Sample Category Title

Jury Still Out on Fed’s Next Plans

Markets

The jury is still out on the Fed’s next plans after payrolls failed to tilt the balance one way or the other. Markets initially erred on the dovish side, but the case wasn’t compelling enough to fully endorse Q1 rate cut bets (currently 25% probability for January; 55% for March). The US 2-yr yield tested the end of November low at 3.45% but a break lower didn’t occur. Intraday rebound action higher pulled EUR/USD back from first 1.18+ levels since mid-September to close virtually unchanged at 1.1750. The US yield curve eventually bull flattened with yields ending 1.4 bps (2-yr) to 3.3 bps (30-yr) lower. Calm returned on US stock markets with key indices closing 0.6% lower (Dow) to 0.25% higher (Nasdaq).

Better November payrolls (+64k) failed to make up for a weak October report (-105k; mainly DOGE-impact on government). The US unemployment rate increased from 4.4% in September (BLS unable to conduct October household survey) to a 4-yr high of 4.6% in November (vs 4.5% consensus). Since June (4.1%) it has been one-way traffic higher with alarm bells ringing. Filling the blank October unemployment rate number (eg 4.5%) brings you dangerously close to the 0.50% threshold of the SAHM rule. When the 3-month moving average of the unemployment rate exceeds the lowest 3-month moving average of the past year (currently 4.06%) by that amount, the rule indicates a high likelihood of being in the early stage of a recession. Last year, it prompted the Fed into a bigger-than-usual 50 bps rate cut at the start of its cutting cycle. Risks of a breach at the next payrolls release early January are high both because of current elevated levels and because the lowest 3-month moving average of the past year will rise to 4.1% with the Dec2024 point dropping out of the equation. We stick with the view that markets currently underestimate the probability of a continuation of the Fed’s normalization cycle early next year. October US retail sales and December PMI surveys supported the intraday market rebound. The former because of strength, the latter because of prices spiking higher. Sales in the retail control group increased by 0.8% M/M (vs 0.4% consensus). The composite PMI set a 6-month low (53 from 54.2) with details showing a second consecutive month of waning momentum. Signs of weakness were broad-based, with a near stalling of inflows of work into the vast services economy accompanied by the first fall in factory orders for a year. A key concern is rising costs, with inflation jumping sharply to its highest since November 2022, which fed through to one of the steepest increases in selling charges for the past three years.

Significantly lower November UK CPI numbers cement the case for more BoE rate cuts and push EUR/GBP from 0.8750 to 0.8780 in a first reaction this morning.

News & Views

The National Bank of Hungary yesterday kept its policy rate unchanged at 6.5%. However, its assessment clearly turned less hawkish, reopening the debate on potential rate cuts next year. The central bank took notice of recent declines both in headline (3.8%) and core (4.1%) inflation in November. This disinflation process was supported by a decrease in global commodity and food prices and the pass-through of a stronger forint into purchase prices. The MNB also saw more moderate monthly repricings in recent months compared to the first half of the year. Corporate inflation expectations were subdued in November, but consumer inflation expectations were seen as remaining stagnant. In its new forecasts, inflation was downwardly revised both for this year (4.4% from 4.6%) and next year (3.2% from 3.8%). Inflation is expected to average 3.3% in 2027, but is seen reaching the 3% level in H2 of that year. The growth path was slightly downwardly revised to 0.5% this year, 2.4% next year and 3.1% in 2027. MNB still sees positive real rates as necessary. Maintaining tight monetary conditions is warranted, but the MNB shifts to a data-dependent approach. The 2-y HUF swap rate dropped 10 bps to 6.15%. The forint declined to EUR/HUF 386.

The Czech government yesterday approved a plan to reduce electricity bills both for companies and households. From January on, some levies will be transferred to the government. Industry minister Havlicek expects the shift to lower electricity prices by 10%. The move is expected to come at a cost for the budget of CZK17bn, but it is expected to put further downward pressure on inflation. The Czech 2-y swap rate eased 4 bps yesterday. The koruna hardly reacted with EUR/CZK closing the day near 24.32.

