Sample Category Title

Australia March CPI – Goods Deflation Greater than Anticipated

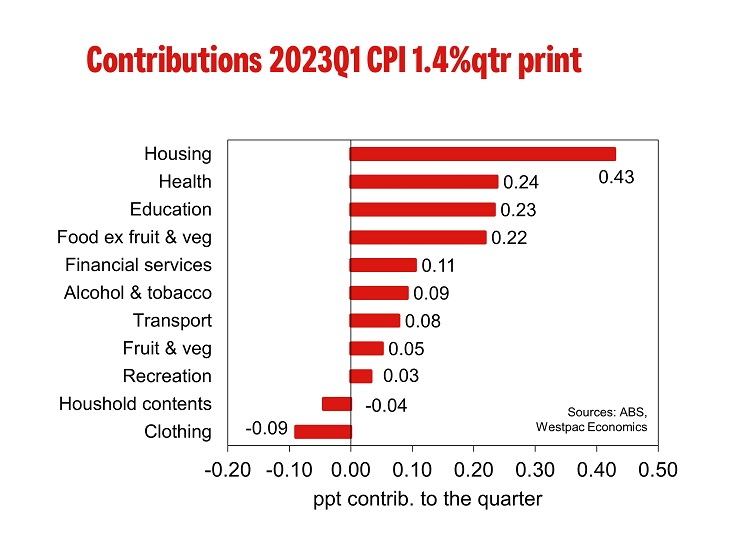

Headline CPI 1.4%qtr/7.0%yr; Trimmed Mean 1.2%qtr/6.6%yr; Weighted Median 1.2%qtr/5.8%yr. The more modest rise in the Trimmed Mean is highlighting that the current disinflationary force, particularly for goods, appears to be greater than we thought.

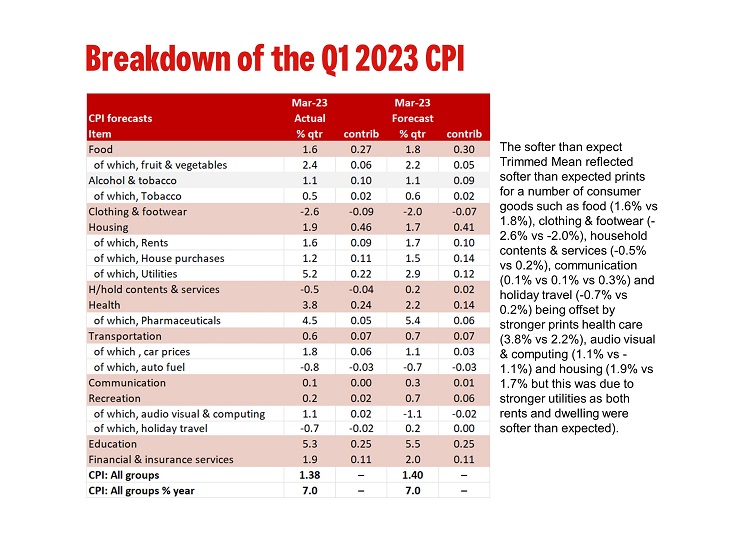

The March quarter CPI came in as broadly as expected rising 1.4%qtr (true it was above market expectation of 1.3% but it was on Westpac’s 1.4%) taking the annual pace down to 7.0%. The Trimmed Mean surprised coming in softer than expected rising just 1.2%qtr for an annual pace of 6.6%. Our end 2023 target for the Trimmed Mean is 3.7%yr. The ABS noted that while prices continued to rise for most goods and services, many of these increases were smaller than they have been in recent quarters.

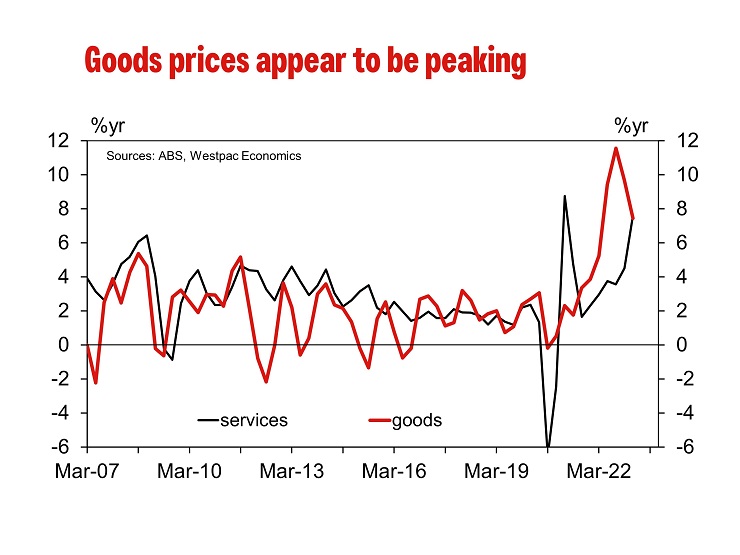

The more modest rise in the Trimmed Mean is highlighting that the current disinflationary force, particularly for goods, appears to be greater than we thought. For while services inflation is holding up, and is likely to prevent inflation falling back within the band in 2023 (and even in 2024 as per our current forecasts) it is not enough to prevent goods disinflation taking the annual pace of inflation back to close to the band by the first half of 2024.

The most significant contributors to the March quarter rise were medical & hospital services (+4.2%), tertiary education (+9.7%), gas & other household fuels (+14.3%) and domestic holiday travel & accommodation (+4.7%). Partially offsetting the rise was international holiday travel & accommodation (-8.2%), as some destinations entered their off-peak seasons following significant rises in recent quarters. Also discounting by retailers resulted in falls across furniture (-4.6%), major & small appliances (-3.8%) and clothing (-3.2%).

We have included a table comparing our forecasts to the actual print. While the headline print came in as we expected the softer than expect Trimmed Mean reflected softer than expected prints for a number of consumer goods such as food (1.6% vs 1.8%), clothing & footwear (-2.6% vs -2.0%), household contents & services (-0.5% vs 0.2%), communication (0.1% vs 0.1% vs 0.3%) and holiday travel (-0.7% vs 0.2%) being offset by stronger prints health care (3.8% vs 2.2%), audio visual & computing (1.1% vs -1.1%) and housing (1.9% vs 1.7% but this was due to stronger utilities as both rents and dwelling were softer than expected).

Annual goods inflation eased after two years of steady increases, from 9.5%yr to 7.6%yr, due to discounting on furniture, appliances and clothes and lower automotive fuel. Annual services inflation recorded its largest annual rise since 2001, driven by higher prices for holiday travel, medical services, rents and restaurant meals. Core market services excluding volatile items gain 0.9% in the quarter, a step down from the 2.7%qtr increase in December but historically March is a soft quarter. This is why the annual pace lifted to 6.8%yr from 6.4%yr (and compared to 2.5%yr in March 2022) with the six-month annualised pace lifting to 9.3%yr from 6.1%yr.

