Sample Category Title

RBA on Hold in 2026, Risks on Both Sides

Westpac Economics sees inflation heading back to target in the year ahead, but this will not be enough to shift the RBA’s more hawkish mindset. Rates on hold in 2026, with risks on both sides.

- Westpac Economics has revised its outlook for the RBA cash rate to an extended hold for the whole of 2026. While the RBA recognised that some of the recent inflation surprise reflected temporary factors, it has clearly taken signal from it. Inflation is expected to moderate in 2026, but not soon enough to induce the RBA to step back from its current hawkish view of the risks. If our broader set of forecasts are borne out, rate cuts are still feasible in February and May 2027.

- There are risks on both sides of our base case view. We reserve the option to put rate cuts in 2026 back on the table if the labour market starts to unravel. We think that rate hike talk is premature. We cannot rule out that more near-term bad news on inflation spooks the RBA and induces a near-term hike, but in our view, it is not the most likely outcome. If it does happen, though, our forecasts for growth, the medium-term inflation outlook and the labour market would need to be revised down, and a subsequent reversal of that policy tightening would be in play in 2027.

The Australian economy has been playing out broadly as Westpac Economics expected. Public sector demand growth is slowing and indeed was negative over the first half of 2025. Private sector demand growth is recovering, and the labour market is gradually easing. Underlying growth in labour costs is also easing, and productivity growth is already running faster than the RBA’s pessimistic trend assumption. Our forecasts see 2026 as involving further recovery from the period of very weak private sector demand growth. The ‘shaky handover’ risk, of private sector growth not picking up as public sector demand growth normalised, looks to have dissipated.

Inflation saw a bump in September quarter and October month. The main sources of the surprise had little to do with domestic demand or labour market pressures. Rather, a sizeable part of that bump looks to have been administered prices and noise. The RBA recognised this at the time but has since communicated that it is more worried about upside risks to inflation. And since what matters for monetary policy is how the RBA sees things, this means that rate cuts are off the table for the time being.

We expect inflation to get back to the RBA’s target (and below the midpoint of the 2–3% range on a trimmed mean basis), but not until later in 2026. This is too late to give the RBA enough comfort to start cutting rates on our previously expected timetable of May and August 2026. Accordingly, we push out the earliest feasible timetable for rate cuts beyond 2026. If our inflation and labour market view is right, by the end of 2026 it will become apparent that domestic inflation pressures have eased. This would leave the way clear to remove remaining policy tightness in the first half of 2027 – we pencil in February and May 2027 for that normalisation. If the labour market weakens noticeably more than we expect, we reserve the option to put earlier rate cuts back on the table.

Following the inflation surprises, markets immediately rushed to the other side of the boat to price in rate hikes. The probability of a hike is not zero, and the RBA was right to warn the community of the possibility. In our view, however, a near-term hike is far from the base case. Labour market data has been less bullish than the inflation data, and the Monetary Policy Board will need to balance this with its fears about inflation. Further upside surprises on inflation in the rest of the December quarter or early 2026 would tip the balance but would not be warranted if our own inflation forecasts are borne out. If a near-term hike does happen, though, our forecasts for growth, the medium-term inflation outlook and the labour market would need to be revised down, and a subsequent reversal of that policy tightening would be in play in 2027.

Our assessment that inflation is still headed down accounts for the role of past restrictive policy and the unwind of earlier government policies. Too much market commentary has understated the role of policy lags. Monetary policy takes time to affect the labour market and inflation, with most estimates pointing to a peak effect after at least a year. This means that recent outcomes mainly reflect the influence of the peak cash rate a year or so ago, and thus that further labour market easing is likely. Some of that policy restrictiveness was masked by the ramp-up in the jobs-rich ‘care economy’ and strong public sector infrastructure spending. As these offsetting factors fade, along with the growth boost from last year’s tax cuts, the effects of past restrictive policy remain in the system because of these usual lags. This would be true for some time even if the 75bp reduction in the cash rate since the peak had fully removed policy restrictiveness, which we do not think is the case. At current levels of the cash rate and other interest rates, monetary policy remains mildly restrictive. Given the usual lags, this will continue to be evident in the data throughout 2026.

Bank of England (BoE) Preview: A Hawkish Cut in a Stagnating Economy? Implications for the GBP & FTSE 10

The Bank of England’s (BoE) final Monetary Policy Committee (MPC) meeting of 2025, scheduled for December 18, arrives amid strong conviction from financial markets: a festive interest rate cut is imminent. After a recent pause, the BoE is widely expected to resume its easing cycle, a move necessitated by a stalling UK economy and confirmed disinflationary signals.

However, the decision is far from unanimous, and the resulting vote split and crucially, the forward guidance that accompanies it and will determine the market reaction and the economic outlook for 2026.

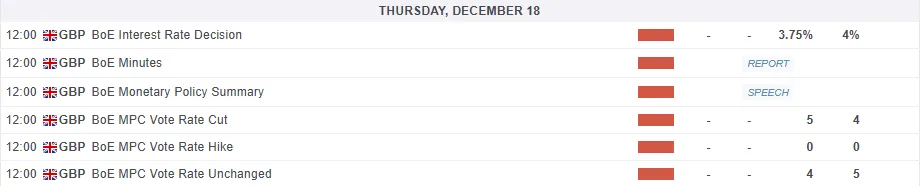

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

The Potential Decision: A Narrow Rate Cut to 3.75%

The overwhelming expectation, priced in by over 90% of the market, is for the MPC to vote for a 25 basis point (bp) cut, lowering the Bank Rate from 4.00% to 3.75%. This would mark the central bank's fourth rate cut of the year.

This move follows a decision to keep rates unchanged in November, when Governor Andrew Bailey said he needed more proof that inflation was truly slowing down before making any changes.

Weak Growth: UK GDP contracted by 0.1% in October, missing forecasts and confirming the economy's anaemic performance since mid-year. Economic growth is expected to remain weak well into 2026.

