Sample Category Title

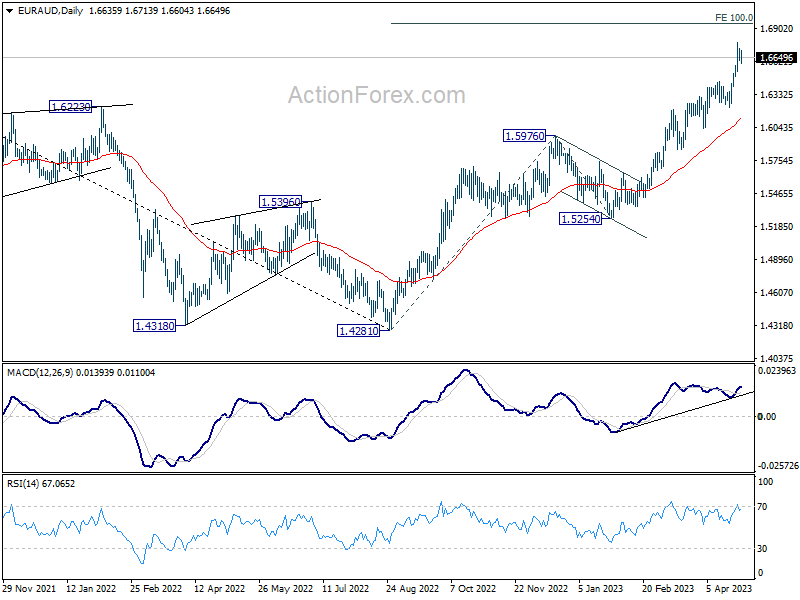

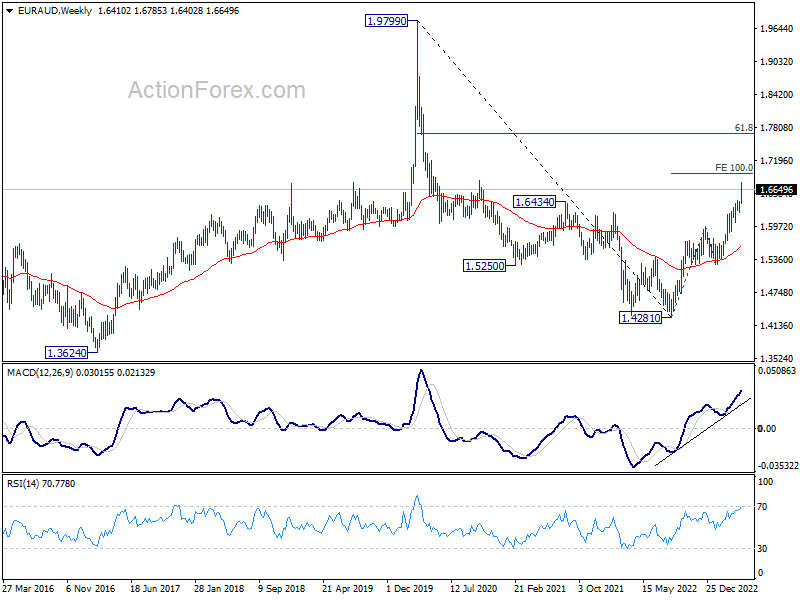

EUR/AUD Weekly Outlook

EUR/AUD's up trend resumed last week and surged to as high as 1.6783. But as a temporary top was formed there. Initial bias remains neutral for consolidations. Downside of retreat should be contained by 1.6444 resistance turned support to bring rally resumption. On the upside, break of 1.6785 will resume larger up trend from 1.4281 to 100% projection of 1.4281 to 1.5976 from 1.5254 at 1.6949.

In the bigger picture, the solid break of 1.6434 resistance argues that whole down trend from 1.9799 (2020 high) has completed at 1.4281 (2022 low). Further rise should be seen to 61.8% retracement of 1.9799 to 1.4281 at 1.7691 next. For now, outlook will stay bullish as long as 1.5976 resistance turned support holds, even in case of deep pull back.

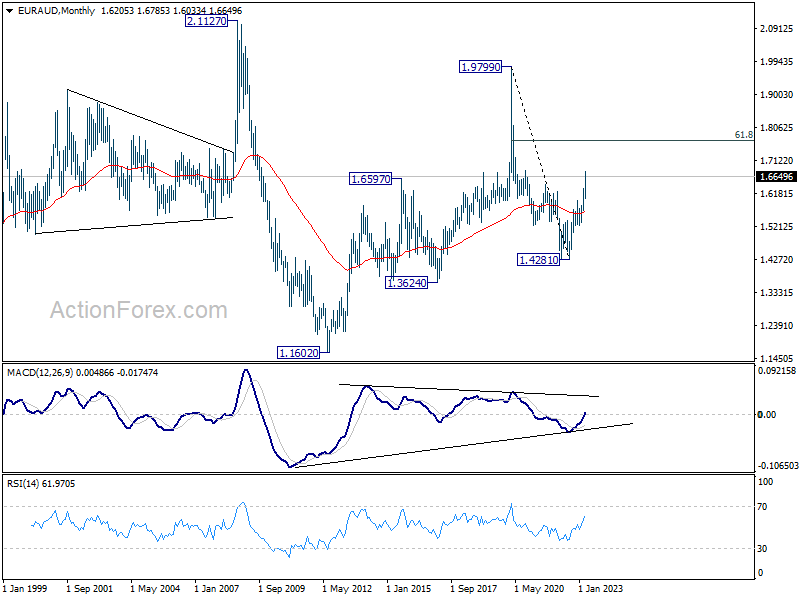

In the longer term picture, it's still early to decide if rise from 1.4281 is resuming whole up trend from 1.1602 (2012 low). Attention will be paid on the structure on the current rally to make an assessment later.

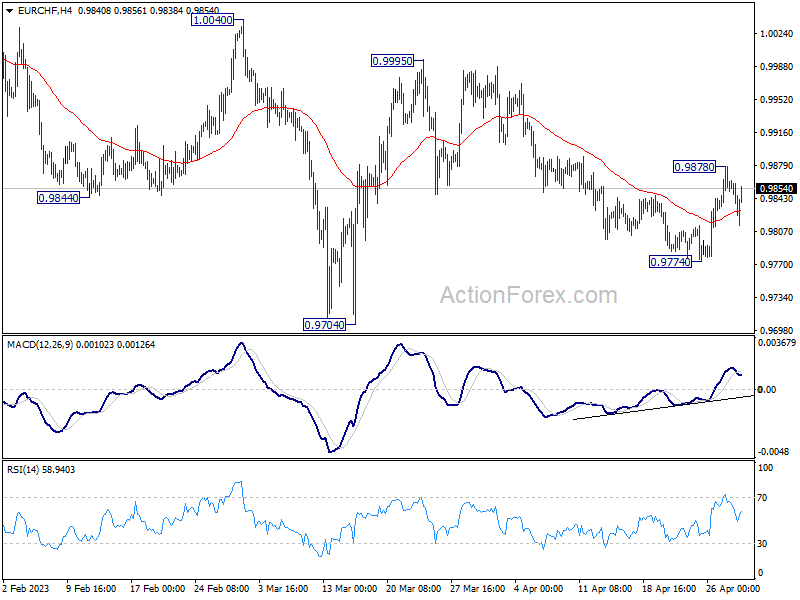

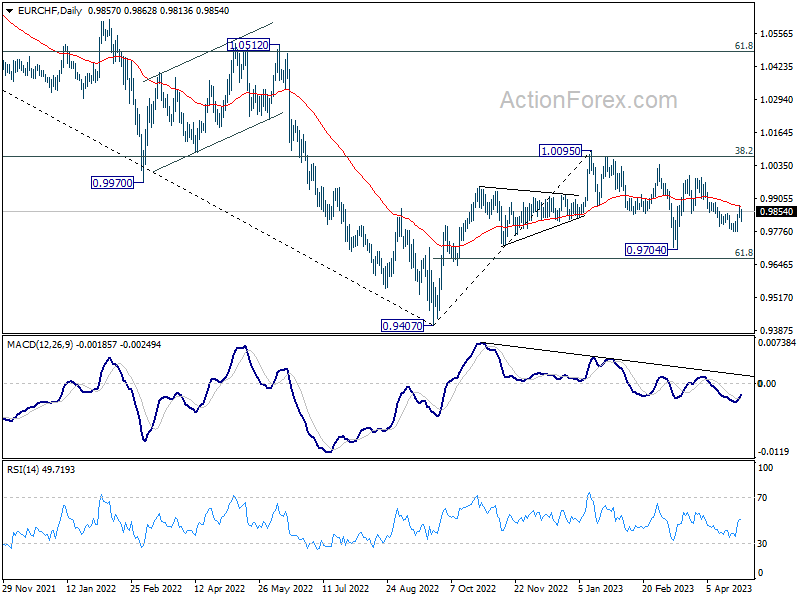

EUR/CHF Weekly Outlook

EUR/CHF rebounded to 0.9878 last week but retreated since then. Initial bias is turned neutral this week for consolidations first. A short term bottoming should be in place at 0.9774 on bullish convergence condition in 4H MACD. Hence, risk will stay on the upside as long as 0.9774 holds. Also, the development revived the case that whole correction from 1.0095 has completed at 0.9704. Break of 0.9878, and sustained trading above 55 D EMA (now at 0.9875) will affirm this bullish case, and target 0.9995 resistance next.

