Sample Category Title

Crypto Rebound Fades With a 40% Drop Possible

Market Overview

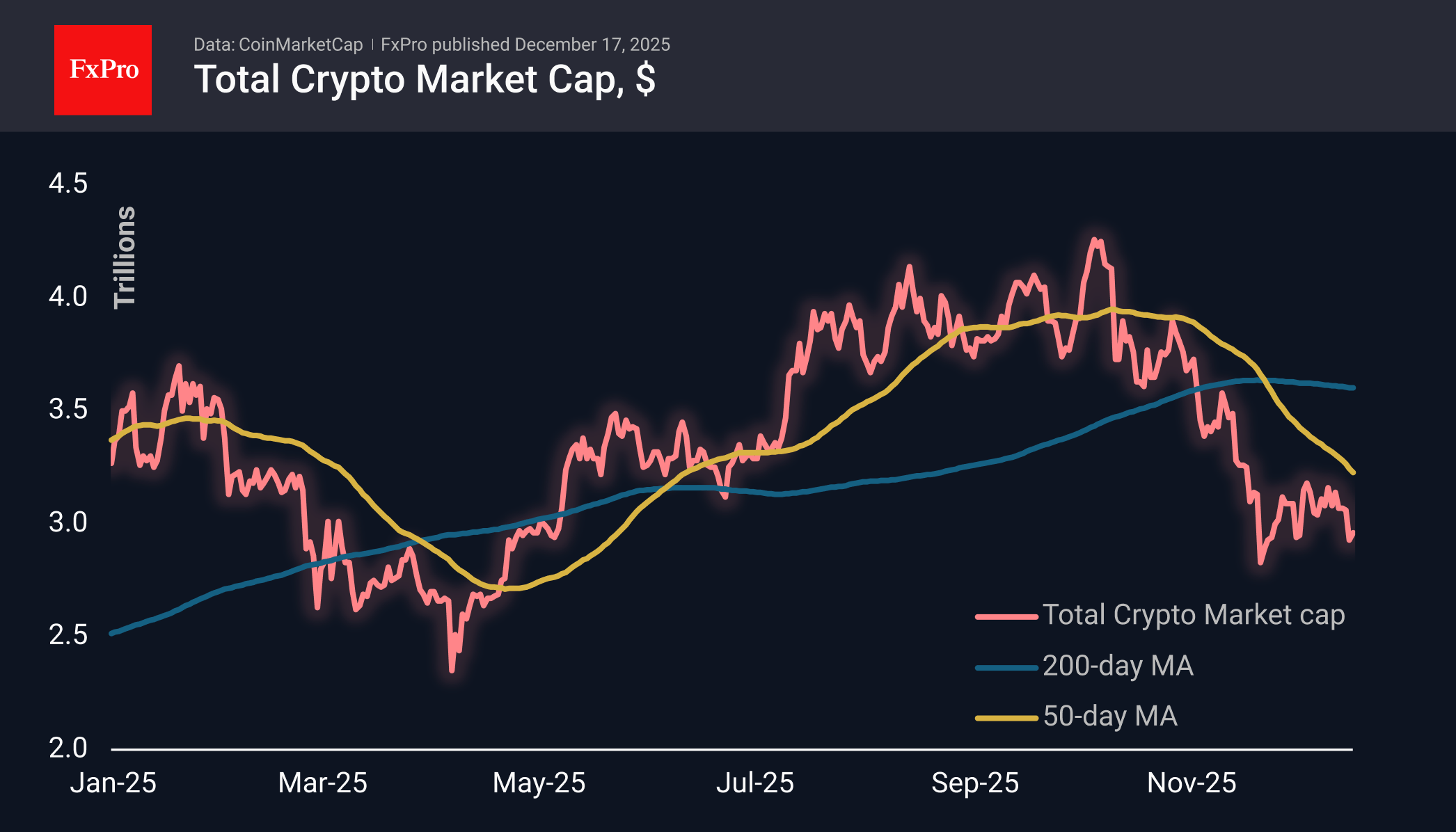

The crypto market capitalisation has changed little over the past 24 hours to $2.96T, remaining close to its late November lows. In the short term, the situation suggests that the rebound has run its course, and we should prepare for a new downward momentum, similar to what was observed in early October. If it falls below $2.75T, it will open a direct path to the $1.8T area, according to the Fibonacci extension pattern. Very close by, in the $1.8T–$1.9T area, is the area of local lows for 2024, which reinforces its importance.

