Sample Category Title

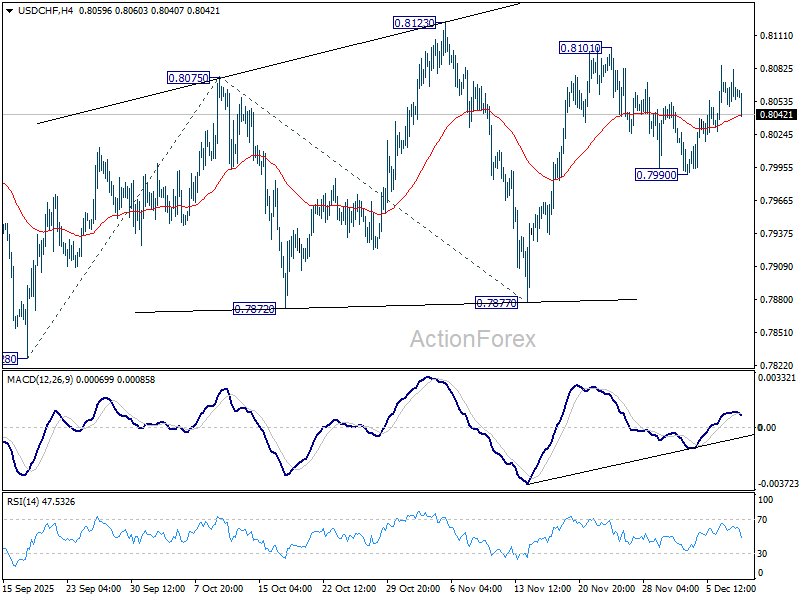

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8047; (P) 0.8065; (R1) 0.8080; More…

Intraday bias in USD/CHF is turned neutral again with current dip. Overall outlook is unchanged that price actions from 0.7828 are developing into a corrective pattern. Risk is mildly on the upside as long as 0.7990 support holds. Firm break of 0.8123 will target 138.2% projection of 0.7828 to 0.8075 from 0.7877 at 0.7812. However, break of 0.7990 support will turn bias back to the downside for 0.7877 support.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

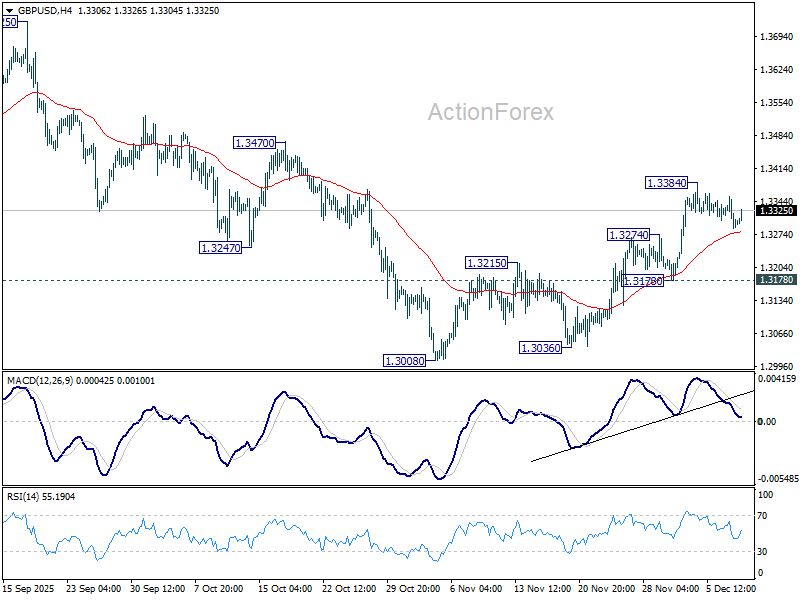

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3271; (P) 1.3314; (R1) 1.3339; More...

GBP/USD is still bounded in consolidations below 1.3384 temporary top and intraday bias stays neutral. With 1.3178 support intact, further rally is expected. As noted before, fall from 1.3787 should have completed as a three-wave correction to 1.3008. On the upside, above 1.3384 will target 1.3470 resistance. Decisive break there will bring retest of 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

