Sample Category Title

EUR/GBP Attacking Key 0.8745/50 Resistance Area

Markets

A dull start in Asian and European trading in the US gradually morphed in to a risk-off pattern. A lukewarm acceptance of strong Nvidia results apparently caused some vertigo, preventing especially US equity indices to go for a retest of the top levels reached end last month. The Dow closed little changed (-0.3%). The Nasdaq dropped 1.18%. Hesitance on US equity markets again directed a safe haven bid to US Treasuries. Treasury yields dropped between 5.3 bps (5-y) and 4 bps (30-y). Comforting (from a Fed point of view) US weekly jobless claims (212k) in this respect had no impact on the intraday dynamics on US interest rate markets. Especially US yields in the 2y-5y sector are now closing in on important support levels (October lows). The 10-y this morning is attacking the 4% barrier. EMU yield followed the US at a distance with German yields easing between 0.6 bp (2-y) and 2.2 bps (30-y), also in a bull flattening move. ECB’s Lagarde in a speech before the EU Parliament elaborating on still elevated consumer inflation expectations despite recent decline in (headline) inflation at least suggests that the bank is in no hurry to change is wait-and-see stance. Neither the risk-off nor the changes in interest rates (differentials) in the end had a big impact on the dollar. EUR/USD rebounded off intraday lows near 1.1775 to close near the 1.18 big figure. USD/JPY finished slightly lower (156.1) as the debate on (the timing of) further normalization between the BOJ and the government continues. Oil showed quite some intraday volatility but holds near $71 (Brent) as the US and Iran indicated to continue talks on Iran’s nuclear program next week.

Asian equities this morning again show a mixed picture, holding up reasonably well given the correction in the Nasdaq yesterday. The Chinese central bank (PBOC) removed a 20% reserve requirement on FX forward contracts, lowering the cost of shorting the yuan in an apparent move to slow recent sharp (and this week even accelerating) rise of the currency. USD/CNY ‘rebounds’ to 6.8575. In the UK, the Green party winning the special election in an Manchester area (Labour dropped to third place after the Reform UK party) again raised questions on PM Starmer’s position adding to broader political (and policy) uncertainty. Sterling’s performance this morning is a first barometer. EUR/GBP is attacking to key 0.8745/50 resistance area. A break at least would be significant from a technical point of view. We also keep an eye on UK gilts, which performed ‘remarkably’ well this month (and also yesterday). Later today, national CPI data will be published in Spain, Germany and France, giving a hint for next Tuesday’s EMU flash release (expected near the January levels). Also the ECB January inflation expectations survey, might get some more attention that is usually the case after Lagarde’s comments yesterday. In the US, January PPI data maybe are a bit outdated. The Chicago PMI frontruns the traditional US early month data update next week. We keep a close eye at US yields closing in on key support levels (cf supra). This weekend, OEPC+ on Sunday will hold a video conference discussing output levels (increases?) for April (and beyond).

News & Views

Tokyo’s headline price level fell by 0.4% M/M in February, with the annual print grinding slightly higher from 1.5% to 1.6%. Core inflation, ex fresh food declined by 0.3% M/M with the Y/Y-figure falling below the BoJ’s 2% inflation target (1.8% from 2%) for the first time since October 2024. A significant plunge in energy prices because of subsidies to support households with rising costs of living pulled utility prices 9.2% M/M and 6.6% Y/Y lower. Core inflation filtering out both fresh food and energy prices increased by 0.3% M/M and ticked up from 2.4% Y/Y to 2.5% Y/Y. Service price inflation rose by 1.5% Y/Y, up from 1.4%. National inflation numbers for the month of February will only be published on March 24. These “sticky” details should keep the Bank of Japan on course to extend its tightening cycle throughout this year. Money markets attach a 70% probability to a rate hike from 0.75% to 1% at the April meeting when the central bank updates its growth and inflation forecast.

UK consumer confidence unexpectedly deteriorated in February, with the index compiled by Growth for Knowledge declining from -16 to -19 (vs -15 consensus) and matching the softest level since May of last year. Details especially showed worries amongst households when it comes to their personal finances. Both on how they perceived them the last 12 months and how they expect them the next year. They’re also less eager to engage in major purchases despite a significant retracement in savings intentions. This mix of details is a clear nod the ongoing cost-of-living crisis with households prioritizing day-to-day spending.

Chart Alert: Gold (XAU/USD) Corrective Rebound Extends Further Above $5,046 Key Support

Key takeaways

- Corrective rebound gaining traction: Gold has broken above $5,170 and extended its bounce from the $4,402 low, with price action evolving within a minor ascending channel and maintaining a bullish bias above $5,046 support.

- Falling real yields supportive: The US 10-year real yield has declined sharply from 1.98% to 1.72%, reducing the opportunity cost of holding non-yielding gold and reinforcing the rebound narrative.

- Upside levels in focus: While momentum remains constructive, a sustained move above $5,307/$5,320 opens room toward $5,448. A break below $5,046 would jeopardize the recovery and expose deeper supports near $4,960–$4,703.