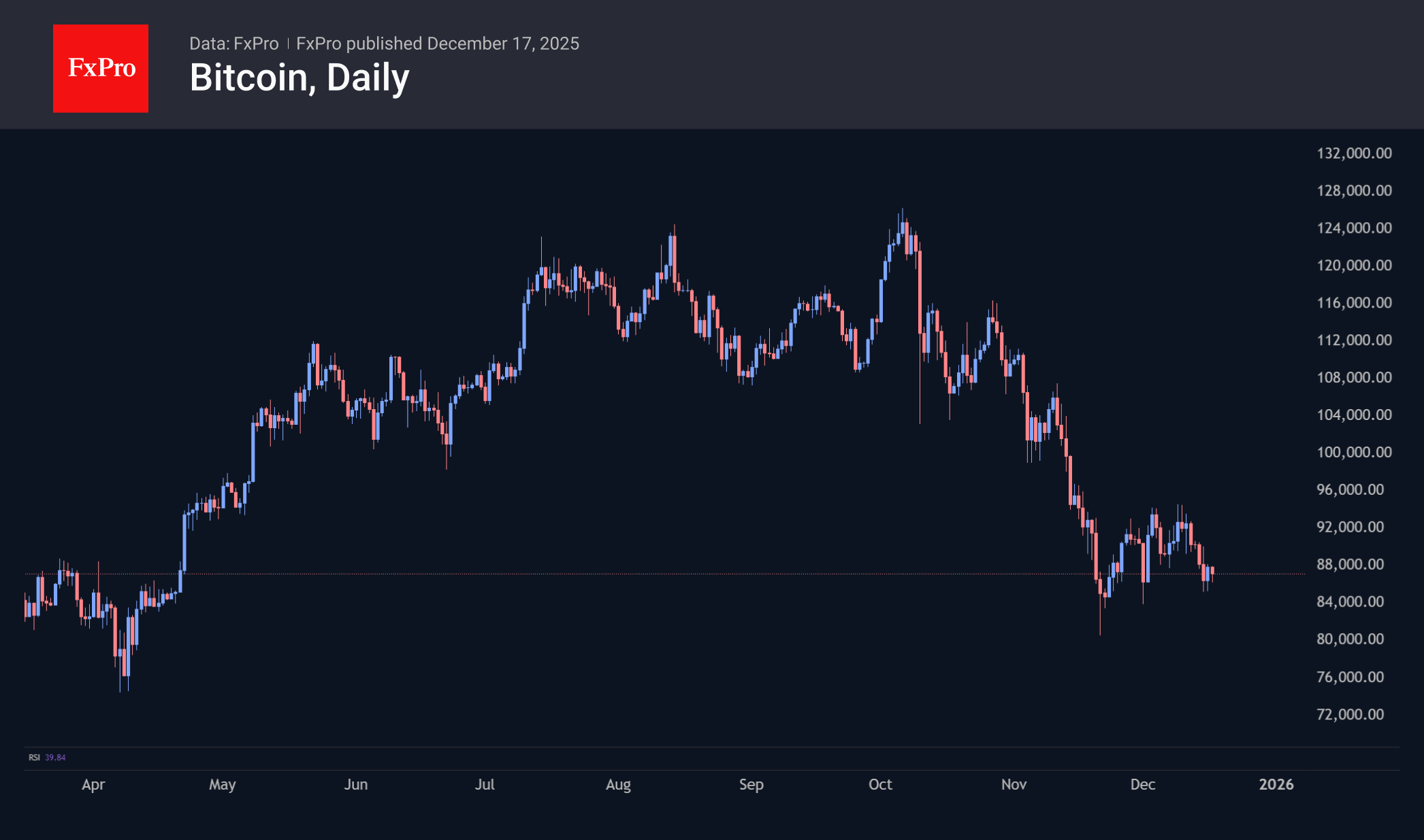

Bitcoin rose to $88K on Tuesday and then returned below $87K on Wednesday afternoon. As with the market as a whole, we are seeing impressive selling pressure with short pauses for a rebound. Bitcoin is still underperforming the stock market. However, this time we see it more as a sign of internal weakness in the crypto market and widespread profit-taking, rather than a bad omen for stocks, but it cannot be completely ruled out.''

News Background

Short-term Bitcoin holders are incurring losses, as the asset has been trading below their average entry price ($104,000) for over a month, according to CryptoQuant. At the same time, long-term holders of the first cryptocurrency continue to actively sell it. According to Glassnode, they have reduced their holdings by ~500,000 BTC since July.

Bitcoin could crash to $10,000 in 2026, warned Bloomberg Intelligence commodities strategist Mike McGlone. He suggested that the next economic recession will be triggered by the collapse of highly speculative digital assets with unlimited supply.

Analyst Peter Brandt predicted that Bitcoin could fall 80% from its record high to $25,240 due to a disruption in the asset’s growth structure.

At the same time, Bitwise and Grayscale predict that Bitcoin will reach new record highs in 2026, as the classic BTC cycle model is outdated.

Japanese financial conglomerate SBI Holdings and Web3 company Startale Group have signed a memorandum of understanding to jointly develop a stablecoin pegged to the yen. The partners plan to launch the asset in the first quarter of 2026.

The number of Britons owning cryptocurrency has fallen from 12% to 8% over the year. However, the average value of assets held by investors has increased.

Sunset Market Commentary

Markets

UK gilts outperform global peers today, dragging yields 4.6-6.5 bps lower in a bull steepening move. It started after this morning’s inflation numbers all but cemented a Bank of England rate cut (to 3.75% from 4%) tomorrow. All kinds of gauges missed expectations: headline dropped 0.2% m/m which lowered the 3.6% annual print to 3.2%, the slowest since March. The underlying series (ex. food and energy) mimicked headline dynamics with the 3.2% y/y here being a YtD low. Price growth in the services sector, a key worry for the hawks at the Bank of England due to its close ties with wages and the labour market, equally slowed to a YtD low of 4.4%. In October’s 5-4 close call for holding rates steady, governor Bailey casted the swing vote. He wanted proof that disinflation would resume after inflation had been rising from 1.7% in September 24 to 3.8% by September 2025. That happened in both October and November, readying Bailey for a position switch. The implied market probability for a rate cut rose from 91% to near-100%. Room for further policy normalization after Thursday is limited though given still too high inflation and yesterday’s PMI’s suggesting the economy holds up relatively well. There’s maybe one additional cut on the horizon. Sterling erases all of yesterday’s gains against the euro, lifting EUR/GBP back towards the 0.88 barrier. The YtD high of EUR/GBP 0.8865 remains nearby and serves as the first technical reference to watch.

