Sample Category Title

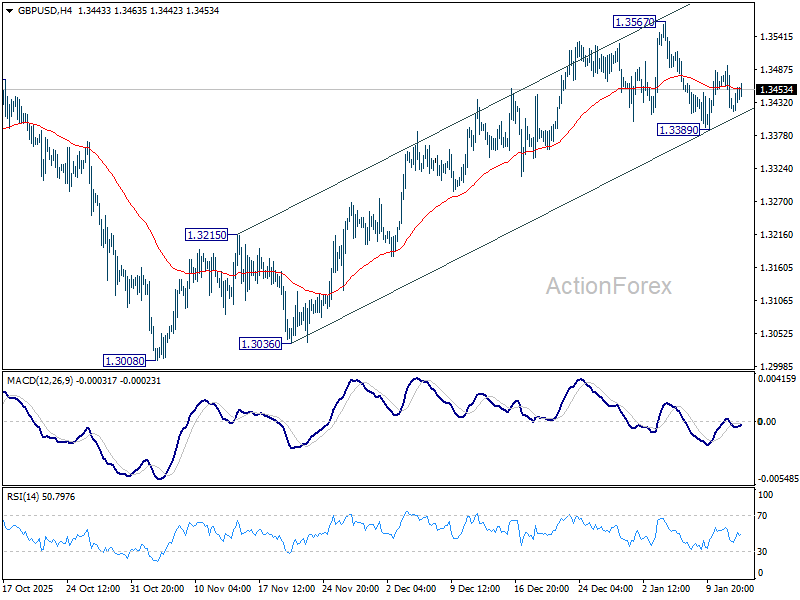

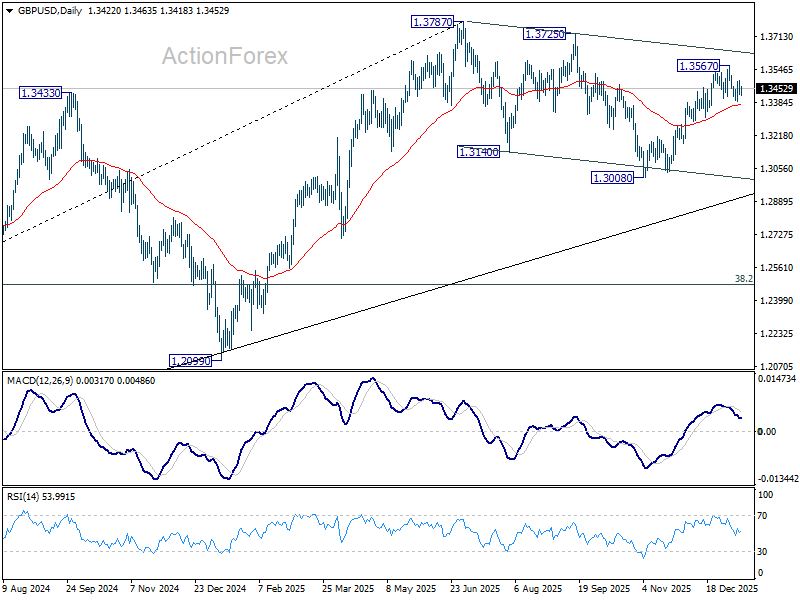

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3397; (P) 1.3446; (R1) 1.3471; More...

No change in GBP/USD's outlook as sideway trading continues and intraday bias remains neutral. On the upside, break of 1.3567 will resume the rally from 1.3008 towards 1.3787 high. On the downside, break of 1.3389 will resume the fall from 1.3567. Sustained break of 55 D EMA (now at 1.3375) will argue that the decline is another falling leg in the corrective pattern from 1.3787. In this case, deeper fall should be seen back to 1.3008 support.

In the bigger picture, price actions from 1.3787 (2025 high) are seen as a correction to the larger up trend from 1.3051 (2022 low). Deeper decline could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.0351 to 1.3787 at 1.2474 to bring rebound. Break of 1.3787 for up trend resumption is expected at a later stage.

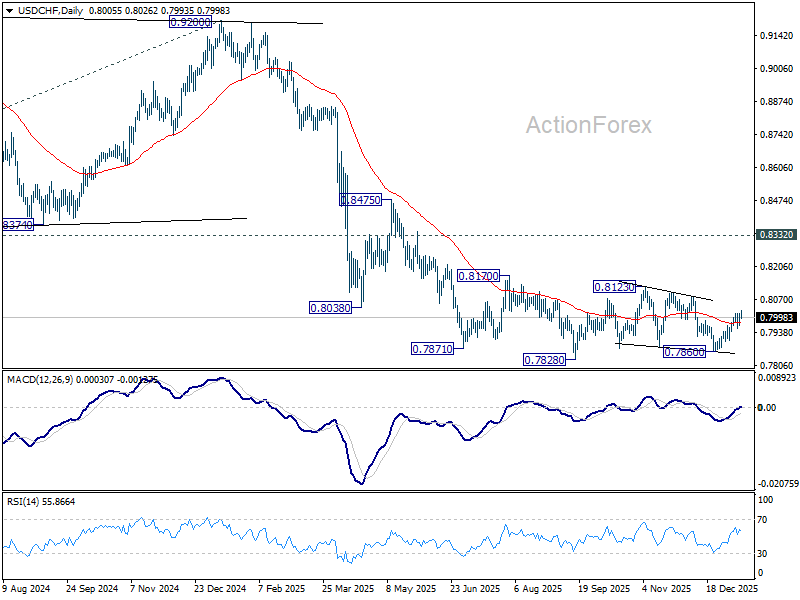

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7981; (P) 0.7998; (R1) 0.8029; More….

