Sample Category Title

RBA Does Not Like Where Prices Headed to

Markets

In advance one could have assumed that a thin calendar and markets awaiting additional guidance from Wednesday’s Fed meeting to result in subdued technical trading in core yield markets. Quod non. It didn’t take into account some trend-supporting quotes from influential ECB board member Isabel Schabel. She advocated that some kind of reflationary momentum helped by a supportive fiscal policy might narrow the EU output gap and prevent a further decline in EMU (core) inflation even as headline inflation might temporarily drop below 2%. However, if this downward deviation is small, Schnabel assesses that the ECB should look through it. In such a scenario, it is possible that after a period of rate stability, the next ECB move could be a rate hike. Over the previous weeks, Japan and the UK often were the drivers of higher risk bond premia. Yesterday’s Schnabel comments took over that role. Bunds underperformed Treasuries, gilts and JGB’s with yields adding 7.8 bps (5-y) to 3.1% (30-y), the belly of the curve underperforming. US yields initially also jumped substantially higher, but momentum dwindled as the US session proceeded. A decent $58 bln US 3-y action helped to smooth the pressure. In a daily perspective, US yields added between 1.5 bps (2-y) and 3.5 bps (5-y). Higher yields/risk premia also arrested the recent equity rebound (S&P 500 -0.35%, Eurostoxx 50 +0.03%). On FX markets, the euro initially tried to capitalize on additional interest rate support, but the move was again abruptly countered by an intraday USD comeback in US dealings. EUR/USD even closed the session marginally softer at 1.1637. USD/JPY extended its recovery to close just below the 156 handle. EUR/GBP finished little changed near 0.8735.

Today’s eco calendar is again relatively thin, but yesterday’s price action illustrated that this is no guarantee for subdued trading. In the US, October JOLTS job openings give some (admittedly) delayed insights on momentum in the US job market. Questions is whether/to what extent markets are prepared to change recent rather ‘hawkish positioning’ even in case of softer than expected data. In Europe, the vote on the French social security budget again is expected to be a close call to avoid further political/budgetary chaos. BoE policymakers will attend a hearing before the Treasury Committee of Parliament. The US Treasury will sell $39 bln of 10-y. In FX markets, current ‘noisy market sentiment’ in some way apparently still supports the dollar even as non-US yields are rising at least as fast as is the case in the US. The EUR/USD 1.1682/1.1725 area in this respect proofs relative strong resistance short-term.

News & Views

“The question is, is it just an extended hold from here or is it possibility of a rate rise?” This one quote from Governor Bullock of the Reserve Bank of Australia is telling of the central bank’s state of mind. It kept the policy rate steady at 3.6% this morning and is clearly worried about inflation. The RBA does not like where prices are headed to and said risks have flipped to the upside. The October monthly print quickened from 3.6% to 3.8%. That’s well above the 2%-3% target range and comes after the Q3 quarterly outcome - still the gold standard for the RBA - had significantly surpassed the RBA’s previous expectations. Core gauges also run hotter than the RBA would like to. The board sees “signs of a more broadly based pick-up in inflation” which against the backdrop of recovering economic activity and still tight labour market conditions needs to be monitored for its persistence. Bullock at the presser said policymakers hadn’t explicitly considered the case for a rate hike but did discuss the circumstances where one could be needed. The market implied probability for such a move increased significantly with 50-50 odds for the March meeting next year. A first full rate hike was pulled forward from August to June. Australian swap yields surge up to 8 bps at the front. AUD/USD appreciates to 0.664.

Consumers’ inflation expectations in the NY Fed’s monthly survey stabilized at all horizons: 3.2% for the one-year ahead gauge and 3% for the 3- and 5-year one. Household perceptions of their current financial situation deteriorated notably, however, with a larger share of respondents reporting they are worse off than a year ago. Expectations about the year-ahead situation also worsened, be it slightly. In a positive sign, the household mean probability of unemployment to be higher one year from now decreased by 0.4 percentage points to 42.1%. Lastly, there is a decrease in the net share of respondents who expect that credit will be easier to obtain a year from now.