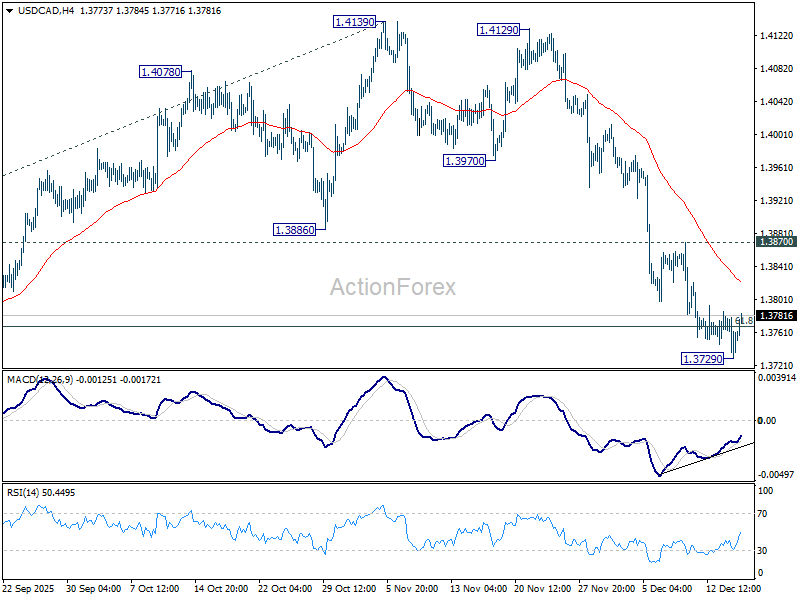

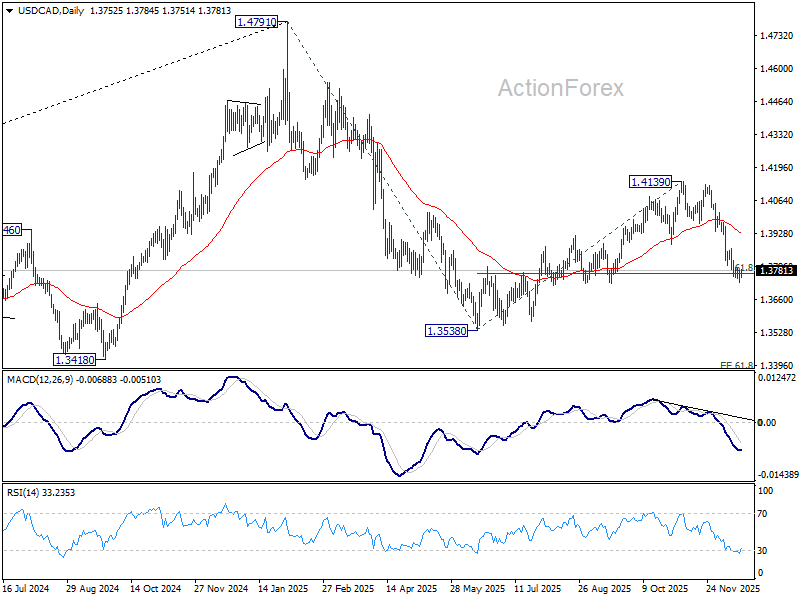

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3729; (P) 1.3755; (R1) 1.3779; More...

USD/CAD recovered after brief dip to 1.3729 and intraday bias is turned neutral. On the downside, Sustained trading below 61.8% retracement of 1.3538 to 1.4139 at 1.3768 will argue that whole fall form 1.4791 might be ready to resume. Retest of 1.3538 low should be seen next. However, firm break of 1.3870 resistance will confirms short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it's just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.

