Sample Category Title

Bitcoin jumps on rebalancing and hedge demand, 98k crucial for bullish reversal

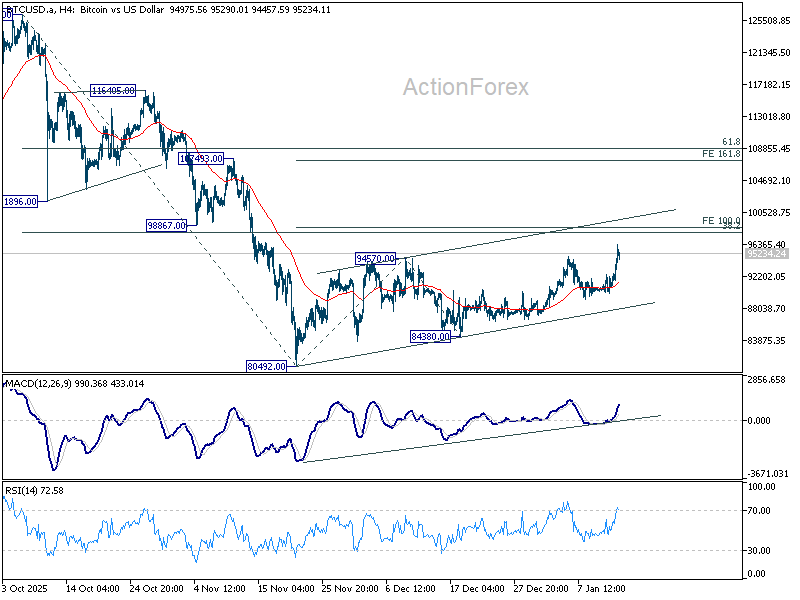

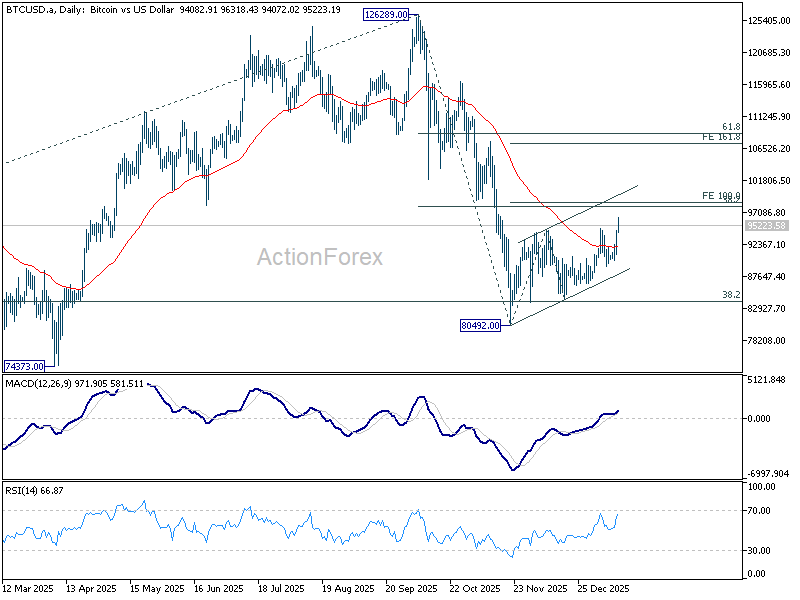

Bitcoin has started the year on a strong footing, surging to a two-month high today as the near-term rebound resumes. The move signals a renewed bid for the world’s largest cryptocurrency after a period of weakness in Q4 last year.

A key driver has been a sharp pickup in institutional flows. U.S. spot Bitcoin ETFs recorded their largest single-day inflows in three months, totaling USD 753.7m on Tuesday. The surge suggests investors are rotating back into risk assets following year-end portfolio rebalancing.

Beyond positioning effects, demand is also being supported by rising geopolitical uncertainty. With tensions intensifying since the start of the year, some investors appear to be revisiting Bitcoin as an alternative hedge alongside traditional safe havens.

A third, more structural factor may also be emerging. Questions surrounding US institutional stability — particularly renewed scrutiny over the Fed — could encourage gradual diversification away from dollar-linked assets, lending longer-term support to "itcoin demand.

