Sample Category Title

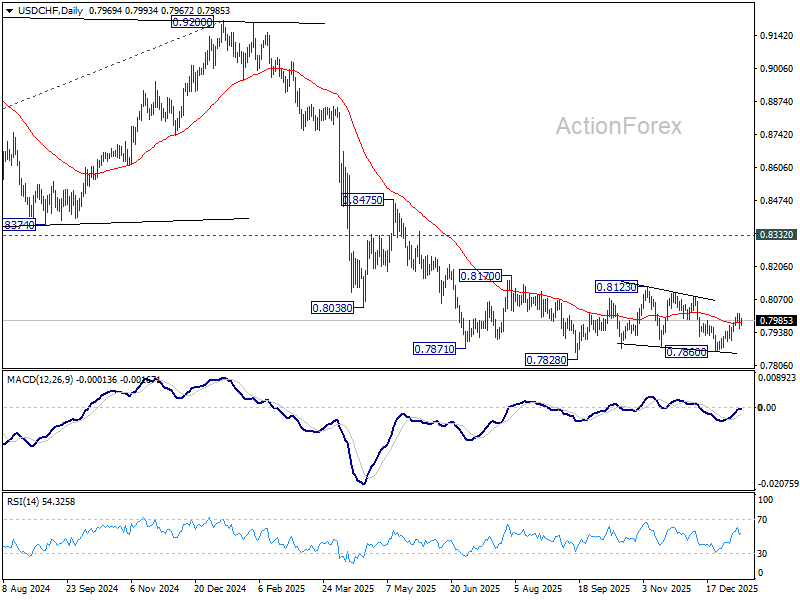

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7949; (P) 0.7984; (R1) 0.8011; More….

Range trading continues below 0.8016 and intraday bias in USD/CHF remains neutral. Corrective pattern from 0.7828 low is extending. On the upside, above 0.8016 will target 0.8123 resistance next. Nevertheless, break of 0.7905 support will resume the fall from 0.8123 to retest 0.7828 low. Firm break there will resume larger down trend.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is in still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

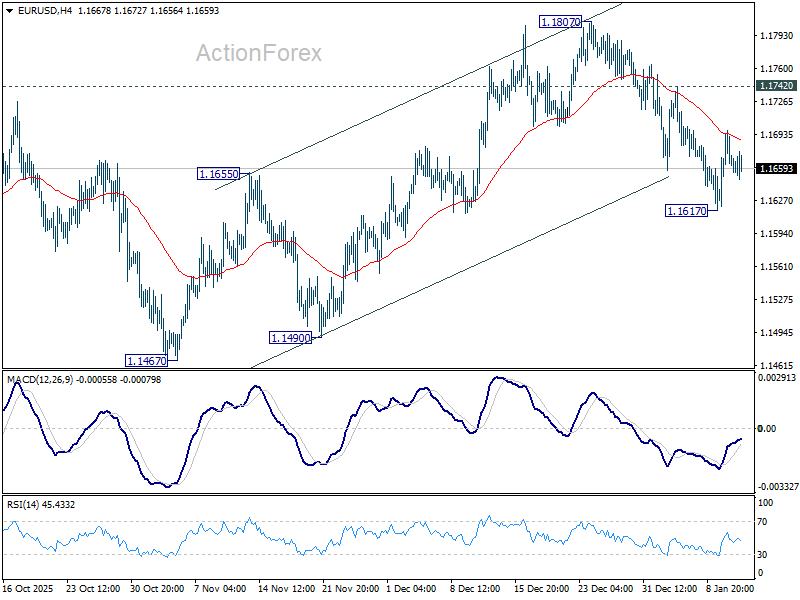

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1625; (P) 1.1662; (R1) 1.1702; More….

No change in EUR/USD's outlook and intraday bias stays neutral. On the upside break of 1.1742 resistance will argue that pullback from 1.1807 has completed. Rise from 1.1467 should then be ready to resume. Further break of 1.1807 will pave the way to retest 1.1817 high. Nevertheless, on the downside, below 1.1617 will target 1.1467 support. Overall, price actions from 1.1917 are seen as a corrective pattern that might extend further.

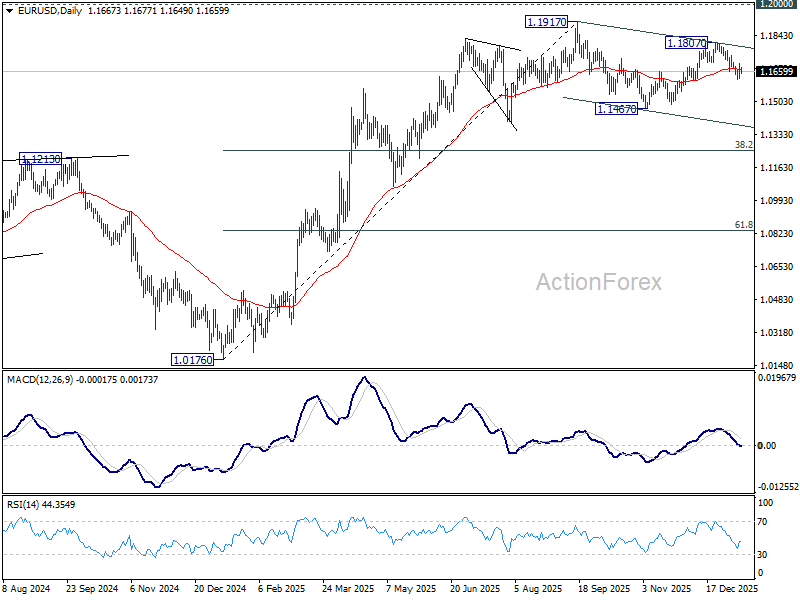

In the bigger picture, as long as 55 W EMA (now at 1.1416) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