Gold (XAU/USD) cleared above a key short-term resistance level at $5,170 (also close to the 61.8% Fibonacci retracement of the waterfall decline from 29 January 2026 all-time high to 2 February 2026 low). It printed an intraday high of $5,250 on Tuesday, 24 February 2026.

Short-term technical elements and intermarket analysis suggest the ongoing corrective rebound phase from the 2 February 2026 low of $4,402 is likely still has room to extend further to the upside.

Lower opportunity cost of holding Gold

Fig. 1: US 10-year Treasury real yield medium-term trend as of 27 Feb 2026 (Source: TradingView)

The 10-year US Treasury real yield (after subtracting 10-year US inflation expectations from the 10-year US Treasury breakeven rate, which is then subtracted from the nominal yield) has staged a bearish reaction from its key medium-term pivotal resistance of 1.98% (see Fig. 1).

It has fallen by 24 basis points (bps) from 5 February 2026 to a current intraday level of 1.72% as of Friday, 27 February 2026, at the time of writing.

Price actions have reintegrated below its 20-day and 50-day moving averages, which suggests further potential weakness for the 10-year US Treasury real yield to retest the 17 September/23 October 2025 swing low area at 1.66%.

Hence, via the lens of intermarket analysis, a further drop in the 10-year US Treasury real yield lowers the opportunity cost of holding Gold (a non-interest income-bearing asset), in turn supporting the ongoing rebound seen in Gold (XAU/USD).

Let’s now focus on the short-term trajectory (1 to 3 days) for Gold (XAU/USD)

Gold (XAU/USD) – Evolving within a minor ascending channel

Fig. 2: Gold (XAU/USD) as of 27 Feb 2026 (Source: TradingView)

Bullish bias above $5,046 key short-term pivotal support (also the 20-day moving average with next intermediate resistances coming in at $5,307/320 (also a Fibonacci extension) and $5,448 (see Fig. 2).

On the flip side, a break and an hourly close below $5,046 put the minor corrective rebound phase (running from 2 February 2026 low) in jeopardy to expose the next intermediate supports at $4,960, $4,842, and $4,703.

Key elements to support the bullish bias on Gold (XAU/USD)

- Its price actions have started to oscillate within a minor ascending channel since 6 February 2025, with its upper and lower boundaries at around $5,448 and $5,046, respectively.

- Its hourly RSI momentum indicator has been supported by an ascending trendline since 24 February 2026 and just pushed above the 50 level. These observations suggest a potential build-up of short-term bullish momentum.

