Sample Category Title

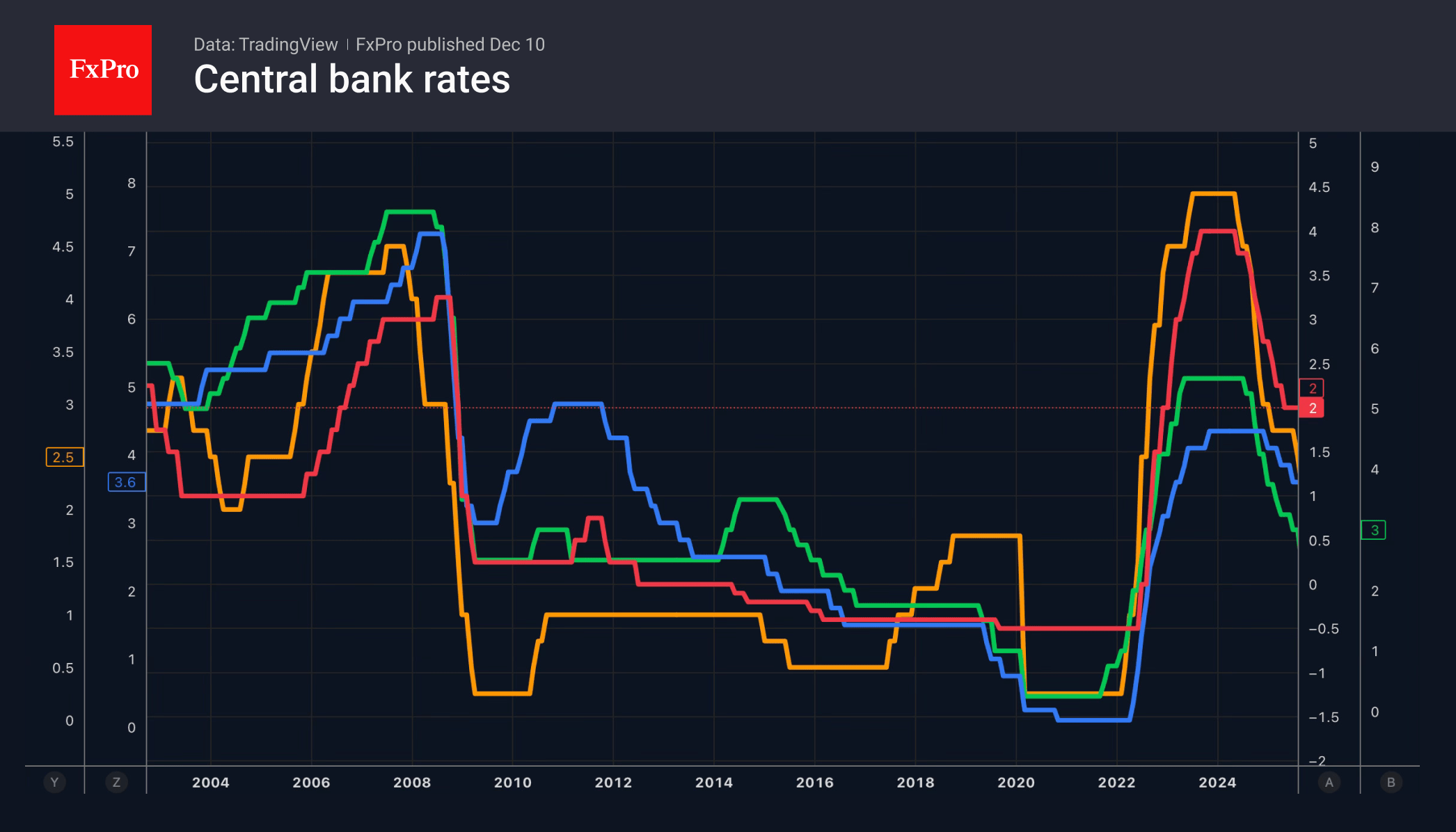

BoC holds steady, points to weak Q4 GDP and balanced inflation outlook

The BoC kept the overnight rate unchanged at 2.25% today, in line with expectations. The most notable element of the statement was the Governing Council’s assessment that, if inflation and economic activity evolve broadly as projected in October, the current policy rate is “about the right level.” This marks a clear signal that the easing cycle has effectively ended and that the bank has entered a long period of steady policy barring major surprises.

