Sample Category Title

Energy Prices Surge amid Middle East Conflict

In focus today

In the euro area, flash February inflation is released today. We expect headline inflation to rise to 1.8% y/y and core inflation to remain at 2.2%. Inflation in France and Spain came in higher than expected while Germany was below expectations. The momentum in services inflation picked up again in February after a very low January print which was due to lower taxes. So, we expect momentum in services inflation to be similar to November and December.

In the UK, the Spring Statement will be delivered today (afternoon) by Chancellor Reeves. It will include a new economic outlook but not a fiscal one. While we do not expect any meaningful changes to the fiscal outlook, we note that UK markets continue to be particularly sensitive to political uncertainty.

Today at 13.00-13.30 CET, we will host a concise 30-minute webinar on the Iran situation. Topics include the most likely path forward, implications for global macro and central banks as well as the cross-asset market impact.

Economic and market news

What happened over night

The conflict in the Middle East continues to escalate, with Saudi Arabia reporting that the US embassy in Riyadh was hit by two drones, causing a 'limited fire'. Addressing the attack and the deaths of American personnel in the Iran conflict, President Trump told NewsNation that details of Washington's retaliation would be revealed "soon," while emphasising that deploying ground troops would not be necessary.

In energy markets, in response to the forced shutdowns of regional energy facilities and disrupted shipping in the Strait of Hormuz, the US administration announced a phased mitigation plan, with Treasury Secretary Scott Bessent and Energy Secretary Chris Wright set to outline measures today. President Donald Trump is scheduled to meet both officials at 2pm (1900 GMT), highlighting the urgency of the situation.

What happened yesterday

Energy markets faced significant turmoil on Monday as oil and gas prices surged amidst the escalating US-Israeli conflict with Iran. With no signs of negotiations, Brent crude peaked at 82 USD/bbl before retreating to close at 77 USD/bbl up 7.26% since Friday. On Monday. European natural gas prices saw an even sharper rise, spiking 40.6% to 43.5 EUR/MWh. These price movements reflect growing supply fears following precautionary shutdowns of key oil and gas facilities in the Middle East. Israeli and US strikes on Iran, along with Tehran's retaliatory actions, prompted QatarEnergy to halt LNG production after its facilities were hit by Iranian drones. Saudi Arabia also shut down its Ras Tanura refinery, a major crude export terminal, after a drone strike.

Shipping through the vital Strait of Hormuz (SOH) has come to a standstill, leaving 77 million barrels of oil stranded on 150 tankers in the Persian Gulf. While an Iranian Revolutionary Guards official declare the SOH closed and threatened to target ships attempting passage, the US military's Central Command insisted the Strait remains open. Nevertheless, shipping is expected to remain idle until safe passage can be ensured. The disruptions further strained global supply chains, pushing the benchmark freight rate to a record high, doubling since Friday. Daily LNG tanker freight rates jumped more than 40% on Monday following Qatar's production halt, amplifying concerns over energy shortages.

In the US, the ISM manufacturing index for February came in close to expectations at 52.4, except for a notable uptick in the prices index. Interestingly, the PMI survey painted a contrasting picture regarding manufacturing price pressures, with both input and output price indices continuing a declining trend. The increase in price pressures is attributed to a sharp rebound in imports, reflecting the delayed impact of tariffs.

In Sweden, the manufacturing PMI for February improved to 56.1 from 55.9. marking its highest level in four years. While the change is modest, it is a reassuring outcome, particularly given the softer sentiment seen in last week's NEIR survey. The details reveal improvements in both employment and production, though inventory build-up and delivery times have weakened since January.

Equities: Global equities declined "only" 0.4% yesterday against the backdrop of a significant geopolitical escalation in the Middle East. Given the scale of events, the market reaction remains relatively contained, but also very telling.

One key reason equities did not fall more materially was strength in US tech. In fact, on a day of severe geopolitical escalation, cyclicals outperformed globally, while min vol underperformed. That is notable. While we argued for composure and against extrapolating into a major equity drawdown, some of yesterday's cross-asset price action stands out.

As expected, energy was the best-performing sector. However, the VIX is at only 21. In the US, the two worst-performing sectors were staples and healthcare, an unusual pattern following geopolitical escalation. This underlines the need to avoid reflex positioning in this conflict. There is a clear element of unwind in crowded trades. Investors should be careful not to be caught short off guard. This unwind dynamic is also visible across regions. South Korea, returning from a long weekend, is down 6% this morning following strong YTD gains. Most of Asia is lower, and US and European futures are trading down this morning.

FI and FX: The market impact on the back of the war between Israel/US and Iran was a solid rise global bond yields yesterday, where 10Y US Treasuries rose more 10bp and 10Y German yields rose 7bp and curves bear flattened. This morning, we have seen a substantial rise in yields in Asian fixed income markets such as Australia and Japan as they follow the sentiment from yesterday. Furthermore, Furthermore, the dollar keeps strengthening.

Volatility is the Name of the Game

Yesterday was an unusual session. Asian and European markets were hammered by the escalation in the Middle East, which sent oil and gas prices sharply higher. US crude jumped more than 10% at the open, while European gas futures were up as much as 50% at one point after Qatar shut down a gas production facility following an Iranian drone attack. TTF futures eventually closed nearly 40% higher.

