Sample Category Title

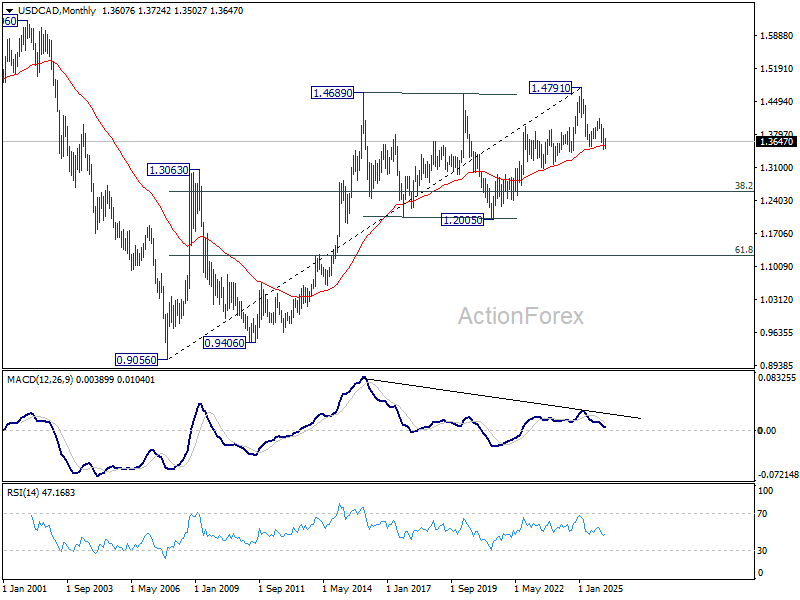

USD/CAD Weekly Outlook

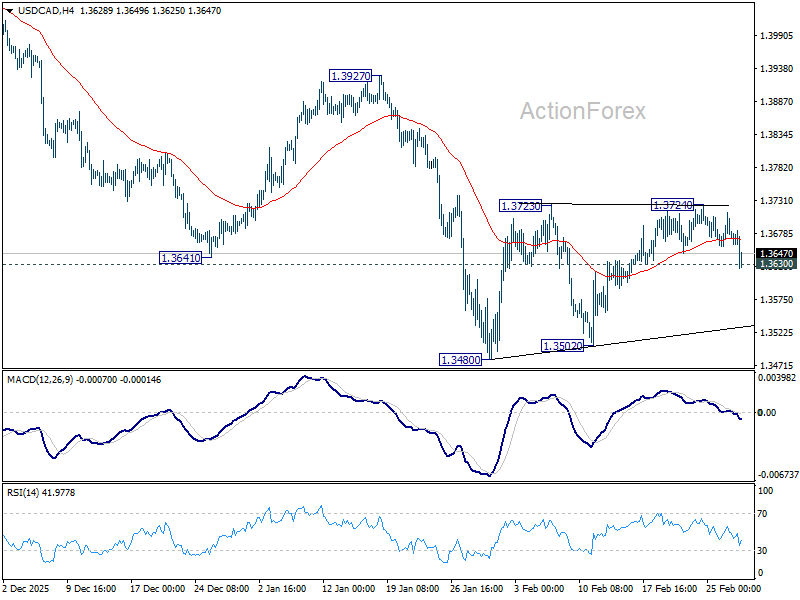

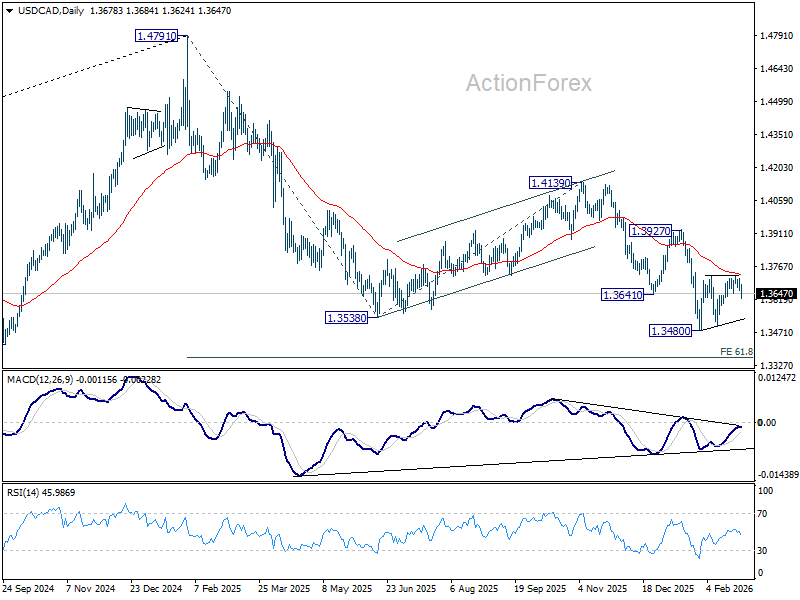

Despite the late dip in USD/CAD, it's still holding on to 1.3630 minor support. Initial bias stays neutral this week first. Outlook is unchanged that price actions from 1.3480 are forming a consolidation pattern. Upside should be limited by 55 D EMA (now at 1.3728). On the downside, firm break of 1.3630 will bring retest of 1.3480 low first. Decisive break there will resume larger down trend 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

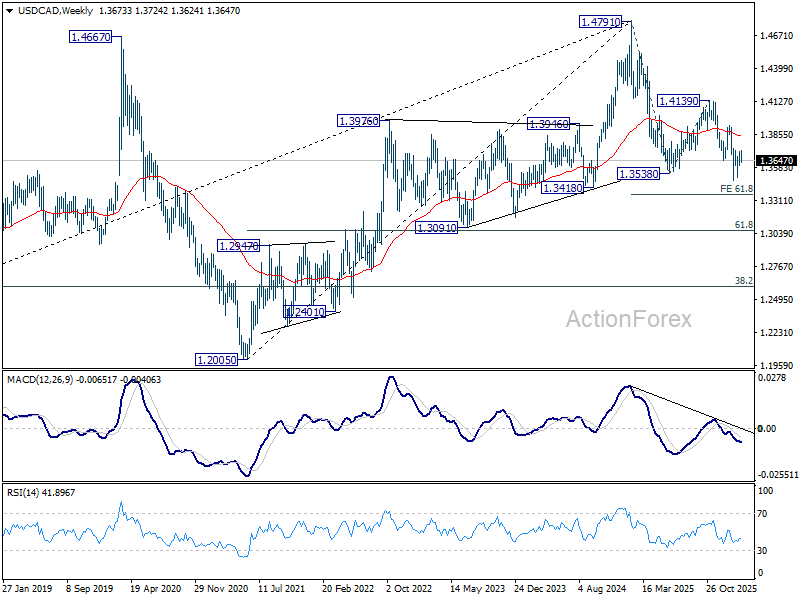

In the long term picture, rising 55 M EMA (now at 1.3569) remains intact. Thus, up trend from 0.9056 (2007 low) could still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

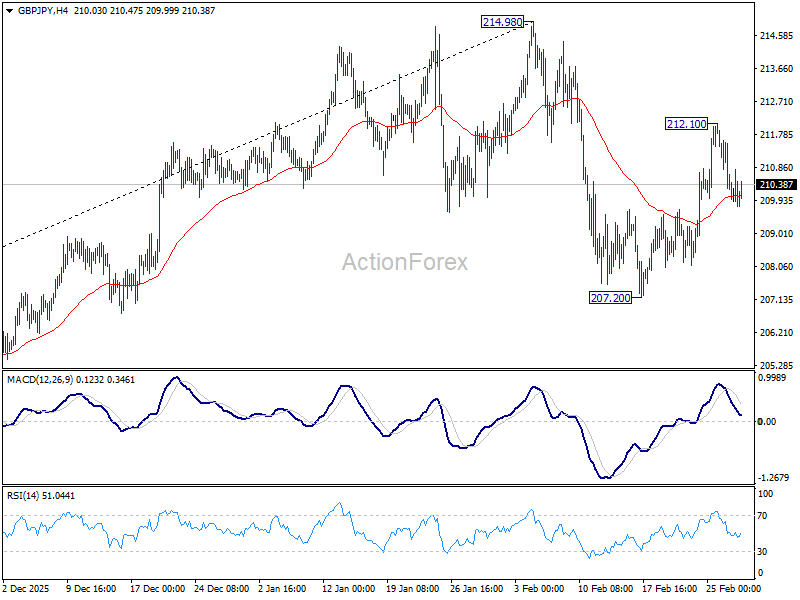

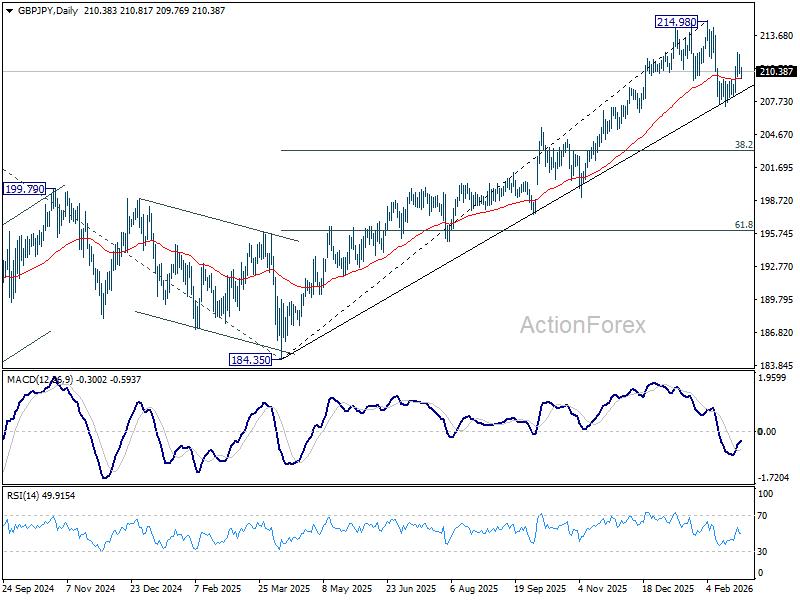

GBP/JPY Weekly Outlook

GBP/JPY's strong rebound last week suggests that corrective fall from 214.98 has completed at 207.20 already. But as a temporary top was formed at 212.10, initial bias remains neutral this week first. On the upside, above 212.10 will resume the rebound from 207.20 to retest 214.98 high. For now, risk will stay on the upside as long as 207.20 holds.