As noted earlier the pace of new dwellings inflation continues to ease following a record annual pace the September quarter. Lifting 1.2% this was softer than our forecast of 1.5% and well down on the 3.7% increase in December, 5.6% in September and 5.75 increase in March. The recent moderation in prices reflects improvements in the supply of construction materials, a softening in demand and the unwinding of various government construction grants.

There was no surprise in rents recording their fastest annual pace since 2010, reflecting strong demand amid low vacancy rates across the country; Sydney and Melbourne both recorded their strongest annual pace since 2012. In the quarter, the 1.6% gain was a gain from the 1.2% increase in December and the strongest increase since March 2009.

For gas & other fuels price reviews reflecting higher wholesale gas prices led to rises across all capital cities. In the quarter gas & other fuels lifted 14.3%, the strongest since September 2012 (14.2%) taking the annual pace to 26.2%yr, the strongest on record.

Electricity prices reviews hit the CPI in the September quarter. However, the respect price rises were partially offset by the introduction of electricity rebates in WA, QLD and the ACT. The unwinding of these rebates has seen the full effects of higher electricity prices reflected in the March quarter (3.0%qtr/15.5%yr).

Auto fuel fell 0.8%qtr with unleaded fuel unchanged and diesel prices –10.3%qtr. While fuel prices remain high it has been a year since Russia invaded Ukraine which saw prices jump 11.0% in the quarter so prices are up just 1.1% in the year to March 2023; it was 13.2%yr in December.

Non-discretionary inflation includes goods & services that households are less likely to reduce their consumption of, such as food, automotive fuel, housing and health costs. Non-discretionary goods & services rose 1.9%qtr/7.2%yr due to medical 7 hospital services (+4.2%), gas & other household fuels (+14.3%) and new dwellings (+1.2%). Discretionary goods & services lifted 0.6%qtr/6.8%yr driven by tertiary education (+9.7%), domestic holiday travel (+4.7%) and motor vehicles (+1.8%).

JPY Carry trade: Downside Pressure Mounts as Global Demand Faces Headwinds

- Commodities and growth proxies JPY crosses are leading the decline in G10 JPY carry trade basket.

- A widening of the US high-yield corporate bonds credit spread may spark a higher volatile movement in the JPY crosses.

- Key US earnings releases from Visa, Microsoft, and Alphabet are indicating slower global demand spending despite expectations beat.

FX volatility may start to increase as G10 JPY crosses have shaped significant reversal movements

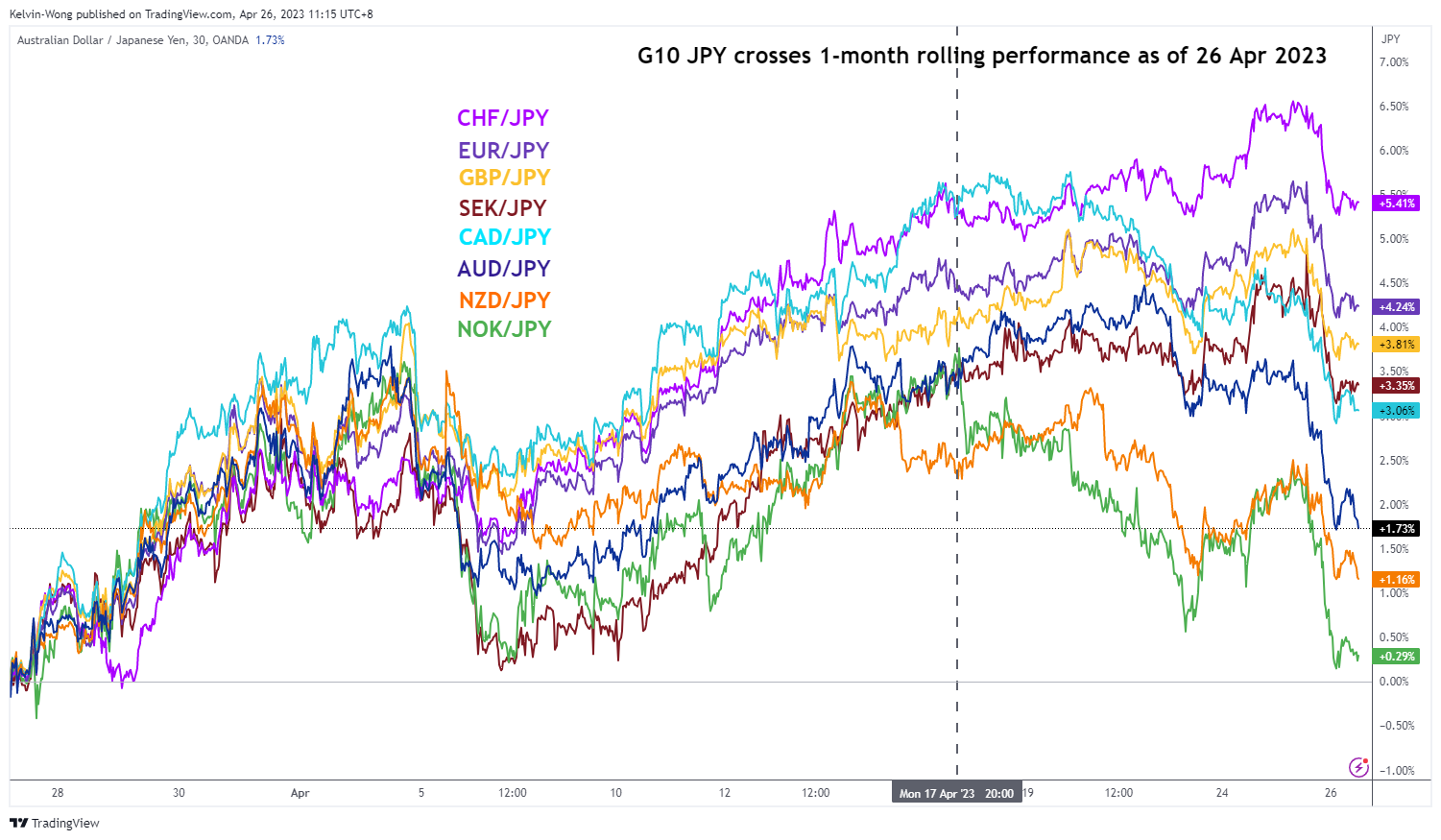

Fig 1: G10 JPY crosses 1-month rolling performances as of 26 Apr 2023 (Source: TradingView, click to enlarge chart)

The G10 JPY crosses have started to exhibit a risk-off liked behaviour due to concerns about global growth expansion.

As for the concerns about global growth, the focus is on the will of China policymakers to implement further liquidity measures to boost domestic economic growth which in turn drives up Chinese consumers and corporate’s spending and investment in international goods and services. That’s a very much needed “support” for the global economy given that the rest of the developed nations’ central banks are still in a tightening mode on their respective monetary policies (except Japan for now, at least in the near term).

The latest guidance from China’s central bank PBoC has indicated that it prefers a “wait and see” approach before implementing any further accommodative measures as recent key economic data such as housing, consumer spending, and industrial production are now in recovery mode.

Therefore, it is interesting to note that the commodities-related JPY crosses (proxies of global growth); NOK/JPY, NZD/JPY, and AUD/JPY have led the recent downside reversal since 17 April 2023 as illustrated on the above chart.