The statement acknowledged mixed growth dynamics heading into year-end. The Bank expects final domestic demand to expand in Q4, but weakness in net exports will leave overall GDP “likely weak.” Growth is projected to firm in 2026, though policymakers warned that uncertainty remains elevated and that swings in trade flows could continue to create quarter-to-quarter volatility.

Employment has posted solid gains over the past three months and the unemployment rate declined to 6.5% in November. However, job markets in trade-sensitive sectors “remain weak,” and economy-wide hiring intentions are still "subdued"—reflecting the broader drag from structural trade reconfiguration.

Despite these pressures, BoC expects the ongoing economic slack to counterbalance cost increases associated with shifting trade patterns. As a result, CPI inflation is still anticipated to stay close to the 2% target, providing the BoC with scope to maintain a steady hand for the foreseeable future.

Bank of Canada maintains policy rate at 2¼%

The Bank of Canada today held its target for the overnight rate at 2.25%, with the Bank Rate at 2.5% and the deposit rate at 2.20%.

Major economies around the world continue to show resilience to US trade protectionism, but uncertainty is still high. In the United States, economic growth is being supported by strong consumption and a surge in AI investment. The US government shutdown caused volatility in quarterly growth and delayed the release of some key economic data. Tariffs are causing some upward pressure on US inflation. In the euro area, economic growth has been stronger than expected, with the services sector showing particular resilience. In China, soft domestic demand, including more weakness in the housing market, is weighing on growth. Global financial conditions, oil prices, and the Canadian dollar are all roughly unchanged since the Bank’s October Monetary Policy Report (MPR).

Canada’s economy grew by a surprisingly strong 2.6% in the third quarter, even as final domestic demand was flat. The increase in GDP largely reflected volatility in trade. The Bank expects final domestic demand will grow in the fourth quarter, but with an anticipated decline in net exports, GDP will likely be weak. Growth is forecast to pick up in 2026, although uncertainty remains high and large swings in trade may continue to cause quarterly volatility.

Canada’s labour market is showing some signs of improvement. Employment has shown solid gains in the past three months and the unemployment rate declined to 6.5% in November. Nevertheless, job markets in trade-sensitive sectors remain weak and economy-wide hiring intentions continue to be subdued.

CPI inflation slowed to 2.2% in October, as gasoline prices fell and food prices rose more slowly. CPI inflation has been close to the 2% target for more than a year, while measures of core inflation remain in the range of 2½% to 3%. The Bank assesses that underlying inflation is still around 2½%. In the near term, CPI inflation is likely to be higher due to the effects of last year’s GST/HST holiday on the prices of some goods and services. Looking through this choppiness, the Bank expects ongoing economic slack to roughly offset cost pressures associated with the reconfiguration of trade, keeping CPI inflation close to the 2% target.

If inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment. Uncertainty remains elevated. If the outlook changes, we are prepared to respond. The Bank is focused on ensuring that Canadians continue to have confidence in price stability through this period of global upheaval.

Information note

The next scheduled date for announcing the overnight rate target is January 28, 2026. The Bank’s next MPR will be released at the same time.

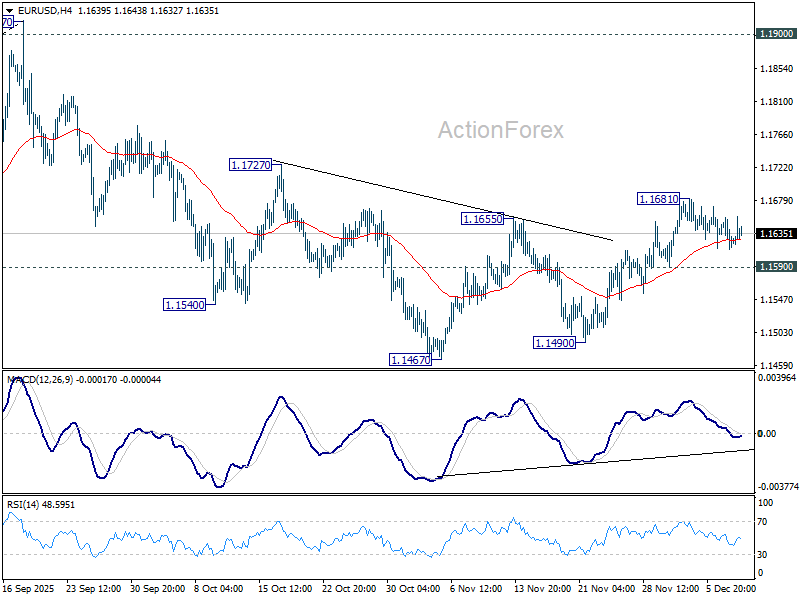

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1608; (P) 1.1633; (R1) 1.1650; More….

