Sample Category Title

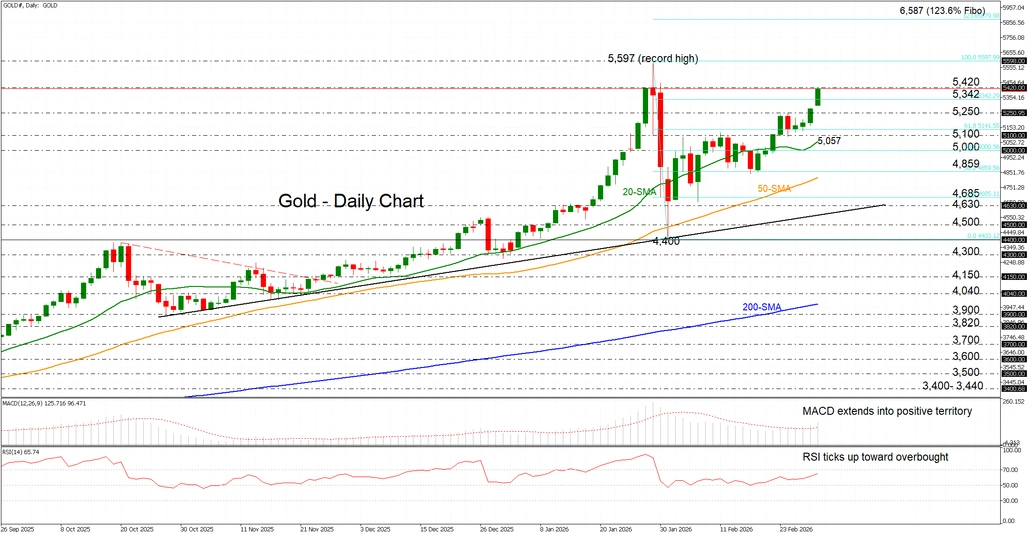

Gold Rises to One-Month High Near 5,400 on Safe-Haven Demand

- Gold extends its four day rally into record territory.

- Price spikes as escalating geopolitical tensions fuel flight to safety.

- Momentum indicators reinforce the bullish bias amidst the angst.

Gold opened with a bullish gap on Monday, rising more than 2.5% to reach a one month high near 5,400, as the conflict in the Middle East jolted markets. The surge came after the US and Israel launched major strikes on Iran, intensifying geopolitical tensions and deepening global economic uncertainty.

The momentum indicators support the upside. The MACD is extending above both the zero line and the red signal line, indicating strengthening bullish momentum. Meanwhile, the RSI is sloping upward toward overbought territory, reflecting heightened risk that is pushing gold prices closer to record highs.

Resistance above the January peaks near 5,420 lies at the record high of 5,597, reached on January 29 – just shy of the 6,000 level. A break above this area would mark a full recovery of the pullback from the January peak toward the February 2 low of 4,400. Beyond that, gold could target the 123.6% Fibonacci extension of that downleg at 6,587, entering uncharted territory.

On the downside, a potential pullback may first seek support at 5,250, the former resistance now turned support. Beneath that, 5,100 comes into play, sitting just below the 61.8% Fibonacci level at 5,141. A further decline would expose the 20 day simple moving average (SMA) at 5,057, followed by the psychological 5,000 mark. Below that, 4,859 remains a significant support level.

Overall, Gold’s broader uptrend is reaccelerating, after a brief consolidation period, and prices may continue to be repriced higher toward fresh record highs as markets enter a new era of geopolitical uncertainty, intensifying safe haven demand.

GBP/USD Weakens Again, EUR/GBP Shows Signs of Stability

GBP/USD failed to climb above 1.3575 and corrected some gains. EUR/GBP started a decent increase and might aim for more gains above 0.8800.

Important Takeaways for GBP/USD and EUR/GBP Analysis Today

- The British Pound is showing bearish signs below the 1.3500 support.

- There is a key bearish trend line forming with resistance near 1.3440 on the hourly chart of GBP/USD at FXOpen.

- EUR/GBP is gaining pace and trading above the 0.8750 pivot level.

- There is a connecting bullish trend line forming with support at 0.8755 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair failed to stay above the 1.3535 pivot level. As a result, the British Pound started a fresh decline below 1.3500 against the US Dollar.

There was a clear move below 1.3485 and the 50-hour simple moving average. The bears pushed the pair below 1.3440. Finally, there was a spike toward the 1.3400 handle. A low was formed near 1.3400, and the pair is now consolidating losses.

There was a minor move above 1.3425 and the 23.6% Fib retracement level of the downward move from the 1.3575 swing high to the 1.3400 low. On the upside, the GBP/USD chart indicates that the pair is facing resistance near a key bearish trend line at 1.3440.