FI in the US and Europe shows modest bear steepening. US rates add 1.3-2.3 bps, European swap yields up to 2.4 bps. The 30-yr swap tenor yesterday suffered from fear of heights after nearing the 2023 multiyear high but is ready to give it another shot. Except for a minor rise in oil prices we saw few reasons for long term yields to rise. It is perhaps testament to the strength of the underlying forces (eg. risk premia) driving the move. Real yields in Germany – which capture amongst others risk premia – just rose to a new 14-year high. Fed governor Waller hit the wires only to spread out his dovish wings: the labour market is very soft, inflation won’t reaccelerate and rates are still 50-100 bps above neutral, allowing for steady policy normalization (or is it easing?). Brent oil prices gain a tad to <$60/b on the news of the US ordering a blockade of sanctioned Venezuelan tankers and the threat to impose additional sanctions on Russia’s energy sector if the country would reject a peace agreement with Ukraine. The black gold remains mired near the lowest levels in around four years. Economic data today was limited to the German IFO (87.6 from 88) coming in to the low side of expectations, mainly as the expectations component disappointed. It wasn’t a major surprise after yesterday’s PMIs. Attention now turns to the US inflation numbers and the ECB policy meeting scheduled for tomorrow. FX markets ex GBP trade muted with some JPY underperformance ahead of Friday’s BoJ meeting. EUR/USD steadies around 1.173.

News & Views

The Confederation of British Industry’s monthly industrial trends survey showed the manufacturing output decline easing in the three months to December (weighted balance of -21% from -30% in the quarter to November). 15 out of 17 sub-sectors showed decreasing output with the fall being driven by chemicals, metal products and mechanical engineering. Activity was clearly held back by uncertainty ahead of the Budget. Significant headwinds remain nonetheless, with demand still soft, high energy, labour and regulatory costs squeezing margins, and uncertainty around key policies and global conditions continuing to weigh on confidence. Total (-32% from -37%) and export order books (-27% from -31%) improved relative to last month, though remain historically weak. Long run averages of both series are respectively -14% and -19%. Stock adequacy eased (+8% from +16%) but manufacturers report that inventories of finished goods remain more than adequate. Expectations for selling price inflation picked up (+19% from +7%), with the survey balance rising above the long-run average (+8%).

The Swedish Origo group published its quarterly inflation expectations survey conducted on behalf of the Riksbank. Interviewees expect annual CPIF (core) inflation at 1.6% in the year-ahead, at 2% in the twelve months thereafter and at 2.1% in year 5. In the September survey, short term inflation expectations were higher, at 2.1% for both year 1 and 2. Simultaneously, the survey paints a brighter economic picture with growth now expected at 2.3%-2.3%-2.2% for year 1, 2 and 5, up from 1.8%-2.2%-2.1% in September. The Riksbank’s policy rate path is still seen very gradually upward sloping from the current 1.75% towards 2.25%.

Fed’s Waller backs steady, not dramatic easing

Fed Governor Christopher Waller said today that policy remains meaningfully restrictive, estimating rates are still around 50 to 100 basis points above neutral. Despite that gap, Waller emphasized there is no rush to get down" on interest rates, arguing the Fed can move rates down to neutral "steadily" as conditions evolve.

Waller said the labor market continues to "soften", but not in a dramatic or disorderly way. That backdrop supports a measured approach to further rate cuts, with no need for aggressive action. The Fed can proceed at a "moderate pace". "I don't think we have to do anything dramatic," he added.

He also noted that the string of rate cuts delivered in the final months of 2025 has already helped offset some risks to hiring. Looking ahead, Waller said prospects for a stronger economy next year—driven by fiscal policy changes and reduced uncertainty—should further support labor demand. For him, the employment side of the Fed’s mandate remains the priority, while inflation is expected to continue easing.