Intraday bias in USD/CHF stays mildly on the upside for the moment. Rebound from 0.7860 would target 0.8123 resistance. On the downside, below 0.7954 support will turn intraday bias neutral again first. Overall, corrective pattern from 0.7828 low is in progress and would extend further.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is in still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

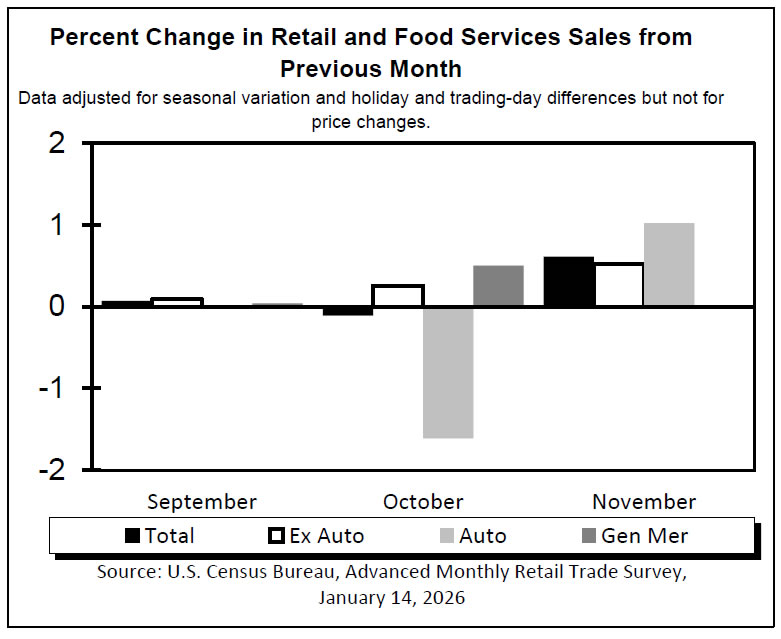

US: Retail Sales Rebound in November

Retail sales rose 0.6% month-over-month (m/m) in November, rebounding from a 0.1% contraction in October. The headline result was stronger than the consensus forecast, which called for a 0.4% m/m gain.

Non-core sales categories were all up on the month, reversing their declines in October. Sales of autos and parts rose by 1% m/m, while sales at gasoline stations increased by 1.4% m/m. Sales at building and garden retailers also improved (+1.3% m/m).

Sales in the "control group", which excludes the three above categories, also rose (+0.4%), although at a slightly slower pace than in October (+0.6% m/m). Strength was seen at clothing retailers (+0.9%), sporting goods (+1.9%), miscellaneous retailers (+1.7%) and non-store retailers (+0.4%). On the other hand, spending was little changed at food & beverage stores, and at electronics & appliance and furniture retailers.

Following a flat performance in October, spending at bars and restaurants rose by 0.6% in November. This is the only service category in the report.

Key Implications

Headline retail sales rebounded in November following a flat reading in the previous month. However, core sales were robust in both October and November, with consumers appearing to have largely shrugged off the impact of the government shutdown. Additionally, various private sector reports indicate that spending was resilient during December's holiday season. Taken together, this suggests that growth in consumer spending was likely stronger in Q4 of 2025 than our earlier tracking of 1.1% (annualized).

We expect consumer spending to remain robust at the start of 2026. Consumers should benefit from previous interest rate cuts as they feed through the economy, some stabilization in the labor market, and non-accelerating inflation. Households will also benefit from the fiscal boost stemming from the OBBBA, as higher tax refunds— which are expected to arrive between February and April—temporarily boost household income and spending.

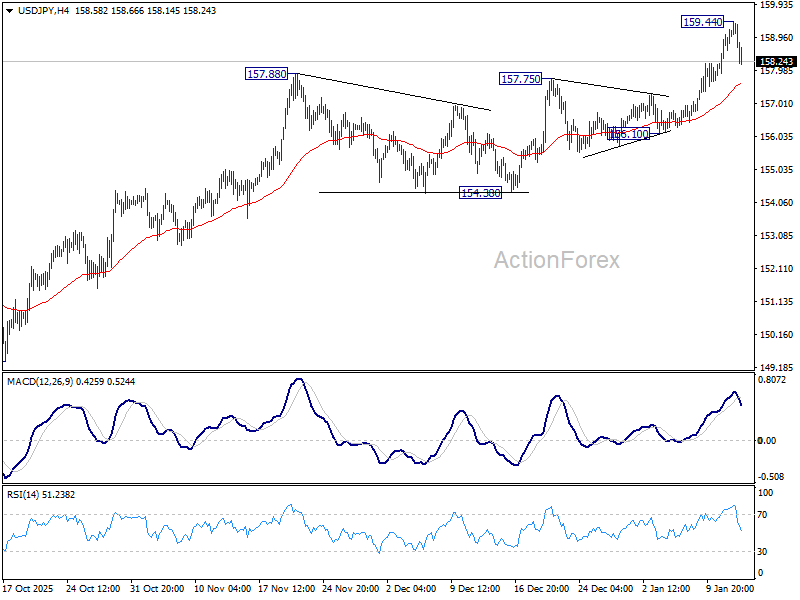

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.32; (P) 158.75; (R1) 159.61; More...

Intraday bias in USD/JPY remains neutral at this point. Retreat from 159.44 temporary top could extend lower. But downside should be contained above 156.10 support to bring another rally. On the upside, above 159.44 will resume larger rise from 139.87. Next target is 200% projection of 142.66 to 150.90 from 145.47 at 161.95, which is close to 161.94 high.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.38 support will dampen this bullish view and extend the corrective range pattern with another falling leg.