In the bigger picture, current development argues that price actions from 214.98 might be a near term consolidation pattern only. That is, larger up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, though, break of 207.20 will revive that case that it's already in a larger scale correction.

In the long term picture, up trend from 116.83 (2011 low) is in progress. Next target is 251.09 (2007 high). This will remain the favored case as long as 55 M EMA (now at 184.02) holds.

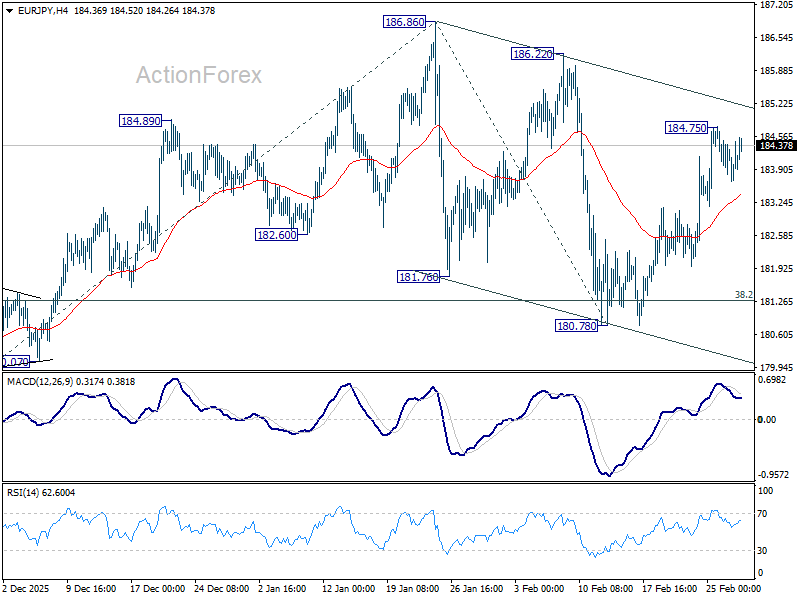

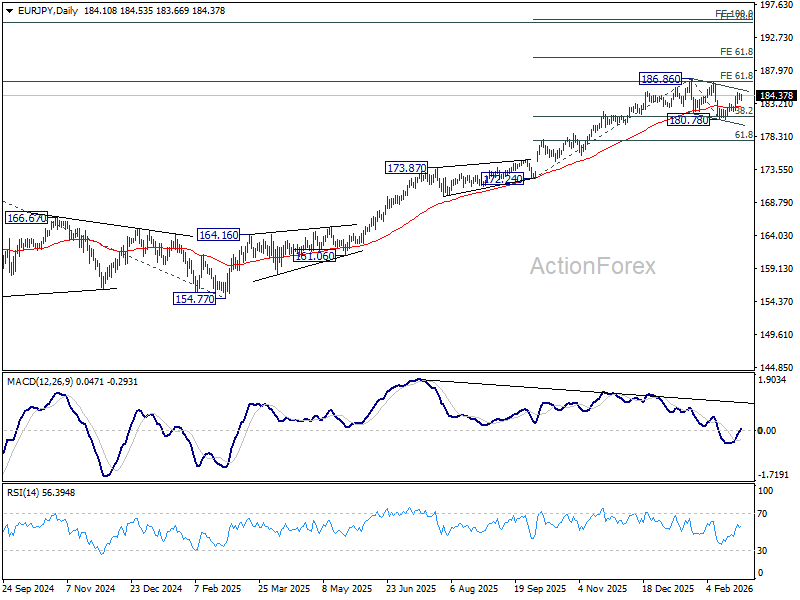

EUR/JPY Weekly Outlook

EUR/JPY's extended rise last suggests that correction from 186.86 has completed with three waves down to 180.78 already. But as a temporary top was formed at 184.75, initial bias remains neutral this week for consolidations first. On the upside, break of 184.75 will target 186.86 high. Firm break there will resume larger up trend to 61.8% projection of 172.24 to 186.86 from 180.78 at 189.81. Overall, outlook will remain bullish as long as 38.2% retracement of 172.24 to 186.86 at 181.27, in case of deep retreat.

In the bigger picture, current development suggests that price actions from 186.86 are merely a near term corrective pattern. In other words, the long term up trend is still in progress. Firm break of 186.86 will pave the way to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next. This will now remain the favored case as long as 180.78 support holds.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

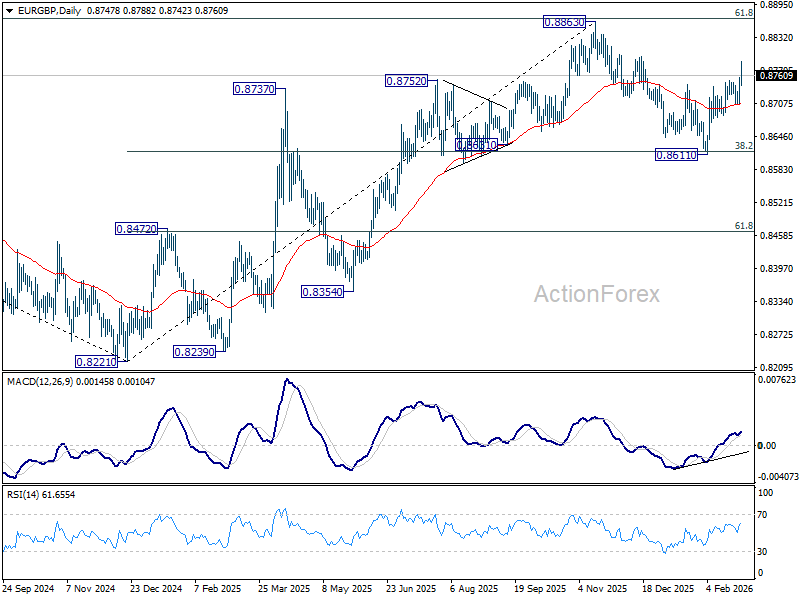

EUR/GBP Weekly Outlook

EUR/GBP's solid break of 0.8744 resistance last week suggests that corrective fall from 0.8863 has completed at 0.8611. More importantly, up trend from 0.8221 is not completed. Initial bias stays on the upside this week for retesting 0.8863 first. For now, further rally is expected as long as 0.8705 support holds, in case of retreat.

In the bigger picture, current development suggests that rise form 0.8221 medium term bottom is still in progress. Decisive break of 61.8% retracement of 0.9267 to 0.8221 at 0.8867 should confirm that it's reversing whole down trend from 0.9267. That should pave the way back to 0.9267.

