Sample Category Title

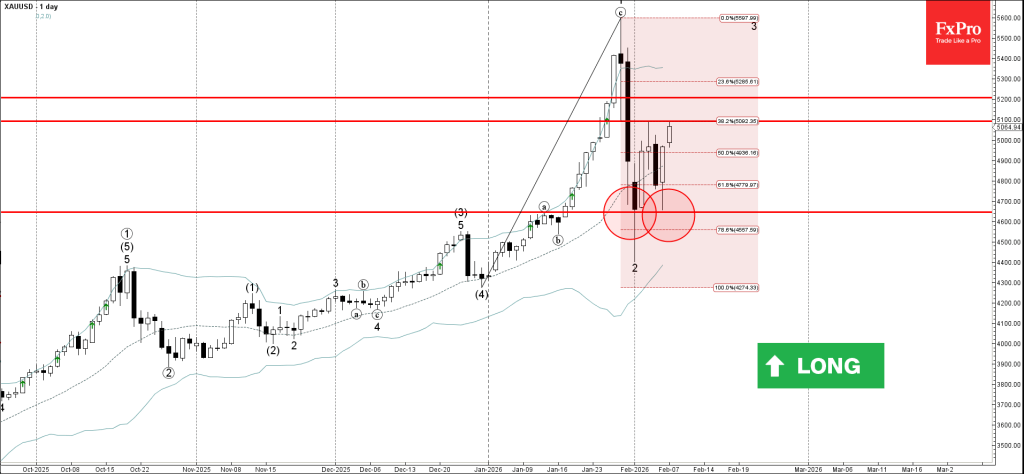

Gold Wave Analysis

Gold: ⬆️ Buy

- Gold reversed from support zone

- Likely to test resistance level 5095.00

Gold recently reversed from the support zone between the strong support level 4645.00 (former resistance from January) and the 61.8% Fibonacci correction of the upward impulse from December.

The upward reversal from this support zone formed the daily Japanese candlesticks reversal pattern Piercing Line.

Given the overriding daily and weekly uptrends, Gold can be expected to rise to the next resistance level 5095.00 – the breakout of which can lead to further gains toward 5200.00.

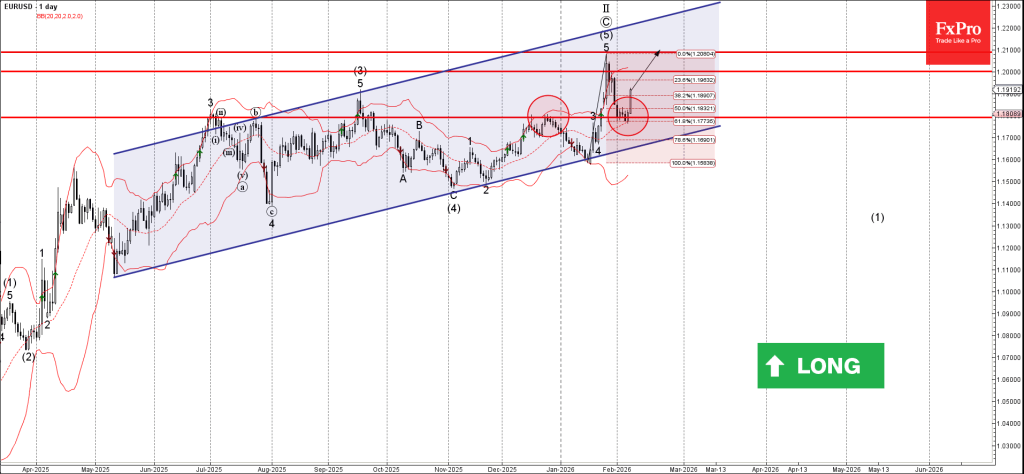

EURUSD Wave Analysis

EURUSD: ⬆️ Buy

- EURUSD reversed from support zone

- Likely to rise to resistance level 1.2000

EURUSD currency pair recently reversed from the support zone between the support level 1.1790 (former double top from December), 20-day moving average and the 61.8% Fibonacci correction of the upward impulse from January.

The upward reversal from this support zone is aligned with the clear uptrend that can be seen on the daily EURUSD charts.

Given the strong daily uptrend, EURUSD currency pair can be expected to rise toward the next round resistance level 1.2000.