Intraday bias in EUR/USD remains neutral and more consolidations could still be seen below 1.1681. Further rally is in favor with 1.1590 minor support intact. Corrective fall from 1.1917 could have completed at 1.1467. Above 1.1681 will target 1.1727 resistance first. Firm break there will solidify this case and bring retest of 1.1917 high. However, break of 1.1590 will revive near term bearishness, and bring retest of 1.1467 low.

In the bigger picture, as long as 55 W EMA (now at 1.1346) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

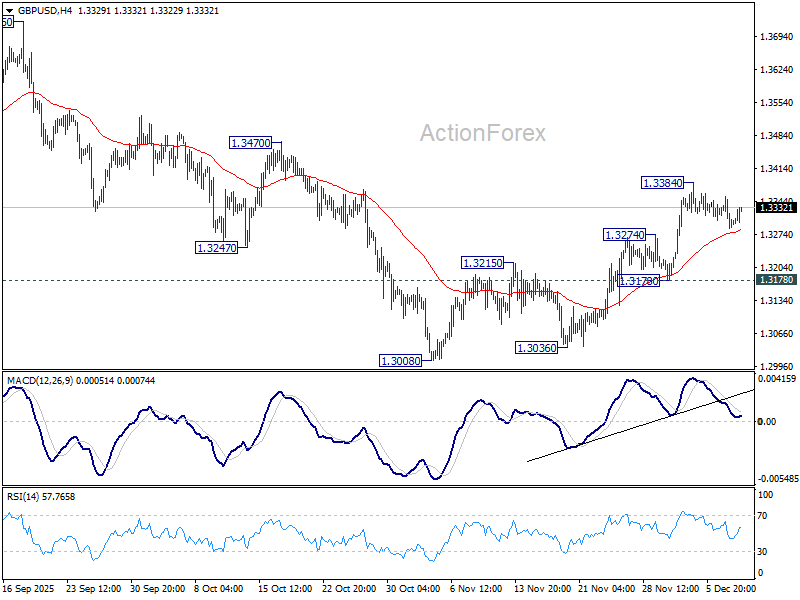

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3271; (P) 1.3314; (R1) 1.3339; More...

Intraday bias in GBP/USD remains neutral as consolidations continue below 1.3384. With 1.3178 support intact, further rally is expected. As noted before, fall from 1.3787 should have completed as a three-wave correction to 1.3008. On the upside, above 1.3384 will target 1.3470 resistance. Decisive break there will bring retest of 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