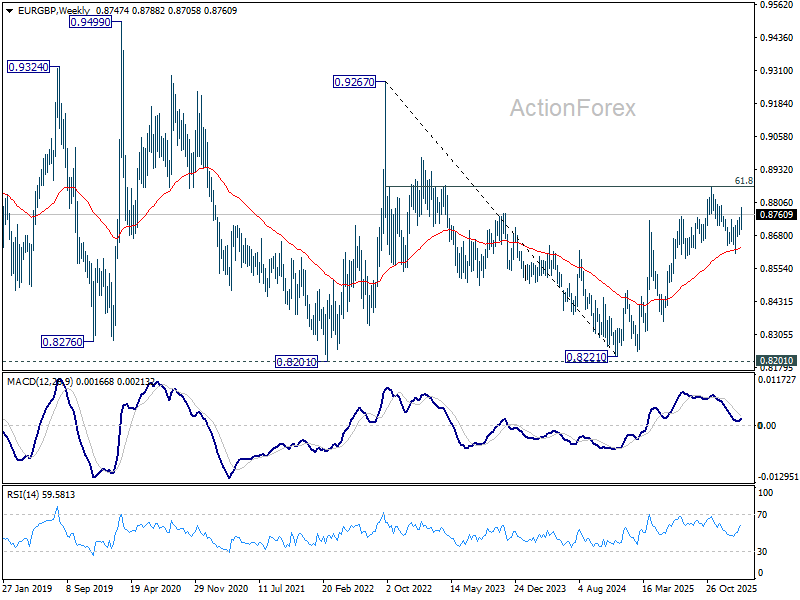

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

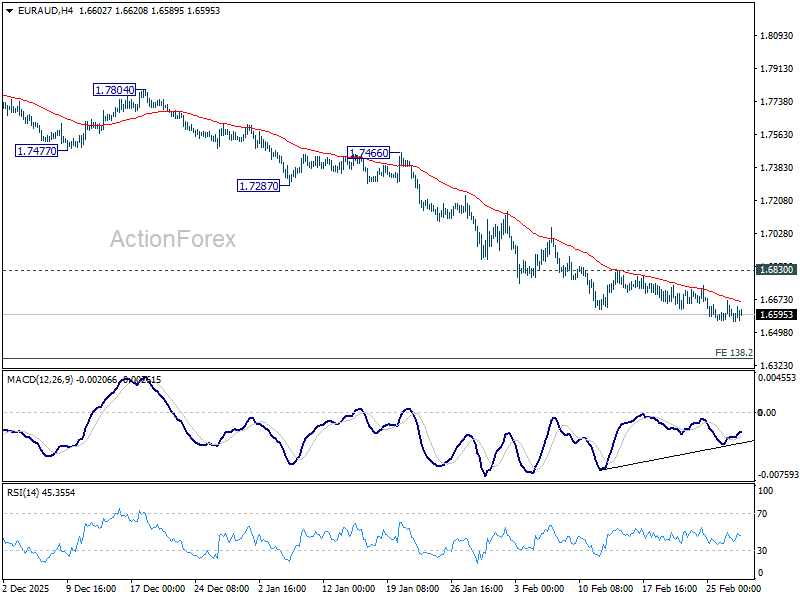

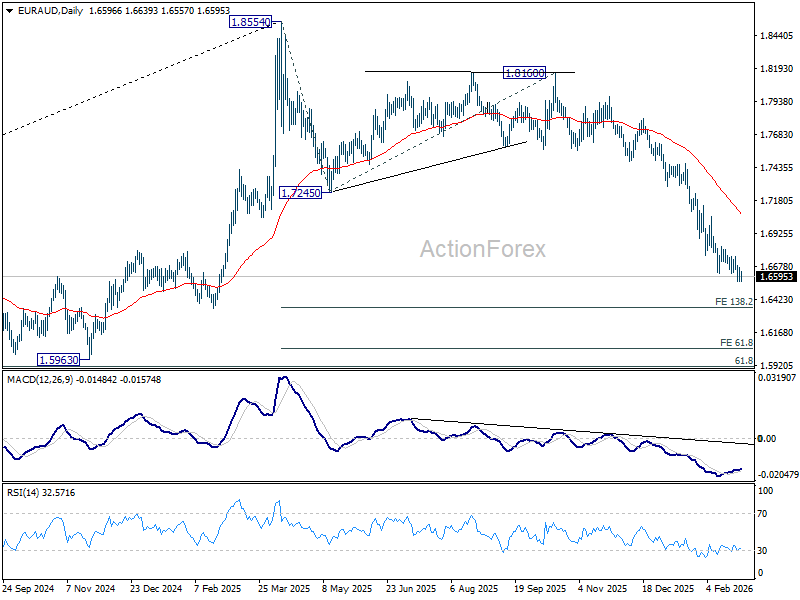

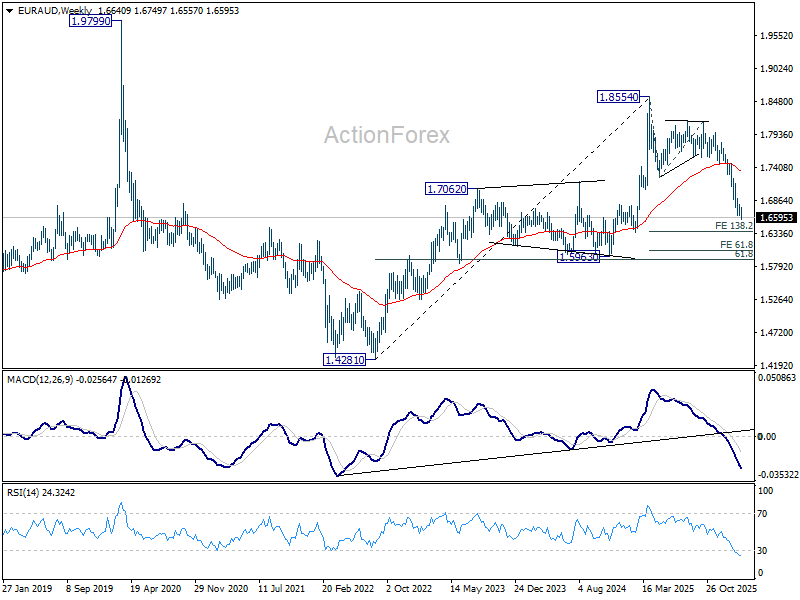

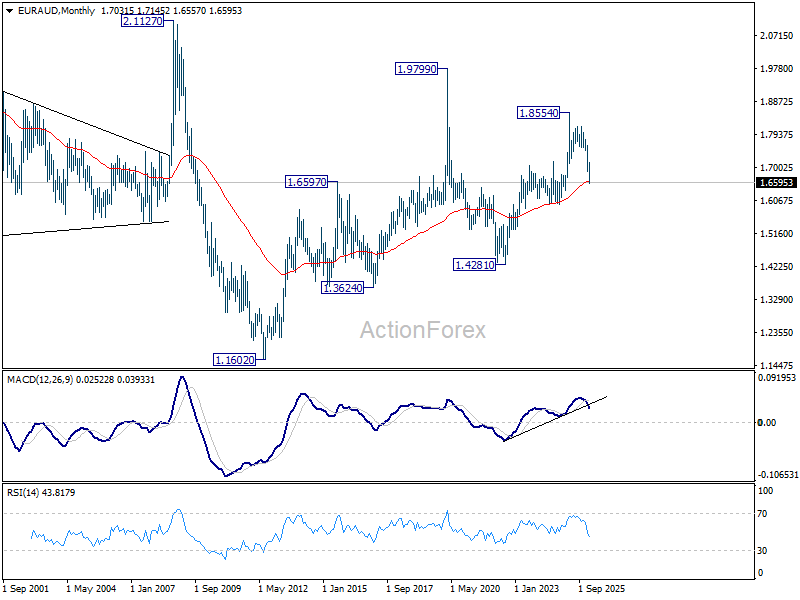

EUR/AUD Weekly Outlook

EUR/AUD's down trend resumed last week but downside momentum has been unconvincing with bullish convergence condition in 4H MACD. Still, there is no clear sign of bottoming yet. Further fall is expected this week to 138.2% projection of 1.8554 to 1.7245 from 1.8160 at 1.6351. However, firm break of 1.6830 resistance will confirm short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 1.8554 medium term top is seen as reversing the whole up trend from 1.4281 (2022 low). Deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. For now, risk will stay on the downside as long as 1.7245 support turned resistance holds, even in case of strong rebound.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). Current development argue that it has already completed at 1.8554. Sustained trading below 55 M EMA (now at 1.6603) will confirm this bearish case, and pave the way back towards 1.4281.

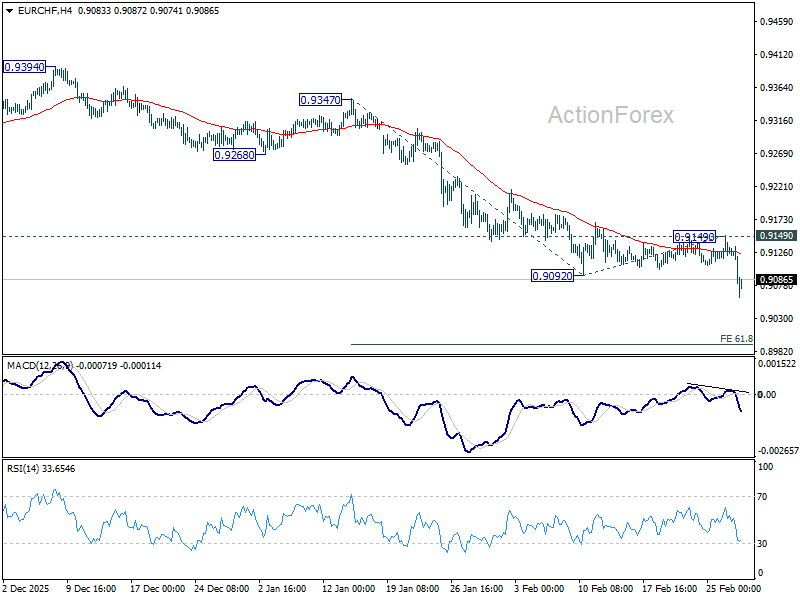

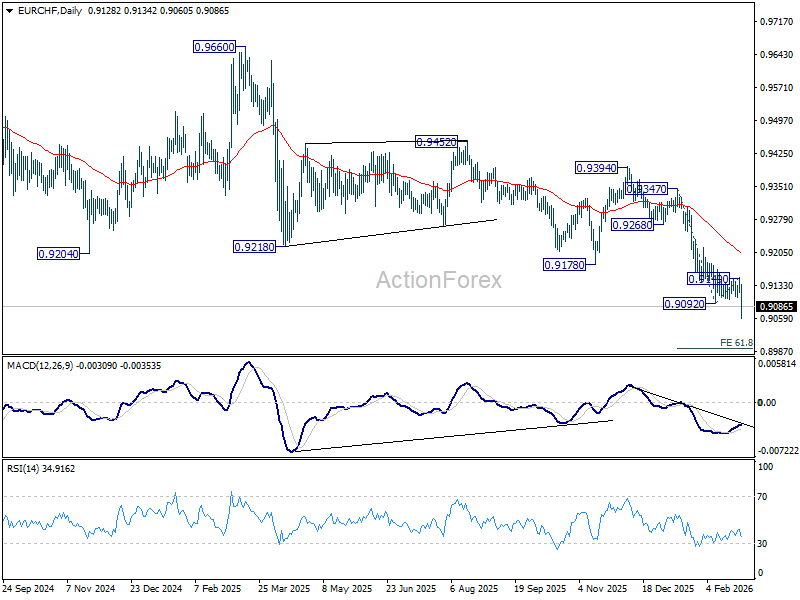

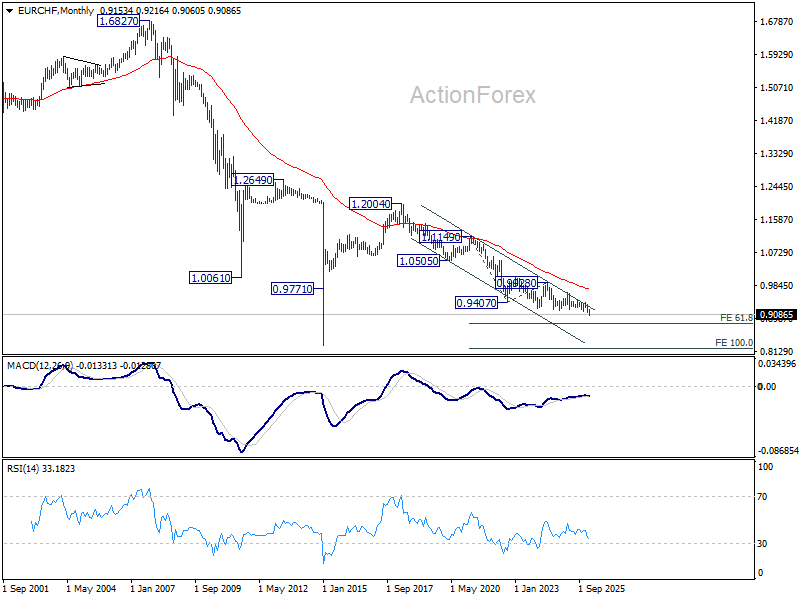

EUR/CHF Weekly Outlook

EUR/CHF's down trend resumed by late break of 0.9092 support last week. Initial bias is back on the downside. Next target is 61.8% projection of 0.9347 to 0.9092 from 0.9149 at 0.8991. For now, near term outlook will stay bearish as long as 0.9149 resistance holds, in case of recovery.

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of rebound.

In the long term picture, EUR/CHF is also holding well inside long term falling trend channel. Down trend from 1.2004 (2018 high) is still in progress. Outlook will continue to stay bearish as long as falling 55 M EMA (now at 0.9739) holds.

Credit Crunch Fears to Conclude a Temperamental Month; NFP Incoming – Markets Weekly Outlook

- Discover our Weekly Market Outlook, exploring themes and events that forged financial flows throughout the week.

- This week concludes a heavy February trading month, with a weighty week incoming right after.

- Get ready for next week's action by exploring upcoming events across global Markets.

Week in review – Markets remain very anxious, and they just found a new reason.

It seems traders will have to keep looking for reasons for volatility, as things won't settle anytime soon.