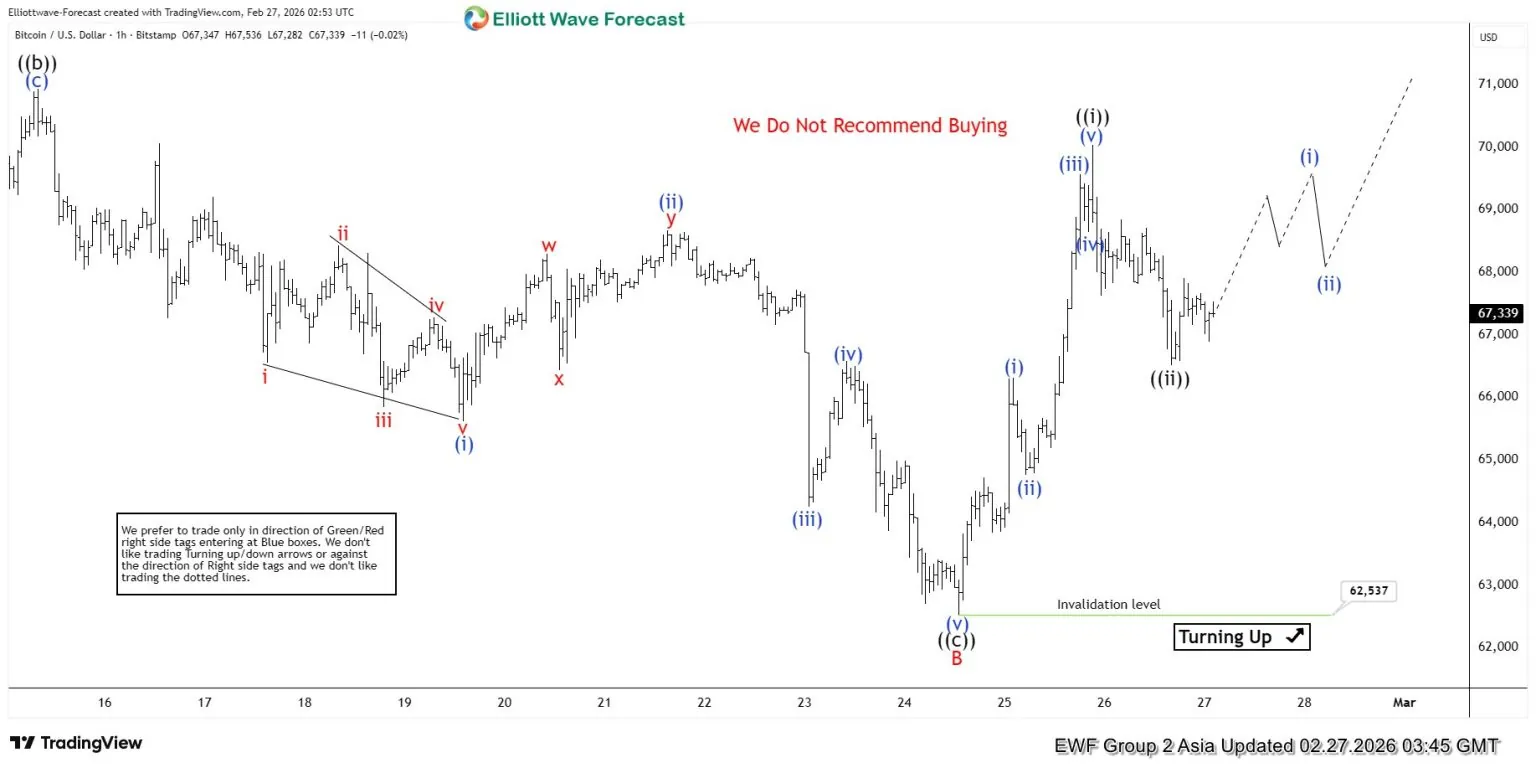

Bitcoin (BTCUSD) Elliott Wave Analysis: Corrective Bounce or Bullish Breakout?

Bitcoin (BTCUSD) continues to display an incomplete bearish sequence from the October 6 peak, which suggests that further downside remains possible. The extreme target zone derived from that peak lies between $41,411 and $52,204, and this area continues to serve as the broader downside objective. Despite this longer-term view, the cryptocurrency has been staging a corrective rally in the near term. From the February 6, 2026 low, Bitcoin has advanced in what appears to be a zigzag Elliott Wave structure, correcting the larger degree cycle that began from the January 14 peak.

Within this corrective move, wave A concluded at $72,174, followed by a pullback in wave B that ended at $62,537. Since then, price action has turned higher again in wave C. The internal subdivision of wave C is unfolding as a five-wave impulse, which provides a clearer framework for short-term expectations. From the wave B low, wave ((i)) finished at $70,038, while the subsequent dip in wave ((ii)) found support at $67,556. The market has since resumed its upward trajectory, reinforcing the view that wave C remains in progress.

As long as the pivot at $62,537 holds, Bitcoin is expected to extend higher in the near term. This corrective rally does not yet invalidate the broader bearish sequence, but it highlights the potential for continued strength before the larger trend resumes. Traders should monitor the unfolding impulse closely, as the completion of wave C will provide important clues regarding whether the rally is merely corrective or the beginning of a more sustained bullish trend.

Bitcoin (BTCUSD) 1-Hour Elliott Wave Chart

BTCUSD Elliott Wave Video:

https://www.youtube.com/watch?v=Iqdmkj_KwfQ

Peak Cycle Behaviour

Nvidia’s eye-popping results and strong beat remained short of triggering the kind of euphoria they would have a year ago. Nvidia printed a sizeable beat on almost every metric it released. Alas, the stock price — which had been set to challenge the $200 per share level in afterhours trading — took an unexpected U-turn. Nvidia dived more than 5% instead, closing the session below the $185 per share mark.

Michael Burry pointed to the company’s $95bn purchase obligations — up from $16bn a year ago — suggesting that if AI demand slows or customers pause orders, Nvidia could be stuck paying for unused capacity, compressing margins and resetting earnings expectations lower. A year ago, the same commitment would have been considered bullish — Nvidia locking in supply early to meet multi-year demand from big customers like Microsoft, Amazon and Google. Today, the interpretation has flipped on fears that AI capex could slow and leave Nvidia with excess capacity. This looks like peak-cycle behaviour. It doesn’t necessarily mean that AI adoption will slow, but that the Big Tech AI push could level out.

So here we are. Nvidia tanks despite blockbuster results and strong guidance — there was little the company could have done differently to change the immediate market reaction.

Salesforce, on the other hand, which was sent lower in afterhours trading, ended 4% higher. Its Agentforce AI generated $800m last quarter, up from $500m. CrowdStrike jumped nearly 5% despite softer-than-expected guidance, while Snowflake rebounded more than 2% on robust AI-related bookings that boosted earnings. The London Stock Exchange Group, which has lost more than 40% since February in the broader software selloff, also beat projections last quarter and guided to a better 2026. The company owns proprietary data that AI cannot easily replicate; on the contrary, AI models are likely to pay for access to that data.

In conclusion, investors are cautiously returning to software names as earnings show AI demand boosting rather than destroying business models. Concerns about AI disruption are not over — Block, for example, announced plans to replace up to 40% of certain roles with automation over time. But if machines replace people, software companies that build the new workforce could ultimately benefit.

We remain in a period of great uncertainty regarding the winners and losers of AI adoption. We don’t know how fast the shift will happen, but volatility is likely to persist due to low visibility.

