Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.22; (P) 155.61; (R1) 156.31; More...

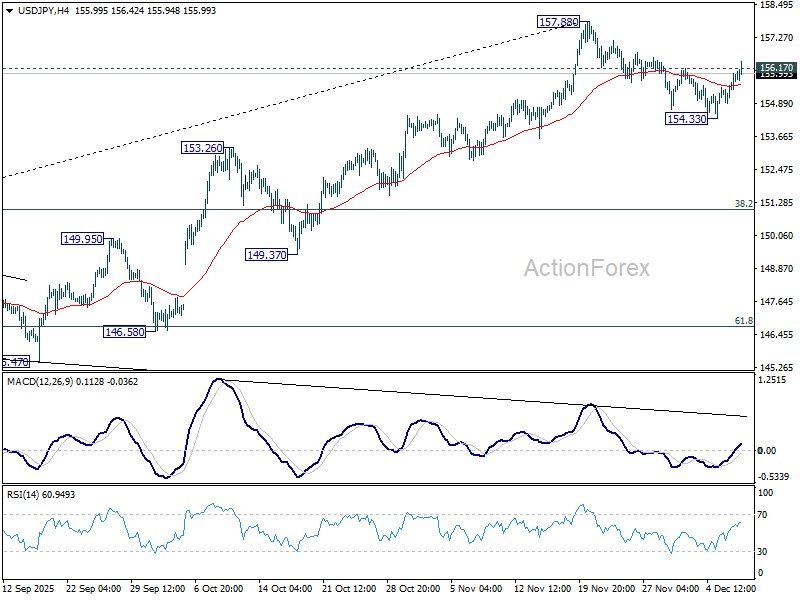

USD/JPY's breach of 156.17 resistance suggests that corrective pullback from 157.88 has completed at 154.33. Intraday bias is back on the upside for retesting 157.88 high. Firm break there will resume larger rally to 158.85 structural resistance. For now, risk will stays mildly on the upside as long as 154.33 support holds, in case of retreat.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3303; (P) 1.3325; (R1) 1.3344; More...

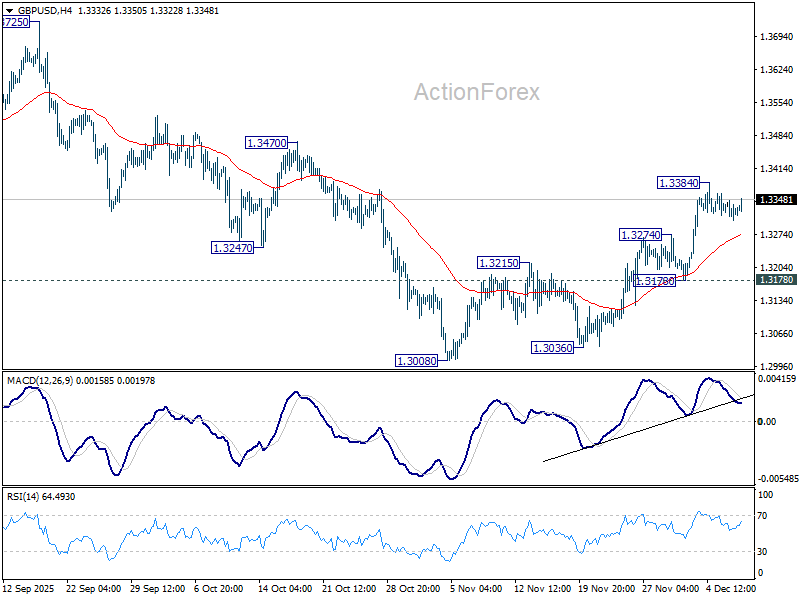

Intraday bias in GBP/USD remains neutral for consolidations below 1.3384 temporary top. With 1.3178 support intact, further rally is still expected. As noted before, fall from 1.3787 should have completed as a three-wave correction to 1.3008. On the upside, above 1.3384 will target 1.3470 resistance. Decisive break there will bring retest of 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