Defense and energy stocks were the biggest winners in Europe, while banks, travel and luxury names tanked. Overall, the Stoxx 600 retreated 1.62% from its all-time high, as European sovereign bonds rebounded. The benchmark 10-year yield rose 8bp.

Sovereign yields around the world jumped as well, including the US 10-year yield — which might normally have attracted safe-haven flows. But not this time. Investors trimmed dovish expectations on fears that rising energy prices will quickly feed into inflation in the US and globally, preventing central banks that were moving toward rate cuts this year (like the Federal Reserve (Fed)) from easing — and potentially forcing others to reconsider tightening if inflation resurges.

So far, the market reaction was logical. The energy-dependent DAX was the biggest loser among major European indices, while part of the FTSE 100’s losses were offset by strong gains in energy and defense stocks.

What was unusual was the US reaction. Headlines worsened throughout the day. Beyond Qatar, Saudi Aramco halted operations at the country’s largest oil refinery after a drone strike in the area. Iranian officials said they were not ready to negotiate and would fight. President Trump said the war could last weeks, not days, and that the US would send troops if necessary — doing “whatever it takes” to achieve its objectives.

Yet oil prices retreated from their early peaks, and as oil pulled back, US equities advanced. The S&P500 and Nasdaq 100 both closed the session with modest gains. As such, US stocks outperformed their peers despite the prospect of a prolonged conflict, fading Fed cut expectations and rising yields. The retracement in oil prices appeared sufficient to reassure investors that buying the dip was justified.

That optimism is fading in Asia this morning. Oil prices are rebounding, with US crude back above $73pb after falling toward $70pb yesterday. US natural gas is trending higher, and US 10-year Treasuries remain under pressure, alongside sovereign bonds from Australia to Japan. Futures are back in negative territory. We are still left scratching our heads seeing how resilient the US session proved:

- On the stock side, Palantir jumped nearly 6% given its military exposure, while Nvidia gained 3% after announcing investments in data-center optics makers Lumentum and Coherent to secure high-speed connectivity critical for scaling AI infrastructure. However, the risk that Middle Eastern clients — facing disruptions to oil facilities and trade — could see revenues fall and delay AI investment plans, including purchases of Nvidia chips, received little attention. It remains to be seen whether that risk will be priced in with a lag.

- On the macro front, US dollar appreciation also plays against Big Tech earnings prospects. Yet Roundhill’s Magnificent 7 ETF rebounded sharply from below its 200-DMA to close 0.42% higher. Software stocks gained as well. US markets traded as if largely unconcerned by the geopolitical escalation.

That said, sustained tensions are likely to weigh on US sentiment, as well. A durable rise in energy prices would eventually hurt corporate margins and consumer demand — including in the US.

Big Tech remains exposed to a potential shift in sentiment from AI euphoria to concerns over heavy capital spending increasingly financed by debt – with or without the rise in energy prices. The rise in energy prices would only amplify the size of a future pullback.

So what’s next? An analyst at Goldman Sachs argued that “the only way up from here is down,” suggesting a correction before further gains. I also believe the recent pullback in US indices has not been sufficient to reflect the shifting risk profile facing Big Tech (as they move toward debt issuance to finance additional capex).

In FX, a prolonged war could further strengthen the US dollar, while gold’s muted reaction suggests that investors are reluctant to move capital after an impressive price rally.

Interestingly, Bitcoin gained yesterday. It traded sideways over the weekend and rebounded more than 4.5% despite questionable risk appetite. Rising energy prices and higher yields would typically weigh on cryptocurrencies, yet some flows appeared to treat Bitcoin as a geopolitical hedge. I remain skeptical about its ability to protect against geopolitical shocks, particularly if Middle East tensions ultimately reinforce regional ties with the US, including Saudi Arabia – a scenario that would only strengthen the dollar’s global status.

In conclusion, geopolitical risks are rising – not easing. Volatility is increasing alongside trade and geopolitical uncertainty, and the risk of renewed inflation could tighten global financial conditions. The US session’s resilience is absent this morning — even Korea’s Kospi is down around 6.5%.

It is never wise to sell in panic, but given limited visibility, the current selloff does not yet look compelling enough to buy the dip.

Fragmented Markets Signal Bet Against “Forever War” Scenario

The global market reaction to the escalating conflict in the Middle East remains remarkably fragmented. U.S. equities successfully staged a "buy-the-dip" recovery overnight after an initial selloff. Both S&P 500 and NASDAQ closed with modest gains. In contrast, Asian markets told a darker story. South Korea’s Kospi tumbled nearly -5% as it caught up with the weekend's escalations, while Japan’s Nikkei 225 shed over -2%. Meanwhile, Hong Kong and China are relatively steady.

The "fear premium" in commodities is showing some signs of exhaustion. Gold briefly breached 5,400 mark but has since lost momentum, with upside resistance capped well below 5,600 record high. Similarly, WTI Crude Oil is gyrating in a tight range (71–73) below yesterday’s spike high, as traders weigh the potential for a Strait of Hormuz closure against current supply buffers and OPEC+ capacity.

Market pricing so far implies investors are leaning toward limited conflict scenario. Three broad paths are being weighed.

- Surgical (1–3 Weeks): A "best-case" scenario — lasting one to three weeks — would involve collapse of Iranian command structure or rapid ceasefire under interim leadership.

- Regime Transition (Up to 2 Months): A prolonged neutralization of "pockets of resistance" and dismantling of nuclear/missile infrastructure. This would sustain volatility but avoid systemic collapse.

