Sample Category Title

EUR/USD Rejected at Resistance, Bears Eye Fresh Decline Ahead

Key Highlights

- EUR/USD started another decline and traded below 1.1840.

- A key bearish trend line is forming with resistance at 1.1800 on the 4-hour chart.

- GBP/USD extended losses and traded below 1.3460.

- Crude Oil prices jumped above $74.50 before trimming some gains.

EUR/USD Technical Analysis

The Euro failed to stay above 1.1900 and declined against the US Dollar. EUR/USD traded below the 1.1850 and 1.1800 levels to enter a bearish zone.

Looking at the 4-hour chart, the pair settled below 1.1820, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). A low was formed at 1.1742, and the pair is now consolidating losses.

There was a minor upward move above the 23.6% Fib retracement level of the downward move from the 1.1928 swing high to the 1.1742 low. However, the bears are active below 1.1840.

On the upside, the pair is now facing hurdles near 1.1800. There is also a key bearish trend line forming with resistance at 1.1800. The first major resistance sits at 1.1840. A close above 1.1840 could open the doors for more gains. In the stated case, the bulls could aim for a move to 1.1900. The main resistance sits near 1.1925.

Immediate support could be 1.1765. The first major area for the bulls might be near 1.1740. The main support sits at 1.1720, below which the pair might gain bearish momentum. In the stated case, it could even revisit 1.1650 in the coming days.

Looking at GBP/USD, the pair started a fresh decline below 1.3500, and there are chances of more losses in the near term.

Upcoming Key Economic Events:

- Euro Zone Manufacturing PMI for Feb 2026 – Forecast 50.8, versus 50.8 previous.

- US ISM Manufacturing Index for Feb 2026 – Forecast 52.3, versus 52.6 previous

WTI soars above 70 despite OPEC+’s “band aid” production hike

On Sunday, the OPEC+ "V8" coalition took a proactive stance by accelerating production hikes to 206,000 bpd starting in April. This move—surpassing the 137,000 bpd initially anticipated—serves as a strategic pivot to buffer a market shaken by the sudden U.S./Israeli strikes on Iran. While the alliance officially points to "market fundamentals," the timing is clearly a response to the geopolitical flashpoint in the Middle East.

Technically, WTI exhibited extreme volatility at the Monday open, surging past 75 before settling to trade near 70. Despite the OPEC+ supply boost, the near-term outlook remains bullish so long as the 67.36 resistance turned support level holds. Sustained trading above 70 psychological mark should open the door for a retest of 78.87 key resistance (2025 high). That should be the "line in the sand" for the current bull run.

While a firm break of 78.87 isn't yet expected, a clean break above it would signal a structural trend reversal, unwinding the multi-year downtrend from of 131.82 (2022 high). That could happen in the "nightmare scenario" of a total blockade in the Gulf, that could easily propel prices toward triple digits.

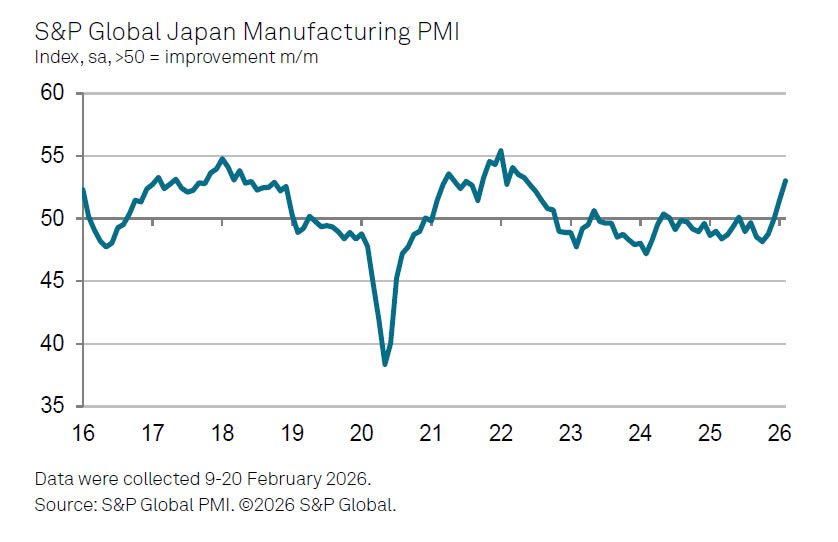

Japan’s PMI manufacturing finalized at 53.0, output and orders post fastest gains in years

Japan’s PMI Manufacturing was finalized at 53.0 in February, rising from 51.5 in January and marking highest reading since May 2022. The data point to a clear acceleration in factory activity, with the sector extending its expansion and signaling that recovery momentum is broadening at the start of Q1.

According to Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, companies reported the quickest increases in output, new orders, employment and purchasing activity in more than four years. Business confidence also climbed to highest level since mid-2024, supported by expectations that global demand will continue to revive, particularly across technology and automotive sectors.

While input cost pressures eased slightly, price growth remained elevated by historical standards, partly reflecting impact of "weak Yen" on imported materials. Nevertheless, stronger demand could improve firms ability to pass on higher costs, helping to stabilize margins.

Eco Data 3/2/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Feb F | 53 | 52.8 | 52.8 | |

| 07:00 | EUR | Germany Retail Sales M/M Jan | -0.90% | 0.00% | 0.10% | 1.20% |

| 07:30 | CHF | Real Retail Sales Y/Y Jan | -1.10% | 2.70% | 2.90% | 2.80% |

| 08:30 | CHF | PMI Manufacturing Feb | 47.4 | 50.1 | 48.8 | |

| 08:50 | EUR | France Manufacturing PMI Feb F | 50.1 | 49.9 | 49.9 | |

| 08:55 | EUR | Germany Manufacturing PMI Feb F | 50.9 | 50.7 | 50.7 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Feb F | 50.8 | 50.8 | 50.8 | |

