Sample Category Title

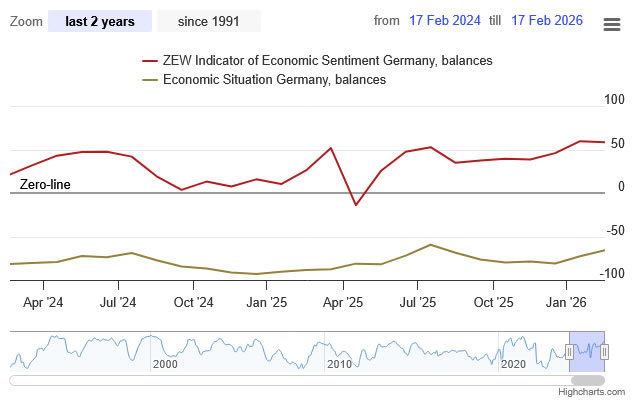

Germany ZEW falls to 58.3 as recovery remains fragile

Germany’s ZEW Economic Sentiment index edged down from 59.6 to 58.3 in February, missing expectations of 65.2 but still pointing to cautious optimism. Current Situation index improved from -72.7 to -65.9, roughly in line with forecasts. At the Eurozone level, ZEW Economic Sentiment index fell from 40.8 to 39.4, undershooting expectations of 45.2. However, the Current Situation measure improved by 4.5 points to -13.6.

ZEW President Achim Wambach described the recovery as “fragile,” noting that structural challenges continue to weigh on industry and private investment. He emphasized that upcoming reforms to Germany’s social insurance system should be used to strengthen the country’s competitiveness as a business location.

Sector breakdown showed moderate to strong improvement in export-oriented industries, including chemicals and pharmaceuticals, steel and metals, and mechanical engineering, likely reflecting stronger incoming orders late last year. Private consumption prospects also improved, while banks, insurers, and IT sectors reported weaker expectations.

GBP/USD Picks Up Bearish Vibes After Weak Jobs Data

- GBP/USD comes under renewed pressure after retreating below 1.3600.

- Short-term bias leans bearish, but confirmation is still required.

- A close below 1.3440–1.3500 would shift the outlook decisively negative.

GBP/USD slid to an almost two-week low of 1.3551 early Tuesday after disappointing UK employment data dampened sentiment. The report showed softer job growth, an unchanged unemployment rate at 5.1%, and a sharper slowdown in average weekly earnings in December – reinforcing expectations that the Bank of England could proceed with a 25bps rate cut in March.

The weaker data revived selling pressure after the bulls failed to secure a close above the 20-day simple moving average (SMA) near 1.3635 on Monday. The technical indicators are now tilting lower, reflecting building downside momentum. However, further losses may remain contained unless the pair violates the tentative support trendline drawn from November near 1.3500. The 200-day SMA might also serve as an additional layer of safety near 1.3440 and around the 50% Fibonacci retracement of the November–January rally. However, any declines lower would weaken the short-term structure and likely accelerate declines toward the 61.8% Fibonacci retracement at 1.3340.

On the upside, a sustained move above the 1.3600–1.3665 resistance region would ease immediate downside pressure and shift the bias back to neutral-to-bullish. In that case, buyers could target the 1.3730–1.3765 area, with January’s peak at 1.3815–1.3840 coming back into view.

Overall, GBP/USD is gradually tilting bearish. Still, only a clear breakdown below the 1.3440–1.3500 support zone would confirm a deeper corrective phase, while rebounds above 1.3600 may keep dip-buying strategies in play.

GBP/JPY Falls to a Year-to-Date Low

As the GBP/JPY chart shows, the pound has dropped below the 12 February low against the Japanese yen, marking its weakest level since the beginning of 2026. The pair last traded beneath the 207.500 mark in mid-December 2025.

→ The yen’s strength is supported by expectations that economic stimulus measures introduced by Prime Minister Sanae Takaichi, in coordination with the Bank of Japan, will underpin the national currency. Barclays forecasts further appreciation of the yen.

→ Sterling weakened today following reports that UK unemployment reached a five-year high in December, while wage growth slowed. This may reinforce arguments in favour of additional interest rate cuts by the Bank of England.

Technical Analysis of GBP/JPY

Long-term moving averages are turning lower, signalling potential structural shifts and possible capital reallocation after five years of an overall uptrend in GBP/JPY.

Price action is forming a well-defined descending channel. In this context:

→ the median line has switched from acting as support to serving as resistance (as highlighted by the thicker lines);

→ today, GBP/JPY is trading in the lower quarter of the channel, indicating continued bearish dominance.

It is worth noting that yesterday’s breakout above local resistance (marked by an arrow) proved to be false, triggering renewed downward momentum.

