Sample Category Title

Energy Shock Cascades Through Markets: Equities Tumble, Fed Odds Shift

Panic has officially seeped into the European sessions. Crude prices are not just rising; they are re-accelerating, after Iran's Revolutionary Guard warned that any ship entering the region would face a "serious response." The death of Supreme Leader Ayatollah Khamenei on February 28 has removed the traditional diplomatic guardrails, leaving markets to fear a prolonged, high-intensity conflict.

The disruption has moved beyond the "price per barrel" to the "price of passage." Charter rates for Very Large Crude Carriers from the Middle East to China have doubled in a week, hitting an all-time high of USD 423,000 per day.

And, it isn't just the Strait. Retaliatory strikes against energy infrastructure in Saudi Arabia and the UAE have introduced a "physical destruction premium." If these disruptions persist for more than 14 days, $100 oil—a figure once thought to be a relic of the past—could become the new baseline for 2026.

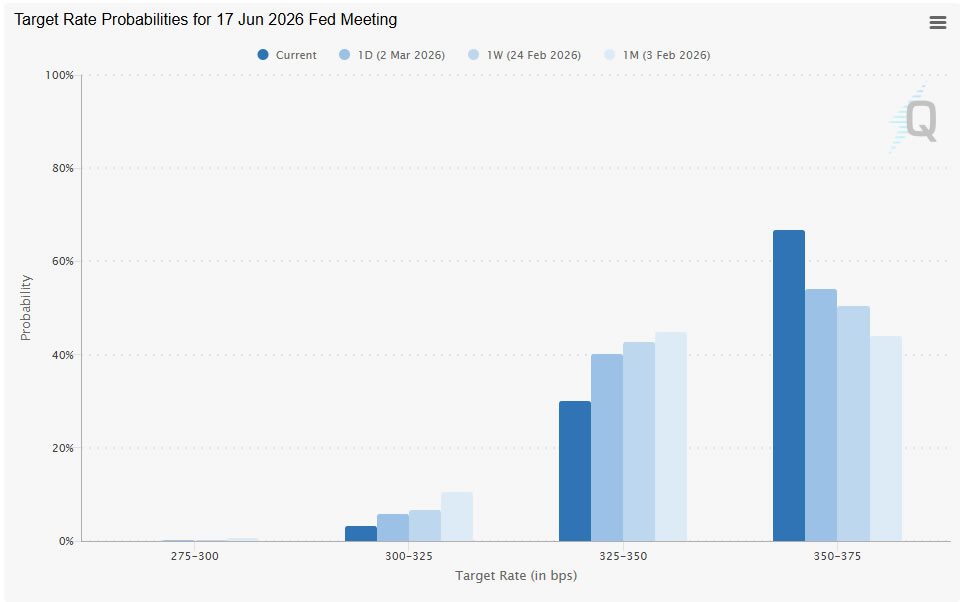

The most significant shift is occurring in interest rate expectations. The "war-induced" inflation spike has forced traders to abandon bets on a June rate cut. Fed fund futures now show a 67% probability of a hold, as central bankers cannot "look through" energy spikes that threaten to unanchor inflation expectations.

As a result, the "buy the dip" mentality that briefly appeared in the stock markets yesterday has been crushed by a sea of red. DAX (-3.3%) and DOW Futures (-700 pts) reflect a massive rotation out of risk.

In the currency markets, Dollar reigns supreme as the ultimate safe haven. Loonie follows as the second strongest, bolstered by surging oil, while Yen takes third place, following by a -3% slide in Nikkei.

Aussie and Kiwi are today's laggards. Despite hawkish comments from the RBA head—which left the door open for a March hike—domestic policy is being overwhelmed by global risk aversion. Both the Euro and Sterling are caught in the crossfire, positioning in the middle of the pack.

In Europe, at the time of writing, FTSE is down -2.60%. DAX is down -3.30%. CAC is down -2.77%. UK 10-year yield is up 0.158 at 4.469. Germany 10-year yield is up 0.083 at 2.794. Earlier in Asia, Nikkei fell -3.06%. Hong Kong HSI fell -1.12%. China Shanghai SSE fell -1.43%. Singapore Strait Times rose 0.53%. Japan 10-year JGB yield rose 0.068 to 2.133.

