Sample Category Title

GBP/USD Slides Further as Bears Tighten Grip on Market

Key Highlights

- GBP/USD started a fresh decline and traded below 1.3400.

- A key bearish trend line is forming with resistance at 1.3485 on the 4-hour chart.

- EUR/USD extended losses and dived below 1.1620.

- Crude Oil prices rallied above $76.00 before trimming some gains.

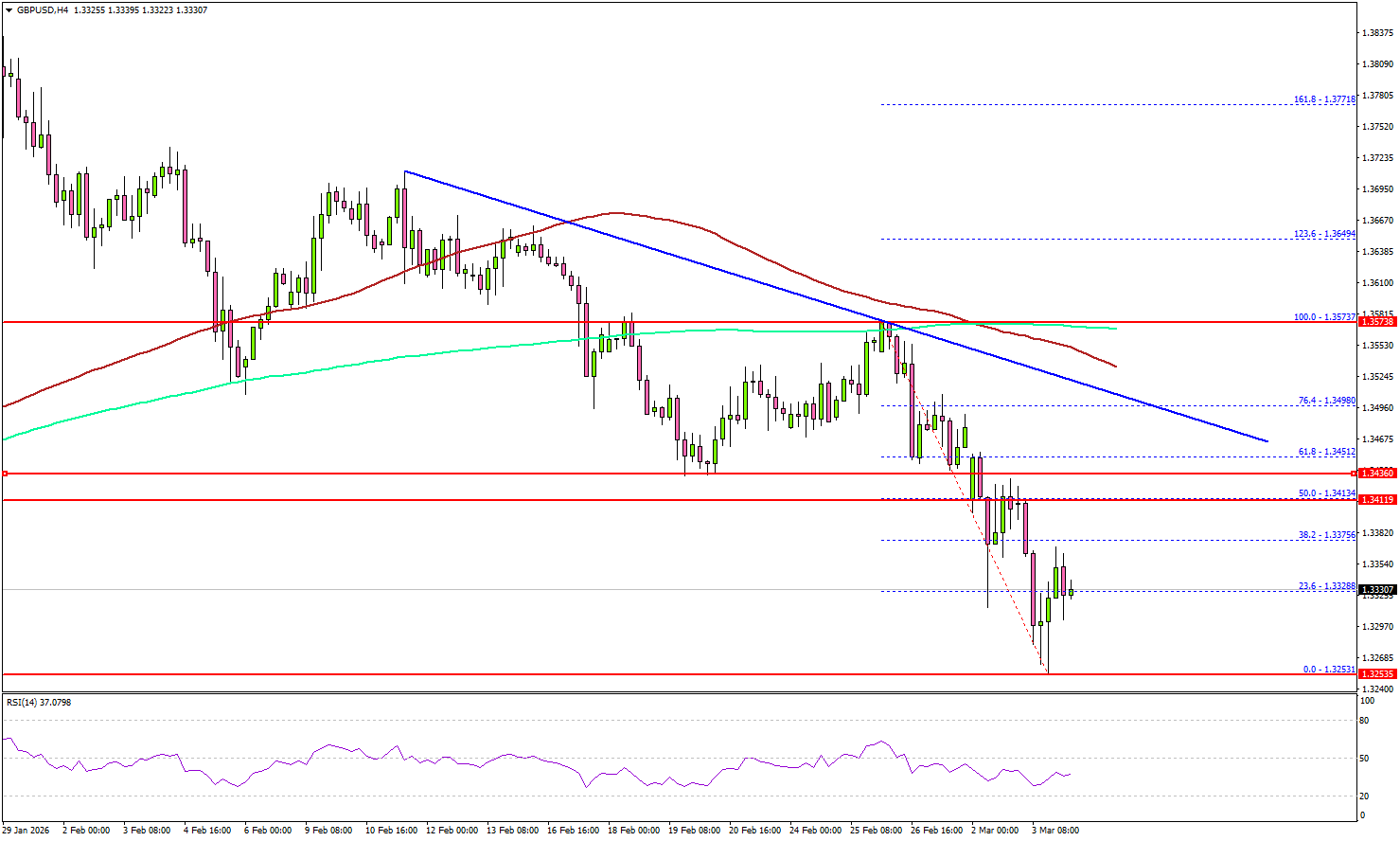

GBP/USD Technical Analysis

The British Pound failed to stay above 1.3500 and declined against the US Dollar. GBP/USD traded below the 1.3450 and 1.3420 levels to enter a bearish zone.

Looking at the 4-hour chart, the pair settled below 1.3400, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). A low was formed at 1.3253, and the pair is now consolidating losses.

There was a minor upward move above the 23.6% Fib retracement level of the downward move from the 1.3573 swing high to the 1.3253 low. On the upside, the pair is now facing sellers near 1.3375.