For now, it feels like valuations in AI enablers — think Nvidia, Meta and Google — may have peaked, while the software selloff appears overdone. Meanwhile, memory chip makers have been among the clearest winners since the last quarter of last year, and higher memory prices could eventually pressure margins at PC and smartphone manufacturers.

Zooming out, Nvidia’s drop pulled the S&P 500 into the red yesterday — but most stocks rose, helped by lower US yields.

The US dollar was better bid but remains capped below its 50-DMA. Gold consolidates gains near the $5’200 per ounce level.

Crude oil wobbles on US-Iran headlines. US crude briefly slipped below $64 per barrel on reports of “significant progress” in negotiations between Washington and Tehran, but rebounded as talks were paused and pushed to a later date — keeping geopolitical risk alive, including the possibility of disruption to oil flows through the Strait of Hormuz. Intraday oil trading remains challenging due to high volatility. But the medium-term outlook is broadly unchanged: crude could give back part of its recent gains once tensions ease. But until then, a direct military escalation involving Iran could push US crude into the $70–80 per barrel range, depending on intensity.

We are coming toward the end of another eventful week. The biggest news was Nvidia earnings, which notably failed to improve appetite for US tech stocks.

Looking further back, the rotation trade strengthened in February: capital flowed out of US technology into US non-tech and global indices, and the MSCI World ex-US widened its outperformance gap throughout the month. Investors largely shrugged off trade tensions with the US. European inflation eased, and Federal Reserve (Fed) rate-cut expectations moderated following stronger-than-expected employment and inflation figures — even though US GDP growth slowed sharply in Q4, reflecting slower consumer spending growth, a negative contribution from government spending due to a federal shutdown, and weaker net exports.

Looking ahead, uncertainty surrounding AI and its social and economic impact will continue to shape markets — sometimes unpredictably. This environment could favour a flight toward “high assets, low obsolescence” — companies with tangible assets or durable competitive moats that face limited disruption risk – the HALO trade that everyone is talking about.

I like the FTSE 100, as its energy and mining exposure fits well with the rotation theme, although elevated valuations in parts of the mining sector could become problematic down the line.

In FX, the US dollar may remain under pressure in the coming weeks, though major peers are approaching key technical levels. The EURUSD, for example, has struggled above the 1.20 mark amid concerns that excessive euro strength could hurt European economies already challenged by US tariffs. The cable outlook remains cautious given policy divergence expectations between the Fed and the Bank of England (BoE), with the latter seen cutting rates twice before summer. Selling pressure on the Japanese yen has eased alongside Japanese yields, which in turn has helped limit upward pressure on global sovereign yields — possibly also influenced by rising stress in private credit markets. But the downside risks in the yen remain on Takaichi’s apprehension regarding rate normalization.

Somehow worryingly, private credit concerns emerged this month linked to the software selloff, but new stress emerged yesterday involving Barclays and Atlas SP (Apollo’s structured-credit arm). The lenders reportedly helped arrange $2.7bn of loans to a UK mortgage company accused of financial irregularities.

In recent years, this type of stress has often been brushed aside, but JPMorgan’s Dimon has repeatedly warned of ‘coach roaches’ that parts of the market may be taking excessive risks to boost returns.

How excessive — time will tell.

Flash Inflation to Set the Tone Ahead to Euro Area Data Next Week

In focus today

In the US, January PPI data will be released this afternoon. The earlier CPI release landed slightly below expectations.

In the euro area, February's flash inflation data from France, Germany, and Spain will give important hints ahead of next week's euro area inflation release. We expect euro area HICP inflation to rise marginally from 1.69% y/y to 1.73% y/y, remaining at 1.7% y/y when rounded. Core inflation is expected to remain at 2.2% y/y. Energy inflation is expected to rise due to lagged effects of January's energy price and higher fuel prices in February, which is the main reason we expect a small rise in the headline at the second decimal. Monthly momentum in services inflation will be crucial, given its notable weakness in January.

In Norway, the last couple of months' NAV figures show that unemployment is falling again, which is a bit surprising given the moderate growth, the slowdown in employment growth, and the decline in vacancies. We expect that the unemployment rate (SA) will be unchanged at 2.1% in January. Finally, we suspect that the weak retail sales figures for December are partly due to problems with seasonal adjustment in connection with Black week. Hence, we expect retail sales to have increased by 0.7% m/m s.a. in January.

In Sweden, we will get the final GDP release for the fourth quarter. We expect GDP to grow by 0.4% q/q and 2.2% y/y. This is slightly stronger than the GDP indicator but is in line with production data, which showed positive signals. Monthly data for consumption indicates that the recovery is underway and has looked noticeably better since the second quarter of last year. We are also keeping an eye out for potential revisions to the third quarter. The most important factor for the Riksbank is domestic demand, particularly how consumption develops.

Economic and market news

What happened overnight

In Japan, Tokyo inflation (a good indicator of the country total) slowed in February, with CPI excl. fresh food at 1.8% y/y, down from 2.0% y/y in January. This marks the first time in 16 months that inflation has fallen below the Bank of Japan's 2% target. The decline was driven by the impact of fuel subsidies and the removal of gasoline tax surcharges, while the effects of recent food price hikes have largely subsided.