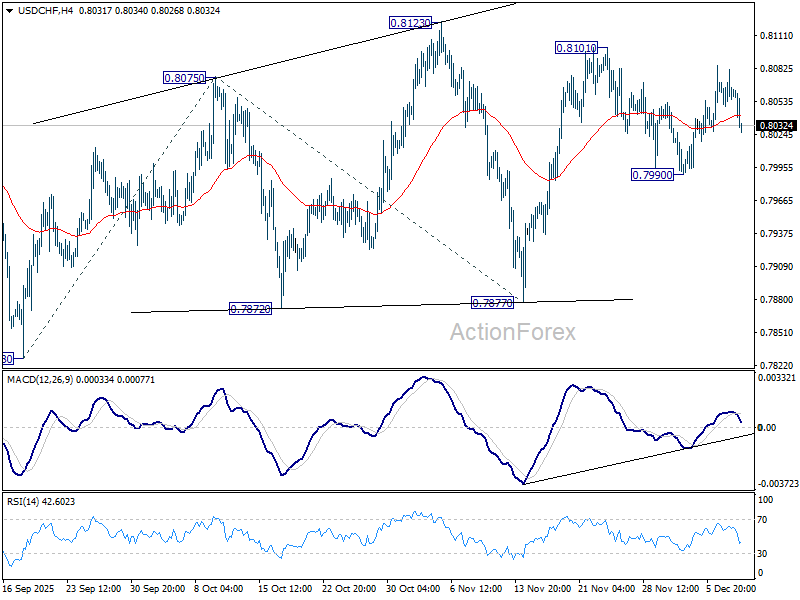

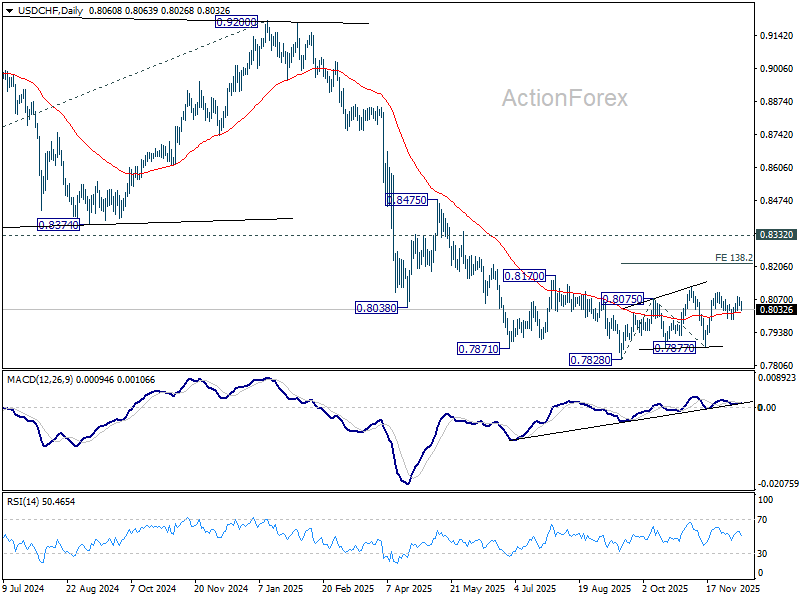

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8047; (P) 0.8065; (R1) 0.8080; More…

Intraday bias in USD/CHF remains neutral for the moment. Overall outlook is unchanged that price actions from 0.7828 are developing into a corrective pattern. Risk is mildly on the upside as long as 0.7990 support holds. Firm break of 0.8123 will target 138.2% projection of 0.7828 to 0.8075 from 0.7877 at 0.7812. However, break of 0.7990 support will turn bias back to the downside for 0.7877 support.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

