversal and target 1.2348 resistance next (2021 high). This will now remain the favored case as long as 1.0515 support holds, even in case of deeper pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | -1273M | -500M | -714M | |

| 01:30 | AUD | Monthly CPI Y/Y Mar | 6.30% | 6.50% | 6.80% | |

| 01:30 | AUD | CPI Q/Q Q1 | 1.40% | 1.30% | 1.90% | |

| 01:30 | AUD | CPI Y/Y Q1 | 7.00% | 6.90% | 7.80% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 1.20% | 1.40% | 1.70% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 6.60% | 7.20% | 6.90% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence May | -25.7 | -27.5 | -29.5 | -29.3 |

| 08:00 | CHF | Credit Suisse Economic Expectations Apr | -33.3 | -41.3 | ||

| 12:30 | USD | Goods Trade Balance (USD) Mar P | -84.6B | -89.8B | -91.6B | |

| 12:30 | USD | Wholesale Inventories Mar P | 0.10% | -0.20% | 0.10% | |

| 12:30 | USD | Durable Goods Orders Mar | 3.20% | 0.80% | -1.00% | |

| 12:30 | USD | Durable Goods Orders ex Transport Mar | 0.30% | -0.20% | -0.10% | |

| 14:30 | USD | Crude Oil Inventories | -1.3M | -4.6M |

EUR/USD Rebounds as German Consumer Confidence Improves

- German consumer confidence rises

- EUR/USD pushes above 1.10

EUR/USD is trading at 1.1040, up 0.60% on the day

German consumer confidence brightens

German consumer confidence continued its upswing heading into May. The German GfK consumer sentiment index rose to -25.7, up from -29.3 in April and above the estimate of -27.5 points. Not exactly red-hot numbers, but the upswing has now extended over seven straight months, a clear trend that the German consumer is becoming more optimistic about economic conditions. As well, income expectations rose for a seventh straight time, the highest level since February 2022 and the main driver for the rise in consumer confidence.

German consumers were able to breathe a sigh of relief as the feared energy crunch this past winter never materialized. Energy prices remained relatively moderate and the government pitched in with subsidies that lowered energy bills for households. Still, consumer demand has been weak, dampened by the double-barreled jab of high inflation and rising interest rates. The German economy is not in great shape, with GDP expected to stagnate in 2023, and as the largest economy in the eurozone that certainly does not bode well for the rest of the bloc.

In the US, it’s the opposite story, as consumer confidence slowed to a nine-month low in April. The Conference Board consumer confidence index slipped to 101.3, down from the March reading of 104.0, which was also the estimate. The survey found that the level of consumers planning to buy major household appliances in the next since months fell to a 13-year low, and that could spell big trouble for the economy, as consumer spending is a key driver of growth. Consumers have been resilient in the face of high inflation and rising rates, but that could be changing as the Fed’s aggressive tightening percolates through the economy.

EUR/USD Technical

- EUR/USD is testing resistance at 1.1023. Above, there is resistance at 1.1056

- There is support at 1.0966, followed closely by at 1.0933

US goods trade deficit narrowed to USD -84.6B in Mar

US goods exports rose USD 4.9B to USD 172.7B in March. Goods imports dropped USD -2.5B to 257.3B. Trade deficit came in at USD -84.6B, smaller than expectation of USD -89.8B.

Wholesale inventories rose 0.1% mom to USD 919.9B. Retail inventories rose 0.7% mom to USD 773.4B.