Since Kevin Warsh's nomination to head the Federal Reserve, Markets have been raging in brutal up-and-down swings.

Despite the harsh narratives, Stock Benchmarks remain near their all-time highs, and the immediate action looks more like a widespread rebalancing than a full-blown risk dump.

The most speculative assets have been slowly being tossed out since the October risk peaks, and this move is quickly translating into a newfound interest in quality (albeit not yet a real migration).

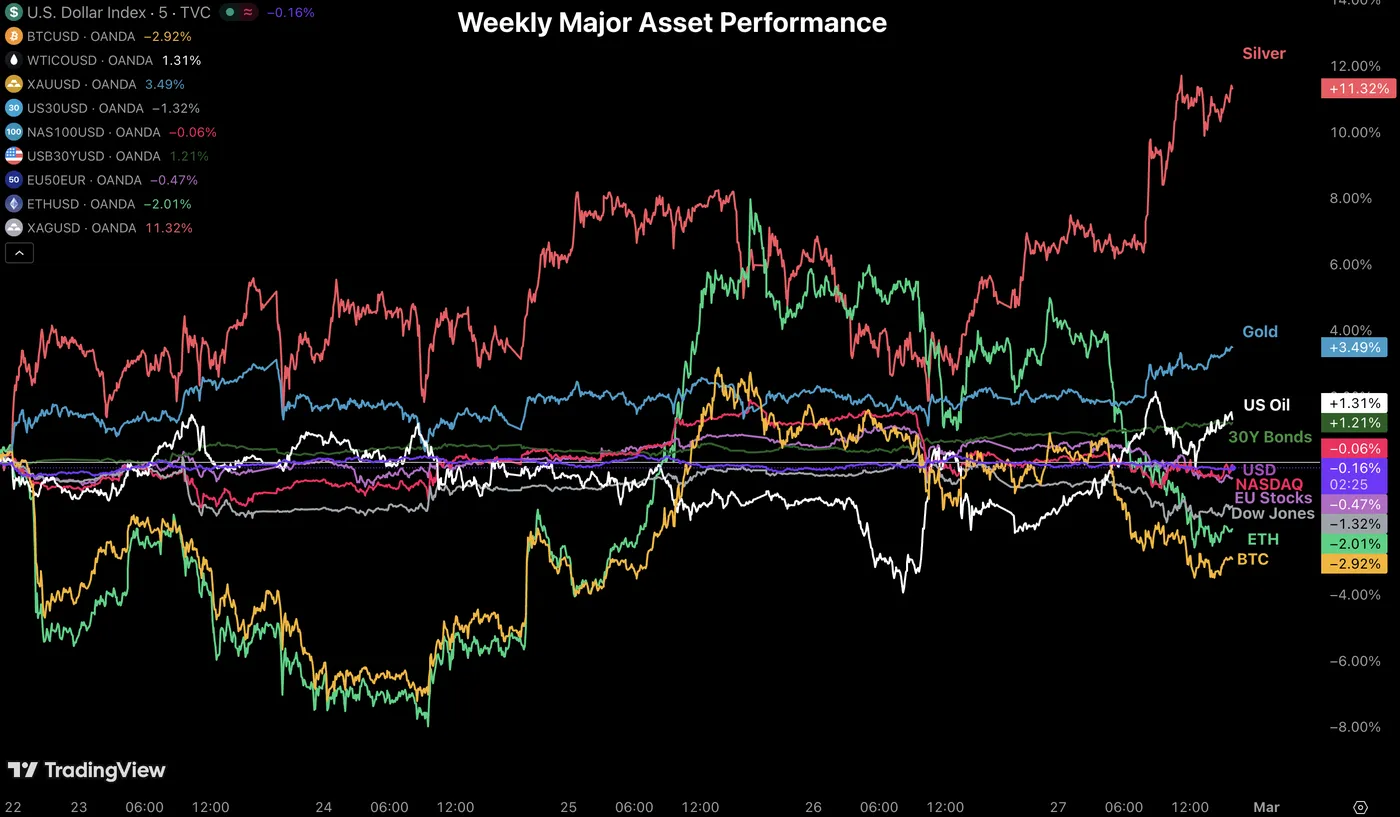

As some analysts call for a transition to the peak of the economic cycle, defensive assets and sectors are attracting attention. Bonds and Metals are actually the best performers this week.

1-month Performance Market Performance – Source: TradingView

After cryptocurrencies, tech/software, and semiconductors, a more concerning wave is gripping Financial Markets.

Waves of defaults among Private Equity and some of the most shaky tech companies are dragging down private lenders, Venture Capital firms, and some financials.

In case you forgot, this comes promptly after Credit Spreads reached new 2007 lows, and within not even a month, they are coming back to their December highs.

What could be concerning is how highly correlated the financial system has become since the Great Financial Crisis. Banks grew enormously, and it seems people quickly turned the page on the 2023 SVB blow-up, which raised questions about how large a credit spider web it has become.

Credit Spreads since mid-December – February 27, 2026 – Source: X, Bloomberg

In any case, the monthly picture is a scary one for Financials, and that's getting even more amplified today – Bank of America is down close to 4%, Goldman Sachs and Morgan Stanley are closer to -8%, but that's only the major banks.

Smaller lenders like Blackstone, Jefferies, and KKR & Co are down close to 30% on the month, and even Robinhood is suffering similar-sized drops. UBS is sending their own warnings and they're not pretty.

Current session in Banks – Source: CNBC – February 27, 2026

This will surely maintain more anxiety in the Markets. It's not that AI will lead to immediate spikes in layoffs; it's more about what happens to those who get replaced and how it spreads through the financial system at this point.

Weekly Performance across Asset Classes

Weekly Asset Performance – February 27, 2026 – Source: TradingView

Silver is calling and it wants its crown back!

The precious metal is closing well above its early February monthly highs as Metals caught a strong bid in today's action. These are preparations for something happening over the weekend.

The Week Ahead – NFP and PMIs all around the globe

Asia Pacific Markets – A condensed data package for APAC

Next week should be exiting for APAC traders. Without countic geopolitics, macro traders will await three PMI reports for China – There has been a surprising drop in the data as of late and the PBoC is talking about supporting their economy, not through Market-wide stimulus but with targeted assistance.

It will be interesting to see how it plays out in the data.

The Australian Dollar will once again be on the front-scene, between Inflation surveys, a speech from Governor Bullock, PMIs, Trade data and GDP.

It's going to be a very essential week for the 2026 FX leader – Let's see if it holds the test.

In Japan, traders will be listening closely to Governor Ueda's speech on Monday night. A hike could be coming towards mid-month for the Bank of Japan and he upped his tone recently regarding the possibility.

With two new decision-makers entering the Bank of Japan in the next months, it could be his last opportunity to build some form of consensus.

Europe and UK Markets – Eurozone and Swiss Inflation

The heavy slate of data also spreads to Europe with Inflation data (Consumer Prices and Producer Prices) releasing. Friday will also see the Yearly data for EU GDP, so keep this one in check.

But the largest culprit will be Swiss Inflation report, where traders should confirm whether negative rates will be a thing or not. A heavy test for FX markets.

North American Markets – More PMIs, but most importantly, Non-Farm Payrolls

Next week is going to be huge for North America. Without mentioning Iran, traders will receive a streak of PMIs from Canada and the US. A first round will come on Monday (Manufacturing) and the second will be on Wednesday (Services), along with the Beige Book (which had been a no-show but slowly getting interesting).

But Markets will have to await for the real Parade: Friday will release a Retail Sales and Non-Farm Payrolls double decker at 8:30 A.M..

Retail sales sent an honest shocker last month, missing by 0.5 percentage points, while Non-Farm Payrolls remained surprisingly strong – Make sure to not miss our incoming Previews.

Now, with a finally timely NFP, Participants shall see if this boost in employment really proves to be solid or just a seasonal one (with new year employment).

Even after the latest ease in narrative, keep a close eye on geopolitical developments, particularly those involving the US-Iran talks, as they are likely to continue influencing Commodity and broader Markets.

Next Week's High Tier Economic Events

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (High-tier data only)

Friday 27's Market Wrap

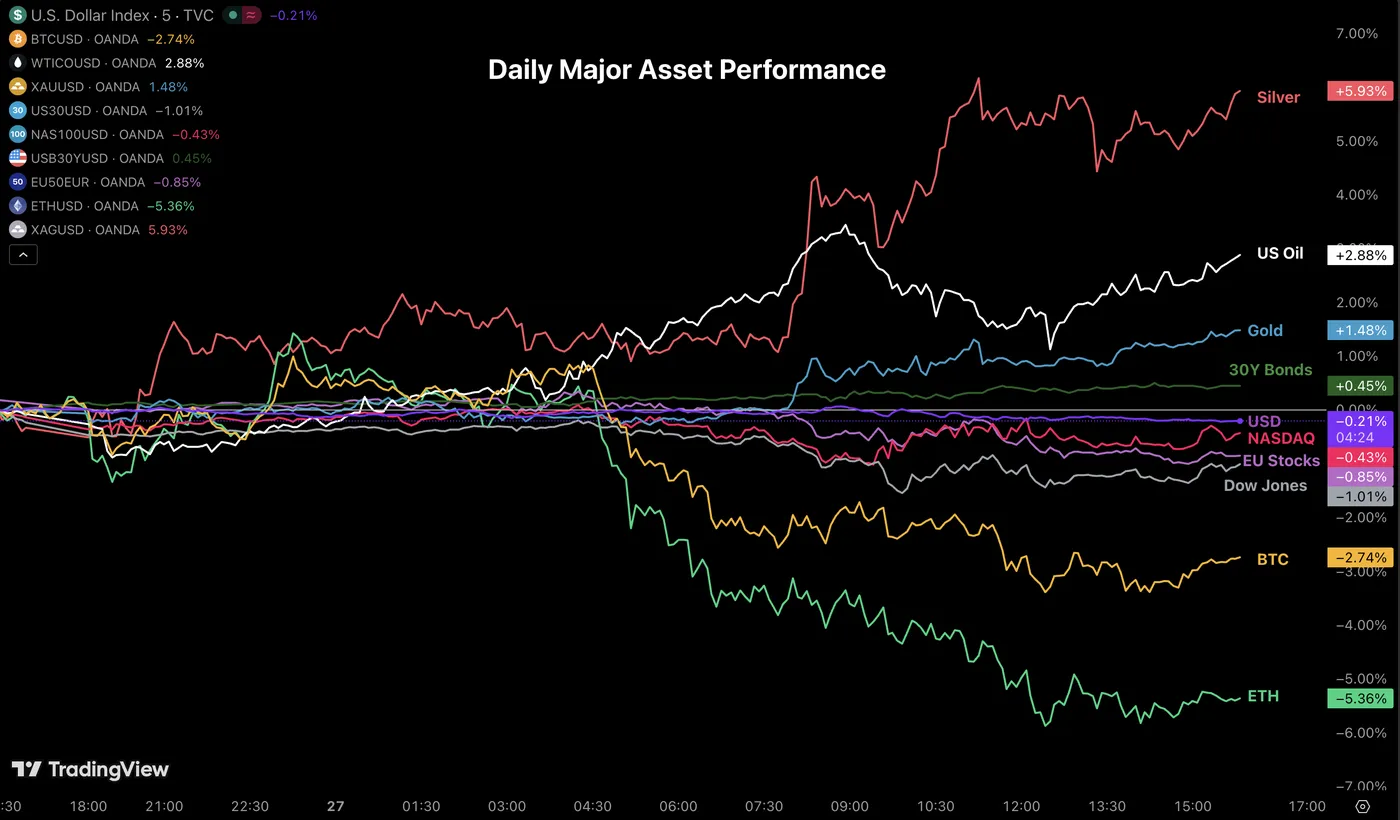

Cross-Asset Daily Performance, February 27, 2026 – Source: TradingView

Today's session really continued the past session's turn towards geopolitical hedges and a general turn towards quality.