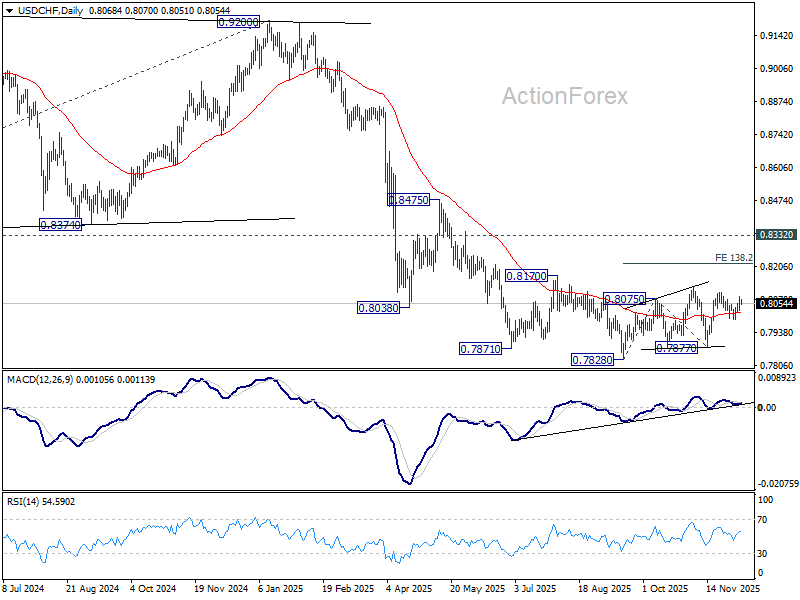

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8035; (P) 0.8061; (R1) 0.8093; More…

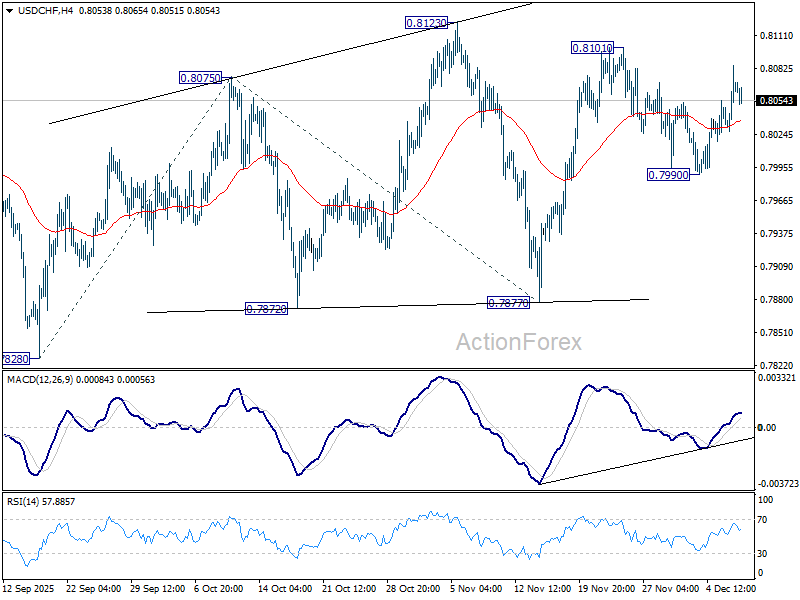

Intraday bias in USD/CHF remains mildly on the upside for 0.8101 and then 0.8123 resistance. . As noted before, price actions from 0.7828 are developing into a corrective pattern. Firm break of 0.8123 will target 138.2% projection of 0.7828 to 0.8075 from 0.7877 at 0.7812. For now, risk will stay on the upside as long as 0.7990 support holds, in case of retreat.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