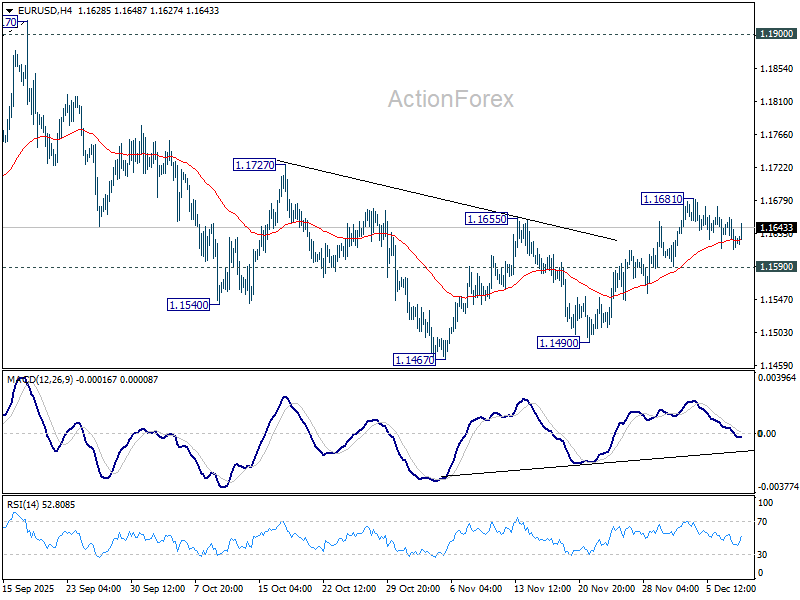

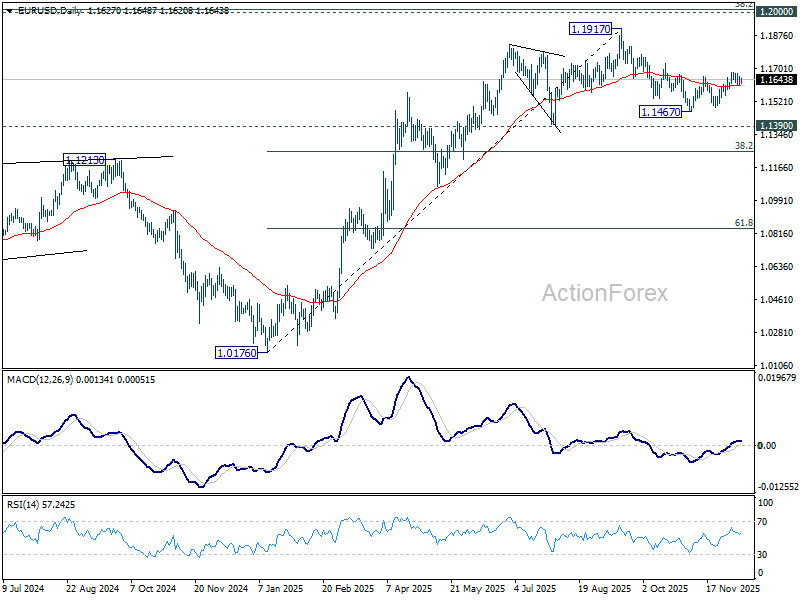

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1608; (P) 1.1633; (R1) 1.1650; More….

EUR/USD recovered after hitting 55 4H EMA but stays below 1.1681 temporary top. Intraday bias stays neutral at this point. Further rally is in favor with 1.1590 minor support intact. Corrective fall from 1.1917 could have completed at 1.1467. Above 1.1681 will target 1.1727 resistance first. Firm break there will solidify this case and bring retest of 1.1917 high. However, break of 1.1590 will revive near term bearishness, and bring retest of 1.1467 low.

In the bigger picture, as long as 55 W EMA (now at 1.1346) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Markets Stand Still Ahead of Fed; Trump’s Chair Search Adds Intrigue

The forex market was subdued through Asian session, mirroring the quiet tone in regional equities. With a major event risk just hours away, traders showed little appetite to adjust positioning, opting instead to wait for tonight’s high-profile FOMC rate decision.

A 25bps cut is fully priced and universally expected, leaving no suspense around the headline move. The real uncertainty lies in how the Fed shapes expectations for 2026 through its updated dot plot, the vote split, the statement, and Chair Jerome Powell’s press conference. With so many moving parts, the stakes are high and volatility is almost certain.

Adding to the broader policy backdrop is continuous attention on the next Fed Chair. The Financial Times reports that President Donald Trump will begin his final round of interviews this week, with senior administration officials indicating Kevin Hassett remains the leading candidate. The prospect of Hassett, viewed as more politically aligned and more dovish-leaning on growth risks, is seeping into market conversations.

A separate CNBC survey shows 84% of respondents believe Trump will choose Hassett, who currently heads the National Economic Council. Yet only 11% believe he should be the pick. Fed Governor Christopher Waller is the top choice among surveyed economists, with 47% support, followed by Kevin Warsh at 23%. Still, just 5% think Trump will select either of them, highlighting how little confidence markets have in an apolitical appointment.

Before the Fed lands, the BoC will deliver its own decision, with a steady hold at 2.25% widely expected. Markets now assume the BoC has entered a long pause following Governor Tiff Macklem’s October comments and the subsequent run of stronger-than-expected data. Any explicit confirmation of this stance today could lift the Loonie further, especially in crosses.