As mentioned in the introduction, banks have seen bloodshed along with tech companies, and this comes right after the gigantic Nvidia earnings.

A very concerning picture for what's coming. Still, Stock markets are closing off-of their session lows, supported by calmer month-end flows in the afternoon.

The US Dollar is also surprisingly at the bottom of the FX board, victim of some heavy repositioning or month-end settling flows. The CHF leading isn't much surprising however.

Expect to hear about Iran this weekend. Stay safe everyone!

Safe Trades and enjoy your weekend!

The Weekly Bottom Line: Weak Q4 Headline GDP Number Masks Solid Domestic Demand

Canadian Highlights

- Capital spending intentions for 2026 flagged a pick-up in nominal private sector investment, alongside continued growth in the public sector.

- Canadian GDP contracted 0.6% annualized in the fourth quarter, thanks to an inventory draw down. Beneath the headline, domestic demand and net trade were much healthier.

- The solid details of the GDP report likely left the Bank of Canada comfortable with its current on-hold stance.

U.S. Highlights

- President Trump focused on tariffs and cost of living issues in his State of the Union Address.

- Consumer confidence edged higher in February on improved expectations, but views of current conditions weakened further as labor market pessimism persisted.

- Mortgage rates fell below 6% for the first time in over three years, offering modest support to the housing market.

Canada – Weak Q4 Headline GDP Number Masks Solid Domestic Demand

Financial markets were hit with a bevy of crosscurrents this week. In the bond market, Canadian yields declined alongside U.S. yields, as ongoing tariff uncertainty encouraged investors to seek the relative safety of U.S. bonds. Oil prices were volatile, affected by fluctuating perceptions of U.S.-Iran tensions as negotiators from both countries met. Oil was up for the month overall, which will upwardly pressure Canadian CPI inflation in February. Equity markets, meanwhile, were higher again this week, supported by bank earnings and commodity prices.

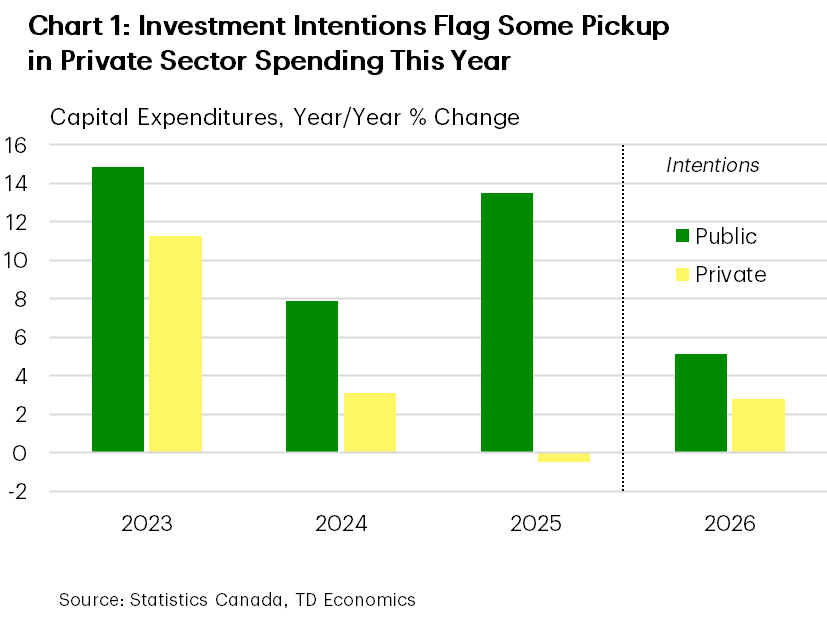

Data flow was mixed this week. Given the importance of business investment in forecasts for Canadian economic growth, we were eagerly anticipating this week’s release of the survey of capital spending for 2026. Last year, nominal non-residential spending on structures and machinery and equpiment increased about 5%. Economic uncertainty led to a pullback in private sector investment, although the public sector increased its investment spending significantly. Investment intentions for 2026 in the survey flagged another outperformance by the public sector. However, the picture is a bit brighter compared to last year for the private sector, where nominal investment is slated to advance 3% (Chart 1).

This week’s Survey of Employment, Payrolls and Hours offered a pulse-check on the jobs market in December. The report sent a much weaker signal than the earlier-released LFS jobs data, as payroll hiring was off 0.2% in the month while hours worked sagged.

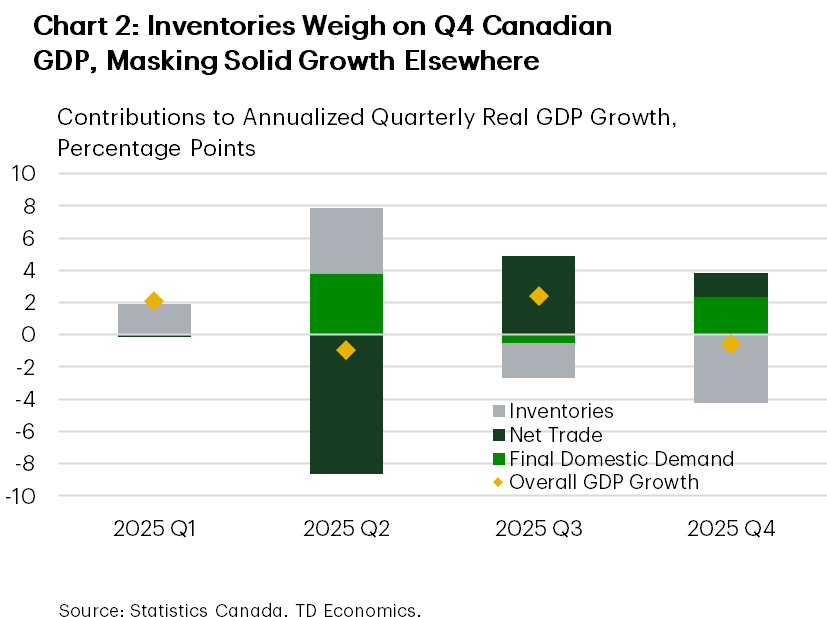

While these reports gave important signals on the economy, the marquee event this week was this morning’s release of Q4 Canadian GDP. Real GDP contracted by 0.6% annualized in Q4. The knee-jerk reaction of markets was to shift the odds slightly more towards a rate cut this year (though they’re assigning less than a 50% chance of one this year) on the headline number. But, peeling back the layers showed a better performance (Chart 2). For starters, inventories were the main growth drag, as final domestic demand was up a sturdy 2.4% annualized (stronger than our expectation) boosted by consumption growth and government spending. There was also a partial bounce-back in non-residential investment, consistent with the tone of the capital intentions survey. Net trade also contributed positively, driven by a solid gain in exports. Even the monthly, industry-based GDP for December was stronger than Statcan had previously guided.

If there was one blemish in the GDP report it was that output may have moderated in January, though even here, winter storms may have had a hand. Overall Canada’s economy felt the impact of U.S. tariffs in 2025. GDP growth slowed from 2% in 2024 to 1.7%, with Statistics Canada pointing out the slowdown was mainly due to weaker exports to the United States.

For the Bank of Canada, there was likely enough in the GDP report to leave them comfortable in their current hold stance, despite the weak headline figure.

U.S. – The State of the Union and the State of the Economy

This week’s economic calendar was light, with highlights including a modest rise in consumer confidence, a drop in mortgage rates, the State of the Union Address (SOTU), and ongoing trade policy uncertainty. In his SOTU, President Trump reaffirmed support for tariffs as a government revenue tool. The U.S. has imposed 10% duties on imports from all countries for 150 days under Section 122, pivoting quickly after last week’s Supreme Court decision striking down the administration’s use of tariffs under the International Emergency Economic Powers Act (IEEPA). The President subsequently threatened to raise the 10% blanket tariff to 15%, but no executive order has been signed.

Questions also remain about whether the $133 billion in IEEPA revenues—60% of total U.S. tariff revenue in 2025—will need to be refunded. The Court did not decide on this, so further litigation is likely. The potential revenue loss could push U.S. Treasury yields higher, as tariff revenue was expected to offset much of the One Big Beautiful Bill Act’s cost. However, markets appear unconcerned, either expecting the administration to find other ways to secure tariff funds or anticipating a lengthy litigation process. So far only a small fraction of importers has filed lawsuits for refunds.

Cost-of-living concerns were also addressed in the speech. The president noted that prices for some key goods have moderated, even as prices broadly continued to rise. He urged Congress to address healthcare costs and highlighted efforts to lower prescription drug prices. Housing affordability was mentioned, with a renewed call to restrict large institutional ownership of single-family homes. On that note, mortgage rates continued to ease this week. The average 30-year fixed rate fell to 5.98% on Thursday—the first sub-6% reading in over three years. Lower rates and a steady labor market should help boost home sales, but without broader affordability and supply improvements, a major turnaround in the housing market is unlikely.