On the other hand, after dipping below the 12 February low near 207.560, the pair has started to rebound, raising the possibility of a mirrored move and a false bearish breakout.

Nevertheless, the outlook for bulls remains challenging. Even if they manage to push prices slightly higher, they may encounter resistance around 208.315 — a level where sellers previously demonstrated strength when breaking local support (shown in purple).

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

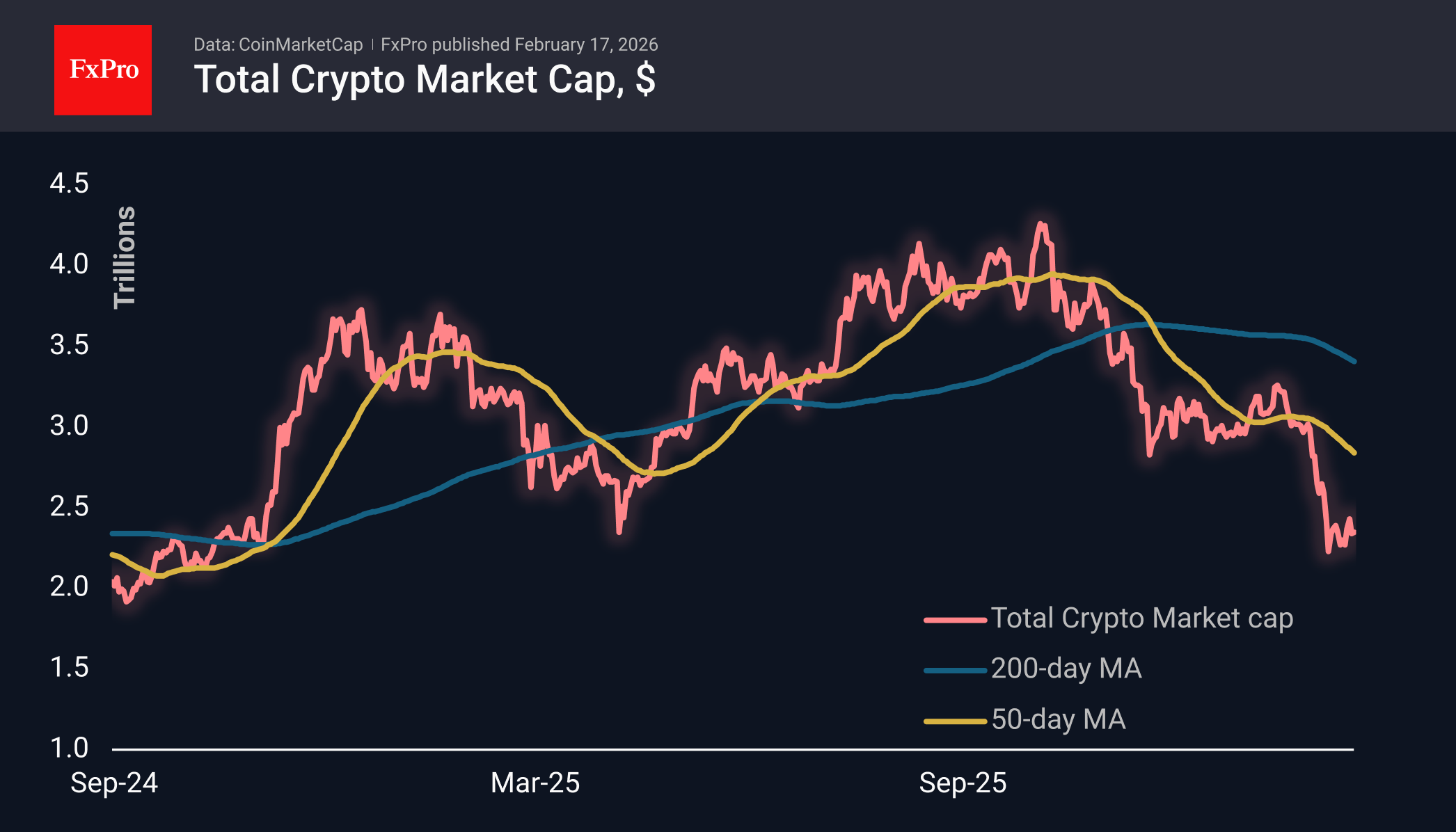

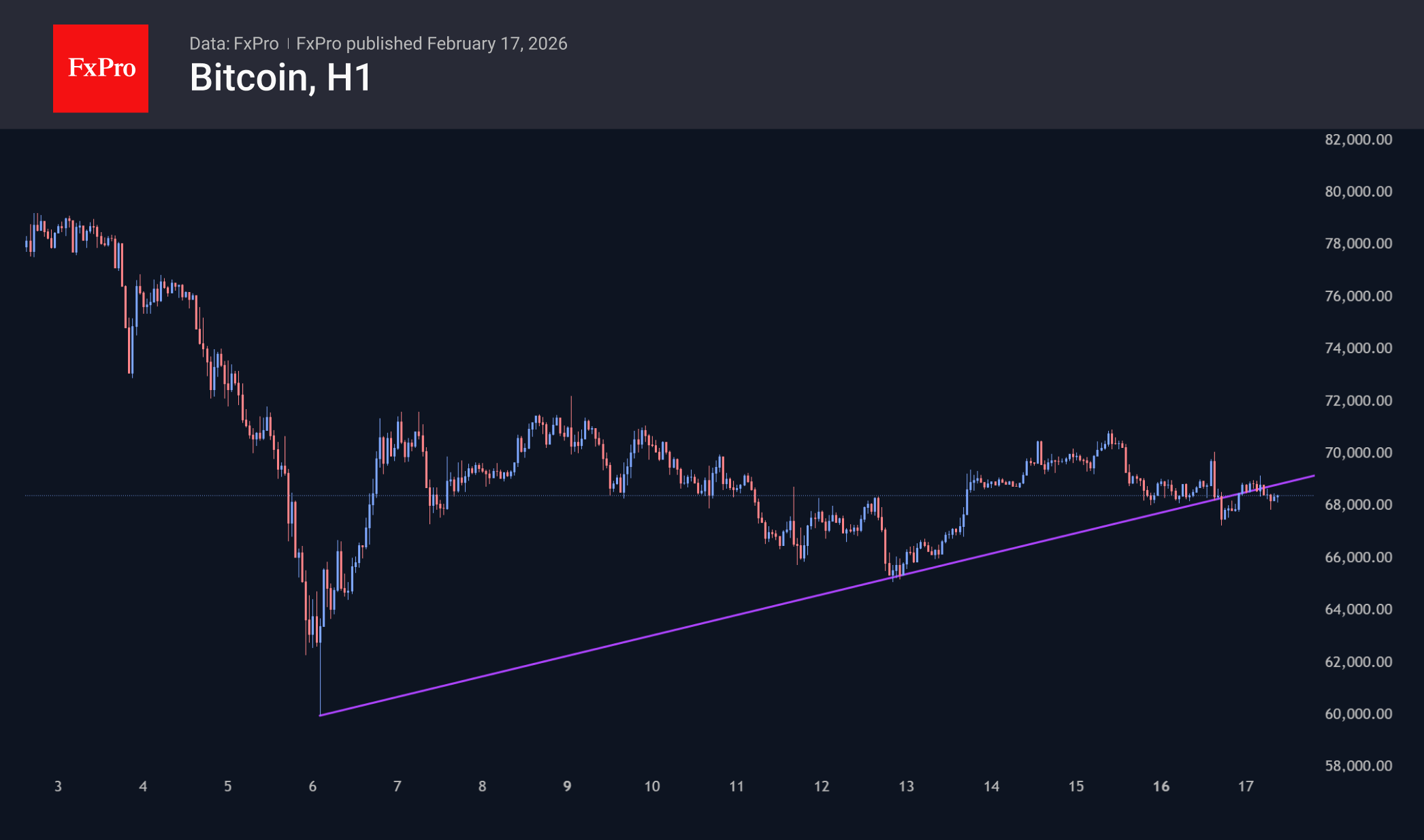

Bitcoin Dips Below Short-Term Support

Market Overview

The crypto market cap stood at $2.35 trillion on Tuesday morning, roughly the same as it was yesterday and seven days ago. The leaders in growth among the most liquid coins over the past week are the anonymous Zcash and Cosmos, which are widely involved in the tokenisation of debt assets, adding over 20%. At the same time, the leaders in decline during this period are Ethereum (-1.7%), BNB (-1.5%) and Bitcoin (-1.1%). The decline of the largest coins is an ominous sign for smaller ones, as it may soon pull them down with it at an accelerated pace.

Bitcoin technically fell below the support line that ran through the extreme lows of the first half of February, as another attempt to break above $70K on Monday attracted the interest of sellers, which quickly pushed the price back to $67K. On Tuesday morning, BTC is trading near $68K, where it was the day before, but the former support now looks like local resistance. Confirmation of this trend reversal will be a fall below the recent lows of $67K, with subsequent targets at $65K and $60K.

News Background

The current situation is more reminiscent of a change in the global BTC trend than a local correction, according to CryptoQuant. The market has already entered a ‘stress zone’ but has not yet reached the stage of final capitulation. To form a ‘true bottom,’ a peak in loss-taking and a complete exhaustion of selling pressure are necessary.