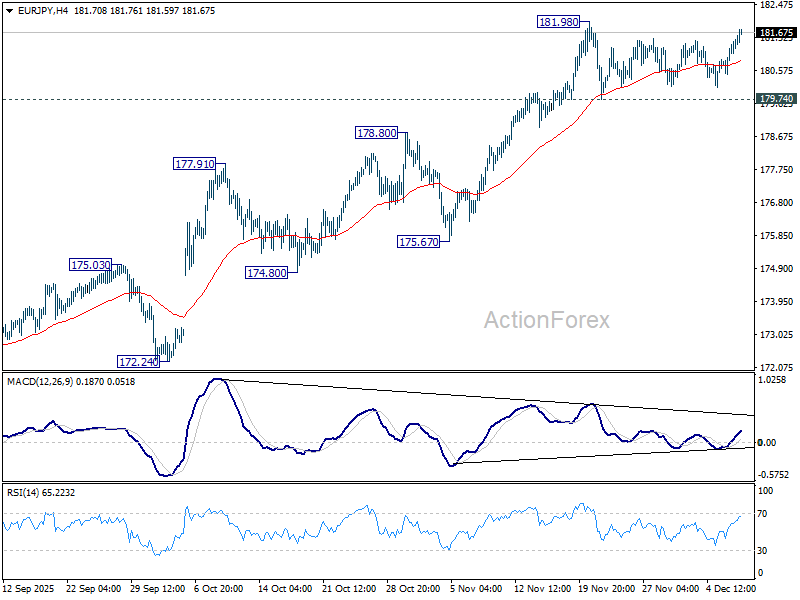

EUR/JPY Daily Outlook

Daily Pivots: (S1) 180.80; (P) 181.15; (R1) 181.81; More...

EUR/JPY is still bounded in range below 181.98 and intraday bias stays neutral. With 179.74 support intact, further rally is expected. On the upside, break of 181.98 will resume larger up trend to 100% projection of 161.06 to 173.87 from 171.09 at 183.90 next. However, firm break of 178.80 will argue that deeper correction is already underway towards 55 D EMA (now at 178.10).

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, considering bearish divergence condition in D MACD, upside should be capped by 186.31 on first attempt. Outlook will continue to stay bullish as long as 55 W EMA (now at 170.25) holds, even in case of deep pullback.

US JOLTs Report to Set the Stage for Tomorrow’s Fed Decision

In focus today

In the US, the delayed September JOLTs report is finally due for release in the afternoon. The number of job openings is a key measure of labour demand for the Fed, and the release will gather extra attention in light of the FOMC rate decision tomorrow. NFIB's small business optimism index for November and ADP's weekly private sector employment estimate will also be released today.

In Denmark, we expect foreign trade data and the current account for October. It will be interesting as exports remain the key driver of growth in Denmark.

In China, overnight, we will see CPI for November, which is expected to move more into positive territory (cons: 0.7% y/y, prior: 0.2% y/y). Core inflation has moved higher over the past six months as well. China still suffers from deflationary pressures in the producer prices, though, and PPI is expected to stay around -2.0% y/y in November.

Economic and market news

What happened overnight

In Australia, the Reserve Bank held its cash rate at 3.60%, citing upside inflation risks and recovering demand. Governor Michele Bullock noted the board is considering the likelihood of rate hikes in 2026 and has not ruled out an increase as soon as its next meeting in February. The move resulted in higher yields and a slightly stronger AUD.

What happened yesterday

In the US, President Trump announced that Nvidia's H200 chips will be allowed for export to China, with Nvidia required to pay a 25% fee on sales, up from the initial 15%. Trump claimed that President Xi reacted positively to the decision, despite China expressing scepticism about such a deal last week. The decision has faced criticism from US lawmakers, who raised concerns over national security and the risk of the chips being used for military purposes in China.

In the euro area, the December Sentix indicator came in slightly better than expected at -6.2 (cons: -7.0, prior: -7.4), indicating investors have gotten less pessimistic about the economic recovery. Given how Sentix is the first sentiment indicator for December, the rise could signal improvements in other sentiment indicators to be released this month.

In Germany, industrial production increased by 1.8% m/m in October, significantly exceeding expectations and marking the second consecutive monthly rise. Growth was driven by construction and manufacturing, while the automotive sector detracted. Despite this sign of short-term stabilisation, soft indicators remain cautious. The Ifo Index fell in November as weaker expectations outweighed a slight improvement in the current assessment, and the Manufacturing PMI dropped to 48.2, its sharpest contraction since February. This highlights that while production shows improvement, weak demand and sentiment suggest recovery remains dependent on the impact of fiscal easing measures.

Equities: Equities had a slow start to the week and generally ended somewhat lower. The S&P 500 closed down 0.4% and the Stoxx 600 slipped 0.1%. Interestingly, the selling was again concentrated in defensives, similar to Friday. Hence, it was a slow day but not risk off emerging. Futures are little changed this morning.

One standout style yesterday was momentum, which has regained traction both on the day and over the past two weeks. One driver is the ongoing TPU-vs-GPU battle between Alphabet and Nvidia, which appears to have stalled. Alphabet fell 2% yesterday, while Nvidia and Microsoft both gained around 2%. After the close, the Trump administration announced that some of Nvidia's chip exports (H200 AI chips) to China may resume, which might have contributed to the rotation.

