Sample Category Title

Hawkish BoE Cut Lifts Sterling, Dollar Weakens on Soft CPI

Sterling rallied broadly after the BoE delivered a widely expected rate cut that came with a distinctly hawkish undertone. The 5–4 vote, with four members dissenting in favor of holding rates steady, was a surprise and prompted a reassessment of how smooth the easing path ahead will be.

Fundamentally, the BoE still sees scope for further easing. However, policymakers were explicit that any additional cuts would now be a much “closer call”. That caution and the tight voting are striking given this week’s downside surprises in both UK employment and inflation. Despite the softer data, the MPC remains deeply divided.

February remains the most likely window for a follow-up cut, particularly with new economic projections due. Still, conviction has clearly faded, and markets are no longer confident that the BoE will simply return to a predictable quarterly easing rhythm.

By contrast, Dollar came under renewed pressure after US CPI undershot expectations. The weaker inflation print prompted a swift repricing of Fed expectations, with markets lifting the probability of a March rate cut to around 60%.

Even so, Dollar downside may not be linear. With risk sentiment fragile, further losses will likely depend on how equities behave through the rest of the session rather than on rate expectations alone. At the time of writing, US futures—particularly NASDAQ—are pointing to a rebound at the open. That recovery, however, remains tentative and vulnerable to reversal.

Looking ahead to Asia, attention turns to the BoJ, which is widely expected to raise rates by 25bps to 0.75%. That would mark the highest policy rate in 30 years, the first hike since January, and the first under Prime Minister Sanae Takaichi. The case for the move rests on persistently elevated core inflation and easing uncertainty tied to US tariffs, as confirmed by recent Tankan data. Political resistance to tightening has also softened.

Still, further tightening is far from assured. The BoJ is likely to wait for clearer evidence of sustained wage growth into 2026, with January’s economic projections set to shape expectations for what comes next.

In Europe, at the time of writing, FTSE is down -0.22%. DAX is up 0.40%. CAC is up 0.27%. UK 10-year yield is up 0.026 at 4.513. Germany 10-year yield is up 0.031 at 2.899. Earlier in Asia, Nikkei fell -1.03%. Hong Kong HSI rose 0.12%. China Shanghai SSE rose 0.16%. Singapore Strait Times fell -0.11%. Japan 10-year JGB yield fell -0.019 to 1.966.

US CPI slows sharply to 3.7% in November, core down to 2.6%

US inflation slowed more than expected in November, with the data compared against September levels due to the absence of October figures following the government shutdown.

Headline CPI eased from 3.0% yoy to 2.7%, undershooting expectations for a pickup to 3.1%. Core CPI also surprised to the downside, slowing from 3.0% yoy to 2.6% , well below forecasts for no change at 3.0%.

The broad-based moderation reinforces the view that underlying inflation pressures are easing faster than previously anticipated. Within the components, energy prices rose 4.2% yoy, while food prices increased 2.6% yoy.

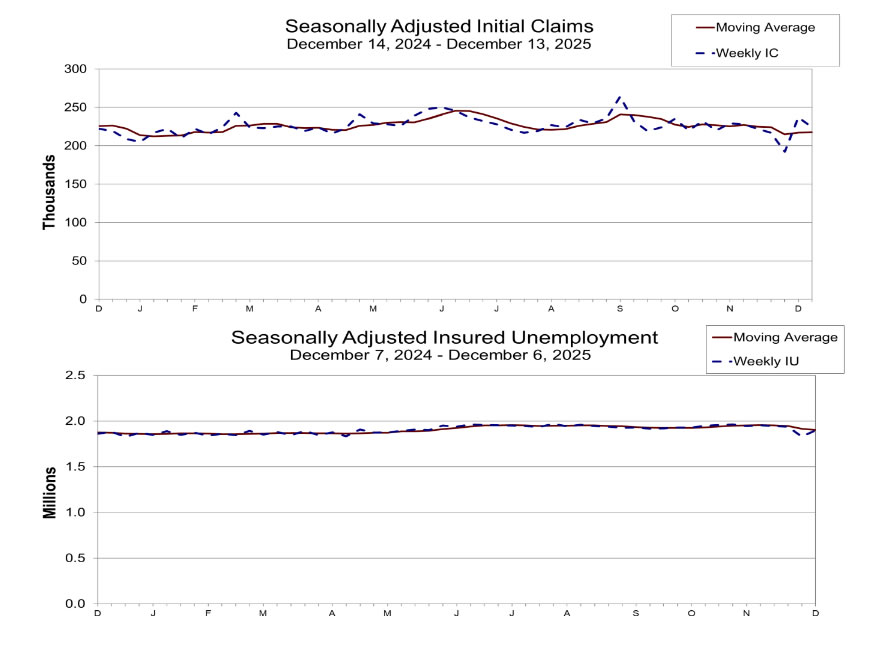

US initial jobless claims fall back to 224k, match expectations

US initial jobless claims fell -13k to 224k in the week ending December 13, matched expectations. Four-week moving average of initial claims rose 500k to 217.5k.

Continuing claims rose 67k to 1897k in the week ending December 6. Four-week moving average of continuing claims fell -14k to 1902.

ECB holds rates, forecasts reinforce inflation convergence around target

The ECB left its deposit rate unchanged at 2.00%, in line with expectations, signaling continued confidence that current policy settings remain appropriate. With inflation broadly converging around target and growth improving, policymakers saw no need to adjust rates at this stage.