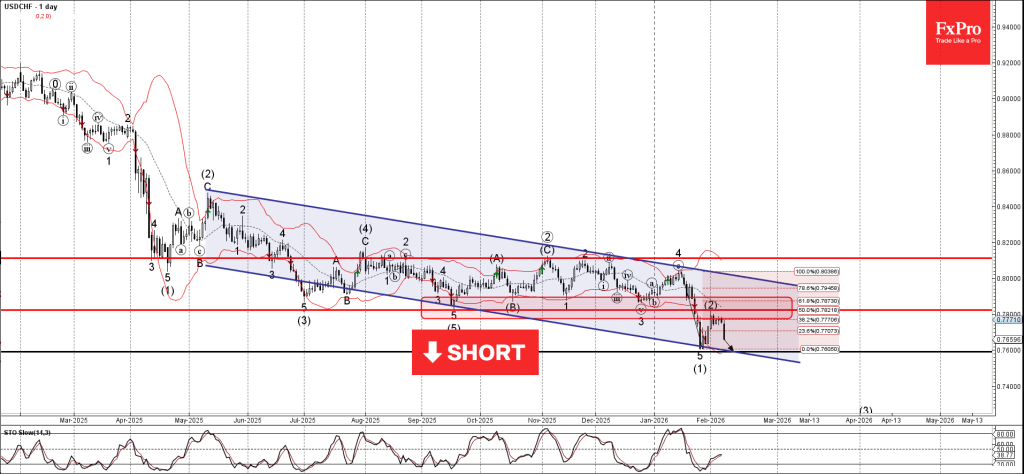

USDCHF Wave Analysis

USDCHF: ⬇️ Sell

- USDCHF reversed from resistance level 0.7800

- Likely to fall to support level 0.7600

USDCHF currency pair recently reversed down from the resistance level 0.7800 (former strong support from September, acting as the resistance after it was broken last month) intersecting with the 50% Fibonacci correction of the downward impulse 5 from January.

The downward reversal from the resistance level 0.7800 started the active impulse wave (3).

Given the clear daily downtrend and the strongly bearish US dollar sentiment seen across FX markets today, USDCHF currency pair can be expected to fall toward the next support level 0.7600 (low of the previous impulse wave (3)).

Sunset Market Commentary

Markets

(Bear) steepening is name of the game today with UK Gilts underperforming. UK yields add up to 8.2 bps at the 30-yr tenor, lifting it to the highest level (5.4%) since mid-November of last year. UK PM Starmer’s chief of staff McSweeney offered his resignation this weekend, taking “full responsibility” for his advice in hiring Peter Mandelson as UK ambassador in the US. It doesn’t take pressure off the PM though with several Labour members suggesting that Starmer should quit his job. McSweeney was credited with taking Labour policy away from the hard-left to a more centrist approach. Markets fear that the (fiscal) credibility of whoever, if any, comes next will be tested. If Starmer stays on, his political mandate will also be significantly weakened. Apart from UK Gilt yields, the higher risk premium is visible in sterling as well. EUR/GBP moves from 0.8682 to 0.8720.

Changes on the US yield curve range between -1.8 bps (2-yr) and +1.5 bps (30-yr). The long end of the curve responded this morning to news that China urged banks to curb US Treasuries exposure in the context of diversifying market risk, but that move didn’t really stick. The front end of the curve will continue to (out)perform, we believe, in the run-up to January non-farm payrolls which are up for release on Wednesday. Last week, some disappointing second tier labour data caused a US jobs recession scare and added to Thursday’s risk-off move. US National Economic Council Director Hassett, long frontrunner to succeed Fed Chair Powell, warned to expect slightly smaller job numbers but that those are consistent with high GDP growth this year because population growth is going down and productivity growth is skyrocketing. It’s unsure whether animal spirits will take into account that disclaimer in case of disappointing data. Today, markets ignored the “lower jobs numbers shouldn’t trigger panic” part of his story. Intraday dollar weakness became more pronounced after the Hassett remarks with EUR/USD starting the week at 1.1816 but currently clearing the 1.19-handle.

USD/JPY (155.50 from 157) moved away from potential FX intervention territory after the landslide LDP-victory in lower house elections. PM Takaichi gets the strong mandate she was looking for with a 2/3rd constitutional majority. Markets take it from the political stability point of view rather than the fiscally irresponsible one. The very long end of the Japanese yield curve erased an initial increase of around 5 bps, unlike the <=10y part of the curve.

News & Views

Norwegian GDP (excluding the offshore energy and shipping industry) grew by 0.4% in the final quarter of last year. The outcome was close to expectations. The Norges Bank (NB) in its Q4 monetary policy report forecasted growth of 0.5%. GDP growth for the mainland economy over 2025 was 1.8% (0.6% in 2024). Growth was driven by solid domestic demand including a 1% Q/Q rise in household consumption and 0.4% Q/Q rise in government consumption. Gross capital formation rose by 7.2% Q/Q. External trade components were reported at 3.6% volume growth for both exports and imports in Q4. Today’s data should confirm the assessment of the Norges Bank that a restrictive policy is needed as inflation is still too high. The NB guided that the policy rate might be reduced later this year, if the economy evolves as expected. The Q4 data release today suggests that there is no need for the NB to rush to rate cuts to support economic activity, as growth is holding up fairly well. The Norwegian krone gains marginally. After the recent (USD & commodity driven) rebound of the krone, EUR/NOK at 11.43 is coming closer to a MT-range bottom in the 11.26 area (2025/2024 lows).

Bank of France governor Francois Villeroy de Galhau announced that he will resign from his job as Bdf head in June of this year. The resignation was due to personal reasons as Villeroy said he will take the opportunity to lead a foundation supporting vulnerable youth and families. His (second) full term was only scheduled to expire end of October 2027. In this respect, it is now up to French president Macron to propose a new candidate for the job. The new candidate will be subject to hearings at the financial committees of the Senate and the National Assembly. They can block the presidents’ choice by a combined overall negative vote of three-fifths over the two Committees. Villeroy was one of the more dovish, heavy-weight, governors at the ECB.