The first major resistance sits at 1.3410 or the 50% Fib retracement level of the downward move from the 1.3573 swing high to the 1.3253 low. A close above 1.3410 could open the doors for more gains. In the stated case, the bulls could aim for a move to 1.3450.

The main resistance sits near 1.3500. There is also a key bearish trend line forming with resistance at 1.3485. Immediate support could be 1.3265. The first major area for the bulls might be near 1.3250.

The main support sits at 1.3220, below which the pair might gain bearish momentum. In the stated case, it could even revisit 1.3000 in the coming days.

Looking at EUR/USD, the pair started a fresh decline below 1.1620, and there are chances of more losses in the near term.

Upcoming Key Economic Events:

- UK Services PMI for Feb 2026 – Forecast 53.9, versus 53.9 previous.

- US ISM Services Index for Feb 2026 – Forecast 53.5, versus 53.8 previous.

Gold falls as Fed repricing trumps war premium, second leg consolidation finished

Gold weakened sharply overnight as markets moved past the initial geopolitical shock of the widening Middle East conflict and began repricing the Federal Reserve outlook. The early safe-haven surge faded as investors reassessed the broader implications of the conflict, particularly the inflationary impact of surging oil prices.

The threat to the Strait of Hormuz has driven crude prices higher, but the implications for Gold are more complex than a simple risk-off rally. While geopolitical tensions typically support bullion, the resulting spike in energy costs also raises the prospect that global inflation could remain elevated for longer than previously expected.

Higher oil prices act as a direct challenge to the Fed’s disinflation narrative. Energy costs effectively operate as a tax on economic activity while simultaneously pushing headline inflation higher. As a result, traders have begun pushing back expectations for the next Fed rate cut from June or July toward September.

That shift implies a longer period of policy restraint as the Fed waits to assess how persistent the energy shock may prove. If inflation expectations begin to rise again, policymakers are likely to remain cautious, preferring to keep rates higher for longer until the second-round effects of oil prices become clearer.

In that environment, Gold faces increasing competition from Dollar. During periods of stress, investors often prioritize liquidity, and the greenback tends to benefit more directly from global risk aversion. With Dollar Index moving back toward the 100 level, Gold is facing renewed pressure from its inverse correlation with the currency.