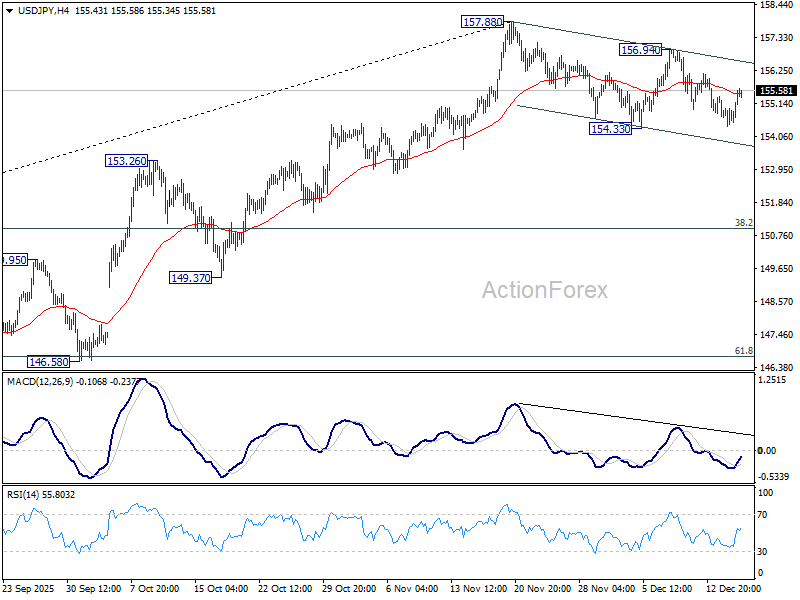

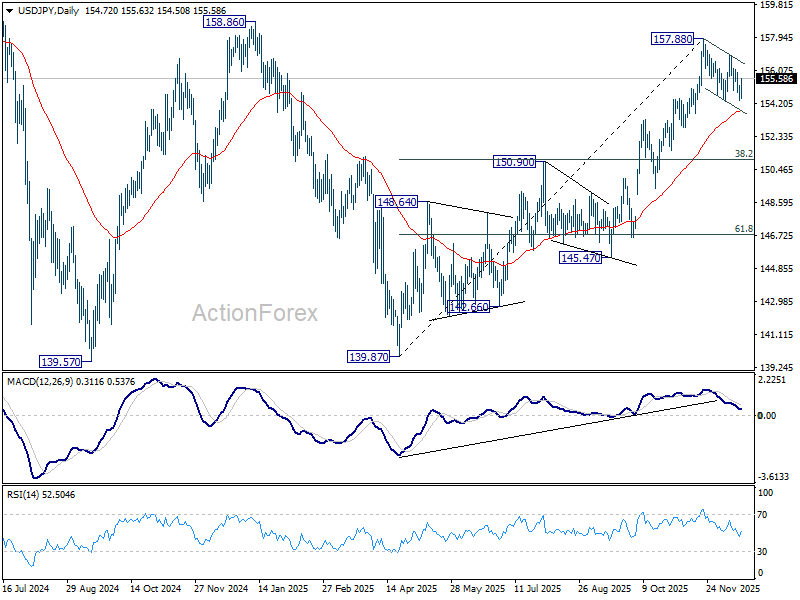

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.30; (P) 154.82; (R1) 155.24; More...

USD/JPY recovered ahead of 154.33 support and intraday bias stays neutral. Overall outlook is unchanged that corrective pattern from 157.88 is still extending. On the downside, break of 154.33 will target 55 D EMA (now at 153.66) and possibly below. On the upside, above 156.94 will bring retest of 157.88. Firm break there will resume whole rally from 139.87 to 158.85 key structural resistance.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

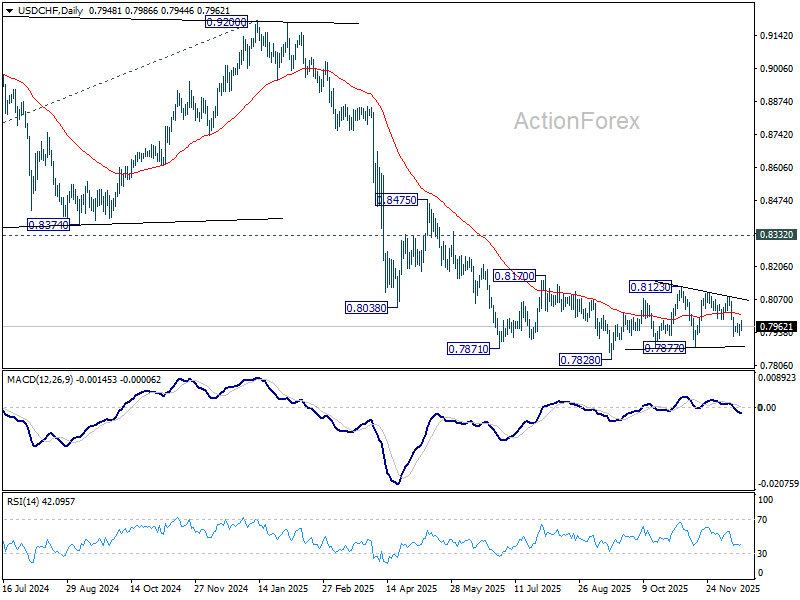

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7928; (P) 0.7950; (R1) 0.7973; More…

Intraday bias in USD/CHF stays neutral as sideway trading continues. Overall, corrective pattern from 0.7828 is still extending. On the upside, break of 0.7990 support turned resistance will bring stronger rebound towards 0.8084. On the downside, below 0.7923 will target 0.7877 support.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

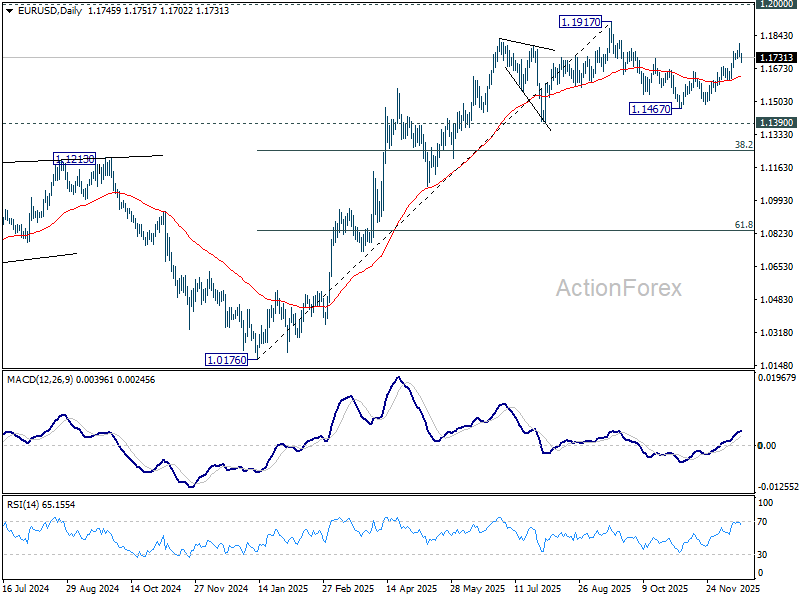

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1723; (P) 1.1737; (R1) 1.1753; More….