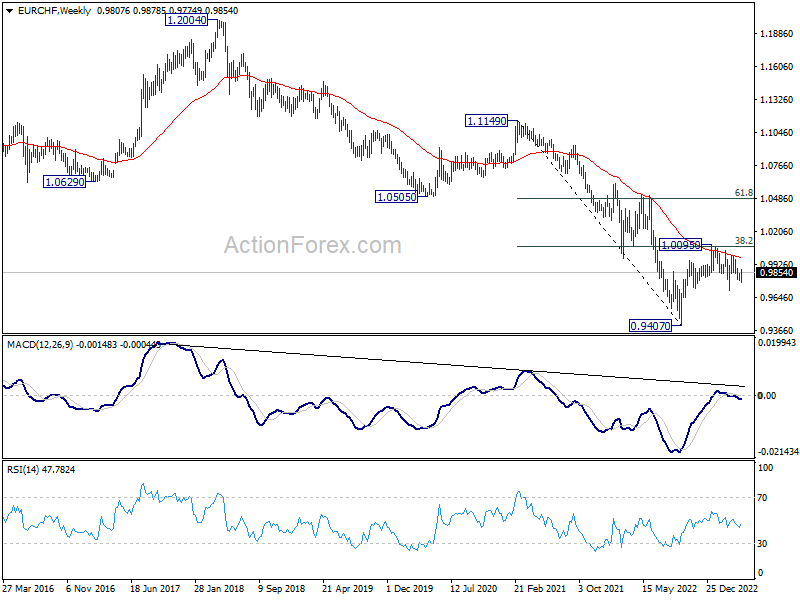

In the bigger picture, prior rejection by 55 W EMA (now at 0.9989) and 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. That is, down trend from 1.2004 is not completed yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

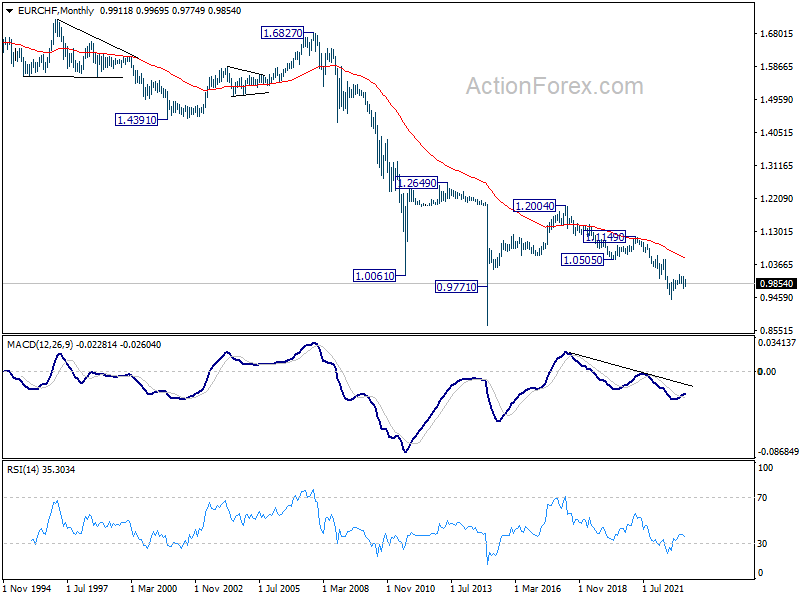

In the long term picture, it's still way too early too call for bullish trend reversal with upside capped well below 55 M EMA (now at 1.0566) and 1.0505 support turned resistance (2020 low). The multi-decade down trend could still continue.

Summary 5/1 – 5/5

Monday, May 1, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Apr F | 49.5 | 49.5 |

| 01:00 | AUD | TD Securities Inflation M/M Apr | 0.30% | |

| 05:00 | JPY | Consumer Confidence Apr | 35 | 33.9 |

| 13:30 | CAD | Manufacturing PMI Apr | 50.5 | 48.6 |

| 13:45 | USD | Manufacturing PMI Apr F | 50.4 | 50.4 |

| 14:00 | USD | ISM Manufacturing PMI Apr | 46.6 | 46.3 |

| 14:00 | USD | ISM Manufacturing Prices Paid Apr | 50.4 | 49.2 |

| 14:00 | USD | ISM Manufacturing Employment Index Apr | 46.9 | |

| 14:00 | USD | Construction Spending M/M Mar | 0.20% | -0.10% |

| 23:50 | JPY | Monetary Base Y/Y Apr | -1.50% | -1.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Apr F | |

| Forecast: 49.5 | Previous: 49.5 | ||

| 01:00 | AUD | TD Securities Inflation M/M Apr | |

| Forecast: | Previous: 0.30% | ||

| 05:00 | JPY | Consumer Confidence Apr | |

| Forecast: 35 | Previous: 33.9 | ||

| 13:30 | CAD | Manufacturing PMI Apr | |

| Forecast: 50.5 | Previous: 48.6 | ||

| 13:45 | USD | Manufacturing PMI Apr F | |

| Forecast: 50.4 | Previous: 50.4 | ||

| 14:00 | USD | ISM Manufacturing PMI Apr | |

| Forecast: 46.6 | Previous: 46.3 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Apr | |

| Forecast: 50.4 | Previous: 49.2 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Apr | |

| Forecast: | Previous: 46.9 | ||

| 14:00 | USD | Construction Spending M/M Mar | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 23:50 | JPY | Monetary Base Y/Y Apr | |

| Forecast: -1.50% | Previous: -1.00% | ||

Tuesday, May 2, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | AUD | RBA Interest Rate Decision | 3.60% | 3.60% |

| 06:00 | EUR | Germany Retail Sales M/M Mar | 0.40% | -1.30% |

| 07:00 | CHF | SECO Consumer Climate Q2 | -22 | -30 |

| 07:30 | CHF | Manufacturing PMI Apr | 50 | 47 |

| 07:45 | EUR | Italy Manufacturing PMI Apr | 49 | 51.1 |

| 07:50 | EUR | France Manufacturing PMI Apr F | 45.5 | 45.5 |

| 07:55 | EUR | Germany Manufacturing PMI Apr F | 44 | 44 |

| 08:00 | EUR | Eurozone Manufacturing PMI Apr F | 45.5 | 45.5 |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 3.10% | 2.90% |

| 08:30 | GBP | Manufacturing PMI Apr | 46.6 | 46.6 |

| 09:00 | EUR | Eurozone CPI Y/Y Apr P | 6.90% | 6.90% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr P | 5.70% | 5.70% |

| 14:00 | USD | Factory Orders M/M Mar | 0.80% | -0.70% |

| 22:45 | NZD | Employment Change Q1 | 0.40% | 0.20% |

| 22:45 | NZD | Unemployment Rate Q1 | 3.50% | 3.40% |

| 22:45 | NZD | Labour Cost Index Q/Q Q1 | 1.10% | 1.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 3.60% | Previous: 3.60% | ||

| 06:00 | EUR | Germany Retail Sales M/M Mar | |

| Forecast: 0.40% | Previous: -1.30% | ||

| 07:00 | CHF | SECO Consumer Climate Q2 | |

| Forecast: -22 | Previous: -30 | ||

| 07:30 | CHF | Manufacturing PMI Apr | |

| Forecast: 50 | Previous: 47 | ||

| 07:45 | EUR | Italy Manufacturing PMI Apr | |

| Forecast: 49 | Previous: 51.1 | ||

| 07:50 | EUR | France Manufacturing PMI Apr F | |

| Forecast: 45.5 | Previous: 45.5 | ||

| 07:55 | EUR | Germany Manufacturing PMI Apr F | |

| Forecast: 44 | Previous: 44 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Apr F | |

| Forecast: 45.5 | Previous: 45.5 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | |

| Forecast: 3.10% | Previous: 2.90% | ||

| 08:30 | GBP | Manufacturing PMI Apr | |

| Forecast: 46.6 | Previous: 46.6 | ||

| 09:00 | EUR | Eurozone CPI Y/Y Apr P | |

| Forecast: 6.90% | Previous: 6.90% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Apr P | |

| Forecast: 5.70% | Previous: 5.70% | ||

| 14:00 | USD | Factory Orders M/M Mar | |

| Forecast: 0.80% | Previous: -0.70% | ||

| 22:45 | NZD | Employment Change Q1 | |

| Forecast: 0.40% | Previous: 0.20% | ||

| 22:45 | NZD | Unemployment Rate Q1 | |

| Forecast: 3.50% | Previous: 3.40% | ||

| 22:45 | NZD | Labour Cost Index Q/Q Q1 | |

| Forecast: 1.10% | Previous: 1.10% | ||

Wednesday, May 3, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Mar | 0.20% | 0.20% |

| 08:00 | EUR | Italy Unemployment Rate Mar | 8.10% | 8.00% |

| 09:00 | EUR | Eurozone Unemployment Rate Mar | 6.60% | 6.60% |

| 12:15 | USD | ADP Employment Change Apr | 150K | 145K |

| 13:45 | USD | Services PMI Apr F | 53.7 | 53.7 |

| 14:00 | USD | ISM Services PMI Apr | 53.1 | 51.2 |

| 14:30 | USD | Crude Oil Inventories | -5.1M | |

| 18:00 | USD | Fed Interest Rate Decision | 5.25% | 5.00% |

| 18:30 | USD | FOMC Press Conference | ||

| 22:45 | NZD | Building Permits M/M Mar | -9.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Mar | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 08:00 | EUR | Italy Unemployment Rate Mar | |

| Forecast: 8.10% | Previous: 8.00% | ||

| 09:00 | EUR | Eurozone Unemployment Rate Mar | |

| Forecast: 6.60% | Previous: 6.60% | ||

| 12:15 | USD | ADP Employment Change Apr | |

| Forecast: 150K | Previous: 145K | ||

| 13:45 | USD | Services PMI Apr F | |

| Forecast: 53.7 | Previous: 53.7 | ||

| 14:00 | USD | ISM Services PMI Apr | |

| Forecast: 53.1 | Previous: 51.2 | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -5.1M | ||

| 18:00 | USD | Fed Interest Rate Decision | |

| Forecast: 5.25% | Previous: 5.00% | ||

| 18:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 22:45 | NZD | Building Permits M/M Mar | |

| Forecast: | Previous: -9.00% | ||

Thursday, May 4, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Mar | 13.00B | 13.87B |

| 01:45 | CNY | Caixin Manufacturing PMI Apr | 50.8 | 50 |

| 06:00 | EUR | Germany Trade Balance (EUR) Mar | 17.1B | 16.0B |

| 07:45 | EUR | Italy Services PMI Apr | 56 | 55.7 |

| 07:50 | EUR | France Services PMI Apr F | 56.3 | 56.3 |

| 07:55 | EUR | Germany Services PMI Apr F | 55.7 | 55.7 |

| 08:00 | EUR | Eurozone Services PMI Apr F | 56.6 | 56.6 |

| 08:30 | GBP | Mortgage Approvals Mar | 46K | 44K |

| 08:30 | GBP | Services PMI Apr F | 54.9 | 54.9 |

| 08:30 | GBP | M4 Money Supply M/M Mar | 0.10% | -0.40% |

| 09:00 | EUR | Eurozone PPI M/M Mar | -0.50% | |

| 09:00 | EUR | Eurozone PPI Y/Y Mar | 13.20% | |

| 12:15 | EUR | ECB Main Refinancing Rate | 4.00% | 3.50% |

| 12:30 | CAD | Trade Balance (CAD) Mar | 1.0B | 0.4B |

| 12:30 | USD | Initial Jobless Claims (Apr 28) | 235K | 230K |

| 12:30 | USD | Trade Balance (USD) Mar | -68.9B | -70.5B |

| 12:30 | USD | Nonfarm Productivity Q1 P | -0.70% | 1.70% |

| 12:30 | USD | Unit Labor Costs Q1 P | 8.40% | 3.20% |

| 12:45 | EUR | ECB Press Conference | ||

| 14:00 | CAD | Ivey PMI Apr | 59 | 58.2 |

| 14:00 | CAD | Ivey Purchasing Managers Index s.a Apr | 58.2 | |

| 14:30 | USD | Natural Gas Storage | 79B |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Mar | |