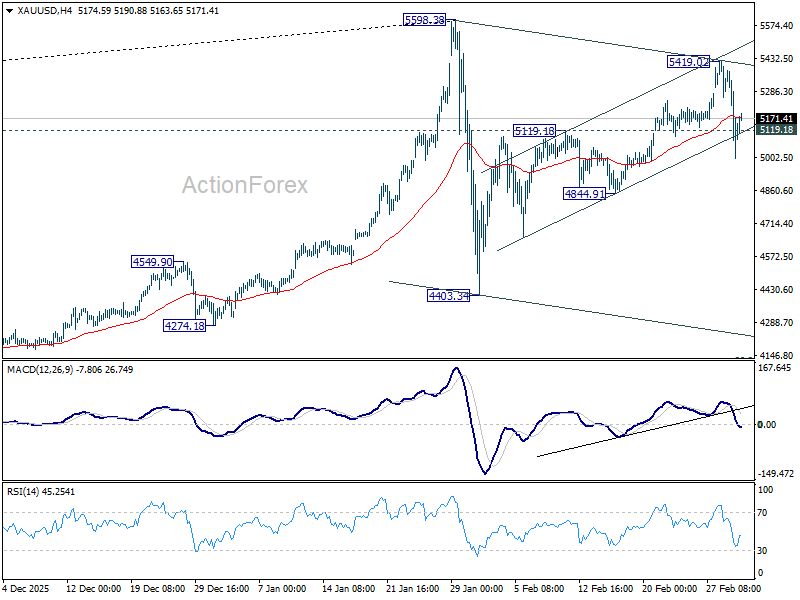

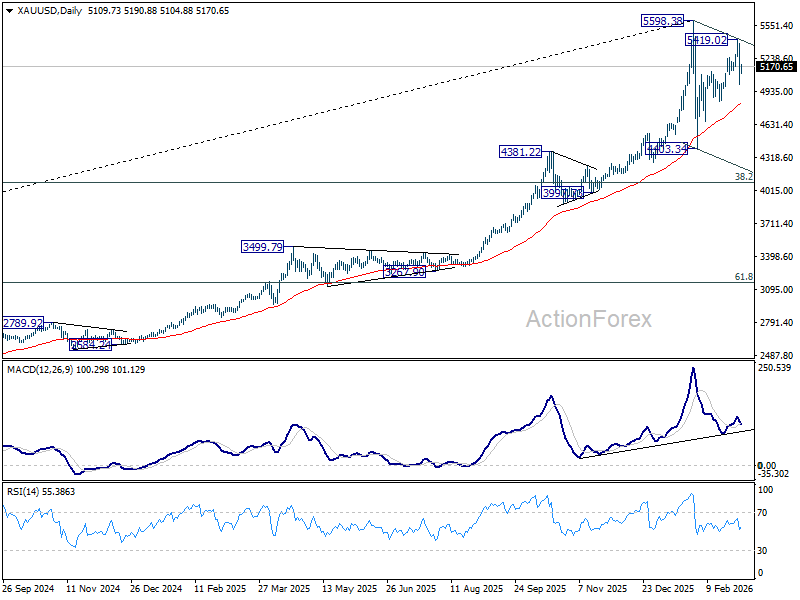

Technically, however, the current development remains consistent with our view. Price actions from 5598.38 record high are seen as a corrective pattern, with the first leg completed at 4403.34.

The current break of 5119.18 resistance turned support argues that the second leg from 4403.34 might have already completed at 5419.02 already. Risk will stay on the downside for 4844.91 support first. Firm break there should solidify this case and bring deeper decline back towards 4403.34.

However, break of 5419.02 will extend the rise with 4403.34 with on more upleg, and possibly with a retest of 5598.38 before completion.

China PMIs show two-speed economy as official data contracts

China’s February PMI data revealed a widening divide between official indicators and private surveys, highlighting the uneven nature of the country’s economic transition.

The official manufacturing PMI, released by the National Bureau of Statistics of China, slipped to 49.0 from January’s 49.3, missing expectations and marking a second consecutive month of contraction. Activity in services and construction also stayed weak, with the non-manufacturing PMI edging slightly up from 49.4 to 49.5.

However, private-sector surveys paint a starkly different picture. According to data compiled by RatingDog, manufacturing PMI surged from 50.3 to 52.1, its strongest level since December 2020. The services PMI jumped even more sharply, rising to 56.7, the highest reading in nearly three years.

This divergence suggests a “dual-track” economy emerging in China. State-dominated sectors tied to construction and traditional heavy industry appear to be cooling, while private, export-oriented firms are experiencing a resurgence in demand, particularly in higher-value manufacturing and technology-linked industries.

Part of the discrepancy may also reflect seasonal distortions around the Lunar New Year. Large state factories often shut down for extended periods during the holiday, while smaller and more flexible private firms tend to ramp up production quickly to capture early-year export orders.

The February data may therefore capture both the growing pains of China’s structural shift toward “new productive forces” and the short-term disruptions created by the holiday cycle.

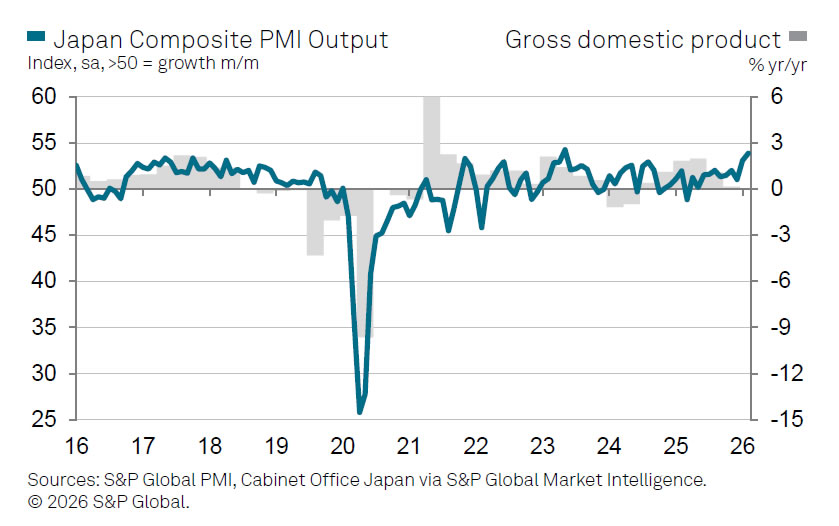

Japan PMI composite finalized at 53.9, firms pass rising costs to customers

Japan’s service sector maintained steady momentum in February, with the final PMI Services reading edging up to 53.8 from January’s 53.7. The figure marks the strongest level since May 2024 and signals continued expansion in business activity, supported by improving demand conditions.

The broader picture for the economy also strengthened. PMI Composite rose to 53.9 from 53.1, pointing to the fastest pace of private sector expansion in nearly three years.

According to Annabel Fiddes of S&P Global Market Intelligence, the services sector recorded its quickest rise in sales in almost two years, while manufacturing performance also remained robust.

At the same time, cost pressures intensified across the private sector. Input costs climbed at a historically sharp pace, but improving demand allowed businesses to pass those increases on to customers. Selling prices rose at the fastest rate in nearly twelve years, suggesting firms are regaining pricing power while inflationary pressures remain elevated.