A close above the trend line might send the pair toward the 50% Fib retracement at 1.3485 and the 50-hour simple moving average. If the bulls remain in action, they could aim for more gains.

In the stated case, the pair might rise toward 1.3535. The next major hurdle for GBP/USD sits at 1.3575. On the downside, there is a key support forming near 1.3400. If there is a downside break below 1.3400, the pair could accelerate lower. The next key interest area might be 1.3360, below which the pair could test 1.3320. Any more downside could lead the pair toward 1.3250.

EUR/GBP Technical Analysis

On the hourly chart of EUR/GBP at FXOpen, the pair started a decent increase from 0.8700. The Euro traded above 0.8750 to enter a positive zone against the British Pound.

The pair settled above the 50-hour simple moving average and 0.8760. The pair traded as high as 0.8789 before there was a downside correction. There was a move below the 23.6% Fib retracement level of the upward move from the 0.8702 swing low to the 0.8790 high.

However, the pair is stable above 0.8750 and the 50% Fib retracement. Besides, there is a connecting bullish trend line forming with support at 0.8755.

A downside break below 0.8755 might call for more downsides. In the stated case, the pair could drop toward 0.8745. Any more losses might call for an extended drop toward the 0.8730 pivot zone.

If there is another increase, the EUR/GBP chart suggests that the pair is facing hurdles near 0.8775. A close above 0.8775 might accelerate gains. In the stated case, the bulls may perhaps aim for a test of 0.8800. Any more gains might send the pair to 0.8840.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

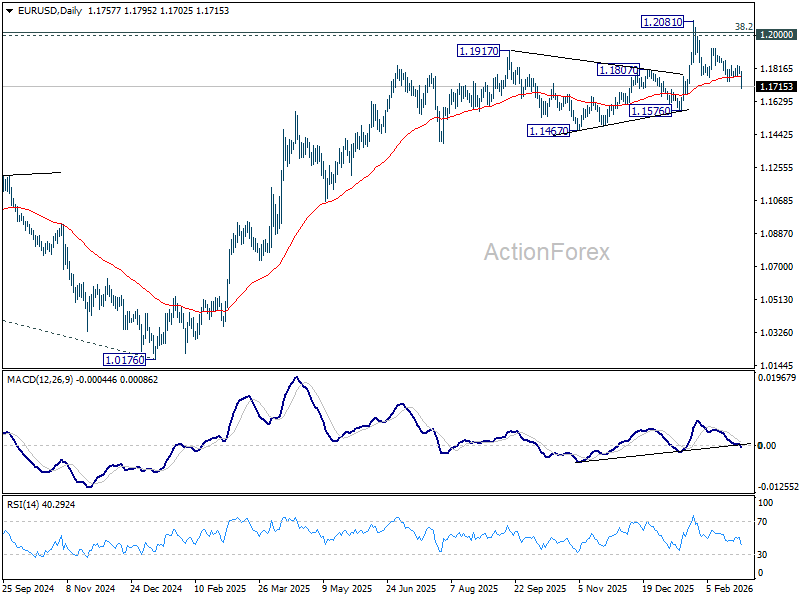

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1796; (P) 1.1812; (R1) 1.1834; More….

EUR/USD's fall from 1.2081 resumed by breaking through 1.1740 temporary low. Intraday bias is back on the downside for 1.1576 structural support. Firm break there should confirm rejection by 1.2 key psychological level and turn near term outlook bearish. For now, risk will stay on the downside as long as 1.1826 resistance holds, in case of recovery.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