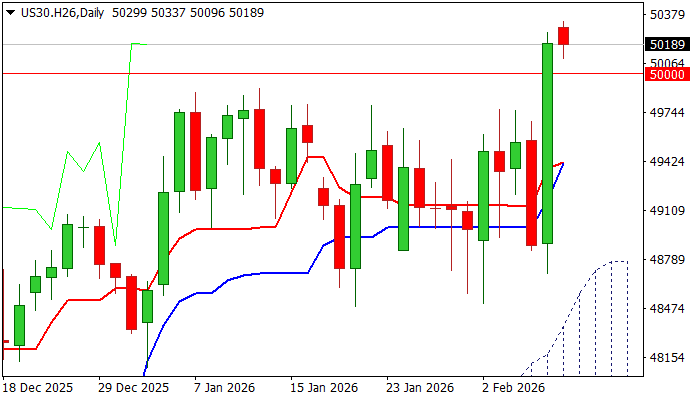

Dow Jones: Bulls Consolidate After Hitting New Record High Above 50K

Dow eases from new record high (50337) on Monday but remains steady and holds above broken magic 50K barrier that was taken out last Friday after almost 2.7% advance (the biggest daily gain since 9 April 2025).

The index outperformed major Wall St peers, with gains of Caterpillar, Goldman Sachs and Nvidia shares being mainly behind the latest strong rally.

Violation and weekly close above 50K (also the top of recent range at 49900) was strong bullish signal which looks for validation on sustained break higher that would open way towards projections at 50434, 50599, 50764 and 51000 round figure barrier.

Positive daily studies (strong bullish momentum, MAs in bullish setup and the action being underpinned by rising and thickening daily cloud) remain supportive, along with formation of bullish engulfing pattern (Friday).

Profit taking after strong gains last Friday should be limited and provide better levels to re-enter bullish market, as overall environment remains positive.

Broken 50000 barrier and 49900 former range top reverted to solid supports which should ideally hold dips and keep bulls intact.