In weekly FX performance, Aussie remains the best performer so far. Kiwi follows as the second strongest, while Dollar sits in third place as traders hedge cautiously ahead of the FOMC. Yen is the weakest currency this week, followed by Loonie and then Swiss Franc, with Euro and Sterling holding mid-table positions.

In Asia, Nikkei fell -0.10%. Hong Kong HSI is up 0.21%. China Shanghai SSE is down -0.23%. Singapore Strait Times is down -0.20%. Japan 10-year JGB yield fell -0.008 to 1.957. Overnight, DOW fell -0.38%. S&P 500 fell -0.09%. NASDAQ rose 0.13%. 10-year yield rose 0.014 to 4.186.

Fed Preview: If March cut odds fall tonight, Santa rally is done

FOMC rate decision is the clear centerpiece of today’s sessions, with markets fully convinced the Fed will deliver a 25bps cut to 3.50–3.75%. The probability of anything else is effectively zero, and policymakers have little incentive to risk unsettling sentiment by defying expectations at this stage of the cycle. The real debate is not about tonight’s move, but about what the Committee signals for 2026 and the broader path ahead.

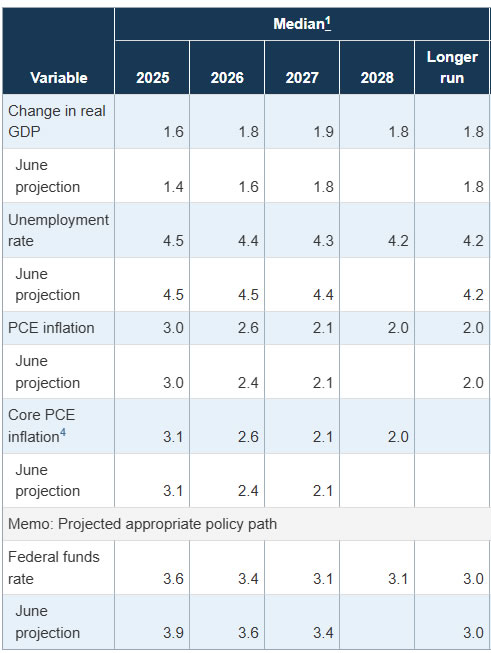

Turning back to September’s meeting, the median dot plot penciled in only one additional cut in 2026, taking the policy rate to 3.25–3.50%. A key question now is whether the Fed keeps that projection unchanged. While, that is the most likely outcome, but the dot plot itself will not reveal when that single cut is expected—whether early in the year or toward year-end. That ambiguity will shape how markets interpret tonight’s guidance.

This leads to the second major issue: whether the Fed is effectively entering a pause after today’s cut. One of the first clues will come from the vote split. A tight or divided vote would reinforce the view that the bar for further reductions is rising, and that January is likely to be another hold. The follow-through will come from the statement and Chair Jerome Powell’s press conference, where the tone will be scrutinized closely.

While all of this will ultimately be re-priced once next week’s November CPI and NFP data arrive, tonight’s communication is still critical for setting the base case for early-2026 policy expectations. Markets will be particularly sensitive to any shift in how the Fed describes labor market resilience, wage cooling, and tariff-related inflation risks.

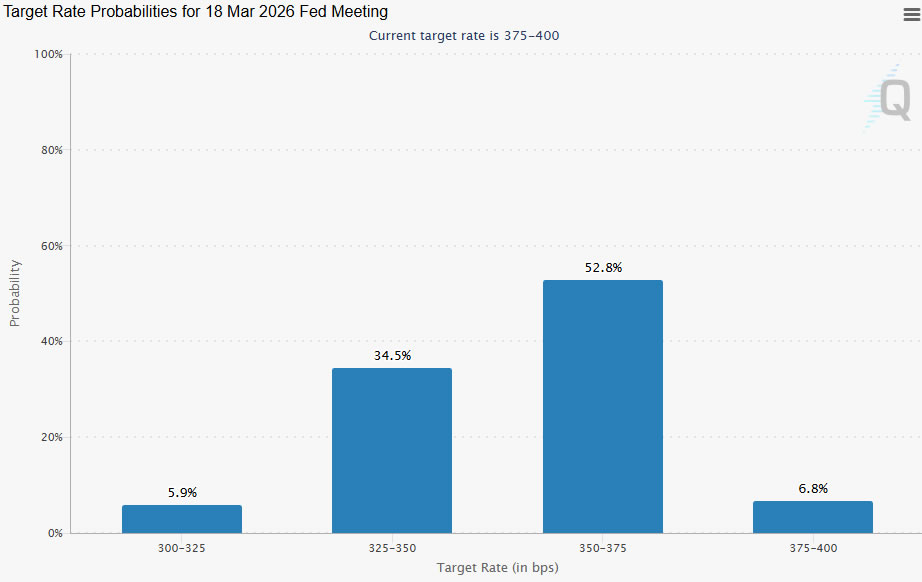

In terms of market reaction, the most important gauge is pricing for a March rate cut. Fed fund futures currently assign roughly a 40% probability of a 25bps cut in March and about a 60% probability of a hold. Any move in those probabilities—driven by dots, tone, or vote split—will dictate how equities, yields, and Dollar respond.