| 09:30 | GBP | Mortgage Approvals Jan | 60K | 62K | 61K | |

| 09:30 | GBP | M4 Money Supply M/M Jan | -0.10% | 0.20% | 0.30% | |

| 09:30 | GBP | Manufacturing PMI Feb F | 51.7 | 52 | 52 | |

| 14:30 | CAD | Manufacturing PMI Feb | 51 | 50.4 | ||

| 14:45 | USD | Manufacturing PMI Feb F | 51.6 | 51.2 | 51.2 | |

| 15:00 | USD | ISM Manufacturing PMI Feb | 52.4 | 51.9 | 52.6 | |

| 15:00 | USD | ISM Manufacturing Prices Paid Feb | 70.5 | 59 | ||

| 15:00 | USD | ISM Manufacturing Employment Feb | 48.8 | 48.1 |

| 00:30 | JPY |

| Manufacturing PMI Feb F | |

| Actual | 53 |

| Consensus | 52.8 |

| Previous | 52.8 |

| 07:00 | EUR |

| Germany Retail Sales M/M Jan | |

| Actual | -0.90% |

| Consensus | 0.00% |

| Previous | 0.10% |

| Revised | 1.20% |

| 07:30 | CHF |

| Real Retail Sales Y/Y Jan | |

| Actual | -1.10% |

| Consensus | 2.70% |

| Previous | 2.90% |

| Revised | 2.80% |

| 08:30 | CHF |

| PMI Manufacturing Feb | |

| Actual | 47.4 |

| Consensus | 50.1 |

| Previous | 48.8 |

| 08:50 | EUR |

| France Manufacturing PMI Feb F | |

| Actual | 50.1 |

| Consensus | 49.9 |

| Previous | 49.9 |

| 08:55 | EUR |

| Germany Manufacturing PMI Feb F | |

| Actual | 50.9 |

| Consensus | 50.7 |

| Previous | 50.7 |

| 09:00 | EUR |

| Eurozone Manufacturing PMI Feb F | |

| Actual | 50.8 |

| Consensus | 50.8 |

| Previous | 50.8 |

| 09:30 | GBP |

| Mortgage Approvals Jan | |

| Actual | 60K |

| Consensus | 62K |

| Previous | 61K |

| 09:30 | GBP |

| M4 Money Supply M/M Jan | |

| Actual | -0.10% |

| Consensus | 0.20% |

| Previous | 0.30% |

| 09:30 | GBP |

| Manufacturing PMI Feb F | |

| Actual | 51.7 |

| Consensus | 52 |

| Previous | 52 |

| 14:30 | CAD |

| Manufacturing PMI Feb | |

| Actual | 51 |

| Consensus | |

| Previous | 50.4 |

| 14:45 | USD |

| Manufacturing PMI Feb F | |

| Actual | 51.6 |

| Consensus | 51.2 |

| Previous | 51.2 |

| 15:00 | USD |

| ISM Manufacturing PMI Feb | |

| Actual | 52.4 |

| Consensus | 51.9 |

| Previous | 52.6 |

| 15:00 | USD |

| ISM Manufacturing Prices Paid Feb | |

| Actual | 70.5 |

| Consensus | |

| Previous | 59 |

| 15:00 | USD |

| ISM Manufacturing Employment Feb | |

| Actual | 48.8 |

| Consensus | |

| Previous | 48.1 |

From Geneva Collapse to Market Shock – Technical Levels for DOW, TNX, DXY, CHF, Gold and WTI

Global markets closed February under conditions few anticipated even days ago. The events in the last 48 hours have shifted the framework from negotiation risk to open conflict. A geopolitical “black swan” has moved from theoretical scenario to live reality.

What had been treated for months as a tail risk scenario has now materialized into direct military confrontation. Markets are no longer pricing probabilities; they are reacting to reality.

The collapse of the Geneva negotiations on February 26–27 marked the final diplomatic failure. By February 28, the long-running shadow war transitioned into open kinetic engagement. The shift from proxy skirmishes to direct aerial bombardment of Iranian territory represents a structural escalation, not a tactical flare-up.

The reported targeting of leadership compounds in Tehran signals something more consequential than a punitive strike. It suggests a strategic pivot away from containment. The objective appears not merely to deter, but to reshape.

Reports that Supreme Leader Ali Khamenei was killed in an Israeli airstrike—if confirmed—would represent the most significant political rupture in Iran since 1979. For 36 years, Khamenei functioned as the final arbiter of Iranian military and nuclear doctrine. His removal introduces a power vacuum at the highest level of the regime.

That vacuum is not administrative; it is existential. Authority now fragments across the Guardian Council, the Islamic Revolutionary Guard Corps, and competing clerical factions. The uncertainty over who controls strategic assets—including nuclear decision-making—has elevated geopolitical risk to unprecedented levels.

This is the primary driver behind the immediate “panic bid” in traditional safe havens. Markets are not responding to a headline; they are repricing systemic uncertainty. The absence of a clear successor or stabilization mechanism removes the typical “off-ramp” that traders rely upon in geopolitical crises.

Institutional positioning suggests that some participants had anticipated escalation. Late Friday saw evidence of quiet risk reduction. When US President Donald Trump signaled that the diplomatic window was effectively closed, institutional desks treated the rhetoric as a near-certainty of kinetic action, particularly with carrier strike groups already deployed.

What distinguishes this episode from prior Middle Eastern tensions is the shift in scale and intent. This is not limited retaliation; it is leadership targeting. That distinction changes the risk matrix from cyclical volatility to structural regime uncertainty.

Energy markets are immediately implicated. Any instability in Iran’s command structure raises questions over the Strait of Hormuz, regional oil flows, and the behavior of proxy forces such as Hezbollah and the Houthis. The implications extend beyond crude prices to European energy security.

Europe, in particular, faces second-order risks. The region remains sensitive to supply disruptions following the prior energy shock. Currency markets have already begun to treat this as a European security issue, not merely a Middle Eastern conflict.

Financial markets now enter a new phase where geopolitical premium becomes embedded rather than episodic. This environment challenges traditional cross-asset relationships. Inflation expectations, safe-haven flows, and energy risk may all move simultaneously—but not necessarily in predictable directions.

The technical structures across equities, bonds, currencies, and commodities will now determine whether this shock becomes a temporary dislocation or the start of a broader trend reversal. Key support and resistance levels across major benchmarks will serve as early stress tests.

Volatility at the start of the week will likely reveal whether institutional capital views this as a contained military episode or the beginning of a protracted confrontation.

In the sections that follow, we examine how this geopolitical rupture is interacting with technical inflection points in DOW, US 10-year yields, Dollar Index, Swiss Franc, Gold, and WTI crude. The macro shock has arrived. Now the charts will determine its staying power.

DOW Faces First Real Stress Test at 48,459

DOW now sits at a critical technical juncture as markets reopen under full geopolitical stress. Immediate focus is on 48,459.88 support. Decisive break below that level would strongly suggest that the uptrend from 36,611.78 (2025 low) has completed a five-wave sequence at 50,512.79. If that interpretation holds, the current decline would represent more than a routine pullback; it would mark the start of a broader corrective phase.

In such a scenario, the next key downside target lies near 45,728.93. Importantly, that area aligns with a dense cluster of structural support, including the 55 W EMA (now at 45,874) and 38.2% retracement of 36,611.78 to 50,512.79 at 45,202.60. Such confluence zones should attract defensive positioning on first test, making this band a likely battleground between dip buyers and macro de-risking flows.

However, the true line in the sand sits at the 45,000 psychological level. Decisive weekly break below 45k would signal that the market has shifted from corrective weakness to medium-term bearish reversal.

10-Year Yield Breaks 4% as Panic Bid Overwhelms War Inflation

The US 10-year Treasury yield delivered one of the clearest signals of the shock’s intensity, gapping lower on Friday and closing at 3.962 after decisively breaking below the 4.0% psychological mark. In a typical war scenario, investors might price higher inflation risk through elevated energy costs and supply disruptions. Instead, the immediate reaction has been a forceful rush into principal safety, overwhelming any inflation premium.

Momentum now suggests a break of 3.947 medium-term support is likely. The next critical level is 3.886 (2025 low). A firm move below that would confirm that the rejection from the 55 W EMA (now at 4.194) was not temporary, but structural. In that case, yields could extend toward the 61.8% projection of 4.809 to 3.886 from 4.311 at 3.740, with even deeper downside potential toward 100% projection at 3.388 if safe-haven flows intensify.

However, markets remain at a fork in the road. Should yields instead reclaim 4.106 resistance, it could signal that the “sell America” narrative is back.

Dollar Index at Structural Crossroads Amid Conflicting Forces

Dollar Index now finds itself at a critical inflection point, caught between opposing macro currents. On one hand, geopolitical escalation and equity weakness typically generate safe-haven demand for the greenback. On the other, the sharp decline in US yields compresses rate differentials, undermining one of the Dollar’s primary pillars of support. The result is hesitation rather than conviction.

In the short term, attention centers on the 55 D EMA (now at 97.91). A firm push above that level would reinforce rebound momentum. Yet the broader technical structure remains vulnerable unless 100.39 resistance is decisively reclaimed. That level serves as the threshold separating corrective bounce from genuine trend reversal.

More structurally, the Index is pressing against the lower boundary of the long-term channel that has defined the uptrend since the 2008 low at 70.69. This is a make-or-break moment. A strong bounce from here, followed by a break of 100.39, would argue the multi-decade uptrend remains intact. Conversely, a clean fall below 95.55 would confirm a broader multi-year downtrend, potentially accelerating Dollar weakness at precisely the moment global uncertainty is rising.