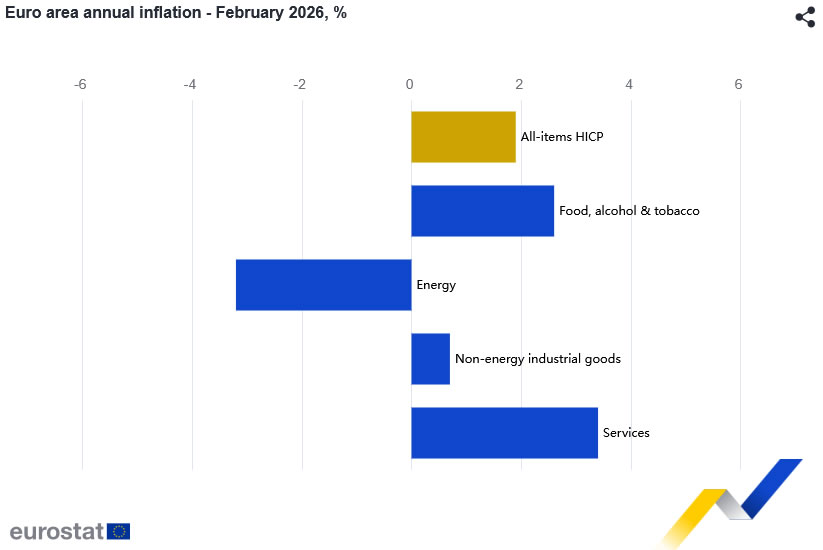

Eurozone CPI reaccelerates to 1.9% in Feb, as core and services pick up

Eurozone CPI accelerated from 1.7% year-on-year in January to 1.9% in February, exceeding expectations of 1.7%. Core CPI, which excludes energy, food, alcohol and tobacco, also firmed from 2.2% to 2.4%, above expectation of 2.2%, pointing to renewed underlying price pressures.

The composition of the increase suggests services remain primary driver. Services inflation rose to 3.4% from 3.2%, maintaining its position as the most persistent component.

Food, alcohol and tobacco held steady at 2.6%, while non-energy industrial goods picked up to 0.7% from 0.4%. Energy prices remained negative at -3.2%, though the drag eased compared to -4.0% in January.

ECB's Lane warns Middle East war could spike inflation, hit growth

ECB Chief Economist Philip Lane warned that a prolonged conflict in the Middle East could significantly raise inflation in the Eurozone while undermining economic growth.

In an interview with the Financial Times, Lane said "Directionally, a jump in energy prices puts upward pressure on inflation, especially in the near-term, and such a conflict would be negative for economic activity."

He emphasized that the ultimate impact would depend on the "breadth and duration" of the war.

Still, with current inflation running at 1.7%, below the ECB’s 2% target, a limited energy-driven uptick would not necessarily warrant immediate action. In particular, monetary policy cannot effectively counter short-term price swings as it operates with long lags.

RBA's Bullock reopens door to March hike as oil risks mount

RBA Governor Michele Bullock delivered a distinctly hawkish message at the AFR Business Summit today, warning markets not to assume a March rate hold is a done deal. She stressed that the upcoming meeting is “live,” pushing back against expectations that policy decisions are effectively pre-set or limited to quarterly moves.

Bullock highlighted that inflation remains elevated at 3.8% while unemployment at 4.1% still reflects tight labor market conditions. The Board, she said, will be “actively looking” at whether it needs to "move more quickly", explicitly discouraging the view that the RBA only adjusts rates at predictable intervals.

Central to her remarks was the risk of a prolonged oil price spike stemming from escalating Middle East tensions. While she emphasized that it is too early to quantify the impact, Bullock warned that a supply-driven shock could add to inflation pressures and, critically, influence inflation expectations — a development the RBA is “very alert to.”