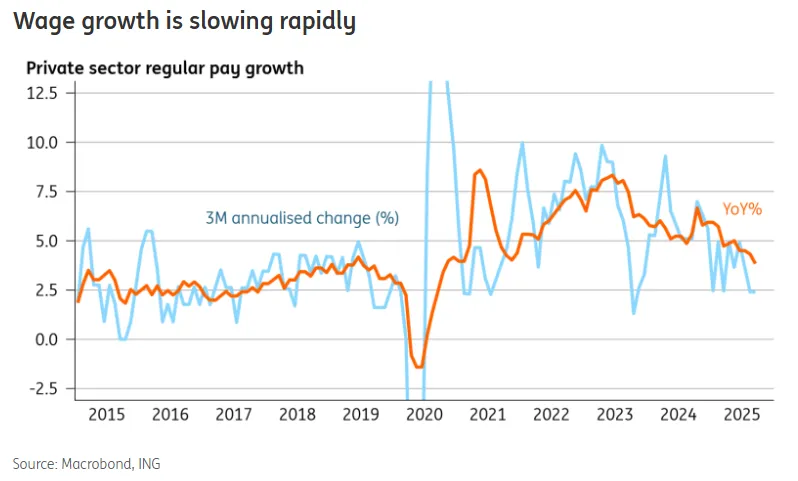

Soft Labour Market: Unemployment has crept up to 5%, hiring surveys remain weak, and wage growth, a key indicator for underlying inflation, is rapidly slowing toward more manageable levels.

Source: ING Think

Cooling Inflation: Headline Consumer Price Index (CPI) has fallen to 3.6%, generally tracking the BoE’s projections.

Despite these strong reasons to cut rates, the decision will likely be very close, with a predicted 5-to-4 vote. Governor Bailey is expected to be the deciding vote, likely siding with the group that favors lower rates (the "dovish" camp). This sharp division among the voters highlights just how difficult the current economic situation is for the central bank to manage.

Given the split and the challenges facing the BoE a ‘hawkish cut’ may be the compromise. The Bank will deliver the 25bps reduction to support growth but will utilize the meeting minutes and the Governor's press conference to issue cautious guidance.

Message: "We are adjusting the level of restriction, not stimulating the economy."

Guidance: They will likely signal that future cuts are not automatic and will depend on data, specifically services inflation. This is designed to prevent the market from pricing in an aggressive 50bps cut cycle that could devalue the Pound too rapidly.

I could of course be wrong but this would seem like the most logical step for the BoE.

Market Implications: Pricing the Pivot

Market participants have aggressively positioned for this outcome, but the nuance of the decision will determine price action across asset classes.

Sterling (GBP) Outlook

The Pound is trading in a precarious range, heavily influenced by the divergence between the UK’s stagnation and the US’s relative resilience.

GBP/USD (Cable): Currently trading near 1.3360-1.3400. The pair has been supported recently by a broadly weaker US Dollar (following the Fed’s dovish signals).

- Reaction to Cut: A "dovish cut" (cut + signal of rapid future easing) could see GBP/USD break support at 1.3280. A "hawkish cut" (cut + caution) would likely see the pair test resistance at 1.3420-1.3500.

- Strategic View: The medium-term outlook for GBP is negative due to the weak growth fundamentals (GDP -0.1%) and the correlation to risk-off sentiment. If the UK enters a technical recession while the US achieves a soft landing, the yield differential will move against Sterling.

GBP/USD Daily Chart, December 16, 2025

Source: TradingView (click to enlarge)

EUR/GBP: With the European Central Bank (ECB) expected to hold rates in December , a BoE cut widens the policy divergence in favor of the Euro. This could put upward pressure on EUR/GBP.

Gilt Markets (Government Bonds)

The Gilt market is poised for a "bull steepening" of the yield curve.

- Short End (2-Year): Yields are expected to fall as they track the reduction in the Bank Rate to 3.75%.

- Long End (10-Year): Goldman Sachs forecasts 10-year yields to fall to 4.25% by year-end and 4.00% by end-2026. However, concerns about the fiscal deficit (increased borrowing in the Reeves budget) provide a floor to how far long-term yields can fall.

FTSE 100: The impact is mixed. While lower rates help, a stronger Pound (if the cut is hawkish) hurts the overseas earnings of the large-cap exporters. Conversely, if the Pound falls, the FTSE 100 typically outperforms.

FTSE 100 Daily Chart, December 16, 2025

Source: TradingView (click to enlarge)

Challenges and Risks for the Bank of England Moving Forward

The Bank of England's Three Big Risks In 2026, the Bank of England faces a difficult situation where it must choose between three dangerous paths, often called a "trilemma."

Risk 1: Causing a Recession If the bank is too cautious and cuts interest rates too slowly, the slight economic shrinkage we saw in October could turn into a serious recession. This would likely cause unemployment to shoot up past 5.5%, forcing the bank to make panic cuts later, which would make people lose trust in the economy.

Risk 2: Letting Inflation Return On the other hand, if the bank cuts rates too quickly while the government’s new budget raises business costs, inflation could get stuck at a high level of 3% to 4%. This would make everything more expensive for longer and might force the bank to suddenly raise rates again—a chaotic cycle similar to the economic trouble of the 1970s.

Risk 3: Corporate Bankruptcy Finally, there is a risk to businesses. Although banks are currently safe, many companies need to refinance their debts in 2026. If interest rates stay high, these companies might not be able to afford their loans and could go bankrupt. A wave of business failures would eventually hurt the banks that lent them money.

Final Verdict

Market participants should prepare for a rate cut that feels "hawkish" in its delivery. The BoE will cut, but they will promise nothing regarding the speed of future easing.

This creates a complex environment for Sterling, which may struggle to find direction until the 2026 inflation data clarifies the path to the terminal rate. The era of 4% interest rates is ending; the era of managing the "stagflation exit" has begun.

WTI Oil Prices at 2025 Lows – Opportunity or Trap?

Oil prices have been tumbling without stopping in a stable but continuous downtrend.

A positive development that encourages cuts by reducing inflation expectations for consumers, but with prices back to January 2021 levels, producers are pressured to decrease investment in technology and rig development.

For example, US Shale is known to be profitable at around $70 per barrel.

As pressure mounts, producers can be squeezed out of the Market, which can then result in a too-short supply in the future, potentially raising future prices in the energy commodity.