Another notable sector is health care: A top performer over the past three months—up roughly 8% in global terms. However, it has also been the sector investors have found financing in during the recent rebound, falling about 3% the last two weeks. This contributes to the divergence between defensives and cyclicals, both in risk-off and risk-on phases. Strong recent performance has narrowed global health care's valuation discount to global equities from 20% earlier this year to about 9% today. That is still one standard deviation below the 10-year average of 0%, and so we continue to recommend an overweight in this sector but admit that the upside has declined.

FI and FX: Yields are grinding higher despite the expectations of a Fed rate cut on Wednesday. Markets are seemingly getting a bit worried that the cut will be delivered with a more hawkish communication, and risk sentiment has also been dented with small declines in US and Asian equity indices overnight. EUR/USD declined towards 1.1620 yesterday afternoon as US yields temporarily spiked around 16.00 CET. With yields subsequently moving lower, EUR/USD settled around 1.1640-1.1650. The RBA kept the policy rate on hold at 3.60% as widely expected and signaled that risks from here are on the upside, resulting in a bearish steepening of the curve with the 2y point rising 9bp and the 10y rising 5bp, along with a stronger AUD.

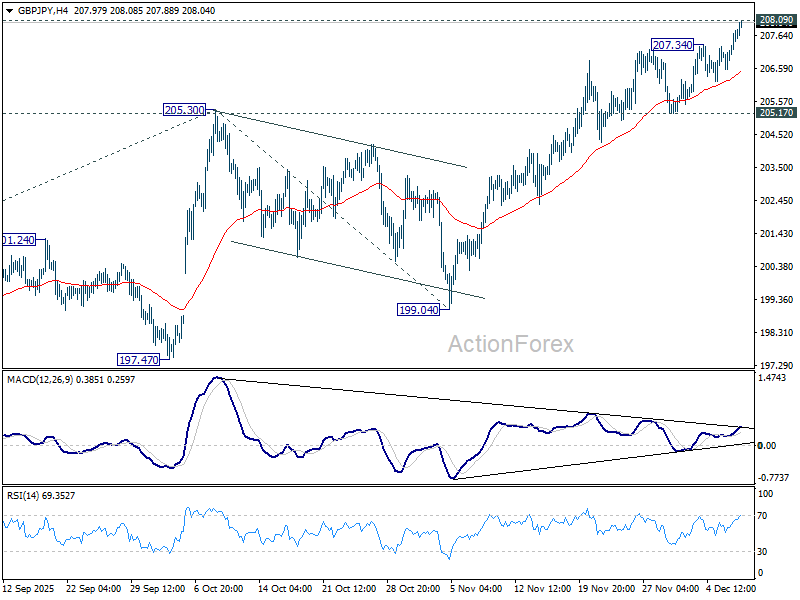

GBP/JPY Daily Outlook

Daily Pivots: (S1) 206.94; (P) 207.37; (R1) 208.16; More...

GBP/JPY's rally resumed after brief consolidations and it's now pressing 208.09 high. Intraday bias is back on the upside, and decisive break of 208.09 will confirm larger up trend resumption. Next near term target will be 61.8% projection of 184.35 to 205.30 from 199.04 at 211.98. Outlook will stay bullish as long as 205.17 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 199.04 support will dampen this view and extend the corrective pattern with another fall.

Markets Turn Cautious Ahead of FOMC as Talk of “Hawkish Cut” Builds

Global markets adopted a more cautious tone today, with Asian equities drifting lower after Wall Street’s soft session. The price action reflects hesitation rather than fear, with most investors choosing not to commit ahead of tomorrow’s critical FOMC outcome.

Talk has intensified that the Fed could deliver what many are calling a “hawkish cut.” A 25bps reduction to 3.50–3.75% is essentially a done deal, but the messaging around it may matter more. After three straight cuts aimed at stabilizing the labor markets, the Committee may use this meeting to telegraph that a long pause is now appropriate.

The Fed’s own estimates put neutral at 2.8–3.5%. Given inflation’s persistence, particularly in services and wages, policymakers may need to retain a modest level of restriction. This would limit the scope for additional cuts unless the disinflation trend strengthens, or labor market deterioration intensifies.

Meanwhile, equity sentiment may see pockets of relief today. Nvidia rallied after President Donald Trump posted on Truth Social that the chipmaker could ship its H200 processors to “approved customers” in China and elsewhere, provided a quarter of the sales revenue is paid to the U.S. government. Still, any bounce is likely to be temporary given the scale of event risk tied to tomorrow's FOMC projections and press conference.