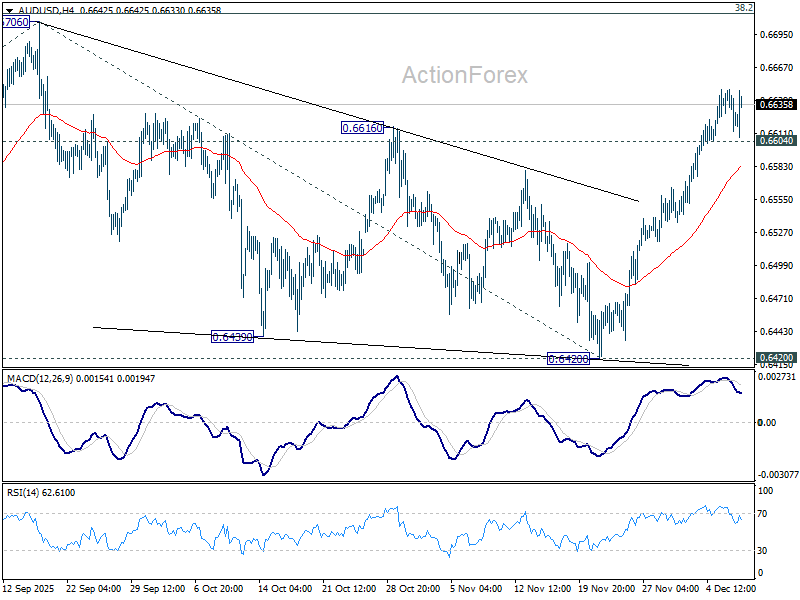

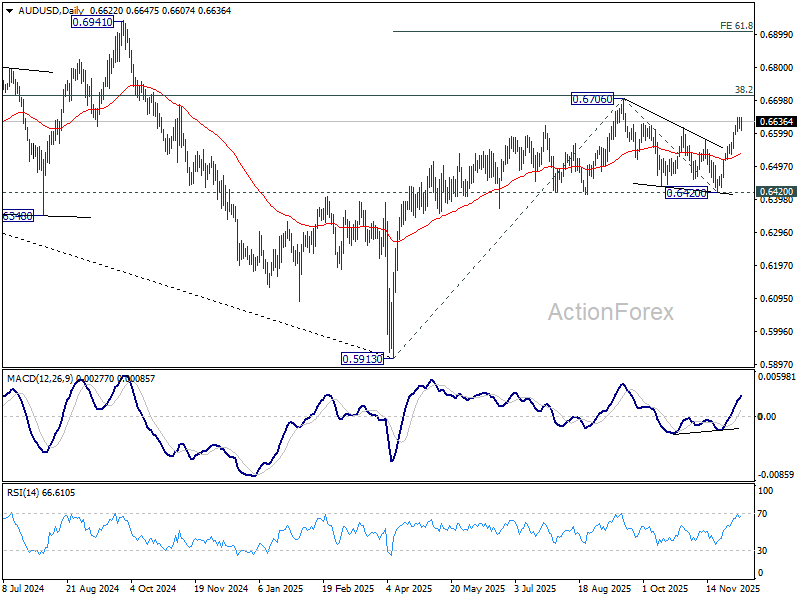

AUD/USD Daily Report

Daily Pivots: (S1) 0.6610; (P) 0.6630; (R1) 0.6644; More...

Intraday bias in AUD/USD stays mildly on the upside at this point. Rise from 0.6420 is in progress for retesting 0.6706 high. Decisive break there will confirm and target 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. On the downside, below 0.6604 minor support will turn intraday bias neutral and bring consolidations, before staging another rise.

In the bigger picture, the break of multi-year falling trend line resistance suggests that rise from 0.5913 is possibly reversing whole down trend from 08006 (2021 high). Decisive break of 38.2% retracement of 0.8006 to 0.5913 at 0.6713 will solidify this case, and bring further rally to 61.8% retracement at 0.7206. On the downside, however, firm break of 0.6420 support will suggest rejection by 0.6713 and retain medium term bearishness.

