Sample Category Title

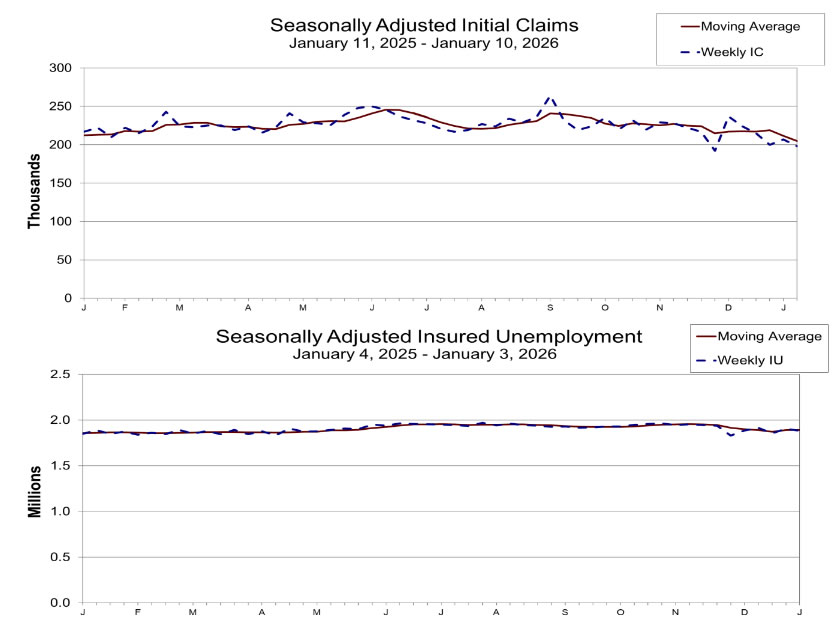

US initial jobless claims fall to 198k, signal little labor market stress

US labor market conditions showed renewed firmness, with initial jobless claims falling more than expected in the latest week. Claims dropped by -9k to 198k in the week ending January 10, below expectations of 208k and marking one of the lowest readings of the past year.

The four-week moving average of initial claims declined by -6.5k to 205k, the lowest level since January 20, 2024. The smoothing measure confirms that layoffs remain limited, with little evidence of sustained deterioration in hiring conditions.

Continuing claims also edged lower, falling 19k to 1.884 million in the week ending January 3. The four-week average was broadly unchanged at 1.889 million.

Markets Pick Up Signals from the White House

- Donald Trump has no intention of dismissing Jerome Powell.

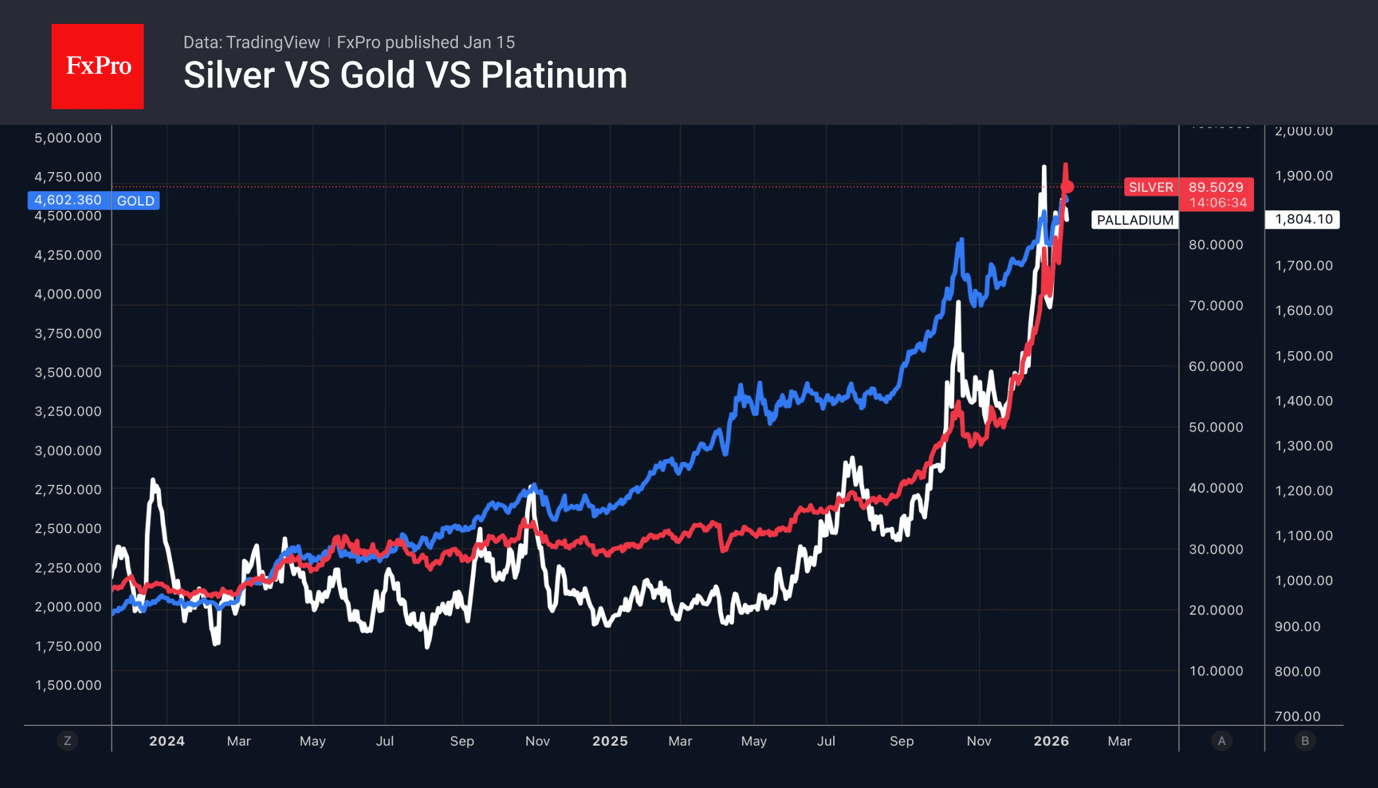

- The White House’s decision to postpone tariffs on minerals has dealt a blow to precious metals.

When Donald Trump sneezes, the markets get a fever; when he is in a nice mood, they flourish. The US president’s statement that he has no plans to oust Jerome Powell has bolstered the US dollar. The White House’s decision to postpone tariffs on imports of critical minerals has caused precious metal prices to plummet. The Republicans’ words that Iran no longer plans large-scale executions of protesters cut off oxygen to oil.