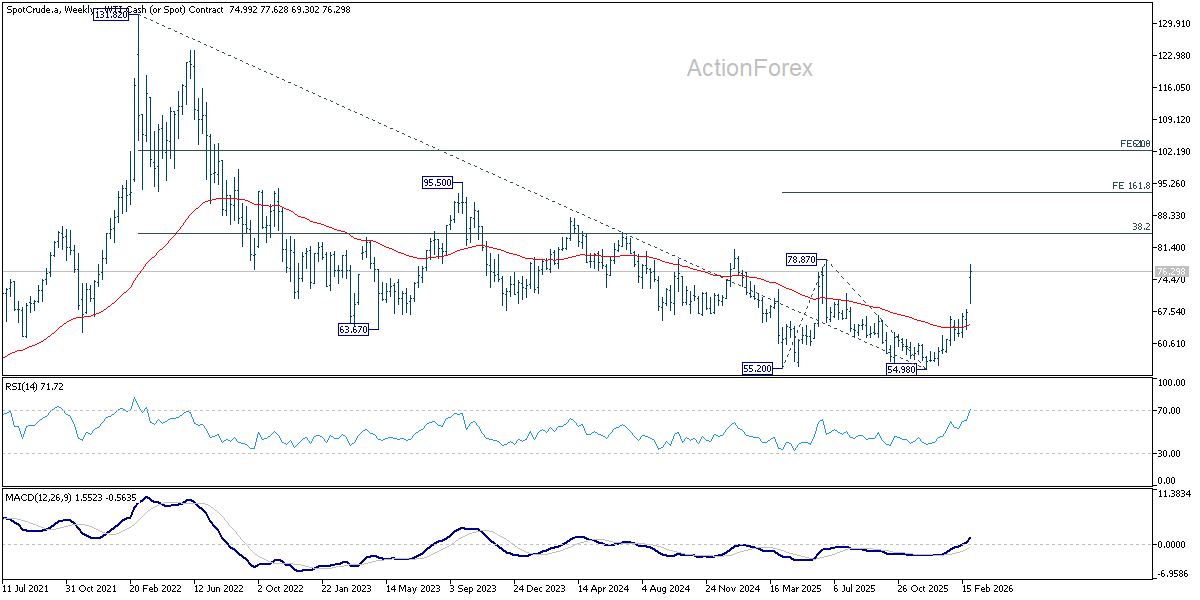

WTI oil eyes key resistance at 79 as energy markets seized by panic

Oil prices surged again today, breaking through yesterday’s spike with aggressive upward acceleration. Markets are entering a state of panic following explicit threats from Iranian officials to "set fire" to any vessel attempting to navigate the Strait of Hormuz.

Ebrahim Jabbari, an adviser to the commander-in-chief of Iran’s Islamic Revolutionary Guard Corps (IRGC), told state TV: "Ships should not come to this region. They will certainly face a serious response from us."

The Strait of Hormuz is a vital artery for the global economy, carrying approximately 20% of the world’s oil and gas. This flow has effectively ceased following a series of kinetic attacks on tankers over the last 72 hours.

Beyond the surge in raw commodity prices, the conflict has sent shipping overheads into uncharted territory. The cost of hiring a supertanker to move oil from the Middle East to China hit an all-time high on Monday, exceeding $400,000 (£298,300) per day. According to data from the London Stock Exchange Group, this represents a near-doubling of costs in just seven days.

Technically, WTI is now eyeing a key structural resistance level at 78.87. Decisive break there would confirm that the multi-year down trend from 131.82 (2022 high) has completed at 54.98. This supported by the double bottom reversal pattern (55.20, 54.98). In this case, WTI could extend current rise to 38.2% retracement of 131.82 to 54.98 at 84.33 next. In any case, near term outlook will remain bullish as long as 70.15 support holds.

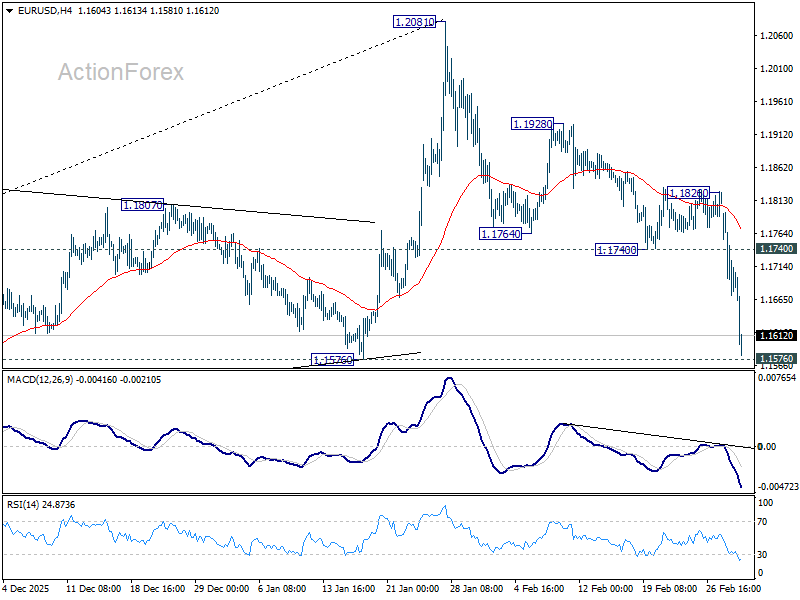

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1641; (P) 1.1719; (R1) 1.1765; More….

Intraday bias in EUR/USD remains on the downside, and immediate focus is now on 1.1576 structural support. Firm break there would confirm rejection by 1.2 key psychological level. That should also confirm medium term topping on bearish divergence condition in D MACD. Further decline should be seen to 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. For now, risk will stay on the downside as long as 1.1740 support turned resistance holds, in case of recovery.