What happened yesterday

In US-Iran talks, 'significant progress' was reportedly made in Geneva on Tehran's nuclear programme, with technical negotiations set to resume on Monday in Vienna. According to the Wall Street Journal, the US has outlined key demands, including dismantling key nuclear sites, signing a permanent agreement, and transferring Iran's enriched uranium stockpile to the US. While the US has shown some openness to limited enrichment for medical purposes, this could still leave the door open for Iran to quite easily continue enrichment to weapons grade levels. With diplomacy still on the table, concrete results remain elusive, leaving crude markets in a wait-and-see mode and continuing to price in a significant risk of military escalation.

In Sweden, February's NIER Economic Tendency Survey showed weaker sentiment, with the Economic Tendency Indicator at 100.1 (prior: 102.8). Manufacturing confidence fell to 97.7 (prior: 103.4), while consumer confidence rose slightly to 96.3 (prior: 95.3). Sentiment now aligns with our GDP forecast, reducing the recent upside risks. For the Riksbank, the survey was relatively neutral. Price plans in the service sector remain elevated, but food price plans signal a decline, reflecting willingness to adjust prices ahead of April's VAT reduction.

In Denmark, PM Mette Frederiksen has announced parliamentary elections will be held on 24 March. Among other things, her party is running on introducing a new wealth tax to fund increasing spending on primary schools and a cut in property taxes on lowest valued homes. Denmark was set to hold elections in the autumn, but the government has the option of calling for earlier elections.

Equities: Global equities declined 0.3% yesterday. S&P500 declined 0.5%, while Nasdaq was down 1.2% and Russell2000 was up 0.5%. Stoxx600 was virtually unchanged. The slide was heavily concentrated in AI/tech exposed companies, with tech down 1.8%. In fact, it was only 30% of the S&P500 names that ended lower yesterday. Nvidia ended 5.5% lower, amid their report on Wednesday night showing strong sales, but AI implications investor concerns continue to linger, and when such a large company declines by more than 5%, it is hard for the rest of the market not to notice. Firms within the private equity/credit space suffered markedly following an Apollo private credit fund marked down its value of the assets and cut dividends, identifying the recent turmoil around private credit/equity names. Overnight, Asian stocks are generally positive with US futures in red.

FI and FX: Talks between Iran and the US have been described as constructive, although no concrete results have been announced. EUR/USD continues to trade near the 1.18 level, while EUR/SEK remains below 10.70. EUR/NOK has been range-bound between 11.20 and 11.35 over the past two weeks.

Rates have rallied in most markets in recent days. In the US, the 10y Treasury yield is trading at 4.0% this morning, while the 10y gilt yield has fallen to 4.27%, its lowest level since late 2024. EUR swap rates have also drifted lower, and today's preliminary inflation data from France, Spain and Germany could put additional downward pressure on yields if the figures surprise to the downside.