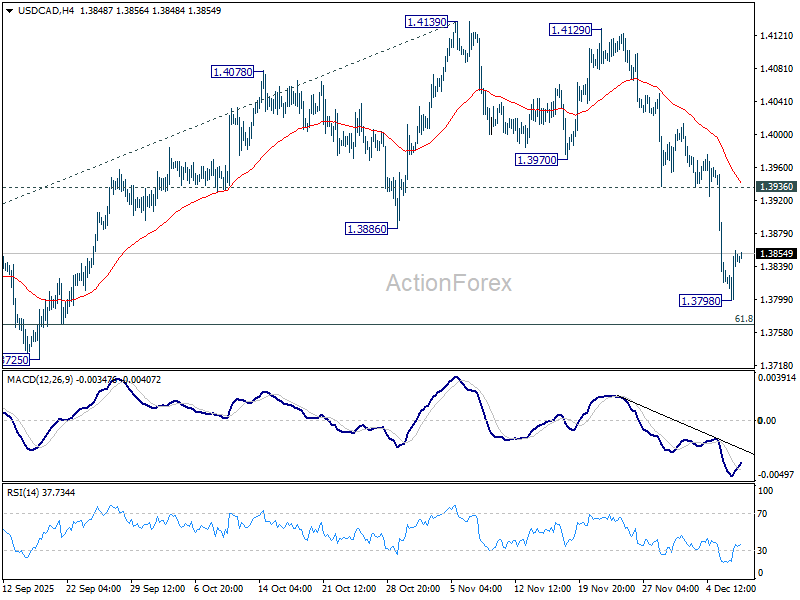

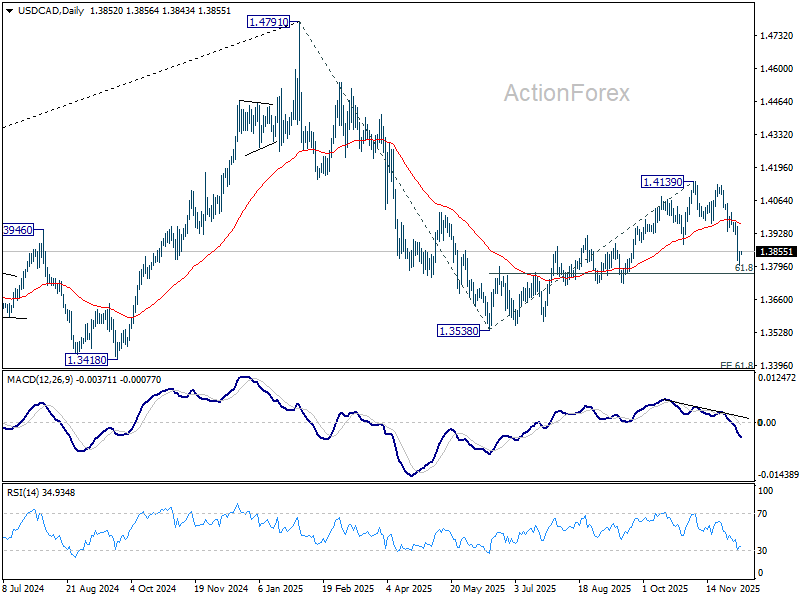

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3819; (P) 1.3840; (R1) 1.3879; More...

Intraday bias in USD/CAD is turned neutral with current recovery, and more consolidations could be seen above 1.3798 temporary low. Further decline is expected as long as 1.3936 support turned resistance holds. On the downside, below 1.3798 will resume the fall from 1.4139 to 61.8% retracement of 1.3538 to 1.4139 at 1.3768. Firm break there will argue that whole decline form 1.4791 might be ready to resume through 1.3538 low.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it's just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.