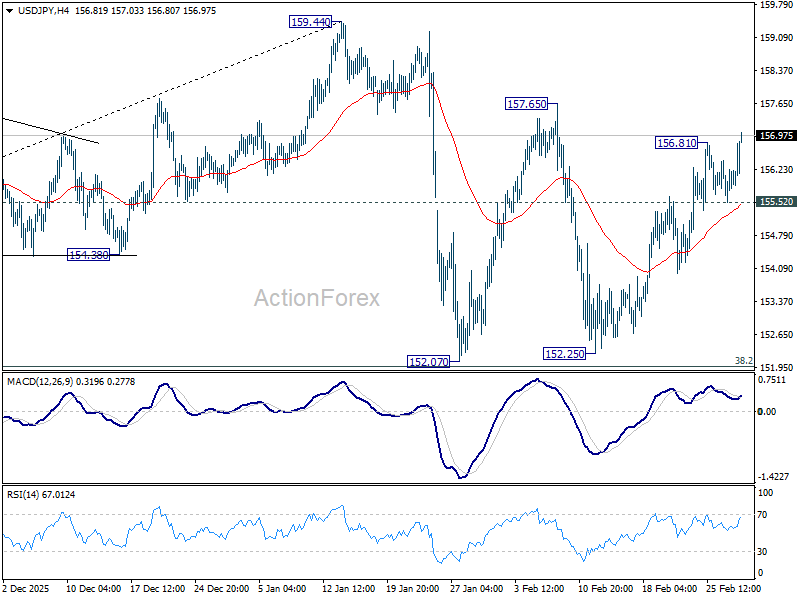

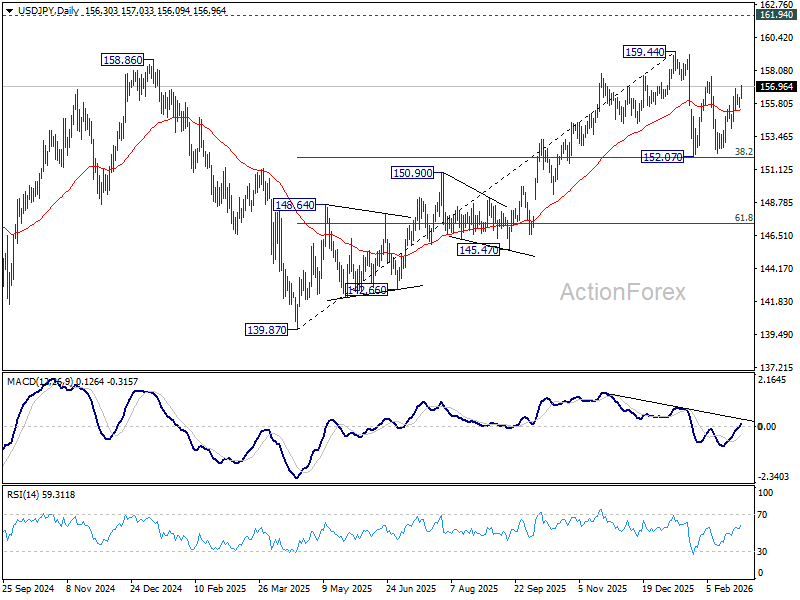

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.66; (P) 155.95; (R1) 156.36; More...

USD/JPY's rally from 152.25 resumed by braking through 156.81 temporary top. Intraday bias is back on the upside for 157.65 resistance first. Firm break there will pave the way to retest 159.44 high. On the downside, below 155.52 minor support will turn intraday bias neutral. Overall, price actions from 159.44 are viewed as a near term consolidation pattern. Outlook will remain bullish as long as 38.2% retracement of 139.87 to 159.44 at 151.96 holds.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