Res: 50337; 50434; 50600; 50764

Sup: 50000; 49900; 49750; 49400

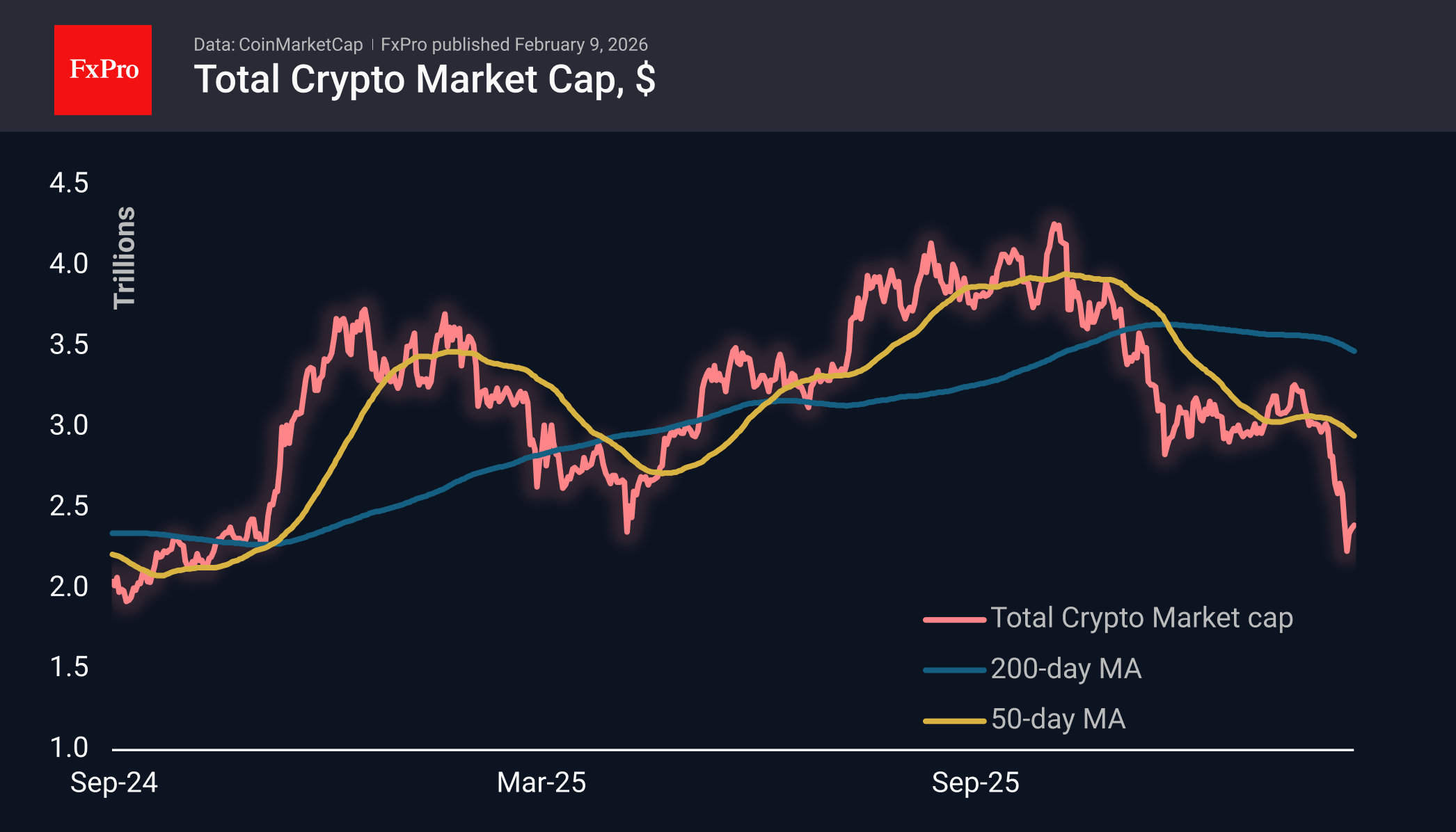

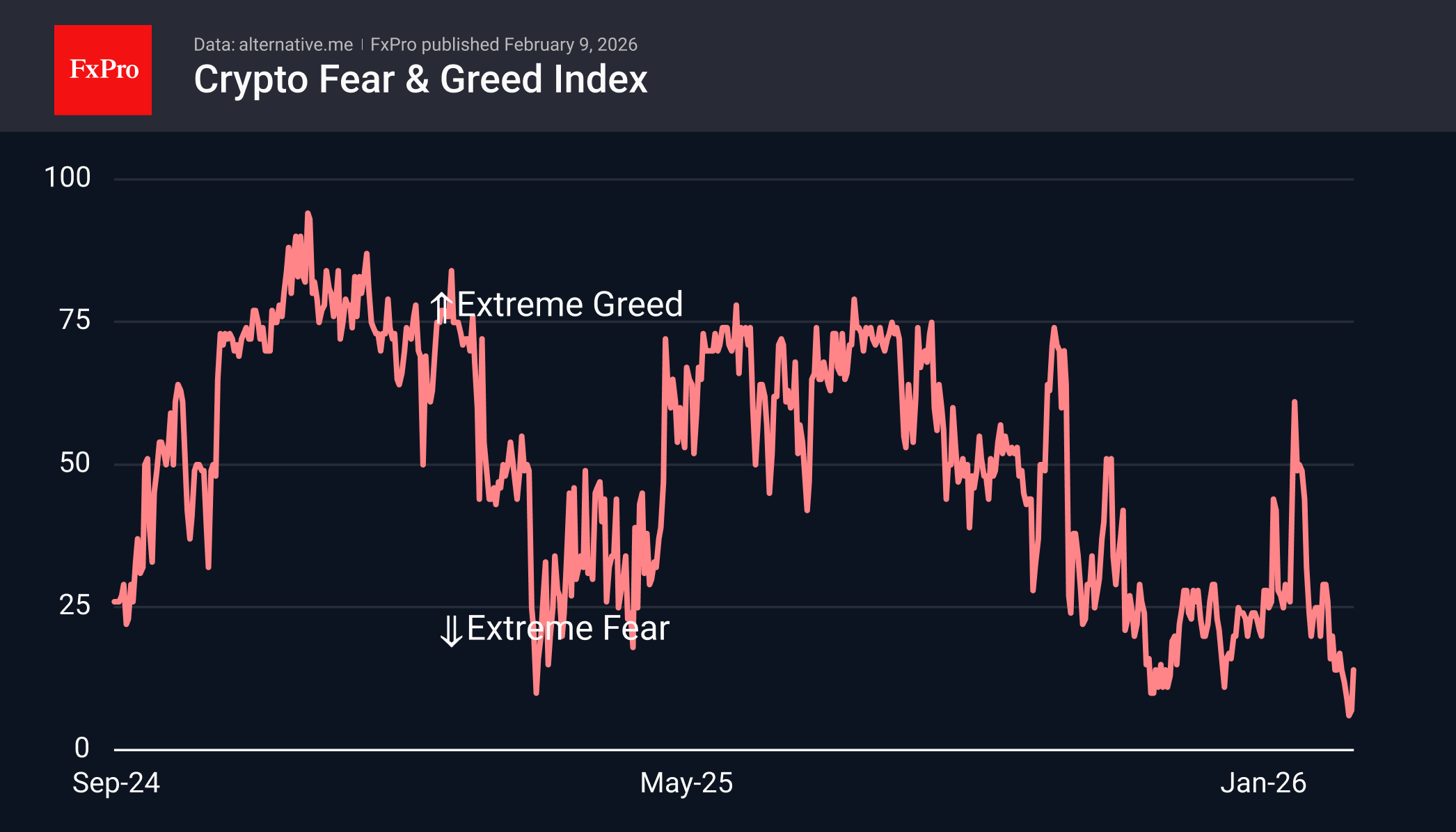

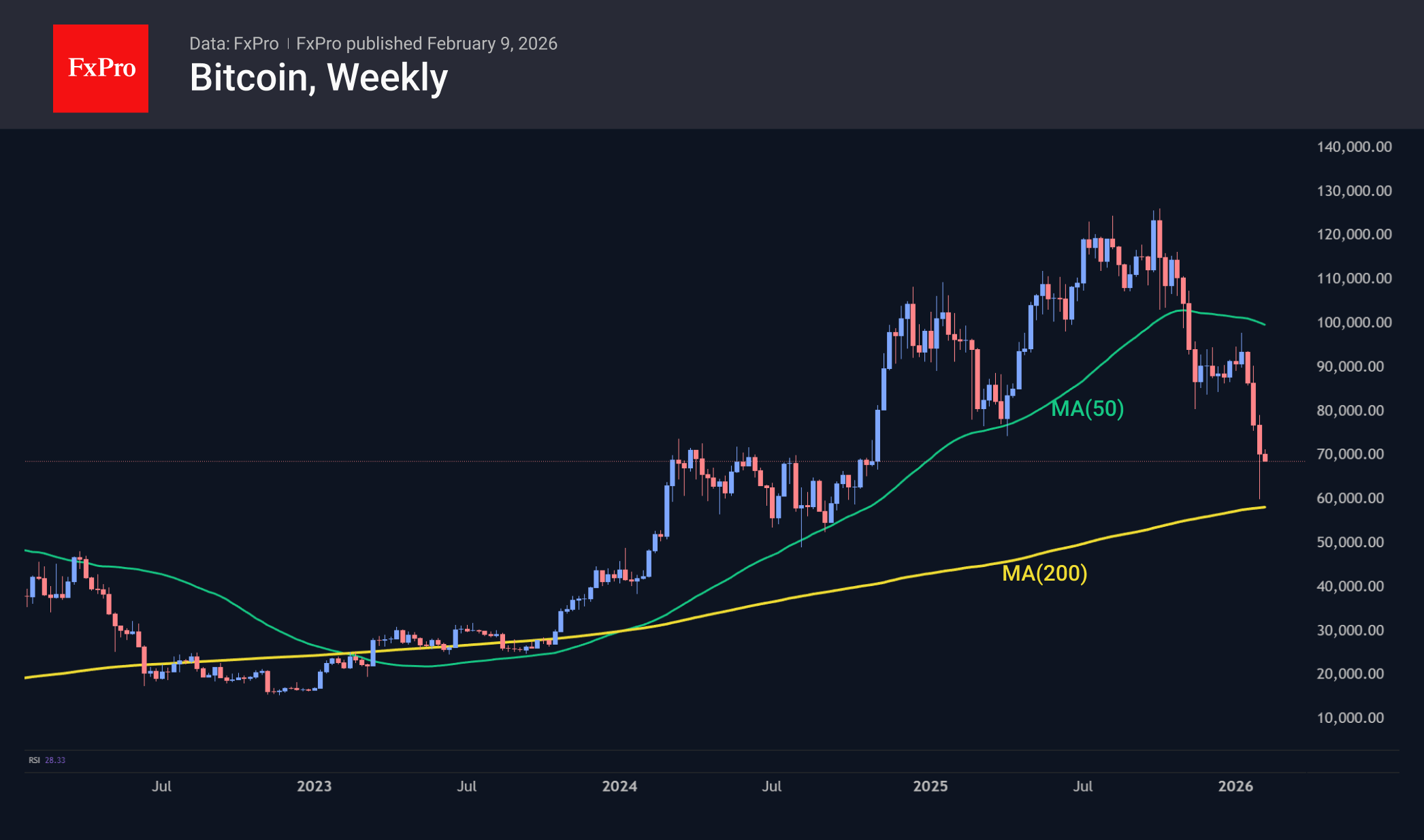

Bitcoin Has Encountered New Resistance

Market Overview

The crypto market cap has declined by approximately 10% over the past seven days to $2.36 trillion. Ironically, this appears to be positive news, as it represents a 10% increase from Friday’s lows. However, we remain very sceptical about the near future, as the recovery momentum lost steam over the weekend, encountering a sell-off near the $2.4T level. Perhaps we have only seen a bounce on the way down, which is not yet complete.

The sentiment index plunged to 6 over the weekend, repeating the lows of June 18-19 from 2022, and we have only seen this indicator lower on August 22, 2019. By Monday, this indicator had recovered to 14, following the quotes. These are still too low levels for confident purchases.

Bitcoin grew steadily on Friday after crashing at the very beginning of the day, but since Saturday, it has faced resistance near $71K. There is still a huge supply in the markets from those who want to exit the first cryptocurrency on the rebound. In such conditions, it is worth being prepared for a new test of the 200-week moving average soon.

News Background

The fall in Bitcoin prices was accompanied by a reduction in liquidity, a surge in volatility, a decline in risk appetite, and an increase in correlation with stock indices. CryptoQuant admits that BTC could fall to $54,600, where the market could move from a phase of capitulation to a phase of accumulation.

Against the backdrop of the crypto market decline, Strategy’s net loss for the fourth quarter was $12.6 billion, according to the company’s quarterly report, and its operating loss reached $17.4 billion. Strategy CEO Fong Le assured investors that risks to the company’s debt servicing would only arise in the event of an extreme drop in BTC to $8,000.