Technically, as Bitcoin's rebound from 80,492 resumed, the focus is now firmly on cluster resistance zone around 98k. That area includes 38.2% retracement of 126,289 to 80,492 at 97,986, and 100% projection of 80,492 to 94,570 from 84,380 at 98,458.

Decisive break of 98k zone is needed to solidify the case that "itcoin is reversing the whole down trend from 126,289. In that case, strong rise would be seen back to 61.8% retracement at 108,794 and above.

However, rejection by 98k zone will setup another falling leg to resume the fall from 126,289 through 80,492 at a later stage.

Solidarity in the Face of Trumped-Up Charges

Fed Chair Powell’s principled resistance to the ‘pretext’ DOJ investigation should be no surprise considering his legacy and the values ingrained into monetary policymakers. The public support from other central bank heads shows the role of the BIS-hosted forums and other meetings in building solidarity between them.

- The US Department of Justice’s investigation into and possible criminal charges against Fed Chair Jerome Powell is a whole new level of attempted government coercion of the Fed on monetary policy. Given how ingrained the value of independence is for central bankers, Powell’s strongly worded response is both warranted and unsurprising. We expect him to stay in his post until at least the end of his term as chair in May.

- The extraordinary DOJ action has spurred equally extraordinary, yet also unsurprising, support from other central banks and eminent economists. The relationships built over many meetings in Basel and elsewhere would have been a factor in creating the kind of solidarity that made the central bank statement possible.

- Powell’s response and broad-based support suggest there is a limit to Trump’s ability to coerce the central bank. But with the late January FOMC meeting expected to leave the Fed funds rate unchanged and the next Fed Chair still not announced, the next few weeks could provide to be quite eventful in central banking world.

Over the weekend, the US Federal Reserve received subpoenas related to possible criminal charges against Fed Chair Jerome Powell. Note, no charges have been laid just yet. In response, Powell released a strongly worded video statement, labelling the investigation a ‘pretext’. We think this characterisation is completely warranted, given the administration’s previous actions. The investigation is just the latest attempt to bully the Fed into conducting monetary policy according to President Trump’s wishes, to lower interest rates significantly and boost US demand even as inflation remains above target.

Like Governor Cook before him, we expect Chair Powell to stay in his post until at least the end of his term as chair in May. Although his term on the Board of Governors extends beyond that, typically former Chairs do not remain on the Board once they are no longer Chair. If Powell were to step down from the Board when his term as Chair ends, we would not take that as a signal that the Trump Administration’s pressure tactics were working.

Powell’s resistance should be no surprise to observers of monetary policymaking. Central bankers truly believe – with much justification – that having ‘instrument independence’ (operational independence) is essential for good policy. That is, it is appropriate for government or Parliament to decide what the central bank’s policy should try to achieve, but it should be up to the central bank to work out how to achieve it. This is the distinction between ‘goal independence’ and ‘instrument independence’ first made in the early 1990s in a seminal paper by the eminent academic and central banker, the late Stanley Fischer and his coauthor Guy Debelle. As is well known, Debelle went on to become Deputy Governor of the RBA, and gave his later perspective on central bank independence in a 2017 speech.

Central bankers also know what happens if operational independence is absent. Not only can they point to the example of the 1970s, but also to the more recent experiences of Argentina and Türkiye. Powell would not want his legacy to be the Fed Chair that folded in the face of political bullying.

Powell’s response shows that Fed officials regard the administration as having crossed a line. Politicians will always express views about what they would like central banks to do with monetary policy. And that is their prerogative, no need to be outraged by it. What the current US administration is doing, though, is on a whole other level. Nor is it just about central banks being somehow special. The same principle of operational independence applies to national statistical agencies, though they do not tend to host whole academic conferences to talk about it. The earlier sacking of the head of the Bureau of Labour Statistics needs to be seen as part of the context for Powell’s reaction.

In another extraordinary turn, late in the evening of 13 January Australian time, a group of central bank governors and the Bank for International Settlements (BIS) released a short statement of solidarity with Chair Powell, emphasising the need for central banks to have operational independence. A separate similar statement was released by eminent US economists, including the three previous Fed Chairs. The central banks’ statement was released on multiple web sites (see RBA version here) and very likely organised by the BIS and the European Central Bank (ECB); ECB President Lagarde has previously commented publicly in support of the Fed in forthright terms.