EUR/USD is still extending consolidations below 1.1803 and intraday bias stays neutral. On the upside break of 1.1803 will resume the rally from 1.1467 to retest 1.1917 high. Decisive break there will resume larger up trend. ON the downside, however, firm break of 55 D EMA (now at 1.1633) will turn bias back to the downside for 1.1467 support, to extend the corrective pattern form 1.19717 with another falling leg.

In the bigger picture, as long as 55 W EMA (now at 1.1373) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

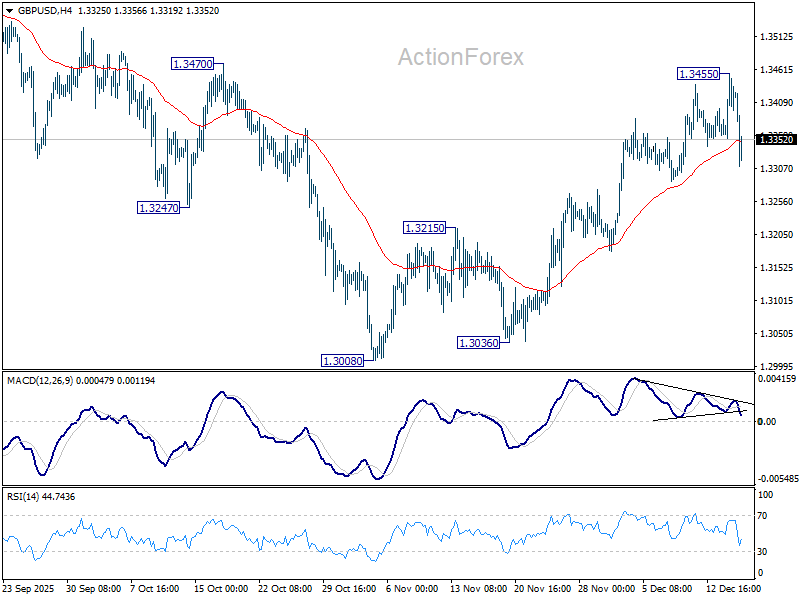

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3366; (P) 1.3411; (R1) 1.3467; More...

GBP/USD is staying in consolidations below 1.3455 and intraday bias remains neutral. On the upside, above 1.3455 will resume the rebound from 1.3008. Firm break of 1.3470 resistance will pave the way to retest 1.3787 high. However, sustained break of 55 D EMA (now at 1.3293) will argue that the rebound has completed. Deeper fall would be seen back to 1.3008 support to resume the whole corrective pattern from 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

Sterling Avoids Heavy Selling So Far, Silver Power Continues

Sterling continues to underperform today, though losses remain contained. The lack of aggressive selling suggests markets are already well positioned for near-term policy easing and are now grappling with uncertainty further along the curve rather than reacting to fresh surprises.

This week’s string of weaker UK employment data has erased any remaining doubt over a BoE rate cut tomorrow. The decision has become a formality, shifting attention to guidance and the sequencing of subsequent moves.

There is no consensus on what follows. Some analysts caution that November’s softer inflation reading was influenced by temporary discounting effects tied to early Black Friday promotions. If so, inflation could firm again in coming months.

Still, even a cut in February or March would not represent a shift in policy tempo. The BoE has clearly signaled a preference for a measured approach, and with inflation still far above target, there is little scope for a faster pace than one cut per quarter.

From a trading standpoint, the exact timing of the next cut is unlikely to be a major market driver. February may be marginally favored due to the release of new forecasts, but the broader message of gradual easing remains intact regardless.

The larger uncertainty lies in the terminal rate. How far policy ultimately moves into neutral territory is still an open question, and one that markets are in no position to answer with confidence given lingering inflation risks.

In FX markets today, Sterling is still the weakest performer, followed by Yen and Loonie. Dollar leads the pack, with Swiss Franc and Kiwi also firmer. Euro and Aussie sit in the middle.

Oil prices, meanwhile, are staging a notable rebound after hitting multi-year lows earlier this week. The move follows US President Donald Trump’s decision to label Venezuela’s government a terrorist organization and impose a full blockade on sanctioned oil tankers. That move injects fresh supply risk, while optimism around a Ukraine–Russia peace deal has yet to deliver concrete follow-through.

In Europe, at the time of writing, FTSE is up 1.49%. DAX is down -0.06%. CAC is down -0.27%. UK 10-year yield is down -0.056 at 4.467. Germany 10-year yield is up 0.013 at 2.859. Earlier in Asia, Nikkei rose 0.26%. Hong Kong HSI rose 0.92%. China Shanghai SSE rose 1.19%. Singapore Strait Times fell -0.09%. Japan 10-year JGB yield rose 0.029 to 1.985.

Silver outpaces sluggish Gold, pushes towards 70 as record run extends

Silver’s uptrend extended again today, pushing to fresh record highs above the 66 mark and reinforcing its status as the standout precious metal. Momentum remains firmly on the upside, with prospects growing for a move toward 70 psychological level and potentially beyond. By contrast, Gold continues to struggle near its recent highs, with momentum turning sluggish and risks skewed toward a near-term bearish extension of its medium-term corrective pattern.