In stocks, a key to watch is 477560.29 support in DOW. Firm break there should indicate rejection by 48431.47 high, and the corrective pattern from there should be starting a third leg. In this case, deeper pullback would be seen to 55 D EMA (now at 46797.21) and below. Effectively, the Santa rally is killed in this case before it starts. But of course, decisive break of 48431.57 will bring another record run through to year-end.

China CPI hits 21-month high, but weak demand keeps PPI in deep negative

China’s November inflation data paint a picture of an economy showing modest signs of surface-level improvement while still grappling with entrenched deflationary pressures.

CPI accelerated from 0.2% yoy to 0.7% yoy, matching expectations and marking a 21-month high. The gain was driven primarily by food prices, which rose 0.2% yoy after a -2.9% yoy drop in October. Core inflation held steady at 1.2% yoy, while energy prices slid -3.4% yoy—an even deeper decline than the prior month.

On a monthly basis, CPI fell -0.1% mom after October’s 0.2% mom increase, contrary to expectations for another rise.

PPI slipped from –2.1% yoy to –2.2% yoy, extending China’s factory-gate deflation streak into a fourth year. Manufacturers continue to cut prices aggressively to clear excess supply, a sign that domestic and external demand remain too weak to absorb output.

Coal mining prices tumbled -11.8% yoy, while the oil and gas extraction sector saw a -10.3% yoy decline—deep drops that suggest little improvement in industrial profitability.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1608; (P) 1.1633; (R1) 1.1650; More….

EUR/USD recovered after hitting 55 4H EMA but stays below 1.1681 temporary top. Intraday bias stays neutral at this point. Further rally is in favor with 1.1590 minor support intact. Corrective fall from 1.1917 could have completed at 1.1467. Above 1.1681 will target 1.1727 resistance first. Firm break there will solidify this case and bring retest of 1.1917 high. However, break of 1.1590 will revive near term bearishness, and bring retest of 1.1467 low.

In the bigger picture, as long as 55 W EMA (now at 1.1346) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Fed to Proceed With Another Precautionary Rate Cut Despite Highly Divided MPC.

Markets

Monday’s ECB Schnabel driven rally in EMU yields ran into resistance yesterday. Investors in some way embraced her message that the next ECB move, after a period of rate stability, will likely be a rate hike. EMU money markets priced out the probability of a final fine-tuning/risk management cut next year and at the same time raise chances of higher rates from the turn of 2026/27 on. US markets are preparing for another ‘hawkish’ rate cut today despite ongoing pressure for the government to ease policy in a more aggressive way. Visibility on upcoming data-guidance remains low but yesterday’s rise in yields after better than expected JOLTS job openings data only illustrated market sensitivity to the topic. US yields added between 4 bps (2 & 5-y) and 0.6 bps (30-y). US yields are close to the top of the post-summer sideways technical trading ranges. A $39bn 10-y US Treasury auction delivered ‘neutral’ bidding metrics and had little impact. Equity markets took a pause with record levels back within reach. Changes in the intraday interest rate dynamics between the dollar and other currencies, including the euro, again lacked directional impact. DXY (close 99.22 from 99.08) gained marginally, mainly driven by a rebound in USD/JPY (close 156.9). EUR/USD softened slightly (close EUR/USD 1.1627). French Parliament yesterday approved the social security bill, removing an hurdle to get budget approved as soon as next week, but more likely early 2026. For now this French ‘muddling through’ scenario doesn’t help the euro.

The Bank of Canada (expected unchanged at 2.25%) and the Banco National do Brasil (expected unchanged at 15%) join the Fed in deciding on monetary policy today. The Fed is expected to proceed with another precautionary 25 bps rate cut (to 3.5%-3.75%) despite a highly divided MPC. Markets will keep a close eye at the new Summery of Economic Projections (dots) and any guidance from Fed Chair Powell. However, news from those sources will probably be highly conditional. Governors since the September forecast had little hard evidence on the labour market and even less on inflation to make substantial changes. One can expect the Fed chair to shift to an outright data-dependent narrative as the policy rate is coming closer to neutral. This puts the focus on data updates between now and Christmas (payrolls, CPI and Q3 GDP). With yields having rebounded/priced out more aggressive easing, there might again be room for some correction in case of softer data. However, question is whether today’s FOMC meeting will already allow for such a reaction. On FX, DXY and EUR/USD show little directional momentum. On the euro side of the equation, uncertainty on France and maybe even more on the outcome of negotiations to end the war in Ukraine are a drag for further euro gains.