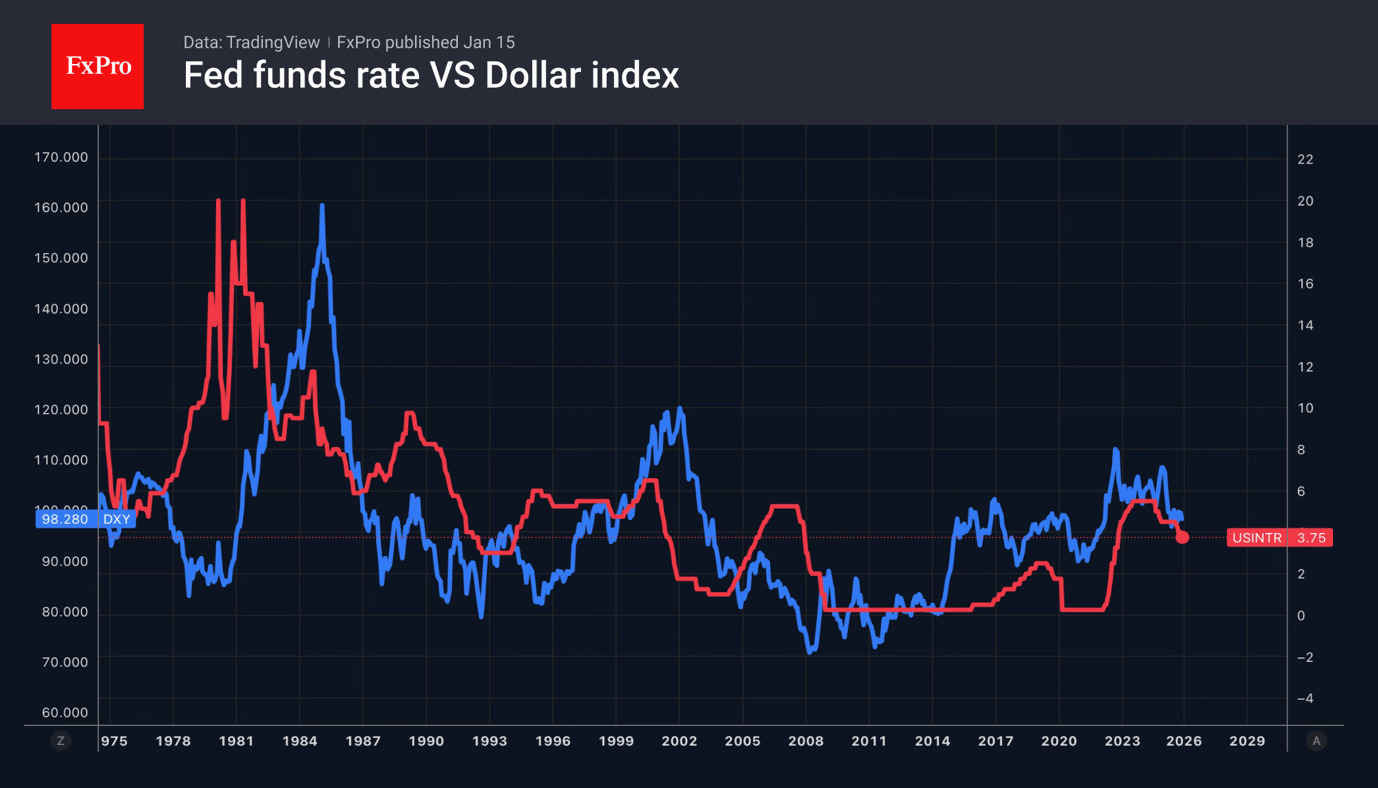

The Trump factor will undoubtedly manifest itself in the fate of the US dollar. However, this will most likely happen in the second quarter. The appointment of a new Fed chair and the replacement of FOMC governors with people loyal to the president will allow the composition of the Committee to be reshuffled and force the derivatives market to bet on aggressive monetary expansion. Until then, the EURUSD is likely to continue falling.

The US dollar is benefiting from a prolonged pause in the Fed’s cycle. The economy remains strong. This is confirmed by the acceleration of retail sales to 0.6% m/m in November. Inflation is slowing down, and producer price growth slowed to 0.1% in October and 0.2% m/m in November. The central bank can afford to sit back and watch how events unfold.

Meanwhile, passion surrounding the yen continues to run high. Japanese Finance Minister Satsuki Katayama said that the government will take appropriate measures against speculators on Forex, without ruling out any options. Similar statements were previously used by Tokyo immediately before currency interventions. Unsurprisingly, USDJPY bulls got scared and retreated.

US Treasury Secretary Scott Bessent noted the undesirability of excessive yen volatility and the need for sound monetary policy. He has repeatedly stated that USDJPY can be forced to fall by raising the overnight rate.

Precious metals took a step back due to the White House’s intention to postpone tariffs on imports of critical minerals. Fears over the introduction of tariffs were the catalyst for the transfer of bullion from Europe and Asia to the US. This resulted in a shortage of physical assets, which fuelled the rally in silver, platinum and palladium. Gold was less affected by Donald Trump’s decision.