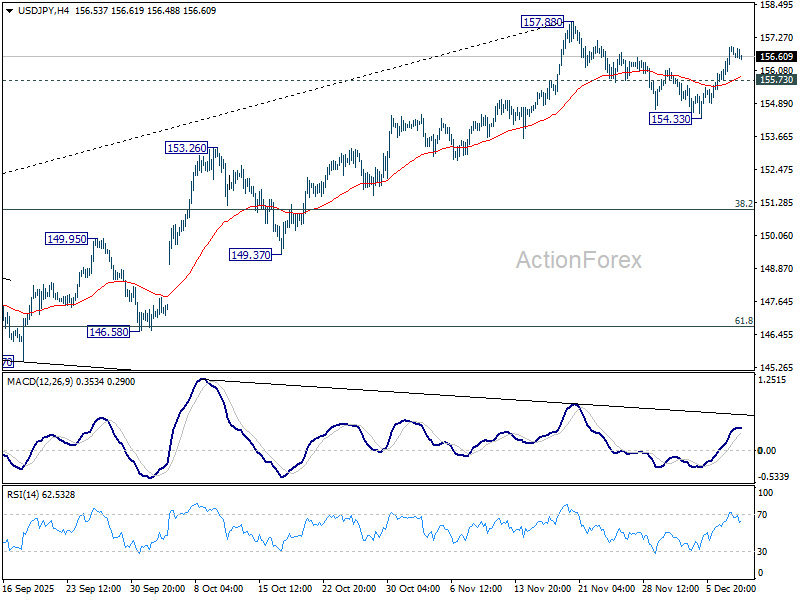

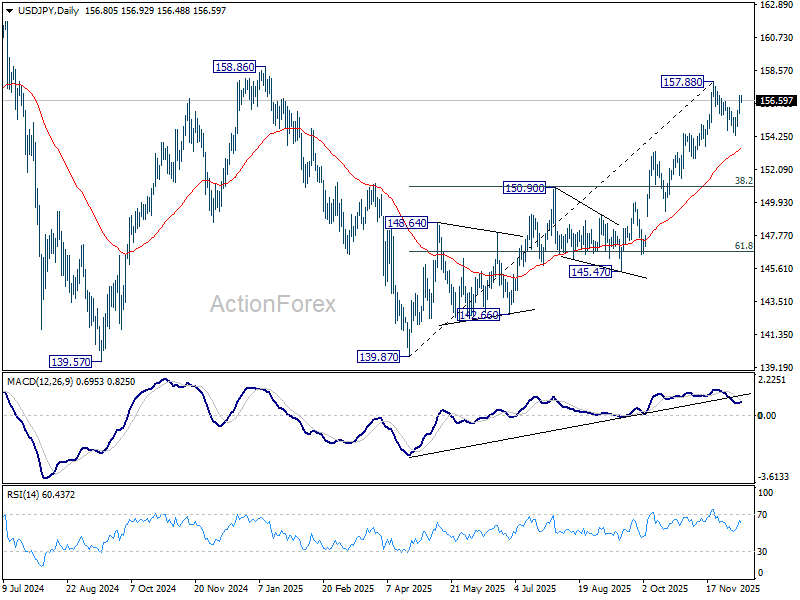

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.11; (P) 156.53; (R1) 157.33; More...

Intraday bias in USD/JPY remains on the upside as rise from 154.33 is in progress for retesting 157.88. Decisive break there will will target 158.85 structural resistance. Firm break there will be a strong bullish sign, and should target a retest on 161.94 high next. On the downside, below 155.73 minor support will turn bias neutral first. But risk will stays mildly on the upside as long as 154.33 support holds, in case of retreat.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

USD/JPY: 5-Day JPY Weakness Has Reached an Inflection Point for Potential Reversal as FOMC Looms

Key takeaways

- AUD is leading the FX space on renewed RBA hawkishness, while the JPY remains the weakest major currency as BoJ signals flexibility on policy.

- USD/JPY’s recent five-day rally is losing steam, with momentum indicators and resistance confluence pointing to a potential minor bearish reversal.

- A break below 156.00 on the USD/JPY could open the way toward 155.35 and 154.40, while a move above 157.15 would negate the downside setup.