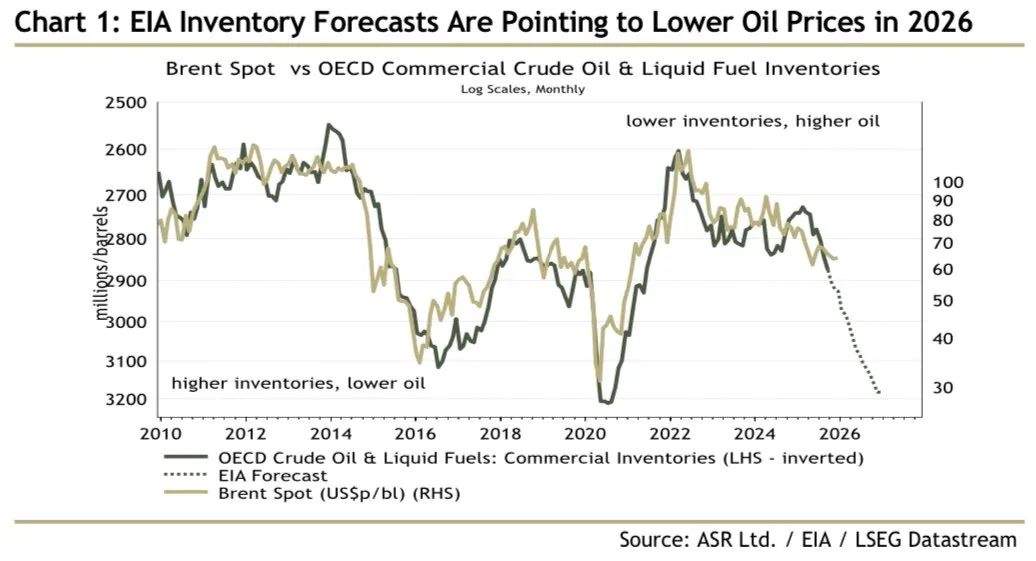

Falling Inventories and Falling Oil Prices – Source: LSEG, published by Ian Harnett

Following a mid-October trough, better-looking Chinese demand led to a rebound in prices to $60 in mid-November; however, prices have since fallen rapidly.

Current factors for the fall in Oil include:

- The current OPEC+ high supply is known to hurt demand, as intra-organizational dynamics point to some members wanting to restrain margins to capture market share.

- The Market could also be pricing a reopening of the Venezuelan Oil Market to OECD markets if pressure on Maduro from the Trump Administration increases.

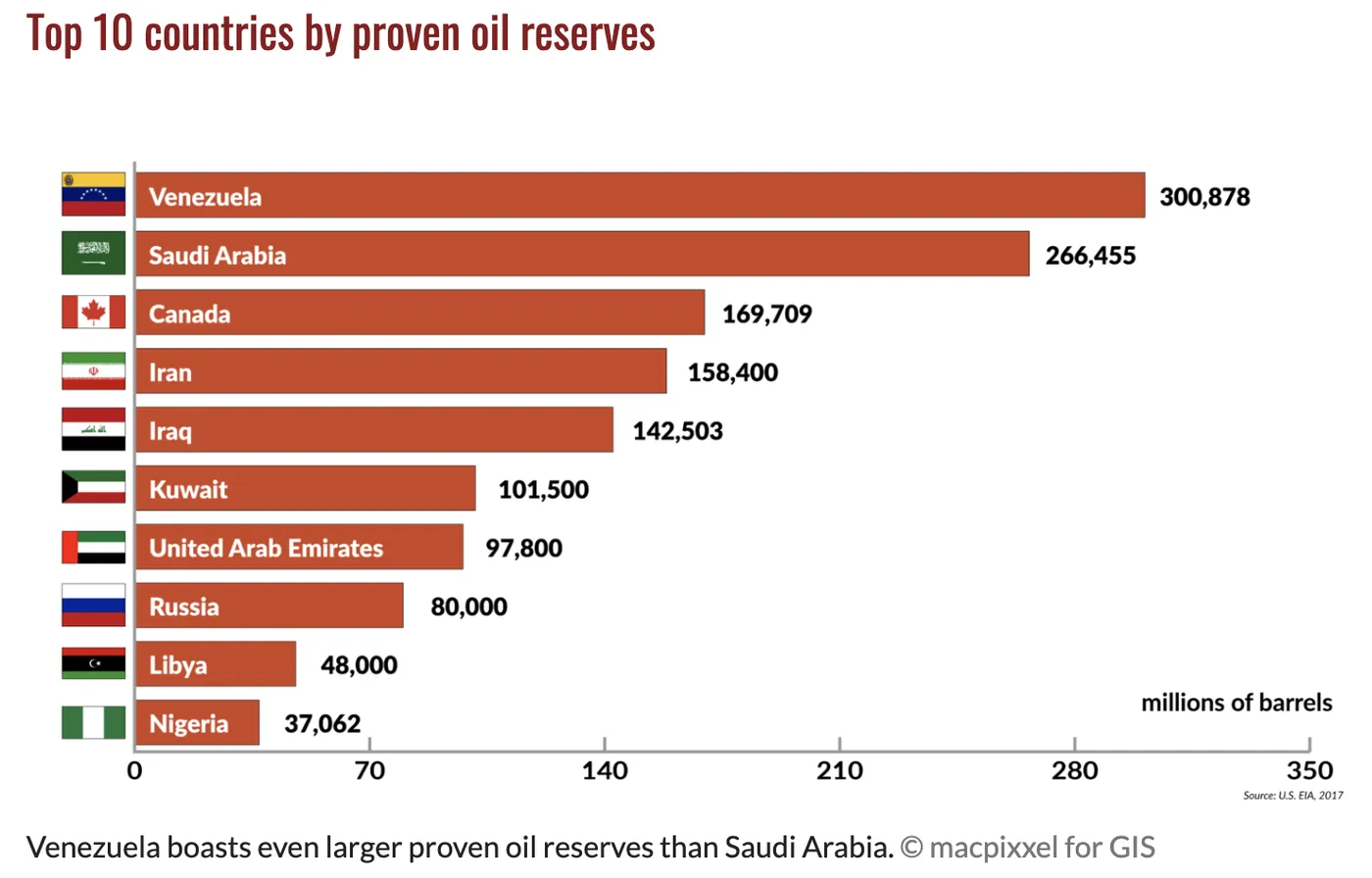

- We are still far from this, but the rising tensions between Washington and Caracas are surely getting priced into the Market. In case you did not know, Venezuela sits on the largest proven Oil reserves in the world, even surpassing Saudi Arabia, the world's largest producer.