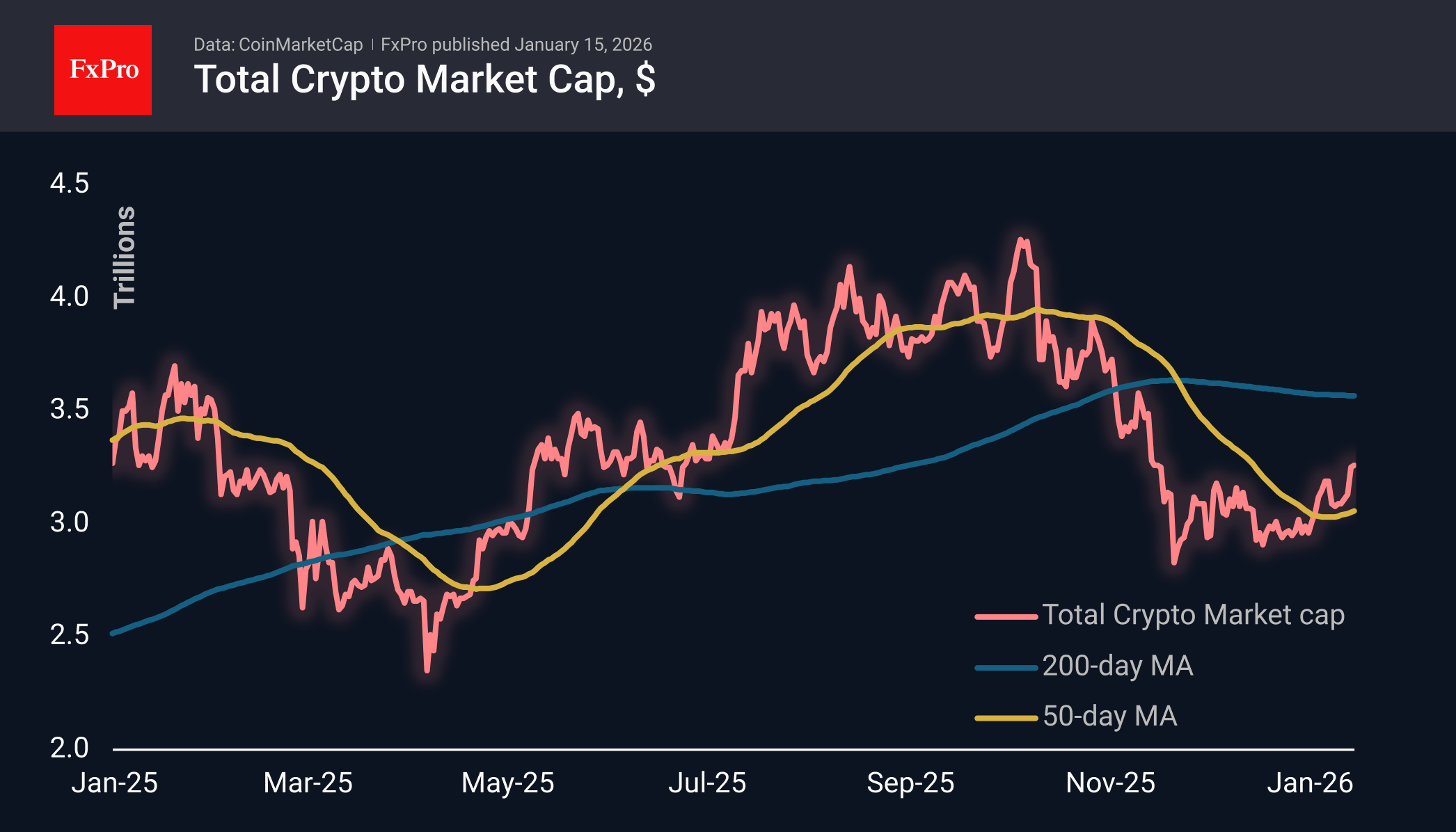

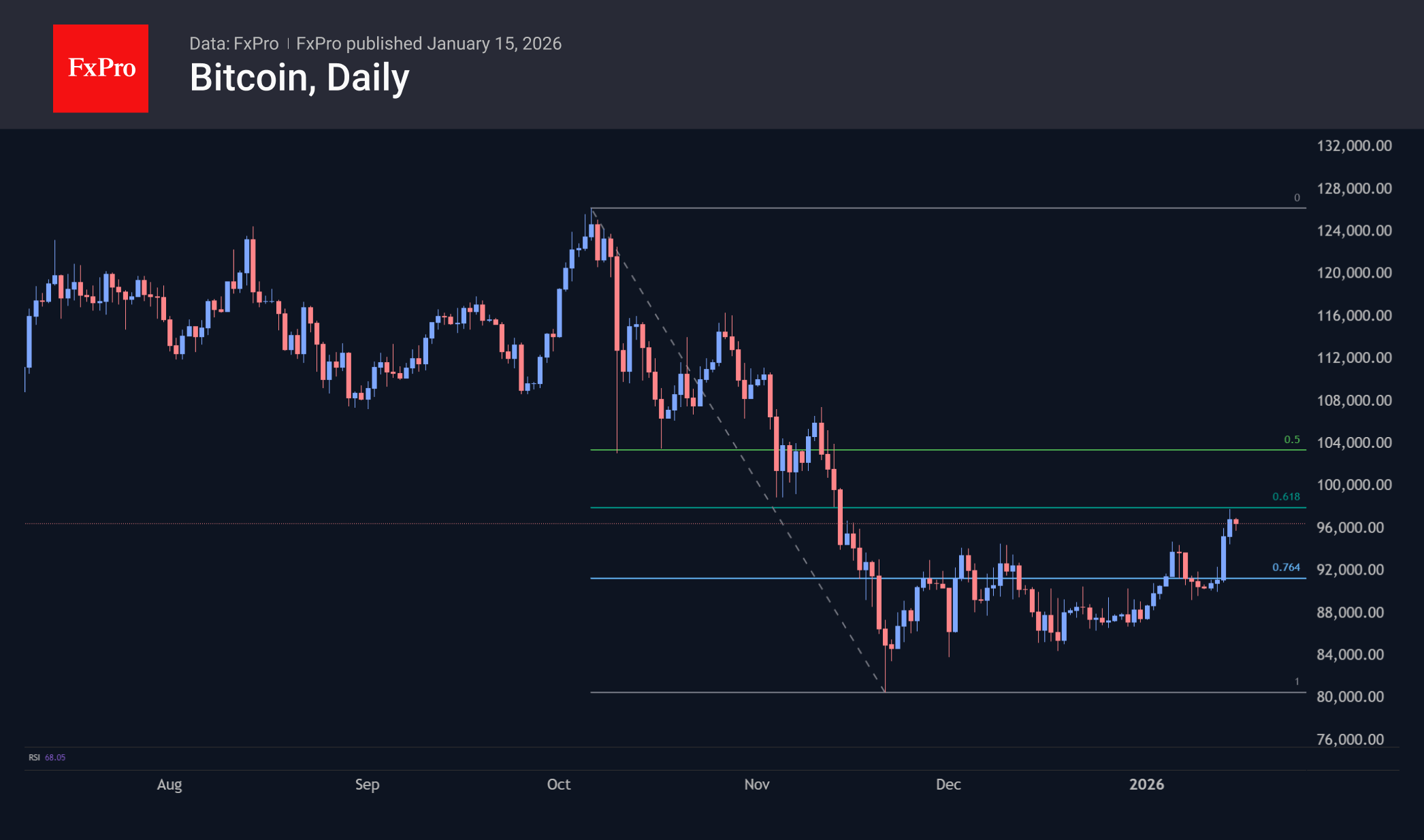

Bitcoin Aims to Break Out of a Corrective Rebound

Market Overview

The crypto market capitalisation has shown a slight increase to $3.26T over the past 24 hours, as it paused its growth, releasing steam after rallying to a total capitalisation of $3.30T. The recovery to a two-month high still keeps the market within a typical corrective rebound of 61.8% of the initial downward momentum. Although it would be too hasty to ignore the sequence of rising local lows, it is still worth being prepared for the recovery momentum to lose steam.

Bitcoin rose to $98K on Wednesday, gaining for the third day during the US session, while Asian and European trading saw a correction and lull, respectively. The price of BTC touched the 61.8% level of the decline from the peak of $126K to the November lows of $80K. Further growth from these levels, especially exceeding $100K, will be an important signal that the decline in October and November may have been a deep correction, but did not break the bull market.