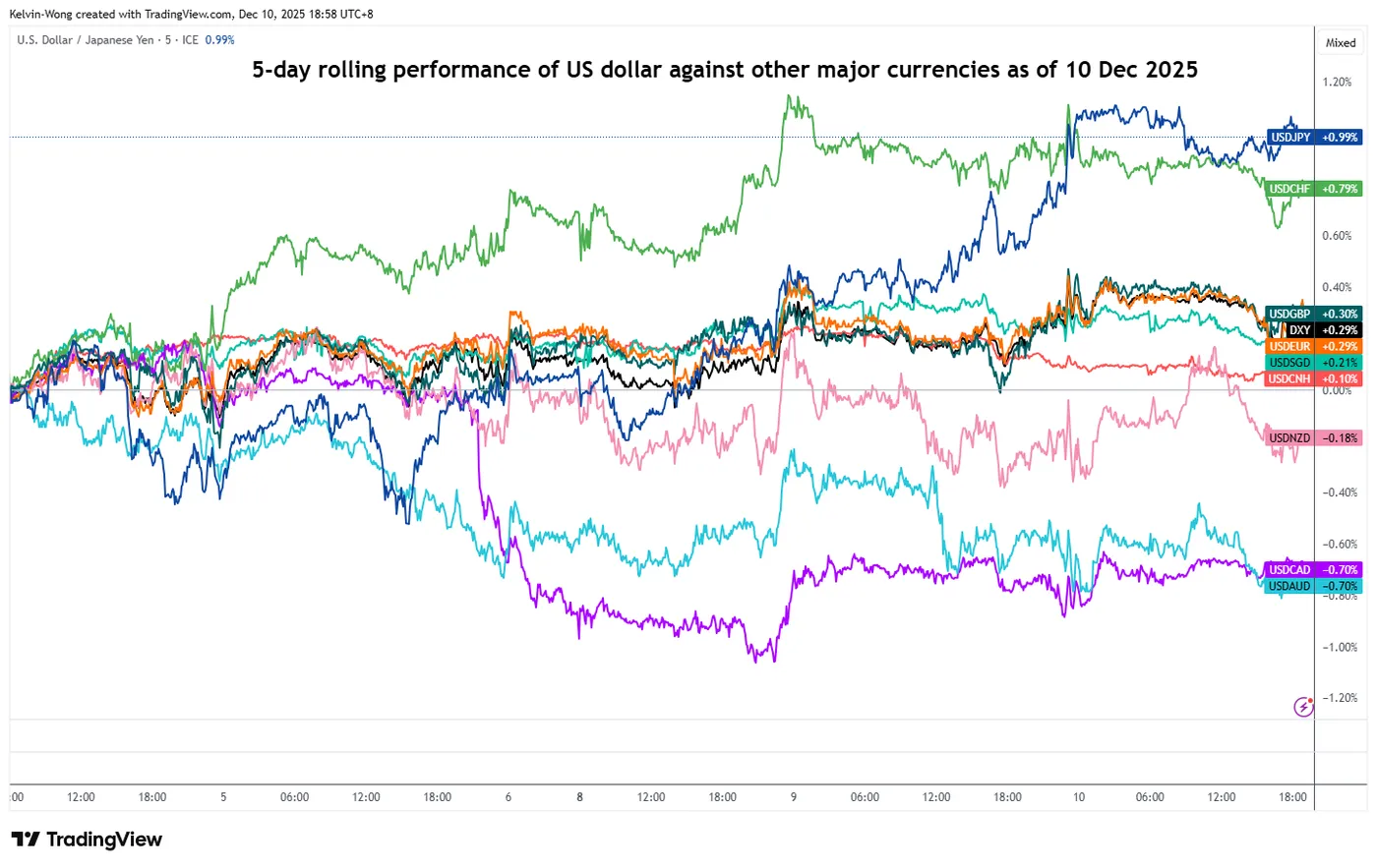

In the FX market, a “K-shaped” performance has emerged with the AUD rallying and outperforming among the major currencies against the US dollar due to the hawkish monetary policy guidance from the Australian central bank, RBA. In today’s Asia session, AUD extended its gains by 0.1% after a 0.3% return seen on Tuesday, 9 December, towards a three-month high at 0.6650 (see Fig. 1).

Fig. 1: 5-day rolling performance of the US dollar against major currencies as of 10 Dec 2025 (Source: TradingView)

At the end of the spectrum, the Japanese yen weakened for the third consecutive session against the greenback (USD/JPY rallied by 1% on a 5-day rolling basis) due to mixed messages from the Bank of Japan (BoJ) Governor Ueda’s speech on Tuesday, 9 December.

Ueda highlighted that the BoJ may ramp up government bond buying if long-term JGB yields rise rapidly, which appeared to be a signal that the BoJ is willing to tweak its existing policy after the BoJ ended its yield curve control programme in March 2024 that previously suppressed the rise in the 10-year JGB yield.

Interestingly, technical analysis suggests that the recent 5-day rally of the USD/JPY from its 154.40 minor swing low printed on 5 December 2025 has started to lose upside momentum that may lead to a potential minor bearish reversal on the USD/JPY.

Let’s unravel in greater detail.

Preferred trend bias (1-3 days) – Bearish with 156.00 as potential downside trigger

Fig. 2: USD/JPY major & medium-term trends as of 10 Dec 2025 (Source: TradingView)

Fig. 3: USD/JPY minor trend as of 10 Dec 2025 (Source: TradingView)

Watch the 157.15 key short-term pivotal resistance on the USD/JPY, and a break below 156.00 key near-term support (also the 20-day moving average) may trigger a minor bearish reversal to retest the next intermediate supports at 155.35 and 154.40.

A break and an hourly close below 154.40 may kickstart another minor downtrend sequence to expose 153.70 (also the 50-day moving average) next in the first step (see Fig. 3).

Key elements

- Tuesday, 9 December 2025’s rally on the USD/JPY ex-post BoJ Governor Ueda’s speech has stalled at the pull-back resistance of a former medium-term ascending support from 29 October 2025 low, the minor swing high area of 24 November 2025, and close to the 76.4% Fibonacci retracement of the prior minor downtrend from 20 November 2025 high to 5 December 2025 low, all confluence at the 157.15 level.

- The hourly RSI momentum indicator has just staged a bearish breakdown below a key ascending support after it exited from the overbought region (above 70). These observations suggest that the recent short-term upside momentum of the USD/JPY has eased.

Alternative trend bias (1 to 3 days)

A clearance above 157.15 invalidates the minor bearish reversal view for a further potential squeeze up for the next intermediate resistance to come in at 158.00/158.35.