Capriole Investments founder Charles Edwards cited the quantum threat as one of the reasons for the current BTC correction. In contrast, Benchmark considers such fears to be exaggerated, and Blockstream expects supercomputers to appear only in 20-40 years. Growing attention to the threat of quantum computing is beginning to reduce the long-term appeal of Bitcoin compared to gold, said analyst Willy Woo. In his opinion, about 4 million ‘lost’ coins could be dumped on the market after a quantum computer hacks Bitcoin.

Blockstream CEO Adam Back criticised the BIP-110 update aimed at combating ‘spam’ on the Bitcoin network. He called the initiative a threat to the reputation of the first cryptocurrency.

In the fourth quarter, Harvard University’s management company withdrew more than 20% of its investments from the Bitcoin ETF, investing in an Ethereum-based ETF for the first time. Despite the partial sale, Bitcoin ETF shares remain the most significant public asset in Harvard’s portfolio.

Gold Price Falls to a 10-Day Low

As today’s XAU/USD chart shows, the price of gold has dropped below the lows of 12 February, marking its weakest level in ten days. According to media reports, several factors are weighing on bullion:

- → Easing geopolitical tensions. Safe-haven demand has diminished amid US–Iran and Russia–Ukraine negotiations.

- → Slowing US inflation. This may be prompting traders to reassess expectations for Federal Reserve policy in 2026.

- → The holiday effect. With Presidents’ Day in the US and Lunar New Year celebrations in Asia, trading volumes have declined. In such thin market conditions, prices can become more vulnerable to speculation and abrupt moves.

On 9 February, when analysing gold price movements, we:

- → confirmed the validity of the long-term ascending channel;

- → noted that following a spike in extreme volatility at the turn of the month, the market could begin seeking a new equilibrium;

- → suggested a scenario involving a contraction in price swings on the XAU/USD chart, with the potential formation of temporary balance between supply and demand around the psychological $5k mark.

Indeed, from 9 to 12 February the market formed a consolidation zone slightly above $5k — more precisely, between resistance R1 and local support S1.

Technical Analysis of the XAU/USD Chart

A false bullish breakout (indicated by the arrow) highlighted the bulls’ inability to sustain momentum and effectively became a trap for buyers.

This, in turn, allowed bears to attempt to seize the initiative, resulting in a successful break below the S1 level. Subsequently, the breached level acted as resistance (R2).

Today’s decline on the XAU/USD chart suggests that:

- → bears remain in control, as evidenced by the break of local support S2;

- → a key argument in favour of the bulls may come from the major support at the lower boundary of the long-term channel.

In February, the market has already twice returned within the boundaries of the long-term upward channel. It cannot be ruled out that the price will remain inside it. Notably, if a decisive break above the resistance line (shown in red) occurs, this could reasonably be interpreted as a breakout of a bullish flag pattern.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