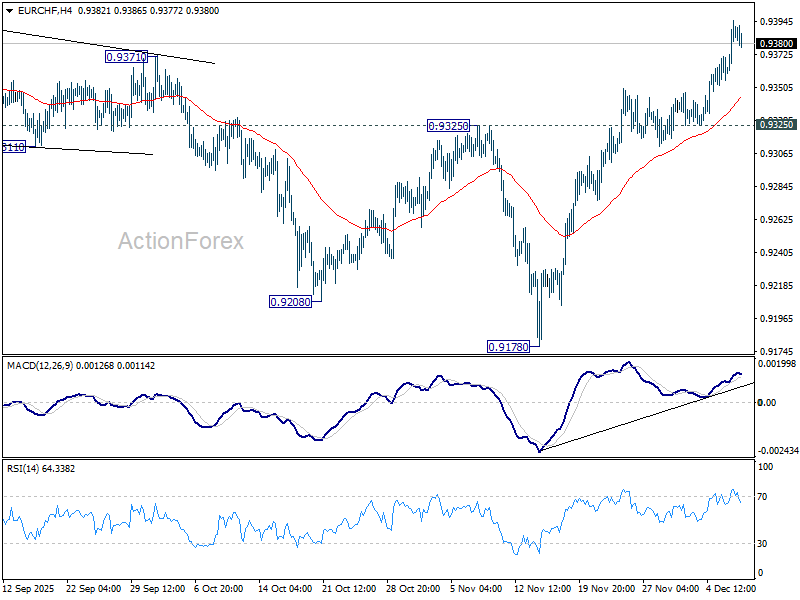

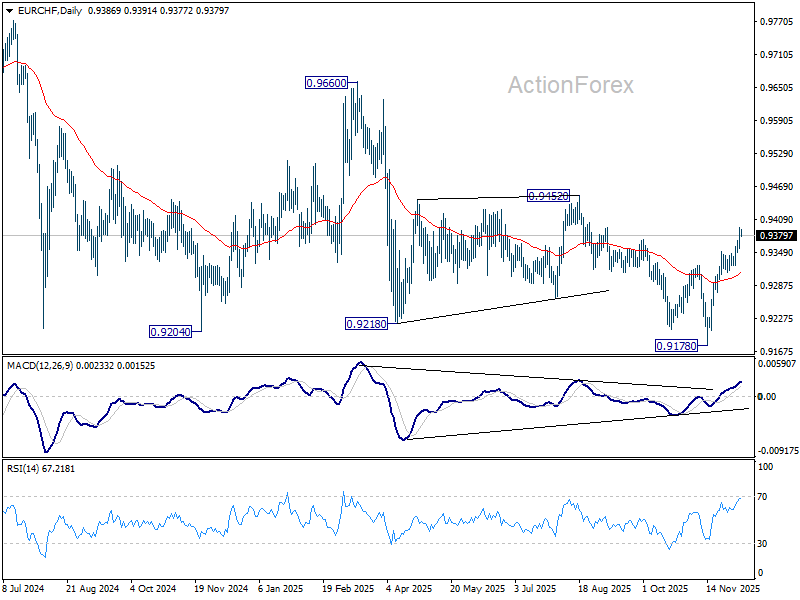

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9368; (P) 0.9382; (R1) 0.9404; More....

EUR/CHF's rally from 0.9178 is in progress and intraday bias stays on the upside for 0.9452 key structural resistance. Decisive break there will carry larger bullish implications. For now, risk will stay on the upside as long as 0.9325 support holds, in case of retreat.

In the bigger picture, EUR/CHF has breached long term falling channel resistance as the rebound from 0.9278 extends. Considering bullish convergence condition in W MACD, sustained trading above 55 W EMA (now at 0.9372) will indicate medium term bottoming, and suggests that it's already in larger scale rebound. Further break of 0.9452 resistance will bring stronger medium term rally towards 0.9228 resistance next. Nevertheless, rejection by 55 W EMA will retain bearishness for another fall through 0.9278 at a later stage.