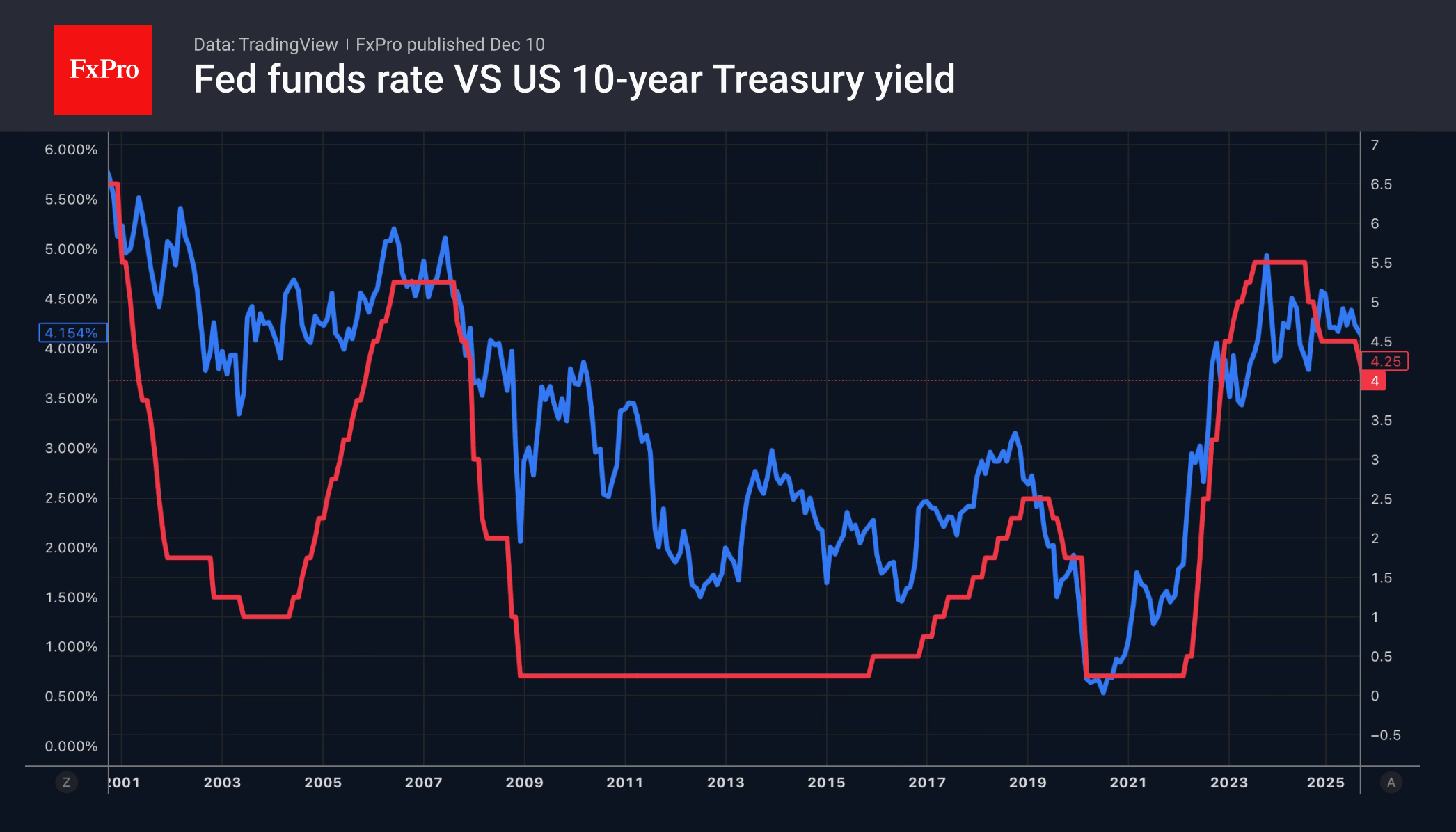

FOMC Will Take Another Route

- While some central banks are signalling that they have finished easing, the Fed intends to continue.

- The US dollar remains stable as the White House confirms the Fed’s independence.

In the Foreign Exchange market, an increasing number of key central banks are ending their easing measures. The Reserve Banks of Australia and New Zealand have made it clear that they have finished their rate-cut cycles. Similar signals are expected from the Bank of Canada. The ECB feels comfortable with the current level of rates. As a result, markets are beginning to price in that the next step will be a tightening. This is leading to a strengthening of the world’s major currencies against the dollar. But the latter is not giving up without a fight.

The Fed is likely to cut rates for the third consecutive time in 2025, but as in the previous two cases, the USD index risks rising. The baseline scenario is a hawkish shift, where the rate cut will be accompanied by less dovish rhetoric on the outlook and hints of a pause in policy easing. Judging by the quotes, the probability of one rate cut in 2026 is rising in the futures market, while the chances of three cuts are falling. This allows the US dollar to remain stable amid the changing policy landscape.