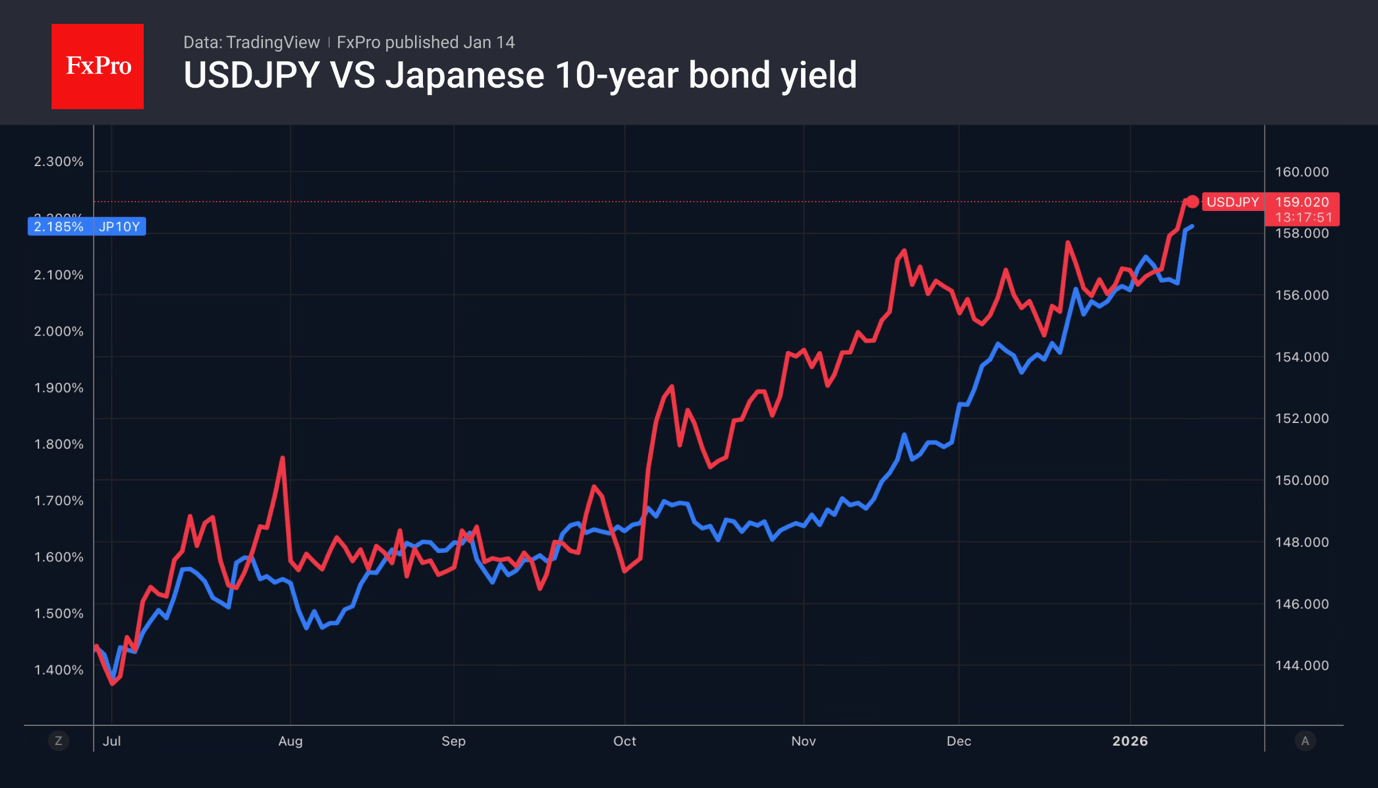

Japan Steps Up Verbal Intervention, Yen Finds Temporary Breathing Room

Yen recovered broadly today after Japan delivered its strongest verbal intervention in months, temporarily slowing the currency’s slide. The shift in tone came as USD/JPY neared 160, its strongest level since July 2024, prompting officials to push back more forcefully against what they described as excessive moves.

Crucially, the rhetoric was aimed at speed and volatility rather than level. Japan has repeatedly stressed opposition to speculative, one-sided moves, without defining a red line or objecting to depreciation per se. That distinction matters for markets still aligned with a structurally weaker-Yen view.

Finance Minister Satsuki Katayama said authorities would “take appropriate action against excessive currency moves without excluding any options,” calling the recent swings “extremely regrettable” and out of line with fundamentals. The comments marked a clear escalation in language, even if no action followed.

Japan’s top currency diplomat Atsushi Mimura echoed the warning, describing recent moves as “one-sided and rapid.” Pressed on whether intervention was on the table, he declined to be specific, stressing that volatility and speculative behavior — not the exchange rate level — were the real concern.

Despite the firmer tone, Yen’s rebound should be treated more as a pause rather than a reversal. The so-called “Takaichi trade” remains firmly in force, with Japanese equities continuing to surge. The Nikkei hit another record today, underlining persistent risk-on sentiment tied to domestic politics.

That backdrop is political. It is now confirmed that Prime Minister Sanae Takaichi plans to dissolve parliament next week and call a snap election, seeking public backing for expansionary spending plans. Liberal Democratic Party Secretary General Shunichi Suzuki said a fresh mandate is needed, noting that the public has yet to pass judgment on the current coalition arrangement. The prospect of fiscal stimulus continues to support equities and weigh on Yen.

Beyond Japan, central-bank independence is spreading as a sensitive global theme. New Zealand Foreign Minister Winston Peters publicly rebuked RBNZ Anna Breman for signing a statement in support of Fed Chair Jerome Powell, arguing the RBNZ should avoid involvement in US domestic politics.

The controversy followed a rare joint declaration by global central bank heads backing Powell and defending monetary independence. Peters said the governor should “stay in her New Zealand lane,” highlighting how politically charged the issue has become even outside the US.

Japan’s absence from the signatories also drew attention. According to government sources, the BoJ consulted officials informally but was unable to approve participation in time, reflecting election sensitivity and the delicate US relationship. Former BoJ board member Takahide Kiuchi said the episode highlight how the BoJ still operates within political constraints, even as it guards its neutrality.

In Europe, at the time of writing, FTSE is up 0.25%. DAX is down -0.37%. CAC is up 0.03%. UK 10-year yield is down -0.021 at 4.381. Germany 10-year yield is down -0.006 at 2.844. Earlier in Asia, Nikkei rose 1.48%. Hong Kong HSI rose 0.56%. China Shanghai SSE fell -0.31%. Singapore Strait Times rose 0.11%. Japan 10-year JGB yield rose 0.019 to 2.186.

US retail sales beat expectations with 0.6% mom growth in November

US retail sales posted a solid upside surprise in November. Headline sales rose 0.6% mom to USD 735.9B, beating expectations of a 0.4% increase.

The gains were broad-based. Sales excluding autos increased 0.5% mom to USD 597.2B, also above forecasts of 0.4%. Sales excluding gasoline climbed 0.6% mom to USD 683.0B. The data suggests that underlying consumption momentum remains intact rather than being driven by volatile components.

On a quarterly basis, total retail sales for the September–November period were up 3.6% from a year earlier.