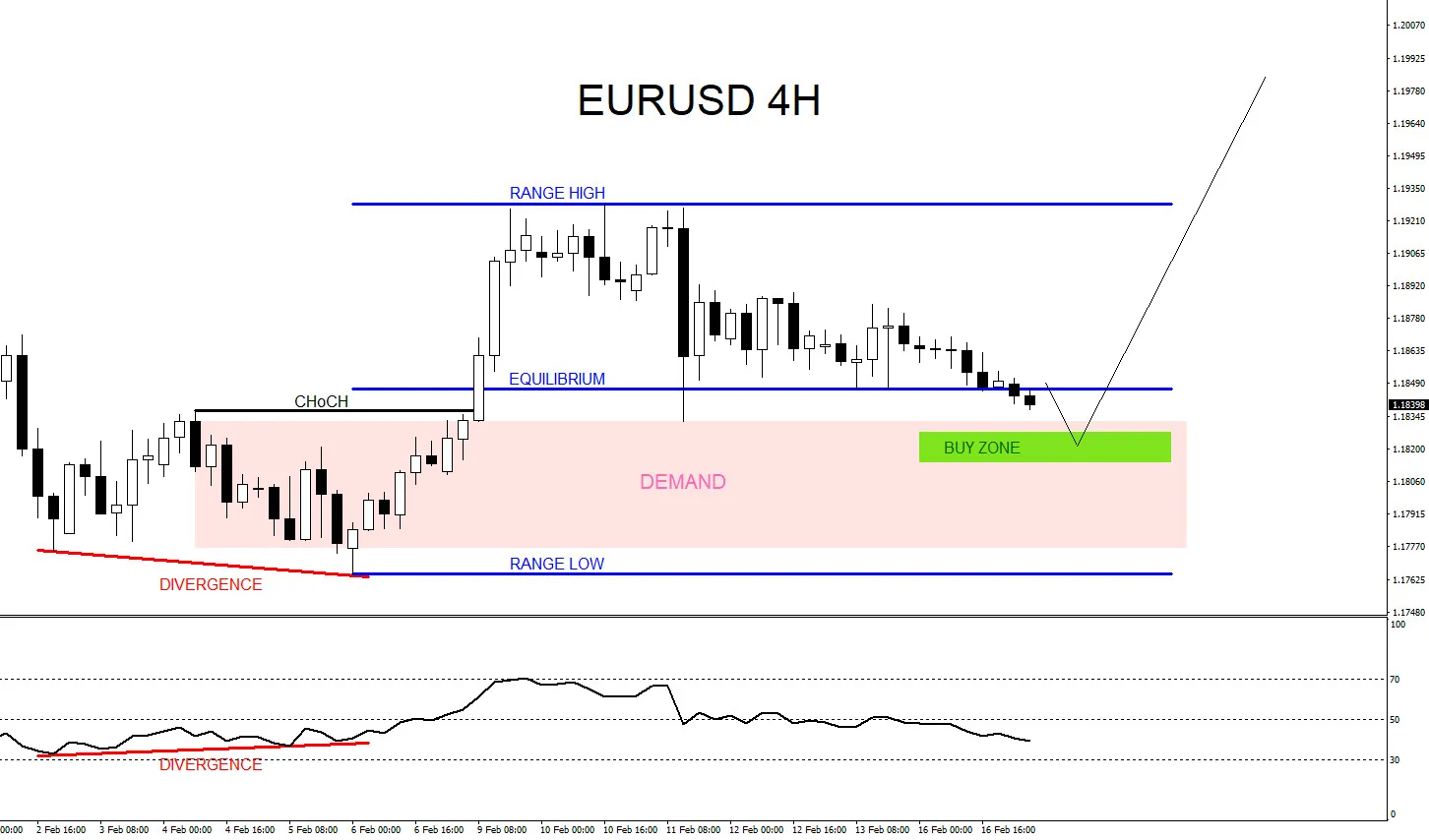

EURUSD Buy Setup

EURUSD Buy Trade Setup:

- Bullish divergence market pattern. (Red line)

- Bullish CHoCH/Change of Character. (Black line)

- Price below equilibrium level where buyers are waiting. (Blue)

- Wait for price to tap demand zone (Pink) and buy zone (Green) first then enter BUY/LONG with stop loss at the range low and target at 2R minimum.

EURUSD 4 Hour Chart February 16 2026

A trader should always have multiple strategies all lined up before entering a trade. Never trade off one simple strategy. When multiple strategies all line up it allows a trader to see a clearer trade setup. We at EWF never say we are always right. No market service provider can forecast markets with 100% accuracy. Only thing we at EWF 100%, is that we are RIGHT more than we are WRONG.

Of course, like any strategy/technique, there will be times when the strategy/technique fails so proper money/risk management should always be used on every trade. Hope you enjoyed this article and follow me on social media for updates and questions> @AidanFX

At Elliottwave-Forecast we cover 78 instruments (Forex, Commodities, Indices, Cryptos, Stocks and ETFs) in 4 different time frames and we offer 5 Live Session Webinars everyday. We do Daily Technical Videos, Elliott Wave Trade Setup Videos and we have a 24 Hour Chat Room. Our clients are always in the loop for the next market move.

RBA Minutes: Never Mind the Greenbacks

RBA Minutes reprise inflation and capacity concerns but downplay the USD sell-off's role in the AUD’s appreciation.

- In recent times, RBA minutes have typically added little information beyond what is already discussed at the media conference or published in the Statement on Monetary Policy (SMP). This time, though, the minutes highlighted how poor model-based measures of the ‘neutral interest rate’ are as a guide for policy.

- More concerningly, the minutes were quite dismissive of the exchange rate’s role in holding down inflation. It is true that much of the recent appreciation in the AUD reflects the changing interest rate outlook and so is already in the (small) disinflationary impact forecast from that source. However, the exogenous-to-Australia sell-off in the USD and associated hedging behaviour is an independent element that the RBA seems not to have allowed for. While this will not become apparent for a while, it does suggest some downside risk to imported goods inflation.

- The bulk of the minutes were devoted to concerns about capacity pressures and the (smaller) proportion of the recent pick-up in inflation that was potentially persistent, which were already canvassed in the RBA’s other communication. The risks around the market path for interest rates were seen as two-sided, depending on how demand pressures and supply constraints evolve from here.

With the advent of media conferences after every meeting, RBA minutes have tended to provide less information value of late than in the past, particularly for SMP meetings. This time around, there were some interesting points that could point to under-appreciated risks for the policy outlook.

Their assessment of financial conditions was quite backward-looking, especially around credit. Credit responds to interest rate and economic conditions with a lag, so strong credit growth now tells you about conditions a little while ago, when rates were expected to fall further. While the higher exchange rate tightened financial conditions at the margin, there was considerable scepticism in the minutes about whether financial conditions at the beginning of this year were tight in an absolute sense.