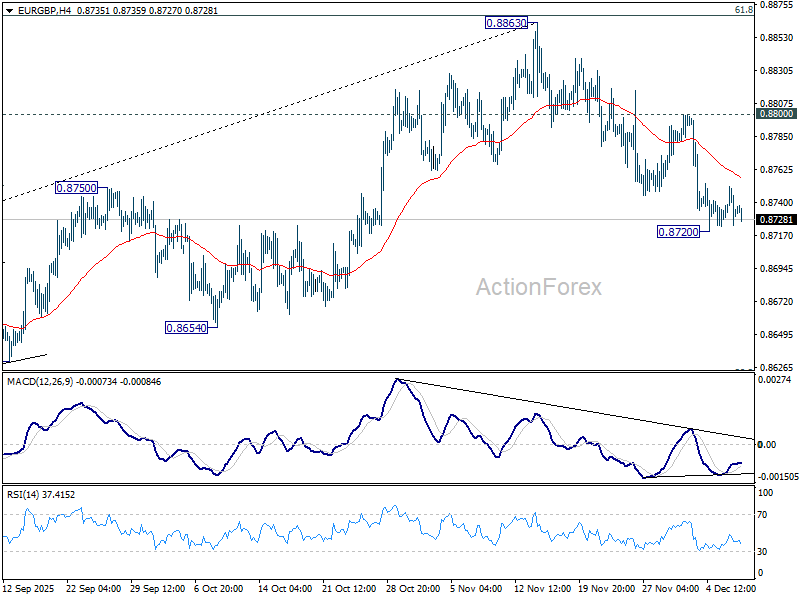

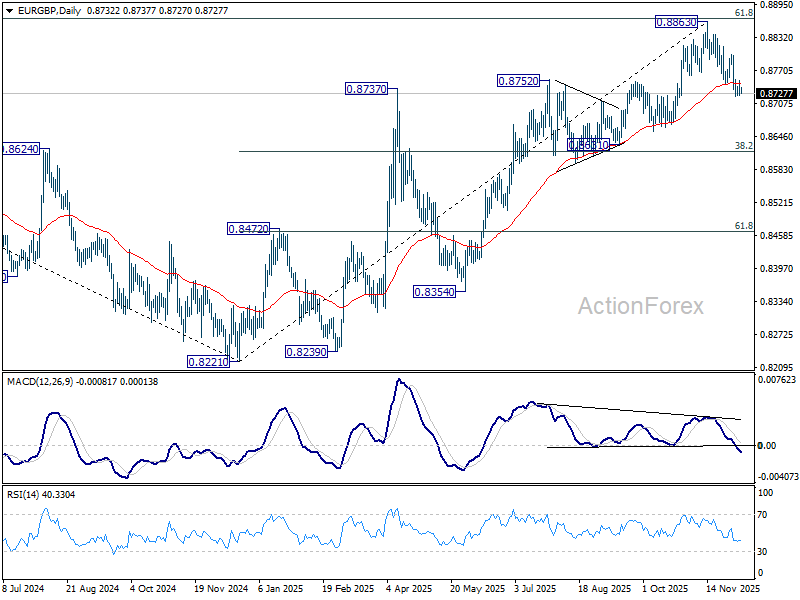

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8722; (P) 0.8738; (R1) 0.8750; More…

Intraday bias in EUR/GBP stays neutral for consolidations and with 0.8800 resistance intact, further decline is expected. Fall from 0.8863 should at least be a correction to the up trend from 0.8221, with risk of bearish reversal. Below 0.8720 will target 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618).

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8600) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