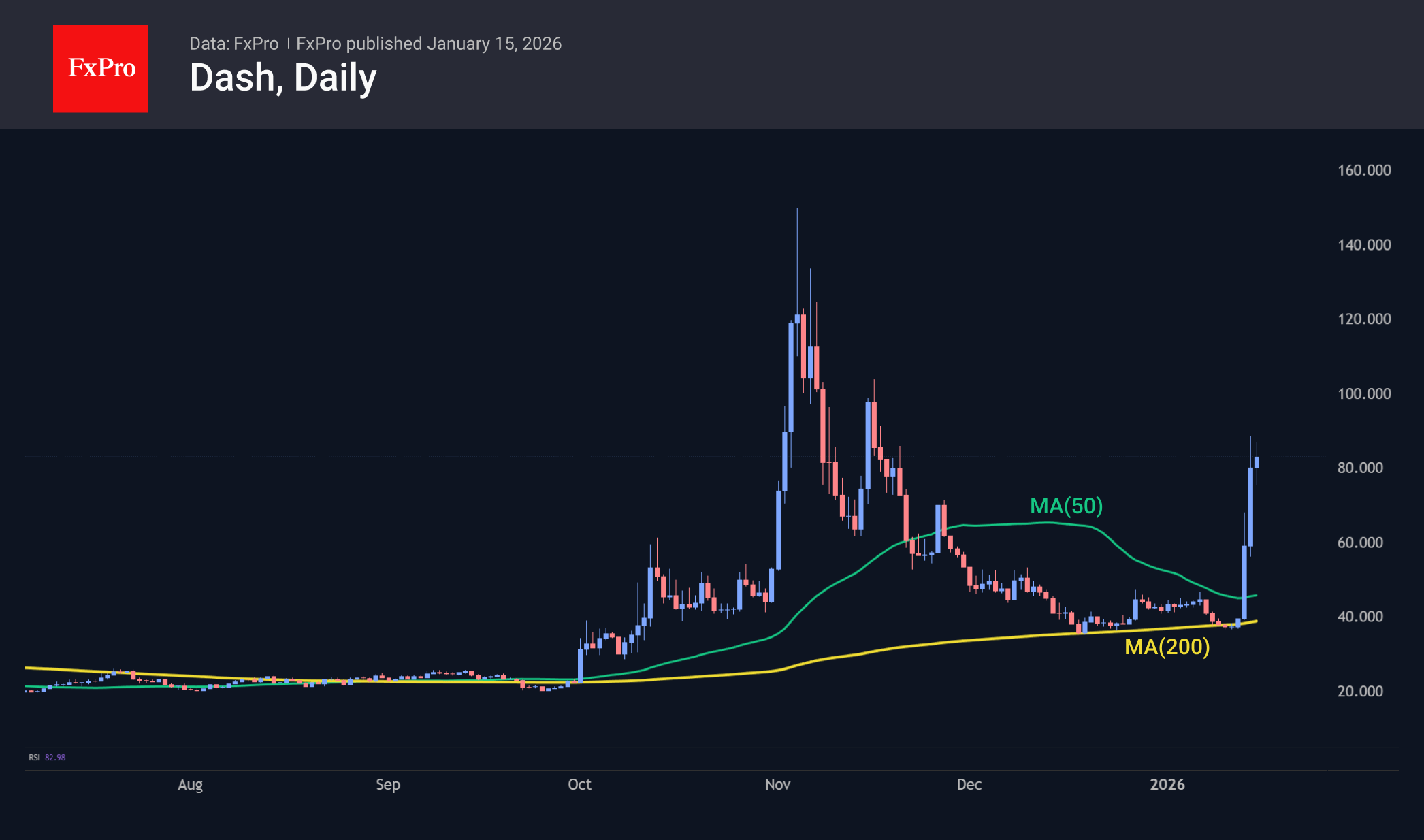

The relatively small Dash coin is experiencing an impressive rally, gaining over 130% since the beginning of the week. Technically, buyers pushed off the 200-day moving average, which had been providing support since September. The last comparable rise in scale was in early November, after which the price fell even lower over the next month and a half. It seems that the main reason for the growth is insufficient liquidity and the pump & dump approach, rather than the start of the alt season.

News Background

The revival of institutional demand signals that investors are actively reallocating capital after a period of caution and risk reduction at the end of last year, according to LVRG Research.

For the first time since mid-2022, the 52-week correlation between Bitcoin and gold has fallen to zero. Historically, the decoupling of these assets has preceded rallies in the first cryptocurrency.

According to Validator Queue, the number of coins locked in Ethereum staking has reached a new all-time high. There are 35.8 million ETH in the Beacon Chain network, which is 29.57% of the market supply of the second-largest cryptocurrency by capitalisation.

Liquidity in cryptocurrencies ceased to be distributed evenly last year, mainly concentrating in Bitcoin, Ethereum and a few other major coins, Wintermute notes. The situation arose against the backdrop of large institutional players actively entering the market.

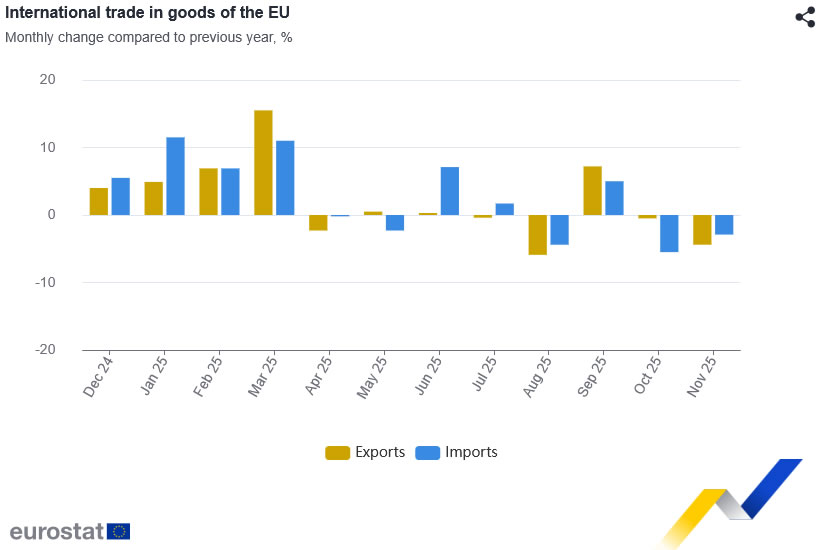

Eurozone exports fall -3.4% yoy in Nov, EU down -4.4%, external demand drags

Eurozone trade data for November pointed to weakening external demand, even as the bloc maintained a modest surplus. Goods exports fell -3.4% yoy to EUR 240.2B, while imports declined -1.3% to EUR 230.3B, leaving a trade surplus of EUR 9.9B. The resilience came from within the bloc. Intra-Eurozone trade rose 0.8% yoy to EUR 220.9B, partially offsetting softness in extra-Eurozone flows.

At the broader EU level, goods exports dropped -4.4% yoy to EUR 213.8B and imports fell -2.9% to EUR 205.7B, resulting in a EUR 8.1B trade surplus.

By trading partner, exports to the US fell sharply by -20.3% year-on-year, while shipments to the UK declined -6.0%. Trade with China was broadly stable, with exports down just -1.2% despite stronger imports, keeping the bilateral deficit large. Switzerland stood out as a relative bright spot, with EU exports rising 6.7%.

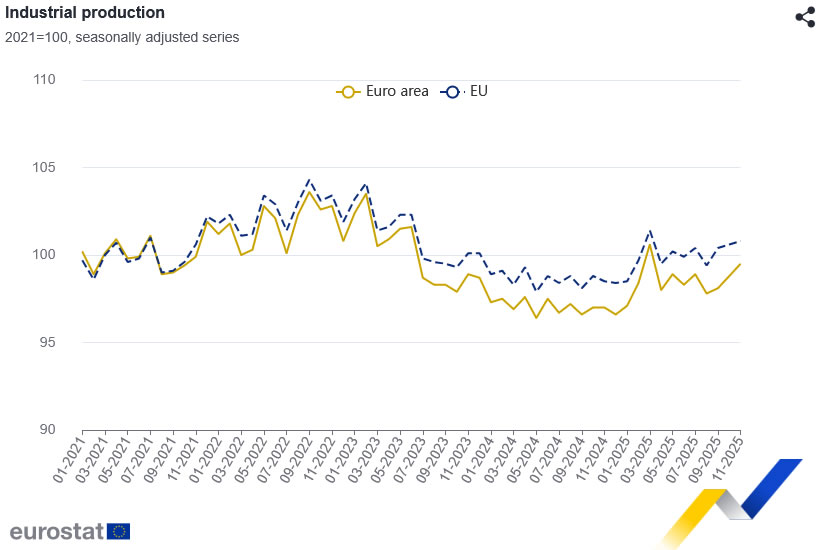

Eurozone industrial output rises 0.7% mom in November, led by capital goods

Eurozone industrial production rose 0.7% mom in November, outperforming expectations for a 0.5% gain. The gains, however, were uneven across categories.