- Traders are also pricing a ceasefire between Russia and Ukraine, which could lead to more supply, leading to the current substantial fall.

World's Proven Oil Reserves by Country – Source: GIS

Caveat on the Russia-Ukraine ceasefire acting as bearish force

Throughout this conflict, there has been many mentions of Russian supply to the West being reduced, but to sponsor their war, Russians have found ways.

Finding new buyers is one: by offering cheap oil and flooding the Markets, there is still large interest for Russian Oil – China and India, the two largest Oil consumers being the biggest buyers (without counting some EU countries still dependent on the imports)

Shadow Fleets are also common, with Tankers from Turkey allowing to transport and sell sanctioned Oil to Western buyers under legal names – Discover the Sanctions Paradox

My contrarian view is one of a Russia-Ukraine conflict ending which could actually be a bullish catalyst for Oil prices, as illegal, cheaper oil would be less available and a reopening of traditional Markets to Russia could add to the competitive bidding. That could result in a sell-the-rumour, buy-the-news reaction.

But it's just a theory.

In any case, let's dive into a multi-timeframe analysis of WTI Oil to spot if Oil trading at 2025 presents a technical opportunity or a trap.

US Oil (WTI) Multi-timeframe Technical Analysis

Daily Chart

US Oil (WTI) Daily Chart, December 16, 2025 – Source: TradingView

Oil has broken below its short-term Channel mentioned in our preceding Analysis, strongly reacting to the 50-Day Moving Average.

The MA stands out as the key Technical Indicator for the Oil trend, providing very strong entry points throughout the descent.

As a matter of fact, any long-term technical reversal would be valid only on a weekly close above the 50-Day MA.

With no sign of divergence and a consistent fall, technicals are signalling that the downtrend is stable and is not showing signs of weakness.

Nevertheless, some reversal signs could be emerging on shorter timeframes.

Let's dive into it.

4H Chart and Technical Levels

US Oil (WTI) 4H Chart, December 16, 2025 – Source: TradingView

A reversal could be near, with the second wave of selling forming an exact measured move of the preceding selloff.

Coming in precisely at the lows of the Daily Channel seen on the higher timeframe, elements are adding into a potential reversal.

The price action is still mostly bearish, so to get confirmation of such a reversal, traders will need to see a bullish candle which closes at least above the preceding 4H candle ($55.65).

Levels to place on your WTI charts:

Resistance Levels

- Key September Resistance $65 to $66

- May range Resistance $63 to $64

- $60.90 Past Week highs

- $58.265 short-timeframe pivot level

- May Range lows support $59.00 to $60.50 (Broken, now Major Pivot)

Support Levels

- $55 to $56.50 2025 Support and Channel lows (testing)

- Session lows $55.00

- 2019 mini support $53 to $54

- Mid-2019 Main support $51 to $52.50

1H Chart

US Oil (WTI) 1H Chart, December 16, 2025 – Source: TradingView

The selloff is very strong and may not reverse suddenly.

Keep an eye on whether the session closes below $55.00 which acts as the key level for further action.

A weekly close would confirm a further breakdown.

Failing to break the lows however may lead to some consolidation. As said on the 4H timeframe, any reversal would require an initial sign of reversal (strong bull candle).

Safe Trades!

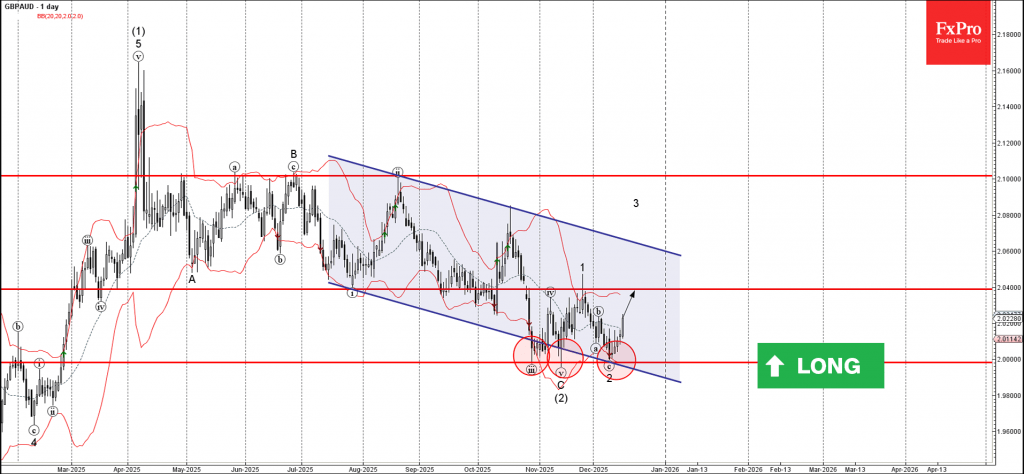

GBPAUD Wave Analysis

GBPAUD: ⬆️ Buy

- GBPAUD reversed from support area

- Likely to rise to resistance level 2.0400

GBPAUD currency pair recently reversed up from the support area between the round support level 2.000 (which has been reversing the price from October, as can be seen below), lower daily Bollinger Band and the support trendline of the down channel from July.

The upward reversal from this support area started the active short-term impulse wave 3 of the intermediate impulse wave (3) from November.

Given the strength of the support level 2.000 and the bearish Australian dollar sentiment seen today, GBPAUD cryptocurrency can be expected to rise to the next resistance level 2.0400.