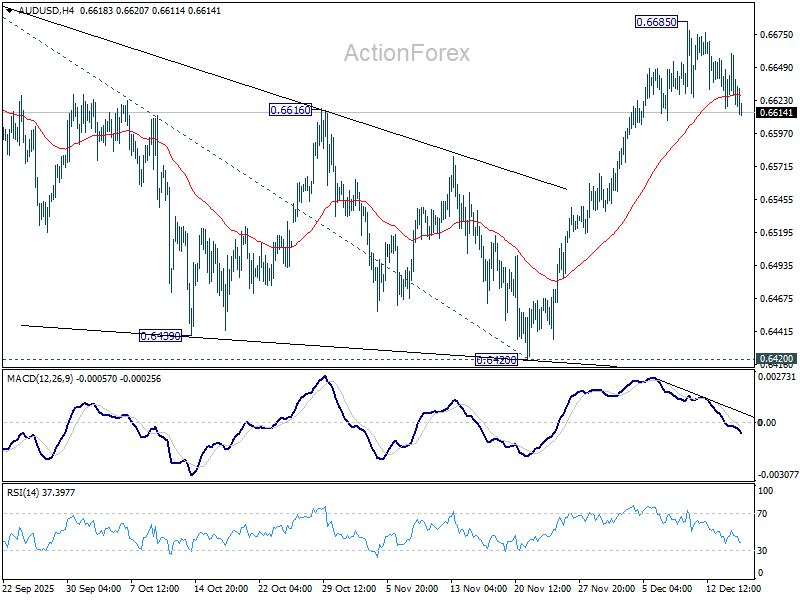

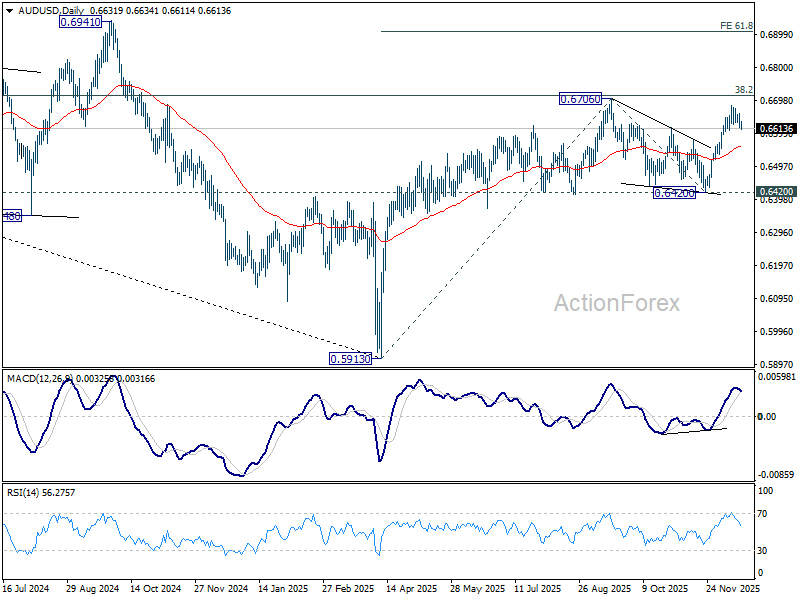

AUD/USD Daily Report

Daily Pivots: (S1) 0.6613; (P) 0.6637; (R1) 0.6656; More...

Intraday bias in AUD/USD remains neutral first as consolidations from 0.6685 extends. On the upside, firm break of 0.6706 will confirm resumption of whole rise from 0.5913. Next target is 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. However, break of 55 D EMA (now at 0.6560) will extend the corrective pattern from 0.6706 with another falling leg, and target 0.6420 support.

In the bigger picture, the break of multi-year falling trend line resistance suggests that rise from 0.5913 is possibly reversing whole down trend from 08006 (2021 high). Decisive break of 38.2% retracement of 0.8006 to 0.5913 at 0.6713 will solidify this case, and bring further rally to 61.8% retracement at 0.7206. On the downside, however, firm break of 0.6420 support will suggest rejection by 0.6713 and retain medium term bearishness.