Cardano founder Charles Hoskinson reported unrealised losses of more than $3 billion. He stressed that he does not intend to liquidate positions, even if the market situation worsens.

Bitcoin miners are massively shutting down their equipment due to mounting losses. The BTC mining profitability indicator has fallen to record lows amid a decline in the crypto market and rising electricity prices. JPMorgan estimates the cost of mining to be around $87K.

As a result of the latest recalculation, the difficulty of mining Bitcoin has plummeted by 11.16% to 125.86 T. This is the most significant drop since 2021, when the Chinese authorities banned cryptocurrency mining.

Despite the current negativity, JPMorgan is optimistic about BTC and predicts that in the long term, the first cryptocurrency could reach $266K. Earlier, the bank raised its long-term forecast for gold to $8,000–8,500.

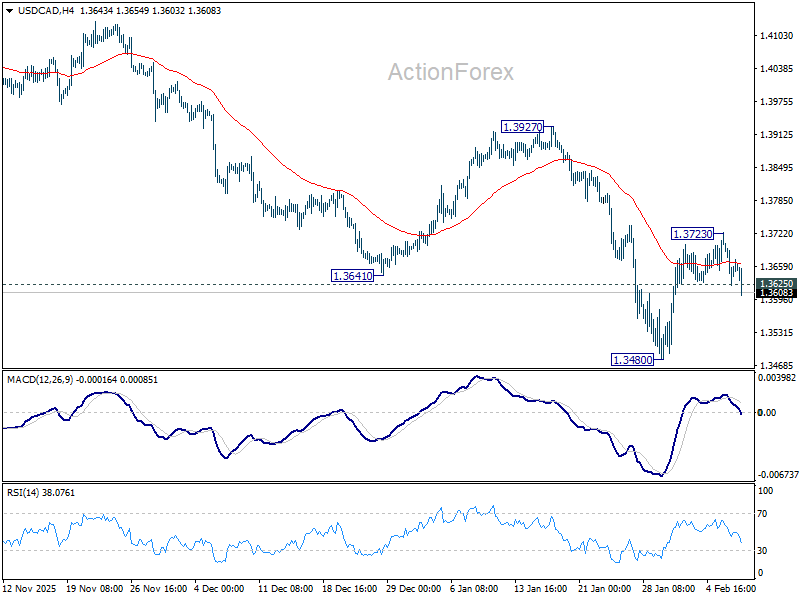

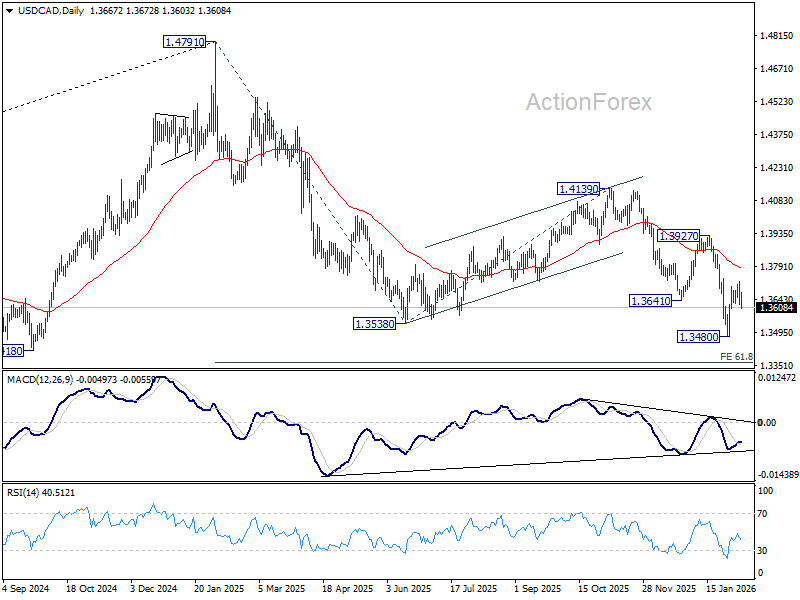

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3624; (P) 1.3675; (R1) 1.3725; More...

USD/CAD's break of 1.3625 support suggests that corrective rebound from 1.3480 has completed at 1.3723 already. Intraday bias is back on the downside for retesting 1.3480 first. Firm break there will resume larger down trend from 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.