Capital goods output jumped 2.8%, providing the main lift, while intermediate goods rose a modest 0.3%. By contrast, energy production fell sharply by -2.2%, while durable and non-durable consumer goods declined -1.3% and -0.6% respectively, pointing to still-soft consumer demand.

Across the wider EU, industrial production increased just 0.2% on the month. Estonia (6.0%), Lithuania (5.8%), and Czechia (2.8%) recorded the strongest gains, while Luxembourg (-7.3%), Denmark (-5.1%), and Portugal (-3.0%) posted the steepest declines.

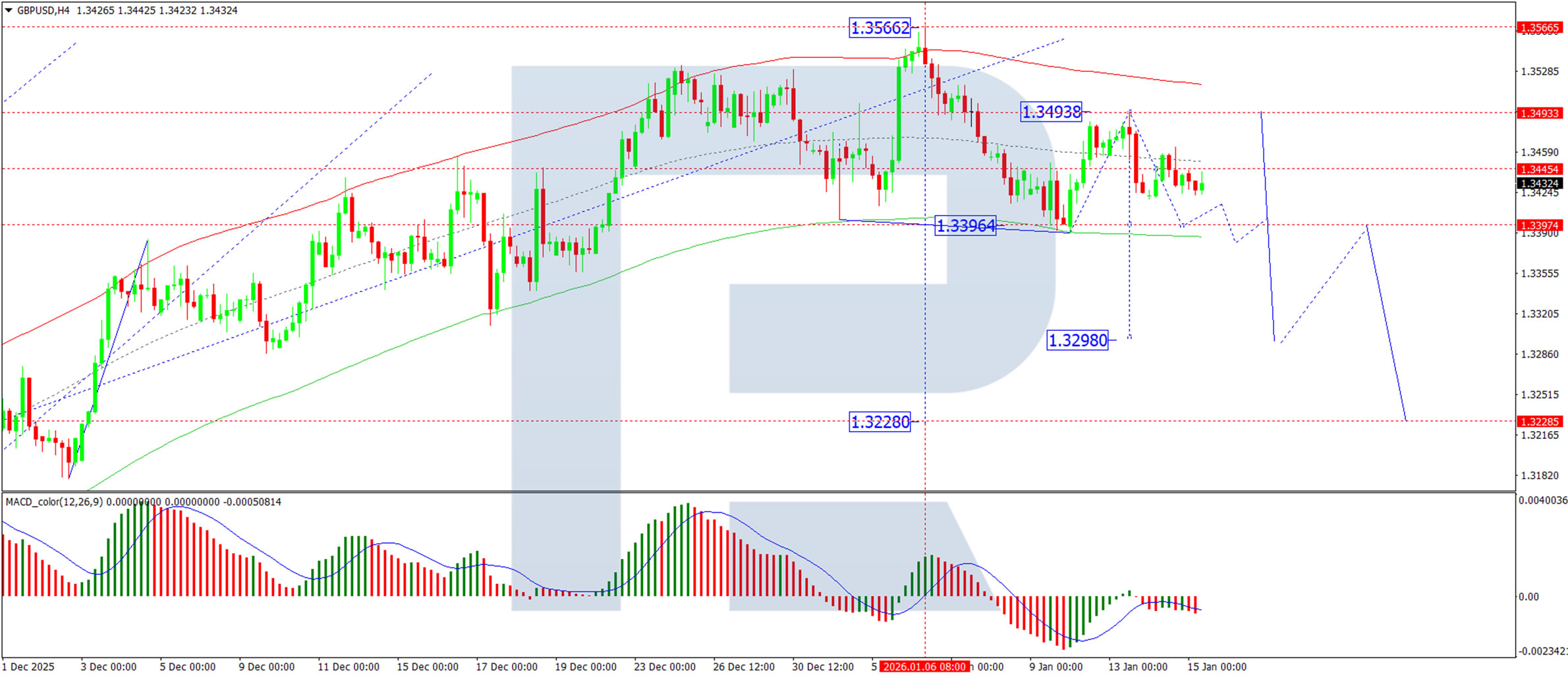

GBP/USD Stable: Sentiment Shifts in Favour of Sterling

The GBP/USD pair held around 1.3430 USD on Thursday, with the pound strengthening yesterday following better-than-expected UK economic growth data. These figures may shape market expectations for Bank of England policy in the coming months.

Since the start of January, sterling has made limited headway against the US dollar but has strengthened notably against the euro. Dollar sentiment remains cautious due to geopolitical tensions involving Iran and Greenland, as well as renewed comments from President Donald Trump questioning the Federal Reserve's independence.

Investor sentiment toward the pound has turned more constructive at the start of 2026. According to the US Commodity Futures Trading Commission (CFTC), traders reduced bearish bets on the pound at the fastest pace in five months during the first week of January. The net long dollar position against sterling fell sharply to 2.577 billion USD, down from 6.586 billion USD at the end of December—marking the steepest weekly decline since September 2019.

Inflation in the UK eased faster than expected toward the end of 2025, and markets are currently pricing in two BoE rate cuts this year. However, analysts view this as overly optimistic: persistently weak growth and subdued inflation could ultimately weigh on the currency. Upcoming soft employment and inflation data for December will be key to reassessing the likelihood of a rate cut as early as February, though markets currently assign low odds to such a move.

Next week brings key releases, including consumer prices and labour market data, followed by GDP figures on Thursday. A Reuters poll suggests the UK economy contracted by 0.2% in the three months to November, with annual growth estimated at around 1.1%.

Technical Analysis: GBP/USD

H4 Chart:

On the H4 chart, GBP/USD is forming a broad consolidation range around 1.3455 USD. The range is expected to extend toward 1.3395 USD, followed by a corrective bounce to 1.3415 USD. Once complete, the downtrend may resume toward 1.3290 USD, with further potential to 1.3220 USD. The MACD indicator supports this bearish near-term outlook, with its signal line below zero and pointing firmly downward.