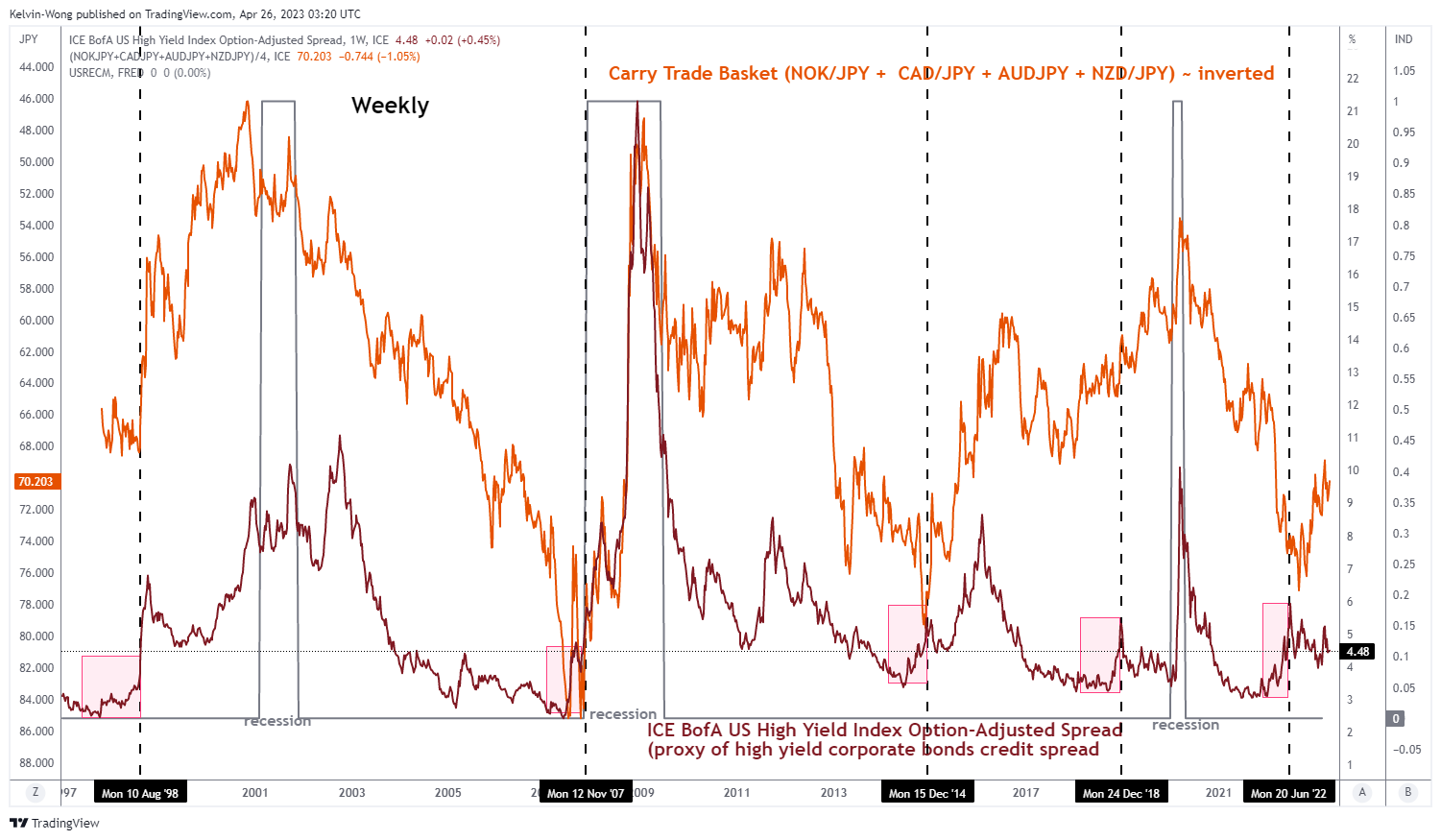

Widening of US high-yield corporate bonds credit spread precedes significant movements on a JPY carry trade basket

Fig 2: ICE BofA US high yield index option-adjusted spread & JPY carry trade basket as of 24 Apr & 26 Apr 2023

(Source: TradingView, click to enlarge chart)

We have highlighted earlier in a previous article the elements that may trigger an imminent widening of the US high-yield corporate bonds credit spread.

Right now, the focus is on inter-market analysis; the pink-coloured shaded boxes in the above chart highlighted previous episodes in the significant widening of the credit spread in the weekly periods of 10 August 1998, 12 November 2007, 15 December 2014, 24 December 2018, and 20 June 2022 have led to a similar movement of the inverted commodities and growth proxies related JPY carry trade basket (equal weightage of NOK/JPY, CAD/JPY, AUD/JPY & NZD/JPY).

The above-mentioned correlation also has logical economic reasoning as a widening of high-yield corporate bonds credit spread indicates a rising default risk. For such a scenario to take shape, we need to have a credit crunch that led to a slowdown in global growth, which eventually tends to have a negative feedback loop into the JPY crosses due to JPY being a “traditional safe haven and funding currency” of choice by market participants.

Key US earnings releases point to global growth deceleration despite expectations beat by Microsoft, Alphabet & Visa

Visa Inc is a market leader in the online payment business space where its financial data can be used as a proxy to gauge global consumer spending. Its overall net revenue growth for fiscal Q2 2023 slowed to 11% year-on-year from 12% in fiscal Q1 2023, its slowest revenue growth since fiscal Q3 2021.

Microsoft’s crown jewel cloud services business segment; Azure recorded a slower growth for fiscal Q3 2023 at 27% year-on-year from 31% in fiscal Q2 2023, its cloud business revenue growth has recorded four consecutive quarters of slowdown.

Alphabet, the parent company of Google has reported a second consecutive quarter of slowdown in Google advertising revenue that decrease by less than 1% year-on-year in Q1 2023 from a decline of close to 4% posted in Q4 2022.

CAD/JPY Technical Analysis – short-term downside momentum intact below 99.00 key resistance

Fig 3: CAD/JPY trend as of 26 Apr 2023 (Source: TradingView, click to enlarge chart)

The minor uptrend phase of the CAD/JPY cross pair from its 24 March 2023 low of 94.07 to its recent 18 April 2023 high has been damaged and the current observations seen on the 4-hour MACD indicator have indicated a revival of short-term downside momentum.

A break below the intermediate support of 97.10 exposes the next supports at 95.70 and 94.65 (the lower limit of the medium-term sideways range configuration in place since the 19 January 2023 low).

On the other hand, a clearance with a 4-hour close above 99.00 key medium-term pivotal resistance negates the bearish tone to see the next resistance coming in at 100.65 (the upper limit of the sideways range configuration).

Nasdaq (NQ) Buyers Can Appear Soon According to Elliott Wave

Short Term Elliott Wave in Nasdaq (NQ) suggests the Index is cycle from 3.13.2023 low ended in wave ((1)) at 13349.37 as the 1 hour chart below shows. Wave ((ii)) pullback is currently in progress to correct cycle from 3.13.2023 low. Internal subdivision of wave ((ii)) is unfolding as a double three Elliott Wave structure.