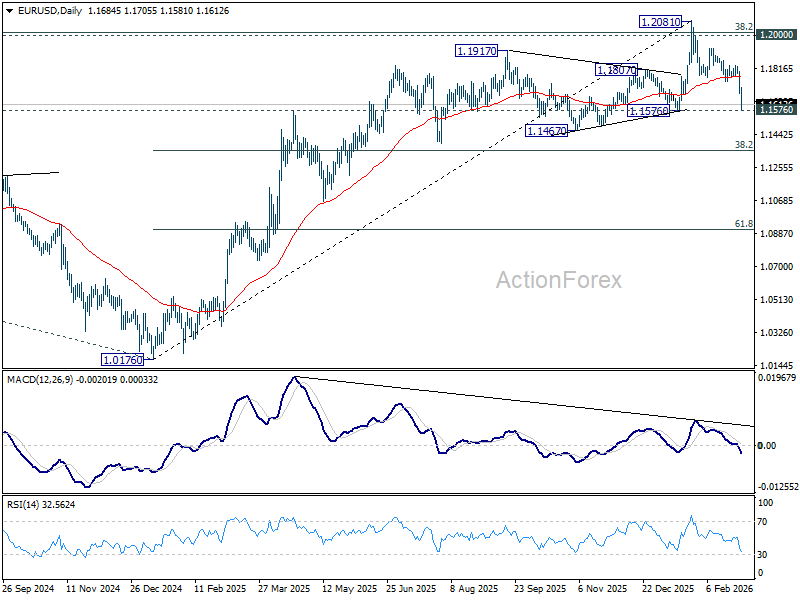

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

WTI oil eyes key resistance at 79 as energy markets seized by panic

Oil prices surged again today, breaking through yesterday’s spike with aggressive upward acceleration. Markets are entering a state of panic following explicit threats from Iranian officials to "set fire" to any vessel attempting to navigate the Strait of Hormuz.

Ebrahim Jabbari, an adviser to the commander-in-chief of Iran’s Islamic Revolutionary Guard Corps (IRGC), told state TV: "Ships should not come to this region. They will certainly face a serious response from us."

The Strait of Hormuz is a vital artery for the global economy, carrying approximately 20% of the world’s oil and gas. This flow has effectively ceased following a series of kinetic attacks on tankers over the last 72 hours.

Beyond the surge in raw commodity prices, the conflict has sent shipping overheads into uncharted territory. The cost of hiring a supertanker to move oil from the Middle East to China hit an all-time high on Monday, exceeding $400,000 (£298,300) per day. According to data from the London Stock Exchange Group, this represents a near-doubling of costs in just seven days.

Technically, WTI is now eyeing a key structural resistance level at 78.87. Decisive break there would confirm that the multi-year down trend from 131.82 (2022 high) has completed at 54.98. This supported by the double bottom reversal pattern (55.20, 54.98). In this case, WTI could extend current rise to 38.2% retracement of 131.82 to 54.98 at 84.33 next. In any case, near term outlook will remain bullish as long as 70.15 support holds.

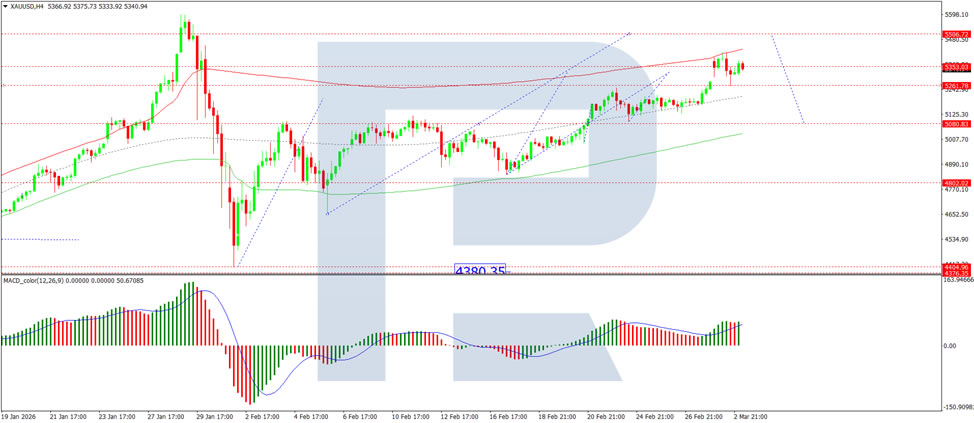

Gold Rallies for Fifth Day, With External Risks Mounting

Gold rose to 5,350 USD per ounce on Tuesday, marking its fifth consecutive session of gains. Demand for safe-haven assets continues to grow amid the escalating conflict in the Middle East.

President Donald Trump stated that the United States will continue its strikes on Iran until the country loses its ability to pose a threat. According to him, the conflict could last a month or "much longer." In response, Iran has announced the closure of the Strait of Hormuz and threatened attacks on ships passing through this strategically vital energy corridor.