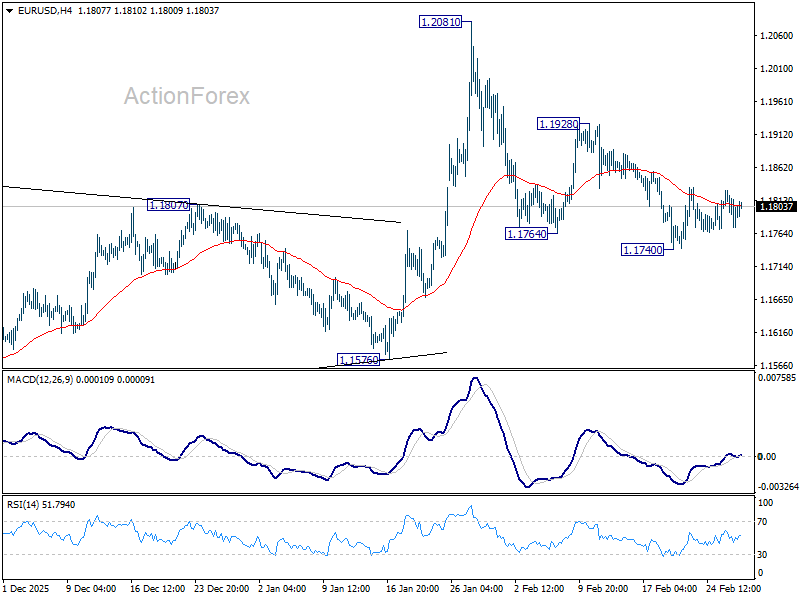

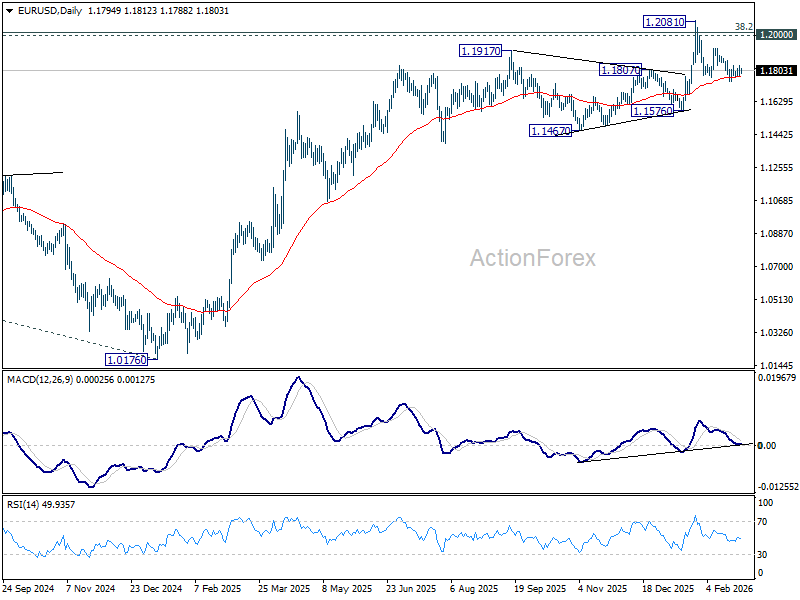

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1773; (P) 1.1801; (R1) 1.1828; More….

EUR/USD is still bounded in tight range above 1.1740 and intraday bias stays neutral. Near term risk will remain on the downside as long as 1.1928 resistance holds. Below 1.1740 temporary low will target 1.1576 support next. Firm break there should confirm rejection by 1.2 key psychological level and turn near term outlook bearish. However, break of 1.1928 argue that fall from 1.2081 has completed as a correction, and revive near term bullishness. Retest of 1.2081 should then be seen next.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

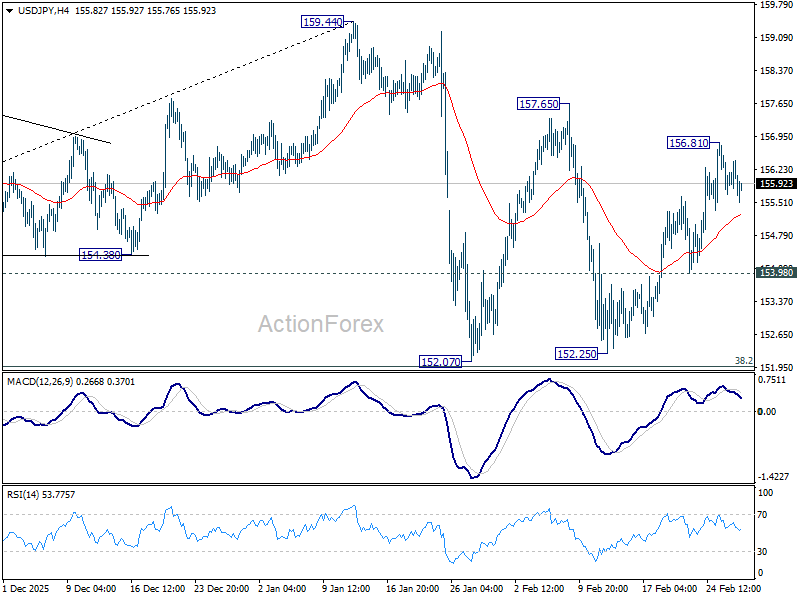

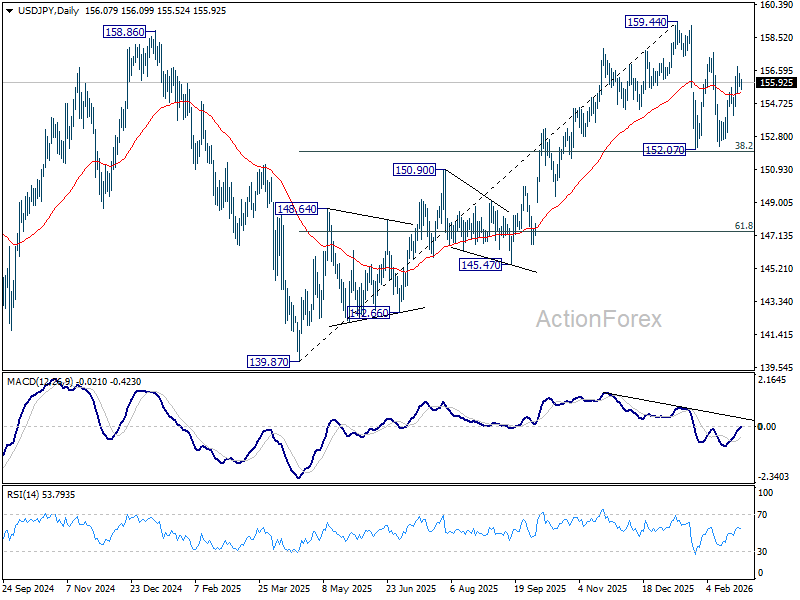

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.71; (P) 156.13; (R1) 156.55; More...