Bank of Japan Preview

Summary

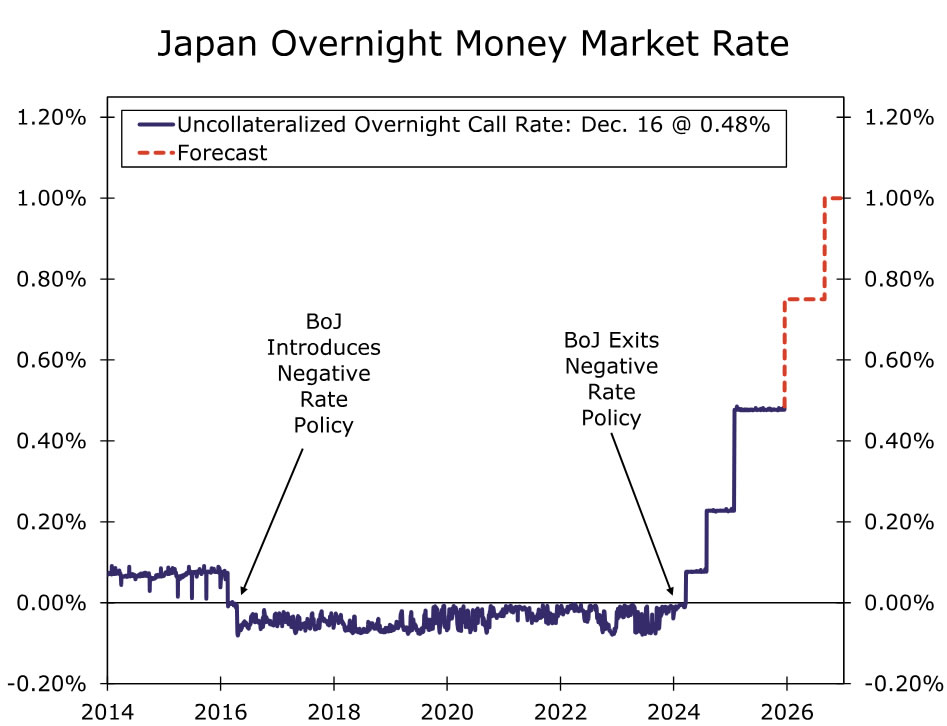

Bank of Japan (BoJ) policymakers are set to raise rates 25 bps this week, a now consensus view but a stance we took well before financial markets fully priced tighter BoJ monetary policy. Markets fully digesting a BoJ December rate hike likely means the Japanese yen will fall short of hitting our YE-2025 USDJPY target; however, no element of surprise also means emerging market currencies should be more protected and not experience much post-hike volatility, a different dynamic relative to last year's BoJ August hike that injected volatility across many high-yielding emerging currencies as the yen funded carry trade unwound.

Looking ahead, even before we hear from BoJ policymakers on the outlook for monetary policy, we are adjusting our BoJ forecast profile to now include another 25 bps rate hike in Q3-2026. Financial markets are priced for the BoJ to deliver a rate hike closer to the end of next year, which puts our updated BoJ outlook moderately out of consensus on the more hawkish side. Our revised view leads us to believe the yen may be more resilient in H2-2026 than we originally forecast on diverging paths for BoJ-Fed monetary policy.

Bank of Japan Preview

Bank of Japan (BoJ) policymakers will make their final monetary policy decision of 2025 at the end of this week, and we—alongside the broader consensus—expect a 25 bps rate hike to be delivered. We have been steadfast in our view that the BoJ would raise rates this week, a forecast we highlighted in our 2026 Annual Economic Outlook well before financial markets fully priced a December rate hike. Our rationale for a hike came down to our assessment of underlying economic fundamentals in Japan which—despite political preference for easier monetary policy after Prime Minister Takaichi's election earlier this year—we felt were consistent with tighter BoJ monetary policy. Since we published our year ahead outlook, economic fundamentals, in our view, have become more consistent with higher interest rates. This conviction stems from wage hikes that are above the current pace of inflation, fiscal stimulus deployed by the Takaichi administration and leading indicators that suggest activity is still firm. Adding to our conviction is a Japanese yen that has broadly remained on the defensive and has not participated in the dollar depreciation trend as much as peer G10 currencies.

Going forward, we do not believe that Japanese economic conditions are set to change all that materially. Meaning, we expect the Japanese economy to remain supported, and while GDP growth will not be all that exciting in 2026, we expect activity to continue to be consistent with an economy that can digest higher interest rates. On inflation, headline CPI may slip back toward the BoJ's target next year; however, wage hikes, fiscal stimulus and the lagged effect of U.S. imposed tariffs keep the balance of risk tilted to the upside. Taken together, resilient growth and upside risks to inflation, we are revising our Bank of Japan forecast profile to now include another 25 bps rate hike to be delivered Q3-2026 (Figure 1). As of now, financial markets are priced for additional BoJ tightening in Q4-2026, leaving our view moderately out of consensus and more hawkish relative to peer economists. Similar to the upcoming December hike, local political dynamics will remain the biggest hurdle to additional tightening. But if local economic conditions evolve as we expect in 2026, we have our doubts that political preference or interference will prevent BoJ policymakers from taking the BoJ Target Rate to 1.00% by the end of next year.