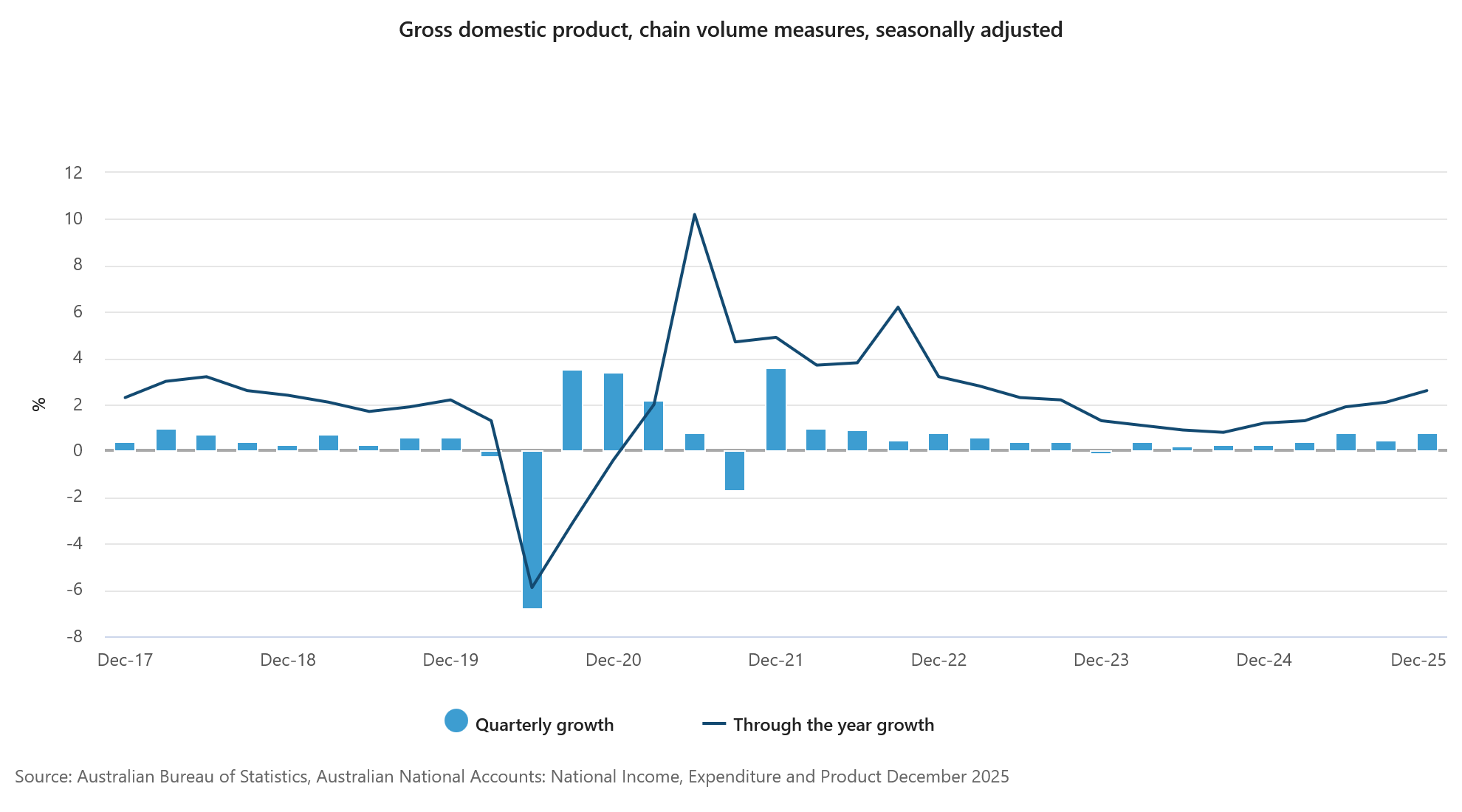

Australia Q4 GDP beats with 0.8% qoq growth, reinforcing RBA demand concerns

Australia’s economy expanded faster than expected in the fourth quarter, reinforcing concerns that domestic demand may still be running hotter than the RBA would like. GDP grew 0.8% qoq, beating forecasts of 0.7% and accelerating from the previous quarter’s 0.5% pace. On an annual basis, growth came in at 2.6% yoy, also above expectations of 2.2%.

The expansion was broad-based, with output rising in 17 of the economy’s 19 industries. Both public and private demand contributed equally to the result, each adding 0.3 percentage points to overall growth. Household activity also showed resilience, with discretionary spending increasing 0.4% during the quarter, helped by strong retail events such as Black Friday.

At the same time, households continued to rebuild financial buffers. The saving ratio climbed to 6.9%, the highest level in more than three years, while per capita GDP rose 0.9% yoy — its strongest reading since 2022.