RBA Governor Michele Bullock was among the signatories, along with the heads of the ECB, Bank of England and the central banks of Sweden, Denmark, Switzerland, Norway, Canada, South Korea, Brazil, South Africa and New Zealand. The ECB and RBA versions of the statement both note that other names might be added to the list later; indeed, it seems that the RBNZ was added in a subsequent iteration. The absence of some key countries – including Japan, Mexico and a few other G20 members – is probably not a signal of anything other than a desire to move quickly on the initial statement. Some central bank governors would have wanted to consult with the other members of their board or needed to translate the statement before publishing on their own websites.

The central bank statement should also not be surprising. The need for operational independence of monetary policy is widely viewed as bedrock for central banks more generally, not just the Fed. We should also not underestimate the role of the substantial calendar of meetings of central bankers in building solidarity between them. In this, the role of the BIS is key. It hosts meetings for central bank heads every two months – a significant call on the time of its more far-flung members in the Asian time zone, but a commitment they value and take seriously. On top of this, there are IMF meetings and regional forums where the principal players also interact. These Governors know each other well, so it is no surprise they were willing to support one of their own. It also may have given Powell some moral support to push back in the way he did. Consider also that if he had instead folded under the administration’s pressure, he would have had to face his peers at a couple more meetings in Basel before May.

(Full disclosure: I worked for the BIS in Basel for nearly two years over 2007–08, attended countless meetings there and still jump at the opportunity to attend their annual meeting of private sector chief economists.)

Where to from here? This week’s events suggest that there is a limit to Trump’s ability to coerce the central bank. But this turn of events poisons the well for Powell’s successor – an appointment that is yet to be announced. Who would agree to take a position in government service in the US knowing that you might be subjected to trumped-up criminal investigations?

The next few days and weeks could prove to be quite eventful in the central banking world. A decision to hold rates steady at the next FOMC meeting in late January, as is widely expected, could spark a new round of friction. Look also for potential future Fed Chairs to indicate their support for the principle of operational independence, as Kevin Hassett is reported to have already done.

China’s exports jump 6.9% yoy in Dec, US decoupling continues

China’s December trade data surprised to the upside, pointing to resilient external demand despite ongoing tariff tensions. Exports surged 6.6% yoy, more than double expectations of 3.0%. Imports rose 5.7% yoy, far exceeding forecasts of 0.9% and marking the strongest growth since September last year. The trade balance posted a USD 114.1B surplus, broadly in line with expectations.

However, the headline strength masked a deepening collapse in trade with the US. Shipments to the US plunged -30% yoy, extending a ninth straight month of contraction, while imports from the US fell -29% yoy. By contrast, China’s trade with other regions remained robust. Exports to the EU and ASEAN climbed 12% and 11% respectively. While imports from Europe jumped 18%. Imports from Southeast Asia declined -5%.

For the full year, exports grew 5.5% while imports were flat, driving China’s trade surplus to a record USD 1.19T, up 20% from 2024. Trade with the US weakened sharply amid tariff frictions, with exports down -20% and imports falling -14.6%.

Commenting on the data, General Administration of Customs spokesperson Lv Daliang called for dialogue and negotiation, stressing that China–US trade relations should remain mutually beneficial.

Japanese Takaichi Trade Continues This Morning

Markets

Last week’s payrolls ended the debate on whether or not the Fed should further reduce its policy rate anytime soon. They simply weren’t weak enough for the US central bank to neglect the fact that it is taking too long to bring inflation back to its policy target. Yesterday’s US inflation figures in this respect didn’t bring profound new insights. Headline inflation was exactly in line with expectations at 0.3% M/M and 2.7% Y/Y. Core inflation was marginally softer than expected at 0.2% M/M and 2.6% Y/Y. In a first reaction, markets tried to embrace this perceived softness. However, with a lot of statistical noise from the shutdown playing on the background, markets soon concluded that it was futile to try to draw any firm conclusions on the timing of the next Fed rate cut. Except for political pressure, the Fed finds itself in a good place to wait and see. After rising slightly in the run-up to the release, US yields at the end of the day changed less than 1 bp across the curve. A $22bn 30-y bond auction didn’t cause any ripples on broader interest rate markets. There’s no indication that the debate on Fed independence has any material impact on LT US risk premia for now. European yields also found some kind of short-term equilibrium. German yields changed between -0.3 bps (2-y) and +1.7 bps (30-y). The lingering unease about Fed independence for now also has little negative impact on the dollar. DXY reversed Monday’s setback (close 99.13). EUR/USD slipped back to close at 1.164. Geopolitical considerations add to the market conclusion that other majors including the euro aren’t a real alternative to the dollar. In this respect, metals (gold, silver but also the likes of copper and tin) nearing/hitting record levels seem to reflect a better store of value.