The worsening conflict has triggered a sharp rise in oil prices and intensified fears of accelerating US inflation. This has led to selling in US government bonds and a reassessment of expectations for further Federal Reserve rate cuts.

The market is now shifting its forecast for the next Fed rate cut to September, later than previously anticipated.

Technical Analysis

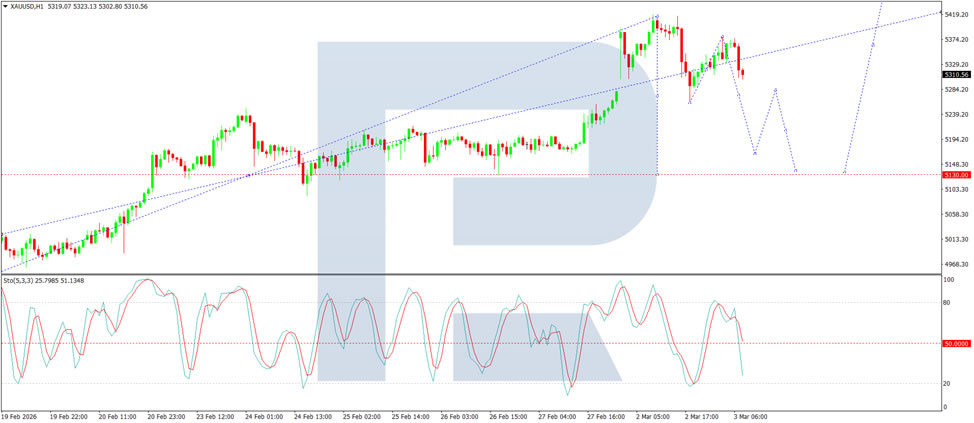

On the H4 XAU/USD chart, the market is forming a consolidation range around the 5,353 USD level. A downside breakout would open the way for a continuation of the correction towards 5,130 USD. Conversely, an upside breakout would open up potential for a wave towards the 5,599 USD level. The MACD indicator confirms the current momentum, with its signal line at highs and pointing strictly upwards.

On the H1 chart, the market has broken below the 5,333 USD level, suggesting a continuation of the trend towards 5,166 USD, with the potential for the wave to extend further to 5,130 USD. The stochastic oscillator supports this scenario, with its signal line remaining above the 80 level and under pressure to turn lower towards the 20 level.

Conclusion

Gold's rally to record highs reflects escalating demand for safe-haven assets amid intensifying geopolitical risks in the Middle East. The conflict has not only boosted bullion but also lifted oil prices and stoked concerns about inflation, prompting markets to push back expectations for Fed rate cuts. While the short-term technical outlook remains bullish, traders are watching for potential corrections following such a strong upward move.