China's exports jump 6.9% yoy in Dec, US decoupling continues

China’s December trade data surprised to the upside, pointing to resilient external demand despite ongoing tariff tensions. Exports surged 6.6% yoy, more than double expectations of 3.0%. Imports rose 5.7% yoy, far exceeding forecasts of 0.9% and marking the strongest growth since September last year. The trade balance posted a USD 114.1B surplus, broadly in line with expectations.

However, the headline strength masked a deepening collapse in trade with the US. Shipments to the US plunged -30% yoy, extending a ninth straight month of contraction, while imports from the US fell -29% yoy. By contrast, China’s trade with other regions remained robust. Exports to the EU and ASEAN climbed 12% and 11% respectively. While imports from Europe jumped 18%. Imports from Southeast Asia declined -5%.

For the full year, exports grew 5.5% while imports were flat, driving China’s trade surplus to a record USD 1.19T, up 20% from 2024. Trade with the US weakened sharply amid tariff frictions, with exports down -20% and imports falling -14.6%.

Commenting on the data, General Administration of Customs spokesperson Lv Daliang called for dialogue and negotiation, stressing that China–US trade relations should remain mutually beneficial.

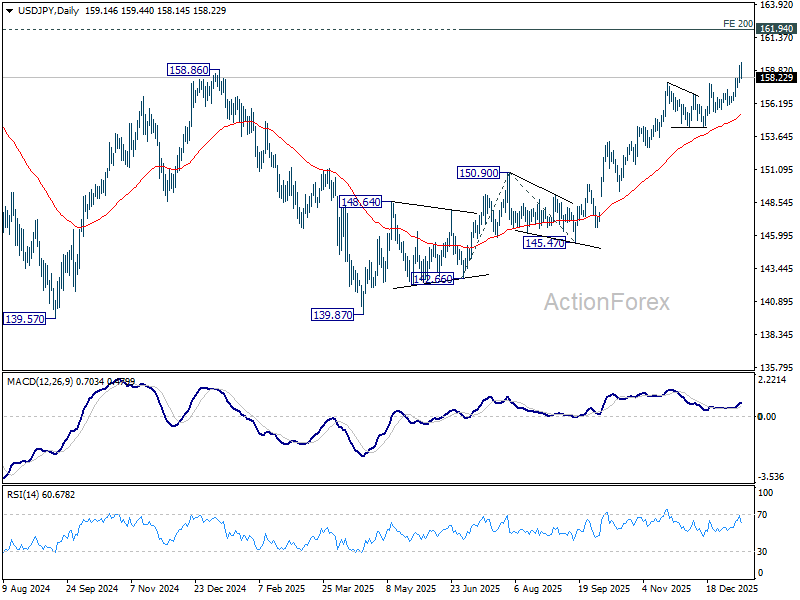

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.32; (P) 158.75; (R1) 159.61; More...

Intraday bias in USD/JPY remains neutral at this point. Retreat from 159.44 temporary top could extend lower. But downside should be contained above 156.10 support to bring another rally. On the upside, above 159.44 will resume larger rise from 139.87. Next target is 200% projection of 142.66 to 150.90 from 145.47 at 161.95, which is close to 161.94 high.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.38 support will dampen this bullish view and extend the corrective range pattern with another falling leg.

US retail sales beat expectations with 0.6% mom growth in November

US retail sales posted a solid upside surprise in November. Headline sales rose 0.6% mom to USD 735.9B, beating expectations of a 0.4% increase.

The gains were broad-based. Sales excluding autos increased 0.5% mom to USD 597.2B, also above forecasts of 0.4%. Sales excluding gasoline climbed 0.6% mom to USD 683.0B. The data suggests that underlying consumption momentum remains intact rather than being driven by volatile components.

On a quarterly basis, total retail sales for the September–November period were up 3.6% from a year earlier.

Chart Alert: Silver (XAG/USD) Resumes Accelerated Uptrend, US$90.90 Upside Trigger to Watch

Key takeaways

Silver breaks into price discovery: XAG/USD has erased its early-January correction, surged alongside gold, and hit a fresh record high above US$91, confirming the resumption of an accelerated short-term uptrend.

Macro tailwinds remain supportive: Rising geopolitical risk premiums, softer US inflation, and expectations of continued Fed rate cuts into 2026 are reinforcing bullish momentum in silver.

Key technical levels to watch: Holding above US$86.27/84.03 keeps the minor uptrend intact, while a sustained break above US$90.90 opens the door toward US$94.60–95.81 and US$98.74–99.46, with a longer-term secular target near US$101.15.

The recent bullish price actions of Silver (XAG/USD) in the past four trading sessions that moved in line with Gold (XAU/USD), another precious metal, have eradicated the earlier expected extended minor corrective decline structure of Silver (XAG/USD) where price staged a prior decline of 10% (high to low) from 7 January to 8 January 2026.

In today’s Asia session, 14 January 2026, Silver (XAG/USD) has continued to extend its up move with an intraday rally of 4.3% to hit another record high of US$91.57 at this time of writing, breaching above the US$90.00 psychological level for the first time.

Macro factors such as rising geopolitical risk premiums in the Middle East arising from Iran’s civil unrest, which may lead to regime change with involvement from the US, together with a likely continuation of the US Federal Reserve’s rate cuts extension into 2026 after US core CPI for December 2025 came in below expectations (both m/m and y/y basis) have served as reinforcing positive feedback loops into Silver (XAG/USD).

Let us now take a look at Silver (XAG/USD) from a technical analysis perspective to decipher its short-term movement (1 to 3 days).

Short-term trend bias (1 to 3 days): Relentless minor uptrend intact

Fig. 1: Silver (XAG/USD) minor trend as of 14 Jan 2026 (Source: TradingView)

Fig. 2: Silver (XAG/USD) long-term secular trend as of 14 Jan 2026 (Source: TradingView)

Watch the US$86.27/84.03 key short-term pivotal support on Silver (XAG/USD) to maintain the short-term minor uptrend phase in motion since the 8 January 2026 low of US$73.84.

A clearance above a major resistance of US$90.90 (depicted on the weekly chart) increases the bullish acceleration mode for Silver (XAG/USD) for the next intermediate resistances to come in at US$94.60/95.81(upper boundary of the minor ascending channel and Fibonacci extension cluster), followed by US$98.74/99.46 (Fibonacci extension cluster).