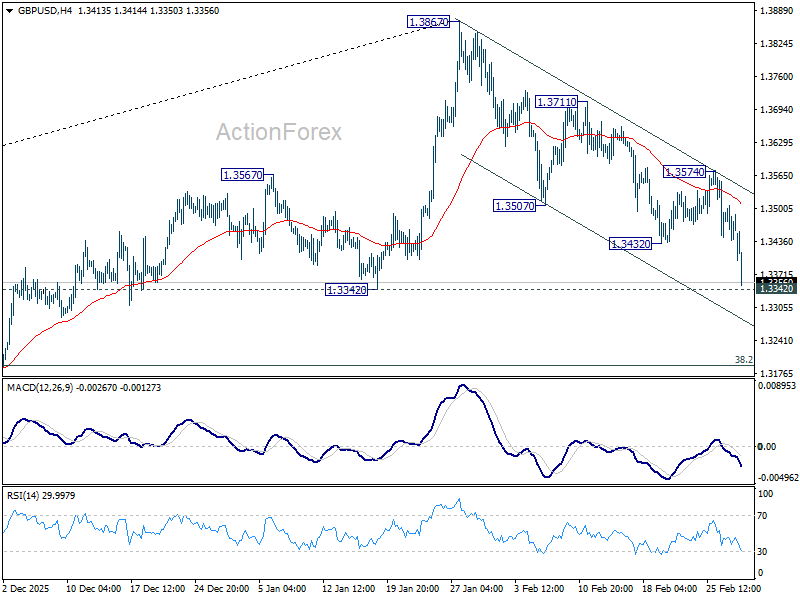

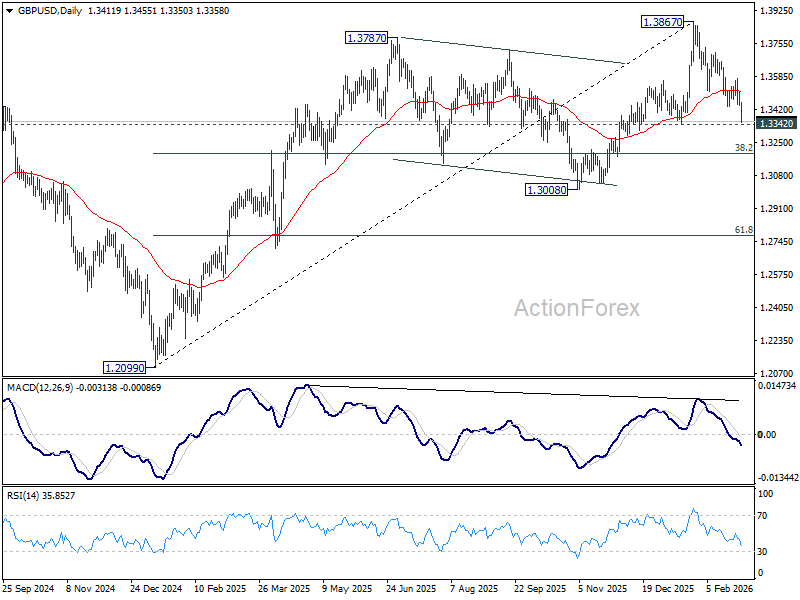

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3449; (P) 1.3478; (R1) 1.3517; More...

GBP/USD's decline from 1.3867 resumed by breaking through 1.3432 today, and intraday bias is back on the downside. Firm break of 1.3342 support should confirm that confirm that it's already correcting the whole rise from 1.2099. In this case, deeper fall should be seen to 1.3008 support next. For now, risk will stay on the downside as long as 1.3574 resistance holds, in case of recovery.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.

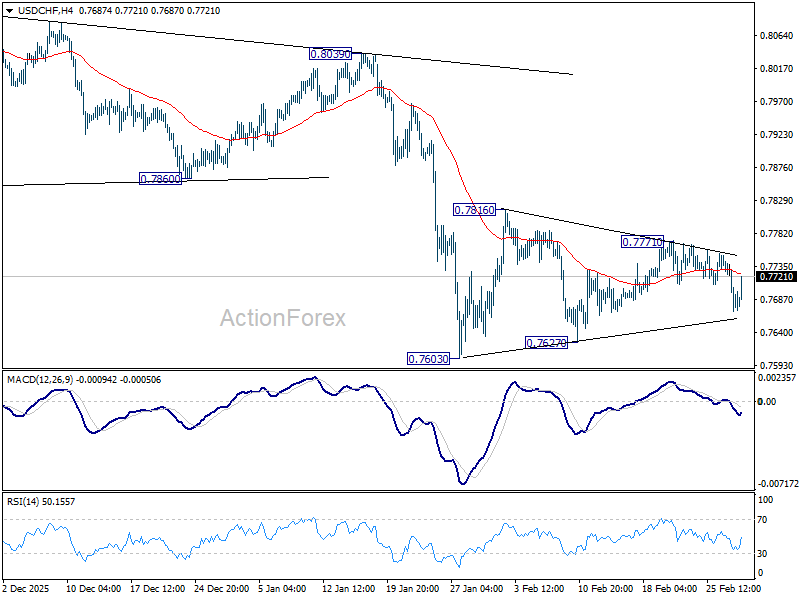

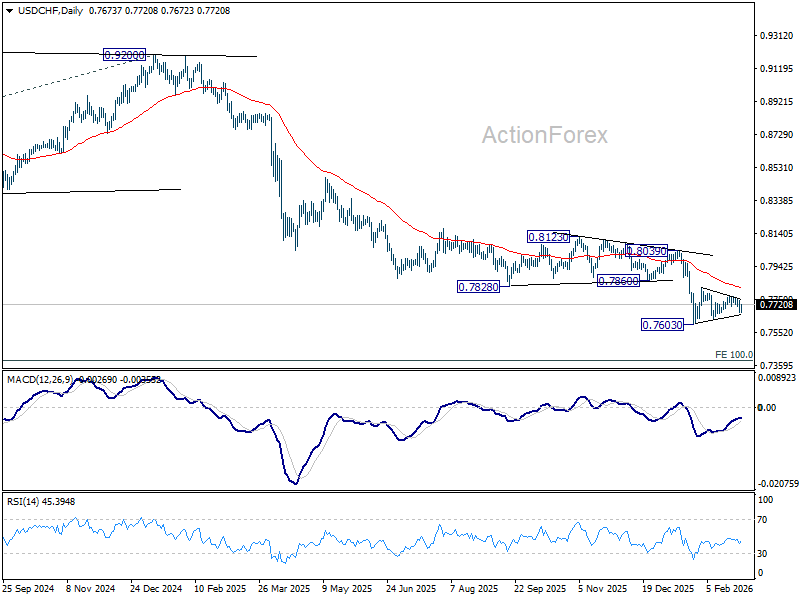

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7659; (P) 0.7705; (R1) 0.7737; More….