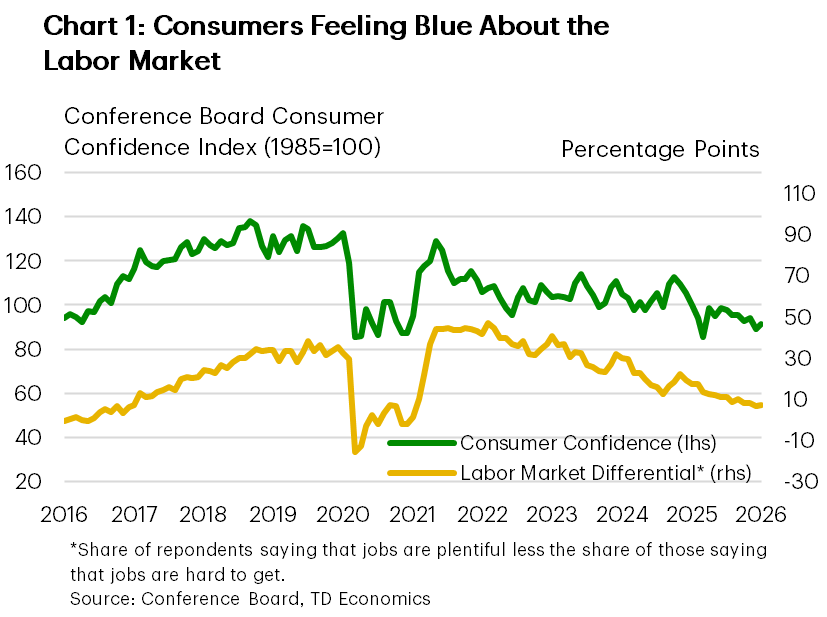

Cost-of-living worries and a slowing labor market remain top of mind for consumers. While consumer confidence index edged up in February, rising from 89.0 to 91.2, the gain was due entirely to improved expectations. Meanwhile, households’ views of current conditions softened further, with the present situation subcomponent declining to its lowest level since the pandemic, pointing to persistent pessimism about the job market. The gap between the share of households saying jobs are plentiful versus hard to get has been narrowing, weighing on confidence (Chart 1).

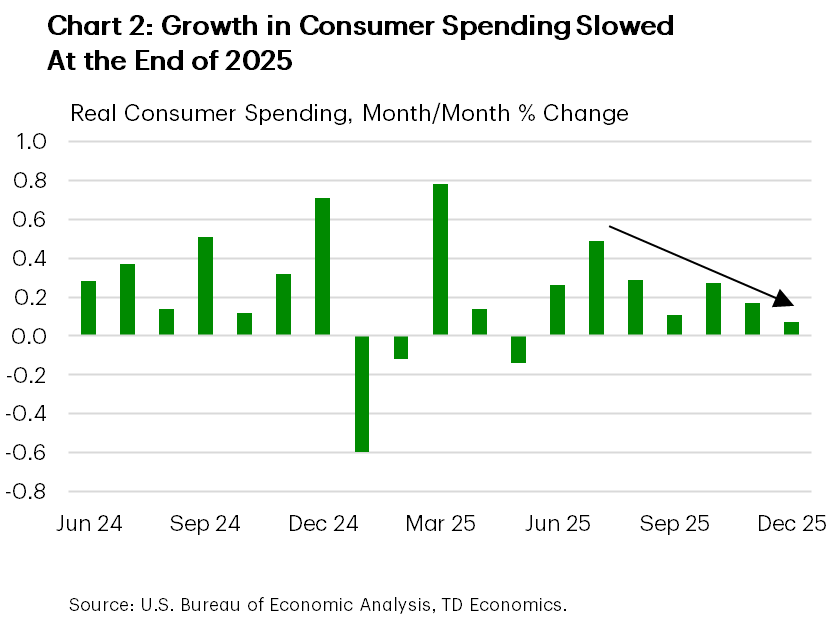

Consumer spending momentum faded at the end of last year (Chart 2), suggesting a weak handoff for Q1 and likely slower spending growth, before a possible Q2 pickup as higher tax refunds arrive. Next week, February’s jobs report should show labor market stabilization, while retail sales and ISM indexes will offer insights into consumer and business activity. We expect these indicators to show the economy continues to chug along despite the uncertainty, keeping the Fed on hold for now, especially with tariff policy in flux and inflation still above target.

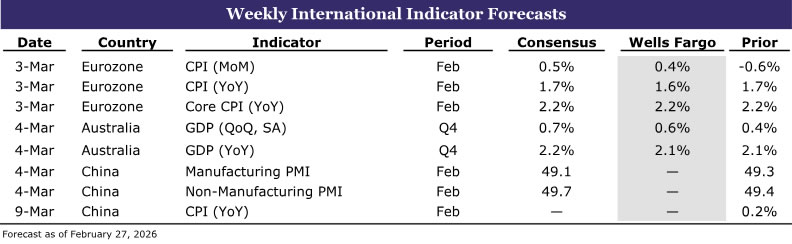

International Week Ahead: Broader Disinflation to Keep ECB Asymmetry for Rate Cuts

International Week Ahead

- Eurozone CPI: Disinflation to Keep ECB Asymmetry for Rate Cuts

- Australia GDP: Q4 Growth Recovery Expected, Driven by Consumption

- China PMIs: Contraction, but IEEPA Ruling May Cloud Takeaways

- China Inflation: Deflation Pressures to Remain Present

- China NPC and 15th Five-Year Plan: Significance Has Dwindled

G10

Eurozone February CPI • (03/03)

Broader Disinflation to Keep ECB Asymmetry for Rate Cuts

We expect preliminary readings for February CPI to come in at 0.4% month-over-month, below consensus at 0.5% (per Bloomberg). In terms of the year-over-year numbers, we expect headline inflation to decline to 1.6% from 1.7% and core to hold at 2.2%. Disinflationary pressures have broadened in recent months beyond energy prices and have encompassed both non-energy industrial goods (NEIG) and services. A stronger EUR, goods diversion from China and weak global demand has helped drive the softness in NEIG price inflation, whereas easing wage momentum has helped push services inflation lower. Although our baseline remains for the European Central Bank (ECB) to remain on hold, the asymmetry remains firmly tilted towards easing, in our view. The ECB appears comfortable with a slight undershoot of inflation vs. its target (ECB forecast of 1.9% and 1.8% for 2026 and 2027, respectively), however larger shortfalls are likely to bring rate cuts back on the table. Moreover, the ECB is likely to be sensitive to signs of weakness in growth and/or tightness in credit conditions. We continue to believe meaningful support from fiscal policy is not likely until 2027. On the flip side, upside risks to inflation have dissipated significantly absent a meaningful rebound in oil/gas prices.

Australia GDP • (03/04)

Q4 Growth Recovery Expected, Driven by Consumption

Australia’s growth likely strengthened at year-end after a softer Q3 print. While we and consensus expect a Q4 rebound, we see less upside, with GDP rising 0.6% quarter-over-quarter on a seasonally adjusted basis and 2.1% year-over-year (versus consensus expectations of 0.7% and 2.2%, respectively). Q3 GDP grew 0.4% quarter-over-quarter and 2.1% year-over-year, driven mainly by a 0.8% increase in private business investment led by a 7.6% rebound in machinery and equipment. That momentum appears to have faded, as recent capital expenditure data show machinery and equipment spending slowing, and while non-residential construction remained firm, overall business investment momentum likely softened. Consumption, which accounts for roughly half of GDP, was more resilient in Q4, with monthly household spending indicators pointing to stronger activity despite a weaker December, and should be the main growth driver as Reserve Bank of Australia (RBA) rate cuts continued to filter through the economy. As in Q3, net exports and inventories are likely to weigh on growth, with imports continuing to outpace exports and monthly trade data pointing to another drag. In terms of monetary policy implications, we remain comfortable with our base case of one additional rate hike in May, taking the Cash Rate to 4.10%, given still-elevated inflation. However, a weaker-than-expected Q4 growth outcome could likely cap the tightening cycle at a single hike and reduce the risk of further increases later this year.

EM

China Manufacturing & Non-Manufacturing PMI • (03/04)

Contraction Territory, but IEEPA Tariff Ruling May Cloud Takeaways

With most hard activity data delayed due to Lunar New Year celebrations, PMIs will be closely watched to gauge underlying economic sentiment in China. As of January, both the manufacturing and non-manufacturing PMIs are in contraction territory and expectations are for both sentiment indices to remain below 50 when February data are released. Historically, PMI data have been useful to gauge trend direction of China's economy. Below 50 prints are consistent with decelerating activity, and vice versa. But keep in mind, while February data may show both sectors in contraction, they both may not fully capture a lower effective tariff rate applied to Chinese exports headed for the U.S. after the U.S. Supreme Court's IEEPA tariff ruling. So while we will be paying attention to both, we will take each with a modest grain of salt. March PMIs next month will likely be more reflective of whether U.S. importers will rush to place orders in China as tariff rates are lower, especially with the Trump administration set to raise the baseline tariff to 15% in the coming weeks and possibly explore new country-specific tariffs through another legal avenues in the coming months. While we remain steadfast in our view that China's economy is riddled with structural imbalances that will pressure long-term growth rates, short-term growth prospects are holding up on exports with risks to our 4.7% 2026 GDP forecast tilted to the upside.

China Inflation • (03/09)

Weak Consumer Spending and Subdued Export Prices Keep Deflation Pressures Present

Deflation pressures are one of the structural deficiencies within China's economy, a challenge for short and long-term growth that should be on display when February CPI and PPI data are released next week. On the consumer side, subdued inflation is a product of weak consumer confidence and subdued domestic demand. We can point to a myriad of issues that contribute to soft consumer spending, but an unwillingness by Chinese policymakers to reflate the economy via monetary policy accommodation and fiscal support should mean soft consumer activity likely remains a theme for the foreseeable future. For producers, exporters are still trying to clear our excess inventory and still keeping export prices low. Export prices have come up a bit as authorities have pursued an anti-involution agenda, but we would not expect any significant changes to export prices nor PPI next month. Thematically, exporters may also look to keep prices permanently lower in an effort to maintain market share won last year. China now has ~22% of the global export market, up from ~17% at the end of 2024. How does China maintain market share? Pull-forward of external demand and front-running tariff hikes will help, but keeping prices low doesn't hurt either.