However, a break with an hourly close below US$84.03 invalidates the minor bullish impulsive sequence to flip the bias back to a likely minor corrective decline sequence again to expose the next intermediate supports at US$79.86 and US$74.07 (also the 20-day moving average).

Key elements to support the bullish bias

- The price actions of Silver (XAG/USD) have continued to trade above its rising 20-day and 50-day moving averages.

- Since 8 January 2026 low of US$73.84, the price actions of Silver (XAG/USD) has evolved into a minor ascending channel.

- The hourly MACD trend indicator has staged an intraday bullish breakout in today’s Asia session, 14 January 2026, above its centreline, which reinforces the ongoing minor uptrend phase for Silver (XAG/USD).

- In a longer-term secular trend structure from an Elliot Wave/Fibonacci analysis perspective, Silver (XAG/USD) is likely in an extended major/secular bullish impulsive up move sequence, labelled as wave III in place since 29 August 2022 low, with the next major resistance coming in at US$101.15 (see Fig. 2).

Dollar Does Not Tolerate Dissent

- US GDP growth is driven not by the White House, but by AI.

- The Bank of Japan’s sluggishness is weighing on the yen.

JP Morgan believes that the White House’s focus on lowering interest rates will have the opposite effect. Inflation will accelerate, and rates will rise. Donald Trump claims that Jamie Dimon is wrong and just wants rates to be high so that his bank can earn more. He went on to describe Federal Reserve Chair Jerome Powell as a “bad person” who, in his view, is hindering the prosperity of the American economy.

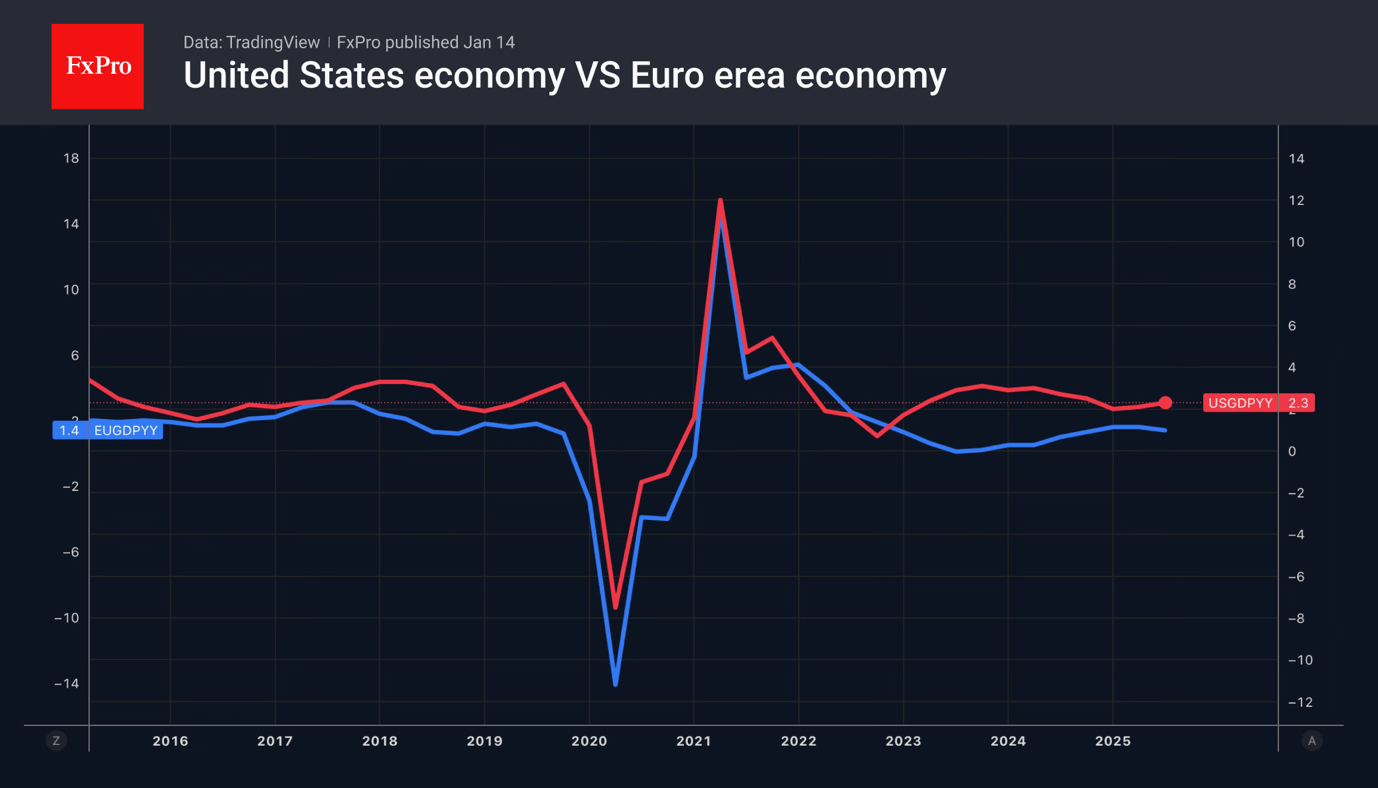

The US economy is indeed pleasantly surprising. The World Bank has pointed to its resilience to tariffs and raised its GDP forecast for 2025 from 1.4% to 2.1% and for 2026 from 1.6% to 2.2%. The growth in these indicators is not based on White House policy, but on large-scale investments in artificial intelligence technology. However, Donald Trump has his own opinion on this matter. According to the president, in 11 months, the American administration has achieved explosive growth in the economy and productivity, victory over inflation, and prosperity in investment. Is more to come?

However, we have to adjust the midterm election promotions. Inflation in the US may have fallen to 2.6-2.7%, but it is still significantly above the 2% target. GDP growth is impressive, but the cooling labour market is causing the Fed to cut the rate from 4.5% to 3.75% in 2025. Currently, FOMC officials believe that monetary policy is well-positioned. They intend to maintain a pause in the cycle, which supports the dollar.