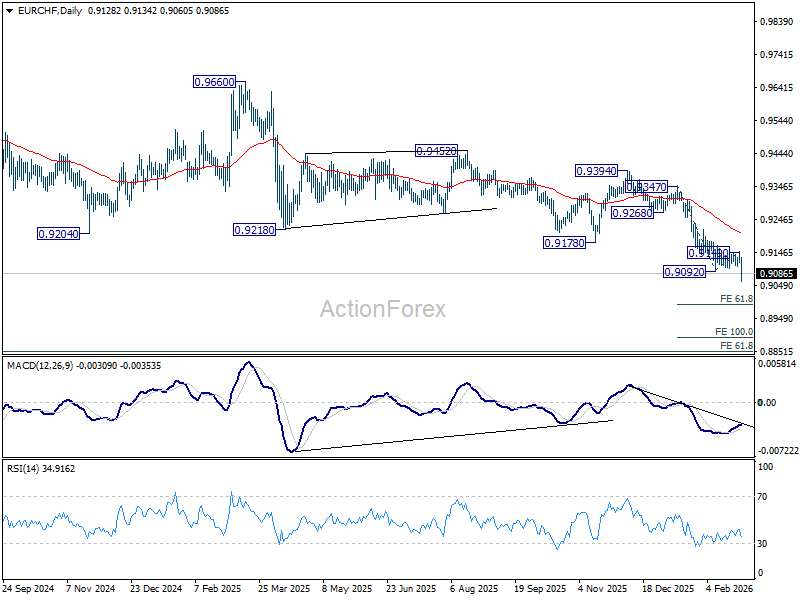

Swiss Franc Confirms Full Risk Escalation as EUR/CHF Breaks Down

The Swiss Franc has emerged as the clearest barometer of geopolitical stress. Its surge to multi-year highs against the Euro confirms that markets view this conflict not merely as a Middle Eastern event, but as a broader European security risk. Energy supply vulnerability and proximity to the geopolitical fault line have amplified defensive flows into CHF.

EUR/CHF has already broken decisively to the downside, resuming its medium-term down trend. As long as 0.9149 resistance holds, the bearish outlook remains intact. The next immediate target stands at the 61.8% projection of 0.9347 to 0.9092 from 0.9149 at 0.8991. A firm break below that would not merely be technical follow-through—it would reflect deepening risk aversion across European assets.

Should downside momentum accelerate, attention would shift toward 100% projection at 0.8894. A move of that magnitude would signal a severe deterioration in market confidence and likely coincide with broader stress in European equities and energy markets.

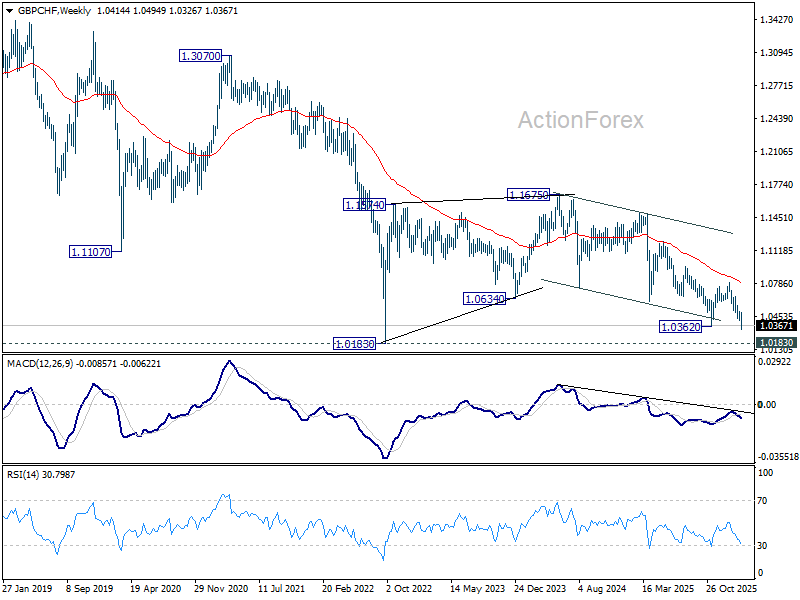

GBP/CHF is also approaching a structural inflection point. The 1.0183 level (2022 low), serves as critical support. A rebound should emerge from that area, at least on first test. However, decisive break below 1.0183 would mark resumption of the multi-decade downtrend, confirming that Sterling-specific weakness is compounding the broader flight to safety.

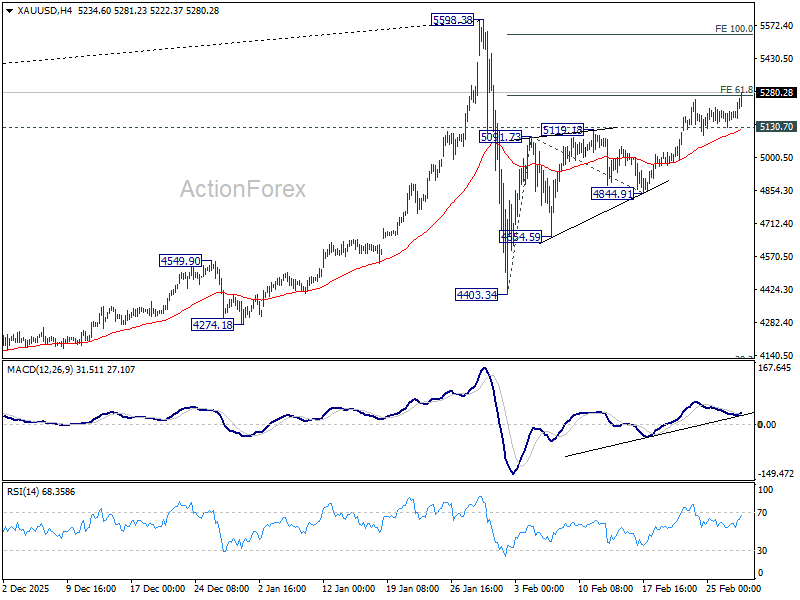

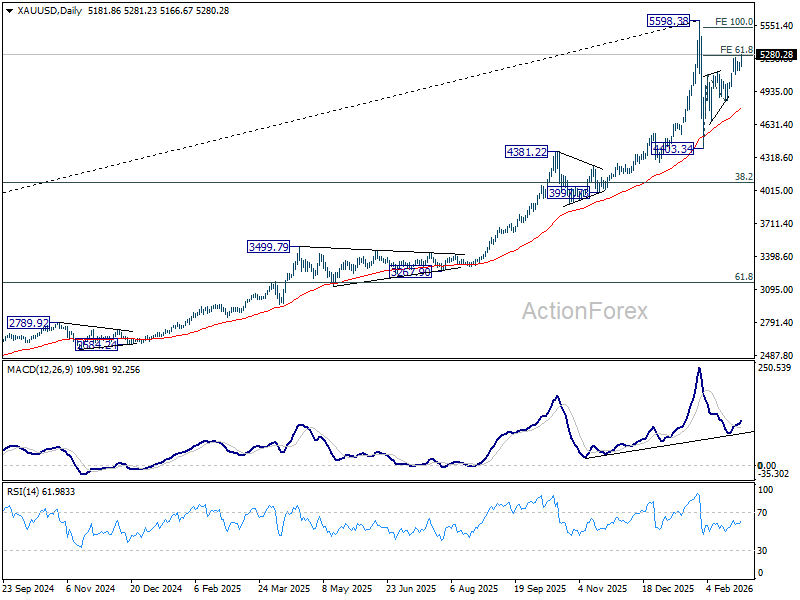

Gold Surges Toward 5,533 as Panic Bid Tests Structural Ceiling

Gold has extended its rally above 5,280 as safe-haven demand intensifies. The move reflects a classic panic bid driven by geopolitical shock, compounded by falling US yields.