In the currency markets, Aussie is the day’s strongest performer following the hawkish RBA hold. Governor Michele Bullock reaffirmed that there is no justification for further cuts and that the board is actively discussing the circumstances under which a hike could occur next year. Kiwi follows closely behind, with Swiss Franc also firm.

Yen, however, continues to underperform sharply. Governor Kazuo Ueda’s comment that confidence in the BoJ’s outlook is “increasing gradually” supports expectations of a December hike. But the market remains unconvinced that such a move would materially shift rate differentials, leaving JPY at the bottom of the pack. Dollar is the second-weakest major today, with Loonie also under pressure, while Euro and Sterling sit in the middle of the performance table.

In Asia, Nikkei rose 0.14%. Hong Kong HSI is down -1.24%. China Shanghai SSE is down -0.38%. Singapore Strait Times is up 0.02%. Japan 10-year JGB yield fell -0.007 to 1.966. Overnight, DOW fell -0.45%. S&P 500 fell -0.35%. NASDAQ fell -0.14%. 10-year yield rose 0.033 to 4.172.

RBA holds at 3.60% as Bullock signals no cuts, open to 2026 hike

RBA kept the cash rate unchanged at 3.60% today, as markets had fully priced. But the tone from Governor Michele Bullock was firmer than expected, pushing back against speculation of early-2026 easing. “Given what’s happening with underlying momentum in the economy … it does look like additional cuts are not needed,” she said, adding that she does not see rate cuts “on the horizon for the foreseeable future.”

While Bullock confirmed the board did not discuss a rate hike as an active policy option today, she stressed members spent “quite a lot” of time examining what conditions might force them to lift rates next year. The discussion centered on the persistence of inflation and how much further the economy needs to cool before the board can be confident price pressures are returning to target.

Asked whether a February rate increase is plausible, Bullock did not rule it out. She said the RBA will monitor whether inflation remains sticky: if inflation fails to move back toward target, “then I think that does raise questions about how tight financial conditions are and the board might have to consider whether or not it’s appropriate to keep interest rates where they are or in fact at some point raise them.” Any decision, she added, will be made “meeting by meeting.”

The accompanying statement echoed this mildly hawkish stance, noting that recent data show inflation risks have “tilted to the upside.” Although the board judges part of the recent lift in underlying inflation as driven by temporary factors, policymakers admit uncertainty about the new monthly CPI series and acknowledge signs of a “more broadly based pick-up” in price pressures that may prove persistent.

Labor market indicators continue to suggest conditions remain “a little tight.” While the Wage Price Index has eased from its peak, broader wage measures are still running strong, and unit labor costs remain high.

For now, the RBA is signaling a steady policy stance, but the barrier to easing has grown significantly while the door to a potential hike in 2026 is now visibly open.

AUD/JPY extends up trend as hawkish RBA fuel upside acceleration

AUD/JPY extended its advance today, with mild acceleration following the RBA’s hawkish hold. Governor Michele Bullock’s explicit dismissal of further rate cuts—and her acknowledgement that rate hikes could be on the table next year—provided the catalyst for renewed Aussie buying. Against this, persistent Yen softness remains a dominant background theme, with markets still doubting that a BoJ hike later this month will materially strengthen the currency.

Technically, the sustained break above the near-term rising channel ceiling signals that an upside acceleration phase is underway. The rise from 86.03 (2025 low) is now tracking toward 161.8% projection of 94.38 to 100.93 from 96.24 at 106.83. Outlook will stay firmly bullish with 100.93 resistance turned support intact, on any pullback.

In the bigger structure, the decisive break of 102.39 structure resistance confirms that corrective decline from 109.36 (2024 high) has ended with a three-wave drop to 86.03. It is still too early to determine whether the current rally is simply the second leg within a larger corrective pattern from 109.36, or the resumption of the long-term uptrend that began at 59.85 in 2020.

Either way, upside is favored while the 55 W EMA (now at 97.50) remains intact, for retesting 109.36. Yet, whether 109.36 gives way will be determined by the RBA’s timeline for tightening.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 206.94; (P) 207.37; (R1) 208.16; More...

GBP/JPY's rally resumed after brief consolidations and it's now pressing 208.09 high. Intraday bias is back on the upside, and decisive break of 208.09 will confirm larger up trend resumption. Next near term target will be 61.8% projection of 184.35 to 205.30 from 199.04 at 211.98. Outlook will stay bullish as long as 205.17 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 199.04 support will dampen this view and extend the corrective pattern with another fall.