The Japanese Takaichi trade continues this morning after recent headlines suggesting that the Japanese Prime Minster might call snap elections, maybe as soon as next month. Japanese equities continue their record race (Nikkei + 1.5%). Japanese yields remain upwardly oriented. This time it’s the turn of the 5-y yield to touch a new historic top (1.61%). The yen (USD/JPY 159.1) continues fighting an uphill battle as markets try to find out where Japanese authorities might step in with interventions. At least for now, this fear apparently isn’t that big. Later today, the eco calendar contains December US PPI price data and retail sales. However, with the payrolls and the inflation data unable to move positioning, it is unlikely that those reports will do the job. Markets will also keep a close eye on the US Supreme Court today which might bring a verdict on the US IEEPA import tariffs. Markets also prepare for the earnings season, with some major US banks reporting Q4 resuts.

News & Views

China’s trade surplus hit a record $1.2tn last year. December’s trade balance came in at $114.14bn, data showed this morning. 2025 was nothing but a bumper year for Chinese trade, with monthly surpluses having hit records in four of the 12 months. While US exports have fallen off a cliff due to import tariffs (-20% y/y for the full year of 2025, Bloomberg calculates), inbound shipments to Africa picked up sharply (by 26% y/y). China also got a bigger foothold in Southeast Asia (+13%), the EU (+8%) and Latin America (+7%). Not only trade flows got rewired, the composition of exports did as well. High(er)-value goods surged with the likes of semiconductors, cars and ships recording +20% gains. Toys, shoes and clothing on the other hand contracted.

The International Energy Agency in its monthly Short Term Energy Outlook Report expects that lower oil prices will cut US drilling activity and reduce the top producing country’s output by 1% this year. The IEA estimates Brent crude oil prices to average $56 a barrel this year, down from $69 in 2025 amid global production continuing to outpace demand, resulting in a buildup of inventories. This forecast was made under the assumption of Venezuelan sanctions to remain in place through 2027. If these are to be lifted further and other US government policy related to Venezuela leads to increased production in the oil rich Latin American country, oil prices could fall more steeply than currently expected, the IEA said.

EUR/USD Retreats as USD/JPY Rally Puts 160 in Sight

EUR/USD failed to clear 1.1700 and trimmed some gains. USD/JPY managed to reclaim 158.00 and might aim for more gains.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro started a downside correction from the 1.1700 pivot zone.

- There is a bearish trend line forming with resistance at 1.1660 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY climbed higher above 158.50 and 159.00.

- There is a bullish trend line forming with support near 158.50 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair started a fresh increase from 1.1620. The Euro cleared a few key hurdles near 1.1650 to move into a positive zone against the US Dollar.

The pair settled above 1.1680 and the 50-hour simple moving average. A high was formed at 1.1698, and the pair started a downside correction. There was a drop below 1.1650 and the 50% Fib retracement level of the upward move from the 1.1618 swing low to the 1.1698 high.

However, the bulls are active above 1.1640 and the 76.4% Fib retracement. On the upside, the pair is now facing bears near 1.1650 and 1.1660. There is also a bearish trend line forming with resistance at 1.1660.

The next breakout region sits at 1.1675. An upside break above 1.1675 could set the pace for another increase. In the stated case, the pair might rise toward 1.1700.

Immediate support is 1.1640. The first major key area of interest on the EUR/USD chart is near 1.1620. If there is a downside break below 1.1620, the pair could drop toward 1.1565. The next key breakdown area sits at 1.1550, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a major increase from 157.00. The US Dollar gained bullish momentum above 158.00 against the Japanese Yen.