From a structural standpoint, the advance from 4,403.34 is still viewed as the second leg of the corrective pattern from 5,598.38 high. The next major resistance lies near the 100% projection at 5,533.30. That level is critical. A rejection there would keep the broader corrective framework intact and suggest consolidation rather than breakout.

However, investors should remain alert to the risk of upside acceleration. In a true regime shock, technical ceilings can be overwhelmed by capital preservation flows. A decisive push through 5,533 and especially through 5,598.38 would invalidate the corrective view and signal that Gold is entering a new impulsive leg higher.

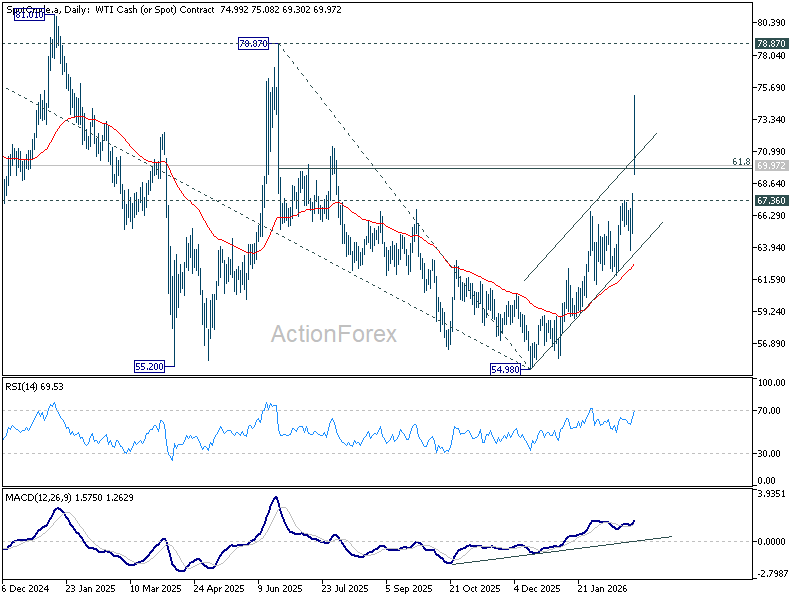

WTI Approaches 70 as War Premium Builds

WTI crude has resumed its rally from 54.98, breaking above 64.36 last week despite an intra-week dip to 63.69. Technically, the next near term target lies at 61.8% retracement of 78.87 (2025 high) to 54.98 (2025 low) at 69.74. The 70 psychological level sits directly above and is likely to act as the first major resistance zone. Under normal volatility conditions, that region could cap upside on initial test.

However, this environment is not normal. A decisive break above 70 would suggest that markets are shifting from precautionary pricing to full disruption pricing, opening the door toward a retest of the 78.87 high.

On the downside, a break below 63.69 would indicate short-term topping and imply that the initial war premium was partially front-run. For now, the path of least resistance remains higher, but the 70 level will determine whether this becomes a sustained energy shock.

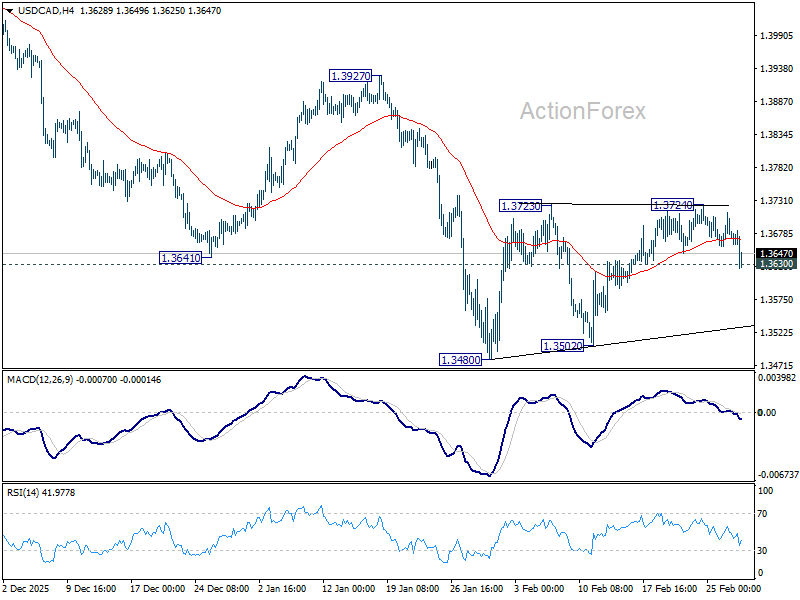

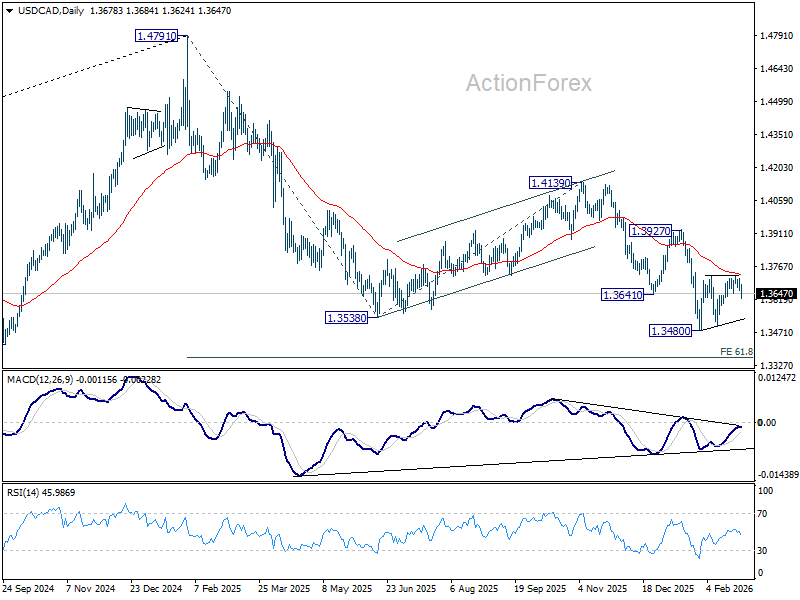

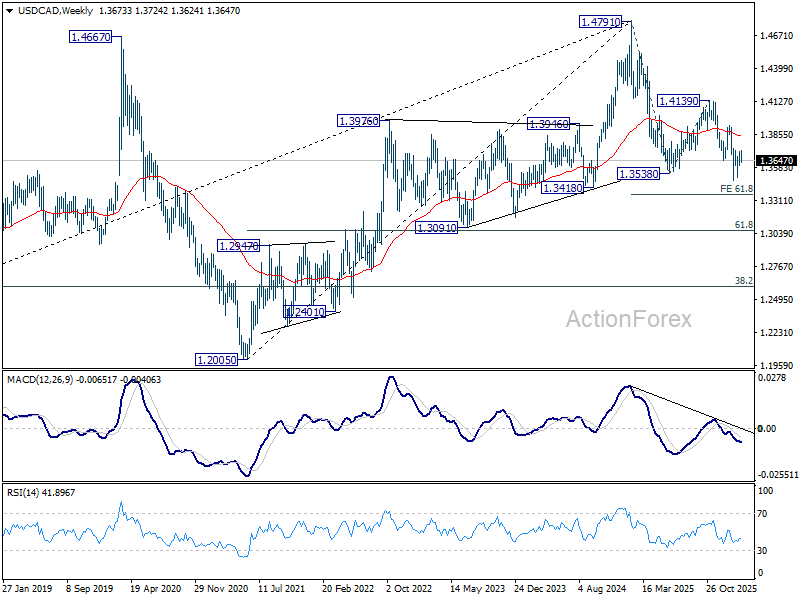

USD/CAD Weekly Outlook

Despite the late dip in USD/CAD, it's still holding on to 1.3630 minor support. Initial bias stays neutral this week first. Outlook is unchanged that price actions from 1.3480 are forming a consolidation pattern. Upside should be limited by 55 D EMA (now at 1.3728). On the downside, firm break of 1.3630 will bring retest of 1.3480 low first. Decisive break there will resume larger down trend 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