Updated Eurosystem staff projections show headline inflation averaging 2.1% in 2025, easing to 1.9% in 2026 and 1.8% in 2027, before returning to 2.0% in 2028. Core inflation excluding energy and food is projected at 2.4% in 2025, 2.2% in 2026, 1.9% in 2027 and 2.0% in 2028.

The inflation outlook for 2026 was revised higher, mainly reflecting expectations that services inflation will decline more slowly than previously anticipated.

On growth, projections were revised higher across the forecast horizon. GDP is now expected to expand by 1.4% in 2025, 1.2% in 2026 and 1.4% in 2027, with growth holding at 1.4% in 2028. The improvement is driven primarily by stronger domestic demand.

BoE cuts to 3.75% with hawkish vote, future easing a closer call

The BoE delivered a widely expected 25bps rate cut, taking Bank Rate to 3.75%. However, the decision was accompanied by a surprisingly hawkish 5–4 vote split.

Supporters of the cut, led by Governor Andrew Bailey (with Sarah Breeden, Swati Dhingra, Dave Ramsden and Alan Taylor), argued that disinflation remains broadly on course. Some members emphasized that "upside risks to inflation had continued to recede". Others focused on weakening activity and downside inflation risks.

In contrast, four members (Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) voted to hold rates steady, expressing concern on "prolonged inflation persistence". They highlighted elevated services inflation, wage growth, and inflation expectations. These members are "not convinced that the monetary policy stance was meaningfully restrictive" That main require a more "prolonged period of policy restriction".

Overall, while reaffirming that Bank Rate is likely to continue on a "gradual downward path", it stressed that further easing decisions will become a "closer call".

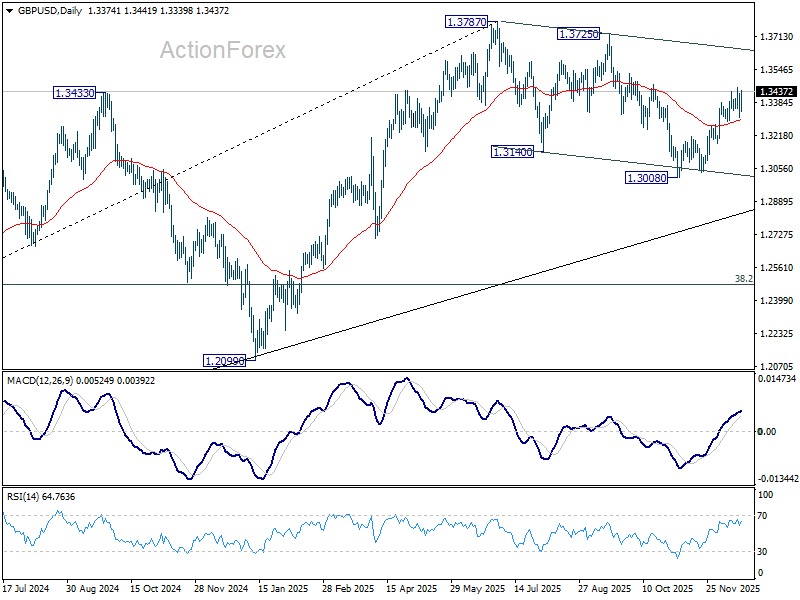

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3315; (P) 1.3372; (R1) 1.3431; More...

GBP/USD rebounds notably but stays below 1.3455 temporary top. Intraday bias remains neutral at this point. On the upside, above 1.3455 will resume the rebound from 1.3008. Firm break of 1.3470 resistance will pave the way to retest 1.3787 high. However, sustained break of 55 D EMA (now at 1.3295) will argue that the rebound has completed. Deeper fall would be seen back to 1.3008 support to resume the whole corrective pattern from 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

US initial jobless claims fall back to 224k, match expectations

US initial jobless claims fell -13k to 224k in the week ending December 13, matched expectations. Four-week moving average of initial claims rose 500k to 217.5k.

Continuing claims rose 67k to 1897k in the week ending December 6. Four-week moving average of continuing claims fell -14k to 1902.

US CPI slows sharply to 3.7% in November, core down to 2.6%

US inflation slowed more than expected in November, with the data compared against September levels due to the absence of October figures following the government shutdown.

Headline CPI eased from 3.0% yoy to 2.7%, undershooting expectations for a pickup to 3.1%. Core CPI also surprised to the downside, slowing from 3.0% yoy to 2.6% , well below forecasts for no change at 3.0%.

The broad-based moderation reinforces the view that underlying inflation pressures are easing faster than previously anticipated. Within the components, energy prices rose 4.2% yoy, while food prices increased 2.6% yoy.

ECB holds rates, forecasts reinforce inflation convergence around target

The ECB left its deposit rate unchanged at 2.00%, in line with expectations, signaling continued confidence that current policy settings remain appropriate. With inflation broadly converging around target and growth improving, policymakers saw no need to adjust rates at this stage.

Updated Eurosystem staff projections show headline inflation averaging 2.1% in 2025, easing to 1.9% in 2026 and 1.8% in 2027, before returning to 2.0% in 2028. Core inflation excluding energy and food is projected at 2.4% in 2025, 2.2% in 2026, 1.9% in 2027 and 2.0% in 2028.

The inflation outlook for 2026 was revised higher, mainly reflecting expectations that services inflation will decline more slowly than previously anticipated.

On growth, projections were revised higher across the forecast horizon. GDP is now expected to expand by 1.4% in 2025, 1.2% in 2026 and 1.4% in 2027, with growth holding at 1.4% in 2028. The improvement is driven primarily by stronger domestic demand.