Meanwhile, the yen continues to get battered. Investors expect Sanae Takaichi to dissolve parliament and call new elections as early as February. This is leading to higher Japanese bond yields and a surge in USDJPY to 18-month highs, returning to the previous territory of currency intervention. The stronger the Liberal Democratic Party’s footing, the more chances of higher fiscal stimulus. At the same time, the government may put pressure on the central bank to prevent interest rates from rising, as this increases the cost of servicing the national debt.

In this regard, Kazuo Ueda’s speech on continuing the cycle of monetary policy normalisation while meeting the conditions required by the Bank of Japan can be seen as justifiable. Investors do not expect an overnight rate hike before June, which, against the backdrop of a prolonged pause by the Fed, allows USDJPY to rise.

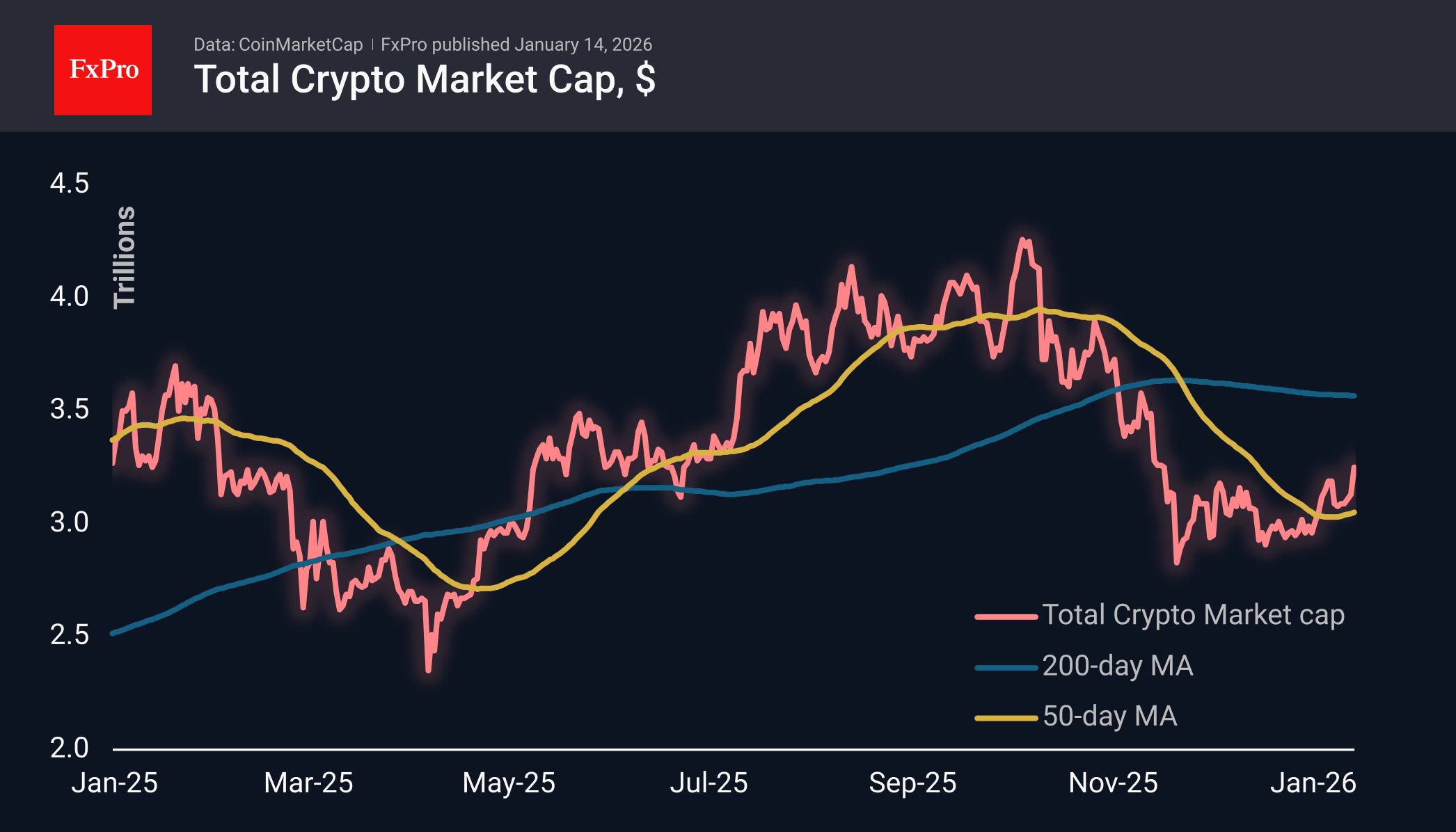

Crypto Market Has Made a Breakthrough

Market overview

The crypto market capitalisation has increased by almost 5% over the past 24 hours to $3.25T. This rise above previous local highs confirms the formation of a bullish trend with a sequence of higher local highs and lows. The crypto market has few technical obstacles until it reaches $3.32T, which is the classic Fibonacci retracement level of 61.8% of the decline from the peak in early October.