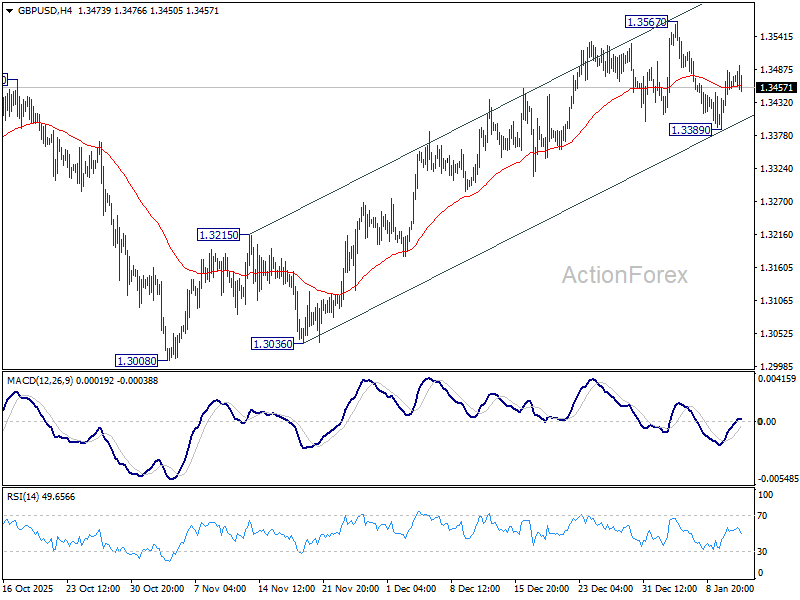

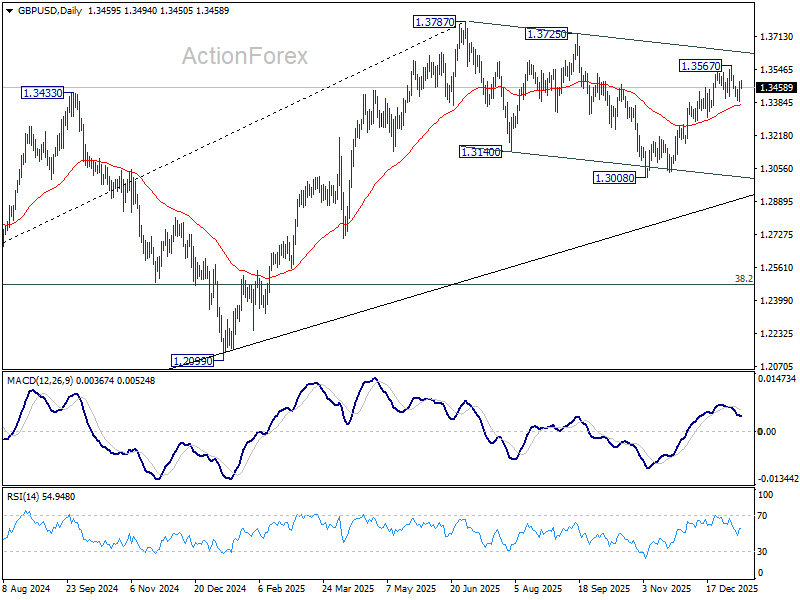

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3409; (P) 1.3447; (R1) 1.3504; More...

GBP/USD is staying in range between 1.3389/3567 and intraday bias remains neutral. On the upside, break of 1.3567 will resume the rally from 1.3008 towards 1.3787 high. On the downside, break of 1.3389 will resume the fall from 1.3567. Sustained break of 55 D EMA (now at 1.3374) will argue that the decline is another falling leg in the corrective pattern from 1.3787. In this case, deeper fall should be seen back to 1.3008 support.

In the bigger picture, price actions from 1.3787 (2025 high) are seen as a correction to the larger up trend from 1.3051 (2022 low). Deeper decline could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.0351 to 1.3787 at 1.2474 to bring rebound. Break of 1.3787 for up trend resumption is expected at a later stage.

Dollar Stalls as CPI Confirms Fed Pause in January

Dollar gyrates in a tight range and remains an underperformer for the week, showing little reaction to December US consumer inflation data. With no meaningful downside surprise in the data, inflation figures effectively cemented expectations for a policy hold by the Fed at its upcoming meeting. Futures now assign around 95% probability that interest rates will remain unchanged at 3.50–3.75% at the January 28 FOMC decision.

Pricing for a March rate cut was also largely unchanged, hovering slightly above 70%. That pricing remains conditional, however, as policymakers will have two additional CPI prints in hand before deciding whether inflation is cooling fast enough.

A central question is whether tariffs could continue to feed into prices over the coming months, either lifting inflation or preventing further progress toward lower core readings. While the base case still calls for at least one more Fed cut later this year, the length of the current pause will depend on how persistent price pressures prove to be. Any sign that inflation is stabilizing rather than easing would argue for a longer hold, even if the easing cycle is not formally over.

Tariffs have returned to the macro conversation after US President Donald Trump threatened to impose a 25% tariff on countries doing business with Iran. The move risks reopening old geopolitical and trade tensions with China, Iran’s largest trading partner. Although Trump has not named China directly, renewed efforts to isolate Iran are likely to sharpen scrutiny of Belt and Road Initiative, where Iran plays a strategic role as a transit hub for Chinese goods into the Middle East under President Xi Jinping’s flagship project.

In FX performance terms this week, Yen sits firmly at the bottom of the ladder, followed by Dollar and then Euro. Kiwi leads gains, with Sterling and Swiss Franc also outperforming. Aussie and Loonie trade in the middle.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is up 0.33%. CAC is down -0.14%. UK 10-year yield is up 0.19 at 4.394. Germany 10-year yield is up 0.019 at 2.863. Earlier in Asia, Nikkei rose 3.10%. Hong Kong HSI rose 0.90%. China Shanghai SSE fell -0.64%. Singapore Strait Times rose 0.85%. Japan 10-year JGB yield rose 0.07 to 2.167.