(ECB) Monetary policy decisions

18 December 2025

The Governing Council today decided to keep the three key ECB interest rates unchanged. Its updated assessment reconfirms that inflation should stabilise at the 2% target in the medium term.

The new Eurosystem staff projections show headline inflation averaging 2.1% in 2025, 1.9% in 2026, 1.8% in 2027 and 2.0% in 2028. For inflation excluding energy and food, staff project an average of 2.4% in 2025, 2.2% in 2026, 1.9% in 2027 and 2.0% in 2028. Inflation has been revised up for 2026, mainly because staff now expect services inflation to decline more slowly. Economic growth is expected to be stronger than in the September projections, driven especially by domestic demand. Growth has been revised up to 1.4% in 2025, 1.2% in 2026 and 1.4% in 2027 and is expected to remain at 1.4% in 2028.

The Governing Council is determined to ensure that inflation stabilises at its 2% target in the medium term. It will follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance. In particular, the Governing Council’s interest rate decisions will be based on its assessment of the inflation outlook and the risks surrounding it, in light of the incoming economic and financial data, as well as the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

Key ECB interest rates

The interest rates on the deposit facility, the main refinancing operations and the marginal lending facility will remain unchanged at 2.00%, 2.15% and 2.40% respectively.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP and PEPP portfolios are declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation stabilises at its 2% target in the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.

BoE cuts to 3.75% with hawkish vote, future easing a closer call

The BoE delivered a widely expected 25bps rate cut, taking Bank Rate to 3.75%. However, the decision was accompanied by a surprisingly hawkish 5–4 vote split.

Supporters of the cut, led by Governor Andrew Bailey (with Sarah Breeden, Swati Dhingra, Dave Ramsden and Alan Taylor), argued that disinflation remains broadly on course. Some members emphasized that "upside risks to inflation had continued to recede". Others focused on weakening activity and downside inflation risks.

In contrast, four members (Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) voted to hold rates steady, expressing concern on "prolonged inflation persistence". They highlighted elevated services inflation, wage growth, and inflation expectations. These members are "not convinced that the monetary policy stance was meaningfully restrictive" That main require a more "prolonged period of policy restriction".

Overall, while reaffirming that Bank Rate is likely to continue on a "gradual downward path", it stressed that further easing decisions will become a "closer call".

(BOE)Bank Rate reduced to 3.75%

Monetary Policy Summary, December 2025

At its meeting ending on 17 December 2025, the Monetary Policy Committee voted by a majority of 5–4 to reduce Bank Rate by 0.25 percentage points, to 3.75%. Four members voted to maintain Bank Rate at 4%.

CPI inflation has fallen since the previous meeting, to 3.2%. Although above the 2% target, it is now expected to fall back towards target more quickly in the near term. Reflecting restrictive monetary policy, and consistent with evidence of subdued economic growth and building slack in the labour market, pay growth and services price inflation have continued to ease.

Monetary policy is being set to ensure CPI inflation settles sustainably at 2% in the medium term, which involves balancing the risks around achieving this. The risk from greater inflation persistence has become somewhat less pronounced since the previous meeting, while the risk to medium-term inflation from weaker demand remains.

The extent of further easing in monetary policy will depend on the evolution of the outlook for inflation. The restrictiveness of policy has fallen as Bank Rate has been reduced by 150 basis points since August 2024. On the basis of the current evidence, Bank Rate is likely to continue on a gradual downward path. But judgements around further policy easing will become a closer call.

Minutes of the Monetary Policy Committee meeting ending on 17 December 2025

1: Before turning to its immediate policy decision, the Monetary Policy Committee (MPC) discussed key economic developments and its judgements around them, as well as its views on monetary policy strategy.

Current economic conditions

2: Twelve-month CPI inflation had eased to 3.2% in November from 3.6% in October and 3.8% in September. This was below the short-term forecast published in the November Monetary Policy Report, largely reflecting downside news to food price inflation. The October release had triggered the exchange of open letters between the Governor and the Chancellor of the Exchequer that was being published alongside these minutes.

3: Services consumer price inflation was 4.4% in November, compared with the most recent peak of 5.4% in April. Measures of underlying services price inflation had pointed to the disinflation process continuing, as pay growth had eased. The impacts of one-off shocks to the price level, such as the employers’ National Insurance Contributions increases and unusually large increases in some administered prices earlier in the year, had continued to restrain this downward trend to a degree.

4: CPI inflation was expected to ease further in 2026 Q1, to around 3%. Before that, CPI inflation was expected to rise temporarily in December 2025, owing to an increase in tobacco duty and a pickup in airfares price inflation.

5: Some measures announced in the Budget, in particular one-off reductions to regulatory costs levied on households’ energy bills, and changes to fuel duty, were likely to lower CPI inflation in April by around ½ percentage point. This Budget news, in combination with other news in recent CPI data and with some downward moves in sterling oil and gas futures curves since November, had led Bank staff to lower their expectation for CPI inflation to closer to 2% in 2026 Q2.

6: There had been small movements in inflation expectations over recent months. Market measures of medium-term inflation compensation had been little changed since the MPC’s November meeting. The Bank/Ipsos and Citi/YouGov indicators of households’ short and medium-term inflation expectations had eased slightly in November, albeit remaining at elevated levels. The Decision Maker Panel (DMP) survey had reported that firms’ year-ahead own-price inflation expectations rose slightly to 3.7% in the three months to November and were close to realised own-price inflation, suggesting that firms continued to expect little change in inflation a year ahead. Intelligence from the Banks’ Agents suggested that firms did not expect to pass on fully increases in costs given the weak demand environment.