It settled above the 50-hour simple moving average and 158.80. The upward move was such that the pair even tested 159.50. A high was formed at 159.45 and the pair is now consolidating gains. There was a minor pullback below 159.20.

The pair tested the 23.6% Fib retracement level of the upward move from the 157.89 swing low to the 159.45 high. The current price action is positive, and the pair seems to be aiming for more gains. There is also a bullish trend line forming with support near 155.50 and the 61.8% Fib retracement.

Immediate resistance on the USD/JPY chart is near 159.45. The first key hurdle sits at 159.50. If there is a close above 159.50 and the RSI moves above 75, the pair could rise toward 160.00.

The next stop for the bulls might be 160.80, above which the pair could test 162.00 in the coming days. On the downside, the first major support is 159.10. The next area of interest could be near the trend line at 158.50.

If there is a close below the trend line, the pair could dip and test 157.90. Any more losses could open the doors for a move toward 156.90.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Chart Alert: Gold (XAU/USD) on the Brink of Bullish Acceleration, US$4,780 Next

Key takeaways

Gold breaks into price discovery: XAU/USD reversed sharply from a shallow pullback, cleared its prior all-time high, and is now entering a bullish acceleration phase, with US$4,780 emerging as the next upside target if momentum holds.

Macro backdrop strongly supportive: Softer US labour data, cooler-than-feared core inflation, rising geopolitical risk, and mounting concerns over Fed independence are reinforcing demand for gold as a defensive asset.

Technical and intermarket signals align: Gold remains firmly above its rising 20- and 50-day MAs, momentum is constructive, and capped US real yields are reducing opportunity costs, supporting further upside as long as US$4,512 holds.

The price actions of Gold (XAU/USD) have only done a shallow, minor corrective pull-back towards the first immediate support zone of US$4,430/4,403 (printed an intraday low of US$4,407 on last Thursday, 8 January 2025.

Thereafter, the yellow metal underwent a bullish reversal and surged above its prior all-time high of US$4,550, set on 26 December 2025. In today’s Asia session, 14 January 2026, it traded firmer, rallied by 0.8% to hit another intraday all-time high of US$4,639 on the time of writing.

These are the four key near-term supporting macro factors

A soft US labour market (non-farm payroll for December missed expectations).

US inflation is not as red hot as feared (US core CPI for December came in below that expected on both m/m and y/y).

Fed’s independence at stake; after a surprising US Department of Justice’s criminal charge being slapped on Fed Chair Powell, in a possible attempt to remove him as a Fed Governor after his chairmanship ends in May.

Rising geopolitical risk premium in the Middle East arising from Iran’s civil unrest, which may lead to regime change with involvement from the US.

Let us now decipher the next short-term movement in Gold (XAU/USD) based on a technical analysis perspective.

Short-term trend bias (1 to 3 days): Bullish acceleration

Fig. 1: Gold (XAU/USD) minor trend as of 14 Jan 2026 (Source: TradingView)

Fig. 2: 10-year US Treasury real yield major trend with Gold (XAU/USD) as of 14 Jan 2026 (Source: TradingView)

Watch the US$4,512 key short-term pivotal support on Gold (XAU/USD). A clearance above US$4,645 increases the odds of a bullish acceleration towards the next intermediate resistances at US$4,684/4,687, US$4,720, and US$4,774/4,780 (Fibonacci extension clusters) (see Fig. 1).

On the flip side, a break and an hourly close below US$4,512 negates the bullish tone to open up scope for another round of minor corrective decline sequence to expose the next intermediate support zone at US$4,430/4,403 (also the rising 20-day moving average).

Key elements to support the bullish bias

- Price actions of Gold (XAU/USD) remain in a constructive minor and medium-term uptrend phases as it continues to trade above its rising 20-day and 50-day moving averages.

- The hourly RSI momentum indicator of Gold (XAU/USD) is holding above a parallel ascending trendline at the 50 level, which suggests a potential short-term bullish condition.