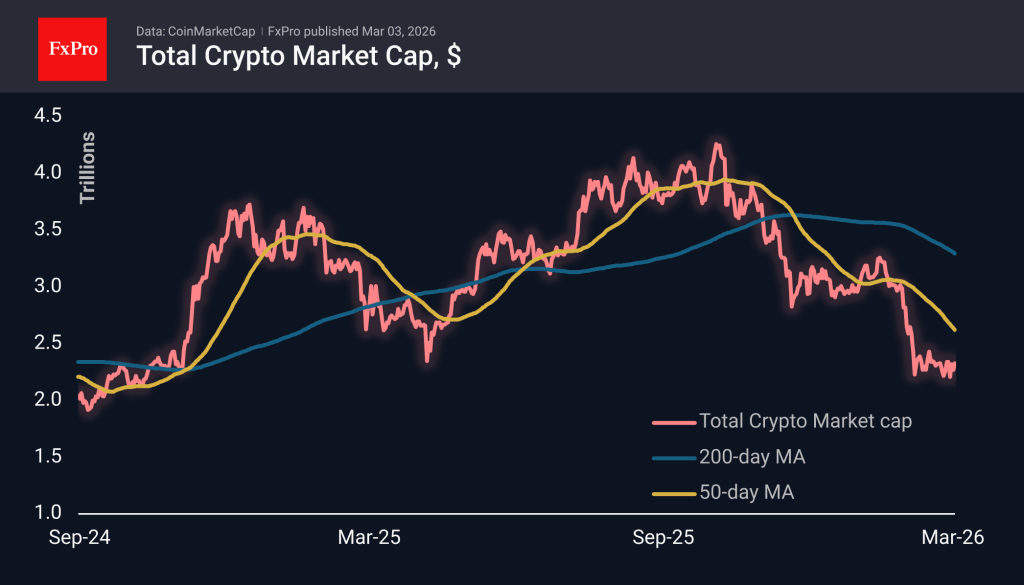

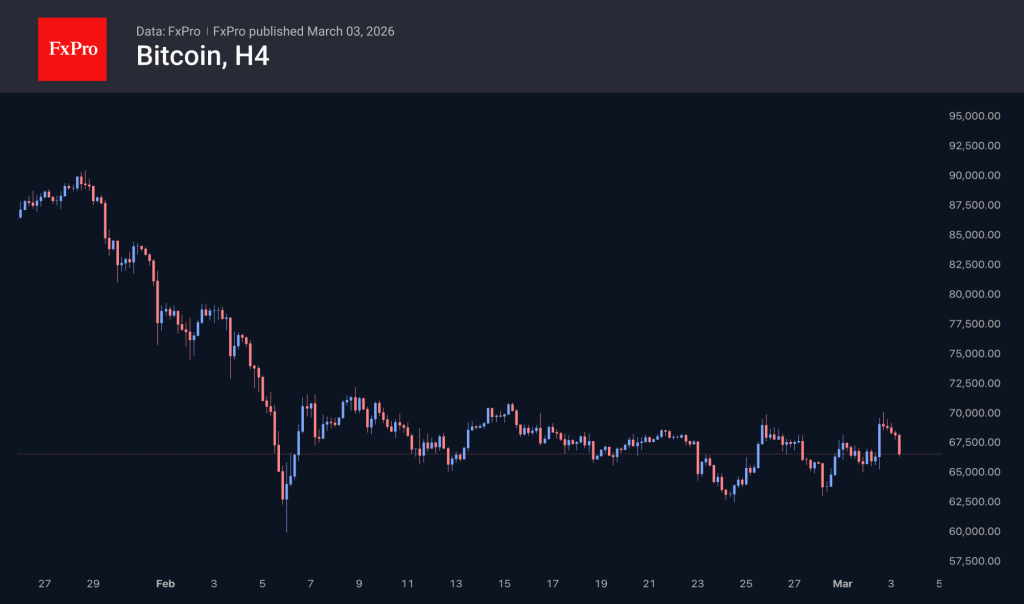

Crypto Market Failed to Break Out of Range

Market Overview

The crypto market cap grew by 2.6% to $2.33 trillion. The market remains stuck in a narrow range, moving from the lower boundary on Saturday to the upper boundary at the start of the day on Tuesday. At times like this, attention turns to whether there will be an upward breakout and a reversal of the February pattern. On the sellers’ side, the pull towards the dollar is a strong headwind for USD-denominated quotes. On the other hand, this is a chance for Bitcoin and major cryptocurrencies to play their role as a safe haven, providing shelter from the storm.

Bitcoin rose to $70K, but Tuesday morning’s decline brought its price back to $67K, indicating significant resistance from sellers on the upside. The first cryptocurrency failed to break out of horizontal consolidation, which again forces us to consider a decline to $63K as a working scenario.

News Background

The positive market sentiment on Monday was a combination of a low base after the previous price decline, a breakout of key technical levels and a resumption of accumulation by large investors, CoinShares notes. At the same time, both Ethereum and Bitcoin have seen net outflows since the beginning of the year.

Bitcoin is undervalued compared to ‘overheated’ gold and global money supply, which could contribute to a possible upward reversal for BTC, according to JAN3 CEO Samson Mow.

Ethereum co-founder Vitalik Buterin presented a plan for two key changes to the network’s execution level: the transition to a binary state tree and the long-term replacement of EVM.

Strategy bought 3,015 BTC ($204.1 million) last week at an average price of $67,700 per coin. Strategy now owns 720,737 BTC, purchased for $54.8 billion at an average price of $75,985 per bitcoin.

BitMine acquired 50,928 ETH over the past week. The company’s reserves have reached 4.47 million ETH, which is 3.71% of Ethereum’s market supply. BitMine plans to accumulate 5% of all Ether.

Natural Gas Prices Rise Amid Middle East Conflict

The recent strike by Israel and the US, along with Iran’s retaliatory actions, has pushed energy asset prices higher. Yesterday, we reported on a bullish gap in oil markets, and while US natural gas prices have not surged as sharply, they are also on the rise. Traders’ attention is focused on news from the Strait of Hormuz, through which around 20% of global liquefied gas shipments pass.

Today’s XNG/USD chart reflects the increase in natural gas prices – driven by concerns over potential disruptions to supply chains.

Technical Analysis of XNG/USD

The long-term descending channel, repeatedly referenced in previous analyses, remains relevant – its median acted as resistance on 6 February.

A notable event occurred on 9 February, when a bearish gap formed on the XNG/USD chart (around the 3.200 level). This area acted as resistance on 12 February.

From a bullish perspective:

- → The market finds support near the 2025 low, likely an economically justified support level close to production costs.

- → The reversal on 26 February resembles a Rounding Bottom pattern.