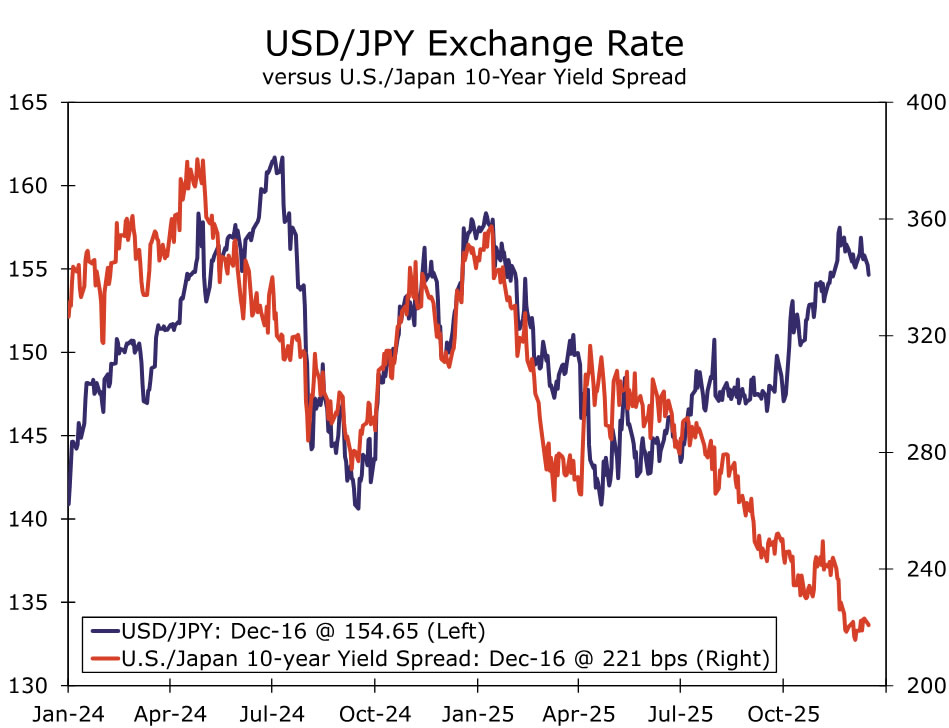

Should the BoJ move ahead with a hike this week, the yen may not strengthen the way we outlined in our 2026 outlook, at least not in the near-term. When we published our 2026 outlook, our BoJ December hike forecast was very much out of consensus, and we believed the rate hike would be more of a surprise that would prompt a sharp JPY rally headed into the end of the year. But as mentioned, with a hike almost fully priced, near-term upside for the Japanese yen is likely limited. Or said another way, for JPY to strengthen in line with our forecast, an exogenous catalyst would need to materialize. Rather than a USDJPY move lower toward our original Q4-2025 target of JPY152.00, USDJPY is likely to hover around current levels through the end of this year. Also, with financial markets expecting a BoJ December rate hike, volatility across emerging market currencies, similar to what unfolded after the BoJ raised interest rates in August 2024, is unlikely. Carry positions funded by Japanese yen have been scaled back as other funding currencies (i.e., CHF) have become associated with less hawkish central banks, and in turn, have become more popular alternatives. Positioning data suggests leveraged funds are also net long JPY, additional evidence that EM currencies should be more protected in the upcoming BoJ hike. More medium-term, the Japanese yen could be more resilient than we initially expected. An earlier rate hike in 2026 than markets are pricing should be supportive of the yen, especially when considering USDJPY has been disconnected from U.S. Treasury and Japanese Government Bond yield differentials over the back half of 2025 (Figure 2). We still believe the U.S. dollar will be in rebound mode when the BoJ delivers its hike in 2026, but against a backdrop of major central banks keeping monetary policy settings on hold by H2-2026, BoJ rate hikes should prevent USDJPY from rising as much as initially expected over the back half of next year.

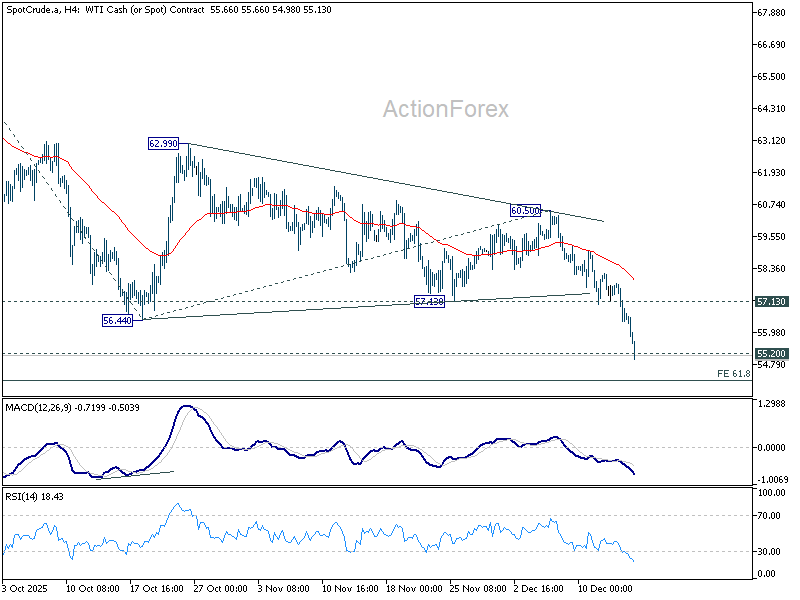

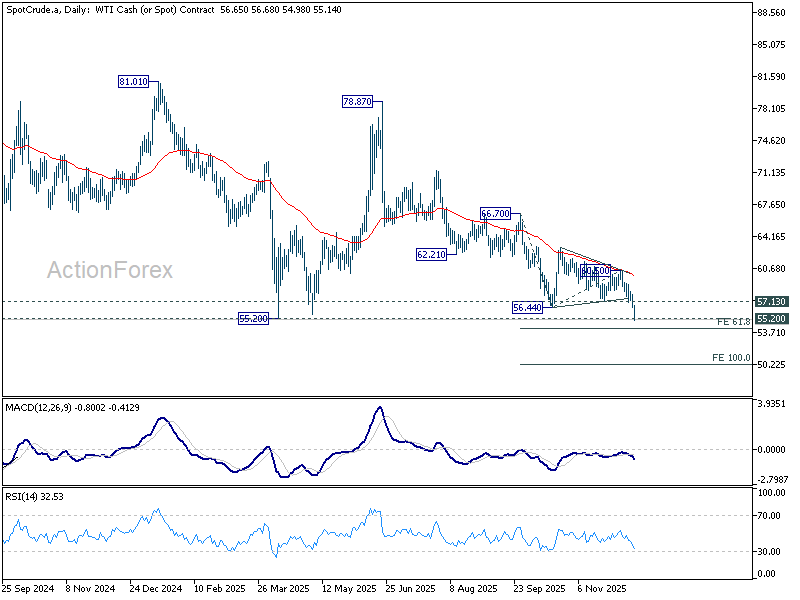

Oil bears regain control as Ukraine peace hopes fuel selloff, WTI eyes 50

WTI crude extended its selloff sharply today, breaking to the lowest level since early 2021 and deepening one of its worst annual performances in years. The US benchmark is now down roughly 22% for the year, marking its weakest showing since 2018. With downside momentum accelerating, WTI might be targeting 50 psychological level if selloff persists in the coming days.

A key catalyst behind this week’s intensified selling has been rising optimism around a peace agreement in Ukraine. Reports earlier in the week suggested US officials believe a deal to end the war is close, with roughly 90% of issues between Ukraine and Russia said to be resolved. That prospect has revived expectations of eventual normalization in energy flows.