AUD/JPY extends up trend as hawkish RBA fuel upside acceleration

AUD/JPY extended its advance today, with mild acceleration following the RBA’s hawkish hold. Governor Michele Bullock’s explicit dismissal of further rate cuts—and her acknowledgement that rate hikes could be on the table next year—provided the catalyst for renewed Aussie buying. Against this, persistent Yen softness remains a dominant background theme, with markets still doubting that a BoJ hike later this month will materially strengthen the currency.

Technically, the sustained break above the near-term rising channel ceiling signals that an upside acceleration phase is underway. The rise from 86.03 (2025 low) is now tracking toward 161.8% projection of 94.38 to 100.93 from 96.24 at 106.83. Outlook will stay firmly bullish with 100.93 resistance turned support intact, on any pullback.

In the bigger structure, the decisive break of 102.39 structure resistance confirms that corrective decline from 109.36 (2024 high) has ended with a three-wave drop to 86.03. It is still too early to determine whether the current rally is simply the second leg within a larger corrective pattern from 109.36, or the resumption of the long-term uptrend that began at 59.85 in 2020.

Either way, upside is favored while the 55 Wk EMA (now at 97.50) remains intact, for retesting 109.36. Yet, whether 109.36 gives way will be determined by the RBA’s timeline for tightening.

RBA holds at 3.60% as Bullock signals no cuts, open to 2026 hike

RBA kept the cash rate unchanged at 3.60% today, as markets had fully priced. But the tone from Governor Michele Bullock was firmer than expected, pushing back against speculation of early-2026 easing. “Given what’s happening with underlying momentum in the economy … it does look like additional cuts are not needed,” she said, adding that she does not see rate cuts “on the horizon for the foreseeable future.”

While Bullock confirmed the board did not discuss a rate hike as an active policy option today, she stressed members spent “quite a lot” of time examining what conditions might force them to lift rates next year. The discussion centered on the persistence of inflation and how much further the economy needs to cool before the board can be confident price pressures are returning to target.

Asked whether a February rate increase is plausible, Bullock did not rule it out. She said the RBA will monitor whether inflation remains sticky: if inflation fails to move back toward target, “then I think that does raise questions about how tight financial conditions are and the board might have to consider whether or not it’s appropriate to keep interest rates where they are or in fact at some point raise them.” Any decision, she added, will be made “meeting by meeting.”

The accompanying statement echoed this mildly hawkish stance, noting that recent data show inflation risks have “tilted to the upside.” Although the board judges part of the recent lift in underlying inflation as driven by temporary factors, policymakers admit uncertainty about the new monthly CPI series and acknowledge signs of a “more broadly based pick-up” in price pressures that may prove persistent.

Labor market indicators continue to suggest conditions remain “a little tight.” While the Wage Price Index has eased from its peak, broader wage measures are still running strong, and unit labor costs remain high.

For now, the RBA is signaling a steady policy stance, but the barrier to easing has grown significantly while the door to a potential hike in 2026 is now visibly open.

(RBA) Statement by the Reserve Bank Board: Monetary Policy Decisions

At its meeting today, the Board decided to leave the cash rate unchanged at 3.60 per cent.

While inflation has fallen substantially since its peak in 2022, it has picked up more recently. The Board’s judgement is that some of the recent increase in underlying inflation was due to temporary factors and there is uncertainty about how much signal to take from the monthly CPI data given it is a new data series. Nevertheless, the data do suggest some signs of a more broadly based pick-up in inflation, part of which may be persistent and will bear close monitoring.

Economic activity continues to recover. Growth in private demand has strengthened, driven by both consumption and investment. Activity and prices in the housing market are also continuing to pick up. Financial conditions have eased since the beginning of the year, credit is readily available to both households and businesses and the effects of earlier interest rate reductions are yet to flow through fully to demand, prices and wages. On the other hand, money market interest rates and government bond yields have risen more recently.

Various indicators suggest that labour market conditions remain a little tight. The unemployment rate has risen gradually over the past year and employment growth has slowed. However, measures of labour underutilisation remain at low rates, surveyed measures of capacity utilisation are above their long-run average and business surveys and liaison continue to suggest that a significant share of firms are experiencing difficulty sourcing labour. Wages growth, as measured by the Wage Price Index, has eased from its peak but broader measures of wages continue to show strong growth and growth in unit labour costs remains high.

There are uncertainties about the outlook for domestic economic activity and inflation and the extent to which monetary policy remains restrictive. On the domestic side, the pick-up in momentum has been stronger than anticipated, particularly in the private sector. If this continues, it is likely to add to capacity pressures. Uncertainty in the global economy remains significant but so far there has been minimal impact on overall growth and trade in Australia’s major trading partners.