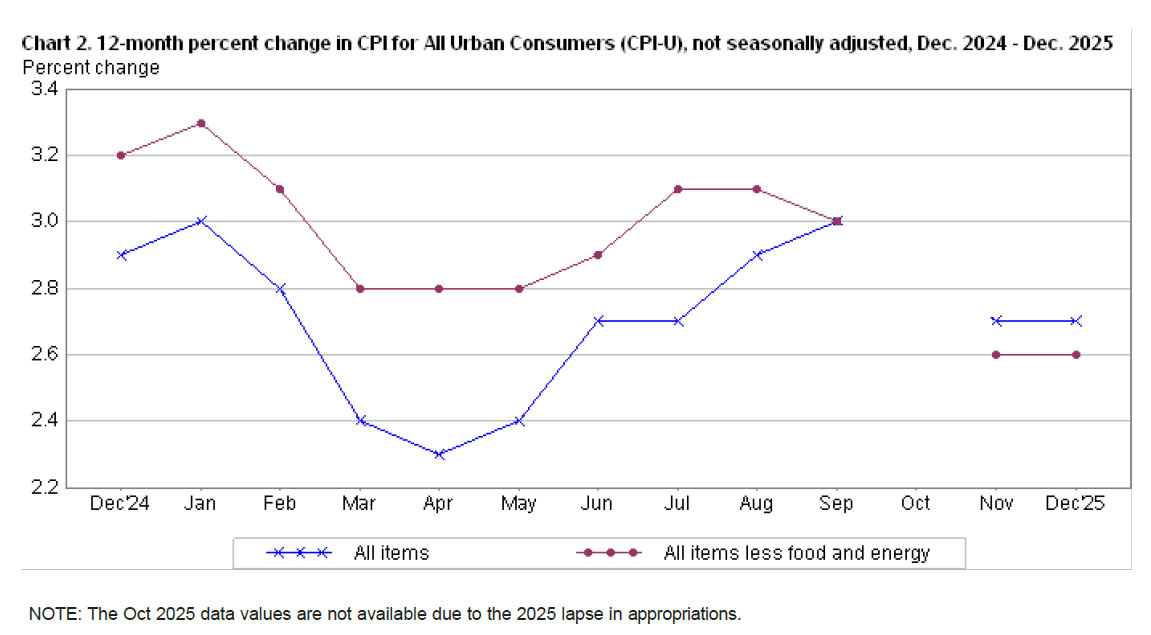

US CPI meets headline, core undershoots at 2.7% in December

US consumer inflation data for December delivered a largely reassuring signal. Headline CPI rose 0.3% mom, in line with expectations. Core CPI increased just 0.2%, undershooting forecasts for a 0.3% gain.

Shelter was the dominant driver of monthly inflation, rising 0.4% and accounting for the largest share of the overall increase. Food prices were also firm, with the food index climbing 0.7% on the month, matching gains in both food at home and food away from home. Energy prices edged up 0.3% in December, contributing modestly to headline pressures.

On an annual basis, CPI was unchanged at 2.7% yoy, matched expectations. CPI core unchanged at 2.6% yoy, below expectation of 2.7% yoy. Energy prices rose 2.3% yoy, while food inflation increased 3.1%.

Australia Westpac consumer sentiment deteriorates, RBA won't tighten precipitously

Australian consumer sentiment weakened further at the start of the year, highlighting growing anxiety over the interest-rate outlook. The Westpac Consumer Sentiment Index fell -1.7% mom to 92.9 in January, pushing sentiment deeper into pessimistic territory.

Westpac pointed to a sharp shift in rate expectations as the main drag. Nearly two-thirds of consumers who expressed a view now expect mortgage rates to rise over the next 12 months, more than double the share seen back in September.

For policy, Westpac expects the RBA to stay on hold when it meets on February 2–3, and through the remainder of 2026. While the RBA has flagged readiness to tighten if inflation proves stubborn, softer labor market conditions and limited price pressures across many goods and services should allow inflation to drift back into the 2–3% target range without the need to "tighten precipitously."

NZIER confidence hits 10-year high, RBNZ to hold until H2 hike

New Zealand business confidence surged in Q4, reinforcing signs that an economic recovery is starting to form. The New Zealand Institute of Economic Research (NZIER) said a net 39% of firms expect better general economic conditions in the months ahead, a sharp rise from 17% in the September quarter and the strongest reading since March 2014.

NZIER noted that while a gap remains between headline confidence and firms’ own domestic trading activity, the direction of travel is clearly improving. The survey suggests the impact of earlier interest-rate cuts is now filtering through the broader economy, lifting sentiment even as activity indicators lag.

Inflation signals was reassuring. Cost and pricing indicators point to broadly contained pressures in the December quarter, with cost pressures easing and a net 37% of firms reporting higher costs.

With demand recovering but inflation subdued, NZIER expects no further OCR cuts this cycle, forecasting the RBNZ’s Official Cash Rate to trough at 2.25% before hikes begin in the second half of 2026.

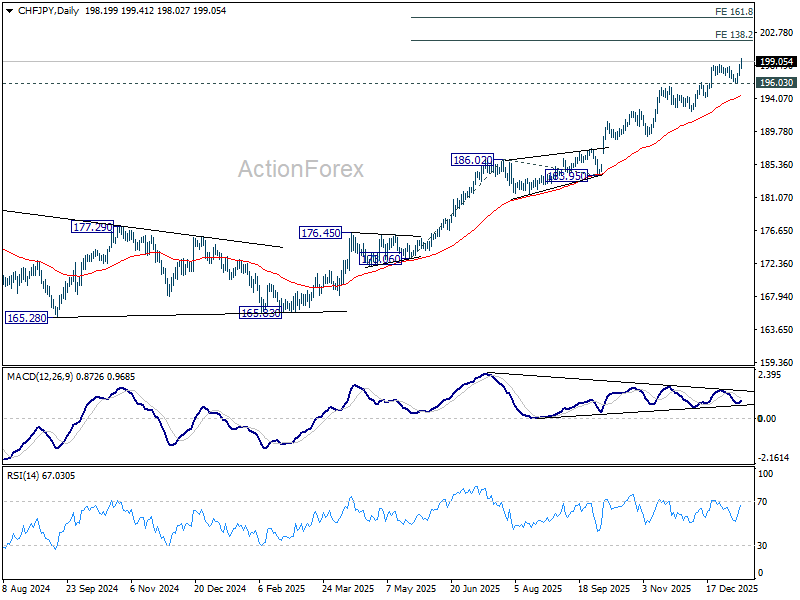

CHF/JPY breaks records as Yen rout meets Fed worries, targets 205 if momentum builds further

CHF/JPY surged to a fresh record high today, driven primarily by accelerating Yen weakness and, to a lesser extent, renewed support for the Swiss Franc. The cross has become a focal point for markets expressing both Japan-specific political risk and broader institutional unease centered on the US.