USD/CHF recovered today but stays in established range. Intraday bias remains neutral for the moment. In case of another rise, upside should be limited by 55 D EMA (now at 0.7816). On the downside, break of 0.7603 will resume larger down trend, and target 0.7382 projection level next. However, sustained break of 55 D EMA will indicate that a larger scale corrective bounce in underway and target 0.8039 resistance next.

In the bigger picture, down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8123 resistance holds.

Safe-Haven Demand Intensifies as US-Iran Conflict Extends – Gold, WTI Crude, Nikkei 225, AUD/USD Short-Term Outlook

Key takeaways

- Geopolitical shock fuels haven flows: Escalating US-Iran conflict and fears over a Strait of Hormuz disruption triggered a “haven first” reaction—gold surged, WTI spiked above $70, US equities and Asian indices fell, while the US dollar firmed.

- Gold and oil in bullish breakouts: Gold maintains a short-term uptrend above $5,238 with scope toward $5,448/$5,602, while WTI crude has broken above major 30-month resistance at $70, opening upside toward $74.70–$78.10 unless $67.80 gives way.

- Equities pressured, AUD resilient: The Nikkei 225 risks a deeper correction below 57,140, while AUD/USD holds above 0.7030/0.7020 support, supported by strong commodities, with 0.7140 as the upside trigger.

The US, in collaboration with Israel, has launched an attack on Iran on Saturday, 28 February 2026, despite an attempt by Oman mediators to extend “diplomacy measures” for another round of negotiation talks over Iran’s nuclear stockpile.

The past 48 hours have seen a flurry of attacks from both sides, with Iran’s retaliation bombardments on US military assets spread across the Middle East in the United Arab Emirates, Kuwait, Bahrain, Qatar, Saudi Arabia, Jordan, and Oman.

The latest US-Iran conflict is likely not going to be a “symbolic attack” akin to last summer, as US President Trump said the US military will continue bombing Iran until his objectives are achieved, despite the confirmed death of Iran's supreme leader, Ayatollah Ali Khamenei.

In today’s Asia session, market participants are generally adopting the strategy of “haven first, ask questions later” amid heightened concerns about the potential closure of the Strait of Hormuz by Iran, a key chokepoint for global oil flows, which can trigger an upward spiral in oil prices.

Here are the intraday performances of key asset classes at the time of writing:

- S&P 500 and Nasdaq 100 futures down around 0.9%

- Japan’s Nikkei 225 down 1.5%

- Hong Kong’s Hang Seng Index down 1.4%

- West Texas crude oil up 6% to around $71.40 per barrel

- Gold (XAU/USD) up 1.6% to around $5,360 per oz

- US Dollar Index up 0.3%

- Japanese yen down 0.5% to 156.80 per dollar

- Swiss franc almost unchanged at 0.7690 per dollar

- Bitcoin (BTC/USD) up 1.7% to around 66,880

Let’s look at the short-term technical outlook and key levels on Gold (XAU/USD), WTI crude oil, Nikkei 225, and AUD/USD.

Gold (XAU/USD) – Short-term uptrend remains intact above $5,238

Fig. 1: Gold (XAU/USD) minor trend as of 2 Mar 2026 (Source: TradingView)

Price actions of Gold (XAU/USD) continue to oscillate within a minor ascending channel since the 6 February 2026 low of $4,655. Watch the $5,238 key short-term pivotal support for a further potential extension for the next intermediate resistance to come in at $5,448 before a retest at the current all-time high of $5,602 printed on 29 January 2026 (see Fig. 1).

However, a break and an hourly close below $5,238 negates the bullish tone for a minor corrective pull-back to retest the next intermediate support zone at $5,111/5,046 (also the 20-day moving average).

WTI Oil – Bullish breakout above 30-month major resistance at $70/barrel

Fig. 2: West Texas Oil CFD minor trend as of 2 Mar 2026 (Source: TradingView)

The West Texas Oil CFD (a proxy of the WTI crude oil futures) has gapped up by 10% on Monday’s Asian opening hour to print an 8-month intraday high of $73.50/barrel before it pared back gains to around 6% to trade at $71.30.

Interestingly, today’s massive rally has triggered a major bullish breakout above its former 30-month major descending resistance from the 28 September 2023 high, which now turns into pull-back support at around $70.00/69.26 (see Fig. 2).

Watch the $67.80 key short-term pivotal support for the next intermediate resistances to come in at $74.70/75.55 and $78.10 (Fibonacci extension).