Decision

The recent data suggest the risks to inflation have tilted to the upside, but it will take a little longer to assess the persistence of inflationary pressures. Private demand is recovering. Labour market conditions still appear a little tight but further modest easing is expected. The Board therefore judged that it was appropriate to remain cautious, updating its view of the outlook as the data evolve.

The Board will be attentive to the data and the evolving assessment of the outlook and risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board is focused on its mandate to deliver price stability and full employment and will do what it considers necessary to achieve that outcome.

Today’s policy decision was unanimous.

FOMC Meeting Preview: How FOMC’s December Dot Plot Will Affect the US Dollar (DXY)

The meeting of the Federal Open Market Committee (FOMC) on December 10, 2025, is a highly important final decision of the year that will determine the immediate direction of interest rates and set expectations for next year's monetary policy. This event is unusually difficult to predict because the policymakers are facing conflicting economic reports such as a softening job market versus still-elevated inflation and are significantly divided over what action to take.

In short, it is the year's last major rate decision, and the mixed signals and internal disagreements among the committee members make the outcome exceptionally unpredictable.

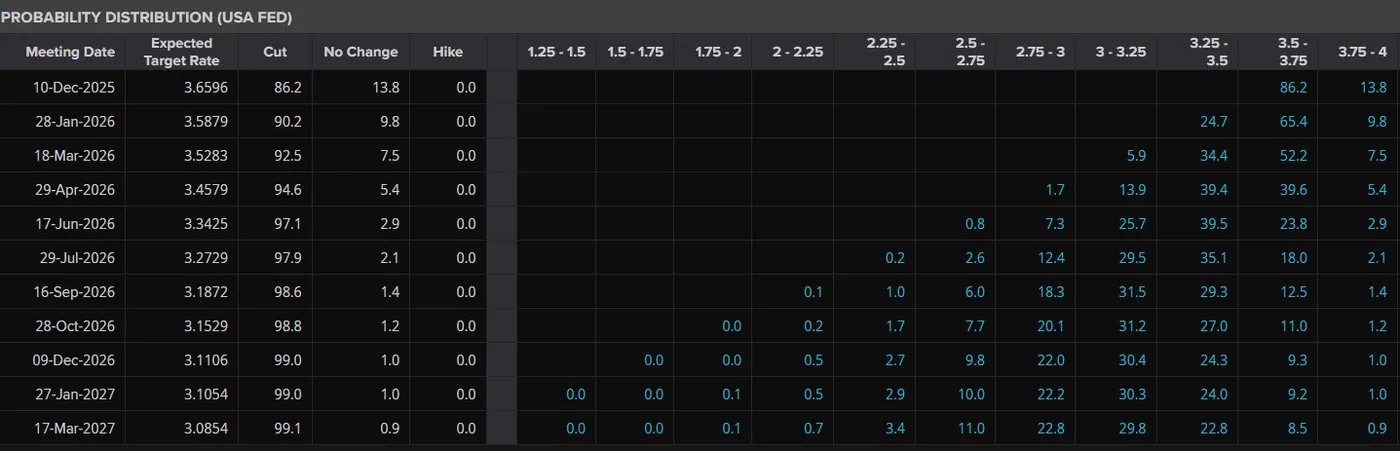

Interest Rate Probabilities Ahead of FOMC

Source: LSEG

Navigating Without a Compass

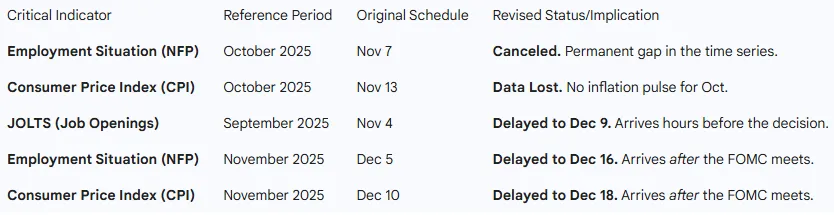

The importance of the December 2025 decision is made much harder by the fact that the Federal Reserve (the Fed) is essentially flying blind right now. The Fed usually bases its decisions on the latest government data about jobs and inflation, but a recent six-week government shutdown has completely stopped the publication of these key statistics. Because of this, the FOMC is meeting on December 10th without any official government inflation or jobs data since September.

The Fed have been forced to rely on unofficial, "private" reports, like the recent ADP report which showed a worrying loss of 32,000 jobs. If this private data is accurate, the Fed needs to cut rates immediately to avoid a recession, but if the private data is wrong, cutting rates could cause inflation to surge again.