The Yen leg of the move was triggered by widespread reports that Japanese Prime Minister Sanae Takaichi intends to dissolve the House of Representatives at the outset of the regular Diet session on January 23, paving the way for a snap general election. The decision was reportedly conveyed to senior members of the ruling Liberal Democratic Party.

With Takaichi’s cabinet enjoying strong approval ratings nearly three months into her term, markets see the move as a calculated gamble to stabilize a fragile governing position. The ruling coalition currently holds only a razor-thin majority in the lower house, raising incentives to seek a fresh mandate while political momentum remains favorable.

If the lower house is dissolved on January 23, official campaigning could begin as early as January 27 or February 3, with voting widely expected on February 8 or February 15. An early election would allow Takaichi to push her agenda of expansionary fiscal spending.

Beyond domestic economics, a renewed mandate could also strengthen Takaichi’s hand on foreign policy. Her recent parliamentary remarks on Japan’s potential response to a Taiwan contingency have already contributed to deteriorating Japan–China relations, and an election win would give her greater backing to confront diplomatic challenges.

At the same time, the Swiss Franc has found support from safe-haven demand as confidence in the US Dollar softens. The Donald Trump administration’s threat of criminal indictment against Fed Chair Jerome Powell has raised concerns about the durability of US institutional credibility, diverting some defensive flows toward the Franc.

Technically, CHF/JPY’s uptrend resumed decisively this week with a break above 198.53. Near-term outlook remains bullish as long as 196.03 support holds, with the next target at the 138.2% projection of 173.06 to 186.02 from 183.95 at 201.86. A break higher in D MACD above its signal line would confirm strengthening momentum and open scope for further gains toward 161.8% projection at 204.91.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3409; (P) 1.3447; (R1) 1.3504; More...

GBP/USD is staying in range between 1.3389/3567 and intraday bias remains neutral. On the upside, break of 1.3567 will resume the rally from 1.3008 towards 1.3787 high. On the downside, break of 1.3389 will resume the fall from 1.3567. Sustained break of 55 D EMA (now at 1.3374) will argue that the decline is another falling leg in the corrective pattern from 1.3787. In this case, deeper fall should be seen back to 1.3008 support.

In the bigger picture, price actions from 1.3787 (2025 high) are seen as a correction to the larger up trend from 1.3051 (2022 low). Deeper decline could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.0351 to 1.3787 at 1.2474 to bring rebound. Break of 1.3787 for up trend resumption is expected at a later stage.

US: Inflation Steadied in December

Headline CPI inflation was 2.7% year-on-year (y/y) in December, in line with consensus expectations. That maintained the deceleration from the recent high of 3.0% in September.

Food prices were a little hot under the collar in December, up 0.7% month/month (m/m), and 3.1% versus a year ago as food inflation trended higher in 2025. In contrast, energy prices rose a more muted 0.3% m/m, as a drop in gasoline prices partially offset higher natural gas utility costs. Energy prices are up 2.3% y/y.

Beneath the surface, core inflation was slightly cooler than expected, up 2.6% y/y, unchanged from November's pace. That is a result of a 0.2% month/month (m/m) increase, one tenth lower than expected.

Within the core, goods prices were flat in December, breaking a streak of five reports of gains. The three-month annualized rate of change slowed to just 0.2%.

Price pressures on the services side were a little firmer (+0.3% m/m) as shelter costs accelerated (+0.4% m/m). Costs for lodging away from home rebounded (+2.9% m/m) after weakness through much of 2025. Recreation costs also surged ahead 1.2% m/m – a one-month record – as video services prices surged. Overall core services were up 3% y/y in December, unchanged from November.

Key Implications

Zooming out, inflation remained steady in December. It was encouraging to see core goods prices stand pat after a period of firming. Similarly, core services continued to cool on a trend basis.

Core inflation is tracking slightly cooler than our December forecast, but we still expect the knock-on effects from tariffs will push inflation higher over the coming months. This is likely to lead the Fed to push pause on its interest rate cuts for at least a couple of meetings. Eventually, we expect it to become clearer that the impact of tariffs on prices was a one-time shift, and a new Fed chair is likely to provide a more dovish tilt, leading to 2 additional quarter-point rate cuts mid-year.

US CPI meets headline, core undershoots at 2.7% in December

US consumer inflation data for December delivered a largely reassuring signal. Headline CPI rose 0.3% mom, in line with expectations. Core CPI increased just 0.2%, undershooting forecasts for a 0.3% gain.

Shelter was the dominant driver of monthly inflation, rising 0.4% and accounting for the largest share of the overall increase. Food prices were also firm, with the food index climbing 0.7% on the month, matching gains in both food at home and food away from home. Energy prices edged up 0.3% in December, contributing modestly to headline pressures.

On an annual basis, CPI was unchanged at 2.7% yoy, matched expectations. CPI core unchanged at 2.6% yoy, below expectation of 2.7% yoy. Energy prices rose 2.3% yoy, while food inflation increased 3.1%.

Silver Prices Stabilise Near Record Highs

As the XAG/USD chart shows, the price of silver per ounce is consolidating near its all-time high, which lies above $85.

Bullish sentiment dominates the market, as concerns over the independence of the US Federal Reserve, heightened geopolitical tensions, and other factors have fuelled demand for safe-haven metals. According to media reports:

→ Official authorities are exerting pressure on the Fed to cut interest rates, having opened a criminal case against its Chair. Powell, in turn, described these actions as a “pretext” for influencing the decisions of an independent financial institution.

→ Traders are also closely monitoring the escalation of protests in Iran, which could lead to US military involvement, alongside President Trump’s statements about the annexation of Greenland. In the aftermath of the operation in Venezuela, such scenarios are increasingly being viewed as realistic.

Technical Analysis of the XAG/USD Chart

On 29 December, we updated the previously drawn ascending channel and suggested a potential decline in silver prices towards its lower boundary, with a possible bearish breakout attempt.

Indeed, prices moved down to the lower boundary. However, after the formation of an Inverted Head and Shoulders (IHS) pattern, bulls found support there and resumed the upward trend.