The strength of the data places the RBA in a difficult position. Just a day earlier, Governor Michele Bullock warned that demand may be outpacing the economy’s capacity. The GDP figures appear to reinforce that view, suggesting the current 3.85% cash rate may not yet be restrictive enough to cool activity.

Fed’s Kashkari reconsiders rate-cut outlook after Middle East escalation

Minneapolis Fed President Neel Kashkari said the escalating conflict in the Middle East has significantly clouded the policy outlook, undermining earlier confidence that easing inflation would pave the way for rate cuts. Kashkari noted that he had entered 2026 expecting that cooling price pressures might justify a single reduction in interest rates.

However, the joint U.S.-Israel attack on Iran has introduced a potential new global shock. Policymakers and markets alike must now determine how severe the disruption might become and whether it will resemble a prolonged geopolitical conflict like Russia’s invasion of Ukraine or a more contained escalation.

Kashkari stressed that the key risk lies in inflation expectations. If headline inflation remains elevated for an extended period following years of already strong price growth, the Fed may need to remain cautious. In such a scenario, policymakers would have to carefully assess the persistence of inflation before moving toward any easing of monetary policy.

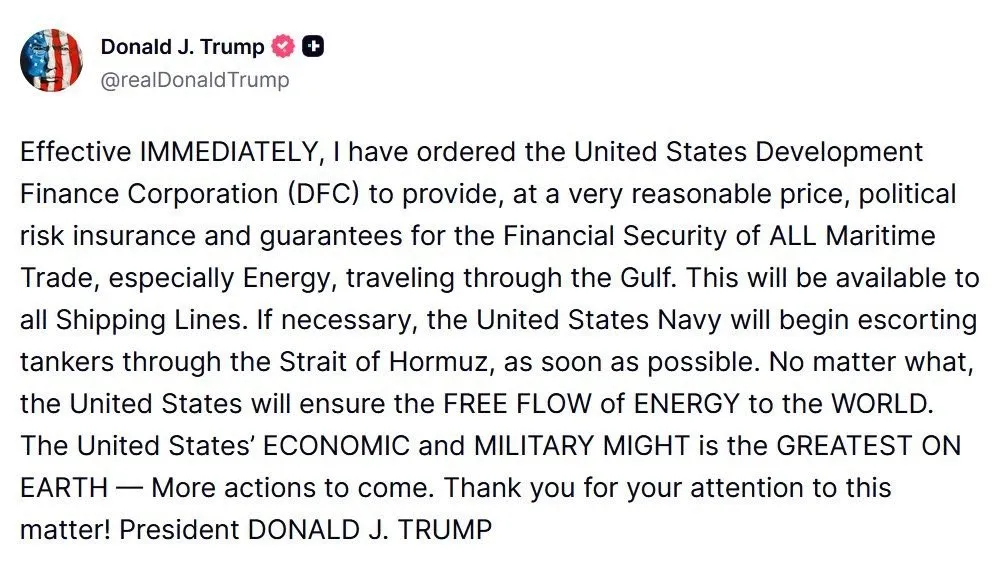

Trump Guarantees Maritime Security in the Strait of Hormuz: Markets U-Turn on Navy Escort Pledge

Markets just took a massive U-turn following a critical address from President Trump.

The US President delivered a lengthy morning speech from the White House, providing further details on the ongoing military operations in Iran.

The core message centered on preemptive defense, with the President stating he "felt strongly that Iran was going to attack first," justifying the administration's recent escalations to secure American interests in the region – He noted a significant progress in operations, which initially stalled the Petrodollar panic move in Markets.

However, what truly helped markets shed their persistent morning anxiety was an early afternoon post from the President on Truth Social.

Trump's Market Moving Truth Social Post

Trump announced a pledge to establish a major security framework to protect commercial shipping routes across the Arabian Sea, with a specific focus on the highly vulnerable Strait of Hormuz.

The immediate reaction in the commodities space was swift.

Oil prices violently retreated by nearly 7% shortly after the announcement before mean-reverting higher.

With WTI currently hovering right around Monday's gap-up levels, broader market sentiment is still looking significantly smoother than it was at the opening bell.

The technical and fundamental picture looks vastly different now compared to the early hours of the session. Let's break down exactly what changed.

Financial Markets are getting rocked from the latest developments, but reactions have remained relatively contained.

Energy Markets

Oil has been subject to aggressive movement in today's session particularly.

After initially exploding back to its June 2025 highs in a move that left other assets in the dust, crude eased its progress throughout the North American morning session.

What followed however was a significant sweep lower.

WTI (US) Oil CFD 30M Chart, March 3, 2026 – Source: TradingView

Knowing that Oil and Strait of Hormuz dynamics were the main contributors to Market panic, it isn't surprising to see such movement and easing in Sentiment.