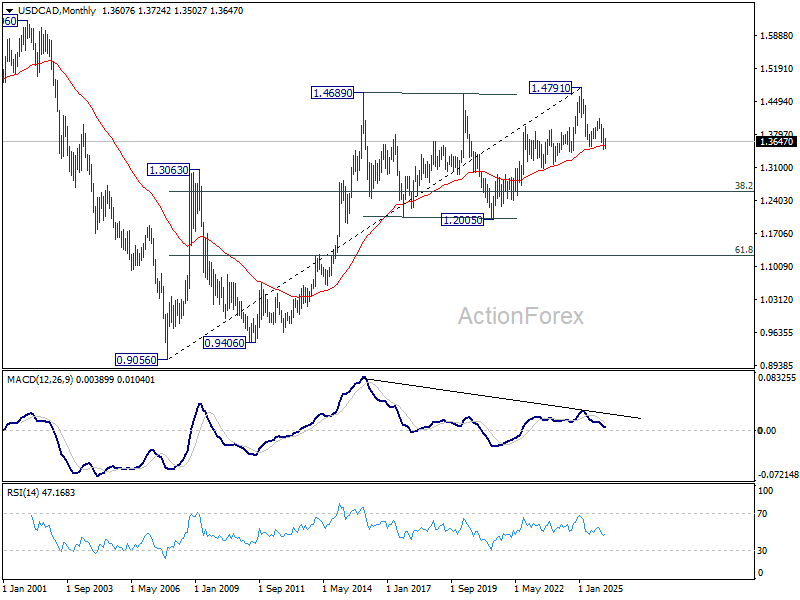

In the long term picture, rising 55 M EMA (now at 1.3569) remains intact. Thus, up trend from 0.9056 (2007 low) could still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

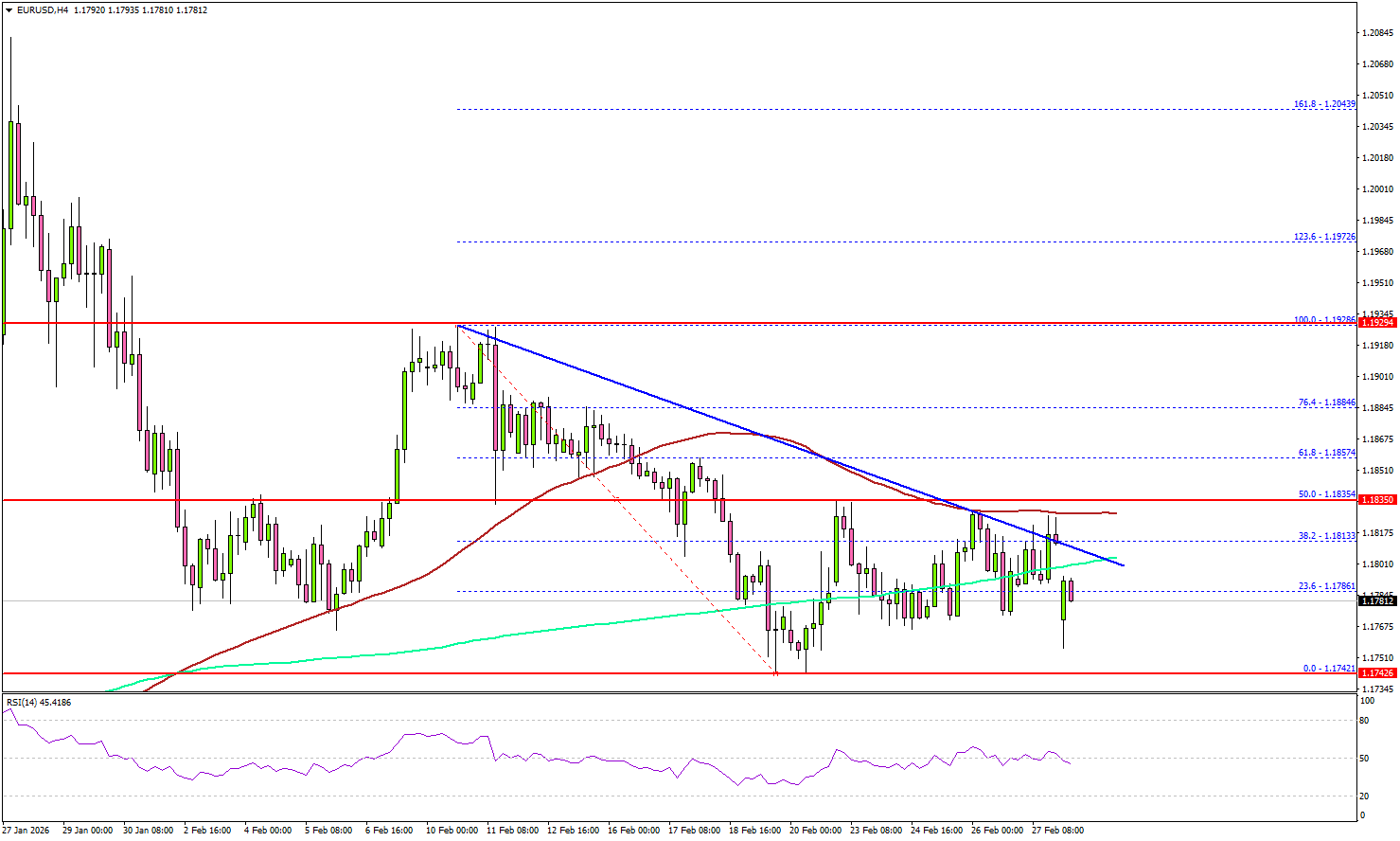

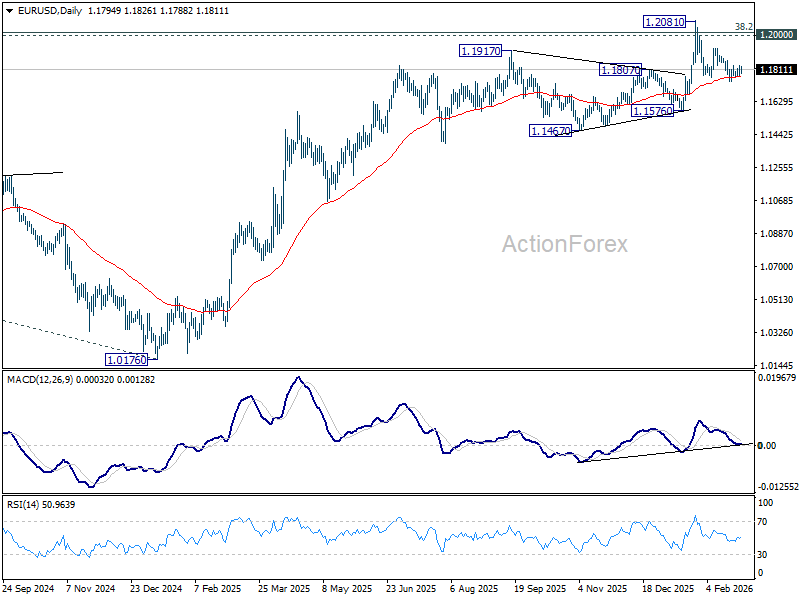

EUR/USD Weekly Outlook

EUR/USD gyrated in tight range above 1.1740 last week. Initial bias remains neutral this week first. Risk will stay on the downside as long as 1.1928 resistance holds. Below 1.1740 will target 1.1576 support next. Firm break there should confirm rejection by 1.2 key psychological level and turn near term outlook bearish. However, break of 1.1928 argue that fall from 1.2081 has completed as a correction, and revive near term bullishness. Retest of 1.2081 should then be seen next.