The current consolidation in XAG/USD confirms the role of the channel median, which appears to act as a reference level acceptable to both buyers and sellers. That said, today’s CPI release could disrupt this balance. Possible scenarios include:

→ a pullback towards the psychological support around $80, where the bullish impulse marked by the arrow began;

→ a rise towards the QH line, which divides the upper half of the channel into two quarters.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

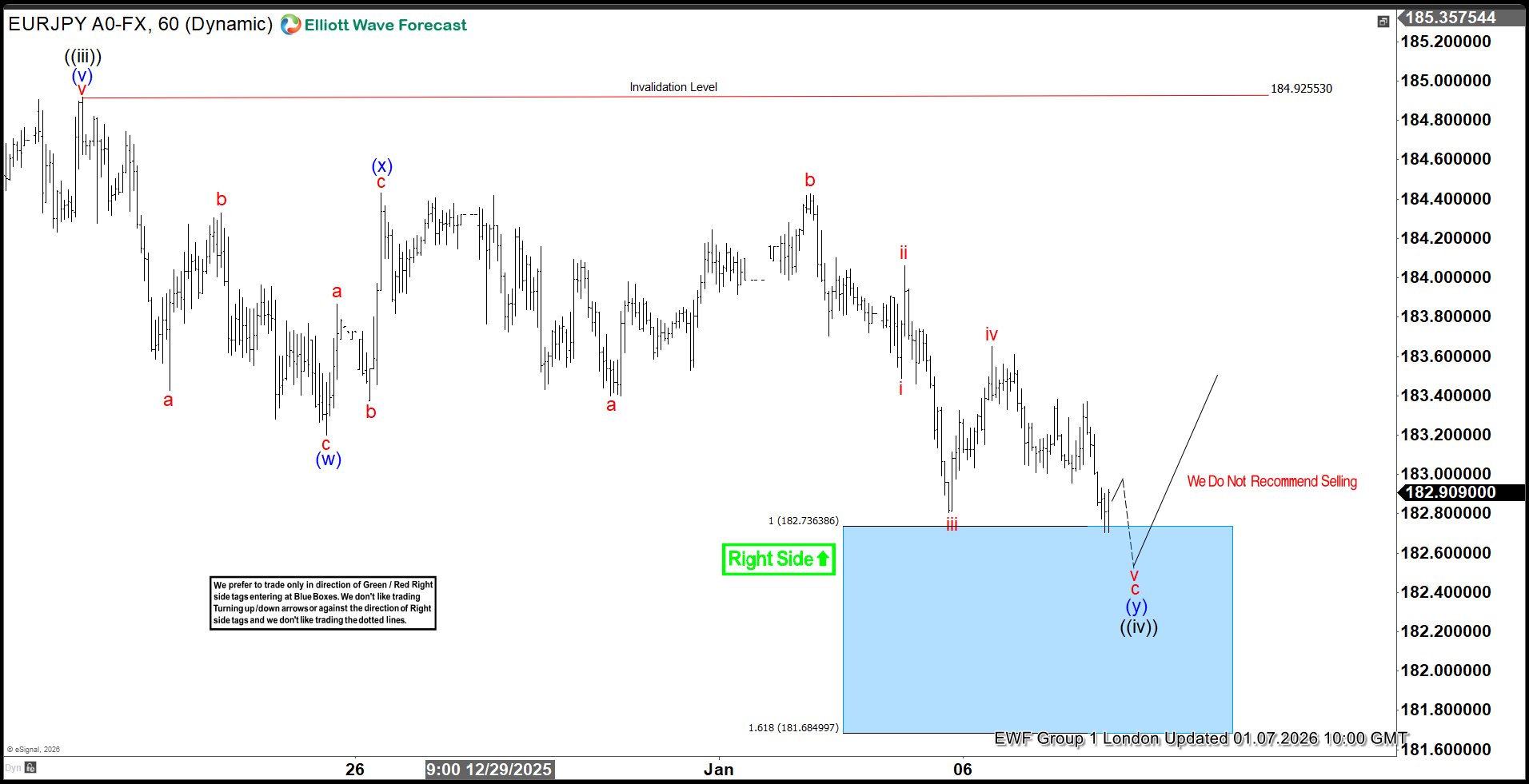

EURJPY Breaks Higher: Blue Box Delivers New Highs

In this technical blog, we will look at the past performance of the 1-hour Elliott Wave Charts of EURJPY. In which, the rally from 31 July 2025 low is unfolding as an impulse sequence. Therefore, called for more upside to take place. We knew that the structure in the pair should remains incomplete & should see more upside. So, we advised members not to sell the pair & buy the dips in 3, 7, or 11 swings at the blue box areas. We will explain the structure & forecast below:

EURJPY 1-Hour Elliott Wave Chart From 1.07.2026

Here’s the 1-hour Elliott wave Chart from the 1.07.2026 London update. In which, the rally to 184.92 high completed wave ((iii)) & made a pullback in wave ((iv)). The internals of that pullback unfolded as Elliott wave double correction where wave (w) ended at 183.19 low. Then a bounce to 184.43 high-ended wave (x) & started the next leg lower in wave (y) towards 182.73- 181.68 blue box area. From there, buyers were expected to appear looking for new highs ideally or for a 3-wave bounce minimum.

EURJPY Latest 1-Hour Elliott Wave Chart From 1.13.2026

This is the latest 1-hour Elliott wave Chart from the 1.13.2026 Asia update. In which the pair is showing a strong reaction higher taking place, right after ending the double correction within the blue box area. Allowed members to create a risk-free position shortly after taking the long position at the blue box area. Since than the pair has already made a new high above previous wave ((iii)) high and now targeting 185.47- 186.34 minimum extension target to end wave ((v)).