Down from wave ((i)), wave a ended at 12953.25 and wave b ended at 13241.75. Wave c lower ended at 12925.50 which completed wave (a) in higher degree. Wave (b) rally ended at 13298.75 with internal subdivision as a zigzag. Up from wave (a), wave a ended at 13255 and dips in wave b ended at 13160.25. Wave c ended at 13297.75 which completed wave (b). Wave (c) lower is in progress as 5 waves. Down from wave (b), wave i ended at 13065 and rally in wave ii ended at 13226.75. Wave iii ended at 12800. Expect wave iv to end soon and Index to turn lower in wave v to complete wave (c) of ((ii)). Potential target for wave (c) of ((ii)) is 100% – 161.8% Fibonacci extension of wave (a) which comes at 12614.1 – 12876.5.

NQ 60 Minute Elliott Wave Chart

Nasdaq Elliott Wave Video

https://www.youtube.com/watch?v=aJVUCAKTqEY

Greenback Tried to Bank on Safe Haven Status, But Didn’t Really Shine

Markets

Q1 First Republic earnings sent the regional lender’s stock price in a tail spin. Huge deposit outflows (>$100bn) and a refusal to take analyst questions or provide guidance for the remainder of the year confirm that the company is on death row “exploring strategic options” in the end game. First Republic is the exception to the rule for now, with other regional lenders managing to restore confidence after the mid-March panic. PacWest was the latest example, reporting a small deposit increase yesterday and propelling its share price. The First Republic earnings nevertheless put a bad taste in investors’ mouth. Especially in combination with some disappointing US eco data. US consumer confidence reached its lowest level since July last year in April (101.3 from 104 vs 104 expected). The decline was solely due to a more pessimistic outlook as the fallout from the mid-March regional banking crisis took its toll (expectations down to 68.1 from 74) while the present situation index, focusing on current labour market etc., rose from 148.9 to 151.1. The April Richmond Fed manufacturing index fell from -5 to -10 (vs -8 expected). The combination of both created a risk-off market environment especially from the start of US dealings. US yields lost 5.3 bps (30-yr) to 13.5 bps (2-yr) in a daily perspective. Changes on the German curve varied between 10.7 bps (30-yr) and 13.5 bps (2-yr). Part of the European moves were catching-up with US action on Monday evening (publication Q1 First Republic results around US close). Main European equity indices lost 0.5% or more with key US gauges tumbling 1% (Dow) to 2% (Nasdaq). The greenback tried to bank on its safe haven status, but didn’t really shine. The US nature of yesterday’s market stress serves as strong counterweight. EUR/USD closed at 1.0973 after testing the YTD highs around 1.1070 early on. The tradeweighted dollar rebounded from 101.26 to 101.95. Technical USD pictures didn’t improve. Today’s eco calendar is less enticing with only march US durable goods orders. The US Treasury continues its end-of-month refinancing operation with a $43bn 5-yr Note auction. Yesterday’s $42bn 2-yr sale tailed slightly with the 2.68 bid cover in line with the recent average (2.66). Overall market sentiment will be the key driver ahead of European and US GDP and inflation numbers tomorrow and on Friday. For the moment, we don’t read too much into yesterday’s risk scare.

News and views

Australian Q1 headline inflation slowed slightly less than expected to 1.4% Q/Q and 7% Y/Y, down from 1.9% Y/Y and 7.8% in Q4 2022. Measures of core inflation printed below consensus though (trimmed mean 1.2% Q/Q and 6.6% Y/Y from 6.9% in Q4). The Australian Bureau of Statistics said that most significant price rises (quarterly) were recorded in medical and hospital services (+4.2%), tertiary education (+9.7%), gas and other household fuels (+14.3%), and domestic holiday travel and accommodation (+4.7%). Goods annual inflation eased after two years of steady increases, from 9.5% to 7.6%. However, services annual inflation recorded its largest rise since 2001 (6.1% Y/Y). The market currently expects the RBA to keep its policy rate unchanged at 3.6% next week, but persistently high services inflation might be a source of debate. The 2-y Australian government bond yield this morning dropped 19 bps, but part of this move already occurred before the CPI release. AUD/USD dropped to the 0.661 area.

The Hungarian Central Bank (MNB) yesterday took a first step in winding down emergency measures put in place in October last year. The significant improvement of the risk environment, including Hungary’s risk perception, triggered the decision to narrow the interest rate corridor by reducing the overnight collateralized borrowing rate to 20.5% from 25.%. The MPC still deems it necessary to maintain the current level of the base rate (13%) over a prolonged period to ensure that inflation expectations are anchored and the inflation target is achieved in a sustainable manner. The MNB also closely monitors the effects of international financial market developments. The central bank will take into account the persistence of improvements in risk perception at the following policy meetings before making a decision to setting the interest rate conditions of overnight instruments. So, the O/N deposit rate for now is kept unchanged at 18%. Vice governor Virage indicated that the MNB will be cautious when assessing changes at upcoming meetings. The forint weakened from an intraday top of EUR/HUF 374.5 to close near EUR/HUF 377.75. However, given the global risk-off the loss was reasonable.

Riksbank to Deliver 50bp Rate Hike Today

Market movers today

The main event today will be the Riksbank Policy Rate decision at 9.30 CET, where we expect a 50bp hike in line with the market pricing. We also expect Riksbank to signal an additional hike in June, see more in the Nordic section below.

On the data front, Swedish and Norwegian March unemployment rates will be released this morning alongside German consumer confidence. This afternoon, US durable goods orders are due for release.

Markets pay close attention to any final ECB comments ahead of the silent period starting tomorrow; de Guindos is scheduled to be on the wires today.

The 60 second overview

Macro: Risk-off dominated global markets with equities lower across the board and core yields lower amid intra-euro area spreads widening. Mixed corporate earnings and concerns over First Republic Bank were the main sources of the risk-off. The sour risk sentiment continued overnight in the Asian session.

Banking turmoil: The earnings report from First Republic Bank showed a deposit outflow of 41% to just above USD 100bn in Q1 and also looks into divest part of its business, which reminded markets of the significant banking turmoil in March.

US Politics: Incumbent President Biden formally announced his campaign to be democratic nominee in the 2024 presidential election.

EU debt: in an FT op-ed yesterday, German Finance Minister Lindner repeated his case that sound public finances need clear fiscal rules. He is opposed to the Commission proposal of country-specific debt plans and instead calls for common fiscal rules that include numerical debt reduction targets, as well as additional measures that ensure compliance and better enforcement. Overall, clearly hawkish overtones from Germany, that makes EU fiscal rules reform seem increasingly like an uphill struggle, as we also discussed in Euro macro notes - Germany is falling back into old habits, 14 April.