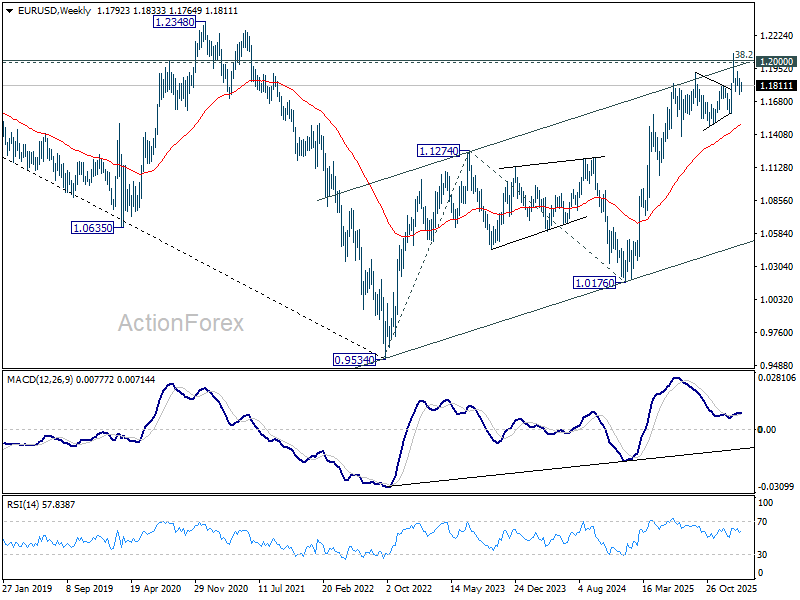

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

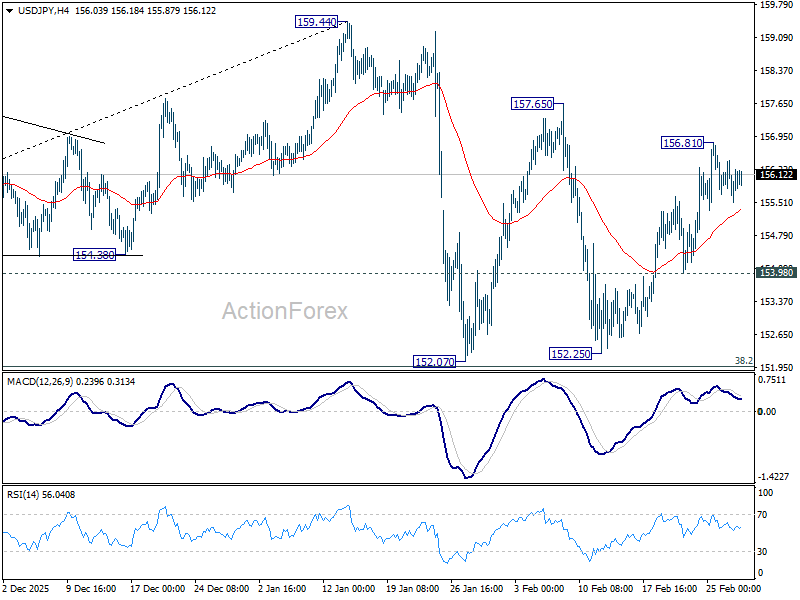

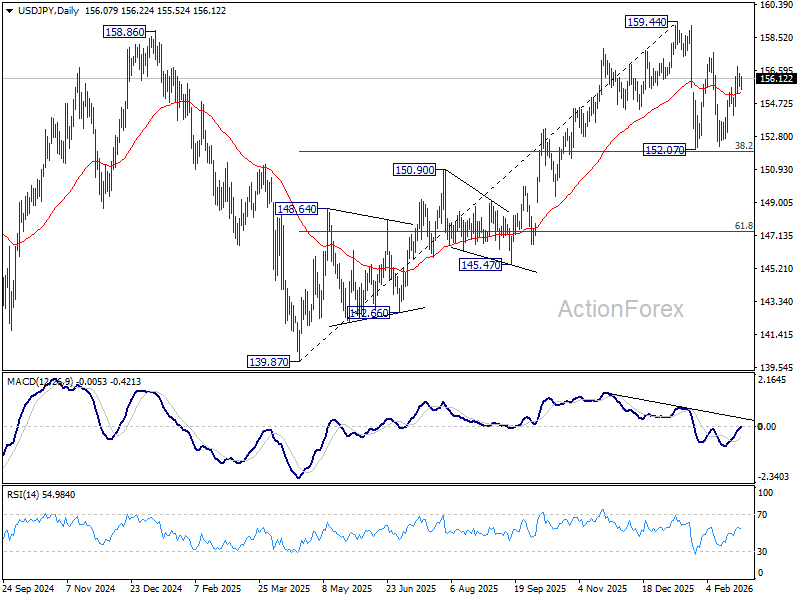

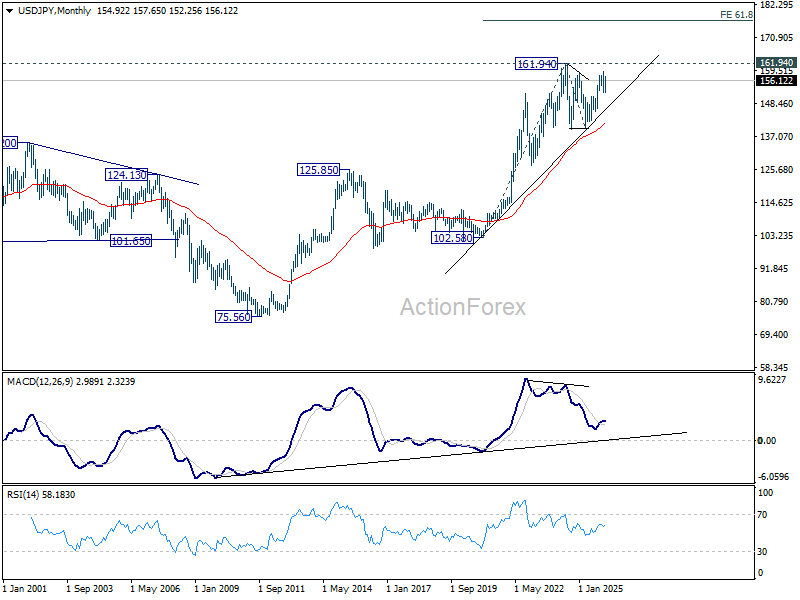

USD/JPY Weekly Outlook

USD/JPY's strong rebound lost momentum after hitting 156.81. Initial bias stays neutral this week first. Nonetheless, current development solidifies the case that price actions from 159.44 are merely a near term consolidation pattern. In other words, rise from 139.87 is still in progress. Above 156.81 will target 157.65 resistance and then 159.44 high. On the downside, however, break of 153.90 will bring deeper fall to 152.25 support. Still overall outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.98) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

In the long term picture, up trend from 75.56 (2011 low) is still in progress and might be ready to resumption. Firm break of 161.94 will target 61.8% projection of 102.58 (2020 low) to 161.94 (2024 high) from 139.87 at 176.55 in the medium term. Long term outlook will stay bullish as long as 139.87 support holds, even in case of deep pullback.