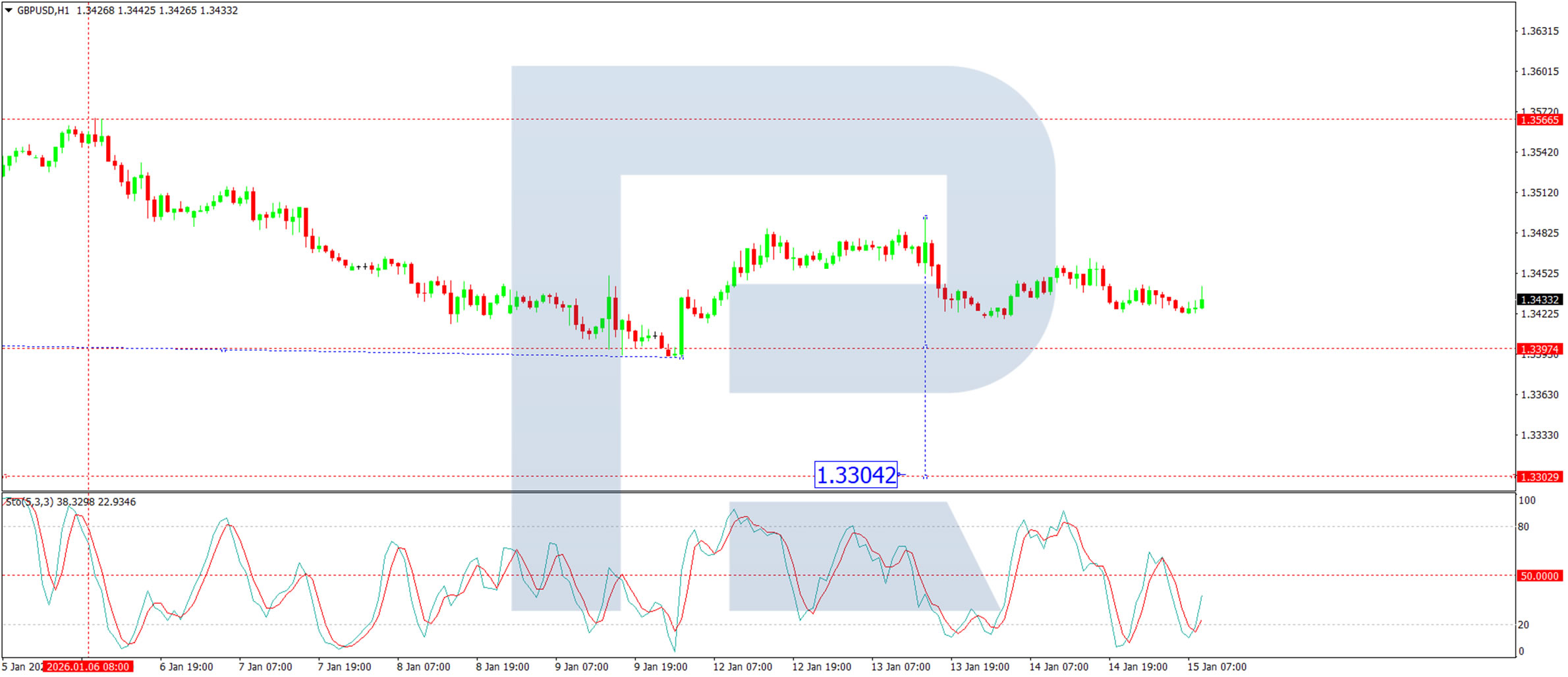

H1 Chart:

On the H1 chart, the pair has established a tight consolidation range around 1.3440 USD. A downward move toward 1.3395 USD is in progress, and a break below this level would open the door to further declines toward 1.3290 USD. The Stochastic oscillator aligns with this view, as its signal line is below 20 and trending lower, indicating sustained selling momentum.

Conclusion

Despite improving sentiment and a sharp reduction in speculative short positions, the pound remains vulnerable to downside risks from domestic data and shifting BoE expectations. Technically, the pair retains a near-term bearish bias, with key support levels at 1.3395 USD and 1.3290 USD. A break below these levels could accelerate declines, while any sustained recovery would likely require stronger-than-expected UK data in the coming week.

Nikkei 225 Forecast: Bullish Acceleration Above 53,370 Key Support

Key takeaways

Nikkei 225 is leading global equity performance in early 2026, rising 7.9% YTD and outperforming major US indices, supported by improving domestic macro conditions and resilience despite concerns over rising JGB yields.

Fundamentals remain a key tailwind, with Japan’s Citigroup Earnings Revision Index hitting a one-year high, signaling improving corporate earnings expectations versus the US and Europe, alongside potential political support from a snap election that could reinforce pro-stimulus policies.

Short-term technicals favour further upside, with bullish acceleration intact above the 53,370 key support; holding this level opens the door to resistance targets in the 54,565–55,623 range, while a break below would signal a near-term corrective pullback.

In our 2026 long-term global stock market outlook, published on December 26, 2025, we selected the Japanese stock market to outperform due to its improving macroeconomic factors and positive technical indicators.

Read more: 2026 Stock Indices Outlook: Dow Jones, Nikkei 225, Hang Seng poised to outperform

In this report, we will shift our focus to a shorter-term trading horizon, focusing on a one- to three-day period to project the likely trajectory of the Nikkei 225.

The narrative so far… Bullish, going against the fears of rising JGB yields

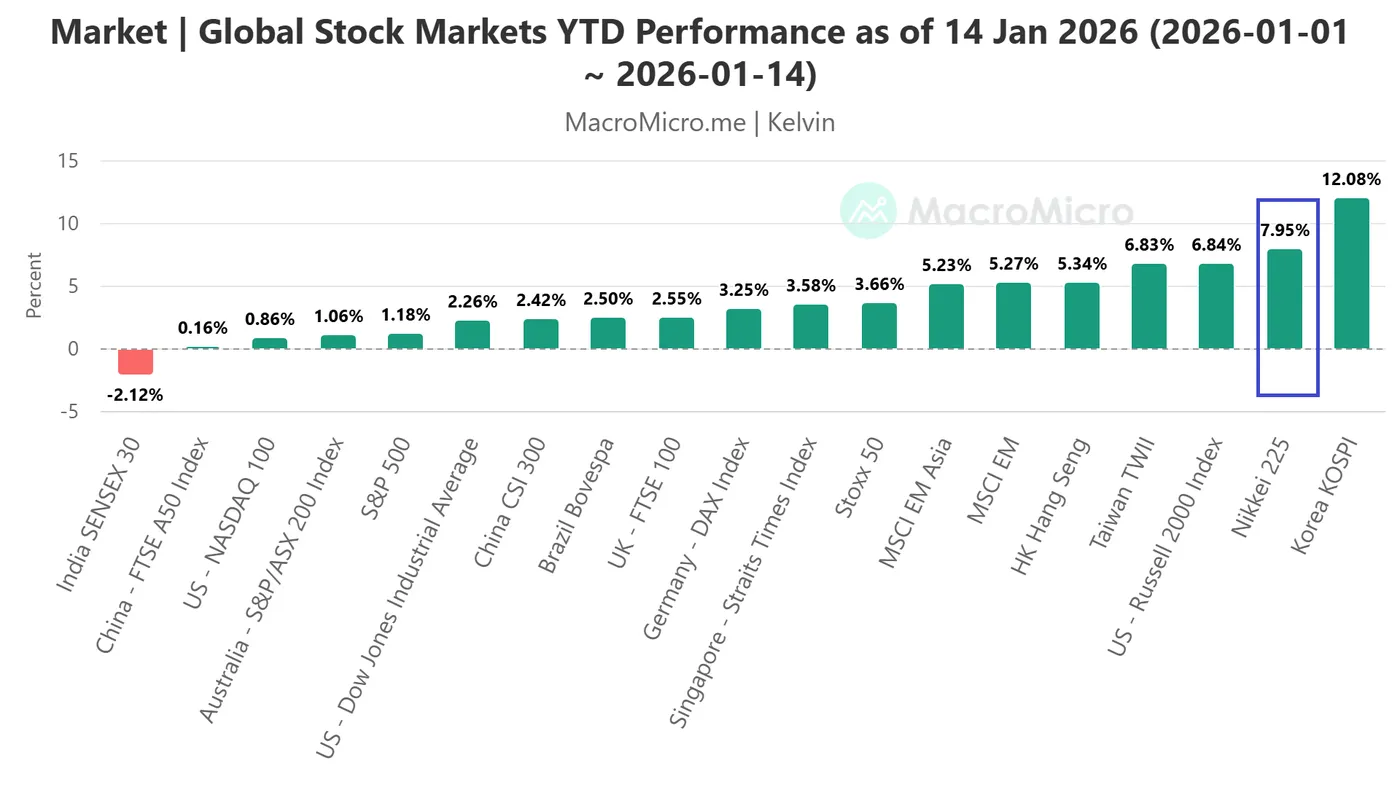

Fig. 1: Year-to-date global stock market indices as of 14 Jan 2026 (Source: MacroMicro)

The Nikkei 225 has continued to trade in a bullish trend since the start of the new year. The Japanese benchmark stock index rallied by 7.9% in local currency terms (ranked 2nd, see Fig. 1), just behind the 2025 red-hot, South Korea’s KOSPI that continues to extend its gains into 2026 with a positive return of 12.1% (see Fig. 1).