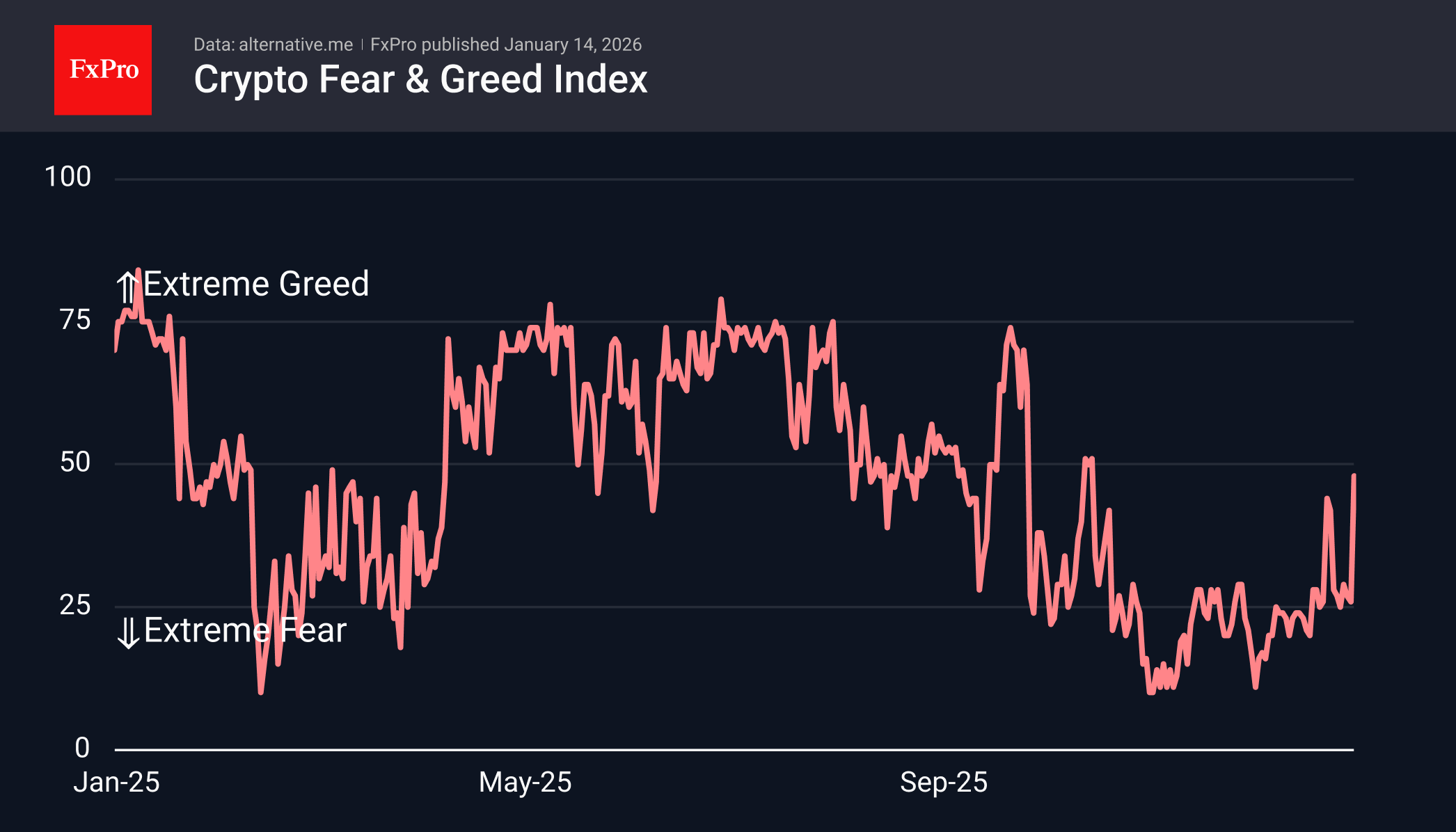

The sentiment index jumped to 48. Although this is the lower half of the sentiment range, we are seeing the highest values for the indicator since the end of October, reflecting a significant change in sentiment. The crypto market did not need support from US stock indices for this, but metals and Asian markets still updated their highs.

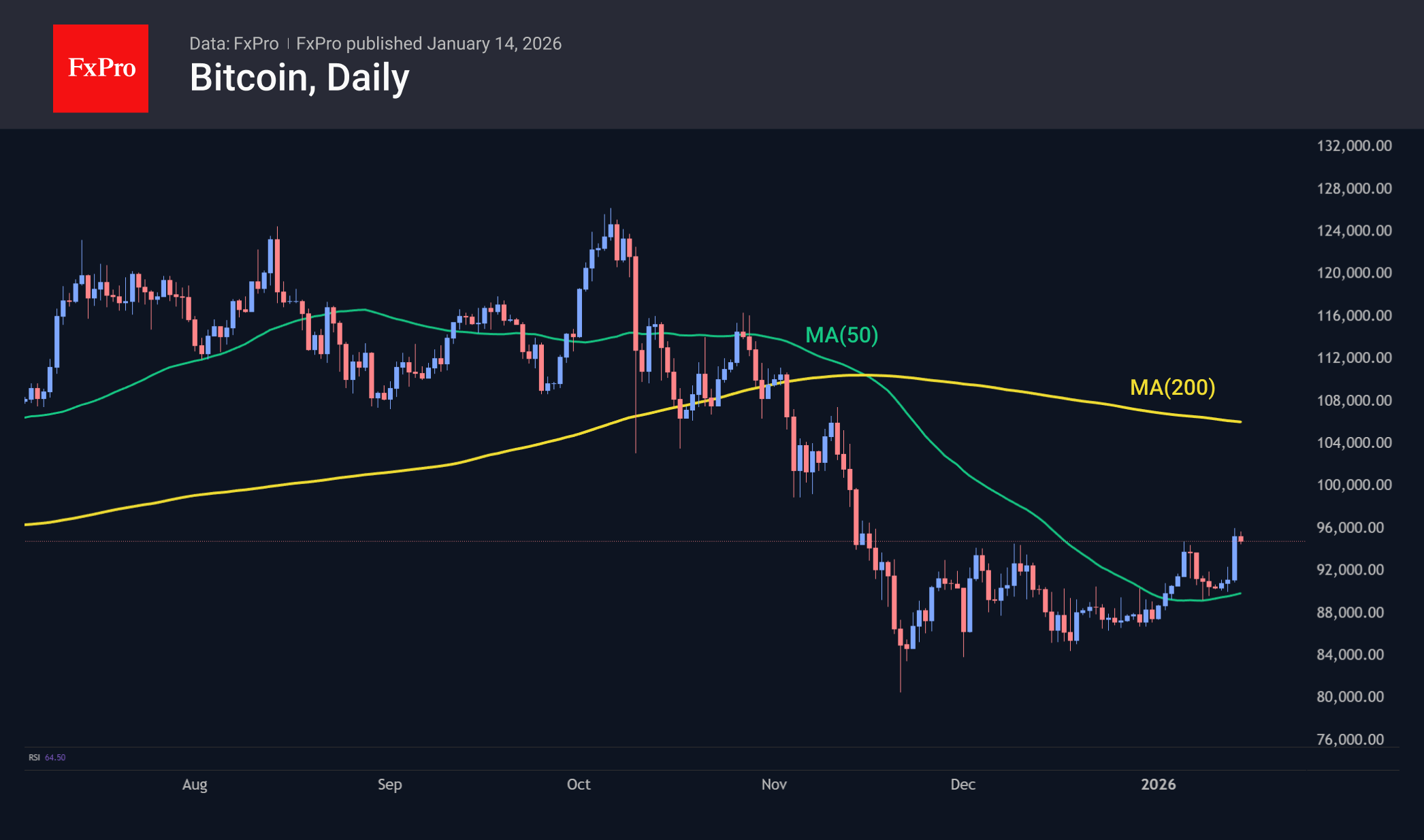

Bitcoin is trading above $95K, its highest since November 17th. It managed to push off the 50-day MA, exceed previous highs and confirm a sequence of higher lows. What other bullish signals do you need? Technically, BTC now has a clear path towards the $100-106K area, limited by the psychologically crucial round level from below and the 200-day MA from above.