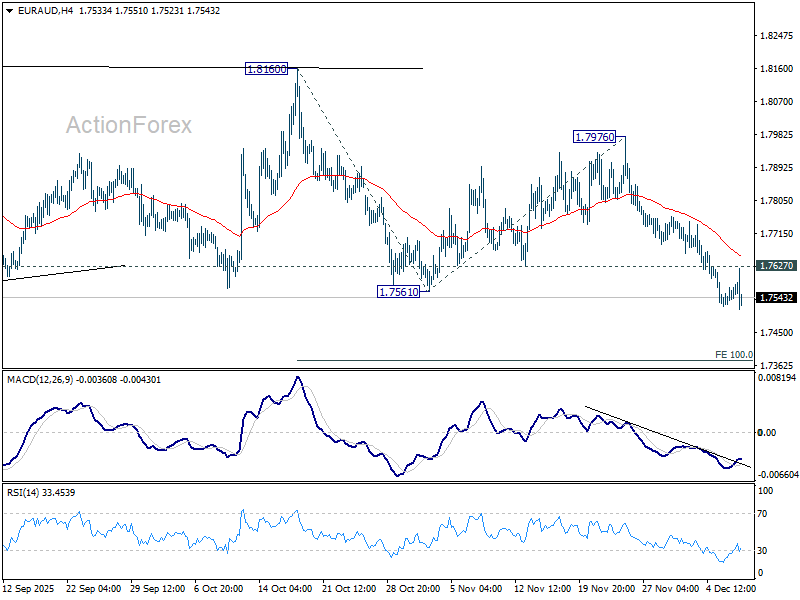

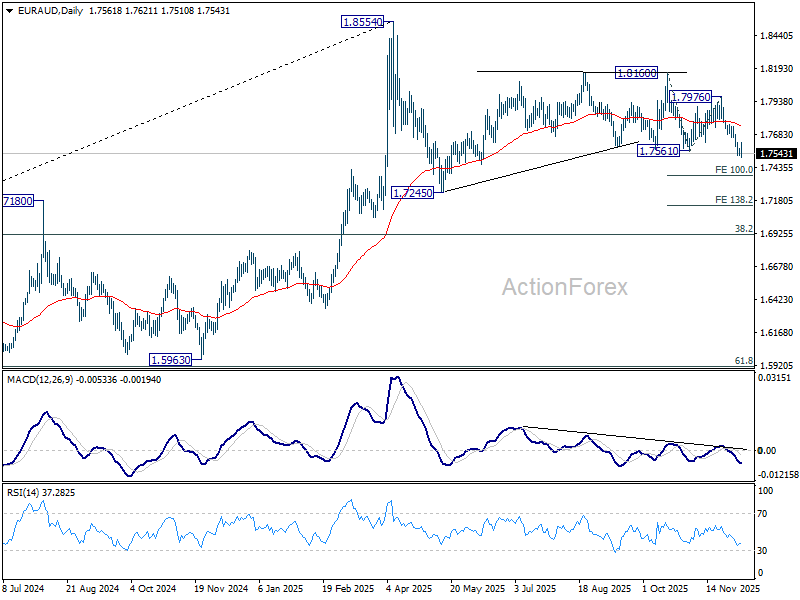

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7499; (P) 1.7565; (R1) 1.7599; More...

No change in EUR/AUD"s outlook and intraday bias stays on the downside. Fall from 1.8160 is seen as the third leg of the pattern from 1.8554. Deeper decline should be seen to 100% projection of 1.8160 to 1.7561 from 1.7976 at 1.7377. Firm break there will pave the way to 138.2% projection at 17148. On the upside, above 1.7627 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, as long as 55 W EMA (now at 1.7456) holds, price actions from 1.8554 could still be a correction to rise from 1.5963 only. However, sustained break of the EMA will argue that it's already correcting the whole up trend from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922.

Gold on Pause Awaiting the Fed’s Verdict

Gold is trading in a holding pattern near 4,200 USD per ounce on Tuesday, as markets remain in a state of suspended animation ahead of the Federal Reserve’s policy decision.

While a 25-basis-point rate cut is almost fully priced in, investors will scrutinise the updated economic projections and Chair Jerome Powell’s subsequent press conference for clarity on the policy trajectory into 2026 and beyond.

Market-implied probabilities currently assign an 87% likelihood to a cut today. However, expectations for future easing have moderated, with just two rounds of cuts now anticipated for next year, down from three a week ago.

Before the Fed announcement, traders will also assess the latest JOLTS job openings data for additional labour market insights.

In a supportive development for the metal, the People’s Bank of China expanded its gold reserves for the 13th consecutive month, bringing its total holdings to 74.12 million troy ounces.

Technical Analysis: XAU/USD

H4 Chart:

On the H4 chart, XAU/USD continues to consolidate in a sideways range following its late-November advance. The price is currently trading below the middle Bollinger Band, suggesting a gradual loss of bullish momentum. The upper band has flattened, confirming the consolidation phase within the 4,163–4,240 USD zone.

Support at 4,163 USD remains critical, with the price having rebounded from this level multiple times in recent sessions. A decisive break below would open the way to the next significant support near 4,136 USD, which aligns with the lower Bollinger Band.

Resistance is clearly defined at 4,240 USD. A sustained move above this level would provide the first strong signal for a renewed upward move, initially targeting 4,265 USD.

H1 Chart:

On the H1 chart, gold shows a near-term bearish bias after failing to break above resistance at 4,240 USD. The price is consistently positioned below the middle Bollinger Band, with the lower band reinforcing the selling pressure. Local support has solidified around 4,163 USD, a level tested repeatedly in recent trading.

The Stochastic oscillator remains near oversold territory, indicating weak momentum, though a clear reversal signal has yet to emerge.

Should buyers defend the 4,163 USD support and propel the price back above the middle Bollinger Band, a recovery toward 4,200 USD and later 4,240 USD would become likely. Conversely, a breakdown below 4,163 USD would signal a deeper corrective move toward 4,136–4,100 USD.