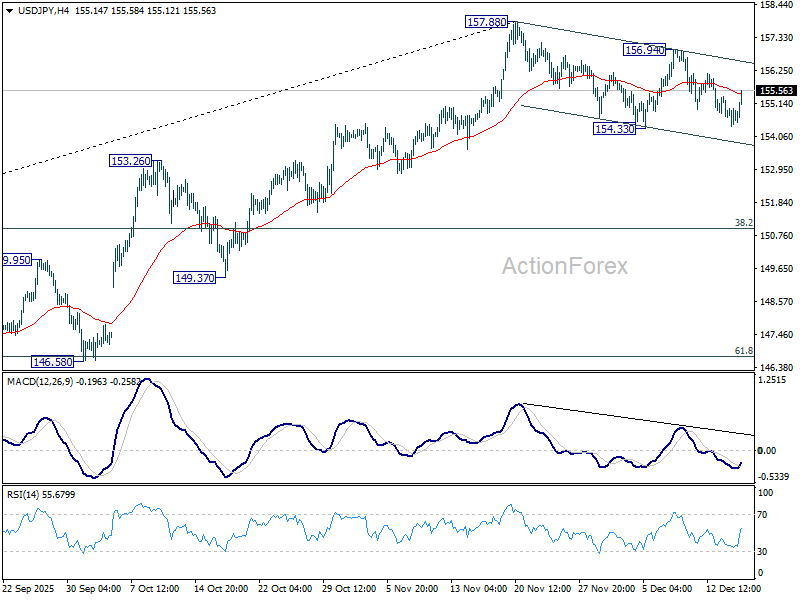

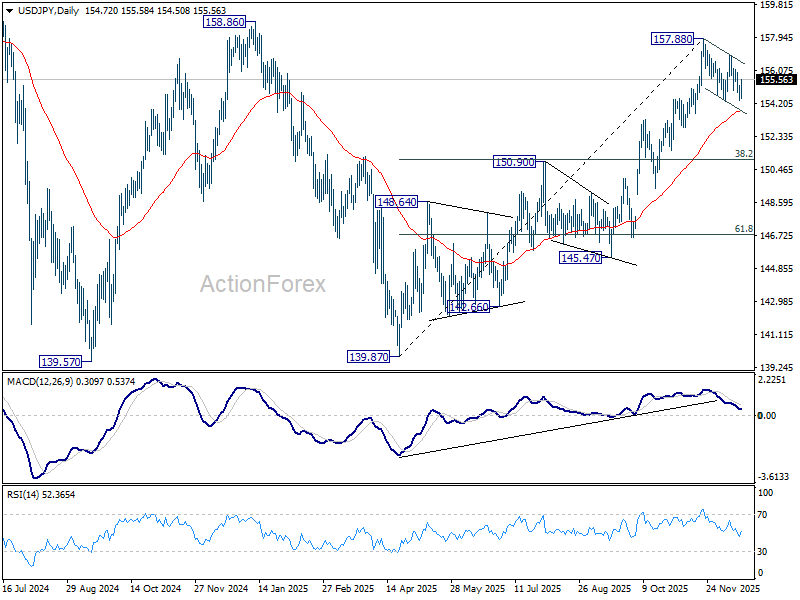

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.30; (P) 154.82; (R1) 155.24; More...

Intraday bias in USD/JPY stays neutral for the moment as corrective pattern from 157.88 is extending. On the downside, break of 154.33 will target 55 D EMA (now at 153.66) and possibly below. On the upside, above 156.94 will bring retest of 157.88. Firm break there will resume whole rally from 139.87 to 158.85 key structural resistance.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

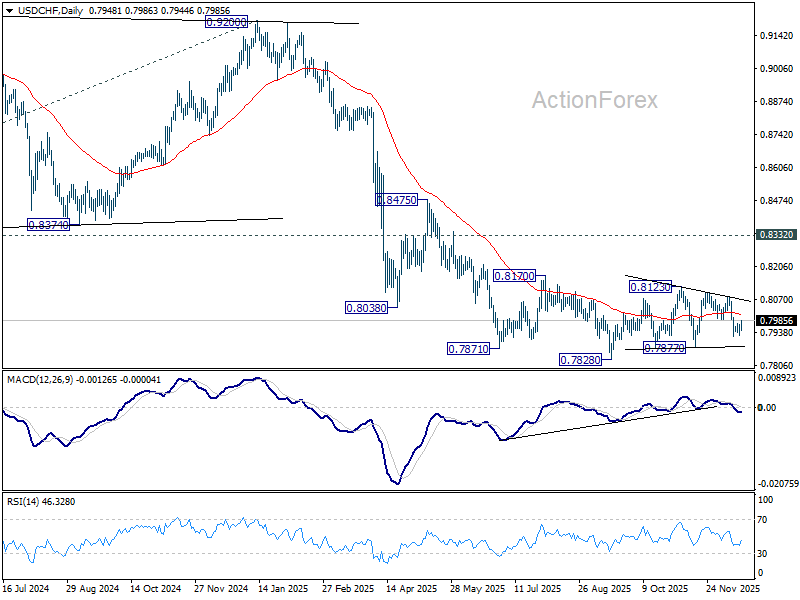

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7928; (P) 0.7950; (R1) 0.7973; More…