On the other hand, a break and an hourly close below $67.80 negates the bullish tone for another round of minor corrective pull-back to expose the next intermediate supports at $64.80 and $63.10/62.05 (also the area of the 50-day and 200-day moving averages).

Nikkei 225 – At risk of shaping a minor corrective decline, breaking below 57,140

Fig. 3: Japan 225 CFD index minor trend as of 2 Mar 2026 (Source: TradingView)

The Japan 225 CFD index (a proxy of the Nikkei 225 futures) has gapped down by 2.3% in today’s Asian opening hour and shaped a bearish reaction at the time of writing right at the former minor ascending support from the 6 February 2026 low, now turns pull-back resistance at around 58,125 (see Fig. 3).

Watch the 58,808 key short-term pivotal resistance, and a break below 57,140 (also the 20-day moving average) may trigger a further minor corrective decline to expose the next intermediate supports at 56,096 and 54,818.

On the flip side, a clearance above 58,808 invalidates the bearish tone to see a retest at the all-time high area of 59,884/60,075 in the first step.

AUD/USD – Holding above the 20-day moving average and 0.7035/7020 support

Fig. 4: AUD/USD minor trend as of 2 Mar 2026 (Source: TradingView)

The AUD/USD has managed to trim its intraday loss of 1% to 0.4% at the time of writing, supported by bullish commodities.

The intraday recovery seen in the AUD/USD has occurred right after the third retest on its 20-day moving average (see Fig. 4).

Watch the 0.7030/7020 key short-term pivotal support, and a clearance above 0.7140 may trigger another round of bullish impulsive up move sequences for the next intermediate resistances to come in at 0.7175 and 0.7210 (also a Fibonacci extension).

On the other hand, a break and an hourly close below 0.7020 invalidates the bullish tone for an extension of the minor corrective decline to expose the next supports at 0.6980 and 0.6905/6890 (also the 50-day moving average).

Middle East Erupts

The weekend was marked by tensions between the US, Israel, and Iran, leading to hundreds of explosions targeting broader Middle East countries as well, including the UAE, Saudi Arabia, Qatar, Bahrain and Kuwait. The flare-up was predictable; markets had been preparing for weeks as US warships advanced to the region preceding the explosions. Yet the events had an immediate effect, sending oil and gas prices higher at the weekly opening bell — casting a shadow over OPEC’s Sunday announcement that the group will accelerate output increases to 206’000 barrels per day in April.

Alas, the disruption of global oil flows due to Middle East tensions dwarfs that number, especially as there are warnings about OPEC’s capacity to significantly increase output and to ship this oil to the market while the Strait of Hormuz — partly controlled by Iran — is now effectively closed.

About 20% of global oil flows transit the Strait of Hormuz, 45% of energy exports are destined for China, more than 80% of LNG exports head toward Asia, and around 30% of Australian refined oil passes through the Strait. Al Jazeera reported yesterday that these developments could remove up to 17 billion barrels of oil from the market — roughly 5.5 months of global crude demand. It’s massive.

No wonder US crude jumped more than 10%, past $75 per barrel at the open, Brent hit $78, and natural gas prices also came under upward pressure. With the initial shock behind, prices are retreating somewhat as investors readjust risk calculations and consider that global oil reserves could cushion part of the disruption — at least temporarily. Also, nearly 70% of global oil production comes from outside the Middle East and does not need to transit the Strait of Hormuz. US shale — which accounts for about 60–70% of US oil production, and more than 20% of global oil supply — could also help mitigate the impact.

But, of course, the longer tensions persist — and the wider they spread geographically — the greater and more durable the impact on energy prices. Recent news suggests that Iran is not ready to negotiate with the US, so for now, tensions appear set to continue. Some analysts already see oil prices rise above the $100pb mark.

Middle East tensions and the disruption to global oil flows could have ripple effects across global economies. Higher energy prices have a notable impact on inflation. Energy typically makes up around 8–10% of CPI baskets, but during major shocks, it can account for up to one-third to one-half of headline inflation — with indirect effects amplifying the impact further.

This, combined with the US PPI coming in significantly higher than expected last Friday, suggests that the last mile toward the Federal Reserve’s (Fed) 2% target could be even more complicated than previously anticipated. In Europe, a period of rising energy prices could compromise the recent easing of inflation below the European Central Bank’s (ECB) policy target. Given that growth in most regions is still recovering from pandemic, trade and geopolitical tensions, stagflation risks may reemerge depending on how long Middle East tensions last.