One key advantage for Silver lies in its structural fundamentals. As of late 2025, the Silver market is in its fifth consecutive year of supply deficit, with mine production and recycling consistently falling short of global demand from both industry and investors. This persistent imbalance has tightened the market in a way gold has not experienced.

Silver has also benefited from a policy-driven tailwind. In November, the US officially added Silver to its Critical Minerals List for the first time, reflecting its essential role in modern technology and national security. Demand from solar energy, electric vehicles, defense, and high-tech manufacturing continues to accelerate, while supply growth remains constrained.

The US currently imports more than 70% of its Silver needs, highlighting a growing vulnerability as global demand outpaces mine supply. That backdrop strengthens the case for sustained investment demand and reinforces Silver’s appeal relative to Gold.

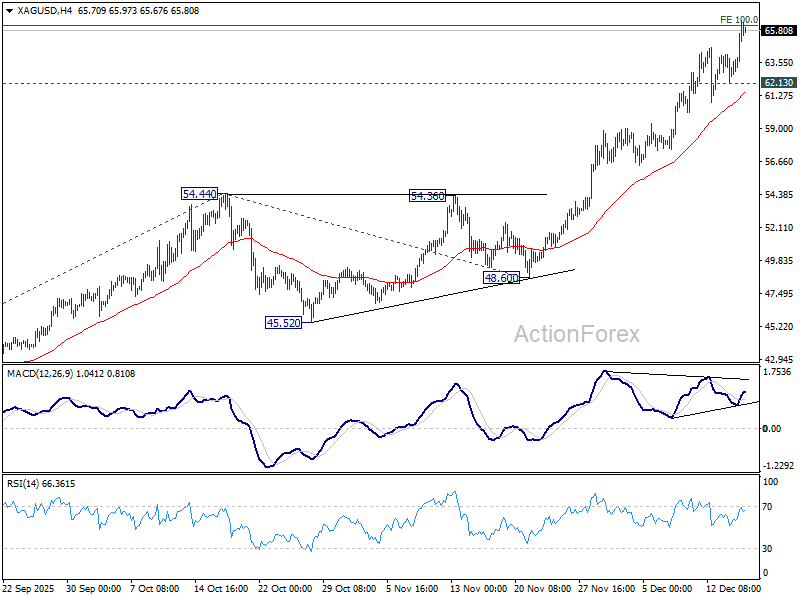

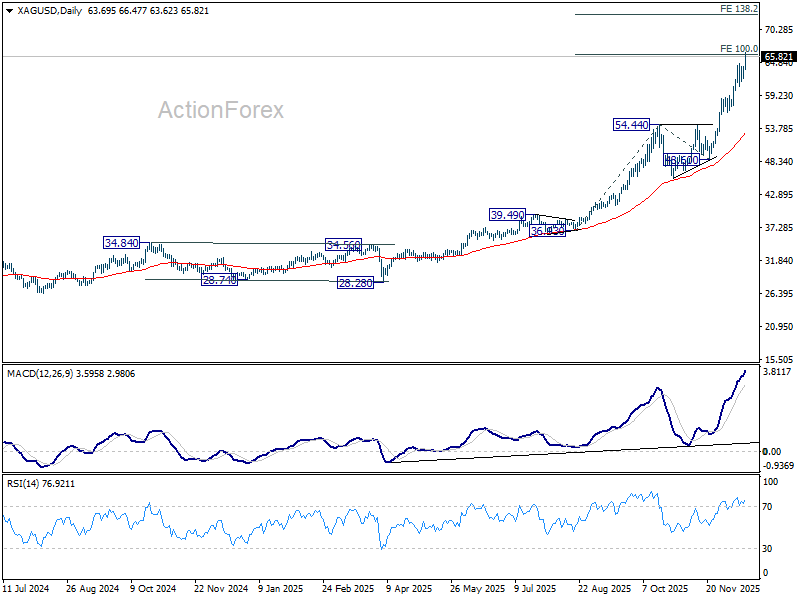

Technically, Silver has already met 100% projection of 36.93 to 54.44 from 48.60 at 66.11 and there is no clear sign of topping yet. Near term outlook will stay bullish as long as 62.13 support holds. The focus is on whether the next up leg of pull 4H MACD above its falling trend line to confirm revival of upside momentum. Sustained trading above 66.11 will pave the way 70 psychological level or even further to to 138.2% projection at 72.98.