News & Views

Chinese inflation rebounded to 0.7% y/y from 0.2%, the quickest pace since February of last year. Food prices were partly responsible for the uptick, rising for the first time since January. Non-food inflation slipped to 0.8%. Filtering for both food and energy prices, core inflation ended a six-month acceleration streak to come in unchanged at 1.2%. Other elements supporting the inflation rebound were surging gold jewelry prices (+58.4% y/y) which lifted the category “miscellaneous goods and services” to 14.2% y/y. Services prices increased at a slower rate compared to October (0.7%), the first slowing since February. The above combined with producer prices unexpectedly showing steeper drops (-2.2% from -2.1% vs -2% expected) means the CPI rebound isn’t a solid sign of deflation risks structurally easing. The Chinese yuan gapped lower at the open this morning but meanwhile swapped losses into gains around USD/CNY 7.06, a more than one year CNY high.

BoE policymakers in yesterday’s parliamentary hearing largely stuck to their personal and mixed views on whether or not it is appropriate to further lower policy rates. One of them, however, offered a glimpse on the BoE’s judgement of the November budget. Deputy governor Lombardelli said it would lower the annual inflation rate by 0.4-0.5 ppts from 2026Q2 while lifting GDP slightly by 0.2 ppts in 2027. The budget together with inflation coming off again were seen as paving the way for a December rate cut. Lombardelli suggested, however, the BoE could look through the one-off impact on inflation from the government measures but added that the latter may help bring down elevated household inflation expectations. It will probably once again be BoE governor Bailey having the swing vote in next week’s policy decision.

Fed Preview: If March cut odds fall tonight, Santa rally is done

FOMC rate decision is the clear centerpiece of today’s sessions, with markets fully convinced the Fed will deliver a 25bps cut to 3.50–3.75%. The probability of anything else is effectively zero, and policymakers have little incentive to risk unsettling sentiment by defying expectations at this stage of the cycle. The real debate is not about tonight’s move, but about what the Committee signals for 2026 and the broader path ahead.

Turning back to September’s meeting, the median dot plot penciled in only one additional cut in 2026, taking the policy rate to 3.25–3.50%. A key question now is whether the Fed keeps that projection unchanged. While, that is the most likely outcome, but the dot plot itself will not reveal when that single cut is expected—whether early in the year or toward year-end. That ambiguity will shape how markets interpret tonight’s guidance.

This leads to the second major issue: whether the Fed is effectively entering a pause after today’s cut. One of the first clues will come from the vote split. A tight or divided vote would reinforce the view that the bar for further reductions is rising, and that January is likely to be another hold. The follow-through will come from the statement and Chair Jerome Powell’s press conference, where the tone will be scrutinized closely.

While all of this will ultimately be re-priced once next week’s November CPI and NFP data arrive, tonight’s communication is still critical for setting the base case for early-2026 policy expectations. Markets will be particularly sensitive to any shift in how the Fed describes labor market resilience, wage cooling, and tariff-related inflation risks.

In terms of market reaction, the most important gauge is pricing for a March rate cut. Fed fund futures currently assign roughly a 40% probability of a 25bps cut in March and about a 60% probability of a hold. Any move in those probabilities—driven by dots, tone, or vote split—will dictate how equities, yields, and Dollar respond.

In stocks, a key to watch is 477560.29 support in DOW. Firm break there should indicate rejection by 48431.47 high, and the corrective pattern from there should be starting a third leg. In this case, deeper pullback would be seen to 55 D EMA (now at 46797.21) and below. Effectively, the Santa rally is killed in this case before it starts. But of course, decisive break of 48431.57 will bring another record run through to year-end.

Winds Shift, Hawks Circle

Everybody knows the Federal Reserve (Fed) will announce a 25bp rate cut today. I know it, you know it, he/she/it knows it, my five-year-old knows it, my cat, your dog, the birds in the sky. Everyone knows the Fed is lowering rates later today. Market pricing is giving it roughly an 88% probability — too high for the Fed to walk back in the absence of an emergency.

What we don’t know is what Fed members are planning for next year. How many cuts they anticipate, and whether their projections will convince markets to react accordingly.

For the doves, the case for rate cuts is clear: the US labour market has softened, partly due to a combination of aggressive anti-immigration policies, tariff uncertainty and fears around AI-related job displacement. Tariff-led price pressures, meanwhile, still haven’t shown up materially since tariffs were announced in April. Add to that the political noise — with Donald Trump pressuring the Fed to cut rates, at times with aggressive public remarks — and poor Jerome Powell is hearing things he probably never expected to hear in his lifetime.