Intraday bias in USD/CHF stays neutral at this point. Overall, corrective pattern from 0.7828 is still extending. On the upside, break of 0.7990 support turned resistance will bring stronger rebound towards 0.8084. On the downside, below 0.7923 will target 0.7877 support.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

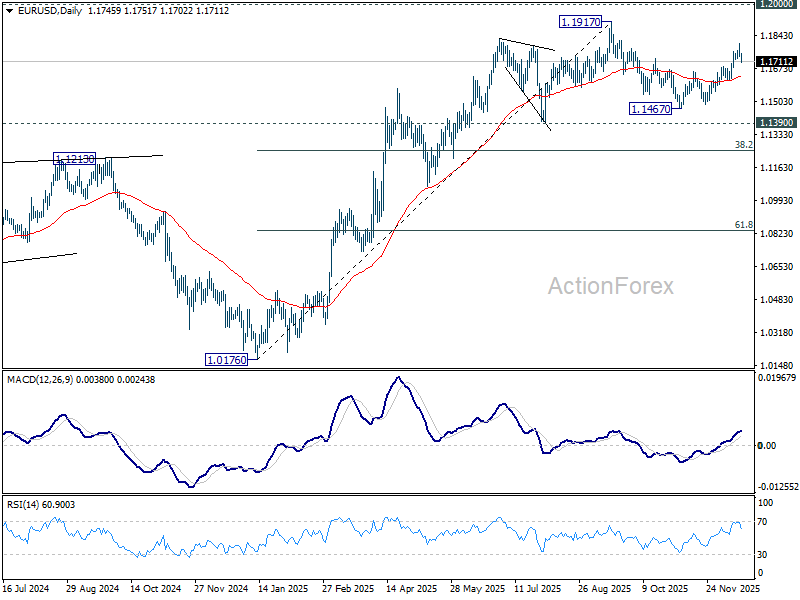

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1723; (P) 1.1737; (R1) 1.1753; More….

Intraday bias in EUR/USD is turned neutral again with current retreat and some consolidations would be seen. On the upside, above 1.1803 will resume the rally from 1.1467 to retest 1.1917 high. Decisive break there will resume larger up trend. ON the downside, however, firm break of 55 D EMA (now at 1.1633) will turn bias back to the downside for 1.1467 support, to extend the corrective pattern form 1.19717 with another falling leg.

In the bigger picture, as long as 55 W EMA (now at 1.1373) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