There were also some inconsistencies in the discussion of financial conditions and the stance of policy as it related to inflation risks. The Financial Conditions section of the minutes pointed to the pick-up in inflation as a sign that policy was no longer restrictive, because it implies demand is outstripping supply. In the Economic Conditions section, though, it was stated that “the larger part of the increase had reflected less-persistent factors, including price volatility in categories such as electricity, travel and groceries,” none of which provides information about demand pressures. Of the factors mentioned in that passage, only durable goods inflation would normally be thought of as signalling demand pressures rather than transitory supply shocks or seasonality. Some of the pick-up in inflation is seen as indicating demand and capacity pressures, but not “the larger part”. This nuance was missing from the discussion of the policy stance, which could either be a (rare) drafting oversight or a hint at differences in opinion within the RBA staff (and possibly also Board members).

In welcome news, the minutes really tried to hose down excessive focus on model-based measures of the so-called ‘neutral interest rate’. This should resolve some confusion among observers. A comment about these measures being regarded as a “misleading signal of the stance of monetary policy prior to the pandemic” was new information. It should be noted that most major central banks have not come to the same view.

More concerningly, the minutes were dismissive of the idea that there has been any exogenous element to the recent exchange rate appreciation. According to the minutes, essentially all the exchange rate move has been the result of higher interest rates and commodity prices, and so the currency is assessed to have had no independent effect on imported prices beyond the interest rate impulse response, for example as traced out in Figure 12 of this RBA research paper. In the ‘Considerations’ section, it was stated “the appreciation had been in response to expectations for tighter monetary policy, not independent of it.” The minutes also stated that “The forecasts also accounted for the 5 per cent appreciation of the exchange rate since November, which was assumed to dampen import prices and net exports.” Observant readers will notice that the AUD appreciation over the past month has been at least double the amount implied by that research paper figure across two different models, for a similar shift in (expected) interest rates.

As we noted last week, we think that some part of the AUD appreciation is in fact the result of the USD selloff (and CNY counterpart), amplified by hedging activity, making it independent of the response to rates and commodity prices. Timing issues might have contributed to the RBA’s judgement on this point, given how close the sharpest part of the appreciation was to the 28 January deadline for finalising forecasts. However, there is also an analytical point here that the RBA’s assessment in the minutes explicitly rules out. If it had just been a deadline issue, the language in the minutes would have been more circumspect.

This part of the appreciation is a source of downside risk for inflation over the next year or so that the RBA have clearly missed. We expect to have a more refined estimate of this impact soon but currently assess the potential impact as being similar to that of interest rates, i.e. of the order of 0.1–0.2ppt off trimmed mean inflation over the next year or so.

The bulk of the minutes was dedicated to the changed assessment of demand and capacity pressures in the economy, and the resulting inflationary impact. Much was made of the staff’s model-based measures of spare capacity, which had been revised considerably since the previous meeting and now matched up better to the results in a leading business survey. (Unlike the models of the neutral rate, this variability was represented to be a good thing.)

Breadth-based measures of inflation were key to the RBA’s concerns about renewed inflation, even as the “larger part” of the pick-up in inflation was seen as mostly temporary.

Like other recent RBA communication, the minutes were circumspect and agnostic about the outlook for the cash rate from here, with risks on both sides of a market path that the minutes seemed to broadly endorse. Some downside risks had abated, notably those concerning global growth. Weaker demand growth, stronger supply capacity growth, sector-specific shocks or a misreading of the stance of policy were all cited as downside risks. On the upside, most of the same factors applied in reverse, along with the question of whether longer-term inflation expectations remained anchored. It should be noted that the recent speech by Assistant Governor Hunter highlighted that the RBA’s updated analytical framework for assessing the labour market assumes that inflation expectations are anchored, so there are some potential inconsistencies in the (low-probability) event that this risk is realised.

The broader strategy of “seeking to bring inflation back to target within a reasonable timeframe while preserving as many of the gains in employment as possible” is still seen as appropriate by the Board. We see this as signalling that the RBA is not pivoting to an inflation-only view. Rather, its policy decisions are better characterised as fine-tuning the setting of policy in light of what the Board sees as shifting risks. This adds weight to our base-case view that the next increase in the cash rate is coming in May, not March.

EURUSD Slides Smoothly: Fed Minutes in Focus

EURUSD is moving smoothly downward and has touched 1.1840. Investors are preparing for the release of key US statistics that could affect expectations for the Fed's future policy.

The focus is on the minutes of the last Fed meeting, a preliminary estimate of GDP, and the PCE core inflation index. The latter is a key policy gauge for the regulator.