- Intermarket analysis: Since 10 December 2025, the 10-year US Treasury real yield (after subtracting the 10-year US breakeven rate that measures US inflationary expectations in the next 10 years) has been capped by its 200-day moving average and a key medium-term resistance at the 1.87% level. These observations suggest that opportunity costs of holding gold are unlikely to see upside pressure, in turn, increasing the demand for gold (see Fig. 2).

Politics at the Heart of the Price Action

US stocks consolidated gains near record highs, as soothing inflation data from yesterday was blurred by concerns over Federal Reserve (Fed) independence and broader political noise.

Looking at the data, the US CPI came in largely in line with expectations. Headline inflation held steady at 2.7% y/y, while core inflation eased to 2.6% — slightly below consensus. Cherry on top for Fed doves: real earnings fell in December, a development that could help cool demand and keep inflation in check.

Still, the US 2-year yield hovered above the 3.50% mark, while the probability of a March rate cut slipped below 30%, down from around 50% last week. US PPI data is due today, but even a soft print may fail to revive dovish Fed expectations.

Why? Because market pricing is no longer driven solely by economic data — politics is playing an increasingly central role.

In particular, broad support for Jerome Powell amid the DOJ-related controversy appears to be influencing markets. JPMorgan CEO Jamie Dimon said yesterday that attacks on the Fed by the Trump administration could “backfire and push borrowing costs and inflation higher.” He’s right: cutting rates more than necessary today risks higher inflation tomorrow, keeping borrowing costs elevated for longer.

That dynamic is pushing longer-dated yields higher and steepening the US yield curve — hardly the outcome the White House would prefer. Still, Donald Trump appears unmoved. Either way, with the next Fed Chair announcement approaching, concerns around Fed independence are likely to remain firmly in the headlines. These worries continue to weigh on the US dollar and Treasuries, while supporting gold and silver, both of which are rallying to fresh records. Silver traded above $91 per ounce in Asia this morning.

On the US economy, Jamie Dimon reiterated that growth remains “resilient,” noting that consumers continue to spend and businesses are generally healthy.

Turning to JPMorgan’s own results, Q4 earnings were solid overall, with stronger-than-expected profits helped by trading and interest income. However, earnings were held back by a large one-off cost linked to the Apple Card business, while dealmaking revenue missed estimates due to transaction delays into this quarter. The stock fell more than 4% post-earnings, the S&P 500 and Nasdaq 100 also fell.

Still, JPMorgan’s broader assessment of the US economy remained constructive — supportive for the wider equity complex. Today, Bank of America, Wells Fargo and Citigroup head to the earnings confessional.

Zooming out, S&P 500 companies are expected to deliver more than 8% earnings growth overall. Technology is once again expected to do the heavy lifting, with Q4 revenues seen growing around 18–20% — strong, but moderating compared with prior quarters.

That said, US tech is priced close to perfection. Impressive headline numbers alone may not be enough to spark fresh rallies. Investors will dig deeper into how revenues and loans are booked, ensuring the figures reflect sustainable growth rather than hidden risks.

Tech investors see two key risks to the AI rally: overspending and over-leverage. Companies addressing both are better positioned to extend gains — namely those with low debt, ample cash, and exposure across the AI supply chain, from chips to models and applications. Google, Microsoft and Amazon fit that profile.

For those seeking cheaper valuations, Asian tech remains attractive. South Korea’s Kospi hit another record today, the Hang Seng is consolidating near last October’s peak, and Japan’s Topix is also at fresh highs, supported by expectations of stronger fiscal stimulus should Takaichi consolidate power in a snap election.

Beyond tech, a softer US dollar and still-low energy prices have supported emerging-market equities. The World Bank raised its global growth forecast, saying the world economy has proven “surprisingly shock-proof” despite a “historic” escalation in trade tensions. The US economy could see a meaningful growth boost, while China and India are expected to grow near 5% and up to 6.5% respectively — a supportive backdrop for EM stocks.

On trade, the US Supreme Court last Friday offered little clarity on the legality of tariffs imposed under questionable justifications. A ruling is expected today. If deemed unlawful, the US may need to refund tariff revenues to companies that filed complaints last year, potentially widening the US budget deficit. That would be negative for US bonds but welcome relief for exporters to, and importers from, the US — including autos, consumer staples and tech.

But the tensions are never over.