For the most extreme doves, the Fed has “plenty of room” to cut. Kevin Hassett — one of Trump’s favourite candidates to lead the Fed next year — said yesterday that the rise of AI gives the Fed an opportunity to run easier policy because lower rates could lift both aggregate supply and demand. Higher supply, he argues, could help contain inflation.

Others think it may be wiser to pause for thought. AI-driven productivity gains are real. But looming inflation risks from tariffs still require a careful playbook — particularly if AI-driven disinflation doesn’t materialise fast enough to neutralize potential tariff-led inflation.

So, it’s complicated. All eyes will be on the Fed’s dot plot. Any hawkish tilt or reluctance to signal further cuts could trigger another repricing and weigh on sentiment.

The good news: investors aren’t walking into this meeting blindly. Money markets have already trimmed their expectations from 2–4 cuts next year to just two, reducing the risk of a sharp reaction to a “hawkish cut.”

And judging by yields, the message from investors is clear: they’re not buying the dovish narrative. Instead, investors worry that lower yields could revive inflation and ultimately prevent the Fed from cutting more — or even force a hike. The proof: the US 10-year yield has climbed since the Fed began cutting in September.

This disconnect between Fed policy and market yields suggests lower policy rates are not fully transmitting. No matter what Fed officials think, markets remain worried about inflation. They won’t absorb lower policy rates until they see evidence of inflation falling. That dynamic could prevent the S&P 500 from pushing higher into year-end.

Meanwhile, global winds are turning hawkish, as well. The Reserve Bank of Australia (RBA) said this week it debated an “extended pause or a hike,” and markets now price a rate increase by June — a stark reversal from expectations of a cut just a month ago. The Australian 10-year yield has jumped from ~4.10% in late October to above 4.80%.

The Bank of Canada (BoC) is expected to hold today, but markets are almost fully pricing a hike by late 2026, on the back of strong Canadian labour data. Canadian 10-year yields have risen from around 3% to near 3.50%.

The European Central Bank (ECB) isn’t expected to cut next year, and Isabel Schnabel said this week she’s comfortable with market pricing that the ECB’s next move could be a hike. The European 10-year yield is now around 2.85%, up from ~2.50% in October.

The Reserve Bank of New Zealand (RBNZ) watchers have also shifted from expecting a September cut to expecting a hike. The 10-year yield has spiked from ~4% to above 4.6%.

And the Bank of Japan (BoJ) is widely expected to hike next week. The Japanese 10-year is flirting with 2%, raising the risk of Japanese pension funds and insurers — major US Treasury holders — repatriating capital back home, and pull the rug from under the feet of US treasuries.

Consequently, even though equity investors still debate whether the tech sector is in bubble territory, global bond investors have little doubt about two things: DM debt is unsustainably high, and central bank expectations are shifting hawkish. The latter pushes the yields higher.

And if yields continue pushing higher, valuations will come under pressure — especially for highly leveraged companies.

So, today’s reaction to the Fed will likely set the tone for the remainder of the year: will Santa bring gifts, or stay snowed out? Answer in a few hours.

All Eyes on Fed Decision – Rate Cut Priced in, 2026 Outlook Uncertain

In focus today

In the US, today's main event will be the FOMC's rate decision. We expect a 25bp cut to the policy rate target, in line with consensus and market pricing. We expect Powell to verbally push back against continuation of sequential rate cuts in early 2026. The updated rate projections, or 'dots', will likely reflect varied views within the FOMC, while macroeconomic projections will see only cosmetic changes. The Fed may also take further steps to support liquidity. See more in our Fed preview: Hawkish cut is a consensus choice, 5 December. Ahead of the decision, Q3 employment cost index (ECI) is due for release.

In Sweden, October economic activity data is released, including the GDP indicator, household consumption, new orders, and production value index. While we expect slower growth for Q4 compared to Q3 due to weaker summer indicators, this does not alter the positive outlook for 2026.

In Norway, we expect November core inflation to decline to 3.1%, matching Norges Bank's September MPR estimate. October core inflation surprised to the upside at 3.4% y/y, likely influenced by price adjustments ahead of Black Week.

In Canada, the Bank of Canada is set to announce its rate decision. We expect the rate to remain unchanged at 2.25%, in line with consensus.

In Denmark, November inflation data is released. We expect it to remain unchanged at 2.1% y/y, with food prices remaining a key focus due to their impact on consumer sentiment.

Economic and market news

What happened overnight

In China, November CPI came in as expected at 0.7% y/y, reaching a 21-month high driven largely by food prices. Core inflation held steady at 1.2% y/y, while PPI remained stuck in deflationary territory at -2.2% y/y (cons: -2.0%). This underlines the persistent weakness in domestic demand and the challenges of achieving a near-term recovery.