- Forever War (1+ Years): Most destabilizing is a descent into a multi-sided civil war, shifting from high-intensity air strikes to long-term regional instability, which would materially alter risk premia across energy, currencies and sovereign markets.

Current cross-asset behavior suggests markets are assigning low probability to “Forever War” scenario. Equity resilience and contained oil pricing indicate belief that escalation will be bounded rather than indefinite.

Central banks are also already evaluating implications. ECB Chief Economist Philip Lane warned today that prolonged conflict could both spike inflation and depress Eurozone output — a classic stagflation risk. Though, he signaled little appetite for tolerating higher inflation under such uncertainty. In Australia, RBA Governor Michele Bullock echoed inflation concerns, explicitly keeping rate hike on table this month due to oil shock risk.

In currency markets, Dollar remains undisputed safe-haven leader this week. Canadian Dollar follows, buoyed by oil support. Aussie ranks third after hawkish RBA rhetoric. Swiss Franc is weakest after intervention warnings from SNB Euro underperforms as traders front-run Europe’s structural exposure, while Kiwi lags and Sterling and Yen hold middle ground.

In Asia, at the time of writing, Nikkei is down -3.18%. Hong Kong HSI is down -1.00%. China Shanghai SSE is down -1.06%. Singapore Strait Times is up 0.86%. Japan 10-year JGB yield is up 0.061 at 2.125. Overnight, DOW fell -0.15%. S&P 500 rose 0.04%. NASDAQ rose 0.36%. 10-year yield jumped 0.086 to 4.048.

RBA's Bullock reopens door to March hike as oil risks mount

RBA Governor Michele Bullock delivered a distinctly hawkish message at the AFR Business Summit today, warning markets not to assume a March rate hold is a done deal. She stressed that the upcoming meeting is “live,” pushing back against expectations that policy decisions are effectively pre-set or limited to quarterly moves.

Bullock highlighted that inflation remains elevated at 3.8% while unemployment at 4.1% still reflects tight labor market conditions. The Board, she said, will be “actively looking” at whether it needs to "move more quickly", explicitly discouraging the view that the RBA only adjusts rates at predictable intervals.

Central to her remarks was the risk of a prolonged oil price spike stemming from escalating Middle East tensions. While she emphasized that it is too early to quantify the impact, Bullock warned that a supply-driven shock could add to inflation pressures and, critically, influence inflation expectations — a development the RBA is “very alert to.”

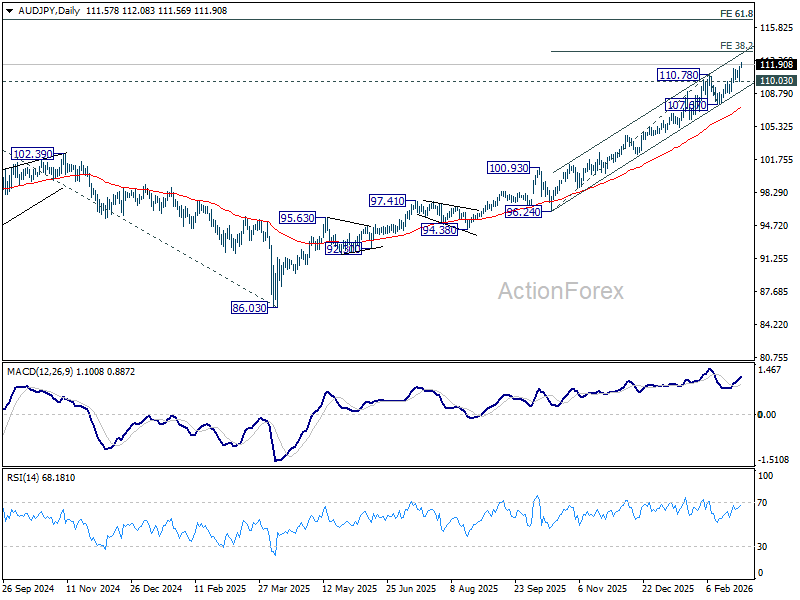

AUD/JPY breaks high after hawkish RBA shift, 113.22 next

Australian Dollar rallied broadly after RBA Governor Michele Bullock delivered hawkish remarks that reintroduced a genuine possibility of a rate hike at the March meeting. By describing the decision as “live” and warning against assuming a hold, Bullock unsettled prior market consensus and injected fresh upside risk into rate expectations. The shift immediately translated into stronger AUD performance across the board.

AUD/JPY led the advance, extending its uptrend and breached 112 level. The move reflects not only renewed tightening speculation from the RBA, but also relatively softer Yen dynamics amid delayed tightening expectations from Tokyo.

Technically, as long as 110.03 support holds, near-term bias remains firmly to the upside. The next target lies at 38.2% projection of 96.24 to 107.67 from 110.78 at 113.22, which aligns closely with the upper boundary of the near term rising channel. That area could present initial resistance and cap gains on first test, particularly if momentum indicators begin to stretch.

However, decisive break above 113.22 would open the path toward 61.8% projection at 116.65 before topping around there. That level represents a much more formidable barrier, coinciding almost precisely with the long-term fibonacci level, 61.8% projection of 59.85 (2020 low) to 109.36 (2024 high) from 86.03 (2025 low) at 116.62.