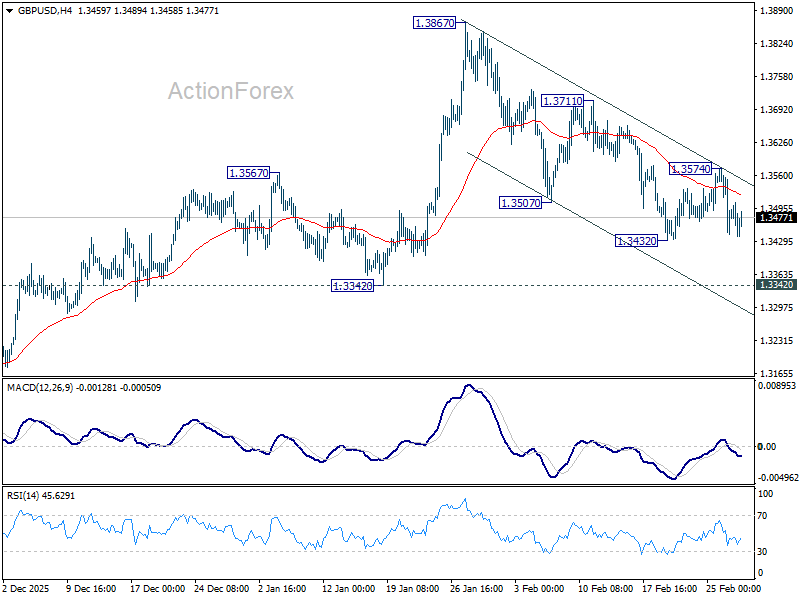

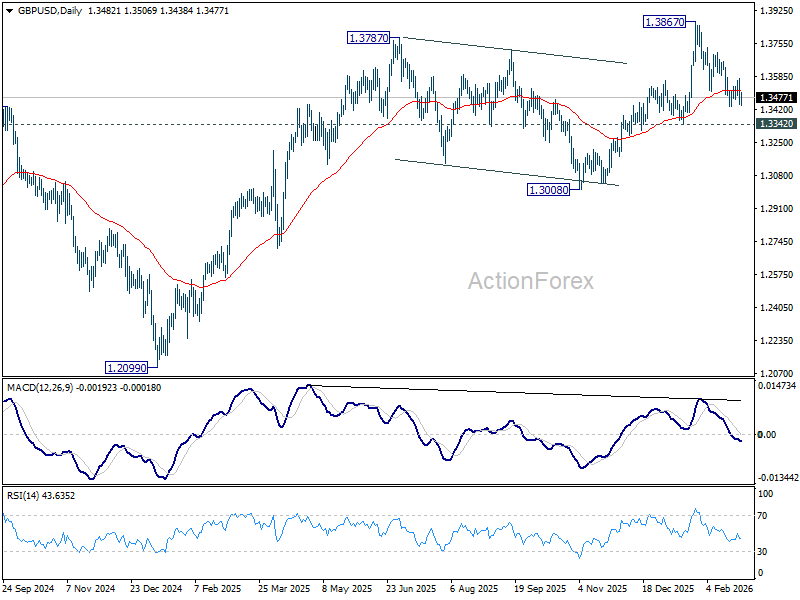

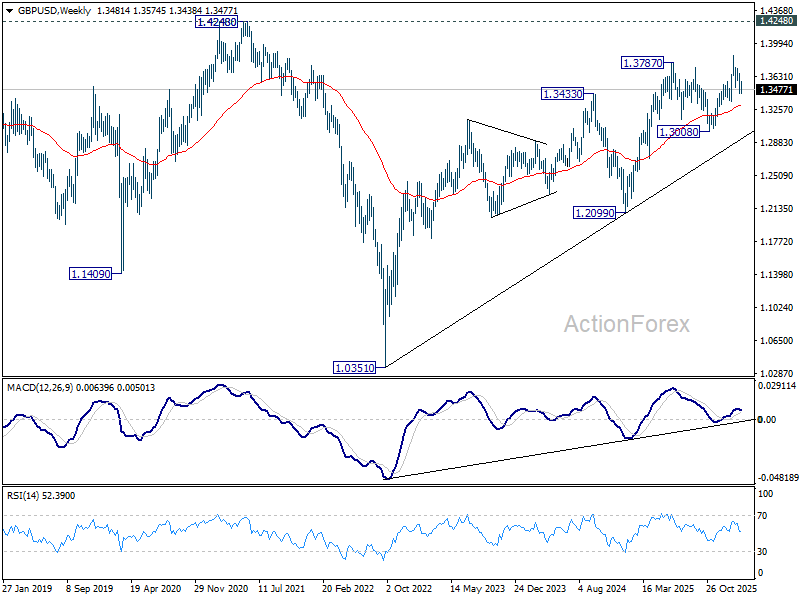

GBP/USD Weekly Outlook

GBP/USD's recovery was capped at 1.3574 last week but subsequent fall was contained contained above 1.3432 temporary low. Initial bias stays neutral this week first. Risk is mildly on the downside as long as 1.3574 resistance holds. Below 1.3432 will extend the fall from 1.3867 to 1.3342 structural support. Firm break there will argue that it's already correcting the whole rise from 1.2099. Nevertheless, break of 1.3574 will turn bias back to the upside for 1.3711 resistance instead.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.

In the long term picture, as long as 1.4248/4480 resistance zone holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.3051 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.

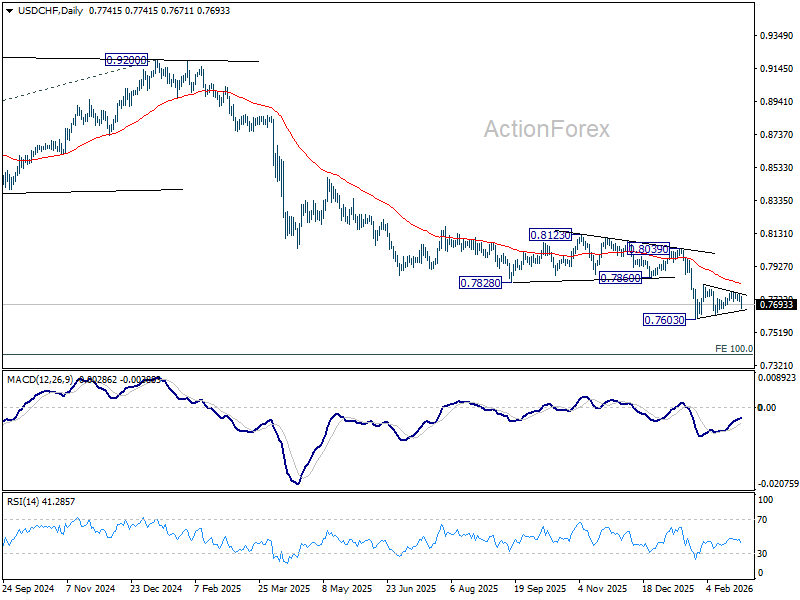

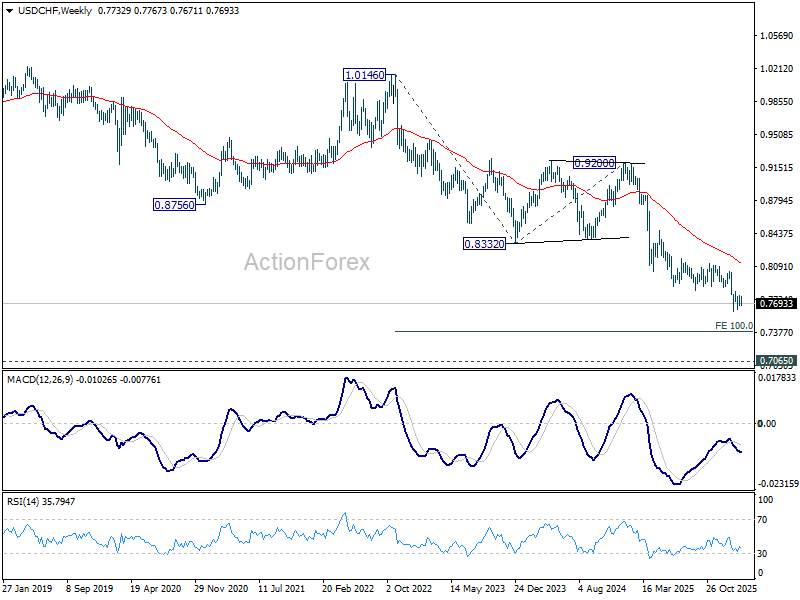

USD/CHF Weekly Outlook

USD/CHF stays in consolidations above 0.7603 last week and outlook is unchanged. Initial bias stays neutral this week first. In case of another rise, upside should be limited by 55 D EMA (now at 0.7824). On the downside, break of 0.7603 will resume larger down trend, and target 0.7382 projection level next. However, sustained break of 55 D EMA will indicate that a larger scale corrective bounce in underway and target 0.8039 resistance next.