Equities pulled back on Tuesday with losses accelerating into the US session. S&P500 closed down -1.8% and Russell 2000 as much as -2.5%. The latter was dragged down by First Republic Bank that plunged 40% after showing a -35% contraction in deposits. Markets shifted to recession fear mode with all sectors lower and a classic defensives-over-cyclicals preference. Let's call it risk off, with VIX rising all the way up to 19, yields falling in tandem with equities (the good old correlation) and industrial metals and oil down 2-3%. Solid tech earnings have bid up the Nasdaq futures this morning, so a shift in sentiment is in the cards.

FI: The sour risk sentiment sent 10y German yields 10bp lower despite the significant supply to markets yesterday from EU and Germany as well as hawkish commentary from Schnabel, who clearly favours a 50bp rate hike next week in our reading. Uncertainty is high for the upcoming ECB meeting whether ECB will deliver a 25bp or 50bp rate hike. Markets price 3.82%, which is 6bp less than on Monday.

FX: USD rebounded yesterday and notably EUR/USD was on a roller-coaster ride. First rising above 1.1060 before falling to around 1.0970 and despite a narrowing of the spread between short-term USD and EUR interest rates. Sour risk sentiment, i.e. a drop in US equities and oil price, looked to be the main culprit.

Credit: Overall the secondary credit markets remained calm while primary markets remained active. The iTraxx Main was unchanged while the iTraxx Xover widened 6bp from yesterday.

Nordic macro

We expect the Riksbank to deliver a rate hike of 50bp bringing the policy rate to 3.50% and to signal an additional rate hike in June, somewhere between 25bp and 50bp. This view is well aligned with current market pricing, which indicates 50+30+15bp=95bp for three upcoming meetings. We still expect a final 50bp in June and a peak rate at 4.0%. After near-term hikes, the Riksbank's rate path projections from the last two meetings have shown a completely flat profile until the end of the forecast period (which will now include Q2 26). If the Riksbank opts to do this again we would find it natural for the market to continue to ignore it. Notably, the market is pricing in the first full 25bp cut by Q1 2024 and close to another 25bp cut in Q2 2024. A signal of eventual rate cuts towards the end of the rate path would make more sense in our view, as the policy rate otherwise would be too restrictive for too long. While March inflation was lower than expectations, the gap to the Riksbank's forecast remains too wide (1.4pp for core). In addition, macro developments have also been stronger than expected at the start of the year. Even the housing market is showing resilience, although we deem this to be temporary. With regards to the active QT, it is still early days so we would not expect any changes at this point. As for the SEK, there is little room for the Riksbank to underwhelm market expectations. The KIX-weighted SEK is back close to February levels, which then prompted the U-turn with regard to krona communication. Board members have then made it clear that their increased focus on the SEK should not be interpreted as them having an exchange rate target. That said, too much FX complacency runs the risk of spurring further SEK weakness. Given current market pricing a 50bp hike should be SEK neutral. Forward guidance and overall communication will be more important.

USD Makes Comeback

EUR/USD hits resistance

The US dollar clawed back losses with robust new home sales in March. The price is still trying to hold on to recent gains after rallying above this year’s high of 1.1000. A drop below the closest support at 1.0970 has broken the latest momentum and may push short-term buyers to the sidelines. With the RSI showing an oversold condition, 1.0910 at the base of a previous bullish breakout and over the 20-day SMA is likely to be tested. The recent high of 1.1075 is the key hurdle to lift before the bulls could regain control.

AUD/USD breaks lower

The Australian dollar slipped over a slowdown in Q1 inflation. The pair continues to struggle to stand its ground against growing selling interest despite an upward consolidation for a month and half. The bulls will need to clear 0.6770 before a meaningful recovery could take shape. Instead, a drop below 0.6620 showed little commitment from the buy side, and could potentially lead to a broader liquidation below the March lows of 0.6590. 0.6680 is a fresh resistance as the RSI attempts to recover into the neutral zone.

UK 100 drifts lower

The FTSE 100 softened as tumbling deposits at First Republic Bank renewed fears about the banking sector. The V-shaped rally has put the index back right under this year’s high with the supply zone 7930-7970 being the bears’ last stronghold. A bullish breakout would signal a continuation to a new all-time high above 8040. However, the bulls would need to catch their breath and consolidate their gains. 7850 is first to assess follow-up interest as the price goes horizontal. A deeper correction would test 7775 on the 20-day SMA.

Technical Outlook and Review

DXY:

The US Dollar Index (DXY) is currently showing bullish momentum, as it could potentially continue to move towards its first resistance level.

At the moment, the first support level for DXY is at 101.52, which is an overlap support. If the price drops further, it could potentially find support at 100.86, which is another overlap support.

However, the overall momentum of the chart remains bullish, so it’s more likely that the price will continue to rise towards the first resistance level of 102.25, which is also an overlap resistance. If it manages to break through this level, it could reach the second resistance level of 102.74, which is an overlap resistance and also coincides with the 38.20% Fibonacci retracement level.

EUR/USD:

The EUR/USD chart shows weak momentum with a bearish bias. Prices could potentially make a bearish continuation towards the first support level. On the upside, prices could face resistance near the swing high resistance level.

Looking at the support and resistance levels, we can see that the first support level is at 1.0949. This level is an overlap support, indicating that it has been an important price level in the past. The second support level is at 1.0908, which is also an overlap support level, and it coincides with the 50% Fibonacci retracement level.

On the other hand, the first resistance level is at 1.1070, which is a multi-swing high resistance level.

GBP/USD:

The GBP/USD pair has been showing weak momentum with low confidence overall. However, there is a possibility for a bullish bounce off the first support level and head towards the first resistance level.

The first support level is at 1.2403, which is an overlap support level. If the price reaches this level, there is a chance that it could bounce off this level and head towards the first resistance level.

The second support level is at 1.2343, which is also an overlap support level. This level may act as a stronger support level if the price falls further.

On the upside, the first resistance level is at 1.2547, which is a swing high resistance level. If the price manages to break above this level, it could potentially continue to rise.

The second resistance level is at 1.2599, which is an overlap resistance level. This level may act as a stronger resistance level if the price manages to break above the first resistance level.

USD/CHF:

The USD/CHF currency pair is currently showing neutral momentum on the charts, with the potential to fluctuate between the 1st resistance and 1st support levels.

The 1st support level is at 0.8860 and is considered a multi-swing low support, while the 2nd support level is at 0.8764 and is an overlap support.

On the other hand, the 1st resistance level is at 0.9006 and is an overlap resistance, with the 50% Fibonacci retracement adding to its significance.

The 2nd resistance level is at 0.9070 and is an overlap resistance, with the 78.60% Fibonacci retracement providing additional support.

USD/JPY:

After breaking out of the rising trendline and prior 1st support of 133.73, USD/JPY could continue its bearish momentum towards the new 1st support level at 132.22. The level is considered a strong support as it has been tested multiple times in the past.

If the price breaks below this level, the next potential support could be at 130.55, which is a key support level based on the 61.80% Fibonacci retracement.

On the upside, the first resistance is at 133.73, which is an overlap resistance level. If the price manages to break above this level, it could potentially head towards the next resistance at 135.11, which is also an overlap resistance level.

AUD/USD:

The AUD/USD pair is currently showing strong bearish momentum as it broke through the prior first support of 0.6623. It could reach the new first support level at 0.6568, which is another multi-swing low support level.