The Nikkei 225 has also outperformed the US stock market: small-cap Russell 2000 (6.8%), Dow Jones Industrial Average (2.3%), S&P 500 (+1.1%), and Nasdaq 100 (0.9%).

On top of the potential near-term positive feedback loop out from the internal political factor, where there is now growing chatter in the marketplace that Japanese Prime Minister Takaichi is likely to dissolve the lower house in parliament as soon as January 23 and call for a snap election soon, either on February 8 or February 15.

A snap election would likely aim to capitalize on high approval ratings of about 70% for Takaichi and could strengthen the Liberal Democratic Party’s grip on power in the more powerful lower house in Japan’s parliament. Hence, if successful as it is intended, Takaichi can have a firmer mandate to pursue pro-stimulus policies that are likely to boost economic growth prospects in Japan.

It’s all about earnings growth prospects

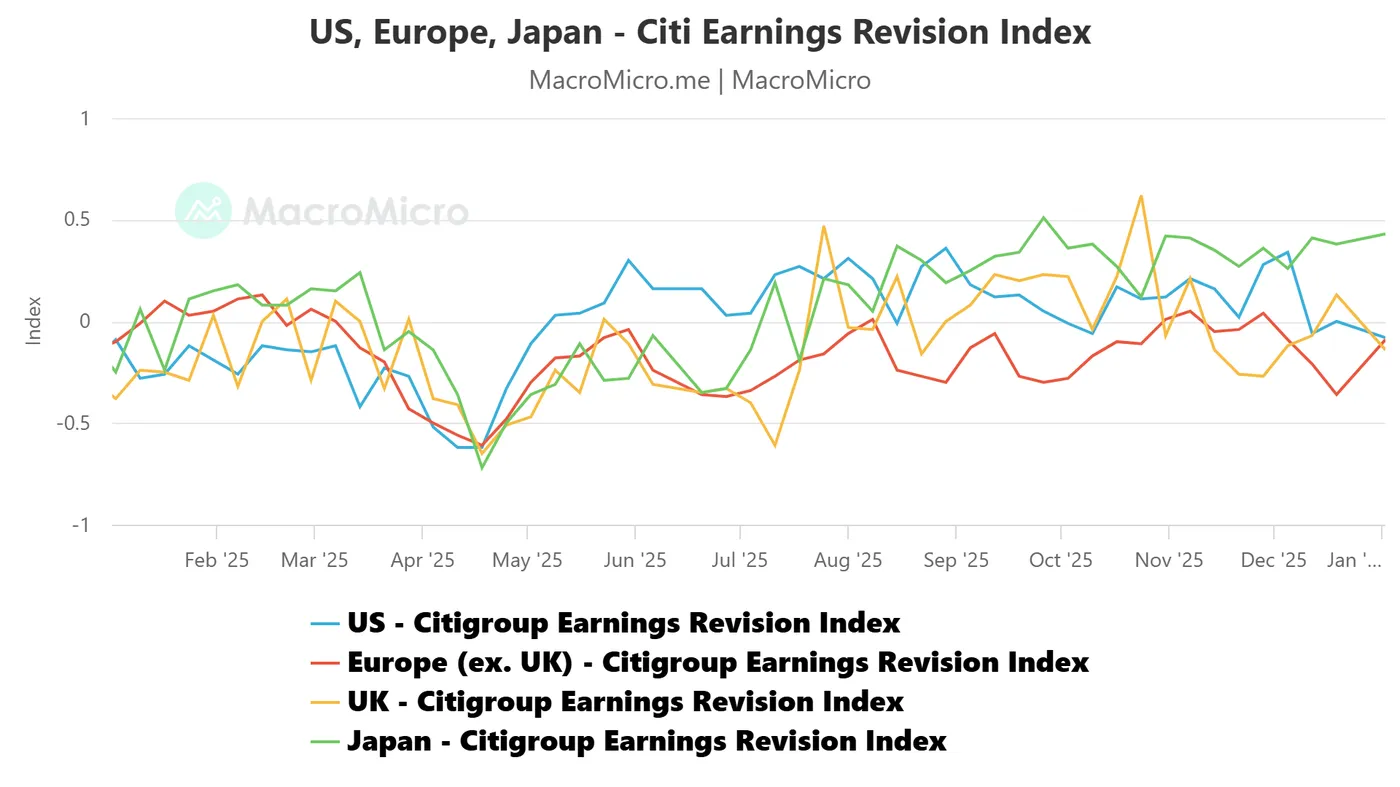

Fig. 2: Citigroup Earnings Revision Index (Japan, US, Europe, UK) as of 2 Jan 2026 (Source: MacroMicro)

Japan Inc’s earnings growth prospects have continued to lead the pack. Citigroup Earnings Revision Index for Japan has continued to trend upwards in the first week of 2026, where it rose to 0.43, a new one-year high as of 2 January 2026, surpassing the US (-0.08), Europe (-0.09), and the UK (-0.14) (see Fig. 2).

The Citi Earnings Revision Index is calculated as “Proportion of Companies with EPS Upgrades (%)” − “Proportion of Companies with EPS Downgrades (%)” (compared to last week). When the index is above the zero axis, it means that analysts on average, are optimistic about the outlook for corporate earnings, and vice versa, it means that analysts are relatively pessimistic.

Let us now focus on the short-term technicals on the Japan 225 CFD index (a proxy of the Nikkei 225 futures).

53,370 key short-term support to maintain bullish acceleration

Fig. 3: Japan 225 CFD index minor trend as of 15 Jan 2026 (Source: TradingView)

Since the 8 January 2026 low of 51,055, the price actions of the Japan 225 CFD index have transitioned into a potential acceleration phase within its latest minor uptrend phase that kickstarted on 18 December 2025.

Watch the 53,370 key short-term support to maintain the current near-term bullish state for the next intermediate resistances to come in at 54,565, 54,910/55,050, and 55,530/55,623 (Fibonacci extension clusters) next (see Fig. 3).

In addition, the hourly RSI momentum indicator has continued to hold above a parallel ascending support that suggests potentially short-term bullish momentum remains intact for the Japan CFD index.

On the flip side, failure to hold at 53,370 with an hourly close below it is likely to invalidate the bullish acceleration scenario to open up scope for a minor corrective decline sequence to expose the next intermediate supports at 52,830/53,644 and 52,060.