The dollar came under pressure last week following softer inflation data, which increased expectations of rate easing in the second half of the year. However, a strong labour market report – showing the highest employment growth in more than a year and an unexpected decline in unemployment – pointed to the resilience of the economy.

The market is now pricing in the first rate cut in June. Overall, around 62 basis points of easing are expected for 2026, corresponding to two 25 bp reductions and roughly a 50% probability of a third step.

Technical Analysis

On the H4 time frame, EURUSD is consolidating after pulling back from January highs. The range has expanded, but the price is gradually moving towards its lower limit.

The key level stands at 1.1835, an intermediate support within the wider range of 1.1765–1.2000. If it holds, sideways movement with attempts to correct upward is likely to persist.

A break below 1.1835 would open the way to 1.1765. A return above 1.1890–1.1900 would ease bearish pressure and return the pair to the middle of the range.

Short-term downward pressure remains on the H1 chart for EURUSD. The price consistently forms lower highs and lows, trading near the bottom of the Bollinger Bands. The middle line acts as dynamic resistance.

The Stochastic oscillator is in the oversold zone, which allows for local rebounds, but the MACD remains in negative territory – momentum is still on the side of sellers. The nearest support is at 1.1835. Securing below it would intensify the decline towards 1.1810–1.1800. Resistance stands at 1.1860–1.1870.

Conclusion

In summary, EURUSD remains under steady selling pressure as markets await pivotal US data that will shape Fed expectations. The pair is testing critical support at 1.1835, with technical indicators confirming bearish momentum despite oversold conditions. The fundamental picture is mixed: softer inflation points to eventual Fed easing, but robust employment data complicates the timeline. The near-term direction hinges entirely on today's releases. A break below 1.1835 would likely accelerate losses towards 1.1765, while a rebound above 1.1890–1.1900 could signal a temporary respite. Until then, the path of least resistance remains lower.

Job Data Adds to March BoE Rate Cut Bets

Markets

US investors return from the long President’s weekend with future markets this morning suggesting that they’ll pick up where they left on Friday. Benign January CPI numbers extended a rally in US Treasuries with the front end (2-yr) at risk of giving away key support at 3.4%. The US 10-yr yield is drifting south to the psychological 4% mark. US money markets suggest more confidence that the Federal Reserve will have leeway to lower its benchmark rate from 3.5%-3.75% to 2.75%-3% by year-end. Today’s thin US eco calendar (weekly ADP numbers and empire manufacturing survey) likely offers little counter-weight to the core bond rally. Especially if risk sentiment hits another snag like equity futures currently suggest. We’ll scan speeches by Fed governors searching for clues about a shift in sentiment in the run-up to the March FOMC meeting. SF Fed Daly and board governor Barr speak during US trading hours. Daly has a more dovish profile and seems to put downside labour market risks ahead of upside inflation risks. She doesn’t vote on policy though this year. Barr has no real track record when it comes to public comments on monetary policy. His voting record is a mirror image of the (majority) consensus. He talks on AI and the labor market at the NY Association for Business Economics in what could be an interesting speech when it comes to interpreting the evolving risk balance around the Fed’s dual policy goals. We’d err on the dovish side of current market pricing given that the next Fed rate cut is only fully discounted by July.