Metals however remain much lower, as Market security leads to further profit-taking in the safe-havens

Metals Markets

Metal Futures Daily Performance, March 3, 2026 – Courtesy of Finviz

Gold and Silver both eased significantly in today's session. They attempted a move higher but this hasn't materialized yet.

US Dollar

The US Dollar also eased quite significantly after the comments – It relates overall to an over-extended move, which actually did retrace all the way to the 99.00 as forecasted in our morning Dollar Index analysis!

Dollar Index (DXY) 4H Chart, March 3, 2026 – Source: TradingView

It wouldn't be surprising to see a Dollar rebound around here – However, it seems that momentum towards the end-afternoon is heavily slowing.

Tomorrow's session should bring further clarity there.

US Stock Markets rebound significantly

The better sentiment was demarcated particularly well in US Stock Benchmarks which saw a fresh buying wave in the final hour.

They have been very unpredictable – But that's the way Markets are in these types of environments.

Dow Jones CFD 30M Chart, March 3, 2026 – Source: TradingView

The rally in the Dow has been nothing short of impressive.

Nasdaq and S&P 500 both saw similar rises – However, US Indexes are now back to their relative resistance levels – The DJIA is actually testing the highs of its downward channel!

Extending higher from there would imply a better risk-sentiment ahead. Failing to do would provide a sweet spot for profit-taking.

Safe Trades and keep track of the evolution of the conflict ahead!

Middle East Conflict: An Initial View for Australia and New Zealand

Using Oxford Economics’ global model, we assess the potential implications for growth and inflation of three different scenarios for the conflict.

The US–Israel attack on Iran over the weekend and Iranian response has disrupted shipping in the Persian Gulf and spiked oil prices. The broader economic impact is highly uncertain, depending on how long the hostilities last and whether there is lasting damage to transport infrastructure. Using the Oxford Economics model, we trace through three different scenarios for their impacts on Australia and New Zealand. These are model results only, and do not represent a forecast of either the conflict or central bank reactions.

What is the extent of the conflict?

Over the past three days, the US and Israel have struck an array of military and infrastructure targets across Iran. Iran’s Supreme Leader Ayatollah Ali Khamenei was killed along with many other senior leaders. Iran retaliated against US military assets in the region, Israel and other infrastructure assets across the region, including Dubai’s airport. President Trump has stated that combat operations will “continue until all of our objectives are achieved”, without elaborating beyond an initial projection of “four to five weeks”. Comments from Israeli Prime Minister Benjamin Netanyahu also alluded to military strikes increasing in intensity in “coming days”.

How has regional trade been affected?

As of 3rd March, the all-important Strait of Hormuz is officially closed to oil, LNG and container trade. A few ships have reportedly been hit, and existing insurance policies have been revoked. Even if this proves short-lived, high insurance costs could stymie any quick resumption in transit. Bloomberg reports DP World has also suspended work at their Jebel Ali port in Dubai.

The conflict has also shut all air traffic across the region, affecting global passenger travel and freight until further notice, including between Europe and Australia / New Zealand.

How have financial markets reacted?

Yesterday, the price of Brent oil opened almost 14% higher at US$82.37. It has remained volatile since but currently trades just below US$78.00 (7% higher than Friday’s close). This is on top of the rise through January and February that occurred in anticipation of conflict. Spot Brent is 32% higher in US dollars than it was in mid-December.

The Australian and New Zealand dollars are little changed overall, down 0.2% and 0.9% since Friday’s close. Equity markets are cautious. Most, including Australia’s ASX 200 have seen little net change, awaiting a better sense of the duration and scale of the conflict. Though Europe’s exposure to energy supplies from the region saw a marked decline in the Continent’s bourses overnight.

How might oil prices respond?

If, as was the case in mid-2025, military conflict is short, the price of oil is likely to retreat quickly and physical trade return to normal. The hit to global trade, inflation and financial markets would be negligible.

However, if the conflict intensifies in coming days and/or persists for weeks, financial market participants are likely to become more anxious. Under these circumstances, Brent oil around US$100 is possible, with consequences for both global growth and inflation. Equities and pro-risk currencies would also come under significant pressure.

Iran produces around 4 million barrels per day (mb/d) of crude and other liquids, roughly 4% of global oil production, with China the largest import market – a manageable supply shock at the global level. The Strait of Hormuz, however, is the main route for 20mb/d of oil supply and circa 30% of global container shipping.

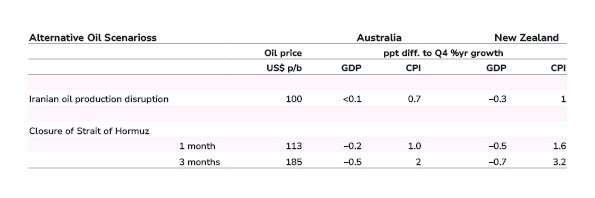

There is significant uncertainty over the potential for disruption, but as a guide we consider three illustrative scenarios using Oxford Economics’ global model.