Conclusion

Gold remains in a state of cautious equilibrium as traders await the Fed’s policy signal and updated economic forecasts. While underlying physical demand – particularly from central banks – continues to provide a supportive floor, the technical picture reflects consolidation with a slight near-term bearish tilt.

RBA Holds Cash Rate at 3.6%, Focused on Upside

The RBA kept the cash rate on hold as expected. The Board was slightly more hawkish but Governor Bullock was firmly focused on the upside risks to inflation. We are less convinced that capacity constraints will be an issue for inflation, which could bring back the debate for rate cuts.

- As widely expected, the RBA kept the cash rate on hold at 3.6% in a unanimous decision. The statement struck a slightly more hawkish note but in the following media conference Governor Michele Bullock was focused on the upside risks to inflation.

- Following the media conference, the probability of a rate hike has risen. But we see this to be dependent on data over the coming months and a more likely scenario is a prolonged pause.

- Rate cuts could still be brought back to the table if our view that supply will not be a constraint and the economy can grow faster without triggering inflation is realised.

- As such, our current baseline is for two 25bp rate cuts but not until mid-2026. This would bring the cash rate to 3.1% –125bp below its peak this monetary policy cycle.

Today’s decision by the RBA to leave the cash rate unchanged at 3.6% was widely anticipated by the market and economists. It was a unanimous decision. The statement struck a slightly more hawkish note but in the following media conference, Governor Bullock indicated that the Board was focused on the upside risks to inflation.

She confirmed that at today’s meeting “a rate cut was not on the table”, adding that supply and demand conditions are a little tight. The potential necessary conditions for a rate hike in 2026 were also discussed as the Board believe the balance of risks for inflation have tilted to the upside.

While the Board acknowledged that some of the recent increase in underlying inflation was due to temporary factors, they still saw some signs of a broader pick-up. They also remain concerned over labour market tightness and strong growth in broader measures of wages and high unit labour costs.

They will continue to monitor these factors against a backdrop of what they believe to be a stronger pick up in private demand that could lead to capacity pressures.

But as our Chief Economist Luci Ellis recently noted in “Swing up, you won’t hit a wall”, the view that stronger private demand will quickly collide with supply constraints is misplaced. Indeed, we think the RBA and some other economists’ projection of trend growth of 2% is too conservative. We see 2¼% or higher as realistic given population, participation, and potential productivity gains.

There is no denying that overall productivity has been very weak. But as we have previously highlighted, this in part reflects the rapid increase in the share of the care economy over recent years, which is very labour intensive and mechanically less productive than the market sector. But as private demand and the market sector become an increasing driver of economic growth, this will support an improvement in headline productivity measures. This is not just a shift in the composition of the economy. The recovery in business investment, as seen in the Q3 National Accounts, and the solid lift in private business capex intentions will see the share of business investment lift from its historical lows. With more capital per worker, we will see stronger productivity. Then there is the technological innovation and adoption, including an eventual lift from AI.

It is also worth noting that the economy is not booming. Real disposable income per person has only just returned to 2020 levels, the stimulatory impact of Stage 3 tax cuts are rolling off and with rates on hold for longer, the boost from earlier rate cuts will also fade.

Overall, we do not expect the economy to hit a hard capacity wall any time soon. If this view proves correct, the economy can grow faster without triggering further inflation, reducing the need for slightly restrictive policy.

Indeed, we expect core inflation to ease back toward, and eventually below, the mid-point of the target band by the end of 2026. Much of the recent increase reflects higher administrative prices, seasonal volatility and the removal of cost-of-living assistance. These are unlikely to be repeated to the same extent. Further out, as productivity improves and wage inflation moderates this will also support lower core inflation.

As such, our current baseline is for two more 25bp rate cuts but not until mid-2026. This would bring the policy rate to 3.1% – 125bp below its peak this monetary cycle.

Still, following Governor Bullock’s comments in today’s press conference, the probability of a rate hike has risen. This would be dependent on persistence of the current reacceleration in inflation. Instead, we see the risks as being more tilted to a prolonged pause. The evolution of the data over the coming months will see the RBA reassess the sustainability of inflation moving back to target and the restrictiveness of current policy settings.