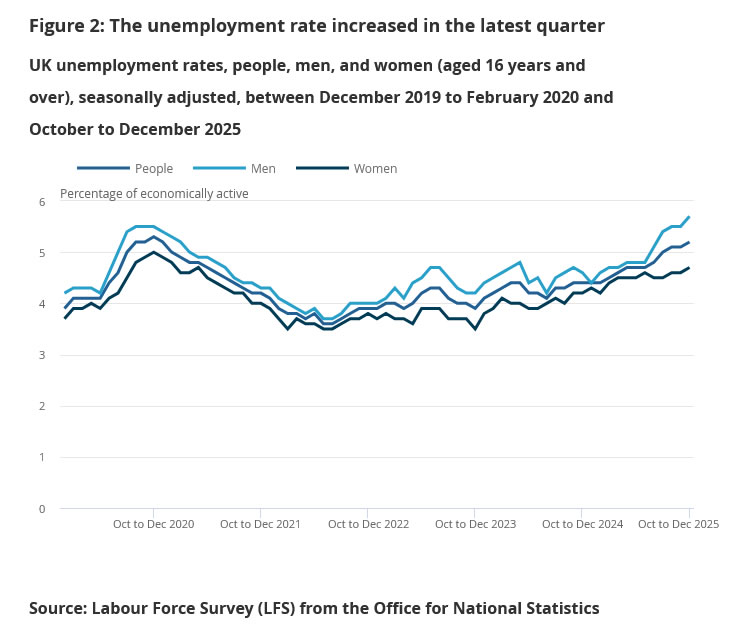

Japanese bonds join the global rally this morning with the curve bull flattening. Yields fall by 4 bps (2-yr) to 8 bps (30-yr). The first auction of conventional JGB’s (5-yr) since the LDP’s huge election victory showed no signs of weakness. USD/JPY holds just below 153. Sterling loses ground (EUR/GBP 0.8720) following monthly labour market data. They show a further moderation in wage growth (4.2%). Weaker than expected employment growth from Q3 to Q4 2025 (+52k vs +108k expected) and January payrolls (-11k) point to a weakening labour market. The unemployment rate rose to 5.2% at the end of last year, only just below the post-pandemic peak of 5.3%. This morning’s numbers will add to March BoE rate cut bets following the close call (5-4) to hold rates unchanged in February. More hawkish members often referred (more evidence of) wage moderation as an important factor to switch sides. British inflation numbers (tomorrow) and retail sales (Friday) are still on tap later this week.

News & Views

Australian central bank policymakers noted the economic outlook had “materially shifted” when it decided to raise rates as the first major monetary authority (excluding the outlier that is the Bank of Japan) earlier this month. The minutes of that meeting released this morning showed that the case was built on a judgment that part of the rise in inflationary pressures would persists amid greater capacity pressures. It flipped the balance of risks around the board’s both objectives of price stability and full employment. RBA members stopped short of flagging more hikes with the minutes stating that “It was not possible to have a high degree of confidence in any particular path for the cash rate”. But inflation in the updated forecast would remain above the mid-point of the 2-3% target range, which policymakers said, if proved true, would mean an extension to “the already long period during which underlying inflation had mostly been above the target range”. Both governor Bullock and deputy Hauser last week suggested further tightening if price pressures would become entrenched. The RBA next meets in March but May is probably more suitable in terms of another hike with Q1 inflation figures available by then.

Fed vice-chair for supervision Michelle Bowman yesterday announced plans to ease US bank capital requirements in an effort to boost mortgage lending. Bowman noted that mortgage activity over the past 15 years had migrated to non-banks, estimating banks’ share in the US mortgage market fell from 60% of home loan origination in 2008 to 35% in 2023. She blamed this shift on “over-calibration of the capital treatment for these activities”, which made “mortgage activities too costly for banks to engage”. Among the changes considered are adjusting the punitive 250% risk weighting for capital purposes as well as turning the standard capital calculation into a more variable one that may take into account parameters such as the size of the loan relative to property value.

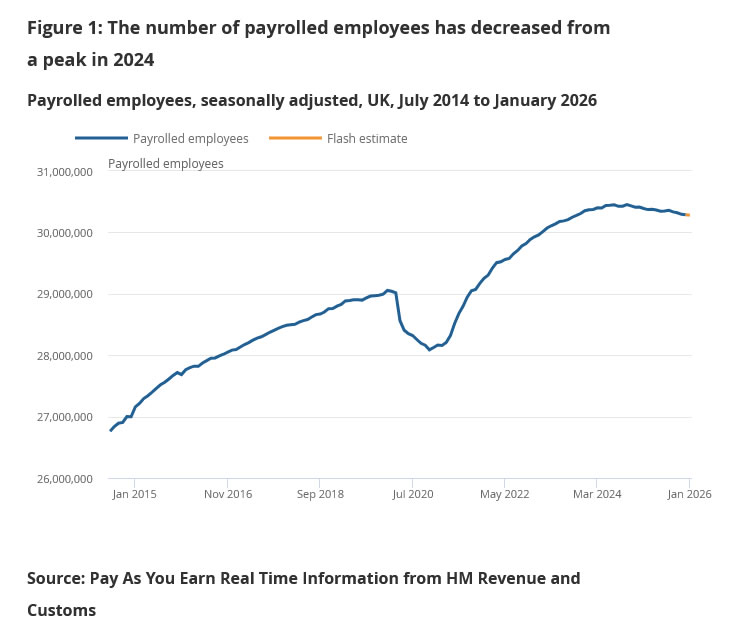

UK unemployment hits five-year high at 5.2%, wage growth slows

UK labor market data pointed to further cooling at the start of the year. Payrolled employment fell by -11k in January and is down -134k over the past 12 months, a -0.4% yoy decline.

Meanwhile, the January claimant count rose by 28.6k, above expectations of 22.8k, signaling rising pressures in the job market. Early estimates for January showed median monthly pay growth ticking up to 4.6% yoy from 4.4%.

In the three months to December, the unemployment rate increased from 5.1% to 5.2% — the highest level since 2020. Wage growth showed signs of moderation. Average earnings including bonus slowed to 4.2% yoy from 4.6%, undershooting expectations of 4.6%. Earnings excluding bonus eased to 4.2% yoy from 4.4%, in line with forecasts.