Euro under siege as Middle East war exposes fragility, EUR/CAD to dive to 1.57

While the military theater of the US-Israel-Iran conflict is centered in the Persian Gulf, its economic epicenter is arguably the Eurozone. The sharp decline in Euro this week is not merely a broad flight into Dollar safety. It reflects targeted repricing of Europe’s structural vulnerabilities at a moment of acute energy risk. Euro has emerged as primary casualty among major currencies, underperforming nearly all peers except Swiss Franc, which relative weakness is largely policy-driven following intervention warning from the SNB

The Energy Storage "Time Bomb"

The timing could hardly be worse. The EU enters March refill season with gas storage around 30%, significantly below roughly 40% seen in 2025 and 60% in 2024. That cushion has evaporated just as maritime energy routes face disruption risk.

With Strait of Hormuz under threat and major shippers such as Maersk and Hapag-Lloyd bypassing Suez Canal, replenishing inventories will come at steep premium. This looming import bill shock acts as direct devaluation pressure on Euro through deteriorating trade balance.

The Stability Proxy

Besides, Euro is treated as a proxy for Eurasian stability. Tehran’s declaration of “Total War” elevates non-financial risks that disproportionately affect Europe. The region’s economic architecture is deeply intertwined with Middle East energy and Asian trade corridors.

Closure or prolonged disruption of Suez Canal forces rerouting around Cape of Good Hope, effectively taxing every Euro-denominated export. Longer shipping times translate into higher freight costs, inventory bottlenecks and margin compression for European manufacturers.

At the sovereign level, rising energy costs and regional instability could renew fiscal strain. Migration pressures and potential need for renewed energy subsidies risk widening deficits.

Monetary Policy "Trapping"

The ECB now finds itself edging toward stagflationary dilemma. Surging natural gas prices are inflationary, yet function as regressive tax on consumers and businesses. Growth erosion could force policymakers to prioritize stability over price control. Markets might start to price in scenario where the ECB is compelled to shift its stance, and even pivoting toward easing again even as inflation risks jump.

The Failure of the 1.2000

Failure to break 1.2000 in EUR/USD now looks pivotal. Throughout 2025, Euro rallied from 1.03 toward 1.20 on hopes of industrial revival. That psychological ceiling proved insurmountable. The weekend escalation is starting to trigger capitulation among long-position holders. What had been narrative of recovery is morphing into unwind of crowded positioning.

EUR/CAD to target 1.57

EUR/CAD is among the bigger movers this week, with Loonie being lifted by surging oil prices. Technically, fall from 1.6465 medium term top resumed by powering through 1.6063 support. Near term outlook will stay bearish as long as 1.6170 resistance holds.

For now, the fall from 1.6465 is seen as a correction to the five-wave rally from 1.4483. Deeper decline should be seen to 38.2% retracement of 1.4483 to 1.6465 at 1.5708. But strong support should be seen there to contain downside to bring rebound.

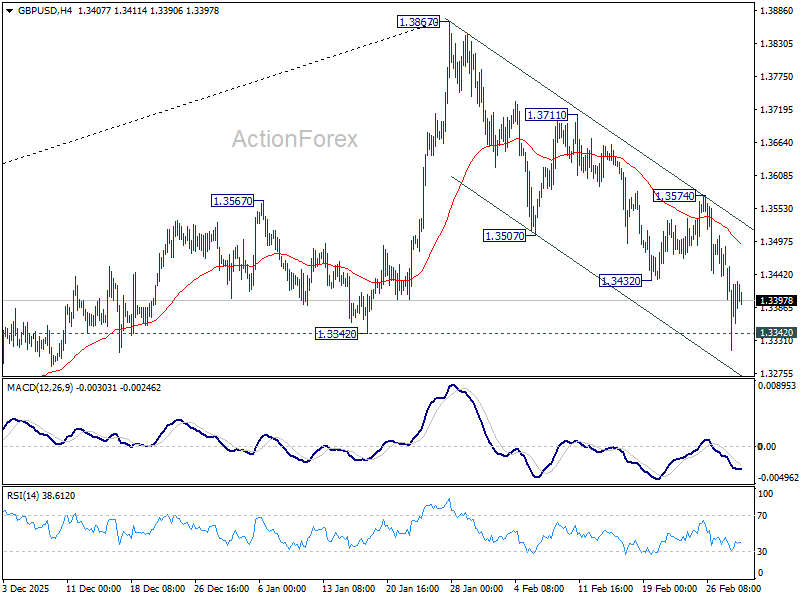

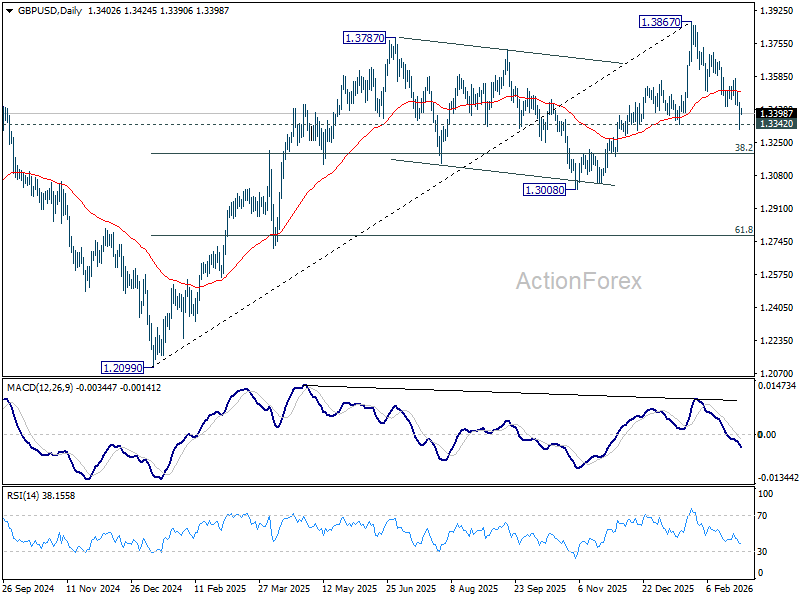

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3329; (P) 1.3393; (R1) 1.3470; More...