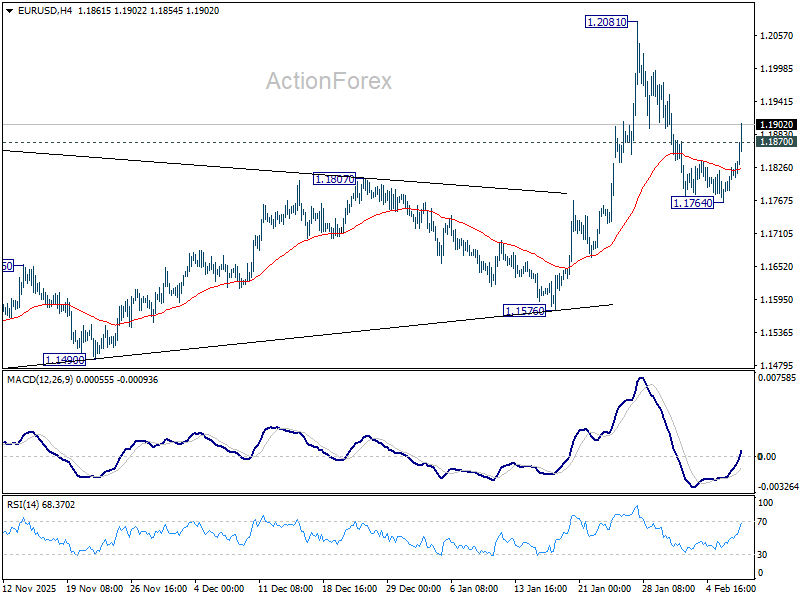

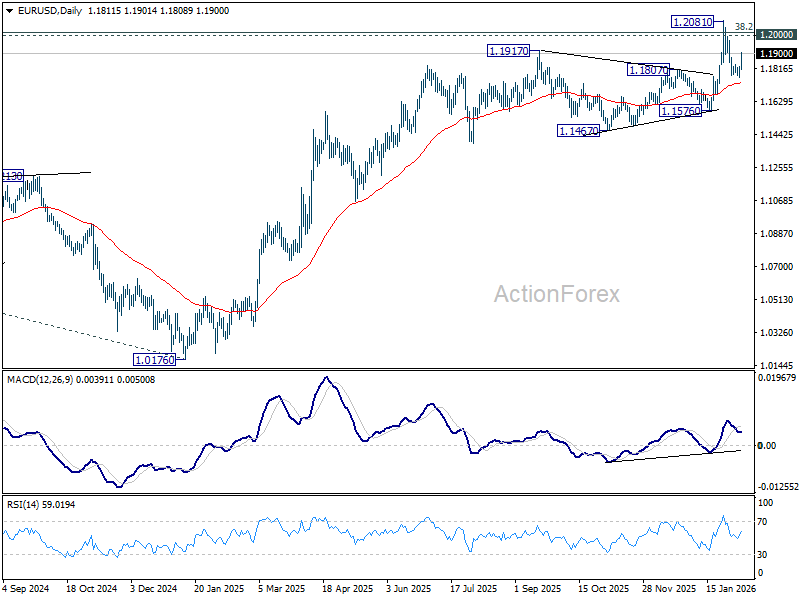

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1780; (P) 1.1803; (R1) 1.1840; More….

EUR/USD's break of 1.1870 minor resistance suggest that pullback from 1.2081 has completed at 1.1764. Intraday bias is back on the upside for retesting 1.2081 high. Decisive break above 1.2 will carry larger bullish implications. On the downside, however, sustained trading below 55 D EMA (now at 1.1730) will raise the chance of reversal on rejection by 1.2 psychological level, and target 1.1576 support for confirmation.

In the bigger picture, as long as 55 W EMA (now at 1.1470) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