However, significant hurdles remain. Any final agreement still hinges on territorial disputes between Kyiv and Moscow, as well as firm security guarantees. While President Volodymyr Zelenskyy has agreed to abandon Ukraine’s goal of joining NATO, he continues to push for Article Five–like security protections from the US and Europe, a demand that remains unresolved.

Beyond geopolitics, oil markets have been under sustained pressure from supply-side developments. OPEC+ members have ramped up production aggressively this year after years of coordinated output cuts, adding to concerns that global supply is now running ahead of demand at a time when growth momentum remains uneven.

Technically, the break of 55.20 low suggests that WTI's long term down trend is resuming. Immediate focus is now on 61.8% projection of 66.70 to 56.44 from 60.50 at 54.15. Decisive break there would pave the way to 100% projection at 50.24. Outlook will stay bearish as long as 57.13 support turned resistance holds, in case of recovery.

Sunset Market Commentary

Markets

European PMIs were nothing but the amuse-bouche ahead of the more important US economic update, if only because they don’t fuel further speculation for rate hikes per se but simply confirm the ECB’s rates status quo for longer. The stoic FX and FI income reaction was testament with EUR/USD hovering directionless just north of the recently conquered 1.1747 (minor) resistance level. European rates trade a tad higher at the long end (30-yr swap closing in on the 2023 12-yr high). The overall PMI came in below expectations by falling to 51.9 from 52.8. The December reading nevertheless marks a one-year long expansion (>50), the first in the post-pandemic era. Services grew slightly slower (52.6) while manufacturing contracted faster (49.2). New orders, though slower than in November, rose for a fifth month but export business decreased at the fastest rate since March. Employment grew enough in services to offset staff reduction in manufacturing. Companies noted a marked rise in input costs in both sectors but that doesn’t translate so far into output inflation, labeled “modest” by the PMI owners. Manufacturers’ optimism for the future reached its highest since February 2022 (German stimulus approval?) while services companies hit a seven-month low. The UK version surprised to the upside and, combined with a slightly less worse than feared labour market report, pushes GBP higher to EUR/GBP 0.876.

Going into the much-anticipated payrolls, ADP’s weekly update of the job market signaled momentum building in the second half of November (and as previous weak prints drop out of the equation). Hiring picked up to 16 250 jobs per week in the four weeks ending November 29 after four weeks of job losses. Next week’s reading could be strong as well with 4-week MA moving beyond the dire Nov 8 week. Turning to the official labour market data, October employment tanked by 105k, driven by the government sector (-157k). Not all losses were recouped for in November, and even though the +64k was a bit more than the 50k expected it was extremely thinly-based with one sector (health, social assistance) accounting for virtually all of the job creation. Employment for August and September was revised down by a combined 33k. The unemployment rate rose from 4.4% in September to 4.6% in November, low still but a 4-yr high and taking the US economy a step closer in triggering the Sahm recession rule (0.376 vs 0.5 trigger). The rise in the participation rate (62.5%) may offset some of the unemployment rate concerns. The BLS noted that the response rate was lower than usual, muddying the underlying trends. The caveat comes on top of Fed chair Powell last week saying the payrolls reports since April may end up having overestimated employment by an average 60k per month when the final benchmark revisions happens early next year. These statistical quirks complicate the market conclusion, especially with additional noise coming from the ADP, the solid (core) retail sales (control group +0.8%) and decent yet lower-than-last-month US PMIs. Front end yields dropped up to 5 bps in a kneejerk reaction but soon pared losses. Fed bets for a January cut remain largely unchanged at 25%. Long maturities are stable. EUR/USD is eager to test the 1.18 big figure. DXY fell towards 98. US equities open slightly lower.

News & Views

UK PMIs signaled accelerating economic output growth in December, led by the sharpest rise in new business for 14 months. The UK composite output index improved to 52.1 from 51.2. Both services activity (52.1 from 51.3) and manufacturing output (51.8 from 50.3, highest in 15 months) contributed. Growth was still subdued compared to long-run trends. The rise in orders mainly came from services. This also helped backlogs of works to have increased from the first time since February 2023. Despite better output and new orders, staffing levels continued to decline at a solid pace, often attributed to intense cost pressures. Especially input prices in the services sector reaccelerated. S&P commented that the report ‘brought welcome news on faster economic growth at the end of the year, with businesses buoyed in part by the post-Budget lifting of uncertainty’. S&P sees current PMI as consistent with growth accelerating to 0.2% in December, but still only expects quarterly growth in Q4 at 0.1%. Today’s report probably won’t change the assessment of the BoE at Thursday’s policy meeting, expected to result in 25 bps lower rates to 3.75%. Better than/less worse than expected PMI’s & labour market data publish morning are (slightly) lifting UK yields. Sterling rebounds from near EUR/GBP 0.8795 to 0.876.

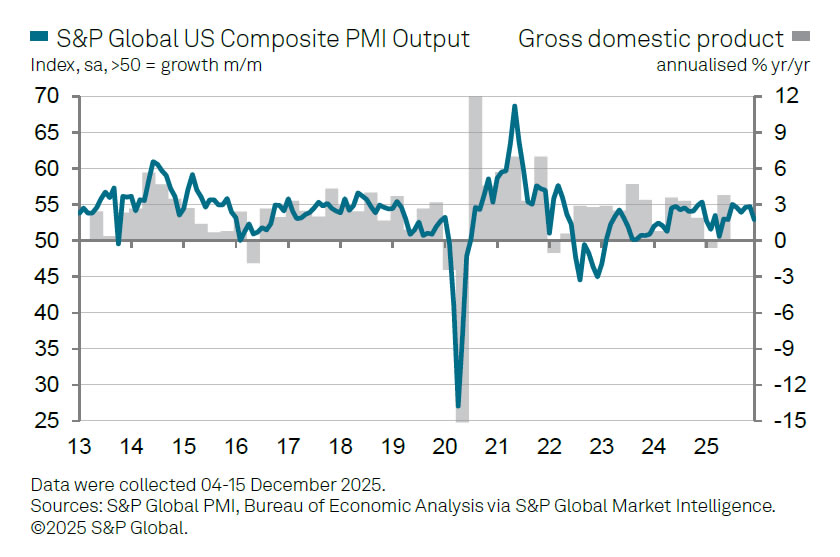

US PMIs point to broad-based cooling despite solid 2.5% annualized Q4 Growth

US PMI readings eased across the board in December, signaling that the "recent economic growth spurt is losing momentum". PMI Manufacturing slipped from 52.2 to 51.8, while PMI Services fell more sharply from 54.1 to 52.9. PMI Composite dropped from 54.2 to 53.0.