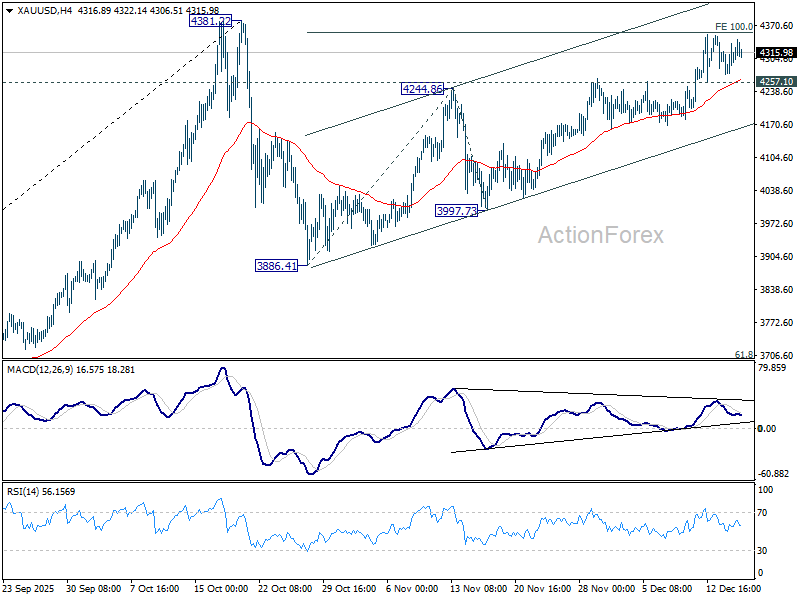

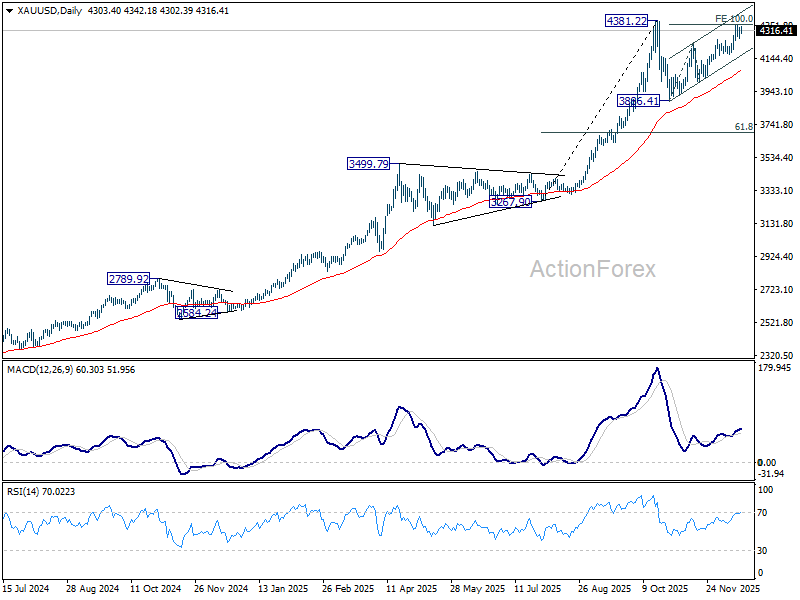

Meanwhile, Gold's momentum as turned sluggish ahead of 4381.22 high. Break of 4257.10 support will turn bias to the downside for deeper pullback. Further break of the near term rising channel will argue that corrective pattern from 4381.22 has already started the third leg down. Nevertheless, decisive break of 4381.22 will confirm long term up trend resumption.

Eurozone CPI finalized at 2.1% in November, services remain main inflation driver

Eurozone inflation was finalized unchanged in November, confirming a stable price environment heading into year-end. Headline CPI held at 2.1% yoy, the same as in October. Core CPI excluding energy, food, alcohol, and tobacco was also unchanged at 2.4%.

Services continued to dominate inflation dynamics, contributing 1.58 percentage points to the annual rate. Food, alcohol, and tobacco added 0.46 pp, while non-energy industrial goods contributed a modest 0.14 pp. Energy prices continued to exert a slight drag, subtracting -0.04 pp from the headline rate.

Across the wider EU, CPI was finalized at 2.4% yoy. Inflation was lowest in Cyprus (0.1%), France (0.8%), and Italy (1.1), while Romania (8.6%), Estonia (4.7%), and Croatia (4.3%) recorded the highest rates. Compared with October, inflation eased in twelve member states, was unchanged in five, and rose in ten.

German Ifo sentiment falls to 87.7, ends year on downbeat note

Germany’s Ifo survey delivered weaker-than-expected readings in December, confirming that business confidence remains under strain. The headline Business Climate index fell to 87.7 from 88.0, missing forecasts of 88.5. Current Assessment remained unchanged at a subdued 85.6. Expectations also softened to 89.7, pointing to a more cautious outlook.

Sector-level details showed little relief. Manufacturing confidence deteriorated further from -13.8 to -14.8. Services sentiment turned negative again fro 0.6 to -2.1. Trade conditions weakened from -22.6 to -24.6. Construction remained stuck at deeply negative levels of -15.2.

According to Ifo, the year is ending "without any sense of optimism". The combination of weak current conditions and declining expectations suggests Germany is struggling to build momentum heading into the new year.

UK CPI undershoots at 3.2% as disinflation broadens in November

UK inflation eased more than expected in November, reinforcing signs that price pressures are moderating. Headline CPI slowed from 3.6% yoy to 3.2%, undershooting expectations of 3.5% and marking a second consecutive monthly decline. On a month-on-month basis, CPI fell -0.2% mom, adding to the disinflationary signal.

Underlying inflation also cooled. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 3.4% yoy to 3.2%, below forecasts of 3.4%, suggesting easing price pressures beyond volatile components.

The moderation was driven mainly by goods, where inflation eased from 2.6% yoy to 2.1% Services inflation edged slightly lower from 4.5% to 4.4%.

Japan posts first trade surplus in five months, US-bound shipments rebound

Japan’s trade data for November delivered a positive surprise, with exports rising 6.1% yoy to JPY 9.72 trillion, beating expectations of 4.8% yoy, and marking the third consecutive month of growth. The strength helped Japan record a JPY 322.2 billion trade surplus, the first in five months.

Exports to the US were a key driver, climbing 8.8% yoy. Auto shipments to the US rose 1.5%, marking the first increase since March and suggesting the drag from higher US tariffs is beginning to ease.