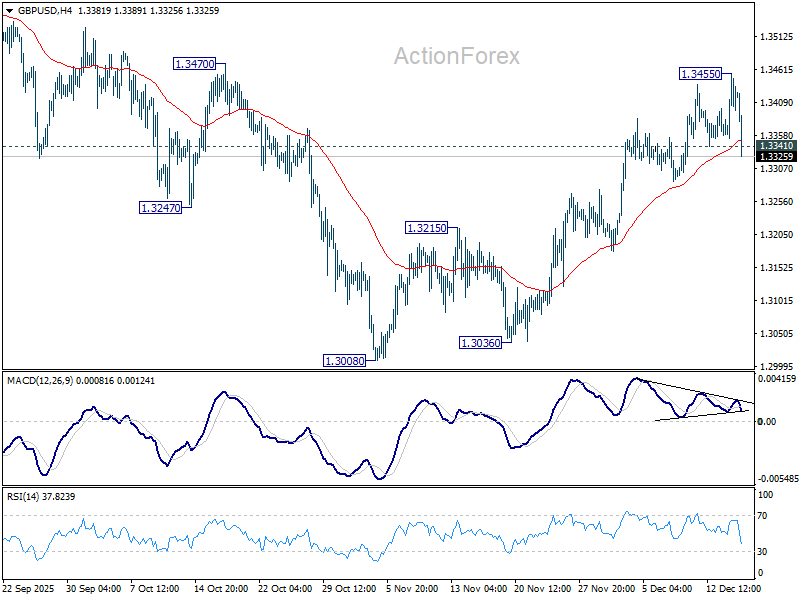

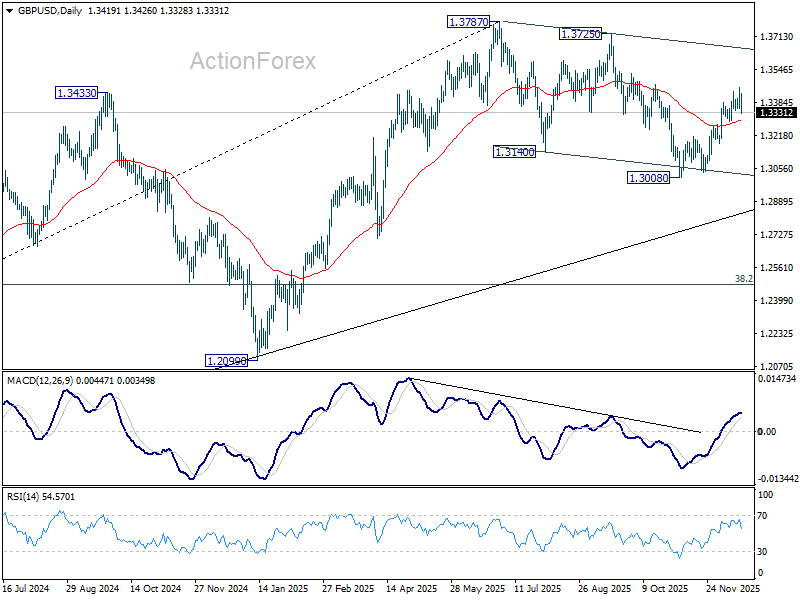

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3366; (P) 1.3411; (R1) 1.3467; More...

Intraday bias in GBP/USD is turned neutral again with current retreat. On the upside, above 1.3455 will resume the rebound from 1.3008. Firm break of 1.3470 resistance will pave the way to retest 1.3787 high. However, sustained break of 55 D EMA (now at 1.3293) will argue that the rebound has completed. Deeper fall would be seen back to 1.3008 support to resume the whole corrective pattern from 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

Sterling Slips as Faster UK Disinflation Firms Up BoE Cut Case

Sterling weakened further today after UK inflation data surprised further to the downside, reinforcing expectations that price pressures are easing faster than previously thought. The softer CPI print extended losses in Sterling following a weak run of domestic data this week.

After inflation peaked at a lower-than-expected 3.8% earlier in the year, disinflation trend now appears to be accelerating. November’s data suggests that inflation is converging toward target more quickly. Alongside weaker UK labor market figures released yesterday, this week’s data all but seals the case for a BoE rate cut tomorrow. Market focus has already shifted beyond the decision itself toward how long the easing cycle could extend into next year.

On current information, policy easing is set to continue next year. The debate is not really about whether the BoE will cut again, but when. February and March are both plausible. Though February stands out given the availability of fresh economic projections, a factor that gains weight in light of this week’s data.

Elsewhere, Dollar staged a notable rebound as the sharp post-NFP selloff faded. After an initial surge, market-implied odds of a March Fed rate cut have slipped back to around 51%, reflecting a partial reassessment rather than a full reversal.

One interpretation is that while October’s sharp contraction in payrolls was clearly alarming, investors are holding out hope for a more sustainable rebound in hiring. Temporary drags from the government shutdown have cleared, while the one-year US–China tariff truce has reduced uncertainty around trade and pricing.

Looking ahead, the December, January, and February US employment reports, alongside inflation data, will be critical in shaping expectations for the March FOMC meeting. With such a heavy data pipeline, it is premature to place strong bets on further Fed easing. At least, that's likely what the majority of traders think.

For now, the currency markets lack a strong directional bias. Yen leads for the week, followed by Dollar and Loonie, while Kiwi and Aussie lag. Sterling and Euro are stuck in the middle.

In Asia, Nikkei rose 0.26%. Hong Kong HSI is up 0.76%. China Shanghai SSE rose 1.19%. Singapore Strait Times is down -0.15%. Japan 10-year JGB yield rose 0.017 to 1.973. Overnight, DOW fell -0.62%. S&P 500 fell -0.24%. NASDAQ rose 0.23%. 10-year yield fell -0.033 to 4.149.