- A disruption to Iranian production only could see the price of oil rise another US$25 per barrel to around US$100. However, inventory draws, a potential release of strategic reserves and/or an increase in supply from other producers would likely ease concerns and see the price of oil retreat quickly. The implications for LNG, container and air trade would also be transitory.

- If shipping through the Strait of Hormuz is affected for up to a month, Brent could instead spike to US$113 per barrel.

- A disruption of three or more months could see the price of Brent oil rise to US$185 per barrel.

The longer and more intense the disruption, the greater the real economy cost and hit to sentiment. Oil and LNG inventories held by both the private and public sector are also finite, and workarounds for supply are limited. Note, these scenarios also assume no damage to oil and LNG production and freight facilities. A permanent loss of supply would prolong the cost to the real economy and financial markets via the price of oil and related energy products.

In addition, we would also likely see lasting supply disruptions across an array of goods globally given the complex nature of global trade and manufacturing. As for oil, the longer the disruption the greater the cost. Arguably, Europe would be most affected given their exposure, but ramifications would be seen across the globe.

How might higher oil prices affect the Australian and New Zealand economies?

Higher oil prices feed rapidly into headline CPI via petrol and transport costs, and indirectly via energy-intensive products such as fertilisers. Under the three scenarios petrol prices could increase by A$0.25 to A$1.00 per litre, dependent on movements in the Australian dollar and refinery margins.

Higher inflation reduces real household disposable income, weighing on consumption, while higher input costs weaken investment. External demand also softens as global growth slows, weighing on exports, with reduced imports providing only a partial offset.

The net impact is consistently larger in New Zealand because there are no offsetting export income effects. LNG and coal prices also rise, partially insulating Australian incomes via higher export revenue, and dampening any exchange rate depreciation. However, it does not fully neutralise the drag from higher fuel costs.

How might Australia and NZ GDP growth and inflation be affected?

If only Iranian oil supply is impacted, the Australian CPI rises by around 0.7ppts (see table), while the near-term impact on real GDP is marginal – GDP growth at Q4 2026 is less than 0.1ppt lower.

If supply from the Strait of Hormuz is disrupted for one month, the Australian CPI lifts by around 1ppt, with GDP growth around 0.2ppt lower. A three-month disruption could see the CPI temporarily spike by around 1.5ppts at the peak, with GDP 0.5ppts lower by end-2026.

In New Zealand, the same shock transmits more forcefully as higher oil prices represent a negative terms-of‑trade and income shock. Under the Iranian supply scenario, the CPI rises by around 1ppt and GDP is circa 0.4ppts lower. With more severe disruptions, the divergence widens. A one‑month Strait of Hormuz closure raises CPI by around 1.6ppts and lowers GDP by around 0.5ppts. A three‑month disruption lifts the CPI by around 3ppts and lowers GDP by around 0.7ppts, reflecting a larger and more persistent squeeze on real household incomes.

How will the RBA and RBNZ interpret the oil price shock?

These three oil supply scenarios represent temporary supply shocks. The price level increases, not ongoing inflation. Typically, central banks look through such shocks, but in these scenarios, the RBA and RBNZ would have to balance the risk that inflation expectations lift against the medium-term effects on activity. They will also be watching for signs of pass-through of higher costs into inflation more broadly.

The conflict in Iran and related impact on oil prices adds to the risks that inflation remains higher for longer. In Australia, Trimmed Mean was already expected to remain above the RBA’s 2–3% inflation target range for a few quarters; an extended conflict would lengthen that period. Similarly, inflation would be expected to remain in the upper part the RBNZ’s target band for an extended period.

What if oil prices spike to US$100 per barrel or US$150 per barrel and remain there?

The policy risks increase if higher oil prices persist and begin to generate secondary inflationary pressures through wages and other goods and services. The Oxford Economics model represents these risks by modelling central bank actions based on a simple (Taylor) reaction rule.

If oil prices were to increase to US$100 per barrel, around US$25 above current levels and stay there, model estimates suggest it could tilt the balance of risks to the RBNZ raising rates by a further 25bps in 2027, relative to 125bp in our baseline, with rates around 25bps higher over the forecast period. For Australia, where the inflation passthrough is comparatively smaller, the balance of risks would be for rates to settle around 25bps higher over the longer term.

Under a US$150 per barrel scenario, monetary policy could diverge. Central banks could look through the first-round inflation effects given the expected negative spillovers to activity as long as inflation expectations remain anchored. However, in New Zealand persistently higher inflation, combined with a low starting point for interest rates, could lead the RBNZ to raise rates by a further 50bps in 2027, to contain ongoing core inflationary pressures. In contrast, in Australia, where interest rates are already restrictive, the drag from higher inflation on household spending and activity may allow the RBA to remain on hold with a hawkish bias.