Currently, US natural gas prices are trading near 1.133, where local February highs formed. However, if escalation in the Middle East continues, XNG/USD may rise toward the noted resistance around 3.200.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Eurozone CPI reaccelerates to 1.9% in Feb, as core and services pick up

Eurozone CPI accelerated from 1.7% year-on-year in January to 1.9% in February, exceeding expectations of 1.7%. Core CPI, which excludes energy, food, alcohol and tobacco, also firmed from 2.2% to 2.4%, above expectation of 2.2%, pointing to renewed underlying price pressures.

The composition of the increase suggests services remain primary driver. Services inflation rose to 3.4% from 3.2%, maintaining its position as the most persistent component.

Food, alcohol and tobacco held steady at 2.6%, while non-energy industrial goods picked up to 0.7% from 0.4%. Energy prices remained negative at -3.2%, though the drag eased compared to -4.0% in January.

Dollar Index (DXY) Climbs to a One-and-a-Half-Month High

Today, the US Dollar Index rose above the 98.70 level for the first time since the third week of January. Monday’s trading opened with a bullish gap, and upward momentum continues to build as news emerges of a major escalation in the Middle East:

- → Demand for safe-haven assets: Historically, the US dollar and US Treasury bonds have served as primary refuges for capital during periods of heightened uncertainty.

- → Military activity around the Strait of Hormuz is pushing oil prices higher (WTI jumped by approximately 10% yesterday) along with gas prices. This creates a direct pathway to another wave of global inflation.

Technical Analysis of the DXY Chart

Six days ago, when analysing the US Dollar Index (DXY) chart, we:

- → Reaffirmed the validity of the descending channel (marked in red), which originated in November 2025.

- → Once again highlighted the strength of demand, reflected in the confident upward trajectory (shown by the arrow) following the false break below the multi-month low of 96.50 at the end of January.

- → Suggested that bulls could regain momentum and break the prevailing downtrend.

Indeed, price action in early March confirms this view: the descending channel is losing relevance, being replaced by an upward trajectory marked in blue. In this context, developments in the Middle East are of critical importance:

- → If tensions begin to ease, the DXY may stabilise around the median line of the blue ascending channel.

- → A renewed escalation and the collapse of potential negotiations could trigger a further advance towards the upper boundary of the blue channel.

It is also worth noting that the area around the 98 level may now serve as support:

- → This zone previously saw rapid price appreciation, signalling strong buying pressure.

- → It was also the point of a bullish breakout from the red channel and above the 97.98 resistance level.

Trade global index CFDs with zero commission and tight spreads (additional fees may apply). Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Distorted Gas Supply is European Economy’s Achilles’ Heel

Markets

It still are the same central banks, but with a different reaction function. A low inflation environment enabled them to conduct demand-stimulating policies from the great financial crisis up until the Covid-19 pandemic to counter any significant (potential) hit to growth. This weekend’s developments, but a decade ago, would have triggered the “transitory” energy-related inflation spike narrative with the focus directed on facilitating growth. Today’s different inflation context (>2%) and lessons learnt from the energy crisis some four years ago implies that central bankers will be vigilant to the inflation rather than the growth side of the story. Markets are clearly aware of that as seen in yesterday’s repositioning. When it comes to Europe, money markets again clearly err on the side of a rate hike as the next move. When it comes to the US (or the UK for that matter), they question the timing of the next rate cut (opting for delay) and the policy room left towards neutral. Daily changes on the US yield curve ranged between +6.8 bps (30-yr) and +10.9 bps (5-yr) with the 2-yr and 10-yr yield moving back above 3.4% and 4% respectively. Apart from the energy-narrative, US Treasuries lost additional ground after the release of the February manufacturing ISM. The ISM printed above the neutral 50-mark for a second consecutive month (52.4 from 52.6). The previous time that happened was in the fall of 2022. The index sported strong details with new order growth, a rising backlog, decent production volumes and slowed job shedding. Tariffs and metal prices (steel and aluminum) did propel the prices paid subindex to its highest level since June 2022 (70.5) and add to the Fed near term rate stability case. The German yield curve bear flattened with yields rising by 4.3 bps (30-yr) to 9 bps (2-yr). Distorted gas supply is the European economy’s Achilles’ heel after being cut off from Russian supplies. The largest LNG production site in Qatar was shut down yesterday following Iranian drone attack. They added to upward pressure on gas prices (Dutch TTF €44.5/Mwh from €32) coming from higher oil prices (Brent $80/b with Strait of Hormuz closed). The huge energy-dependence helps explaining underperformance of European assets in general. Main equity benchmarks lost up to 2.5% yesterday whereas the US managed to hold a status quo. EUR/USD lost first support at 1.1742 with the YtD low at 1.1573 being the next reference. Elsewhere, the Swiss National Bank had to officially step up verbal intervention threats after EUR/CHF was heading towards 0.90 for the first time ever (apart from 2015 volatility). Yesterday’s market dynamics remain in play today with US President Trump warning that “the big wave” is yet to come while continuous Iranian drone attacks spread chaos across the Middle East. Today’s eco calendar contains the February EMU CPI print. Our inhouse KBC Nowcast model points to 1.8% Y/Y inflation, suggesting upside risks to the 1.7% Y/Y consensus estimate. We expect energy prices to rise by 0.8% M/M to be down 2.5% Y/Y. The Iran conflict makes it likely that headline HICP will return to around 2% as early as March which might add to yesterday’s repositioning vibes when it comes to both the direction and (to a lesser extent) the timing of the ECB’s next move. A slightly stronger monthly impulse than in January should keep services inflation at 3.2 and core inflation at 2.2%.