In US-Japan relations, the US criticised China for targeting Japanese military aircraft with radar during a training exercise last week, calling the actions "not conducive to regional peace and stability." Japan welcomed the support, emphasising the strength of their alliance.

What happened yesterday

In the US, the JOLTs job openings report for October came in stronger than expected at 7.670m (cons: 7.150). This indicates that labour demand remains relatively robust, aligning with signals from high-frequency indicators. While the overall labour market balance remains steady, details in the report were less positive: voluntary quits and hires declined, while involuntary layoffs increased. The ratio of job openings to unemployed remains stable at 1.01, consistent with levels observed throughout the year. Thus, the Fed is still likely to cut rates today, but on the margin, this increases the likelihood of a pause in the easing cycle in early 2026.

The NFIB small business optimism index for November rose modestly by 0.8 points to 99.0. Actual price changes increased notably, while plans for future price changes remained stable. Hiring plans also improved, recovering close to pre-pandemic levels.

In France, PM Sébastien Lecornu secured a political win yesterday evening as the parliament narrowly approved next year's social security budget, thereby averting a government crisis. The bill's adoption reduces pressure on PM Sébastien Lecornu to resign, as his strategy to win over the Socialists by suspending the pension reform helped break political deadlock. However, challenges remain with the main budget, which has faced even tougher opposition, with only one lawmaker supporting it in an earlier vote. The debate on the main budget begins on 15 December, which means it might be passed before Christmas, and the government would thereby avoid relying on emergency laws to roll over the 2025 budget. However, there is still a significant risk that the parliament will fail to reach an agreement.

Equities: It was a slow day in equities, as investors are on hold before the Fed meeting tonight. S&P 500 and Stoxx 600 ended a meagre -0.1% lower. Defensives - or should we say health care - underperformed. In fact, global defensives have underperformed cyclicals since 25 November. However, unlike then, this is no longer a broad defensive pullback. In fact, consumer staples was the best performing sector yesterday. The defensive underperformance is transforming more and more to health care simply selling off (after an incredible rally the last three months). Global health care stocks were -1% lower yesterday, quite sizable given the mild moves elsewhere. The wait and see mode is continuing this morning, with futures little changed.

FI and FX: US yields edged higher after a stronger-than-expected October JOLTS report, signalling resilient labour demand despite some softening in quits and hires. The Fed is expected to cut rates today, but data slightly raises the odds of an early-2026 pause. In Europe, yields consolidated as France avoided a government crisis by passing the social security budget, though risks remain around the main budget debate later this month. EUR/USD trades in a tight range ahead of the FOMC, with risks leaning modestly USD-positive, while SEK strengthened despite seasonal outflow expectations. Today's Norwegian inflation data plus the Fed decision might guide the NOK in the near term.

China CPI hits 21-month high, but weak demand keeps PPI in deep negative

China’s November inflation data paint a picture of an economy showing modest signs of surface-level improvement while still grappling with entrenched deflationary pressures.

CPI accelerated from 0.2% yoy to 0.7% yoy, matching expectations and marking a 21-month high. The gain was driven primarily by food prices, which rose 0.2% yoy after a -2.9% yoy drop in October. Core inflation held steady at 1.2% yoy, while energy prices slid -3.4% yoy—an even deeper decline than the prior month.

On a monthly basis, CPI fell -0.1% mom after October’s 0.2% mom increase, contrary to expectations for another rise.

PPI slipped from –2.1% yoy to –2.2% yoy, extending China’s factory-gate deflation streak into a fourth year. Manufacturers continue to cut prices aggressively to clear excess supply, a sign that domestic and external demand remain too weak to absorb output.

Coal mining prices tumbled -11.8% yoy, while the oil and gas extraction sector saw a -10.3% yoy decline—deep drops that suggest little improvement in industrial profitability.