| Forecast: 13.00B | Previous: 13.87B | ||

| 01:45 | CNY | Caixin Manufacturing PMI Apr | |

| Forecast: 50.8 | Previous: 50 | ||

| 06:00 | EUR | Germany Trade Balance (EUR) Mar | |

| Forecast: 17.1B | Previous: 16.0B | ||

| 07:45 | EUR | Italy Services PMI Apr | |

| Forecast: 56 | Previous: 55.7 | ||

| 07:50 | EUR | France Services PMI Apr F | |

| Forecast: 56.3 | Previous: 56.3 | ||

| 07:55 | EUR | Germany Services PMI Apr F | |

| Forecast: 55.7 | Previous: 55.7 | ||

| 08:00 | EUR | Eurozone Services PMI Apr F | |

| Forecast: 56.6 | Previous: 56.6 | ||

| 08:30 | GBP | Mortgage Approvals Mar | |

| Forecast: 46K | Previous: 44K | ||

| 08:30 | GBP | Services PMI Apr F | |

| Forecast: 54.9 | Previous: 54.9 | ||

| 08:30 | GBP | M4 Money Supply M/M Mar | |

| Forecast: 0.10% | Previous: -0.40% | ||

| 09:00 | EUR | Eurozone PPI M/M Mar | |

| Forecast: | Previous: -0.50% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Mar | |

| Forecast: | Previous: 13.20% | ||

| 12:15 | EUR | ECB Main Refinancing Rate | |

| Forecast: 4.00% | Previous: 3.50% | ||

| 12:30 | CAD | Trade Balance (CAD) Mar | |

| Forecast: 1.0B | Previous: 0.4B | ||

| 12:30 | USD | Initial Jobless Claims (Apr 28) | |

| Forecast: 235K | Previous: 230K | ||

| 12:30 | USD | Trade Balance (USD) Mar | |

| Forecast: -68.9B | Previous: -70.5B | ||

| 12:30 | USD | Nonfarm Productivity Q1 P | |

| Forecast: -0.70% | Previous: 1.70% | ||

| 12:30 | USD | Unit Labor Costs Q1 P | |

| Forecast: 8.40% | Previous: 3.20% | ||

| 12:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 14:00 | CAD | Ivey PMI Apr | |

| Forecast: 59 | Previous: 58.2 | ||

| 14:00 | CAD | Ivey Purchasing Managers Index s.a Apr | |

| Forecast: | Previous: 58.2 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 79B | ||

Friday, May 5, 2023

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | RBA Monetary Policy Statement | ||

| 01:45 | CNY | Caixin Services PMI Apr | 56.5 | 57.8 |

| 05:45 | CHF | Unemployment Rate Apr | 1.90% | 1.90% |

| 06:00 | EUR | Germany Factory Orders M/M Mar | -2.00% | 4.80% |

| 06:30 | CHF | CPI M/M Apr | 0.20% | 0.20% |

| 06:30 | CHF | CPI Y/Y Apr | 2.80% | 2.90% |

| 06:45 | EUR | France Industrial Output M/M Mar | -0.30% | 1.20% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Apr | 743B | |

| 08:00 | EUR | Italy Retail Sales M/M Mar | 0.00% | -0.10% |

| 08:30 | GBP | Construction PMI Apr | 51.1 | 50.7 |

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | -0.20% | -0.80% |

| 12:30 | USD | Nonfarm Payrolls Apr | 181K | 236K |

| 12:30 | USD | Unemployment Rate Apr | 3.50% | 3.50% |

| 12:30 | USD | Average Hourly Earnings M/M Apr | 0.30% | 0.30% |

| 12:30 | CAD | Net Change in Employment Apr | 34.7K | |

| 12:30 | CAD | Unemployment Rate Apr | 5% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | RBA Monetary Policy Statement | |

| Forecast: | Previous: | ||

| 01:45 | CNY | Caixin Services PMI Apr | |

| Forecast: 56.5 | Previous: 57.8 | ||

| 05:45 | CHF | Unemployment Rate Apr | |

| Forecast: 1.90% | Previous: 1.90% | ||

| 06:00 | EUR | Germany Factory Orders M/M Mar | |

| Forecast: -2.00% | Previous: 4.80% | ||

| 06:30 | CHF | CPI M/M Apr | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 06:30 | CHF | CPI Y/Y Apr | |

| Forecast: 2.80% | Previous: 2.90% | ||

| 06:45 | EUR | France Industrial Output M/M Mar | |

| Forecast: -0.30% | Previous: 1.20% | ||

| 07:00 | CHF | Foreign Currency Reserves (CHF) Apr | |

| Forecast: | Previous: 743B | ||

| 08:00 | EUR | Italy Retail Sales M/M Mar | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 08:30 | GBP | Construction PMI Apr | |

| Forecast: 51.1 | Previous: 50.7 | ||

| 09:00 | EUR | Eurozone Retail Sales M/M Apr | |

| Forecast: -0.20% | Previous: -0.80% | ||

| 12:30 | USD | Nonfarm Payrolls Apr | |

| Forecast: 181K | Previous: 236K | ||

| 12:30 | USD | Unemployment Rate Apr | |

| Forecast: 3.50% | Previous: 3.50% | ||

| 12:30 | USD | Average Hourly Earnings M/M Apr | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 12:30 | CAD | Net Change in Employment Apr | |

| Forecast: | Previous: 34.7K | ||

| 12:30 | CAD | Unemployment Rate Apr | |

| Forecast: | Previous: 5% | ||

Weekly Economic & Financial Commentary: Eurozone Avoids Recession, Bank of Japan Keeps Policy Unchanged

Summary

United States: Labor Costs Complicate the Ride Back to 2% Inflation

- The U.S. economy expanded at a weaker-than-expected pace in Q1; real GDP grew at a 1.1% annualized rate. The ECI increased a hotter-than-expected 1.2% in Q1, suggesting compensation costs are not cooling as much as the average hourly earnings data indicate.

- Next week: Construction Spending (Mon), ISM PMIs (Mon & Wed), Employment (Fri)

International: Eurozone Avoids Recession, Bank of Japan Keeps Policy Unchanged

- The Eurozone's Q1 GDP data revealed that the economy narrowly avoided recession to start the year, with the economy expanding 0.1% quarter-over-quarter in Q1 after contracting 0.1% in Q4-2022. Elsewhere, the Bank of Japan (BoJ) held its first monetary policy meeting under Governor Ueda and decided unanimously to keep policy settings unchanged. While Ueda's commentary leaned dovish, he did not rule out the possibility of an eventual shift in policy.

- Next week: China PMIs (Sun), Reserve Bank of Australia (Tue), Eurozone CPI & European Central Bank (Tue/Thu)

Credit Market Insights: Corporate Bond Spreads Hanging In

- Investment grade bond spreads began widening in 2022 as monetary policy tightening ramped up and the probability of a recession began to rise. More recent, spreads again widened in the wake of the two regional bank failures that occurred in March. However, spreads have retraced about half of that widening since mid-March and are again back to roughly the same level they were a year ago.

Topic of the Week: Up Close on SNAP

- This week, House Republicans passed a bill that would require substantive spending cuts in exchange for raising the federal debt ceiling. Included within the bill was a proposed change to the eligibility guidelines for the Supplemental Nutrition Assistance Program. With decreasing nominal benefits and still rising food prices, the real benefit received by households could continue to decline and have broader implications for the economy.

The Weekly Bottom Line: Core Inflation Remains Elevated, Fed to Hike Next Week

U.S. Highlights

- U.S. real GDP growth slowed to 1.1% quarter-over-quarter (q/q) annualized in 2023 Q1, from 2.6% q/q in the previous quarter. A measure of underlying domestic demand accelerated to 2.9% q/q, supported by a strong gain in consumer spending, although the monthly pattern revealed that the spending gain was entirely concentrated in January.

- New home sales grew by 9.6% month-on-month in March. While this series is volatile, it has been trending up since the end of last year.

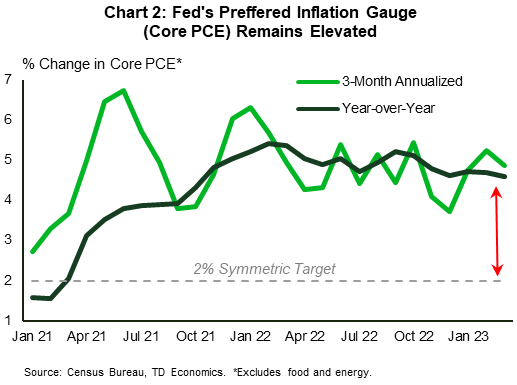

- Core PCE inflation remained elevated in March, easing modestly to 4.6% year-on-year from 4.7% in February.

Canadian Highlights

- February’s GDP print came in weaker than Statistics Canada’s estimate. Accounting for a decline in the flash estimate for March, first quarter GDP growth is tracking at an annualized rate of 2.5%.

- Looking ahead, growth is expected to slow as higher rates continue to work their way through the economy. April’s release of the CFIB small business barometer showed that rising costs of borrowing are a growing concern for entrepreneurs.

- This week was also marked by a continuation of the federal public workers strike. We expect the strike to weigh on GDP growth in the near term, with offsetting growth in subsequent periods, resulting in an overall neutral impact.

U.S. - Core Inflation Remains Elevated, Fed to Hike Next Week

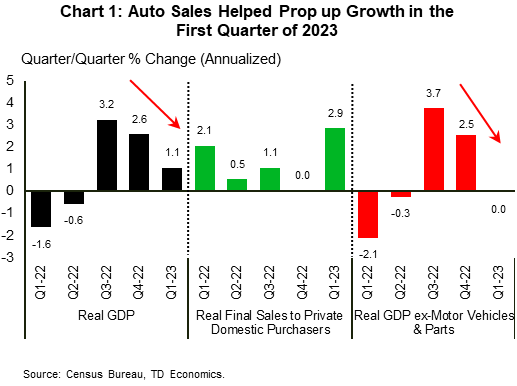

U.S. real GDP growth slowed to a 1.1% quarter-over-quarter (q/q) annualized pace in the first quarter of 2023, from 2.6% q/q at the end of 2022. While consensus expectations were looking for a better print, a slowdown in growth was always in the cards as a reversal of the prior quarter’s inventory built-up was expected. That reversal materialized. Government spending, meanwhile, provided an offset, delivering a 0.8 percentage point (pp) contribution to growth. With the combined impact of inventories and government spending adding volatility to the data, we typically look past these items and focus on ‘final sales to private domestic purchasers’ to get a clearer reading of underlying domestic demand. After several quarters of slow growth, this measure accelerated to 2.9% q/q, supported by a strong gain in consumer spending (+3.7%).

At face value, the acceleration in underlying domestic demand is good news. However, monthly spending data shows that the strength was concentrated in January, with growth flatlining over the next two months. Much of the quarter’s strength came from auto sales. Unit auto sales grew from 14.3 million (annualized) at the end of 2022, to 15.3 million in 2023 Q1, resulting in a 1.1 (pp) contribution to GDP. If we remove that impact, the rest of the economy recorded zero growth (Chart 1). While our forecast calls for motor vehicles sales to remain at a high level over the near-term, as pent-up demand is satiated by improved production (see here), this channel is unlikely to offer the same level of support in 2023 Q2.