Intraday bias in GBP/USD stays on the downside as fall from 1.3867 is still in progress. Decisive break of 1.3342 structural support will argue that it's already correcting the whole rise from 1.2099. In this case, deeper fall should be seen to 1.3008 support next. For now, risk will stay on the downside as long as 1.3574 resistance holds, in case of recovery.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.

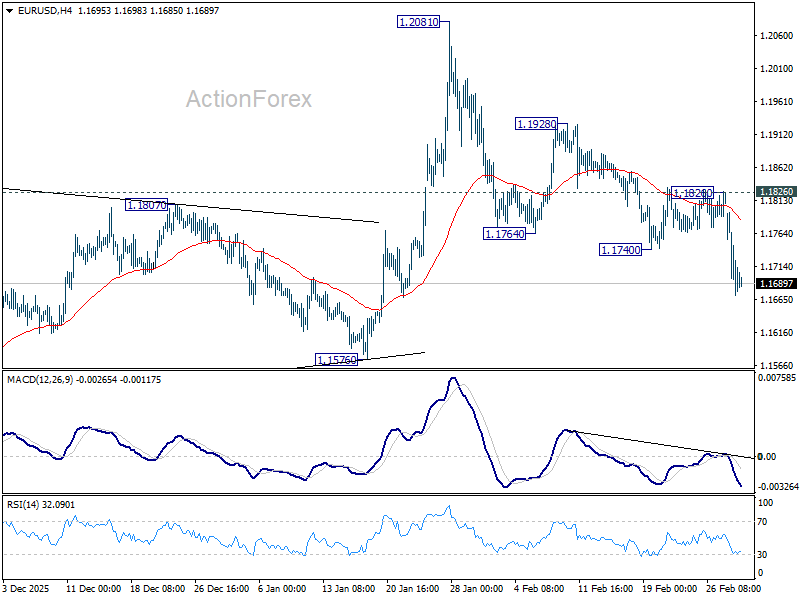

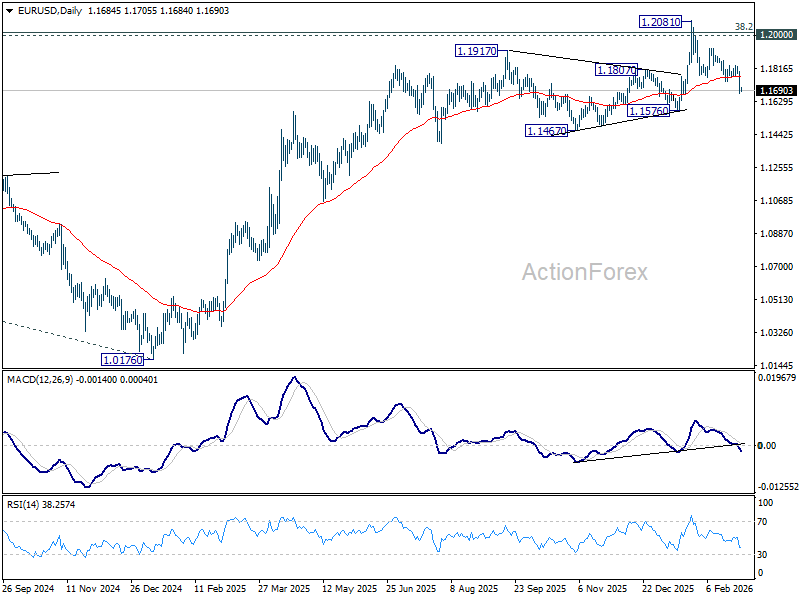

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1641; (P) 1.1719; (R1) 1.1765; More….

Fall from 1.2081 is in progress in EUR/USD and intraday bias stays on the downside for 1.1576 structural support. Firm break there should confirm rejection by 1.2 key psychological level and turn near term outlook bearish. For now, risk will stay on the downside as long as 1.1826 resistance holds, in case of recovery.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