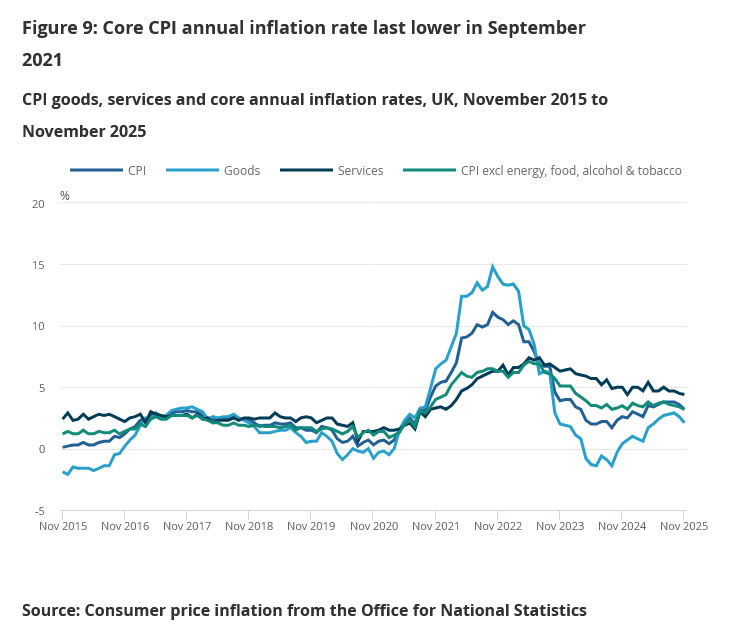

UK CPI undershoots at 3.2% as disinflation broadens in November

UK inflation eased more than expected in November, reinforcing signs that price pressures are moderating. Headline CPI slowed from 3.6% yoy to 3.2%, undershooting expectations of 3.5% and marking a second consecutive monthly decline. On a month-on-month basis, CPI fell -0.2% mom, adding to the disinflationary signal.

Underlying inflation also cooled. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 3.4% yoy to 3.2%, below forecasts of 3.4%, suggesting easing price pressures beyond volatile components.

The moderation was driven mainly by goods, where inflation eased from 2.6% yoy to 2.1% Services inflation edged slightly lower from 4.5% to 4.4%.

Japan posts first trade surplus in five months, US-bound shipments rebound

Japan’s trade data for November delivered a positive surprise, with exports rising 6.1% yoy to JPY 9.72 trillion, beating expectations of 4.8% yoy, and marking the third consecutive month of growth. The strength helped Japan record a JPY 322.2 billion trade surplus, the first in five months.

Exports to the US were a key driver, climbing 8.8% yoy. Auto shipments to the US rose 1.5%, marking the first increase since March and suggesting the drag from higher US tariffs is beginning to ease.

By contrast, exports to mainland China fell -2.4% yoy, weighed down by a sharp -5.9% decline in foodstuff shipments. That weakness came against a backdrop of renewed political tension, after Prime Minister Sanae Takaichi warned that a Chinese attempt to seize Taiwan could prompt Japanese military intervention, followed by Beijing restricting imports of Japanese seafood. Offsetting some of that drag, exports to Hong Kong surged 11.4%.

On the import side, growth was more subdued. Imports rose just 1.3% yoy to JPY 9.39 trillion, undershooting expectations of 2.5%.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3366; (P) 1.3411; (R1) 1.3467; More...

Intraday bias in GBP/USD is turned neutral again with current retreat. On the upside, above 1.3455 will resume the rebound from 1.3008. Firm break of 1.3470 resistance will pave the way to retest 1.3787 high. However, sustained break of 55 D EMA (now at 1.3293) will argue that the rebound has completed. Deeper fall would be seen back to 1.3008 support to resume the whole corrective pattern from 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

UK CPI undershoots at 3.2% as disinflation broadens in November

UK inflation eased more than expected in November, reinforcing signs that price pressures are moderating. Headline CPI slowed from 3.6% yoy to 3.2%, undershooting expectations of 3.5% and marking a second consecutive monthly decline. On a month-on-month basis, CPI fell -0.2% mom, adding to the disinflationary signal.

Underlying inflation also cooled. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 3.4% yoy to 3.2%, below forecasts of 3.4%, suggesting easing price pressures beyond volatile components.

The moderation was driven mainly by goods, where inflation eased from 2.6% yoy to 2.1% Services inflation edged slightly lower from 4.5% to 4.4%.