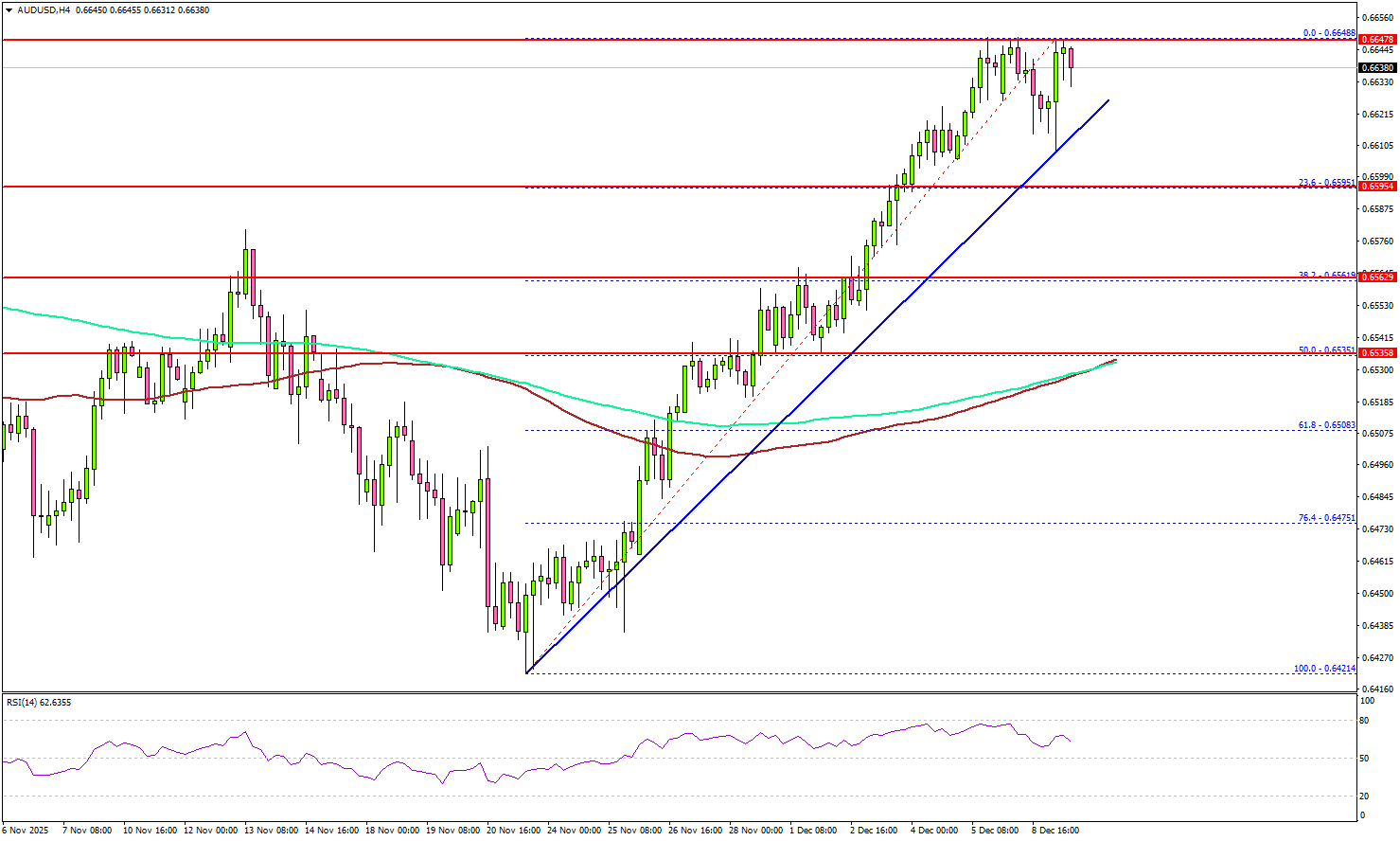

AUD/USD Pushes Higher—Is the Pair Targeting a Fresh Multi-Day Peak?

Key Highlights

- AUD/USD gained pace for a move above the 0.6600 resistance.

- A key bullish trend line is forming with support at 0.6620 on the 4-hour chart.

- EUR/USD failed to continue higher above 1.1680.

- USD/JPY started a fresh increase above the 156.00 resistance.

AUD/USD Technical Analybsis

The Aussie Dollar started a strong increase above 0.6550 against the US Dollar. AUD/USD even cleared the 0.6600 barrier to enter a positive zone.

Looking at the 4-hour chart, the pair settled above the 0.6600 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). A high was formed at 0.6648, and the pair is now consolidating gains.

There is also a key bullish trend line forming with support at 0.6620. Immediate resistance sits near 0.6650. The first key hurdle is seen near 0.6665.

A close above 0.6665 could open the doors for a move toward 0.6700. Any more gains could set the pace for a steady increase toward 0.6740. On the downside, there is key support at 0.6620 and the trend line at 1.1620.

The next support is 0.6595 and the 23.6% Fib retracement level of the upward move from the 0.6421 swing low to the 0.6648 high. A close below 0.6595 could open the doors for a test of 0.6560.

The main support sits near the confluence zone at 0.6535, the 100 simple moving average (red, 4-hour), the 200 simple moving average (green, 4-hour), and the 50% Fib retracement level of the upward move from the 0.6421 swing low to the 0.6648 high.

Looking at EUR/USD, the pair failed to extend gains above 1.1680 and recently corrected lower.

Upcoming Key Economic Events:

- BoE's Governor Bailey speech.

- ECB's President Lagarde speech.

- BoC Interest Rate Decision – Forecast 2.25%, versus 2.25% previous.