In addition, the debt market is not buying into Donald Trump’s idea of flooding the FOMC with doves. Jerome Powell’s resignation and the potential dismissal of Lisa Cook will allow the White House to increase the number of its people on the Committee. This could lead to aggressive rate cuts and a weaker US dollar. Unfortunately, Treasury yields are higher than in September, when the Fed resumed easing. Traders do not believe that the rate will fall below 3.25%.

The White House itself is indirectly to blame for this. Treasury Secretary Scott Bessent noted that the Fed is not a one-person show. The chairman has only one vote there, just like everyone else. The leading candidate for the position, Kevin Hassett, has stated that he does not intend to bow to political pressure. If the US president told him to lower rates and inflation accelerated to 4%, he would not do so.

Most likely, the US administration is being disingenuous. The White House aims to create the appearance of Fed independence to avoid undermining investor confidence in the USD as the primary reserve currency. However, we believe that the policies of Donald Trump and the central bank may be more aligned than ever before, which mitigates the decline in yields and increases the risks of a weakening greenback.

Dollar Index in a Quiet Mode Ahead of Key Fed Policy Decision

The dollar index – recovery leg from 98.70 daily higher base (the bottom of pullback from 100.32 peak) slows on Wednesday, as traders await the verdict from Fed at the end of two-day policy meeting.

Markets widely expect a 25-basis points rate cut, but focus will be on signals about the central bank’s rate path in coming months.

The Fed projected two rate cuts in 2026 (in September) with main question whether the policymakers will stick to existing agenda or will take more dovish stance and signal stronger policy easing, which is President Trump’s favored scenario, as he is in the process of choosing a successor for Jerome Powell, who is going step down in early 2026.

However, decision of 25-based points rate cut should not be the key market driver, but any surprise from the Fed could spark stronger market action.

More dovish than expected, Fed projections should add pressure on dollar and subsequently boost gold, while opposite effects could be expected in case the policymakers take more hawkish stance.

Technical picture is mixed on daily chart as rising thick daily cloud continues to underpin, but positive impact is countered by strengthening bearish momentum, while MAs are in mixed setup, with immediate action being capped by falling converged 10/200DMA’s for the second straight day.

Res: 99.30; 99.51; 99.70; 100.00.

Sup: 98.90; 98.70; 98.60; 98.31.

EUR/USD Stalls at Resistance as USD/JPY Extends Sharp Upside

EUR/USD climbed higher and tested the 1.1680 resistance. USD/JPY managed to reclaim 156.00 and might aim for more gains.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro started a downside correction from the 1.1680 pivot zone.

- There is a key declining channel forming with resistance at 1.1640 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY climbed higher above 155.50 and 156.00.

- There is a bullish trend line forming with support near 156.30 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair started a fresh increase from 1.1550. The Euro cleared a few key hurdles near 1.1600 to move into a positive zone against the US Dollar.

The pair settled above 1.1600 and the 50-hour simple moving average. A high was formed at 1.1681, and the pair started a downside correction. There was a drop below 1.1650, and the pair tested the 50% Fib retracement level of the upward move from the 1.1555 swing low to the 1.1681 high.

However, the bulls are active above 1.1620. On the upside, the pair is now facing bears near 1.1640 and 1.1650. There is also a key declining channel forming with resistance at 1.1640.

The next breakout region sits at 1.1680. An upside break above 1.1680 could set the pace for another increase. In the stated case, the pair might rise toward 1.1750. Immediate support is 1.1620. The first major key area of interest on the EUR/USD chart is near the 76.4% Fib retracement at 1.1585.

If there is a downside break below 1.1585, the pair could drop toward 1.1555. The next key breakdown area sits at 1.1520, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a decent increase from 154.35. The US Dollar gained bullish momentum above 155.00 against the Japanese Yen.

It settled above the 50-hour simple moving average and 156.00. The upward move was such that the pair even tested 156.90. A high was formed at 156.93 and the pair is now consolidating gains. There was a minor pullback below 156.75.

The current price action is positive, and the pair seems to be aiming for more gains. There is also a bullish trend line forming with support near 156.30 and the 23.6% Fib retracement level of the upward move from the 154.34 swing low to the 156.93 high.

Immediate resistance on the USD/JPY chart is near 156.90. The first key hurdle sits at 157.00. If there is a close above 157.00 and the RSI moves above 60, the pair could rise toward 157.50. The next stop for the bulls might be 157.80, above which the pair could test 158.40 in the coming days.

On the downside, the first major support is near the trend line at 156.30. The next area of interest could be near 155.65, below which the pair could test the 61.8% Fib retracement at 155.35. Any more losses could open the doors for a move toward 154.35.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.