Data Void and Release Dates

Source: LSEG

This lack of data forces the Fed to confront the two parts of its mission: keeping prices stable (low inflation) and supporting maximum employment (low unemployment) which are now in direct conflict.

On the one hand, the labor market is showing dangerous cracks. While the unemployment rate is currently 4.4%, the speed at which it's rising is setting off a major recession warning signal, known as the "Sahm Rule." This situation argues for an immediate rate cut to prevent a potential "hard landing" recession. On the other hand, the fight against inflation is not over.

Inflation, as measured by the Fed's preferred index, is stuck at 2.8%, which is almost a full percentage point above their 2.0% target. Cutting rates now could cause inflation to rebound, especially with the potential for new government spending and tariffs. Because they lack the recent data to settle this argument, the December meeting has become a battle between policymakers' opposing fears: the "doves" worry more about a recession, while the "hawks" worry more about runaway inflation.

The Decision Matrix: Potential Scenarios

Despite the economic confusion, the majority of market participants expect the FOMC to make a "safety cut" of 25 basis points (a quarter of a percent). The logic is that this small cut is an insurance policy against the job market completely collapsing, but it's not so large that it fully gives up the fight against inflation.

However, this market consensus hides a major disagreement within the Committee itself. Analysts predict a historically high number of dissenting votes (policymakers who vote against the decision), which would signal to investors that Chair Powell has lost control of the policy message and would introduce a lot of uncertainty for the following year.

The "Dot Plot" Battlefield

The real fight isn't just about the current rate cut, but about the communication of future interest rates. This is shown in the "Dot Plot" , a chart that shows where each Fed member expects the interest rate to be in 2026 and beyond. The market is currently expecting the Fed to cut rates roughly four times in 2026, which would send the stock market soaring (the Bull Case). But some forecasters predict the Dot Plot will show a median expectation of only two cuts for 2026. This would be a "hawkish cut" meaning the Fed cuts now but signals they are nearly done which would severely disappoint the market and could lead to a drop in stock prices.

The "Powell Put" vs. The "Trump Call"

The political dimension of this meeting cannot be overstated. With the transition of power looming in January 2026, the Federal Reserve is under intense scrutiny. President-elect Trump has advocated for lower rates to offset his proposed tariff regime. Powell must navigate the optics of appearing politically independent.

If he cuts aggressively, he risks accusations of juicing the economy for the incoming administration or bowing to political pressure.

If he holds, he risks accusations of sabotaging the economic handover. This political shadow suggests Powell will likely opt for the middle path: a 25bps cut (to satisfy the growth mandate) coupled with stern language about data dependence (to satisfy the inflation mandate).

Market Implications: The US Dollar and Global FX

The Dollar's Dilemma

The US Dollar (DXY) is currently caught between cyclical weakness and structural strength. Seasonally, December is a weak month for the Greenback. However, the medium-term outlook is dominated by the concept of divergence.

The Bear Case for USD: The Fed cuts rates, acknowledging a slowing US economy. The yield advantage that the Dollar enjoys over the Euro and Yen erodes. Simultaneously, the uncertainty regarding the next Fed Chair potentially the dovish Kevin Hassett leads markets to price in a "lower for longer" regime. This pushes EUR/USD back toward 1.15.

The Bull Case for USD (The Disappointment Trade): This is the more nuanced risk. The market is pricing in aggressive cuts for 2026. If the Fed's Dot Plot pushes back, signaling "patience," yields at the short end of the US curve (2-year Treasury) will spike. This would catch Dollar bears offside, triggering a short squeeze that rallies the DXY.

Furthermore, if the US economy continues to grow at 2% while the Eurozone stagnates, the "US Exceptionalism" trade remains the dominant force, putting a floor under the Dollar.

US Dollar Index (DXY) Daily Chart, December 8, 2025

Source: TradingView.Com (click image to enlarge).