China National People's Congress and 15th Five-Year Plan • (03/05 – ~03/19)

Significance Has Dwindled and We Do Not Expect Anything Groundbreaking

The annual gathering of the National People's Congress (NPC) will start next week, yet will run over the course of the next two weeks. Typically, the NPC is a forum for implementing policy already decided and does not generate much in terms of surprises. We expect a similar result this year. But at least this year's NPC will be marked by the Chinese Communist Party (CCP) releasing its updated and 15th "Five-Year Plan" designed to offer insight into economic priorities, how the economy will be managed and economic goals for the next five years. In the past, Five-Year Plans were significant—especially during the Great Leap Forward years and the subsequent recovery and pursuit of a more market-driven economy under Deng. But more recently, Five-Year Plans have not offered much in terms of detail nor significant adjustments to how the CCP wants to evolve China's economy. For the 15th Plan, CCP members have already released a tentative summary of what the final Five-Year Plan will address. Long document, but skimming through suggests little in terms of surprises or significance. While we will pay attention, we anticipate headlines that sound material and economy-altering, particularly in the current tariff and trade backdrop, to amount to more of the same recent trends. We expect market participants to ultimately shrug off the Five-Year Plan and focus elsewhere going forward.

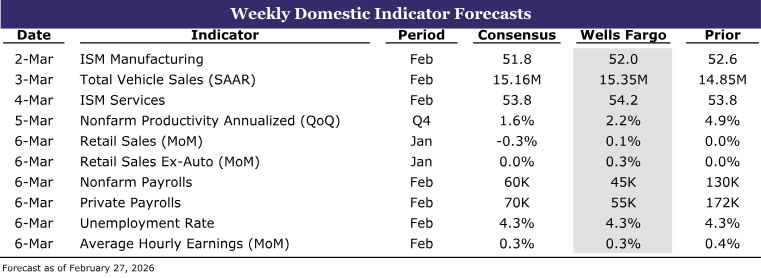

Weekly Economic & Financial Commentary: ISM Surveys, Employment, Retail Sales

Summary

U.S. Week in Review

- The economic data calendar was relatively light this week. However, the major indicators that were published showed that inflation pressures continue to percolate with few signs of the labor market exiting its soft patch. Meanwhile, the Fed communication channel provided comments underscoring the lack of consensus on which side of the Fed’s dual mandate demands the most attention, given still-elevated inflation and labor market risks.

U.S. Week Ahead

- Next week will bring some key readings on the economy's early year momentum. We look for the February ISM surveys to show a modest firming in services activity and that the factory sector is continuing to reemerge from the prior year's slump. Yet, the February employment report is likely to indicate that, while the labor market remains roughly in balance, job growth is struggling more than last month's jump in payrolls indicated. We believe the temperate labor market backdrop along with adverse winter weather led to a muted rise in January retail sales.

U.S. Week in Review

The economic data calendar was relatively light this week. However, the indicators that were published showed that inflation pressures continue to percolate with few signs of the labor market exiting its soft patch.

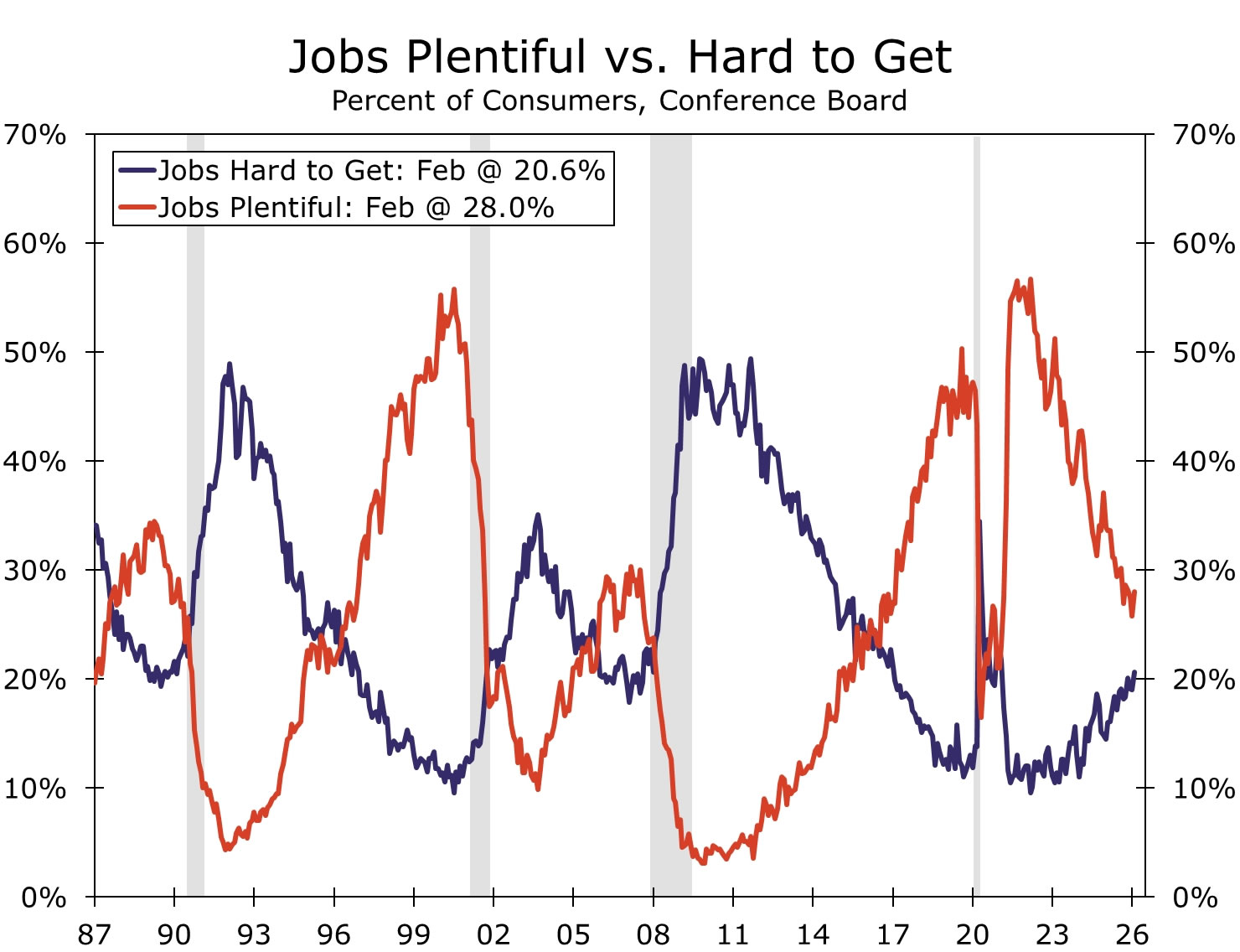

The soft labor market narrative was on display within the details of January’s consumer confidence print. Top-line consumer confidence is still bouncing around at the lower end of its past five-year range but came in a bit stronger than expected during January. The upside surprise was an encouraging development in that it suggests consumers are not feeling any worse about the current state of the economy. That said, the labor differential subcomponent, i.e., the difference between respondents saying “jobs are plentiful” and those saying “jobs are hard to get,” remains a glaring weak spot.

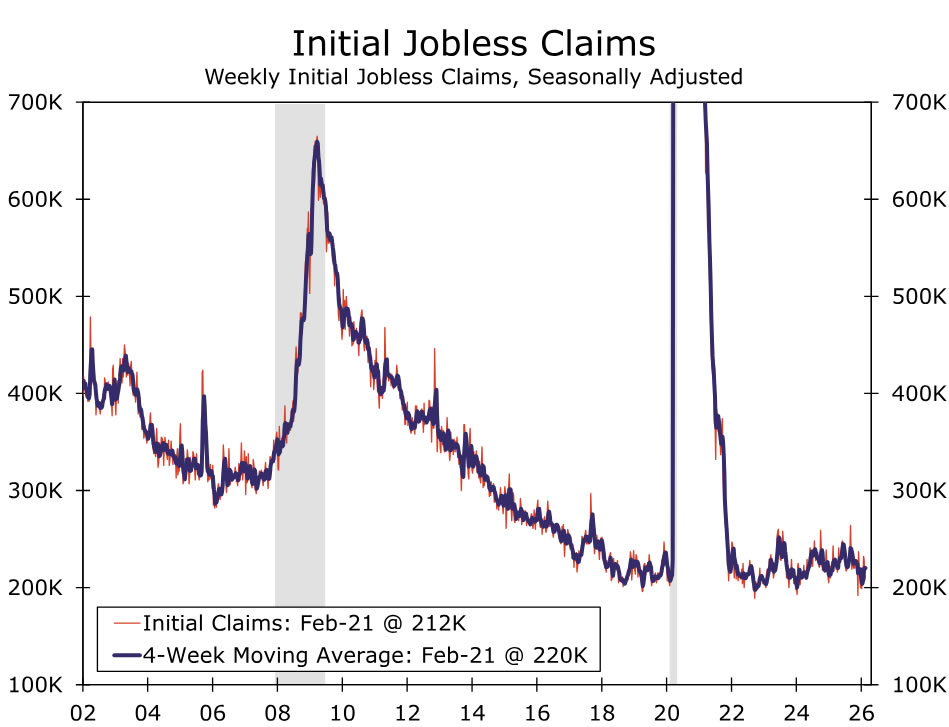

Breaking it down, just 28% of people think “jobs are plentiful,” up slightly during the month but still well off the recent cycle peak of over 50%. This suggests firms are still being cautious on adding to headcounts. But are they reducing payrolls in a material way? “Jobs hard to get” has averaged just 20% over the past several months, up from recent lows but hardly consistent with skyrocketing unemployment. In addition, initial jobless claims declined to 212K during the week ended Feb. 21, further evidence that overall unemployment is not surging higher. The message is that the labor market is currently lethargic, with very slow rates of new hiring. But deep and widespread layoffs (beyond a select few industries) do not appear to be happening either.

The thin flow of major indicators allowed plenty of time to parse through a full week of Fed speak. Generally speaking, the comments provided underscored that there is no clear consensus at the FOMC and among the regional bank presidents on which side of the Fed’s dual mandate demands the most attention. For example, Chicago Fed President Goolsbee stated “I remain optimistic that there can be more rate cuts this year. But that hinges on seeing actual progress on inflation that shows we are on a path back to 2%.” Governor Miran seemed more concerned about downside risks to employment, saying "I think it's way too early to sort of sound an all clear that the labor market doesn't need more support from the Federal Reserve” and “four cuts I think are appropriate and I’d rather get them sooner rather than later.”