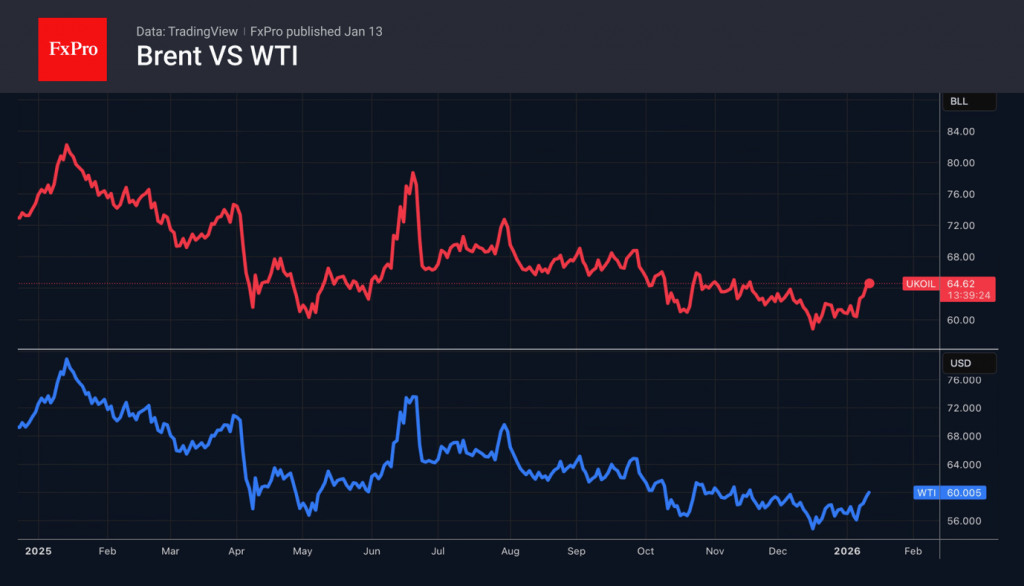

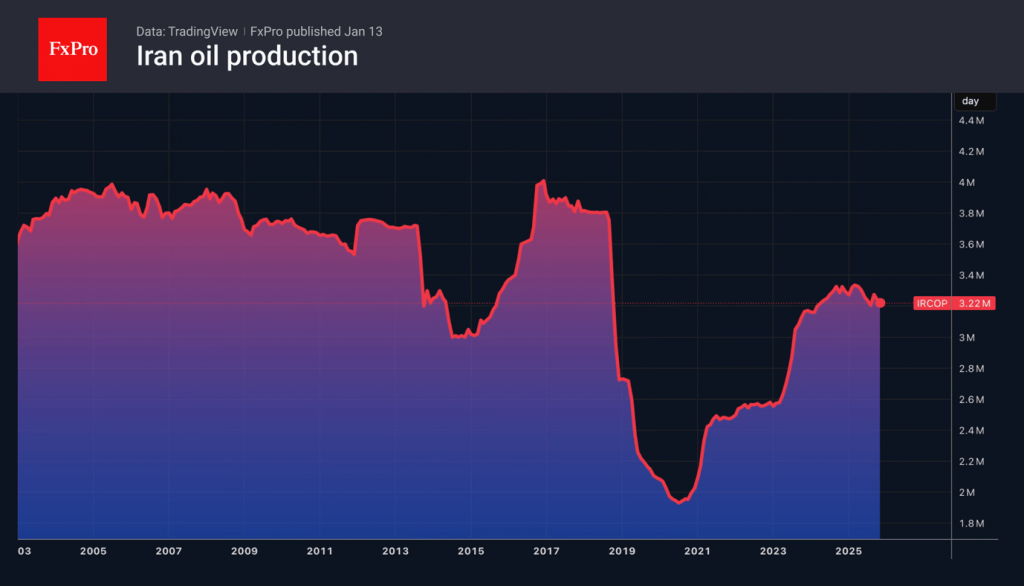

Crude Oil Counteracts

While developments in Venezuela acted as a headwind for oil prices, events surrounding Iran provided clear support. Expectations of an influx of cheaper supply from Latin America pushed Brent crude to its lowest level in eight months. However, escalating tensions in the Middle East helped North Sea crude find a floor and rebound. The four-day rally in black gold highlights a renewed rise in geopolitical risk premiums.

According to Capital Economics, mass protests, oil workers’ strikes, the blockade of the shadow fleet, and Tehran’s threats to close the Strait of Hormuz could push Brent prices up by $15-20 per barrel.

Iran is a much larger oil producer than Venezuela, ranking fourth in OPEC. It accounts for about 3% of global production, or 3.3 million barrels per day. Exports are estimated at 2 million barrels per day, with about 90% going to China. The country’s share of China’s black gold imports is estimated at 15%. Venezuela’s share is only 2%. Western sanctions have significantly undermined Tehran’s potential. At the peak of its glory in the 1970s, Iran’s share of global production was 10%.

Investors are hedging against the risks of Brent’s rally continuing at its fastest pace since the joint US-Israeli attack on Iran last summer. At the same time, the market is considering two key scenarios for further developments. Either there will be a supply crisis, or the resumption of the trade war between the United States and China will deal a blow to the world economy and global demand for oil. Following Donald Trump’s announcement of additional 25% tariffs on countries doing business with Tehran, such a scenario is quite likely.

Such a rapid rally in Brent would not have happened if speculators had not built up huge short positions in North Sea crude against the backdrop of events in Venezuela. Their unwinding is leading to a rebound. Demand for oil call options has jumped to its highest level since October. A significant share of them are trading with strike prices at $80 per barrel.