Donald Trump said he would impose a 25% tariff on goods from countries doing business with Iran amid nationwide protests and a violent crackdown in the country. China, one of the largest buyers of Iranian oil, is watching closely. Such a move could reignite US-China trade tensions.

Soybean futures — a barometer of US-China trade relations — fell on the latest developments.

As for oil, Iranian unrest is adding upward pressure to prices, alongside attacks near the Caspian Pipeline disrupting Kazakhstan’s exports, compounding delays from harsh winter weather and mooring damage. US crude moved above its 100-day moving average and climbed to around $60 per barrel. However, US crude inventories rose by roughly 5.3 million barrels last week — far above expectations for a 2 million-barrel build and the largest increase in two months — suggesting that once temporary supply disruptions fade, prices may drift back toward a bearish trend.

Dual No-Confidence Votes Highlight France’s Political Divide

In focus today

Today the French Prime Minister faces two motions of no confidence for the first time since October. The far-right RN and far-left LFI has filed to separate motions over the government's failure to derail the EU's Mercosur trade agreement, which was adopted on Friday. The motions are unlikely to pass, with the left-wing refusing to back the RN's motion and the Socialists rejecting the LFI's motion. While the risk of a government censure is small the impact in the event of no-confidence is higher than usual as Macron has said it would likely lead to snap elections. These could take place together with the municipal elections in March.

In the US, the Producer Price Index (PPI) and retail sales will be released for November after a lengthy delay caused by the government shutdown. November CPI was distorted by delayed data collection, and similar issues could affect the PPI figures. Retail sales will be interesting to follow given that US economic growth increasingly relies on private consumption. NY Fed's Williams is scheduled to speak this evening.

The US Supreme Court rescheduled its opinion day, initially planned for last week, to today. This could include its first ruling on President Trump's global tariffs.

Economic and market news

What happened overnight

China's December trade data exceeded expectations, with exports rising 6.6% y/y, significantly above the expected 3%. This robust performance drove China's annual trade surplus to a record high, highlighting resilient external demand despite renewed tariff tensions in 2025. Strong export growth has helped offset weak domestic demand. Shipments to the US fell sharply in December, dropping 30% y/y, while imports declined 29%, signalling a significant reduction in US-China trade throughout 2025. Amid these tensions, China's exports fell 20%, as Chinese exporters increasingly redirected trade routes and increased shipments to non-US markets.

What happened yesterday

In the US, December CPI surprised to the downside. Headline inflation rose +0.3% m/m SA, while core CPI grew at a slower pace of +0.2% m/m (cons: +0.3% m/m). The downside surprise was largely attributed to weaker core goods prices, while services inflation rebounded modestly across shelter, health care and other services, largely in line with expectations. Energy and food inflation surprised slightly to the upside, resulting in a mixed inflation picture for December. Markets reacted dovishly, with UST yields declining and EUR/USD edging higher. As the Fed is focused on services inflation, policymakers may await January data before reassessing trends.

The US small business confidence index increased by 0.5 points to 99.5 in December. The NFIB's December survey indicated that US small business optimism improved towards the end of 2025. Both realised and expected price changes, which historically correlate well with CPI, have remained relatively steady in recent months. Hiring plans also showed little change, although they remain below pre-pandemic levels. Overall, the survey suggests that firms perceive a stabilising business environment following a volatile year.

Equities: Equities grinded lower yesterday, in our view despite and not because of the inflation figures. The retreat was undramatic, with the S&P 500 down 0.2% and the Stoxx 600 down 0.1%. The strong cyclical run since the start of the year took a breather. Most cyclical sectors traded lower, primarily banks following Q4 reporting. The rotation out of US tech and into value cyclicals continued, albeit mildly, with industrials and materials outperforming the broader market. US futures point to a similar opening today.

FI and FX: EUR/USD consolidated in the mid-1.16-1.17 range as the broad USD modestly firmed across G10 FX in yesterday's session, following an initial dip after the slightly softer-than-expected US December core CPI print. The IEEPA Supreme Court ruling could emerge today and represents a far more significant catalyst for near-term USD direction. USD/JPY continues to rise as speculation over a snap election grows, which would likely open the door for a pro-stimulus agenda from PM Takaichi. Global swap yields ended yesterday's session largely unchanged. In Sweden, the first SGB auction for the year will be held today, with the auction size having been increased from SEK6bn last year to SEK8bn. We remain negative 10y SGB ASW. EUR/SEK edged higher yesterday after failing to breach the 10.70 level, while EUR/NOK is slightly lower overnight.