7: A range of indicators suggested that pay growth had continued to ease in the second half of 2025, particularly in the private sector. Annual growth in whole economy Average Weekly Earnings (AWE) had declined to 4.7% in the three months to October. AWE private sector regular pay growth had fallen to 3.9%, which was in line with the forecast in the November Report. While still elevated, this rate of pay growth could be broadly explained by economic fundamentals, in contrast to developments over the past few years when pay growth had been stronger than could be explained. Bank staff expected private sector regular AWE pay growth to ease to around 3½% in 2025 Q4, predominantly owing to base effects, which reflected the strength in pay growth at the end of 2024. A range of pay settlements data suggested that the median private-sector settlement had been around 3% in the three months to November, although fewer companies agreed their settlements at this time of the year.

8: Forward-looking wage indicators had remained elevated. Ahead of the Agents’ annual pay survey, which would be a key input into the February MPC round, the Agents’ contacts had suggested that pay settlements were expected to be around 3½% in 2026. This was still an elevated level, although it was nearly ½ percentage point lower than figures reported for 2025. The November DMP survey had reported a slight increase in firms’ twelve-month ahead pay expectations to 3.8%, suggesting that pay growth might not ease materially further into next year.

9: The labour market had loosened further. The LFS unemployment rate had risen to 5.1% in the three months to October, 0.2 percentage points above the expectation in the November Report. The LFS redundancy rate had risen to 5.3 per 1,000 employees, its highest level since 2013, outside of the Covid pandemic period. But this series was prone to volatility, and the latest increase had not been mirrored in HR1 redundancy notifications. In contrast, the level of vacancies had been broadly stable since the summer. Employment growth had remained subdued. An HMRC payrolls estimate of private sector employees had fallen even further than the headline HMRC estimate in the three months to November, extending a recent pattern of weakness. Public sector employment had been stronger.

10: GDP growth had eased to 0.1% in 2025 Q3, slightly below the rate expected in the November Report. Bank staff analysis had suggested that some of this softening was erratic, with underlying quarterly GDP growth closer to 0.2%. Monthly GDP had declined by 0.1% in October, due to a further fall in market sector output. This was weaker than had been expected in the November Report and Bank staff now expected zero growth in headline GDP in Q4. Business surveys had remained subdued, including the S&P Global UK PMI composite output index, although that had picked up in the flash December release and, more generally, had been above the no-change mark for the past eight months. The steer from business surveys suggested that underlying growth in Q4 would be stronger than headline GDP growth, but at a rate that was still below supply growth.

11: Domestic credit volumes had continued to be supported by reduced policy restriction, along with some improvement in credit supply conditions. The Bank’s latest Credit Conditions Survey had suggested that supply was continuing to improve for households and firms, and firms’ access to bank finance appeared resilient. Nevertheless, credit volumes growth had remained subdued relative to pre-pandemic norms in real terms. Households’ and non-financial corporations’ aggregate balance sheets had also remained resilient, according to the Financial Policy Committee’s latest Financial Stability Report. Alongside this, recent annual growth in broad money had remained in line with the rate seen in 2025 so far, with the ratio of money to nominal GDP remaining below levels implied by its pre-pandemic trend.

12: UK financial conditions were little changed relative to the November MPC meeting. Market pricing implied an expectation for a reduction in Bank Rate at this meeting.

13: Global activity indicators had been more resilient than expected at the time of the November Report. This was suggestive of tariffs and trade policy uncertainty not weighing on global economic activity to the extent that had been expected. Alongside this, Chinese export price deflation had increased, following a brief moderation earlier this year.

The Autumn Budget

14: The Autumn Budget had taken place on 26 November, accompanied by an economic and fiscal outlook from the Office for Budget Responsibility. Additional fiscal measures had included: spending increases in the short term in the form of reversals to previously announced welfare cuts and the removal of the two-child limit within universal credit. Beyond the short term, these spending increases would be more than offset by future tax increases, primarily from extending the freezes to income tax thresholds out to 2030-31. Smaller contributions would come from increases to National Insurance Contributions on salary-sacrifice pension contributions and increases to property, savings and dividend taxes.

15: Relative to what had been assumed in the November Monetary Policy Report, Bank staff had provisionally estimated that these additional policy measures could increase the level of GDP by around 0.1–0.2% over the next couple of years, with the fiscal tightening through future tax increases weighing on the level of GDP beyond a three-year horizon.

16: The Budget had also included a set of policy measures that had a direct impact on inflation in the short term, which were likely to lower CPI inflation in April by around ½ percentage point. Subsequently, the impact of the direct and indirect effects of Budget policies were expected to push up on CPI inflation by around 0.1–0.2 percentage points in 2027 and 2028.

17: The Committee considered the total fiscal consolidation envisaged in the latest plans for forthcoming years. Cumulatively, fiscal policies announced to date were expected to widen the output gap by around 1 percentage point over the next three years. The Budget had made only a modest additional contribution to this expected widening beyond the next three years.

18: A fuller assessment of this fiscal news would be conducted as part of the February 2026 Monetary Policy Report round.

Overview and the Committee’s discussions

19: The Monetary Policy Committee’s job is to ensure that CPI inflation falls all the way back to the 2% target and stays there. Monetary policy had helped to reduce inflationary pressures over the past three years. That had allowed the MPC to make policy less restrictive, by reducing Bank Rate since August 2024.