USD/JPY is staying in consolidations below 156.81 temporary top and intraday bias remains neutral. On the upside, above 156.81 will resume the rally from 152.25 to 157.65 resistance first. Firm break there will target a retest on 159.44. high. On the downside, however, break of 153.90 will bring deeper fall to 152.25 support. Overall, with 38.2% retracement of 139.87 to 159.44 at 151.96 intact, price actions from 159.44 are seen as a corrective pattern. Also, rise from 139.87 is expected to resume through 159.44 at a later stage.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.93) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.

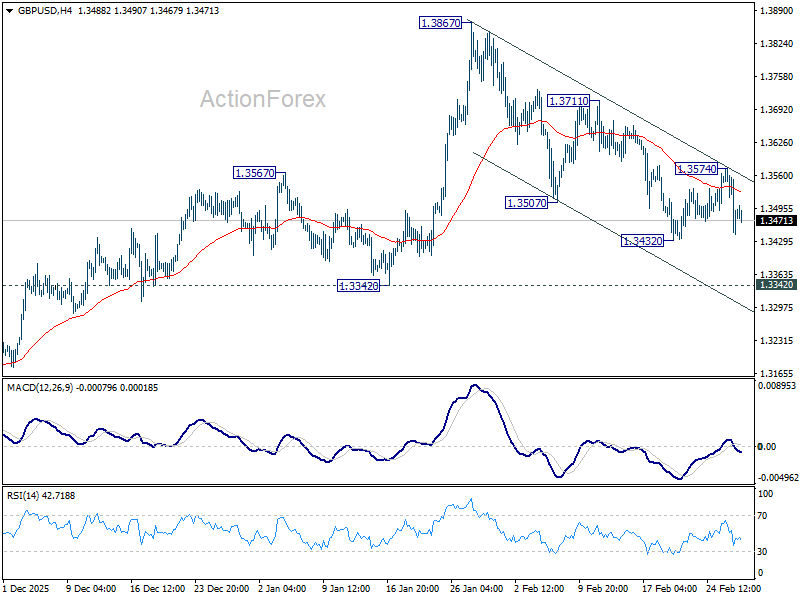

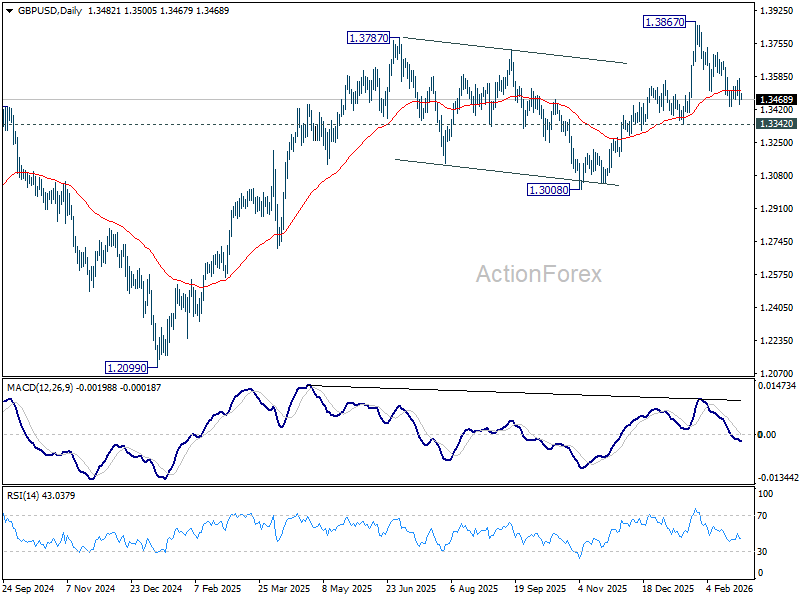

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3426; (P) 1.3501; (R1) 1.3556; More...

Despite the current steep decline, GBP/USD is still holding above 1.3432 and intraday bias remains neutral. On the downside, below 1.3432 will resume the fall from 1.3867 to 1.3342 support. Firm break there should confirm that it's already correcting the whole rise from 1.2099. However, break of 1.3574 resistance will argue that the decline has completed as a near term correction, and turn bias back to the upside for retesting 1.3867.

In the bigger picture, as long as 1.3008 support holds, rise from 1.3051 (2022 low) should still be in progress for 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. However, firm break of 1.3008 will raise the chance of medium term bearish reversal and target 1.2099 support next.