If the price bounces from this new support level, it could head towards the first resistance level at 0.6623. The previous first support level at 0.6623 now acts as the new first resistance, which is an overlap resistance. This second resistance level is an overlap resistance and also corresponds to the 78.60% Fibonacci projection.

NZD/USD:

The NZD/USD chart is currently exhibiting an overall bearish momentum, indicating that the price may potentially break through the first support levels. The first support level is at 0.6132 and may provide potential support.

The next potential support level is at 0.6093, which is a multi-swing low support and may provide additional support for the price if it were to drop further.

On the other hand, if the price were to rise, the 1st resistance level is at 0.6175. This level is a multi-swing high resistance, making it a strong level for potential resistance.

If the price were to break above the 1st resistance level, the next potential resistance level is at 0.6222. This level is also an overlap resistance and coincides with the 50.0% Fibonacci retracement, making it a strong level for potential resistance.

USD/CAD:

The USD/CAD currency pair has been showing bullish momentum recently, with the potential for continued upside movement towards the first resistance level.

The first support level at 1.3555 is a good level to watch, as it represents an overlap support and also coincides with the 23.60% Fibonacci retracement level. A bounce off this level could signal a continuation of the recent bullish trend.

The second support level at 1.3424 is also an overlap support and may provide additional buying opportunities in case of a deeper retracement.

On the upside, the first resistance level at 1.3650 is an overlap resistance and coincides with the 61.80% Fibonacci retracement level, making it a strong area of resistance. If price breaks above this level, it could indicate a sustained bullish trend.

The second resistance level at 1.3753 is also an overlap resistance and coincides with the 78.60% Fibonacci retracement level, adding further strength to this resistance level.

DJ30:

The DJ30 has been showing a weak overall momentum with low confidence. However, the price could potentially make a bullish bounce off the first support level and head towards the first resistance level.

The first support level is at 33,587.40 and it is considered a good support level due to its overlap support and its 23.60% Fibonacci retracement. The second support level is at 33,297.78, and it is also an overlap support, and its 38.20% Fibonacci retracement makes it a good level of support.

The first resistance level is at 34,150.59 and it is considered a good level of resistance due to its multi-swing high resistance. The second resistance level is at 34,370.08, and it is an overlap resistance that provides another potential level of resistance.

GER30:

The GER30 index has been trading in a neutral momentum. The price could potentially fluctuate between the 1st support and 1st resistance level.

The 1st support level is at 15655.92, which is an overlap support and also coincides with the 23.60% Fibonacci retracement level. The 2nd support level is at 15483.15, which is an overlap support.

On the upside, the 1st resistance level is at 15936.79, which is a multi-swing high resistance level. The 2nd resistance level is at 16049.50, which is an overlap resistance level and also coincides with the 127.20% Fibonacci extension level.

BTC/USD:

The current overall momentum of the chart for BTC/USD is showing strong bullishness with high confidence. Based on the current price action, Bitcoin has the potential to continue its bullish trend towards the first resistance level.

The first support level for BTC/USD is located at 27205.00, which is an overlap support level. This support level is expected to hold if the bullish trend continues. However, if the price drops below this level, the next support level is located at 26508.00, which is also an overlap support level and a 38.20% Fibonacci retracement level.

On the upside, the first resistance level is located at 28819.00, which is an overlap resistance level and a 50% Fibonacci retracement level. This level has the potential to attract sellers and push the price lower. However, if the price breaks above this level, the next resistance level is located at 30594.00, which is another overlap resistance level.

US500

The US500 is currently exhibiting neutral momentum. Based on the chart, price could potentially fluctuate between the 1st resistance and 1st support level.

The 1st support level is at 4059.58 and is considered good because it is an overlap support. The 2nd support level is at 4029.41 and is also a good support level because it coincides with the 38.20% Fibonacci retracement.

On the other hand, the 1st resistance level is at 4116.22, which is an overlap resistance. The 2nd resistance level is at 4173.65, which is also an overlap resistance.

ETH/USD:

The chart of ETH/USD is currently showing signs of weakness with low confidence. The price could potentially continue its bearish move towards the first support level, which is located at 1844.24. This level is significant as it has acted as an overlap support in the past, which makes it more likely that it will provide a bounce for the price.

In case the price breaks below the first support level, it may continue to decline towards the second support level at 1784.57. This level is also significant as it represents the 78.60% Fibonacci retracement level of the recent bullish move, adding to its significance.

On the upside, the first resistance level at 1934.69 is significant as it has acted as an overlap resistance in the past. If the price manages to break above this level, it may head towards the second resistance level at 2060.29, which is also an overlap resistance and coincides with the 78.60% Fibonacci retracement level.

WTI/USD:

The overall momentum of WTI chart is currently bullish. The recent dip in price has provided a buying opportunity for traders as the price could potentially make a bullish bounce off the 1st support level and head towards the 1st resistance level.

The 1st support level is at 77.02 and it is a good support level as it is an overlap support level and also a 38.20% Fibonacci Retracement level. A bounce from this level could lead to a bullish momentum in price.

If the price fails to bounce off the 1st support level, it could potentially drop further to the 2nd support level at 73.25. This is also a good support level as it is an overlap support level.

On the other hand, the 1st resistance level is at 79.01 and it is a good resistance level as it is an overlap resistance level. If the price manages to break through this resistance level, it could potentially head towards the 2nd resistance level at 81.47.

XAU/USD (GOLD):

The XAU/USD price has a weak bearish momentum with low confidence, and it could potentially make a bearish continuation towards the first support level before bouncing back up towards the first resistance level.

The first support level is at 1983.34, which is an overlap support. The second support level at 1969.55 is also an overlap support and is at 78.60% Fibonacci retracement.

On the other hand, the first resistance level at 2011.65 is an overlap resistance and is at 50% Fibonacci retracement. The second resistance level at 2048.77 is a swing high resistance.