Residential investment remained a growth detractor for the eight consecutive quarter, but its negative impact moderated noticeably as average declines of 26% q/q in the second half of 2022 eased to 4.2% q/q in 2023 Q1. We expect residential investment to be less of a drag this year, a message echoed by some moderate positive signals out of the housing market. New home sales, a volatile series, continue to trend up since the end of last year, rising 9.6% month-on-month in March. This is happening as tight supply conditions on the existing home market look to be driving some more action towards the new home market. That said, with housing affordability still exceptionally low, buyers are showing increased sensitivity to mortgage rates (though with the typical lag). An index tracking the number of contracts signed to purchase existing homes, a reliable indicator of closed sales, fell 5.2% in March amidst an uptrend in mortgage rates earlier in the month. The stress in regional banking is also likely to have contributed to the hesitation among buyers to sign housing contracts.

In weighing the Fed’s next interest rate decision, the latest PCE report showed that the Fed’s preferred inflation gauge remained elevated in March. While overall PCE slowed noticeably to 4.2% year-on-year (y/y), from 5.1% in the month prior, core PCE eased only modestly to 4.6% y/y (Chart 2). In our view, core PCE inflation has a long way to return to target (see here). As such, we expect the Fed to hike by 25 basis points next week and keep the policy rate at that high level through the end of the year.

Canada – Prepare for Landing

In anticipation of this week's marquee release of industry-based GDP, Canadian financial markets were largely occupied with first quarter corporate earnings reports. The S&P/TSX Composite remained 0.6% weaker on the week at the time of writing, despite a sizeable end of week rebound.

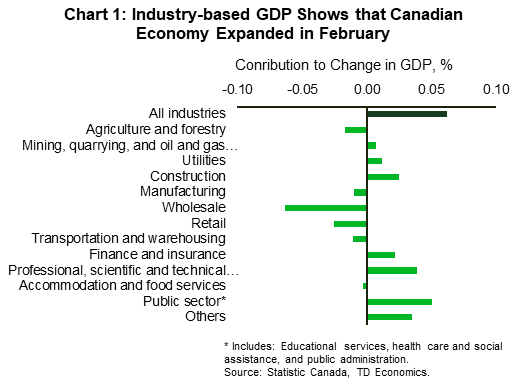

Meanwhile, February's GDP print came in at 0.1% month-on-month (m/m) – weaker than 0.2% m/m expected by the consensus and Statistics Canada's own flash estimate of 0.3% m/m. With today's reading and the flash estimate of -0.1% m/m for March, first quarter GDP is tracking at a rate of 2.5% quarter-on-quarter (q/q) annualized. This is a touch stronger than 2.3% q/q pace the BoC was expecting in its April Monetary Policy Report. Underneath the surface, the major contributor to growth came from residential building construction, which expanded by 0.3% on the month (Chart 1). The public sector, which includes health care and social assistance, public administration, and educational services, was 0.2% higher on the month, clocking in its impressive thirteenth consecutive month of growth.

Offsetting these gains was a decline in manufacturing, transportation & warehousing, as well as retail and wholesale trade. The contraction in trade alone shaved one tens of a percentage points off the headline number, which reiterates our expectation of slowing in household consumption expenditure. According to our internal spend data, services spending growth already shows early signs of moderation, which should help bring down consumption growth to around 1% in 2023 Q2, as higher financing costs continue to work their way through the economy.

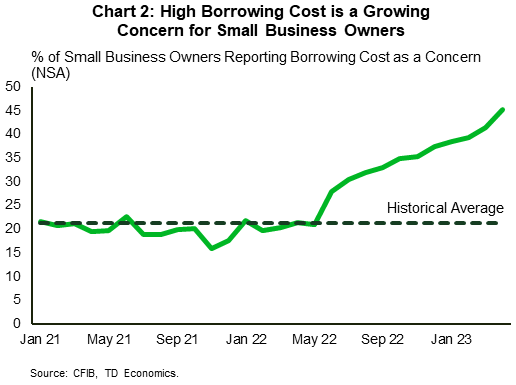

That said, continued fiscal support and robust population growth could buttress demand beyond our current expectations. We estimate that combined new federal and provincial fiscal measures amount to 0.9% of Canadian GDP this year. Notably, government capital spending could boost business investment as private enterprises pull back on investment intentions due to rising costs of borrowing and tighter credit standards. According to April's CFIB small business barometer, 44% of business owners report this as a concern – more than twice the historical average (Chart 2). Another area of concern is rising wage costs, with 68% of business owners identifying it as an impediment to their business and 44% expecting average wage growth to be higher than 3%.

Private enterprises are not the only ones facing wage pressures. This week was marked by a continuation of one of the largest job actions in Canadian history, with more than 100k federal employees on strike. Depending on its duration, we expect it to shave between 0.2 and 0.9 percentage points off monthly GDP growth. But this decline will be reversed in the subsequent periods, with the overall impact being neutral. All in all, "slow but positive growth" remains the most likely scenario for the Canadian economy. Still, we recommend remaining seated with your seat belt fastened as the economy prepares for a soft landing.

Week Ahead – Brace Yourself (Fed, ECB, NFP, Peak Earnings)

US

This week will be extremely busy as we have an FOMC decision, the nonfarm payroll report, peak earnings season, all while Wall Street keeps an eye on the banking industry to see if any news stresses arise. The FOMC meeting is expected to have policymakers deliver one more quarter-point rate rise, possibly leaving the door open for one more. Disinflation trends need to show they are firmly entrenched for the Fed to take their foot off the tightening pedals.

The April nonfarm payroll report is expected to show hiring cooled from 236,000 to 175,000. The labor market is softening, but wages appear to be holding steady.

Peak earnings season is here. Wall Street will pay special attention to results from Adidas, Advanced Micro Devices, American International Group, Anheuser-Busch InBev, Apple, ConocoPhillips, Ford Motor, HSBC Holdings, Infineon Technologies, Intercontinental Exchange, Kraft Heinz, Marriott International, Moderna, Motorola Solutions, Pfizer, Shell, Starbucks, Uber Technologies, UniCredit, Volkswagen, and Yum! Brands

Eurozone

The ECB is under less pressure to pause its tightening cycle than some of its peers. Being late to the party has its perks for once. The health of the European banking system, Credit Suisse aside, is also helpful in that, as was good fortune over the winter which enabled the bloc to not draw too heavily on gas stores. The end result is that the economy looks resilient and the ECB will continue hiking rates, albeit probably by only 25 basis points this time. That said, a nasty shock from the inflation data on Tuesday may change that.

UK

There’s very little from the UK next week barring a few tier three releases including final PMIs, mortgage approvals and house prices. Policywatchers will also pay attention to the BOE’s Decision Maker Panel Survey.

Russia

There’s a few economic releases of note next week including unemployment and the manufacturing and services PMIs.

South Africa

Another quiet week with the whole economy PMI the only notable release.

Turkey

Inflation data in the middle of next week will tell us how much progress has been made in bringing price increases back to more reasonable levels. It’s currently far from that and probably will be for some time, at least until after the election.

Switzerland

Inflation and unemployment data next week will be in focus, the former in particular, given the SNB determination to hike despite the data not being particularly high.

China

A quieter week as China’s stock market will be closed for the Labour Day Golden Week holiday from Monday, 1 May to Wednesday, 3 May. China’s top policy-making body, the Politburo concluded its April meeting last Friday that put emphasis on the role of domestic demand that plays a key role in economic recovery. It added that proactive fiscal policy should be stepped up and work alongside monetary policy to boost the current insufficient levels of demand.

The action comes on Sunday, 30 April for the release of the official NBS Manufacturing and Non-Manufacturing PMI for April. Forecasts are expecting a continuation of manufacturing growth with a slight dip to 51.4 from 51.9 printed in March; as for the non-manufacturing activities where it is expected a slight increase to 58.3 in April from 58.2 in March, and if it turns out as expected, it will be the fourth consecutive month of expansion.

On Thursday, 4 May, the attention will turn to the Caixin Manufacturing PMI for April which consists of smaller SME Chinese manufacturers; forecasts are expecting an expansion to 50.4 from 50.0 recorded in March where it reversed down from its 8-month peak of 51.6 printed in February.

Rounding up the week on Friday is the release of April’s Caixin Services PMI where forecasts are coming in at 58.0, slightly above March’s 57.8. If the estimates turn out as expected, it will mark the fifth consecutive month of growth expansion in the services sector.

Given the latest stance of the Politburo meeting and if April PMIs come in worse than expected, China’s PBOC may be forced to adopt a more expansionary policy soon as it has kept its key policy interest rates unchanged for April.

India

April’s manufacturing PMI is expected to come in at 55.8, a slight dip in growth from a 3-month high of 56.4 recorded in April. Next up, Services PMI for April will be released on Wednesday where consensus estimates are expecting another month of expansion at 57.0, almost unchanged from March’s 57.8.

Australia

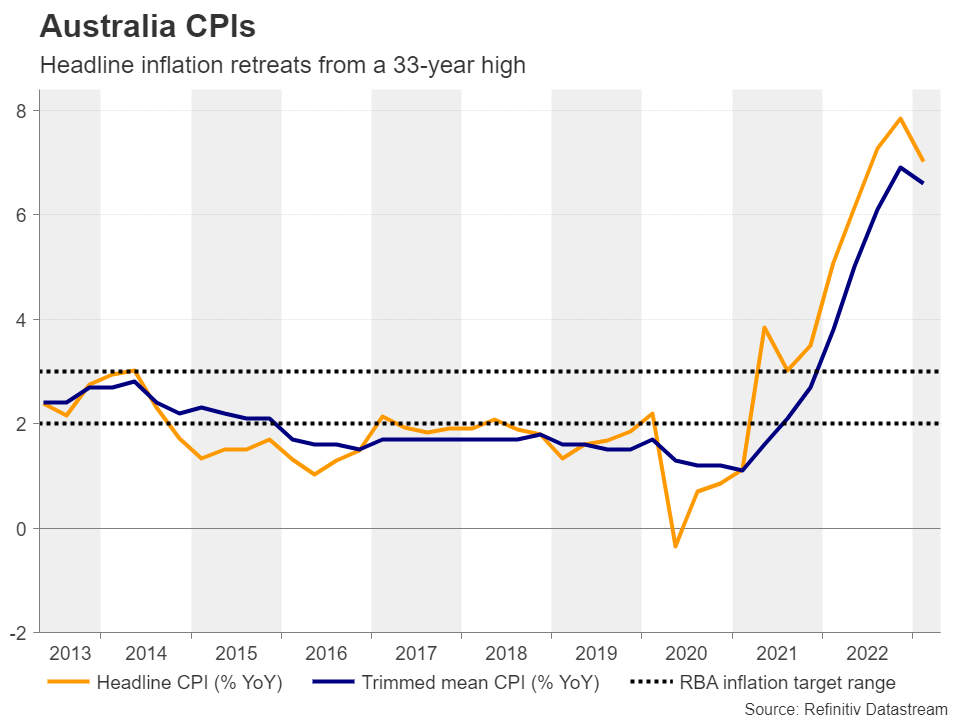

A couple of key data to note, especially the RBA monetary policy decision outcome on Tuesday. The latest Q1 core inflation came in softer than expected which increased the odds of a second consecutive pause on its key policy interest rate at 3.60%.