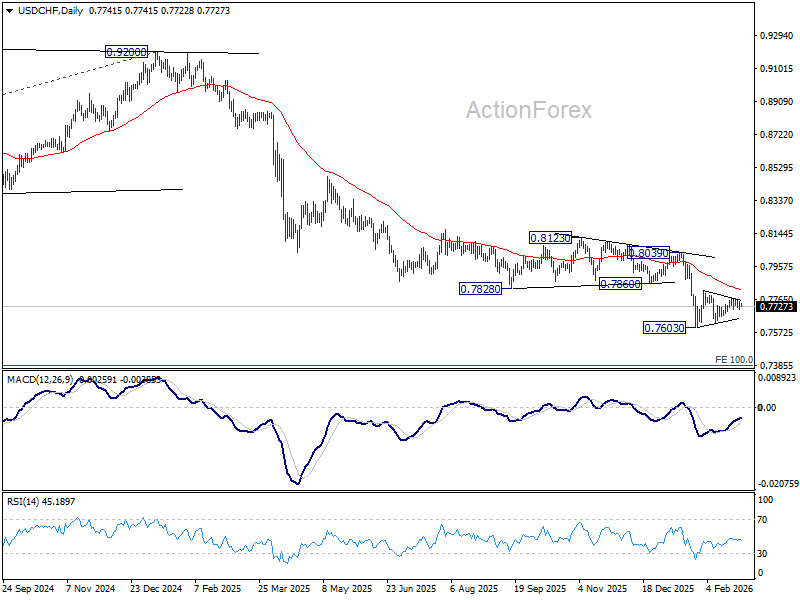

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7716; (P) 0.7735; (R1) 0.7759; More….

No change in USD/CHF's outlook as consolidations continue above 0.7603. Intraday bias remains neutral for now. In case of stronger rise, upside should be limited by 55 D EMA (now at 0.7824) to complete the pattern. On the downside, below 0.7627 will bring retest of 0.7603. Firm break there will resume larger down trend, and target 0.7382 projection level next. However, sustained break of 55 D EMA will indicate that a larger scale corrective bounce in underway and target 0.8039 resistance next.

In the bigger picture, down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8123 resistance holds.

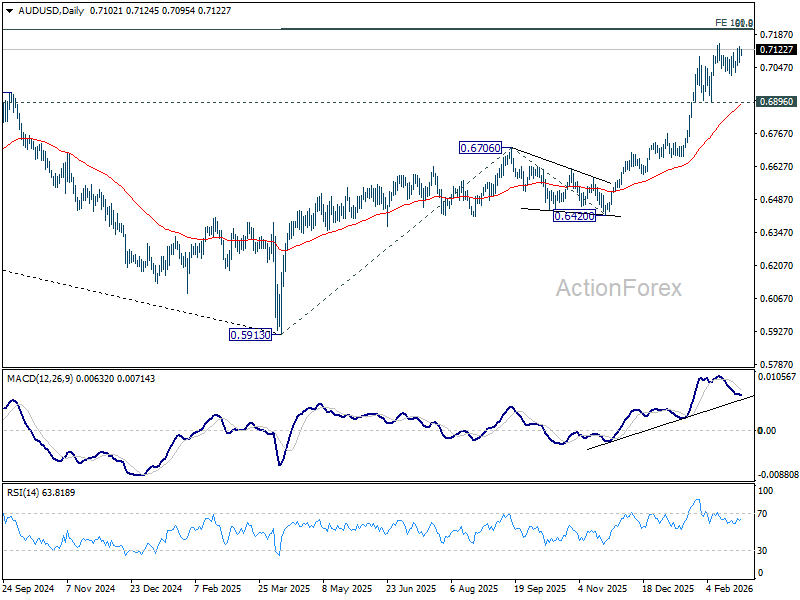

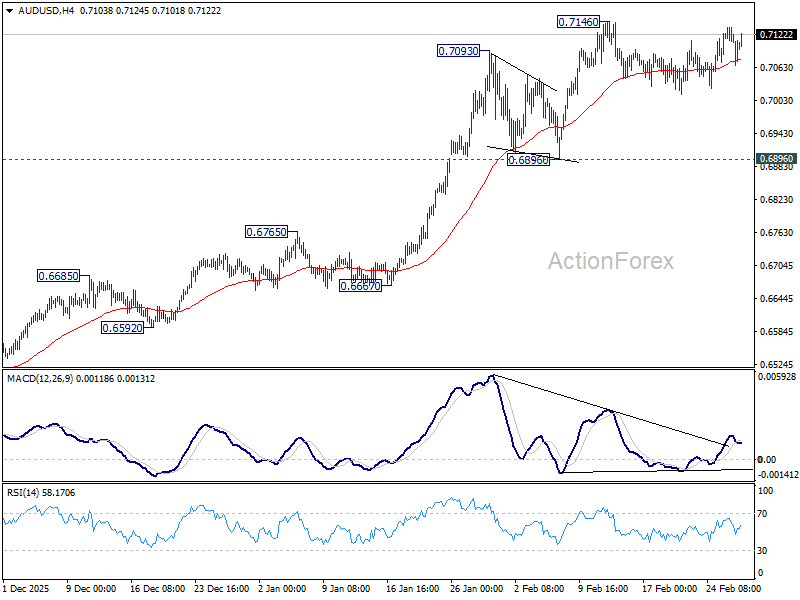

AUD/USD Daily Report

Daily Pivots: (S1) 0.7070; (P) 0.7103; (R1) 0.7140; More...

Intraday bias in AUD/USD remains neutral as it's still bounded in range below 0.7146. Consolidations could continue and deeper retreat cannot be ruled out. But downside should be contained above 0.6896 support. On the upside, above 0.7146 will resume larger up trend to 100% projection of 0.5913 to 0.6706 from 0.6420 at 0.7213.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6706 resistance turned support holds, even in case of deep pullback.