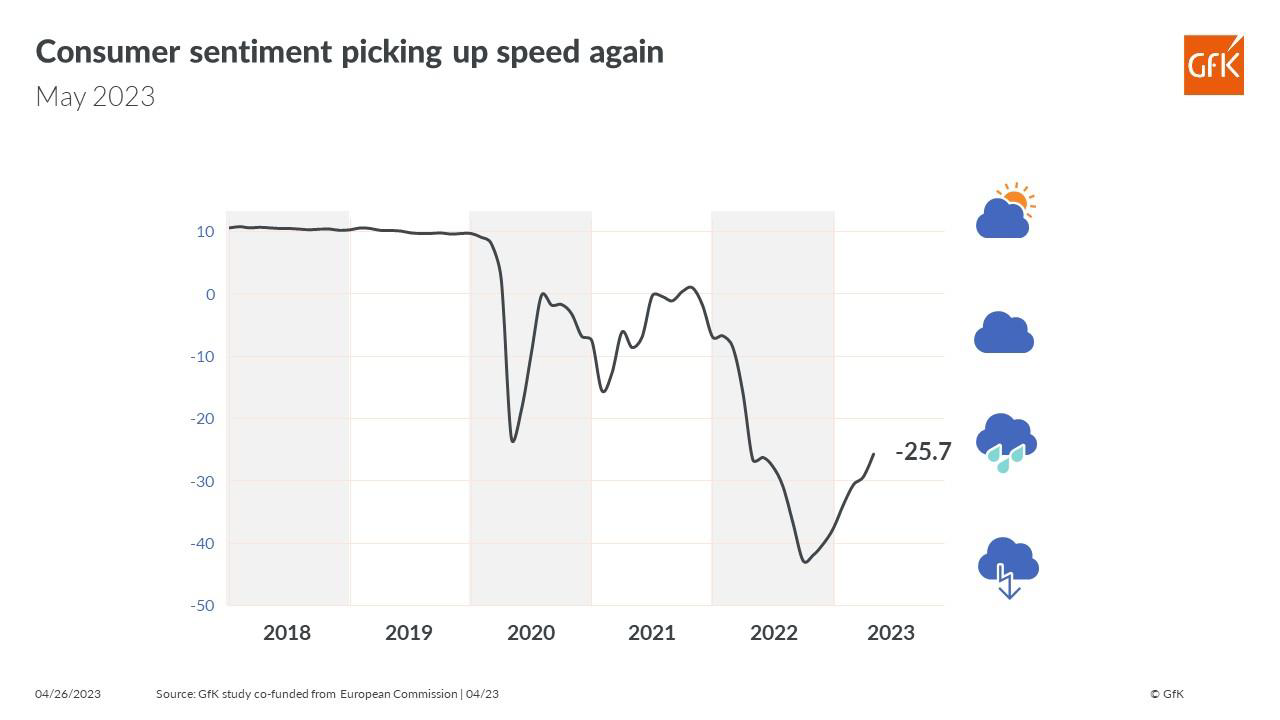

Germany Gfk consumer sentiment rose to -25.7, improved economic and income expectations

Germany Gfk Consumer Sentiment for May improved from -29.3 to -25.7, above expectation of -27.5. In April, Economic Expectations rose sharply from 3.7 to 14.3. Income Expectations rose from -24.3 to -10.7. Propensity to Buy rose from -17.0 to -13.1.

The seventh increase in a row indicates that consumer sentiment is gathering momentum. "Following a rather small increase in the previous month, consumer sentiment is showing clear signs of an upswing this month," explains Rolf Bürkl, GfK consumer expert.

"However, the value still remains below pre-pandemic levels of around three years ago. On another positive note, income expectations have risen for the seventh time in a row, returning to the level prior to the start of the war in Ukraine for the first time."

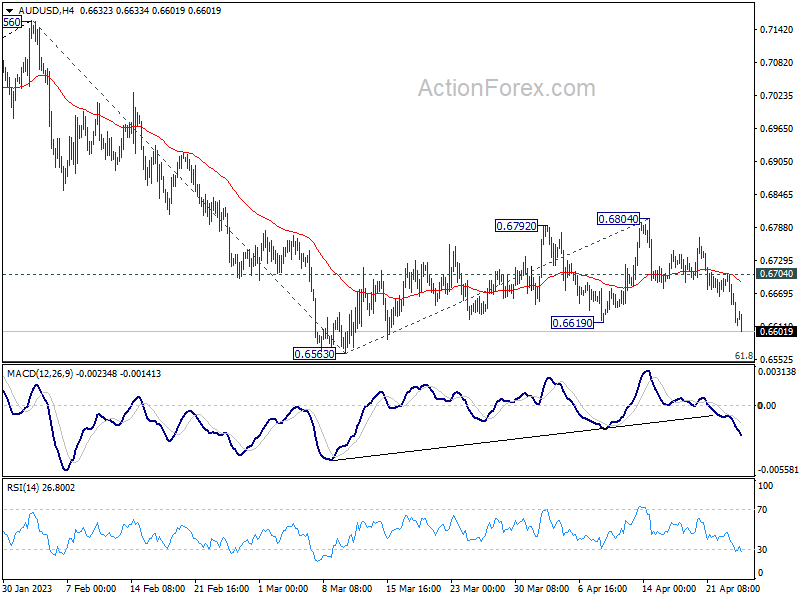

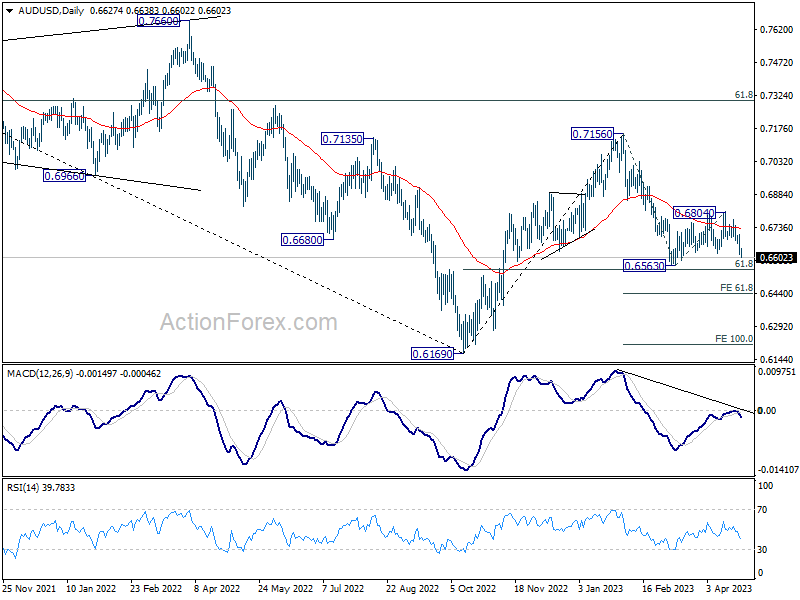

AUD/USD Daily Report

Daily Pivots: (S1) 0.6592; (P) 0.6649; (R1) 0.6683; More...

AUD/USD's break of 0.6619 support argues that consolidation pattern from 0.6563 has completed at 0.6804, and larger fall from 0.7156 is ready to resume. Intraday bias is now on the downside for 0.6563 support first. Firm break there should bring deeper decline through 0.6546 fibonacci level to 61.8% projection of 0.7156 to 0.6563 from 0.6804 at 0.6438 next. On the upside, though, above 0.6704 minor resistance will delay the bearish case and turn intraday bias neutral first.

In the bigger picture, as long as 61.8% retracement of 0.6169 to 0.7156 at 0.6546 holds, the decline from 0.7156 is seen as a correction to rally from 0.6169 (2022 low) only. Another rise should still be seen through 0.7156 at a later stage. However, sustained break of 0.6546 will raise the chance of long term down trend resumption through 0.6169 low.

Risk Aversion Gains Momentum, Aussie Heading Back to Year Low Against Dollar

Risk aversion is intensifying as US stocks tumbled significantly overnight, following First Republic Bank's earnings report, which reignited concerns about the broader banking sector. The troubled regional bank's shares plummeted by nearly half. Concurrently, bonds surged higher, pushing 10-year yield below 3.4% handle. Japanese Yen and Swiss Franc surged following the shift in sentiment, trailed by Dollar.