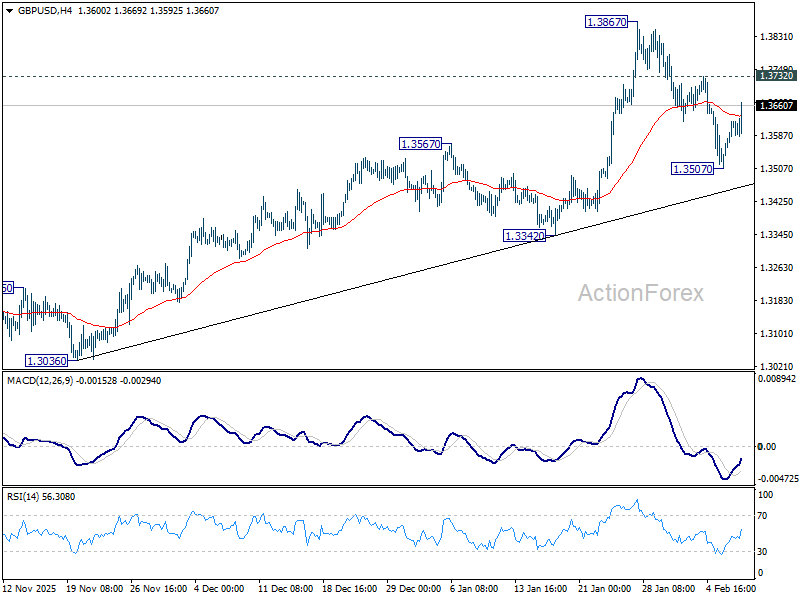

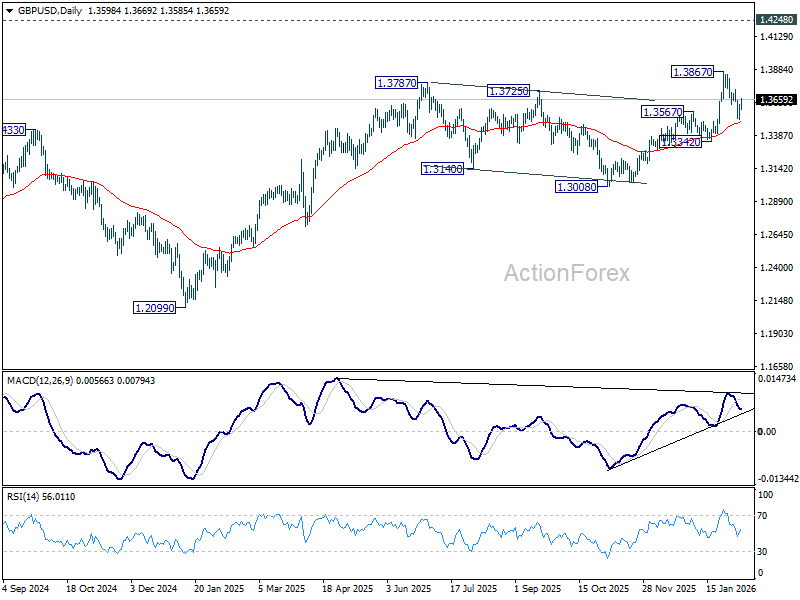

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3540; (P) 1.3581; (R1) 1.3654; More...

Intraday bias in GBP/USD remains neutral for the moment. On the downside, below 1.3507 will resume the fall from 1.3867 to 55 D EMA (now at 1.3490). Sustained break there will raise the chance of larger scale correction, and target 1.3342 support for confirmation. On the upside, above 1.3732 minor resistance will bring retest of 1.3867. Firm break there will resume larger up trend towards 1.4284 key resistance.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.

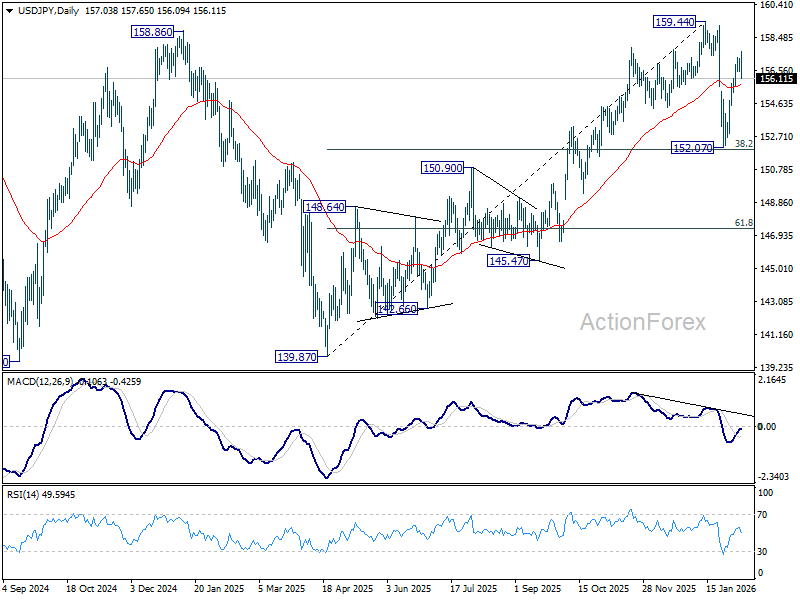

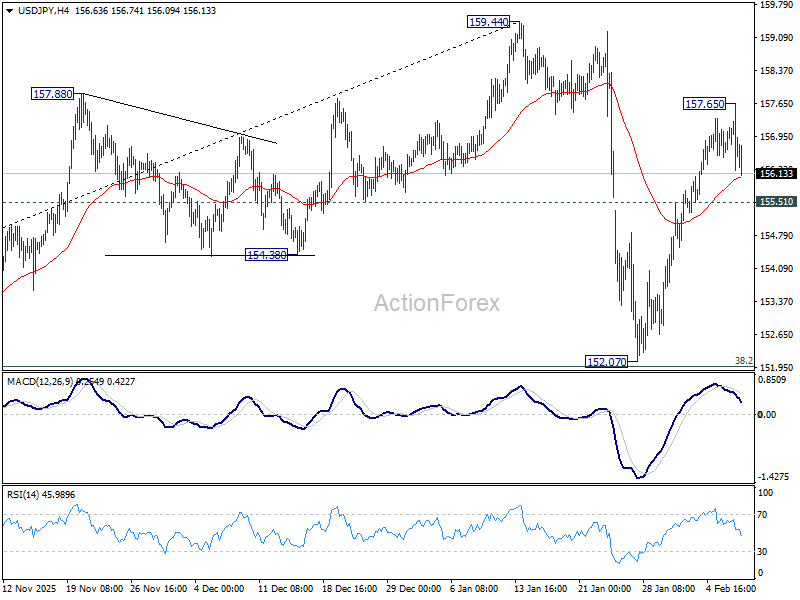

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.75; (P) 157.01; (R1) 157.51; More...

Intraday bias in USD/JPY remains neutral for the moment. Rise from 152.07 is seen as the second leg of the corrective pattern from 159.44. Above 157.65 will target a retest on 159.44 high. However, on the downside, below 155.51 minor support will bring deeper fall as another falling leg. But downside should be contained by 38.2% retracement of 139.87 to 159.44 at 151.96.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 151.68) holds. However, sustained break of 55 W EMA will argue that the pattern from 161.94 is extending with another falling leg.