Bitcoin Trades Sideways as Market Builds Tension for Next Major Move

Key Highlights

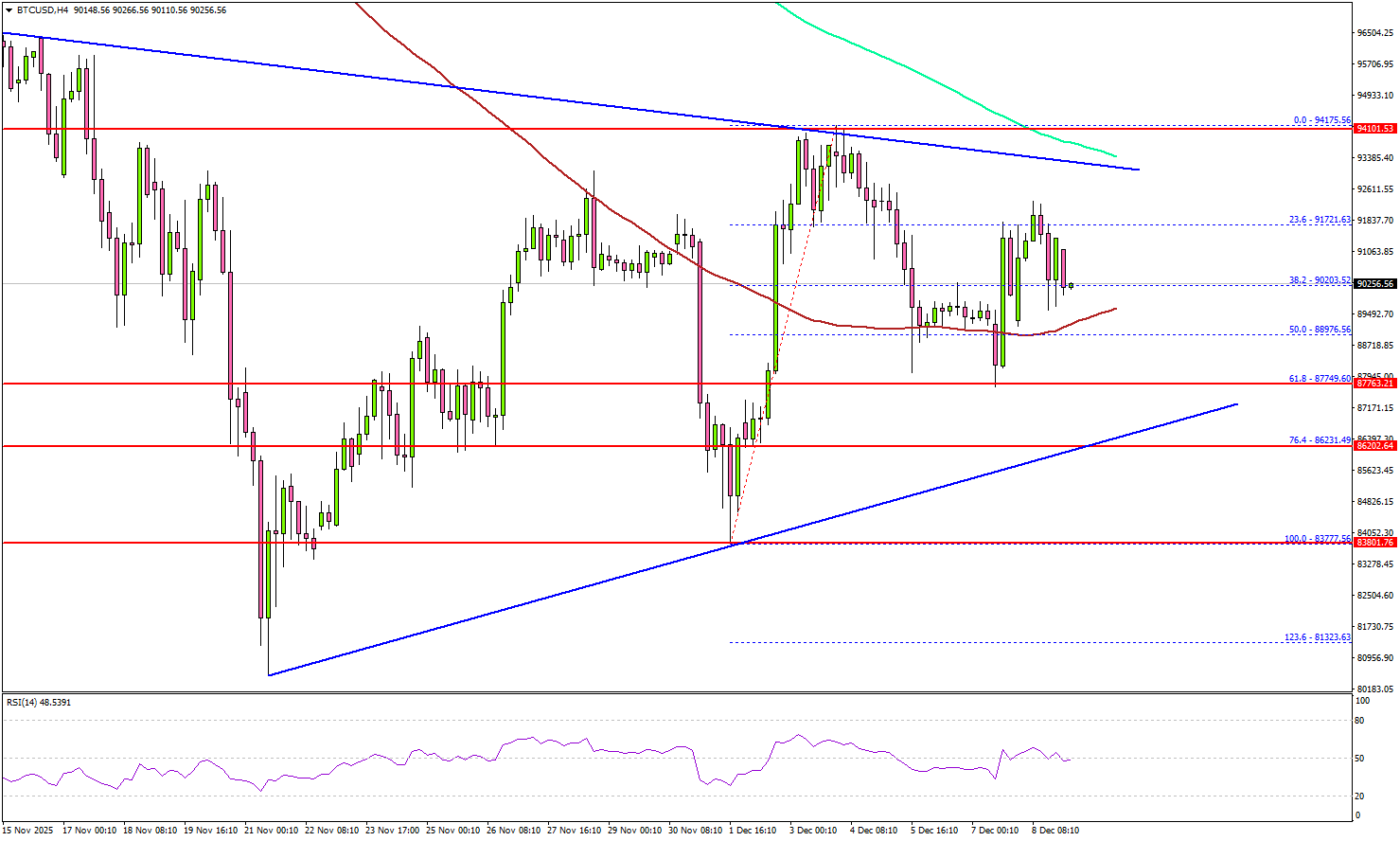

- Bitcoin started a recovery wave above $88,000 and $90,000.

- BTC/USD is trading inside a key contracting triangle with resistance at $93,000 on the 4-hour chart.

- Ethereum also started a decent increase above $3,050.

- XRP price is struggling to settle above the $2.20 resistance.

Bitcoin Price Technical Analysis

Bitcoin price found support near $83,800 and started a recovery wave against the US Dollar. BTC climbed above $88,000 and $90,000 to enter a short-term positive zone.

Looking at the 4-hour chart, the price even surpassed $92,000 before it faced sellers near $94,200. Recently, there was a pullback below $92,000, and the 50% Fib retracement level of the recovery wave from the $83,777 swing low to the $94,175 high.

However, the bulls are active near $88,000, the 100 simple moving average (red, 4-hour), and the 61.8% Fib retracement. On the upside, BTC is facing resistance near $93,000 and the 200 simple moving average (green, 4-hour). There is also a key contracting triangle with resistance at $93,000 on the same chart.

A successful close above $93,000 might start another steady increase. In the stated case, the price may perhaps rise toward the $95,500 level. Any more gains might call for a test of $97,000.

Immediate support sits at $90,000. A downside break below $90,000 might start another decline. The next major support is $88,000. Any more losses might call for an extended decline toward the $86,500 support zone.

Looking at Ethereum, the price was able to follow Bitcoin and climbed above the $3,120 resistance region.

Today’s Key Economic Releases

- US ADP Employment Change 4-week average - Forecast 5K, versus -13.5K previous.