GBP/USD Recovers Lost Ground—But Can the Bounce Last?

Key Highlights

- GBP/USD found support near 1.3400 and recovered some losses.

- It cleared a key bearish trend line with resistance at 1.3430 on the 4-hour chart.

- EUR/USD is facing heavy resistance near 1.1700.

- Gold remains elevated and might rise further above $4,620.

GBP/USD Technical Analysis

The British Pound dipped below 1.3450 and tested 1.3400 against the US Dollar. GBP/USD traded as low as 1.3391 and recently started a fresh increase.

Looking at the 4-hour chart, the pair cleared a key bearish trend line with resistance at 1.3430. There was a move above the 50% Fib retracement level of the downward move from the 1.3567 swing high to the 1.3391 low.

The pair remained well above the 200 simple moving average (green, 4-hour) and surpassed the 100 simple moving average (red, 4-hour). Immediate resistance sits near 1.3500 or the 61.8% Fib retracement.

The first key hurdle is seen near 1.3525. A close above 1.3525 could open the doors for a move toward 1.3565. Any more gains could set the pace for a steady increase toward 1.3700.

If there is no move above 1.3500, there could be a bearish reaction. On the downside, immediate support is near the 1.3450 level. The first major area for the bulls might be near 1.3400. A close below 1.3400 might spark heavy bearish moves. The next support could be 1.3380, below which the bears might aim for a move toward 1.3320.

Looking at Gold, the bulls remain in action and might soon aim for more gains above $4,640 and $4,650 in the near term.

Upcoming Key Economic Events:

- US Retail Sales for Nov 2025 (MoM) – Forecast +0.4%, versus 0% previous.

- Fed's Miran speech.

- BoE's Ramsden speech.

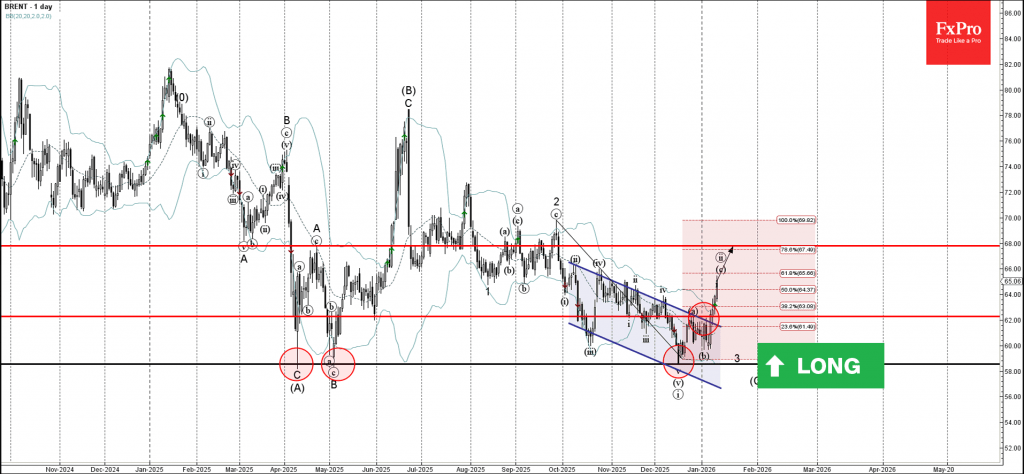

Brent Crude oil Wave Analysis

Brent Crude oil ⬆️ Buy

- Brent Crude oil rising inside impulse wave c

- Likely to rise to resistance level 68.00

Brent Crude oil recently broke the resistance area between the resistance level 62.00, resistance trendline of the daily down channel from October and the 38.2% Fibonacci correction of the downward impulse from September.

The breakout of this resistance area accelerated the active impulse wave c – which belongs to the short-term ABC correction ii from December.

Brent Crude oil can be expected to rise to the next resistance level 68.00 (target for the completion of the active impulse wave c).