S&P Global said the data remains consistent with annualized GDP growth of around 2.5% in the fourth quarter, but noted that momentum has now slowed for a second consecutive month. New sales growth weakened notably ahead of the holiday season,. The slowdown was broad-based, with services seeing near-stalling inflows of new work and manufacturing recording its first decline in factory orders in a year.

At the same time, cost pressures intensified. Firms reported a sharp pickup in inflation to the highest level since November 2022, feeding through to one of the steepest increases in selling prices in three years. Businesses also trimmed hiring and grew more cautious about the outlook, citing tariffs as a renewed source of price pressure that is now spilling beyond manufacturing into services, broadening affordability concerns.

NFP Market Reactions: Stocks Open Timidly, Gold Rallies After NFP Report But Other Markets are Stuck

The Non-Farm Payrolls finally released, relatively on time, and came at a small beat on expectations (64K vs 40K expected) while the Unemployment rate grew from 4.4% to 4.6%.

With downward revisions to the September data (-33K) and a -105K report for October, the labor picture is indeed softening as was highlighted by Fed's Williams throughout a few rounds of interviews yesterday.

But for now, things are not looking scary: The January 28th Meeting is priced only at 25% of a 25 bps cut and odds for cuts modestly rose for later meetings.

Market Reactions

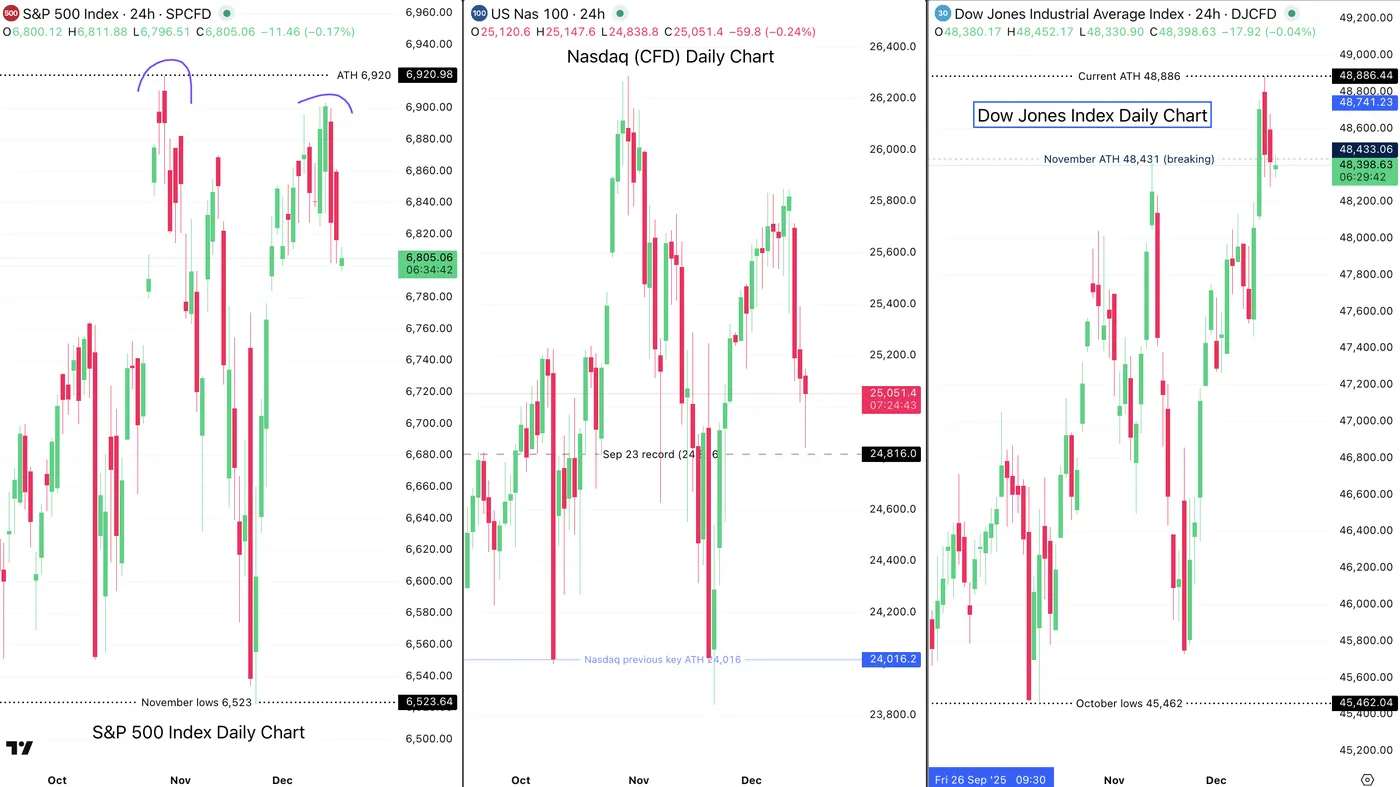

Market Outlook 30M Charts for S&P 500, Oil, 10-Year Bonds, Gold, Bitcoin and the USD. December 16 – Source: TradingView

Even without extra odds for rate cuts in 2026, the US Dollar is struggling quite a lot, breaking its past day support and going towards new lows.

The Dollar Index is testing the 98.00 handle, key for mid-term momentum.

You can also witness Oil falling back to its 2025 lows but attempting a shy rebound from key levels.

Metals on the other hand, are loving the NFP report and bouncing from their relative highs consolidation.

Gold is trading between $4,250 to $4,350 and attempting to break its small-resistance, Silver is roughly doing the same but Platinum is breaking higher this morning.

Stocks are opening timidly also, gapping lower at the open but not by a wide margin.

A detailed analysis for US Indexes is coming up soon in the morning session.

A shy open in Stocks. US Indexes Daily Chart Outlook – December 15, 2025 – Source: TradingView

Safe Trades!