News & Views

In a speech at a business meeting in Sydney, Governor Michell Bullock of the Reserve Bank of Australia (RBA) warned that the March 17 Policy meeting is a live meeting as the RBA board will “be actively looking whether or not it needs to move more quickly”. The comments come as monthly January inflation at 3.8% Y/Y surprised on the higher side of expectations and stays well above the 2-3% RBA target zone. At the same time, labour market data remained solid with the unemployment rate easing to 4.1%. Governor Bullock explicitly questioned the market assumption that the RBA will mostly likely wait for quarterly inflation data to adjust policy. The RBA last month raised its policy rate by 0.25% to 3.85% as inflation remains elevated, the labour market tight and as the economy meets capacity pressures. Tomorrow’s Q4 GDP figures (0.8% Q/Q expected) will give additional info. The 2-y Australian government bond yield jumps 14 bps to 4.3%. The market implied probability of a March rate hike rises from 15% to 30%. The Aussie dollar holds up well against a broadly strong dollar (AUD/USD 0.71).

February UK shop price inflation in February eased to 1.1% against a 1.5% rise in January. Even so, this increase is still in line with the 3-month moving average. Non-food prices fell 0.1% Y/Y, against growth of 0.3% in January. Food inflation increased 3.5%Y/Y in February, against growth of 3.9% in January. The British Retail Consortium comments that fierce competition between retailers is keeping price rises in check as do promotions. Falling global food costs also fed through, pushing food inflation down, with ambient food inflation dropping to its lowest level in four years. While promising, the BRC assess that prices are still rising and that many consumers remain under pressure. It also mentions the risk that government measures might “add further complexity if secondary legislation is implemented without an eye firmly on the potential consequences for the cost of doing business and hence the cost of living”.

ECB’s Lane warns Middle East war could spike inflation, hit growth

ECB Chief Economist Philip Lane warned that a prolonged conflict in the Middle East could significantly raise inflation in the Eurozone while undermining economic growth.

In an interview with the Financial Times, Lane said "Directionally, a jump in energy prices puts upward pressure on inflation, especially in the near-term, and such a conflict would be negative for economic activity."

He emphasized that the ultimate impact would depend on the "breadth and duration" of the war.

Still, with current inflation running at 1.7%, below the ECB’s 2% target, a limited energy-driven uptick would not necessarily warrant immediate action. In particular, monetary policy cannot effectively counter short-term price swings as it operates with long lags.

EURJPY Elliott Wave: Corrective Pullback Confirms Bullish Trend

The short-term Elliott Wave structure in EURJPY continues to indicate a bullish trend. Examination of the 45‑minute chart reveals that the pullback from the wave ((iii)) high unfolded in three distinct waves. This formation suggests a corrective nature rather than the beginning of a larger reversal. Thereby, it supports the expectations of further upside momentum. The rally from the February 13 low is proposed to develop as a five‑wave impulse.

From the February 13 low, wave ((i)) concluded at 182.27, followed by a retracement in wave ((ii)) that ended at 180.80. The pair then advanced in wave ((iii)), which itself unfolded as an impulse of a lesser degree. Within this sequence, wave (i) terminated at 183.15, while the corrective wave (ii) ended at 181.98. Subsequent strength carried wave (iii) to 184.18, before a modest dip in wave (iv) concluded at 183.19. The final leg, wave (v), reached 184.77, thereby completing the larger wave ((iii)) structure.

Attention then shifted to wave ((iv)), which is now proposed to have completed at 183.78 in the form of a triangle. This pattern reinforces the view that the correction was contained and orderly. In the near term, as long as the pivotal low at 180.84 remains intact, the expectation is for EURJPY to extend higher.

EURJPY 45-Minute Elliott Wave Chart

EURJPY Elliott Wave Video:

https://www.youtube.com/watch?v=tmjPs9Qr70s