Retail sales for March will be released on Wednesday and the forecast is expected to show an improvement of a 1% month-on-month growth from 0.2% recorded in February.

Lastly, the trade balance for March is expected to come in at A$12.75 billion, a reduction from A$13.87 billion recorded in February.

New Zealand

The key data to focus on will be Wednesday’s employment data for Q1; the unemployment rate is expected to come in slightly higher at 3.5% from 3.4% printed in Q4 22. In addition, the consensus estimates for the participation rate will be unchanged at 71.7%, a record high.

Lastly, the Labour Cost Index is expected to show an increase of 4.6% year-on-year in Q1 from the previous quarter of 4.3%; if it turns out as expected, it will be the highest growth on record, putting upside pressure on wages.

Japan

A quiet week except for Monday’s final reading of the manufacturing PMI where the earlier preliminary data came in at 49.5, still in a contraction mode but slightly higher than March’s final print of 49.2.

In addition, consumer confidence for April will also be released on Monday, it has shown a remarkable improvement in the previous month where it rose to 33.9 in March, its highest reading since May 2022.

Singapore

The key focus will be on April’s retail sales out on Friday; after a double-digit jump in year-on-year growth to 12.7% in March from a sharp recovery of February’s -0.8% drop, consensus estimates are expecting April’s growth to moderate to 2% year-on-year.

Markets

Energy

It looks like OPEC+ made the right call when they stunned markets with a surprise output cut. The short-term crude demand outlook has not been getting any favors from central banks and this week will likely see a couple big ones, the Fed and ECB will deliver more tightening that will dampen short-term growth prospects. Oil should see some support from the $70 level given the lack of investment in new wells and given how much of the bad news for the US has been priced in and as China’s disappointing COVID reopening should improve going forward.

We’ve heard from the US oil giants, Exxon and Chevron were constructive with the outlook, and now it is BP and Shell’s turn. In addition to some major energy earnings reports, traders will pay close attention to the global manufacturing PMI readings.

Gold

Gold remains a choppy trade after another week filled with renewed banking turmoil, impressive mega-cap tech earnings and mixed economic data that supports more Fed tightening. The upcoming week will have much attention falling on the Fed and ECB rate decisions, but also the nonfarm payroll report. If the US economy continues to show too much resilience, June rate hike odds could grow and that should weigh on gold prices, possibly keeping it from making any serious moves above the $2000 level. .

Crypto

There is a lot of noise in the cryptoverse as investors await clarity over US regulation. The Europeans have been able to create MiCA, the beginnings of legal clarity that provides some rules regarding custody, operations, platforms, advice and portfolio management. Global regulation will be a lengthy process, but seeing some positive developments in the US will be key for investors. Cryptos have been getting a boost as banking crisis jitters remain and as the US economy slows and supports the argument that Fed is nearing the end of its tightening cycle.

For a bullish move higher, Bitcoin needs a major catalyst, perhaps a breakthrough on regulation or a settlement with one of the pending crypto legal cases. Investors will likely remain hesitant to put more money at work with Bitcoin around the $30,000 level unless the fundamentals dramatically change here. The risks are still to the downside for Bitcoin, but major support should come from the $27,000 level.

Saturday, April 29

Economic Events:

- Day 2 of EU finance ministers and central bank governors meeting in Stockholm

Sunday, April 30

Economic Data/Events:

- China April manufacturing PMI: 51.4e v 51.9 prior; Services PMI: 56.7e v 58.2 prior

- UK nurses to strike

Monday, May 1

Economic Data/Events:

- US construction spending, ISM manufacturing

- May Day holiday is observed in the UK, France, and China.

- India manufacturing PMI

- French protests are expected

Tuesday, May 2

Economic Data/Events:

- Fed begins two-day policy meeting

- US factory orders, revised durable goods, light vehicle sales

- Czech Republic GDP

- Eurozone manufacturing PMI, CPI

- France manufacturing PMI

- Germany manufacturing PMI

- Italy CPI

- UK S&P Global/CIPS manufacturing PMI

- RBA Rate Decision: Expected to keep rates steady at 3.60%

- RBA Governor Lowe at RBA Board Dinner in Perth.

- Eurozone bank lending survey.

Wednesday, May 3

Economic Data/Events:

- FOMC Decision: Fed expected to raise rates by 25bps, bringing the target range to 5.00-5.25%

- US ADP payroll data

- Australia retail sales

- Eurozone unemployment

- Italy unemployment

- Mexico international reserves

- New Zealand unemployment

- Russia unemployment

- Spain unemployment

- Thailand CPI

- French constitutional court to rule on referendum request over pension law.

- RBA Assistant Governor Ellis speaks at Committee for Economic Development of Australia in Perth.

- Reserve Bank of New Zealand publishes financial stability report.

Thursday, May 4

Economic Data/Events:

- ECB Rate Decision: Expected to raise rates by 25bps to 3.75%, followed by ECB President Lagarde’s press conference

- US initial jobless claims, international trade in goods and services

- Australia trade balance

- China Caixin manufacturing PMI

- Eurozone S&P Global services PMI, PPI

- Hong Kong retail sales

- Mexico unemployment

- New Zealand building permits

- BOC Governor Tiff Macklem at “fireside chat” at Toronto Regional Board of Trade.

- RBA quarterly update of economic forecasts and policy outlook.

- Norway rate decision: Expected to raise deposit rate by 25bps to 3.25%

- Apple Inc earnings.

Friday, May 5

Economic Data/Events:

- US April Change in nonfarm payrolls: 173Ke v 236K prior; Unemployment Rate: 3.6%e v 3.5% prior; Average Hourly Earnings M/M: 0.3%e v 0.3% prior, Consumer Credit

- Canada unemployment

- China Caixin services PMI

- Eurozone retail sales

- France industrial production

- Germany factory orders

- Singapore retail sales

- Spain industrial production

- US unemployment, non-farm payrolls

- Fed’s Bullard speaks at Economic Club of Minneapolis.

- SNB President Jordan speaks on monetary policy and inflation at event in St. Gallen.

- Riksbank Governor Thedeen speaks at European Competition Day in Arlandastad.

Sovereign Rating Updates:

- EFSF (Fitch)

- ESM (Fitch)

- Switzerland (Fitch)

- Norway (Moody’s)

- Ireland (DBRS)

U.S. Fed Ponders Another Hike Ahead of April Labour Market Data

We expect Canadian employment edged up by about 12,000 in April—the smallest increase since September. That won’t be enough to prevent the unemployment rate from ticking higher as stronger levels of immigration boost the number of workers available for hire. Employment growth early in 2023 has been very strong, but cracks are emerging in the labour demand backdrop. The number of job openings has slowed. And businesses in the BoC’s Q1 Business Outlook Survey highlighted a sharp easing in the intensity of labour shortages. The ongoing Federal employees strike shouldn’t significantly impact the April employment data since those figures are drawn from the week before the strike started. Still, the loss of hours worked will cut into GDP measures that have already been showing signs of slowing. Our own estimate is that the strike will subtract 0.3 percentage points from April’s GDP growth following an initial estimate from Statistics Canada that output already edged lower (-0.1%) in March.

In the U.S., the Federal Reserve will also be watching labour market developments closely. We expect them follow through with one more 25 basis point interest rate hike next Wednesday, though developments in the U.S. job market have largely mirrored Canada’s. Strong headline employment gains have masked some early signs of softening in hiring demand, openings have declined by over a million through February and March and initial claims have been drifting higher. We look for a smaller, but still positive change in employment in April (up 150,000), alongside a tick higher in the unemployment rate. Early signs of labour market weakness are suggesting more deceleration down the road, in both hiring and wage growth. For now, unemployment remains very low and inflation is too high for the Fed’s comfort. But the central bank is likely still approaching the end of the current rate hiking cycle.

Week ahead data watch

The Canadian net trade surplus was likely a bit lower in March. We expect the energy trade surplus to have narrowed on a 4.6% pullback in crude oil prices. Statistics Canada’s advance estimate for March manufacturing sales was reportedly boosted by an increase in transportation equipment sales, which would increase both exports and imports.

Previously released advance estimates of goods trade balance in the U.S. showed a declining deficit, from $92.0B in February to $84.6B in March. We look for a smaller U.S. trade deficit in March, with exports higher by 2% and imports declining by 0.8%.

We expect to see 150,000 jobs to be added to the U.S. labour market in April, down slightly from the 236,000 increase in March. We look for a 0.1 percentage point increase in the unemployment rate, back to February’s 3.6% level.

Week Ahead – Fed and ECB Decisions Set the Stage for US Payrolls

An explosive week lies ahead for global markets, featuring central bank decisions in the United States, Eurozone, and Australia, alongside the latest edition of nonfarm payrolls. The Fed is expected to raise interest rates one final time, so the dollar will react mostly to any signals around future action. But the euro might enjoy even greater volatility, as traders are split on the size of the upcoming ECB rate increase.

Fed to play its final card

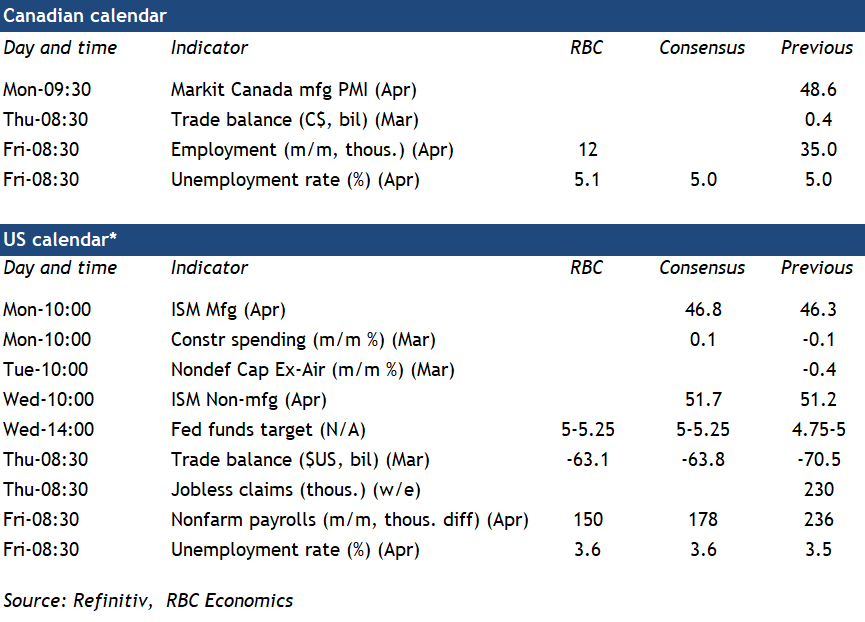

The US economic machine seems to be gathering momentum, with the latest business surveys pointing to a resurgence in demand and an acceleration in jobs growth entering the second quarter. Recession concerns have receded for now, especially after the banking stress calmed down.