This morning, tensions are pushing capital toward safe-haven assets. Gold is flirting with $5’400 per ounce, the US dollar is broadly stronger against major peers, and the US 10-year yield slipped below 4% — already on Friday — due to a major selloff that hit bank stocks over rising stress regarding exposure to private credit risks. That first emerged after an aggressive selloff across software companies this year, topped by news that major lenders had exposure to a UK mortgage company under investigation for irregularities.

Beyond that, strong earnings from Big Tech companies failed to revive appetite in AI enablers, as investors remain uncomfortable with massive capex increasingly financed by debt. Escalating Middle East tensions could further affect Big Tech and software stocks via the inflation and rates channel.

Higher energy prices have a direct earnings impact: data centers are power-intensive, electricity costs rise with energy inputs, logistics and component transport become more expensive, and corporate customers may trim IT spending if energy squeezes margins.

A sustained oil spike could lift inflation expectations and bond yields, pressuring long-duration growth valuations by raising discount rates. That matters for companies like Nvidia, Microsoft, Apple, and Alphabet, whose multiples are sensitive to future revenues and real yields.

Over the latest tightening cycle, these companies managed to outperform thanks to AI enthusiasm. But we have probably hit a peak cycle in AI stocks, and a period of concern has emerged, especially regarding leveraged investments. While a large portion of AI capex is still funded through substantial operating cash flows, the fact that these firms are now issuing debt to finance extra infrastructure build-outs means that additional funding costs could rise in a higher-for-longer rate environment, marginally reducing financial flexibility.

Globally, the combination of higher energy costs, broader economic risks, potentially higher discount rates, and rising financing costs will likely weigh on equity valuations.

Appetite across global equities is limited today. The Chinese CSI 300 is surprisingly higher, but the Japanese Nikkei is down 1% at the time of writing, the Hang Seng Index is pushing below its 100-DMA with around a 2% loss, and US and European markets are set to open on a deeply negative note. Among US indices, tech-heavy Nasdaq futures are leading losses, while in Europe, the energy-sensitive DAX will probably see the biggest pressure.

Overall, this week was supposed to be focused on the latest US jobs figures and a few more earnings — primarily from Broadcom and Alibaba. But the geopolitical headlines are likely to be the biggest driver of prices during what promises to be a highly volatile week.