By contrast, exports to mainland China fell -2.4% yoy, weighed down by a sharp -5.9% decline in foodstuff shipments. That weakness came against a backdrop of renewed political tension, after Prime Minister Sanae Takaichi warned that a Chinese attempt to seize Taiwan could prompt Japanese military intervention, followed by Beijing restricting imports of Japanese seafood. Offsetting some of that drag, exports to Hong Kong surged 11.4%.

On the import side, growth was more subdued. Imports rose just 1.3% yoy to JPY 9.39 trillion, undershooting expectations of 2.5%.

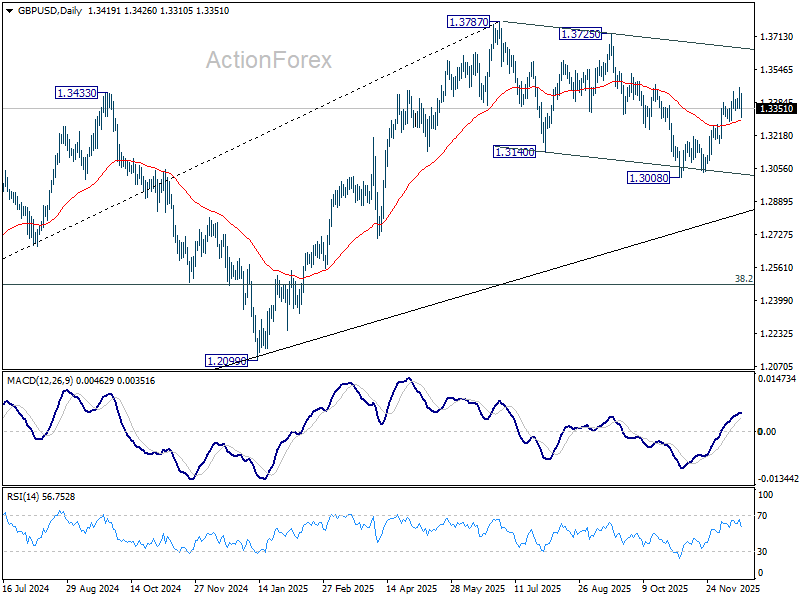

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3366; (P) 1.3411; (R1) 1.3467; More...

GBP/USD is staying in consolidations below 1.3455 and intraday bias remains neutral. On the upside, above 1.3455 will resume the rebound from 1.3008. Firm break of 1.3470 resistance will pave the way to retest 1.3787 high. However, sustained break of 55 D EMA (now at 1.3293) will argue that the rebound has completed. Deeper fall would be seen back to 1.3008 support to resume the whole corrective pattern from 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

XAG/USD: Silver Surges to New Record High, Psychological $70 Barrier in Sight

Silver advanced over 4% and hit new record high ($66.51) on Wednesday, as demand for precious metals gained impetus after US data pointed to further softening in the US labor market that revived expectations for more dovish Fed’s stance on monetary policy.

Fresh gains broke through two round-figure barriers ($65 and $66) and signaled continuation of larger after a three-day consolidation.

Bulls eye targets at $67.23 and $69.36 (Fibo projections 238.2% & 261.8% respectively) with psychological $70 barrier coming in focus.

Meanwhile, overbought daily studies suggest that bulls may take a breather for consolidation / limited correction and position for fresh push higher as all key drivers (geopolitical / monetary policy / industrial demand) remain firmly in play

Dips should be ideally contained at $64.50/00 zone to keep bullish structure intact.

Res: 66.00; 66.51; 67.23; 68.00.

Sup: 64.64; 64.30; 64.00; 63.75.

Silver outpaces sluggish Gold, pushes towards 70 as record run extends

Silver’s uptrend extended again today, pushing to fresh record highs above the 66 mark and reinforcing its status as the standout precious metal. Momentum remains firmly on the upside, with prospects growing for a move toward 70 psychological level and potentially beyond. By contrast, Gold continues to struggle near its recent highs, with momentum turning sluggish and risks skewed toward a near-term bearish extension of its medium-term corrective pattern.

One key advantage for Silver lies in its structural fundamentals. As of late 2025, the Silver market is in its fifth consecutive year of supply deficit, with mine production and recycling consistently falling short of global demand from both industry and investors. This persistent imbalance has tightened the market in a way gold has not experienced.

Silver has also benefited from a policy-driven tailwind. In November, the US officially added Silver to its Critical Minerals List for the first time, reflecting its essential role in modern technology and national security. Demand from solar energy, electric vehicles, defense, and high-tech manufacturing continues to accelerate, while supply growth remains constrained.

The US currently imports more than 70% of its Silver needs, highlighting a growing vulnerability as global demand outpaces mine supply. That backdrop strengthens the case for sustained investment demand and reinforces Silver’s appeal relative to Gold.

Technically, Silver has already met 100% projection of 36.93 to 54.44 from 48.60 at 66.11 and there is no clear sign of topping yet. Near term outlook will stay bullish as long as 62.13 support holds. The focus is on whether the next up leg of pull 4H MACD above its falling trend line to confirm revival of upside momentum. Sustained trading above 66.11 will pave the way 70 psychological level or even further to to 138.2% projection at 72.98.

Meanwhile, Gold's momentum as turned sluggish ahead of 4381.22 high. Break of 4257.10 support will turn bias to the downside for deeper pullback. Further break of the near term rising channel will argue that corrective pattern from 4381.22 has already started the third leg down. Nevertheless, decisive break of 4381.22 will confirm long term up trend resumption.