Nonetheless, the bond market continues to scream that there is economic pain on the horizon, and even the Fed’s own research staff anticipated a “mild recession” later this year in its latest projections. The general sense among investors is that the downturn has merely been postponed, not canceled.

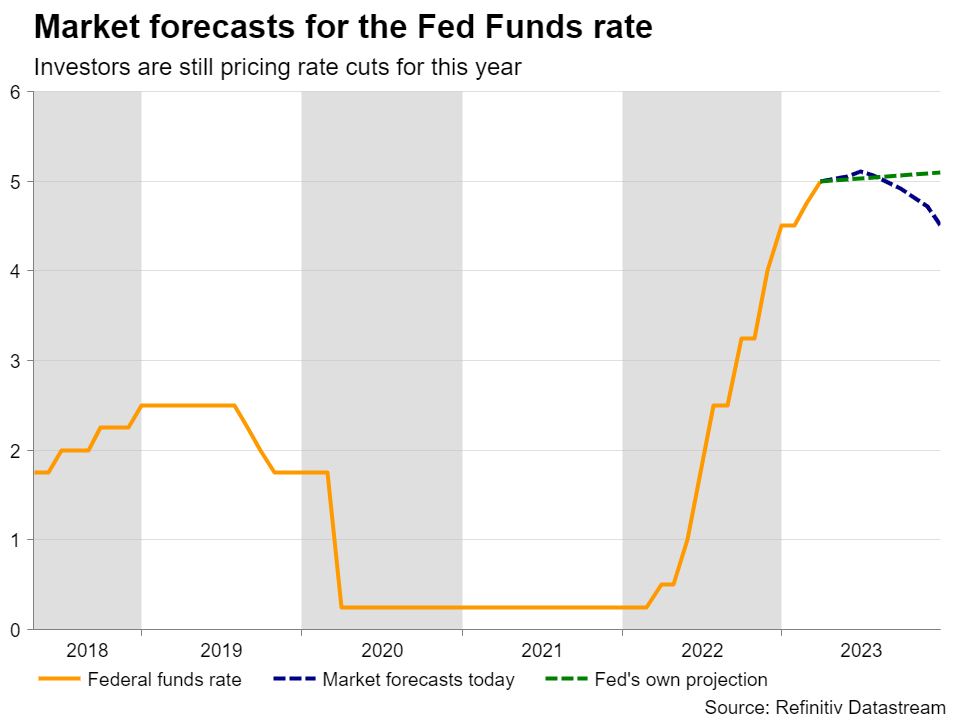

This is probably why market pricing continues to insist the Fed is about to deliver its last rate increase next week, and that rates will be slashed before the year is over. Traders currently assign a 90% probability for the Fed to raise rates by a quarter-point on Wednesday, in what is expected to be the ‘finale’ of this cycle.

Despite mounting signs that core inflation might be stickier than previously envisioned, there’s little concern in market circles about further rate increases beyond next week. And this is precisely the risk surrounding this meeting - will the Fed truly signal that its job is done or keep the door open for more action?

From a risk management perspective, it would be almost foolish to close the door for further tightening. After all, the economy is not rolling over yet and if inflation proves persistent, even higher rates might be required. Policymakers want to preserve optionality in such uncertain times, so the path of least regrets is to put emphasis on data dependence and signal that rates can still edge higher if needed.

Such a message could catch investors by surprise, since market pricing currently does not envision any higher rates. If that’s the case, or if Chairman Powell attempts to dispel speculation for rate cuts like he did at the previous meeting, the dollar could benefit.

On the data front, the ball will get rolling with the ISM manufacturing survey on Monday, ahead of the non-manufacturing index and the ADP jobs print on Wednesday that will serve as a prelude for Friday’s official employment report. Nonfarm payrolls are seen at 180k in April, which seems fair considering the mixed signals from early indicators.

Even though the S&P Global business surveys pointed to the fastest pace of job creation since last summer, applications for unemployment benefits rose during the NFP survey period, indicating a worrisome increase in worker layoffs. The data releases ahead of Friday’s employment stats - most notably the ISM surveys - will provide more color.

How hard will the ECB swing the rate-hike bat?

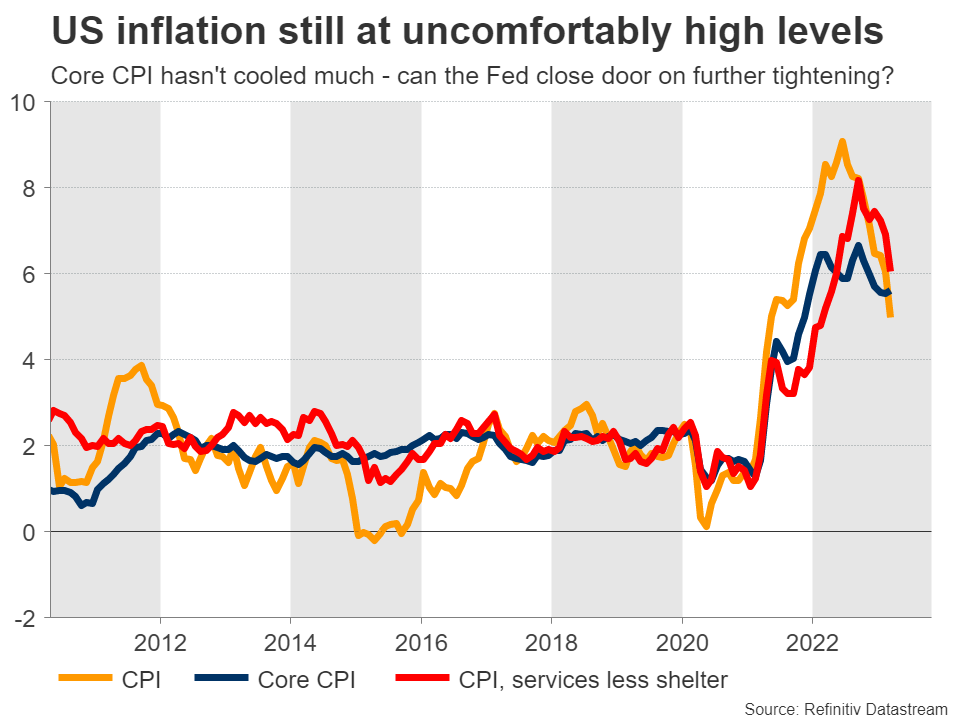

Over in euro land, most financial hubs will remain shut on Monday for the Labor Day holiday, although things will fire up on Tuesday with the latest inflation numbers for the Eurozone.

Forecasts point to a slight deceleration in inflation, something supported by the decline in oil prices but also by business surveys, which showed companies raising their prices at the slowest pace in over a year.

Still, these surveys stressed that the slowdown in price hikes was not very significant and that upward inflation momentum persists, concentrated mostly in the services sector. That’s a worrisome sign for the European Central Bank, which meets on Thursday.

Still, these surveys stressed that the slowdown in price hikes was not very significant and that upward inflation momentum persists, concentrated mostly in the services sector. That’s a worrisome sign for the European Central Bank, which meets on Thursday.

Investors are ‘certain’ there will be a rate increase but are split on the size, assigning a 70% probability for a quarter-point move and a 30% chance for a larger half-point increase. It’s a tough choice because although the economy seems to be gathering momentum and inflation continues to rage, there’s also a risk of overdoing it, since the full impact of previous rate rises hasn’t been felt yet.

A middle-of-the-road solution would be to raise rates only by a quarter-point, but accompany that with hawkish language hinting at more to come. Of course that’s already baked into the cake, as markets think the ECB will keep tightening through the summer.

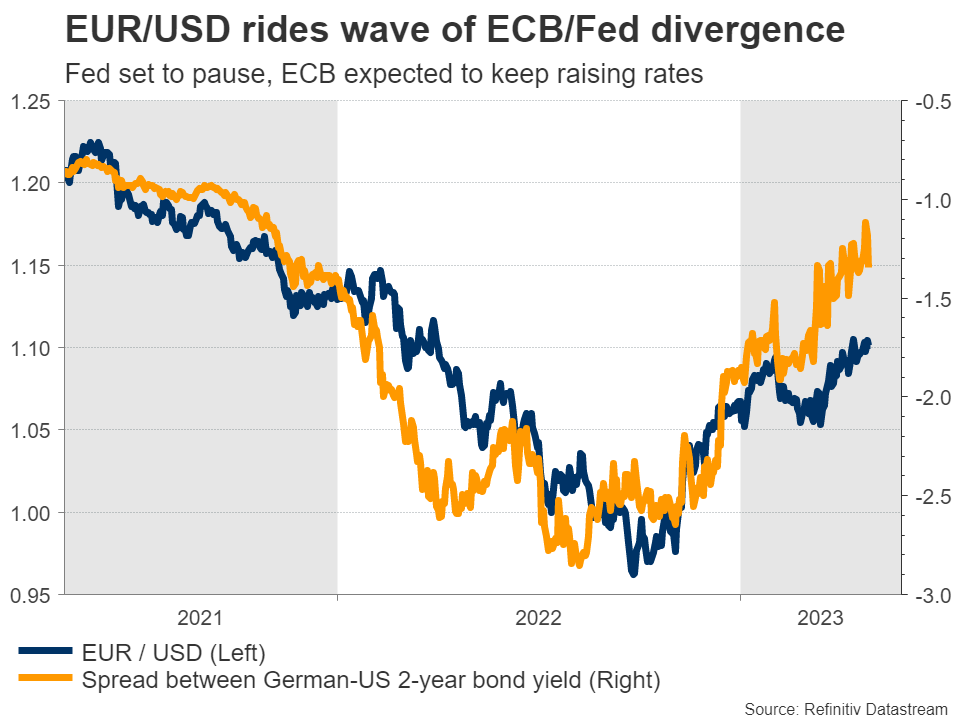

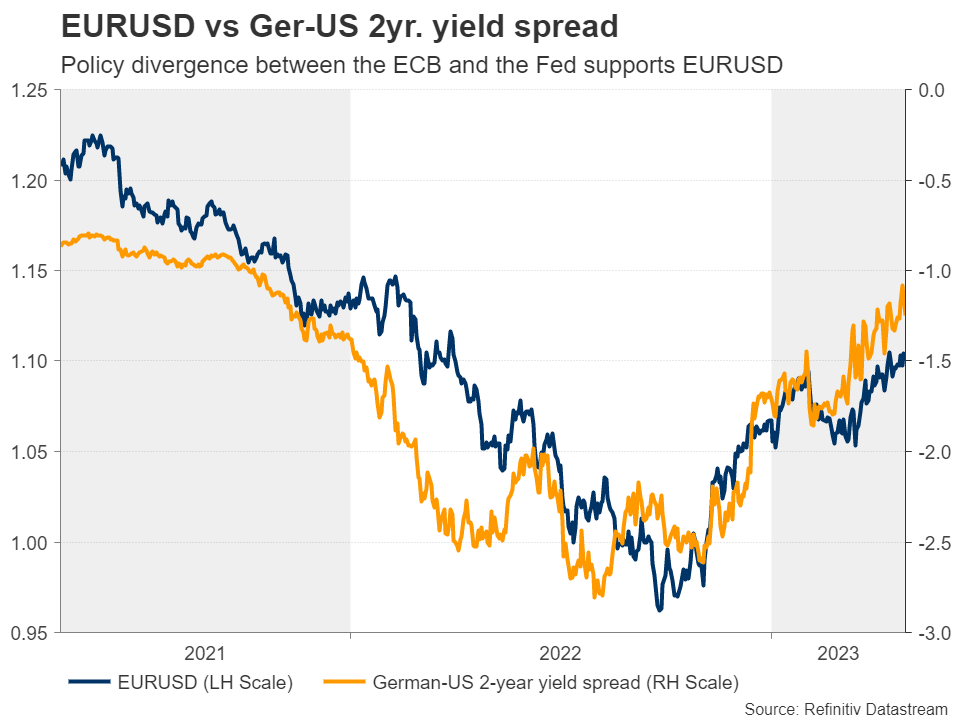

Such an outcome might be somewhat bearish for the euro, at least initially, given how markets have priced this decision. In the bigger picture, the euro seems to be riding the wave of central bank divergence with the ECB expected to race ahead of the Fed in raising rates, although a break above $1.11 in euro/dollar is needed to signal trend continuation.