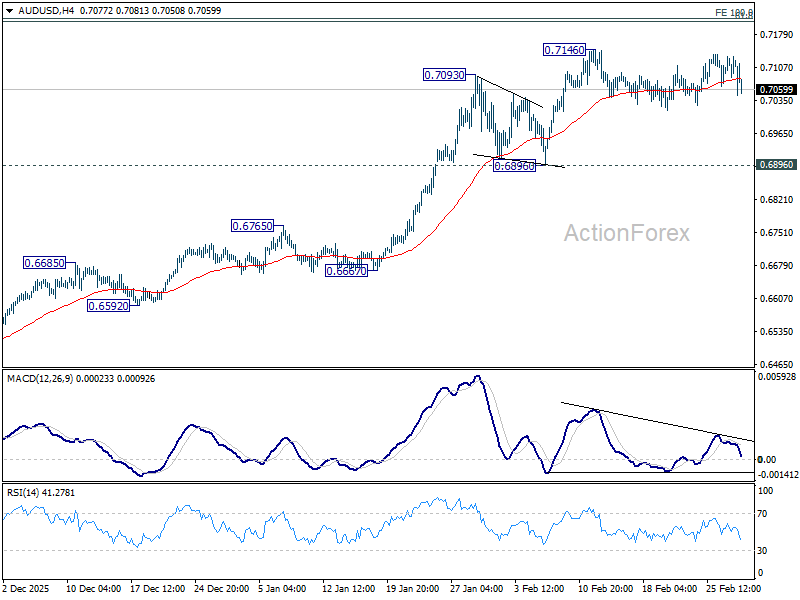

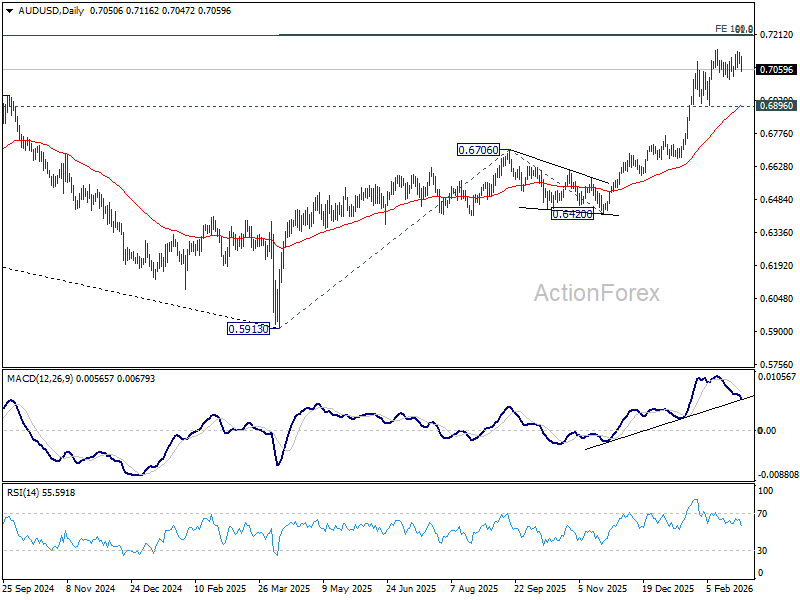

AUD/USD Daily Report

Daily Pivots: (S1) 0.7092; (P) 0.7112; (R1) 0.7137; More...

Range trading continues in AUD/USD and intraday bias stays neutral at this point. Further rise is expected with 0.6896 support intact. On the upside, firm break of 0.7146 will resume resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.

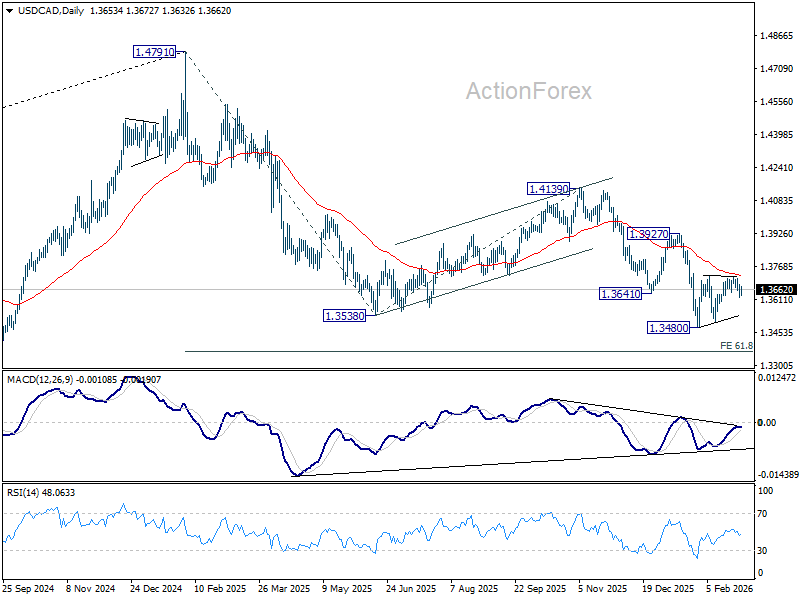

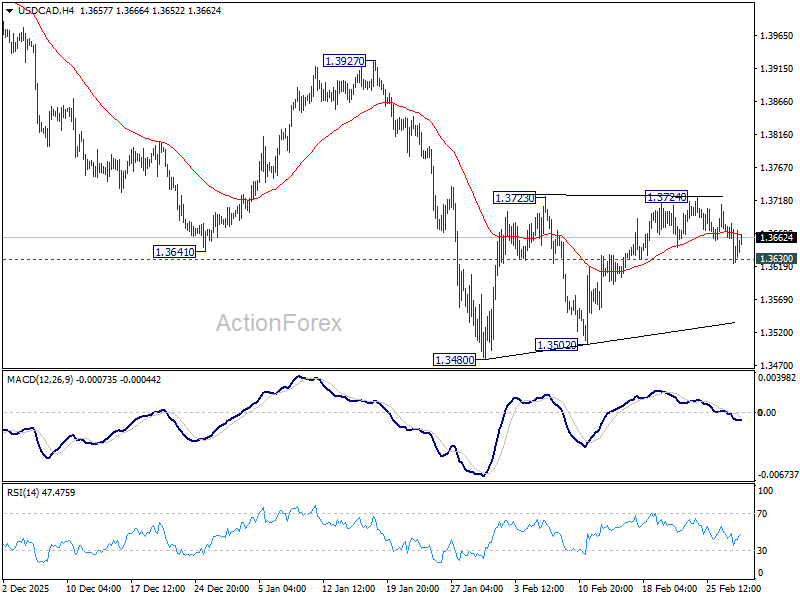

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3615; (P) 1.3652; (R1) 1.3678; More...

Intraday bias in USD/CAD remains neutral for the moment. Outlook is unchanged that price actions from 1.3480 are forming a consolidation pattern. Upside should be limited by 55 D EMA (now at 1.3725). On the downside, firm break of 1.3630 will bring retest of 1.3480 low first. Decisive break there will resume larger down trend 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. However, decisive break of 55 D EMA will bring stronger rebound to 1.3927 resistance instead.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.