News background

The weakening of the US dollar will be a powerful catalyst for Bitcoin’s growth, according to analysts David Brickell and Chris Mills. In their opinion, the first cryptocurrency is the optimal asset for trading depreciation.

Bitcoin is simultaneously forming three serious signals for a decline, notes analyst Doctor Profit. In his opinion, reaching the $70K level is ‘only a matter of time.’

Strategy made its largest weekly purchase of bitcoins since July last year. Between January 5 and 11, the company purchased 13,627 BTC ($1.25 billion) at an average price of $91,519 per coin. Strategy now owns 687,410 BTC, purchased for $51.8 billion at an average price of $75,353 per bitcoin.

BitMine added 24,266 ETH to its crypto reserves last week, accumulating a total of 4,167,768 ETH at an average price of $3,119. The company already owns 3.45% of the total Ethereum supply, with a stated target of 5%.

The collapse of Ethereum’s market value could disrupt the blockchain’s settlement mechanism and cause Ethereum’s infrastructure to collapse, according to a study by the Bank of Italy.

Ethereum co-founder Vitalik Buterin outlined a set of technical requirements that will allow the blockchain to maintain long-term stability without the constant involvement of developers.

Spot crypto market trading volume reached $18.6 trillion at the end of 2025. The figure rose 9% from $17 trillion in 2024, according to CryptoQuant.

Cardano founder Charles Hoskinson called on White House cryptocurrency adviser David Sax to step down from his post for ‘complete failure.’ According to him, since the appointment of the ‘crypto czar’ at the end of 2024, the industry has not seen the progress that everyone was expecting.

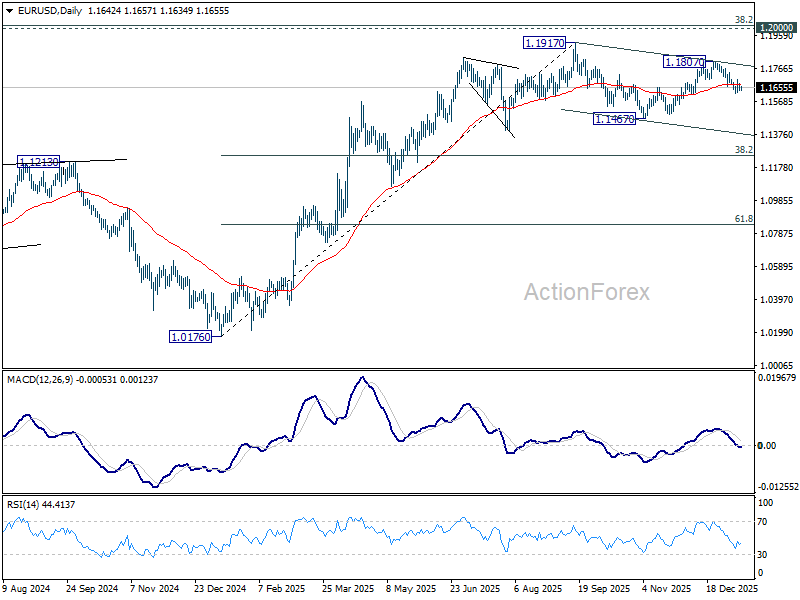

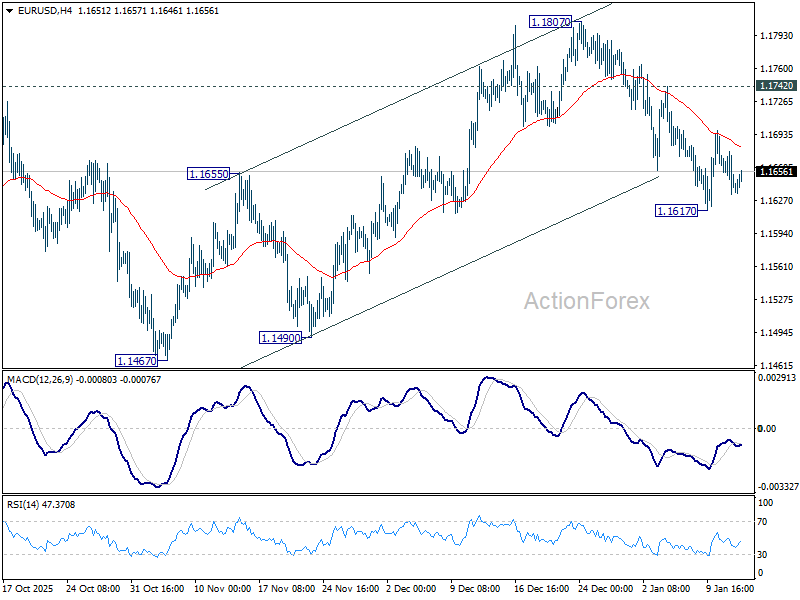

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1626; (P) 1.1652; (R1) 1.1669; More….

Intraday bias in EUR/USD remains neutral as range trading continues above 1.1617. On the upside break of 1.1742 resistance will argue that pullback from 1.1807 has completed. Rise from 1.1467 should then be ready to resume. Further break of 1.1807 will pave the way to retest 1.1817 high. Nevertheless, on the downside, below 1.1617 will target 1.1467 support. Overall, price actions from 1.1917 are seen as a corrective pattern that might extend further.

In the bigger picture, as long as 55 W EMA (now at 1.1416) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.