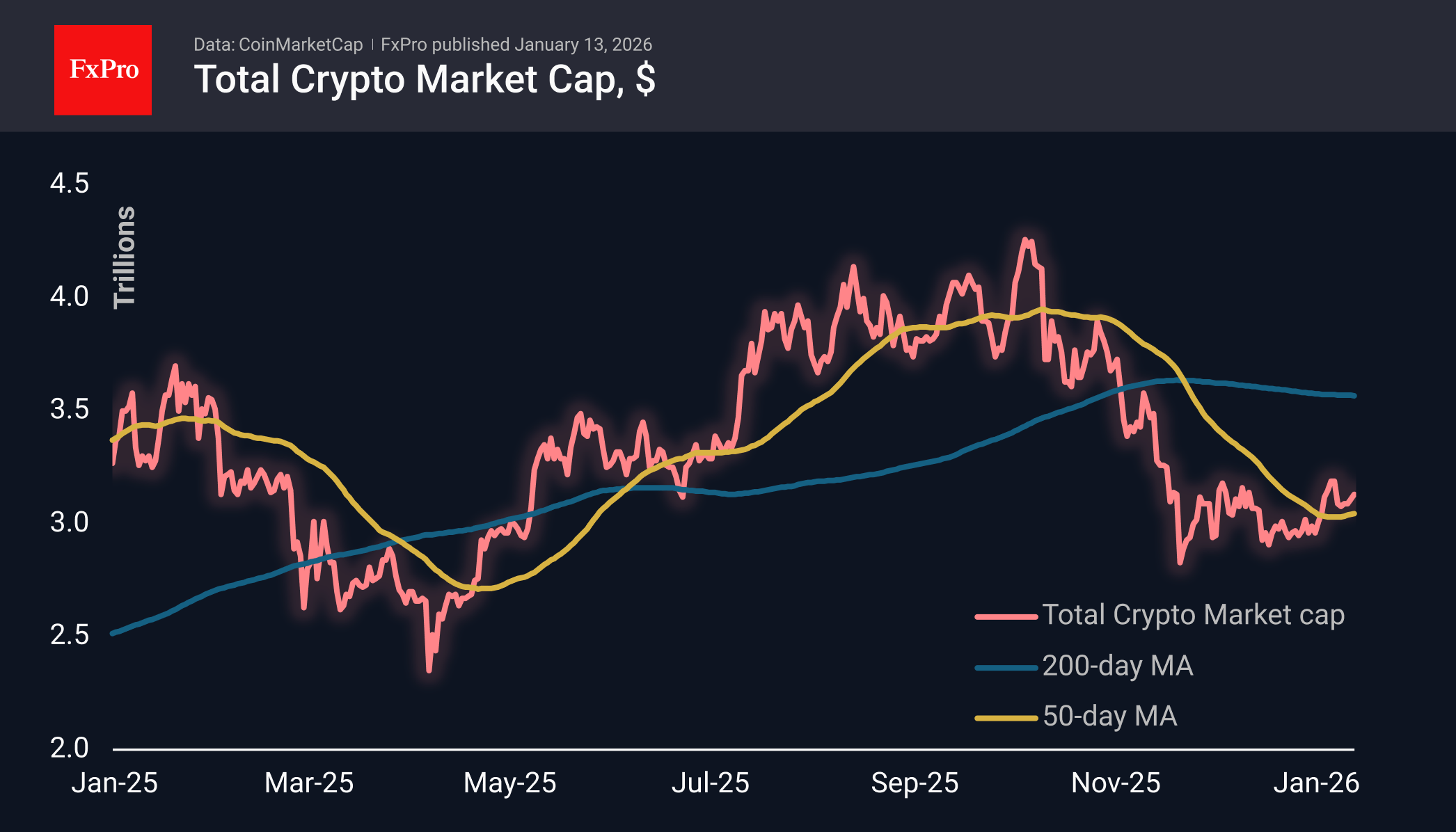

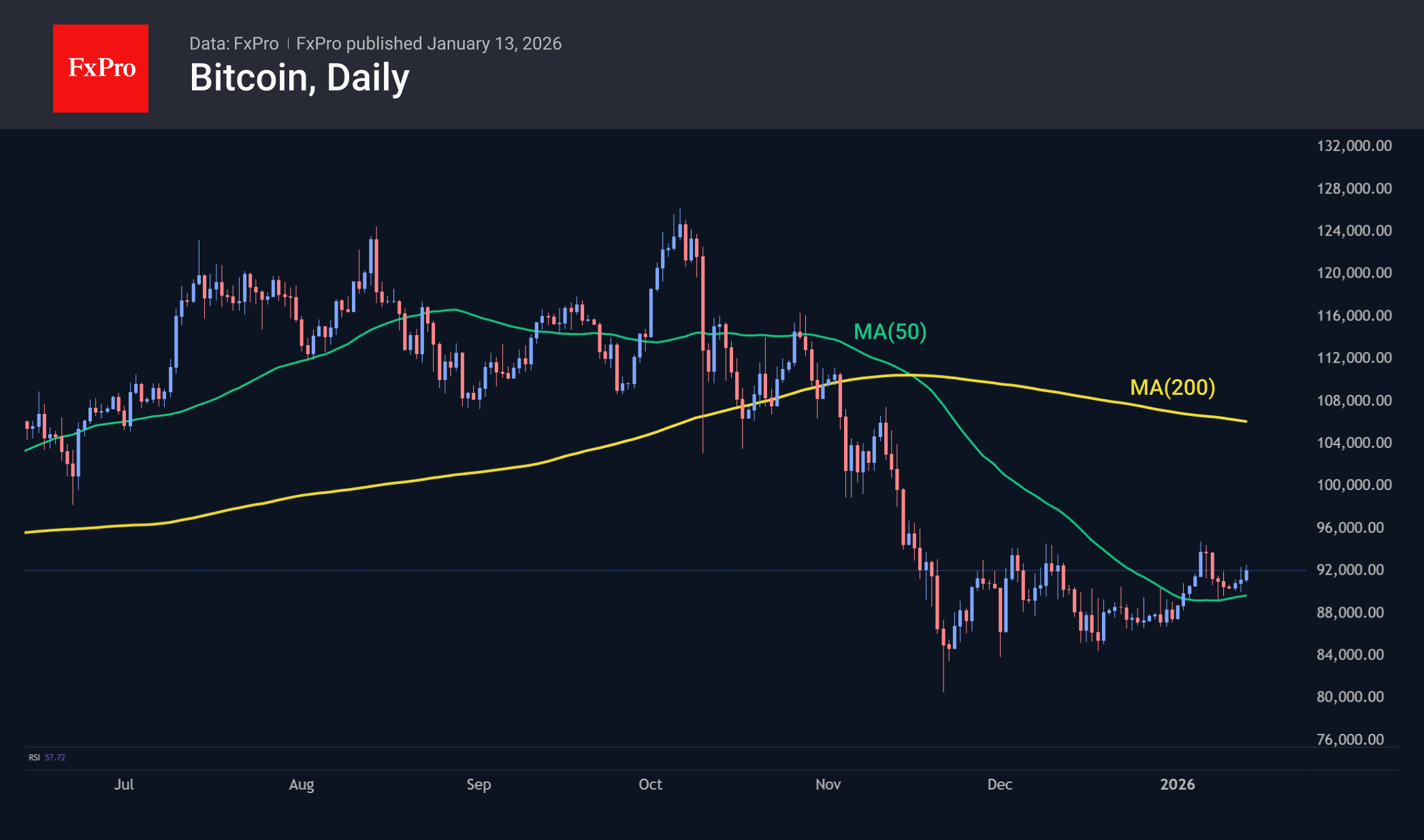

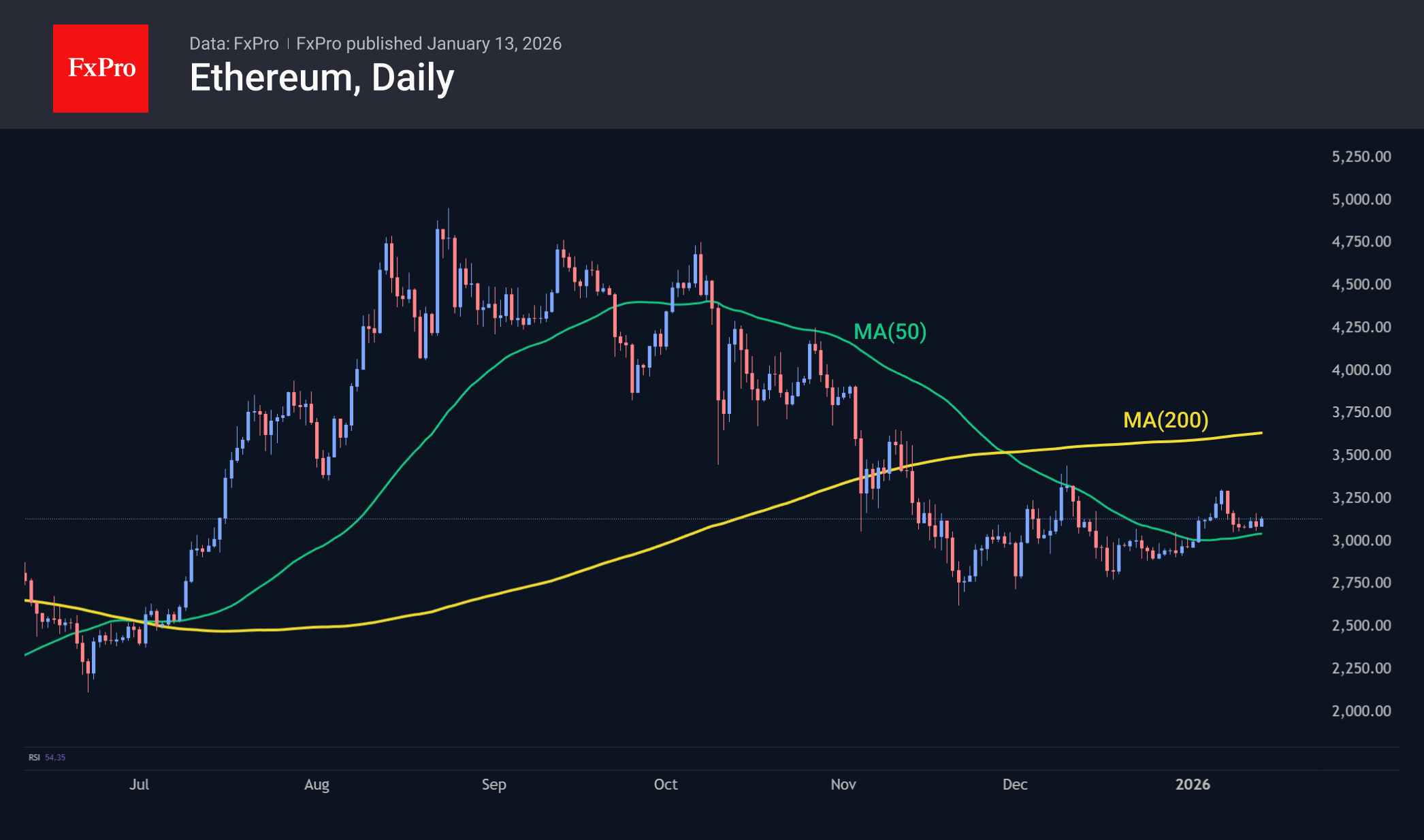

Crypto Market Grows With Risk Appetite in Stocks

Market Overview

The crypto market gained 0.75% over the past 24 hours to $3.13T in another attempt to turn towards growth, pushing off the 50-day moving average. Appetite for crypto grew amid a rebound in US financial markets during Monday’s trading and continued growth in Japanese stocks on Tuesday morning. Steady risk appetite began to spread to cryptocurrencies, which had underperformed the market for many weeks.

Bitcoin has exceeded $92K since Monday evening, attempting to climb above levels seen a week ago. There were wide fluctuations on Monday, with an impressive increase in sales when the price rose above $92K, but this did not deter the bulls from continuing their attempts. It would be too hasty to conclude sustained risk appetite while the price remains below previous local highs of $95K. An optimistic view of the situation considers a series of rising local lows since November.

Ethereum is holding above $3,000, carefully forming a bottom at this level over the past five days. At the end of last month, a similar support level was near $2,920. As with Bitcoin, ETH is trading above the 50-day MA, but still below the local peak on 6 January.

News Background

Retail investors continue to offload loss-making assets due to fears of volatility, which is increasing selling pressure, according to CryptoQuant.

Profit-taking and shifting expectations in the options market indicate that investors are postponing bullish expectations to a later date, not believing in a quick rally. Optimism about a breakout in the first quarter is fading, QCP Capital notes.

Views of cryptocurrency content on YouTube have fallen to their lowest levels since 2021, ITC Crypto notes. A similar decline in social interest has also been recorded on social network X.

According to Arkham Intelligence, the DAT company BitMine has increased the amount of locked assets on the Ethereum network to 1.08 million coins. The value of the portfolio exceeded $3 billion.

The theory of Ethereum’s ‘demise,’ based on its prolonged decline against Bitcoin, is untenable, said MN Trading founder Michael van de Poppe. In his opinion, the ETH/BTC rate has already bottomed out. The key argument in favour of growth is the increase in the volume of stablecoins on the Ethereum network.

South Korea has lifted its ban on corporate investment in cryptocurrencies. Legal entities will be able to allocate up to 5% of their share capital to coins from the top 20 by market capitalisation, excluding stablecoins.