In the bigger picture, down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8123 resistance holds.

In the long term picture, price action from 0.7065 (2011 low) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the downtrend. But in either case, outlook will stay bearish as long as 0.8756 support turned resistance holds (2021 low). Retest of 0.7065 should be seen next.

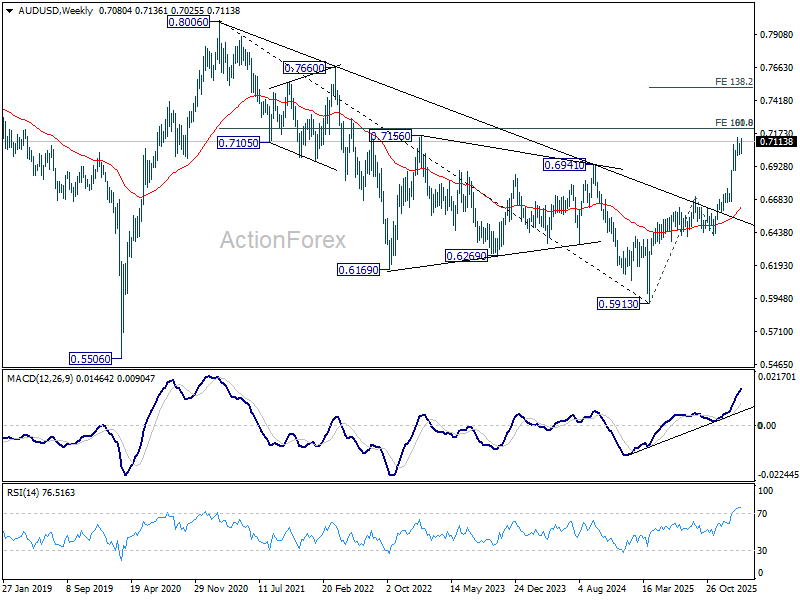

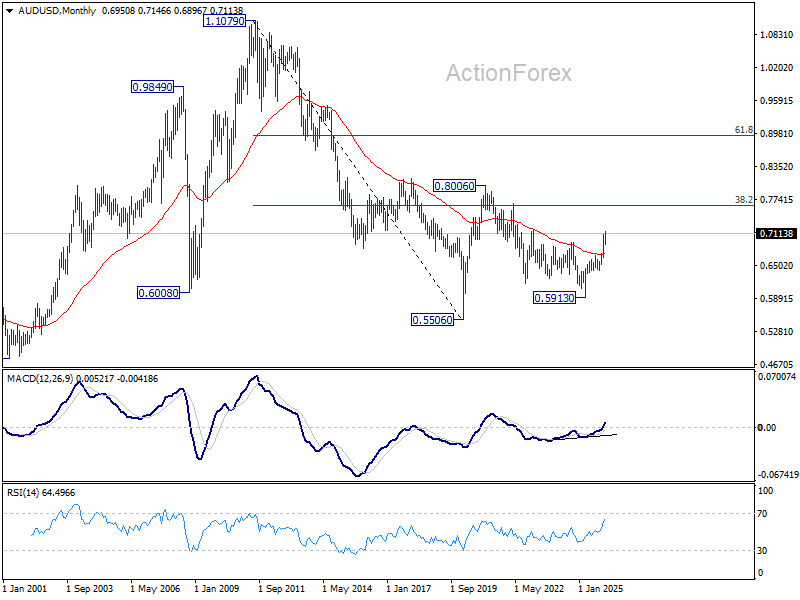

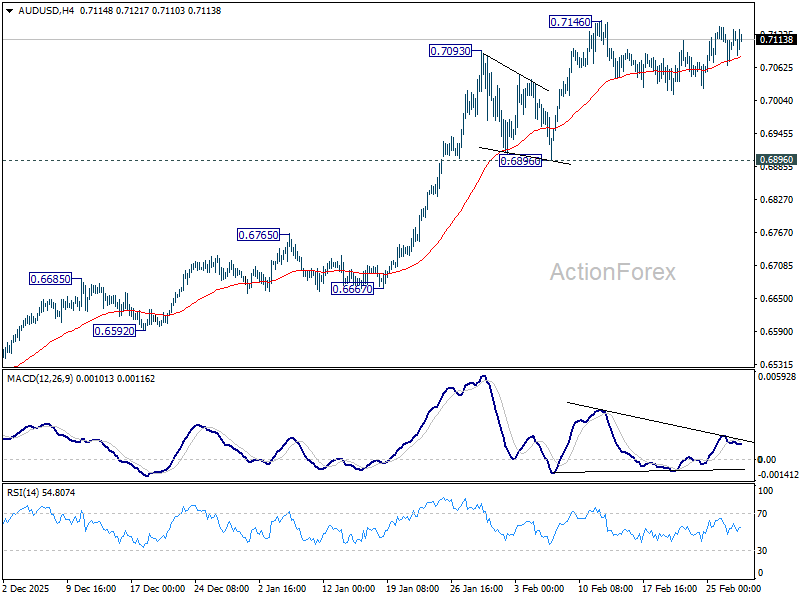

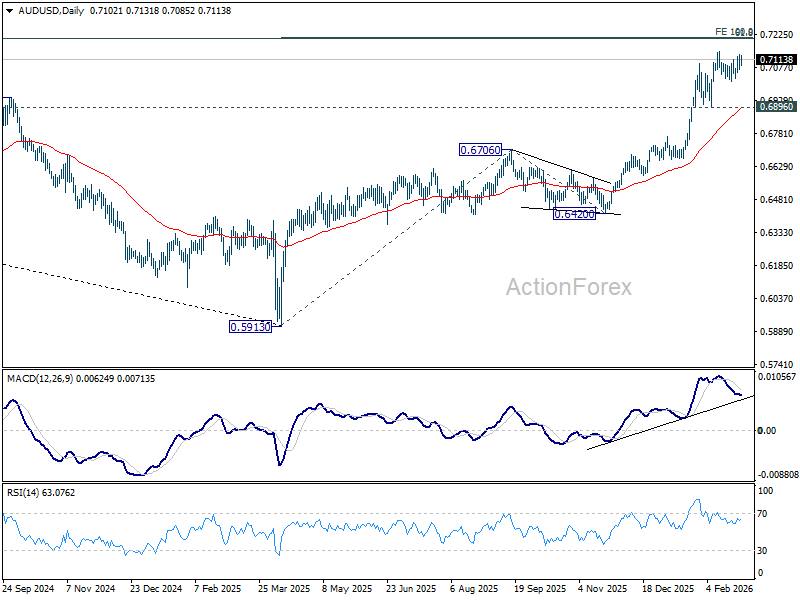

AUD/USD Weekly Report

AUD/USD remained bounded in consolidations below 0.7146 last week and outlook is unchanged. Further rise is expected with 0.6896 support intact. On the upside, firm break of 0.7146 will resume resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

In the long term picture, rise from 0.5913 is seen as the third leg of the whole pattern from 0.5506 (2020 low). It's still early to judge if this is an impulsive or corrective pattern. But in either case, further rise should be seen back to 0.8006 and possibly above.