Note: The Oxford Economics Global Economic Model is an integrated forecasting and scenario model covering 87 key economies, including Australia and New Zealand, and regional blocs. A global commodity block based on country demand and supply allows scenario analysis for price or demand and supply shocks with feedback channels back to demand, prices, monetary policy and other financial asset prices.

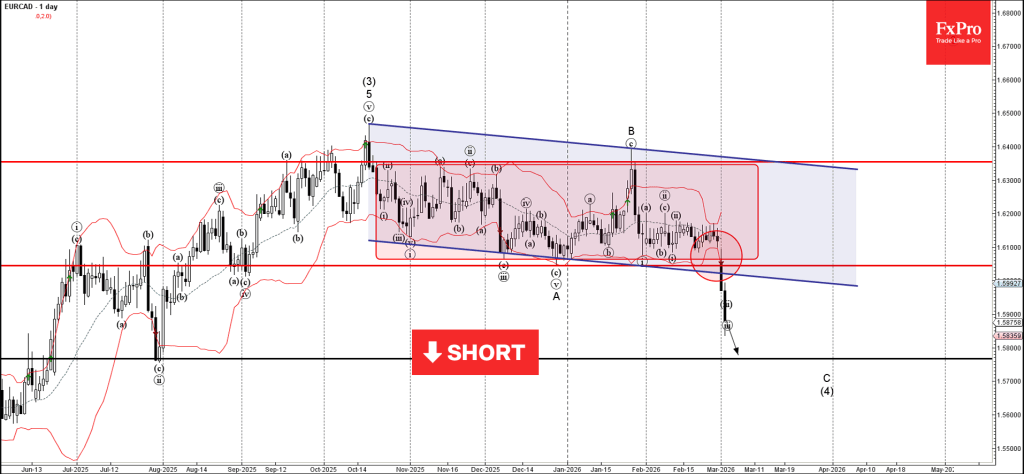

EURCAD Wave Analysis

EURCAD: ⬇️ Sell

- EURCAD broke support zone

- Likely to fall to support level 1.5765

EURCAD currency pair recently broke the support zone between the support level 1.6045 (which has been reversing the price from August) and the support trendline of the daily down channel from October and the lower boundary of the sideways price range from October at 1.6055.

The breakout of these support levels accelerated the active impulse waves C and iii.

Given the bearish Euro sentiment seen today, EURCAD currency pair can be expected to fall to the next support level 1.5765 (former support from July).

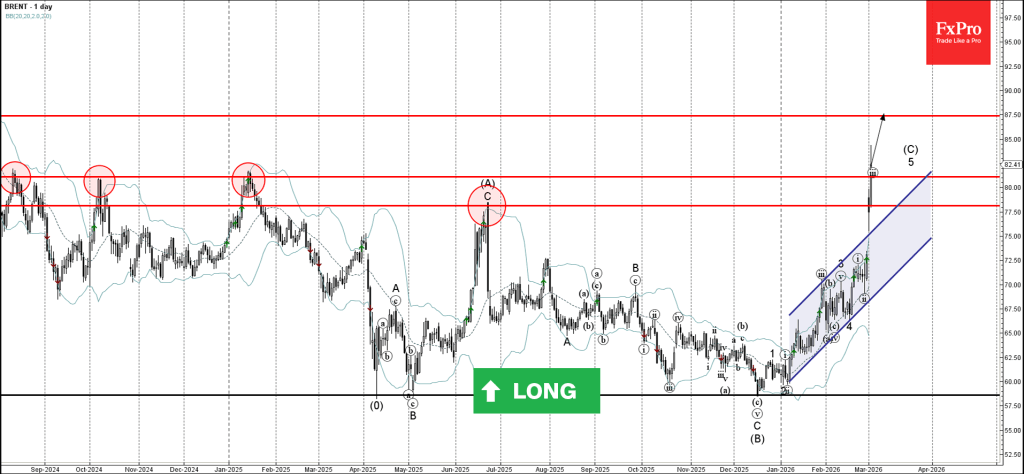

Brent Crude Oil Wave Analysis

Brent Crude Oil: ⬆️ Buy

- Brent Crude Oil broke key resistance levels

- Likely to rise to resistance level 87.500

Brent Crude Oil has been rising sharply in the last few trading session breaking through the key resistance levels – 78.20 (multi-month high from last June) and 81.10 (which has been reversing the price from 2024).

The breakout of these resistance levels accelerated the active short-term impulse wave 5 of the intermediate impulse wave (C) from December.

Brent Crude Oil can then be expected to rise to the next resistance level 87.500 (target for the completion of the active impulse wave 5).