Natural Gas Prices Fall to a Near Five-Month Low

As the XNG/USD chart indicates, natural gas prices are trading very close today to the 2025 low formed in August.

The factors weighing on natural gas prices include:

→ Updated weather models, which are forecasting higher temperatures in the eastern US in late January (24–28), sharply reducing expected demand for gas used for heating.

→ Technical issues with power supply and pipelines at the Cheniere Corpus Christi and Freeport LNG terminals, which have reduced gas flows for export. This means gas that was destined for overseas markets is remaining on the domestic market, adding to inventories.

→ Supply–demand imbalance. US gas production is near record levels (110.7 billion cubic feet per day), while domestic consumption has fallen by 15.5% year-on-year.

Technical Analysis of the XNG/USD Chart

In our earlier analysis of gas prices, we identified a long-term descending channel, shown in red on the chart. On 19 December, we:

→ noted that the price was trading near the channel’s median, where supply and demand typically balance;

→ suggested that the market could enter a consolidation phase.

Indeed, prices hovered around the median until 30–31 December, when a sharp decline began. During this move:

→ bearish gaps formed on the XNG/USD chart, indicating a strong dominance of sellers;

→ based on the price action, a downward trajectory can now be drawn (shown by the orange lines).

Traders should be prepared for the possibility that, in the near term, bears may attempt to break below the 2025 low. In that case, it cannot be ruled out that:

→ this would have a psychological impact on the market;

→ sellers would take profit on short positions;

→ buyers could step in and push gas prices up towards the R2 resistance line.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

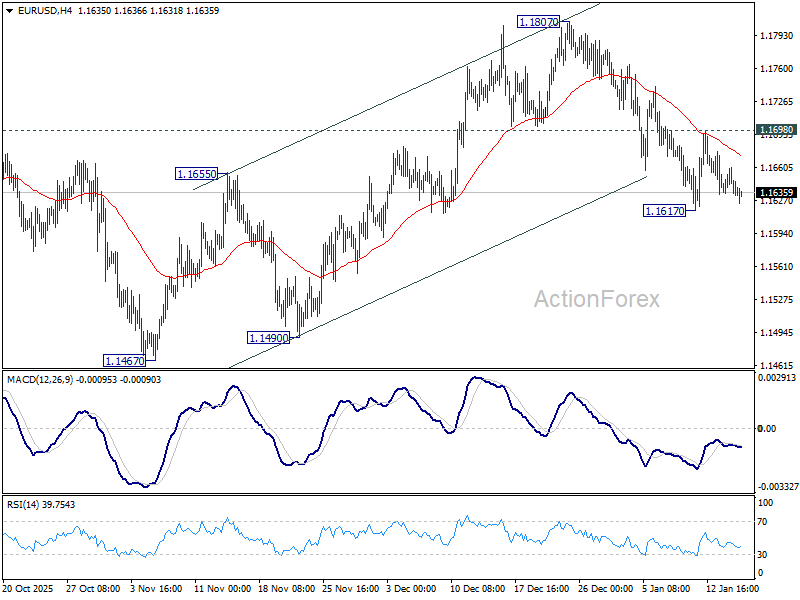

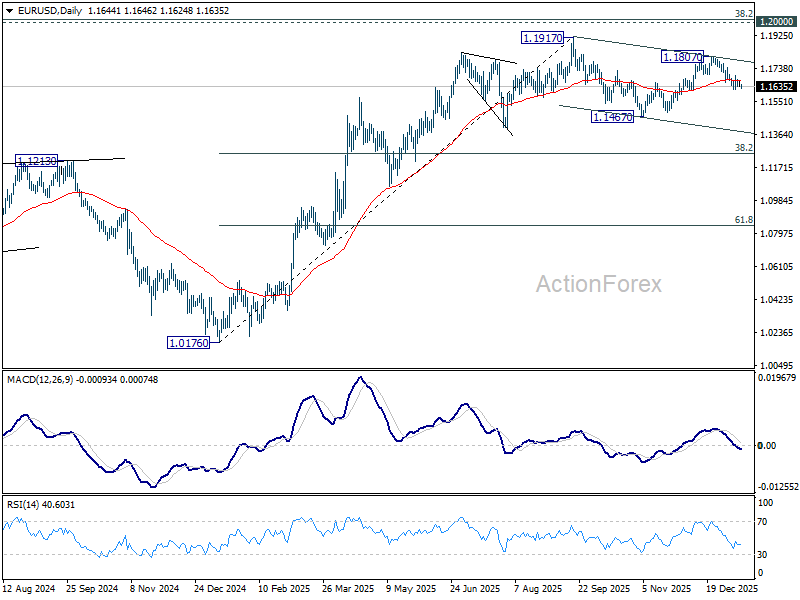

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1633; (P) 1.1648; (R1) 1.1659; More….

Intraday bias in EUR/USD remains neutral as range trading continues. On the downside, below 1.1617 will resume the fall from 1.1807, and target 1.1467 support. On the upside, above 1.1698 will bring stronger rebound to 1.1807. Overall, price actions from 1.1917 are seen as a corrective pattern that might extend further.

In the bigger picture, as long as 55 W EMA (now at 1.1416) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

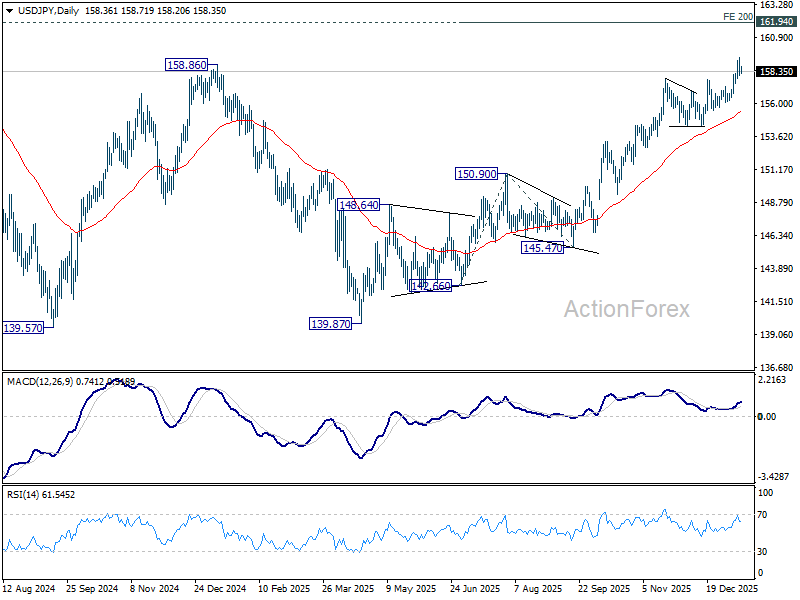

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.87; (P) 158.66; (R1) 159.23; More...

USD/JPY is extending consolidations below 159.44 and intraday bias stays neutral. Deeper retreat could be seen but downside should be contained above 156.10 support to bring another rally. On the upside, above 159.44 will resume larger rise from 139.87. Next target is 200% projection of 142.66 to 150.90 from 145.47 at 161.95, which is close to 161.94 high.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.38 support will dampen this bullish view and extend the corrective range pattern with another falling leg.