RBA meets, New Zealand and Canada await data

Crossing into the realm of commodity-sensitive currencies, the Reserve Bank of Australia is expected to do nothing when it decides on Tuesday. Markets assign just a 10% chance for a rate increase.

With the RBA moving to the sidelines, the main variables of the Australian dollar moving forward might be how global risk sentiment and commodity prices evolve. The same is true for the Canadian and New Zealand dollars, as those central banks have also paused their tightening cycles or are about to.

Those economies will both see the release of employment data next week. New Zealand’s jobs report for Q1 will hit the markets Thursday, ahead of the monthly numbers from Canada on Friday.

Will the Fed Hike Rates for the Last Time?

On Wednesday, the FOMC is widely anticipated to deliver its last rate hike for this tightening cycle. However, with inflation staying well above the Committee’s target and underlying price pressures proving stickier than expected, will policymakers feel comfortable to signal that they are done? Or will they keep the door to more hikes open? And how may the dollar react?

Investors don’t listen to the Fed

At the last FOMC gathering, Fed officials delivered another 25bps hike, but due to the turbulence in the banking sector, they changed their forward guidance, with the change being interpreted as putting on the table the case of a pause as early as at the upcoming gathering, despite the new dot plot still pointing to a median rate of 5.1% for 2023. Investors also continued pricing in rate cuts later this year, although Fed Chair Powell pushed back against such a case. It was once again confirmed that investors do not put much trust in policymakers’ words and instead, they prefer to pay more attention to data.

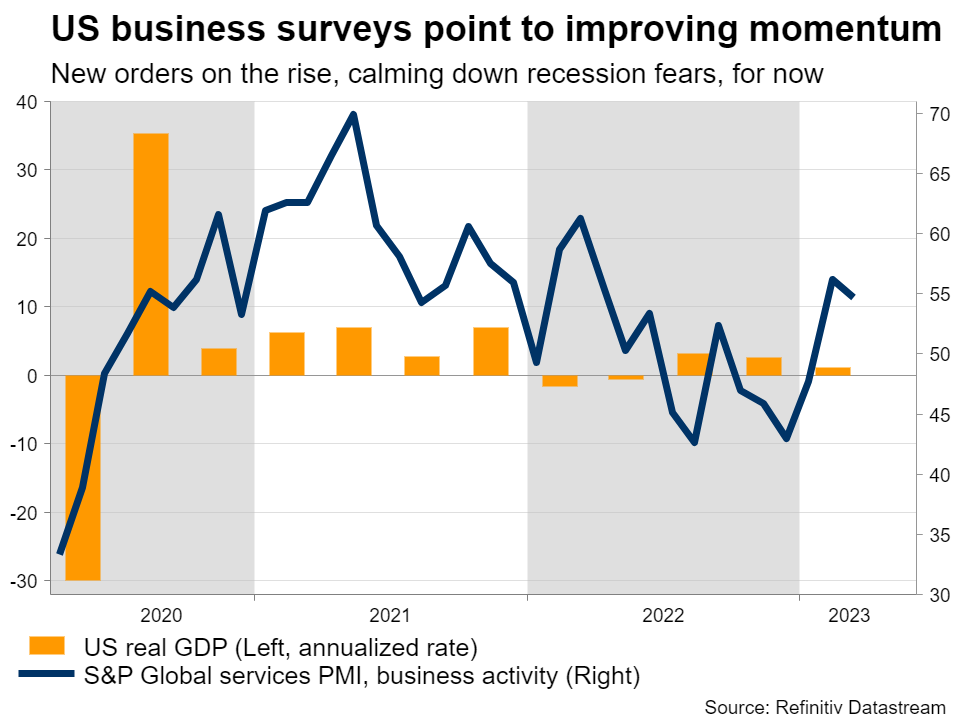

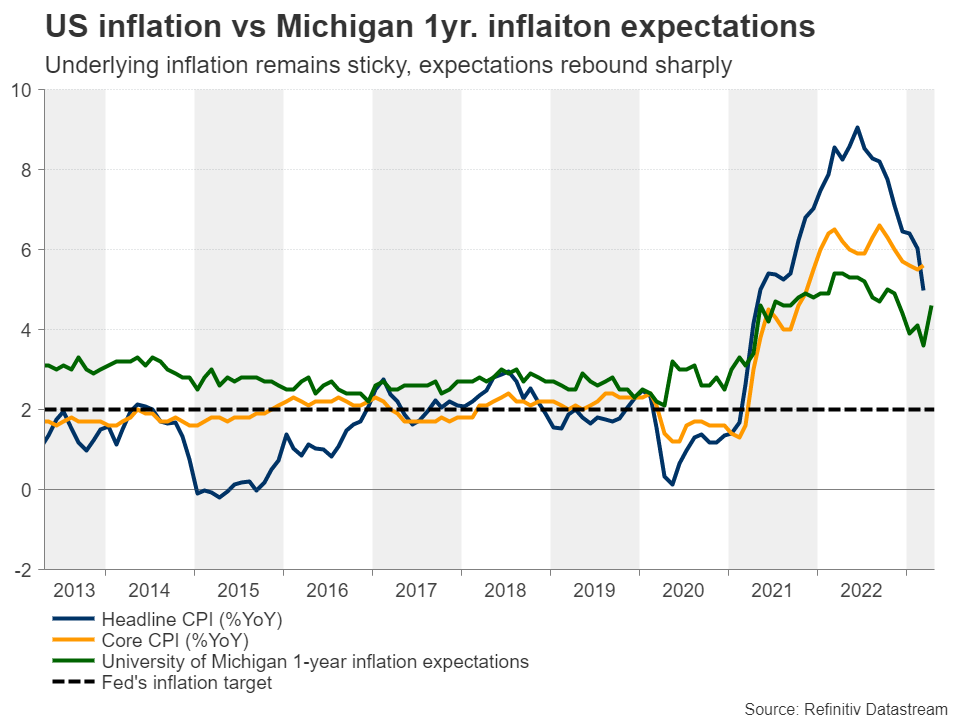

Inflation is still high

Headline inflation in the US slowed by a full percentage point to 5.0% year-over-year in March, but the core rate ticked up to 5.6% y/y from 5.5%. On top of that, business surveys for April showed that overall output prices rose at their fastest pace for seven months, while the Michigan 1-year inflation expectations index rebounded strongly in April to 4.6% y/y from 3.6%.

In terms of economic growth, Thursday’s preliminary GDP data revealed that the US economy slowed to 1.1% quarter-over-quarter in Q1 from 2.6% in the last quarter of 2022. But it was also revealed that core PCE prices accelerated by more than expected in quarterly terms.

With all that in mind, investors are now nearly certain that another quarter-point hike will be delivered on Wednesday. However, they also believe that this will be the last rate increase in this tightening crusade and that the Fed will start cutting later this year. Currently, they are pricing in more than 50bps worth of rate reductions by the end of 2023.

Will this be the last hike?

Therefore, a 25bps hike will probably come as a surprise to no one. Given that this will be one of the smaller meetings, with no updated economic projections, investors may focus on the statement’s language and Fed Chair Powell’s press conference for hints about whether this was indeed the last push of the hike button and clues on how officials are planning to move forwards.

Bearing in mind that underlying inflation remains sticky well above the Committee’s 2% objective and that inflation expectations have started to rebound, it seems a very unwise choice for Powell to dismiss the likelihood of future hikes. For that same reason, he is also very likely to push back against rate cut bets again. However, the big question is whether the market will now believe him.

Dollar could gain but reversal case remains premature

Yes, the dollar could strengthen should officials leave the door open to another hike in June. However, calling for a bullish reversal may be premature. If investors remain convinced that the Fed might be forced to start cutting rates later this year, any decision-related gains could be given back very soon, especially if the ECB continues to sing the same well known hawkish song that calls for more hikes. Dollar traders may want to see evidence that the US economy has gathered more momentum before they initiate bigger long positions.