However, comments from Governor Waller at the NABE policy conference in D.C. on Monday especially stood out to us. "If the labor market data for February are consistent with the stronger job creation and low unemployment rate initially reported in January, indicating that downside risks to the labor market have diminished, it may be appropriate to hold the FOMC's policy rate at current levels and watch for continued progress on inflation and strength in the labor market. But if the good labor market news of January is revised away or evaporates in February, it would support my position at the FOMC's last meeting, that a 25-basis-point reduction in the policy rate was appropriate, and that such a cut should be made at the March meeting. As things stand today, I rate these two possible outcomes as close to a coin flip."

In our view, January's "strong" employment growth may have been overstated and a more moderate payroll gain in February seems likely. For more on our nonfarm payroll forecast, please see below in our Outlook section. Nevertheless, labor market conditions do not appear to be deteriorating and look to have stabilized, albeit within a "low hire, low fire" context. Meanwhile, January's hotter-than-expected rise in both the headline and core Producer Price Index is the latest reminder that price pressures are still evident and that most inflation measures are still running above the FOMC's 2% target. From our standpoint, this lowers the likelihood of a March rate cut, though two additional 25 bps cuts later this year are still on the table, given still-present downside risks in the labor market.

U.S. Week Ahead

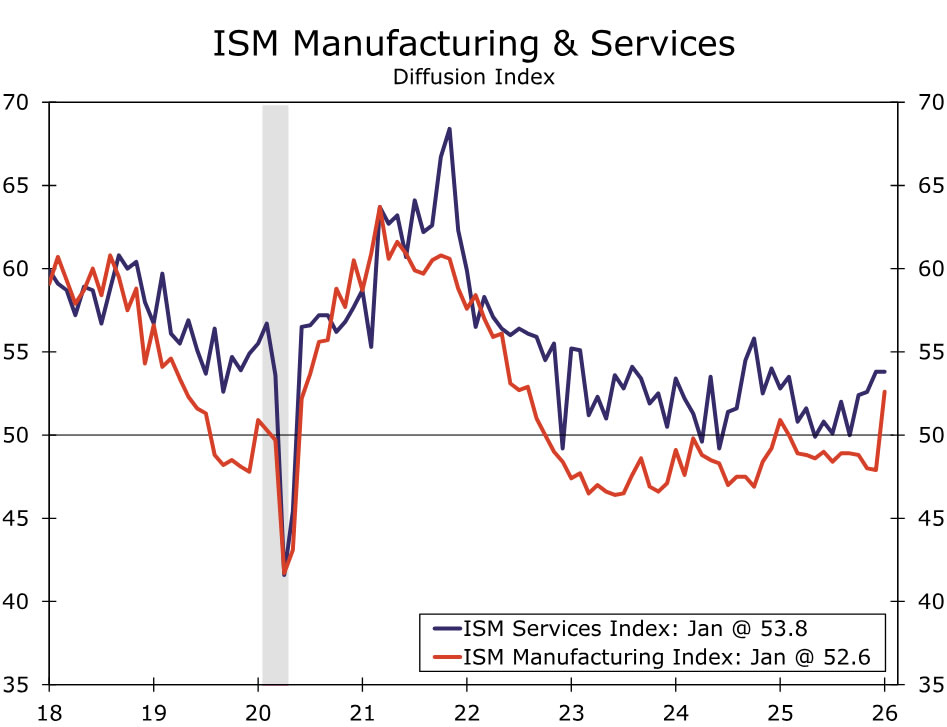

Monday & Wednesday • ISM Surveys

The ISM manufacturing index crossed into expansion territory in January for the first time in 10 months. The improvement comes amid an upswing in capital spending—highlighted by broadening in durable goods orders—as well as restocking efforts in the wake of last year's tariff hikes. We would not be surprised to see a little giveback in February following last month's leap, however, and estimate a February print of 52.0. The nearly 10-point jump in the new orders component in January overstates underlying momentum in the factory sector in our view. Regional PMIs for February show manufacturing activity continued to expand last month, but a more even-keeled pace.

Non-manufacturing activity continues to hold up better, as indicated by the ISM services index maintaining its 14-month high in January. Although firms remain cautious when it comes to hiring, business activity has been sturdy. We look for the February reading, due Wednesday, to edge up to 54.2.

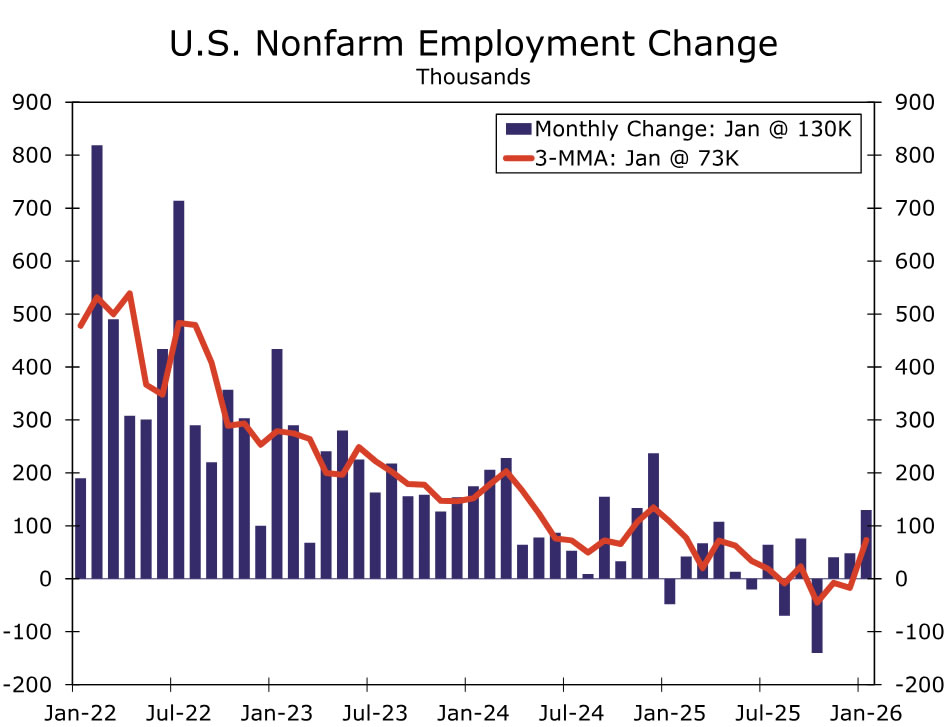

Friday • Employment

We expect the February employment report to show that January’s robust pace of payroll growth overstated underlying momentum in the labor market. While some stabilization in demand for workers is evident, a range of indicators, including JOLTS and consumers' perception of job availability, continue to point to a gradual loosening in labor market conditions rather than a renewed acceleration in hiring. We look for nonfarm payrolls to rise by 45K in February, with weakness in weather-sensitive industries like construction and leisure & hospitality and some payback in healthcare & social assistance after a significantly above-trend reading in January.

We estimate the unemployment rate held steady at 4.3% in February, but see two-sided risk to this call. The household survey's measure of employment growth has been running well ahead of its trend the past two months, leaving some scope for payback in February that could push the jobless rate up to 4.4%. However, the implementation of the household survey's annual population adjustment poses downside risks, given the shift in immigration trends last year. Ratios from the household survey such as the labor force participation rate and unemployment rate are less affected by the population control adjustments than level data, but can move slightly under meaningful changes in the composition of the population.

The roughly balanced labor market should lead to average hourly earnings advancing a trend-like 0.3% in February and 3.7% over the past year. For more information, please see our employment preview.

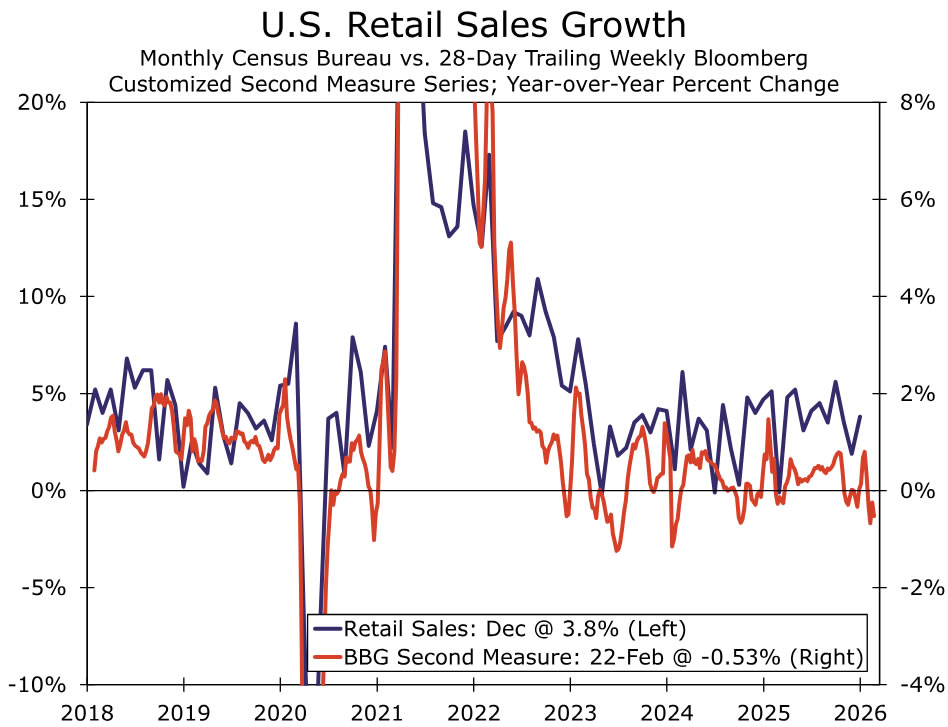

Friday • Retail Sales

The shutdown-delayed January retail sales report is expected to show spending got off to a modest start in 2026. A large winter storm across the central and eastern U.S. likely crimped activity, with auto sales in January already reported to have fallen to nearly a three-year low. Lower gasoline prices will also have weighed on sales, leading us to expect just a 0.1% increase in total retail sales last month.

Yet, consumers are still finding ways to spend despite the cooler jobs market leading to slower income growth and a dampened consumer mood. High-frequency credit card data showed some modest firming in spending in January, leading us to expect retail sales ex-autos rose 0.3% last month. We expect retail sales to show more signs of life in the coming months as larger tax refunds and stabilizing labor market conditions support more discretionary spending.