20: The MPC’s approach to setting Bank Rate outlined in the November Monetary Policy Report had been based on two key policy judgements. First, that underlying domestic wage and price pressures were continuing to ease, and that the risks to medium-term inflation from greater inflation persistence and weaker demand were more balanced. Second, that Bank Rate was likely to continue on a gradual downward path if progress on disinflation continued.

21: Since November, the risk from greater inflation persistence had become somewhat less pronounced, while the risk to medium-term inflation from weaker demand remained.

22: CPI inflation had fallen since the previous meeting, from 3.8% to 3.2%. This was above the 2% target but, following the Budget announcements on administered prices and indirect taxes, headline inflation was now expected to fall back more quickly in April, to closer to 2%. Reflecting restrictive monetary policy, and consistent with evidence of subdued economic growth and building slack in the labour market, pay growth and services price inflation had continued to ease, pointing to further underlying disinflation towards target. Looking forward, however, some indicators of wage and price-setting from the Bank’s Agents and the Decision Maker Panel appeared to have plateaued.

23: Although headline inflation was likely to fall back closer to target in the near term, the Committee would remain focused on ensuring that inflation settled sustainably at 2% in the medium term. The latest data were generally encouraging, but there continued to be risks around that in both directions.

24: The recent experience of high inflation could still be affecting the way wages and prices were being determined in the economy, including owing to structural factors. The hump in inflation earlier this year had not been expected to lead to additional second-round effects in previous central projections. So a faster near-term fall now, owing to similar factors, might be treated in an equivalent way. The Committee would nonetheless monitor carefully the response of still-elevated inflation expectations to recent downside news, including in response to developments in more salient prices such as energy and food. The MPC was also continuing to assess whether and how fast wage and services inflation would fall further towards more target-consistent rates.

25: At the same time, households and businesses could remain cautious about their spending and investment decisions, and the labour market could weaken significantly further. Both of these could lead to inflation falling below target in the medium term. There had been limited news on the demand outlook since the previous meeting. Although GDP growth in 2025 Q4 was likely to be weaker than expected, the flash PMI output index had increased in December. Most labour market data had not suggested a rapid opening up of slack in the economy, even though the unemployment rate had continued to move higher.

26: Different members continued to place different weights on the main risks to inflation. For some of those members who had been more concerned about second-round effects from recent high inflation, the news on near-term inflation from the Budget could lessen these risks to some extent. Nevertheless, other persistence risks remained, particularly in light of the long period of above-target inflation, and the signals from forward-looking indicators were that pay growth could remain elevated next year. For those members who had been less concerned about persistence previously, the remaining upside risks had diminished further, and were now more clearly outweighed by downside risks to demand and the possibility of a more rapid loosening in the labour market.

27: Regarding the second key policy judgement, the extent of further easing in monetary policy still depended on the evolution of the outlook for inflation, and how the evidence on persistence, and on the weakening in demand and the labour market, was playing out. A gradual approach to further easing allowed the Committee to assess carefully the balance of risks to inflation as the evidence evolved.

28: The restrictiveness of monetary policy had fallen as Bank Rate had been progressively reduced. Different members had different views on how, and with what degree of precision, an equilibrium, or neutral, level of Bank Rate could be identified. In the absence of new shocks to the economy, judgements for individual members around further policy easing would become a closer call. This could simply reflect the more limited scope to reduce rates for a given estimate of neutral, or alternatively that the policy approach should recognise the uncertainty around the level of equilibrium rates itself. It could also reflect a high bar for policy reversals, were Bank Rate to be reduced too quickly or by too much, which could undermine credibility.

The immediate policy decision

29: The Committee turned to its policy decision at this meeting and the monetary stance required to achieve the 2% inflation target sustainably in the medium-term.

30: Five members (Andrew Bailey, Sarah Breeden, Swati Dhingra, Dave Ramsden and Alan Taylor) preferred to reduce Bank Rate by 0.25 percentage points at this meeting. The disinflation process was on track and the key question was how sustainably inflation would settle at the 2% target. Three members in this group (Andrew Bailey, Sarah Breeden and Dave Ramsden) judged that upside risks to inflation had continued to recede, but they would continue to assess incoming evidence, particularly around labour market activity and wage growth. Two members in this group (Swati Dhingra and Alan Taylor) attached greater weight to downside risks to activity and inflation. Subdued consumption and rising unemployment were already sufficient to restrain inflation persistence.

31: Four members (Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) preferred to maintain Bank Rate at this meeting, placing greater weight on prolonged inflation persistence, including from structural factors. While acknowledging recent progress on disinflation, the current and forward-looking evidence on services inflation, wage growth and inflation expectations remained above target-consistent levels. This could be symptomatic of more lasting changes in wage and price-setting behaviour. These members were not convinced that the monetary policy stance was meaningfully restrictive. A more prolonged period of policy restriction was warranted to mitigate these upside risks.

32: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be reduced by 0.25 percentage points, to 3.75%.

33: Five members (Andrew Bailey, Sarah Breeden, Swati Dhingra, Dave Ramsden and Alan Taylor) voted in favour of the proposition. Four members (Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) voted against the proposition, preferring to maintain Bank Rate at 4%.

MPC members’ views

34: Members set out the rationale underpinning their individual votes on Bank Rate.

Members are listed alphabetically under each vote grouping.