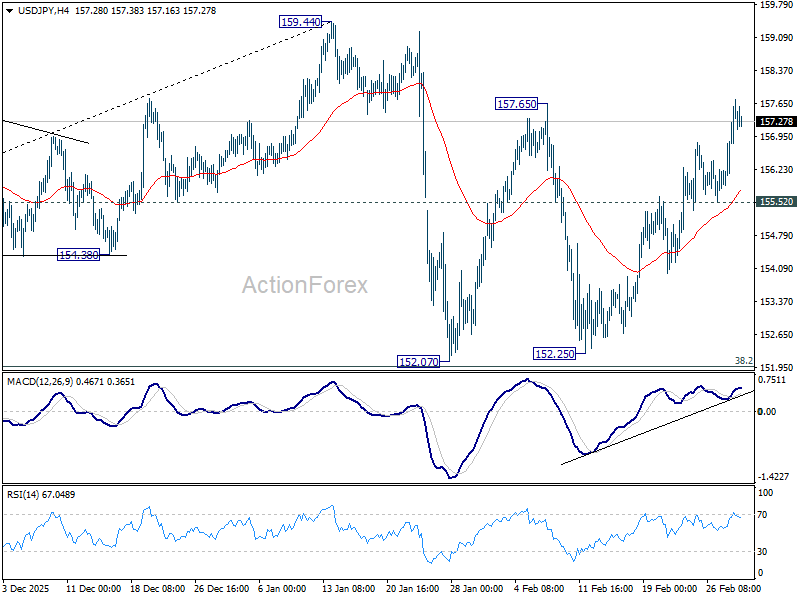

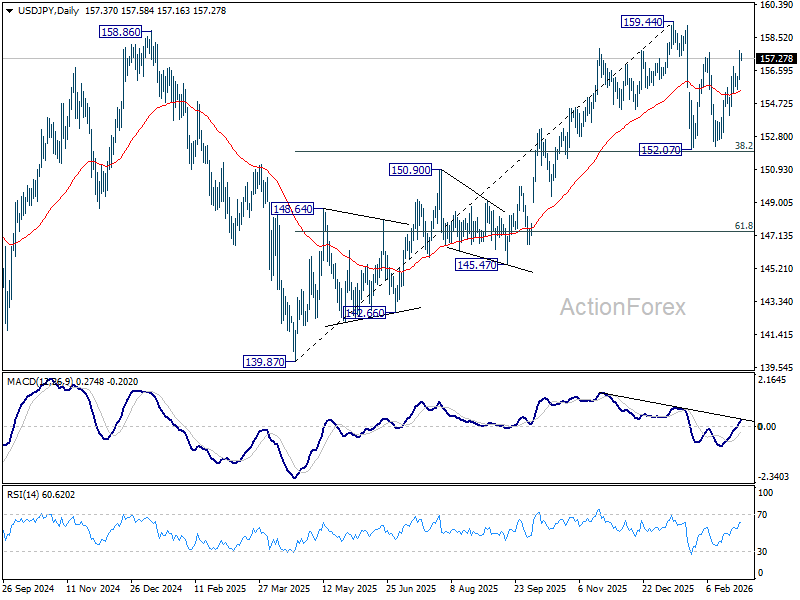

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.30; (P) 157.03; (R1) 158.08; More...

USD/JPY's rally from 152.25 continues today and intraday bias remains on the upside. Further rise should be seen to retest 159.44 high. On the downside, below 155.52 minor support will turn intraday bias neutral. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3329; (P) 1.3393; (R1) 1.3470; More...

Intraday bias in GBP/USD stays on the downside as fall from 1.3867 is still in progress. Decisive break of 1.3342 structural support will argue that it's already correcting the whole rise from 1.2099. In this case, deeper fall should be seen to 1.3008 support next. For now, risk will stay on the downside as long as 1.3574 resistance holds, in case of recovery.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.

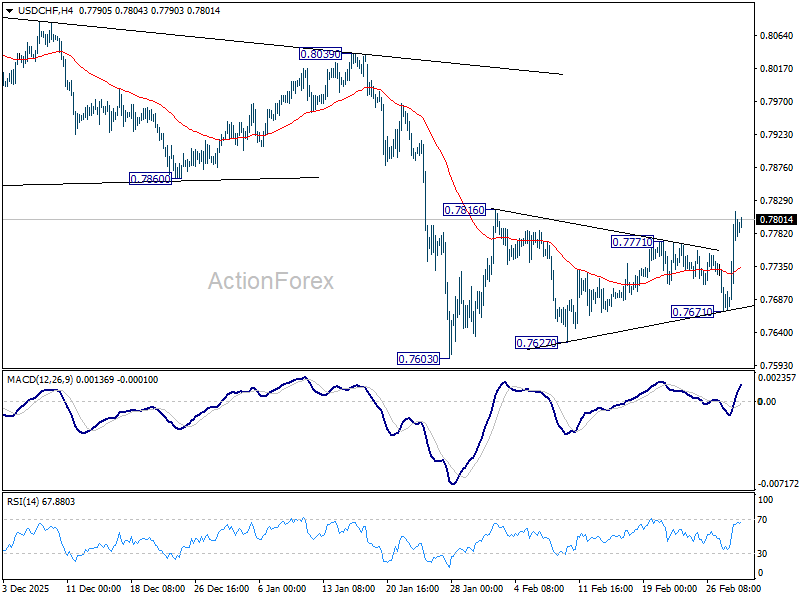

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7706; (P) 0.7760; (R1) 0.7848; More….

Intraday bias in USD/CHF remains neutral for the moment. Consolidations from 0.7603 could extend, but upside should be limited by 55 D EMA (now at 0.7818). Below 0.7671 will bring retest of 0.7603 low. Firm break there will resume larger down trend, and target 0.7382 projection level next. However, sustained break of 55 D EMA will indicate that a larger scale corrective bounce in underway and target 0.8039 resistance next.

In the bigger picture, down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8123 resistance holds.