Final Data Prints Ahead of Big Central Bank Meetings on Thursday

In focus today

Markets are eyeing developments in oil markets amid diplomacy in the Ukraine war and US President Trump blocking oil tankers in Venezuela. Later in the day, we will be following several speeches from Fed members, including Waller on the economic outlook and additionally speeches by Williams and Bostic.

The UK November CPI inflation print is released. Price pressures have eased recently, although core inflation remains too high at 3.4%. We think it will take a print north of the 3.4% consensus to question the Bank rate being cut by the Bank of England tomorrow.

The euro area final inflation print for November is set for release, which we expect to confirm the flash release of 2.2% y/y headline inflation and 2.4% y/y core inflation.

In Sweden the large Origo survey (formerly Prospera) on inflation and wage expectations in the Swedish economy will be released. Inflation expectations are well anchored at or just above the target. The one-year expectations are likely to decline following the reduction in food VAT, in line with the monthly inflation expectations from money market participants. The most interesting aspect will be the wage expectations, as the two-year wage expectations have historically been by far the best leading indicator of actual wage developments in the economy.

Economic and market news

What happened overnight

In Japan, the November export figures exceeded expectations and increased +6.1% y/y (cons: 4.8%), driven by a weaker yen and a rebound in shipments to the US (+8.8% y/y). November imports rose 1.3% y/y.

What happened yesterday

In the euro area, flash PMIs for December weakened, as the composite PMI declined to 51.9 from 52.8 and below market expectations of 52.7. The manufacturing PMI fell to 49.2 from 49.6 in November and the services PMI slipped to 52.6 from 53.6. Overall business confidence weakened, while input cost inflation and output price pressures increased.

In the US, October nonfarm payrolls came in at -105k as the government shutdown caused a dip of -157k government jobs. November nonfarm payrolls were at +64k. Domestic labour supply continued to increase in November (+191k), lifting the unemployment rate higher to 4.6% from 4.4% in September. Even though the figures were likely negatively distorted by the shutdown, the rising unemployment rate suggests the labour market balance is indeed softening.

October retail sales were on the strong side with control group sales growing by 0.8% m/m SA. Discretionary categories saw especially strong growth, including furniture, electronics, sporting goods and online stores. Wage sum growth slowed gradually, as average hourly earnings disappointed with only +0.1% m/m SA in November, but the propensity to spend remains high.

The composite PMI figure for December remained in positive territory but weakened to 53.0 from 54.2 in November. The manufacturing PMI declined to 51.8 from 52.2 and the services PMI declined to 52.9 from 54.1. The services details looked gloomy, with new orders and employment indices weakening, but both input and output prices indices turned higher. On the manufacturing side, the new orders index declined, but so did inventories, so the manufacturing order-inventory balance actually improved from November.

In the UK, the released labour market data showed payrolls declining by 38K in November, although job losses were revised down for September and October. Private sector (3M rolling average) wage growth declined in October to 3.9% from 4.2% in September and below the Bank of England forecast of 4.2% for Q4. Viewing the overall picture, data has turned sourer since the November meeting, and we continue to expect a Bank rate cut on Thursday. The composite PMI exceeded expectations and improved to 52.1, supported by an uptick in both manufacturing and services PMIs. The manufacturing PMI rose to 51.2 in December - the highest level in a year. Services PMI increased to 52.1 in December from 51.3 in November.

Equities: Global equities ended the session 0.4% lower following a busy data day. Performance was clearly driven by the more cyclical and sentiment-sensitive sectors, with tech and consumer discretionary leading the declines, the latter largely dragged down by Tesla. S&P500 ended only -0.2% lower despite almost 75% of the constituents ended the day lower. NASDAQ gained 0.2%, while Russell 2000 and Stoxx600 ended the day both around -0.5% lower. Overnight, futures are in red.

FI and FX: The US labour market data showed enough softness to support the current pricing of two rate cuts from the Federal Reserve in 2026, but other than that market pricing changed very little although the unemployment rate is almost at a 4yr high. The Bund ASW-spread keeps widening together with the Buxl spread, but we expect this has more to do with the outright level for German yields, which is attractive for traditional long-only investors. This can also be seen from the continued spread tightening in e.g. the 10Y OAT-Bund spread as investors are still looking for carry despite the political uncertainty in France.