Votes to reduce Bank Rate by 0.25 percentage points, to 3.75%

Andrew Bailey: Data news since our latest meeting suggests that disinflation is now more established. CPI inflation has fallen from its recent peak and upside risks have eased. Measures in the Budget should reduce inflation further in the near term. The key question for me now is the extent to which inflation settles at the 2% target in an enduring way. Slack has continued to accumulate in the economy. Unemployment, underemployment and flows from employment to unemployment have all risen. While I do not yet see conclusive evidence of a sharper downturn in the labour market, we should be vigilant. On the other hand, inflation expectations have not yet shifted downward sufficiently following the past few years of persistent above-target inflation. And the strength in forward-looking wage growth indicators is hard to reconcile with the downward momentum in current indicators of inflation and pay as well as rising unemployment. I will continue to assess these risks as the evidence accumulates. While I see scope for some additional policy easing, the path for Bank Rate cannot be pre-judged with precision, recognising in part the more limited space as Bank Rate approaches a neutral level.

Sarah Breeden: I judge that disinflation remains on track and that upside risks have diminished a little further since November. Inflation, underlying services inflation, wage growth and households’ inflation expectations have all moved down. Activity data are also consistent with building slack, with a further rise in unemployment and weak employment growth. Previous explanations for why inflation might remain stubbornly above target have become less likely. The Budget has clarified that administered price shocks should not repeat next year. I recognise risks from potential structural changes to the labour market, in particular that matching efficiency may have fallen, and forward‑looking pay surveys are somewhat higher than I would prefer. However, Agents’ reports suggest firms are taking action to contain total wage bills. This, and the weak demand environment, should limit cost pass‑through. Downside risks to the demand outlook remain prominent. As in November, I think it plausible that a structural change in household behaviour means the savings rate remains elevated. Combined with my view that policy remains restrictive and slack continues to build, this gives me enough confidence to cut now. Looking ahead, I will need a greater accumulation of evidence on disinflation as we feel our way towards neutral next year.

Swati Dhingra: I see disinflation continuing and risks to activity skewed to the downside. Nominal indicators have been trending consistently in the right direction. Inflationary pressures have faded, with limited pass-through of global food price inflation to consumer prices, and the impact of domestic one-off factors having come through. Disinflation is particularly observable in underlying inflation measures. Moreover, the dynamics of household-led demand weakness, that have contributed to disinflation so far and contained second-round effects, are still very much at play. Weak household spending look set to continue, which should limit firms’ pricing power. The backdrop of a weak labour market is likely to restrain wage growth going forward. Unemployment has risen more rapidly than I expected, given how activity and real wages have evolved, and vacancies remain 10% below pre-pandemic levels. My outlook at this juncture is one of continued weakness in activity. And I am concerned that a protracted period of stagnation could impede supply-side growth. I favour easing policy now, and would not support a drawn-out normalisation of our policy stance given the balance of risks.

Dave Ramsden: I view the risks around inflation returning sustainably to target late in 2026 as broadly balanced, which is somewhat earlier than in the November central projection. The disinflation process is on track as nominal indicators continue to normalise. Labour market loosening has anchored this disinflation, and against the backdrop of weak activity and subdued sentiment, a further easing to come should lean against any remaining persistence in wage growth. However, elevated forward-looking surveys of wage growth give me pause for thought, particularly as structural supply-side issues, such as labour market participation, that previously sustained inflation persistence appear to be resolving. I will be focused on the results of the 2026 Agents’ pay survey. I continue to see downside risks from weak demand and particularly consumption. Consistently weak consumer confidence and ongoing fiscal consolidation contribute to a sluggish growth outlook, even if the announcement of the Budget offers some certainty. This outlook supports an easing in monetary policy. Further ahead, as restrictiveness falls and with uncertainty around the neutral rate, there could be scope to slow this cadence of easing in due course.

Alan Taylor: Recent developments align with my stated view of the medium-term trajectory: the two key trends are steadily mounting downside risks and inflation firmly on track towards target. The news implies a path for inflation next year that reaches target sooner than in the November central projection. The inflation hump is subsiding a bit earlier: tax and administered price increases drop from annual CPI by April and food inflation is abating faster than expected. High‑frequency CPI indicators, overall and core, are close to target. Wages are on a target‑consistent path, based on incoming settlements data; AWE follows with a lag. Labour market news shows continued loosening. Redundancies are now on the rise and unemployment keeps climbing, markedly so among cyclically-sensitive younger cohorts. Demand is subdued, with surveys signalling weak output, deteriorating investment intentions, and low consumer confidence. Company dissolutions are increasing. These worrying trends point to the risk of at least a costly undershoot on inflation, if not a sharper non-linear deterioration in activity and the labour market, should we brake too hard. I see neutral at about 3%. Given transmission lags, and with inflation expected near target by late 2026, we should be heading there sooner rather than later.

Votes to maintain Bank Rate at 4%

Megan Greene: I think risks to inflation have shifted to the downside since November. I put weight on threshold effects and the salience of food and energy prices in the inflation basket. The budget will mechanically reduce inflation below thresholds that feed into expectations largely because of lower energy prices. Recent food price and CPI price inflation surprised on the downside as well. This should reduce the risk of elevated inflation expectations generating second-round effects, but I remain concerned the disinflation process has slowed and may stall further. Forward‑looking indicators of wage growth from the Agents and Decision Maker Panel remain above target-consistent levels. This could buoy services inflation, while core goods inflation remains above pre-Covid averages. Financial and credit conditions are relatively easy, suggesting the monetary policy stance is not meaningfully restrictive. Labour market slack is rising and, while rising redundancies are a concern, there is little evidence a non-linear rise in unemployment is imminent. Labour market adjustments may also be buffered by resilient corporate balance sheets and loose credit conditions. As Bank Rate approaches neutral, the contribution of monetary policy versus structural factors to disinflation could become harder to discern. This warrants a more cautious cadence of easing.