Meanwhile, Australian Dollar led the decline, as it was further pressured by plunging Copper prices. Aussie could be ready to break through 2023 low against the greenback. Canadian Dollar followed as the second worst performer, with Sterling following. Euro is mixed as partly supported by hawkish comments by ECB officials.

Technically, it appears that NASDAQ's rebound from 10,982.80 has peaked at 12,245.42, just ahead of 12,269.55 resistance. Immediate focus returns to 55 D EMA (now at 11,779.21). Sustained break there could prompt deeper decline back towards 10,982.80 support. As long as 10,982.80 support holds, outlook would be more neutral than bearish, with another rise through 12,269.55 remaining slightly in favor. However, firm break below 10,982.80 could signal that larger downtrend from 2021 high of 16,212.22 is resuming through 10,088.82 low.

In Asia, at the time of writing, Nikkei is down -0.92%. Hong Kong HSI is up 0.59%. China Shanghai SSE is down -0.31%. Singapore Strait Times is down -0.15%. Japan 10-year JGB yield is down -0.015 at 0.465. Overnight DOW dropped -1.02%. S&P 500 dropped -1.58%. NASDAQ dropped -1.98%. 10-year yield dropped sharply by -0.119 to 3.396.

BoE Pill: We've had a series of transitory inflation shocks one after the other

In an interview on the "Beyond Unprecedented" podcast produced by Columbia University's law school, BoE Chief Economist Huw Pill reiterated the central bank's official forecast, stating that some factors maintaining high inflation are likely to recede in the upcoming months and that inflation could fall below the 2% target in the next few years.

Discussing the continuous inflationary shocks faced by the UK, Pill said, "We've had a series of inflation shocks that just come one after the other." He added, "Each of those shocks was in itself transitory, but they just were timed in a way that inflation never dissipated."

Pill emphasized the need for UK citizens to accept being worse off and to refrain from trying to maintain their real spending power by driving up prices through higher wages or passing on energy costs to customers. Pill observed, "What we're facing now is that reluctance to accept that, yes, we're all worse off and have to take our share."

He also highlighted the UK's status as a major net importer of natural gas and the resulting challenges, noting, "The UK, which is a big net importer of natural gas, is facing a situation that the price of what you're buying from the rest of the world has gone up a lot, relative to the price of what you're selling to the rest of the world, which is mainly services in the case of the UK."

Pill concluded, "If what you're buying has gone up a lot relative to what you're selling, you're going to be worse off."

BoJ Ueda: Dealing with cost-push inflation is very difficult

In an address to parliament today, BoJ Governor Kazuo Ueda highlighted the difficulties central banks face when dealing with cost-push inflation.

Ueda explained, "In general, dealing with cost-push inflation is very difficult for central banks. On the one hand, you'd like to curb inflation. On the other hand, you don't want to tighten monetary policy knowing that cost-push inflation will cool the economy."

The governor emphasized the importance of striking the right balance, which he said, "depends on economic developments at the time, including where inflation stood at the outset."

Ueda also noted that cost-push inflation in Japan is likely to ease as prices of imported raw materials have probably peaked.

These comments come ahead of BoJ's two-day policy meeting starting on Thursday, during which the central bank is widely anticipated to maintain its ultra-loose monetary policy.

Australia CPI down to 7.0% yoy in Q1, 6.3% yoy in Mar

Australia CPI slowed from 7.8% yoy to 7.0% yoy in Q1, slightly above expectation of 6.9% yoy. For the quarter, CPI rose 1.4% qoq, down from prior 1.9% qoq, below expectation of 1.3% qoq. Trimmed mean CPI rose 1.2% qoq, 6.6% yoy while weighted median CPI rose 1.2% qoq, 5.8% yoy.

Michelle Marquardt, ABS head of prices statistics, said "CPI inflation slowed in the March quarter, with the quarterly rise being the lowest since December 2021. While prices continued to rise for most goods and services, many of these increases were smaller than they have been in recent quarters."

Monthly CPI slowed from 6.8% yoy to 6.3% yoy in March, below expectation of 6.5% yoy. Excluding volatile items (Fruit and vegetables and Automotive fuel) CPI, rose from 6.8% yoy to 6.9% yoy.

NZ imports surged 10% yoy, export rose 0.6% yoy in Mar

New Zealand goods exports rose 0.6% yoy or NZD 40m to NZD 6.5B in March. Imports rose 10% yoy or NZD 719m to NZD 7.8B. Monthly trade balance recorded a deficit of NZD -1.3B, larger than expectation of NZD -0.5B.

Australia contributed the most to the growth in monthly exports, with a 30% rise. Goods exports to the US was up 4.1%, EU up 28%, but down -9.6% to Japan and down -5.7% to China.

On the other hand, imports from the US leads the monthly rise, up 39%. Imports from EU and South Korea grew 24% and 20% respectively. On the other hand, imports from China was down -13%, Australia down -4.0%.

Looking ahead

Germany Gfk consumer confidence and Swiss Credit Suisse economic expectations will be released in European session. Later in the day, US will publish durable goods orders and goods trade balance.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6592; (P) 0.6649; (R1) 0.6683; More...

AUD/USD's break of 0.6619 support argues that consolidation pattern from 0.6563 has completed at 0.6804, and larger fall from 0.7156 is ready to resume. Intraday bias is now on the downside for 0.6563 support first. Firm break there should bring deeper decline through 0.6546 fibonacci level to 61.8% projection of 0.7156 to 0.6563 from 0.6804 at 0.6438 next. On the upside, though, above 0.6704 minor resistance will delay the bearish case and turn intraday bias neutral first.

In the bigger picture, as long as 61.8% retracement of 0.6169 to 0.7156 at 0.6546 holds, the decline from 0.7156 is seen as a correction to rally from 0.6169 (2022 low) only. Another rise should still be seen through 0.7156 at a later stage. However, sustained break of 0.6546 will raise the chance of long term down trend resumption through 0.6169 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | -500M | -714M | ||

| 01:30 | AUD | Monthly CPI Y/Y Mar | 6.30% | 6.50% | 6.80% | |

| 01:30 | AUD | CPI Q/Q Q1 | 1.40% | 1.30% | 1.90% | |

| 01:30 | AUD | CPI Y/Y Q1 | 7.00% | 6.90% | 7.80% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 1.20% | 1.40% | 1.70% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 6.60% | 7.20% | 6.90% | |

| 06:00 | EUR | Germany Gfk Consumer Confidence May | -27.5 | -29.5 | ||

| 08:00 | CHF | Credit Suisse Economic Expectations Apr | -41.3 | |||

| 12:30 | USD | Goods Trade Balance (USD) Mar P | -89.8B | -91.6B | ||

| 12:30 | USD | Wholesale Inventories Mar P | -0.20% | 0.10% | ||

| 12:30 | USD | Durable Goods Orders Mar | 0.80% | -1.00% | ||

| 12:30 | USD | Durable Goods Orders ex Transport Mar | -0.20% | -0.10% | ||

| 14:30 | USD | Crude Oil Inventories | -1.3M | -4.6M |