Euro/dollar is still in an uptrend

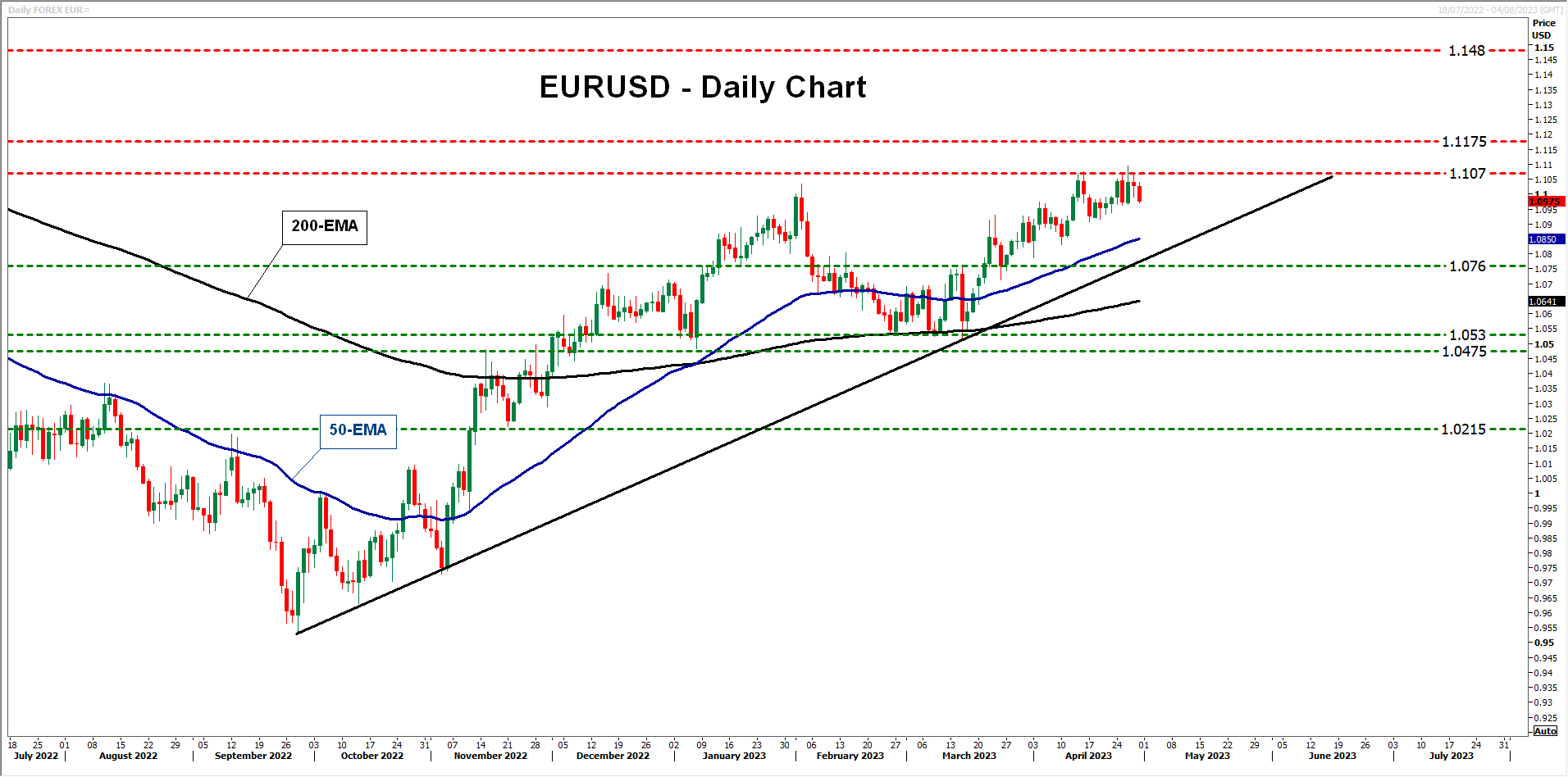

Euro/dollar has been finding it hard to clearly break above the 1.1070 resistance, which means that sellers may be willing to enter the action from near that zone should the Fed keep the chances of another quarter-point hike alive. However, the pair continues to trade above the uptrend line drawn from the low of September 28, which keeps the prevailing uptrend intact.

Any Fed-related declines could still trigger new buy orders near the trendline, with a potential rebound aiming for another test at 1.1070. If the bulls manage to overcome that barrier this time around, their next obstacle may be the 1.1175 level, marked by the highs of March 30 and 31, 2022.

For the outlook to turn bearish, a clear dip below 1.0475 may be needed. Euro/dollar would already be below the aforementioned uptrend line, while the break below that key support would confirm a lower low on bigger timeframes.

RBA Could Opt for a Stronger Aussie at Tuesday’s Rate Decision

It is the start of a new month and time for another RBA rate-setting meeting. While this is expected to be overshadowed by the week’s other key central meetings, the market remains extremely interested in the RBA’s assessment of the economic developments in the wider region. The week also includes some noteworthy data releases and the quarterly Statement of Monetary Policy. Can the aussie bulls count on the RBA for assistance to engineer an upleg in the aussie/yen pair?

RBA in the spotlight

With the market enjoying a quieter April, compared to the hyped March, the next month starts on a high note with an RBA meeting. The market is currently assigning a 70% probability for no change on Tuesday morning with the remaining 30% pointing to a 25bps rate hike. Last month’s rate decision somewhat surprised the evenly split analysts’ polls and there is a good chance of another surprise at this meeting. Based on both the April meeting statement and accompanying minutes, the RBA has kept the door open for further rate hike(s) ahead, if given sufficient evidence.

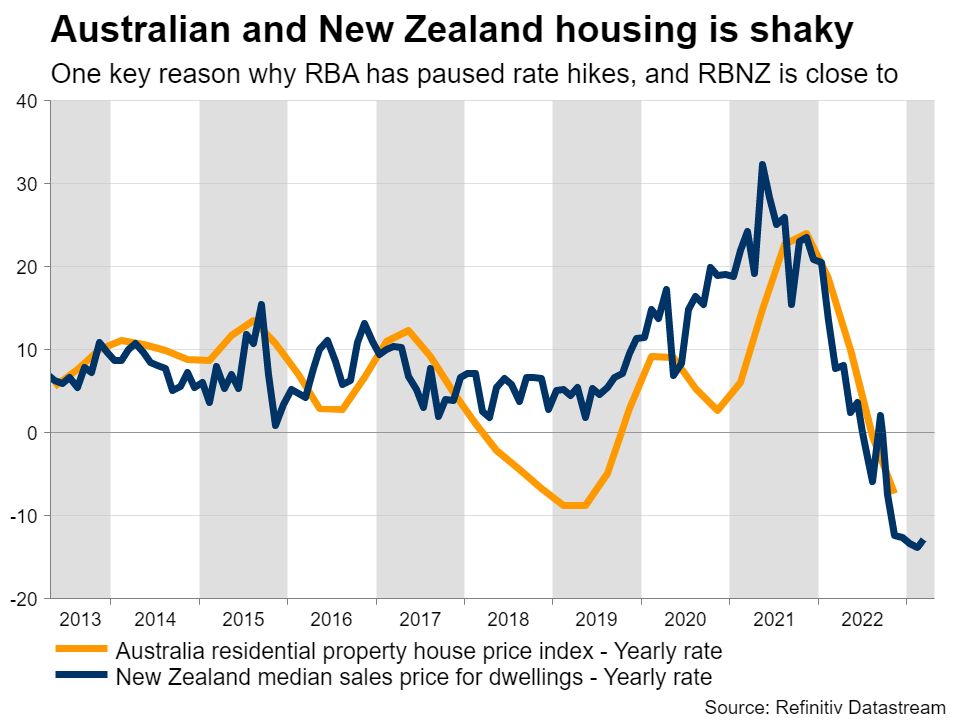

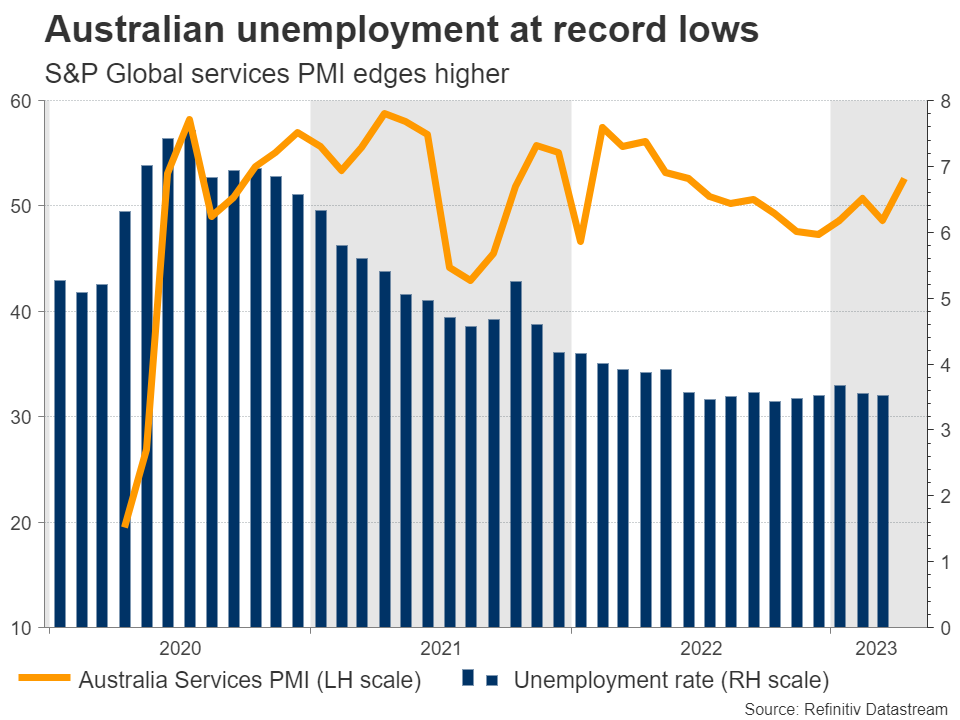

The situation on the ground remains on the positive side. The unemployment rate is at a record-low level, trade balances have edged higher again, and inflation continues its downward path from extremely elevated levels. On the other hand, business surveys and particularly the S&P Global Manufacturing PMI are flashing red, the housing sector is crying out loud for some support from the RBA and the authorities, and the recent encouraging set of data from China are clearly causing heated discussions at the RBA.

Luckily for the market, next week also brings the quarterly Statement of Monetary Policy. This will be released on Friday and will contain the usual economic forecasts. All eyes will be on the headline and trimmed mean inflation forecasts, which at the February edition of this publication, were projected at 3% on a 2-year horizon. A possible pause on Tuesday would most likely be justified by lower projections on Friday at both the inflation figures and the wage price index.

Changes coming at the RBA

It is worth nothing that there is an ongoing process of updating the remit and the structure of the RBA. There seems to be a push for modernization, closer to the standards set by the top-3 central banks. For example, the RBA looks poised to get a much-wanted post-decision press conference and just eight meetings in each calendar year. But they might try to avoid the BoE’s approach of publishing the respective rate decision, the meeting minutes, and the quarterly bulletin on the same day.

Other data in the calendar

Apart from the RBA meeting and the Statement of Monetary policy, the calendar next week is pretty full. The final prints of the S&P Global PMIs and the March trade balance are expected to shed more light on China’s impact, while a strong print at Wednesday’s retail sales could point to more durable consumer spending ahead on the back of stronger wage increases. Unsurprisingly, the RBA will probably have an early peek at this data to have a fuller understanding of the underlying economic conditions.

Aussie: possible reaction to the RBA decision

The aussie has been having a bad year against both the yen and US dollar. A rate hike announcement from the RBA on Tuesday is poised to result in some aussie outperformance, especially if the post-meeting statement points to a strong possibility of further hikes. On the other hand, no change at the cash rate would not shock the market, but the aussie would show some degree of abandonment from the RBA. Hence, the risk is asymmetric with the market reacting more forcefully in case of a surprise rate hike.

Aussie/yen at a crossroads

The rally that started in March 2020 reached its peak on September 13, 2022. Since then, aussie/yen has entered a correction phase and it is currently trading around the 50% Fibonacci retracement of the August 20, 2021 – September 13, 2022 uptrend at 88.19. The overall technical picture is rather mixed at this stage with the momentum indicators sending a message of caution.

An upside surprise on Tuesday morning could push this pair towards the 90.29-90.29 range, defined by the September 21, 2017 high and the 38.2% Fibonacci retracement respectively.

On the other hand, an unchanged RBA rate along with dovish rhetoric will probably open the door for a lower print in aussie/yen with the 61.8% Fibonacci retracement at 86.76 looking like a decent area for aussie bulls to set up their defense.