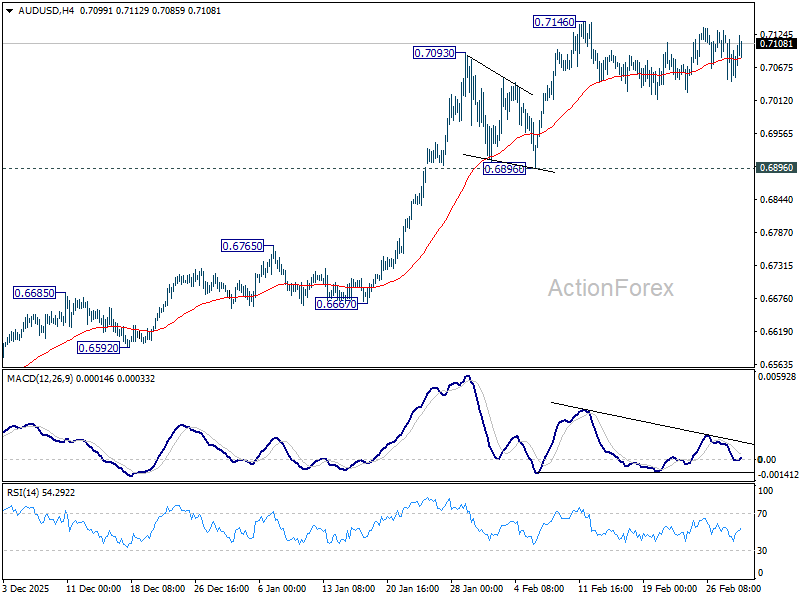

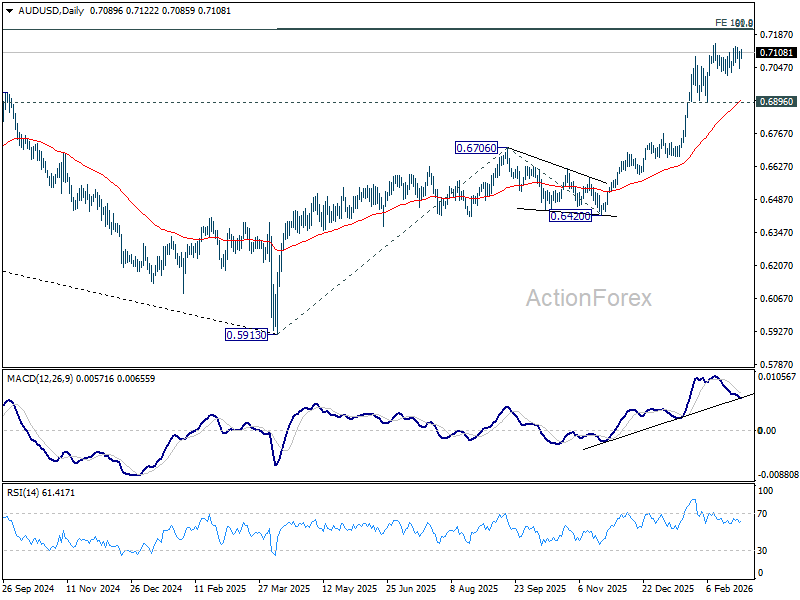

AUD/USD Daily Report

Daily Pivots: (S1) 0.7048; (P) 0.7083; (R1) 0.7129; More...

AUD/USD is still bounded in sideway trading and intraday bias stays neutral. Further rise is expected with 0.6896 support intact. On the upside, firm break of 0.7146 will resume resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