Clare Lombardelli: I continue to be more concerned by the upside risks to inflation, despite growth and inflation data since November having softened at the margin. The Budget should mechanically reduce annual inflation in salient categories, reducing the risk of second-round effects, but in absolute terms underlying inflation is still well above target-consistent rates. Disinflation in wage growth will be crucial in returning inflation sustainably to target, yet forward-looking indicators of wage growth from the DMP and Agents suggest little disinflation in wages over the next year. Elevated wage growth contrasts with softening labour market quantities. This could indicate structural issues in the economy which would sustain greater inflation persistence than embodied in the November central projection. I am also uncertain about the amount of restriction that our current policy stance is imparting, where signals across the data are mixed, and future policy reversal could be costly for policy credibility. This calls for retaining policy restriction and, all else equal, could require slowing the pace of future policy easing.

Catherine L Mann: My decision was quite finely balanced, and made more challenging by the effect of various policies on wage and price dynamics. Two key judgements underpin my decision. First, despite the Budget’s expected mechanical reduction in near-term inflation, this may not be enough to rein-in elevated household inflation expectations that have formed during a prolonged high‑inflation environment. CPI inflation remains above target, services inflation remains high relative to international peers, and core goods inflation is well above historical target‑consistent rates. Second, despite soft private-sector activity, this has not yet sufficiently disciplined wage and price growth. Market sector output is indisputably soft, private employment is falling, and redundancies and business dissolutions are rising. I am particularly attentive to the possibility that these could be signs of a non-linear adjustment. Counterbalancing these data, forward‑looking wage measures are above target‑consistent ranges, government spending and employment has risen, and any potential fiscal overspend could reduce slack, as has been the case in the past. In light of these risks, and given that restrictiveness in financial conditions has already eased over the year, policy needs to remain restrictive for some time longer.

Huw Pill: I continue to judge the risk of inflation stabilising at above-target levels owing to structural changes in price and wage-setting behaviour as greater than the risk of inflation undershooting the target owing to weak demand. Underlying inflationary pressures are stronger than expected a year ago. A number of key indicators of underlying inflationary momentum – such as one-year ahead own price and wage expectations in the Decision Maker Panel, and households’ medium-term inflation expectations – exhibit a shallow saucer-shaped profile, raising concerns about a slowing or stalling in disinflation towards target. While I am attentive to risks from weak demand, still resilient private‑sector balance sheets provide some reassurance against a sharp downturn owing to a corporate cash-flow squeeze. Given this balance of risks, the case for the further withdrawal of monetary policy restriction is becoming more finely balanced, and any additional steps in this direction should be cautious.

Operational considerations

35: On 17 December, the stock of UK government bonds held for monetary policy purposes was £553 billion.

36: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Swati Dhingra

- Megan Greene

- Clare Lombardelli

- Catherine L Mann

- Huw Pill

- Dave Ramsden

- Alan Taylor

Sam Beckett was present as the Treasury representative. On the occasion of her final meeting, the Chair expressed his appreciation on behalf of the Committee for her role as Treasury representative since 2023.

David Roberts was present on 10 December and 15 December, as an observer for the purpose of exercising oversight functions in his role as a member of the Bank’s Court of Directors.

Pound Holds Its Breath Ahead of Bank of England Decision

The British pound declined to around $1.3300 against the US dollar on Wednesday, as UK inflation undershot expectations and reinforced market convictions that the Bank of England (BoE) will cut interest rates on Thursday.

The annual Consumer Prices Index (CPI) inflation rate slowed to 3.2% in November, missing forecasts of 3.5% and falling below the central bank's projection of 3.4%. This followed labour market data earlier in the week, which revealed unemployment rose to its highest level since 2021, while wage growth eased – albeit less sharply than anticipated.

The economic backdrop has weakened further following last week's Gross Domestic Product (GDP) data, which confirmed the UK economy contracted for a second consecutive month in October. Given this deteriorating picture, the BoE is now widely expected to resume its monetary easing cycle, cutting the Bank Rate by 25 basis points to 3.75% – its lowest level since 2022. The central bank has held rates steady at its last two meetings in September and November.

Money markets have adjusted their expectations in response, now pricing in approximately 66 basis points of total easing by the end of 2026, up from around 58 basis points before the latest inflation report.

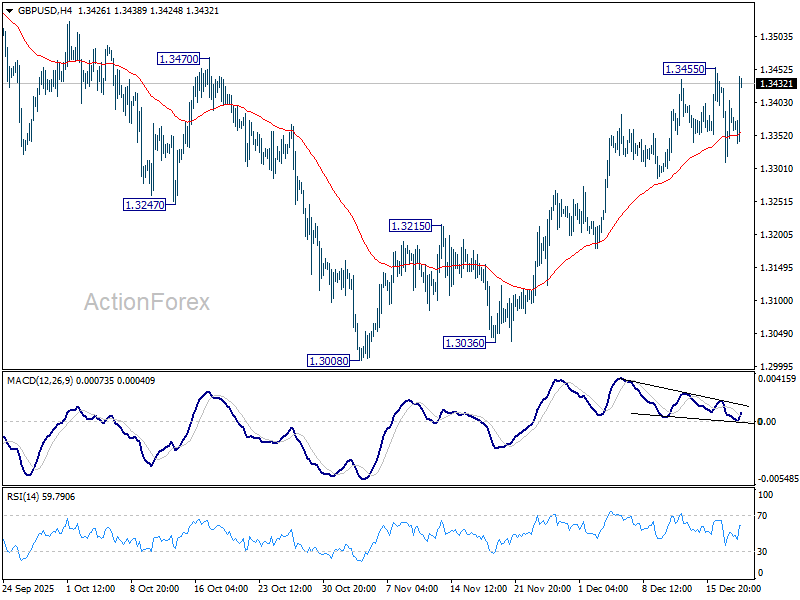

Technical Analysis: GBP/USD

H4 Chart:

On the H4 chart, the pair is developing a downward wave structure with a target at 1.3300. We expect this level to be tested today. Subsequently, a corrective rebound towards 1.3370 is likely. Once this correction is complete, the primary downtrend is anticipated to resume, targeting 1.3240, with potential for an extension towards 1.3175.

This bearish scenario is technically confirmed by the MACD indicator. Its signal line has exited the histogram zone and is near the zero mark, suggesting it will decline to new lows.

H1 Chart:

On the H1 chart, the market is forming a downward impulse targeting 1.3290 as its initial objective. Following this, a correction towards 1.3370 is likely. Upon completion of this corrective phase, the focus will shift to the potential continuation of the downtrend.

This outlook is supported by the Stochastic oscillator. Its signal line is below the 50 level and is pointing firmly downwards towards 20.

Conclusion

The pound remains under clear pressure ahead of Thursday's pivotal BoE meeting, with soft inflation and growth data significantly raising the odds of a rate cut. The technical posture is bearish across timeframes, suggesting any near-term corrective bounce is likely to be sold into, paving the way for a test of lower support levels.

Analysis of the Volatility Spike on the BTC/USD Chart

Yesterday, the BTC/USD chart saw sharp price swings during the US trading session:

→ first, Bitcoin rose by more than 3%;

→ shortly afterwards, it dropped by over 4%.

The main impulses unfolded within just a few hours and triggered liquidations on both long and short positions. In total, around $450 million worth of positions were liquidated across Binance and other crypto exchanges. As a result, on the daily BTC/USD chart, yesterday’s candle resembles a pin bar with a long upper wick, which is typically viewed as a bearish signal.

Notably, it is difficult to identify clear fundamental drivers for the crypto market at this time, aside from growing rumours about a potential military conflict between Venezuela and the United States.

However, looking at the broader, long-term context of the BTC/USD chart provides important clues as to what this price action may signify.

Technical Analysis of the BTC/USD Chart

When a long-term ascending channel is plotted (shown in blue), it becomes clear that Bitcoin’s price is trading near its lower boundary, which has been acting as support since mid-November (marked by the blue arrow).

At the same time, at the peak of yesterday’s rally, the price made a false bullish break above the psychological $90,000 level, as well as above the high of the bearish candle from 15 December. This allows the move to be interpreted as a bearish liquidity grab.

Taken together, these factors suggest that so-called “smart money” is applying increasing pressure on the lower boundary of the blue channel.

Therefore, traders may wish to consider a scenario in which Bitcoin develops further bearish momentum within a descending channel. This channel was first outlined in an analytical note a month ago, has since been extended lower, and its median line has acted as resistance (highlighted by the red arrow), confirming the relevance of this structure.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

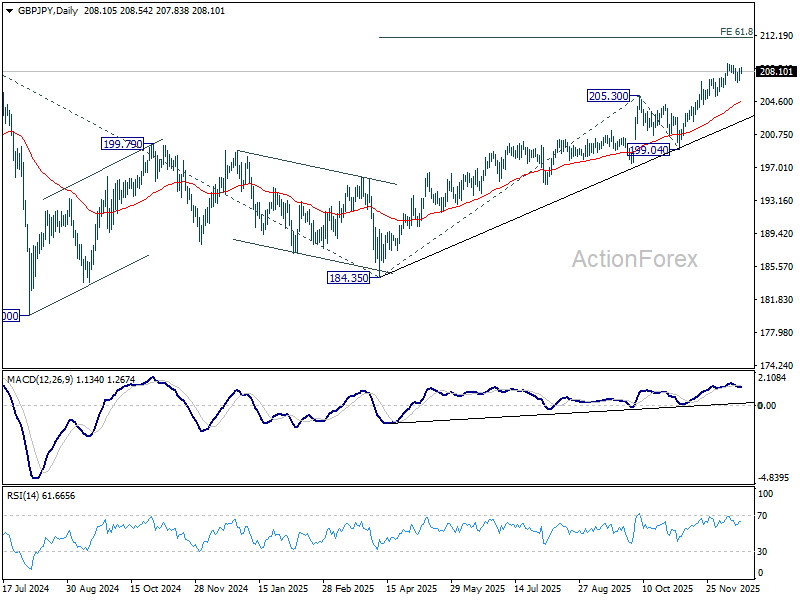

GBP/JPY Daily Outlook

Daily Pivots: (S1) 207.40; (P) 207.90; (R1) 208.75; More...

Range trading continues in GBP/JPY below 208.92 and intraday bias stays neutral. Further rally is expected as long as 205.17 support holds. On the upside, break of 208.92 will resume larger up trend and target 61.8% projection of 184.35 to 205.30 from 199.04 at 211.98 next.

In the bigger picture, up trend from 123.94 (2020 low) is resuming. Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. On the downside, break of 199.04 support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.