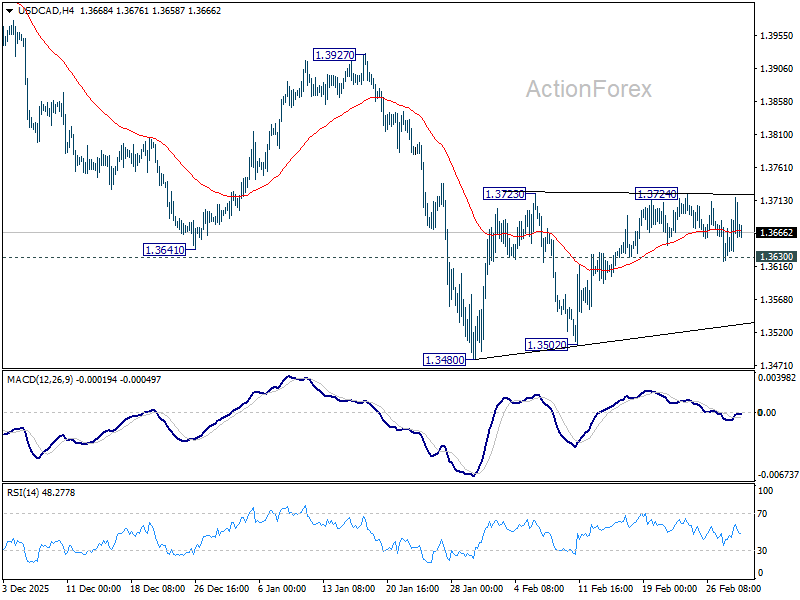

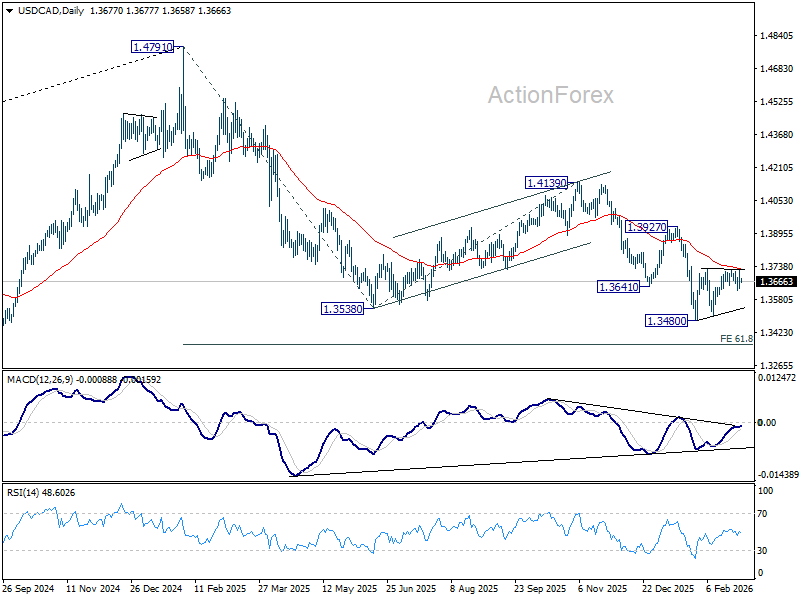

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3636; (P) 1.3677; (R1) 1.3718; More...

No change in USD/CAD and intraday bias remains neutral. Consolidations pattern from 1.3480 could extend. But upside should be limited by 55 D EMA (now at 1.3724). On the downside, firm break of 1.3630 minor support will bring retest of 1.3480 low first. Decisive break there will resume larger down trend 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. However, decisive break of 55 D EMA will bring stronger rebound to 1.3927 resistance instead.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

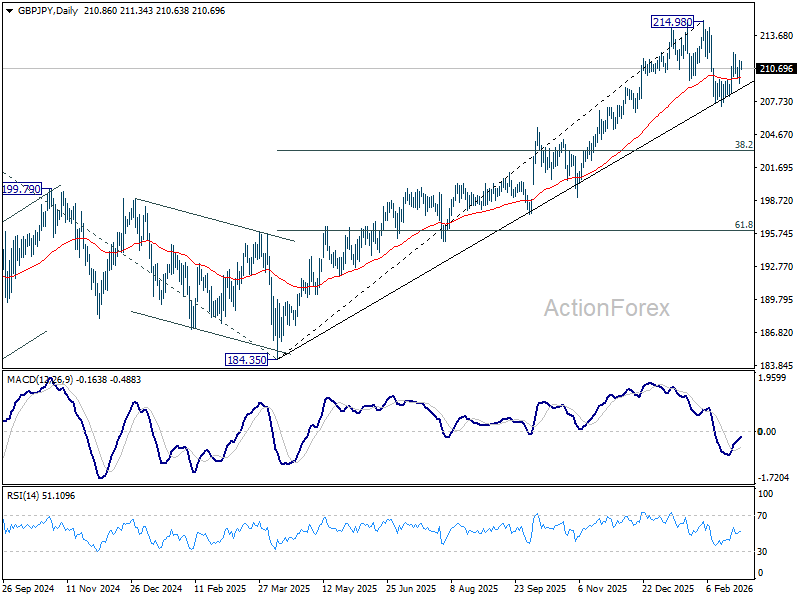

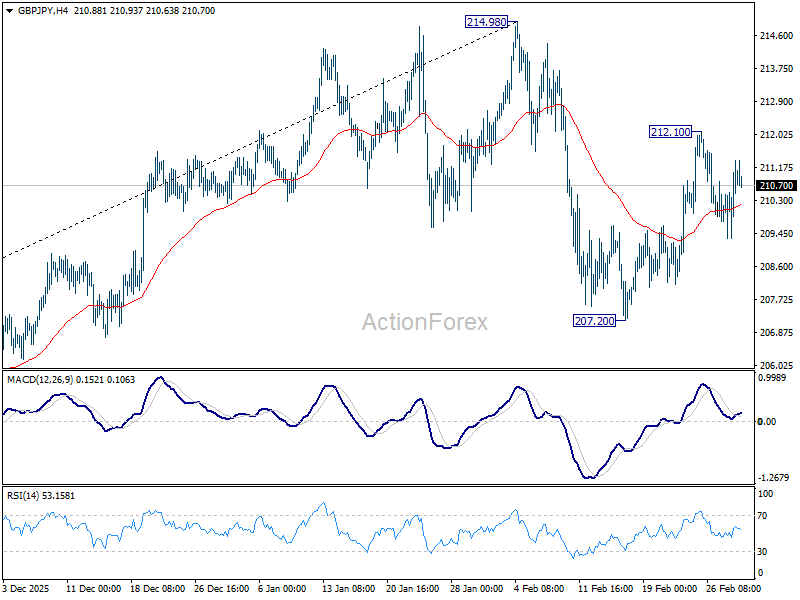

GBP/JPY Daily Outlook

Daily Pivots: (S1) 209.59; (P) 210.49; (R1) 211.84; More...

Intraday bias in GBP/JPY remains neutral and outlook is unchanged. Corrective fall from 214.98 should have completed at 207.20 already. On the upside, above 212.10 will resume the rebound from 207.20 to retest 214.98 high. For now, risk will stay on the upside as long as 207.20 holds.

In the bigger picture, current development argues that price actions from 214.98 might be a near term consolidation pattern only. That is, larger up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, though, break of 207.20 will revive that case that it's already in a larger scale correction.