Sample Category Title

Fed Delivers on Another Quarter-Point Cut, But Signals Higher Bar for Further Policy Easing

The Federal Reserve Open Market Committee (FOMC) reduced the federal funds rate by 25 basis points (bps), lowering the target range to 3.5%-3.75%. The move comes after consecutive quarter-point cuts at each of the prior two meetings.

There were minimal changes to the statement. However, a slight tweak to the reference to further rate cuts reinforced a more hawkish tone. The bolded portion reflects the revised verbiage: "In considering the extent and timing of additional policy adjustments to the target range" – suggesting a higher bar for further policy easing.

The statement also noted that, "the Committee judges that reserve balances have declined to ample levels and will initiate purchases of shorter-term Treasury securities as needed to maintain an ample supply of reserve on an ongoing basis".

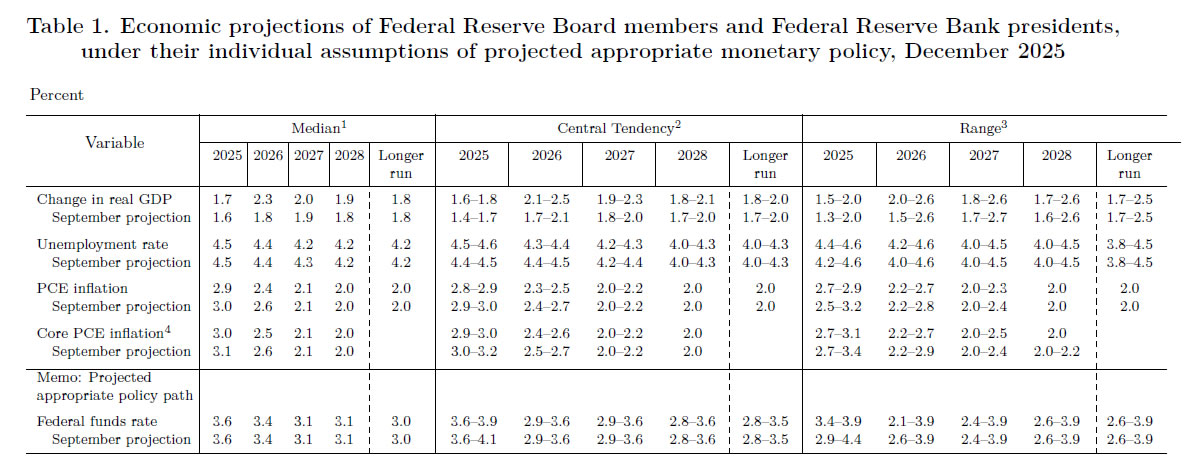

Accompanying the statement, the FOMC also released a revised set of economic forecasts, known as the "Summary of Economic Projections" (SEP). The SEP represents the median of the individual forecasts submitted by each of the FOMC participants. Relative to the September update:

- The median projection for real GDP growth – as measured on Q4/Q4 basis – was upgraded to 1.7% (previously 1.6%) in 2025, 2.3% in 2026 (previously 1.8%) and 2.0% (previously 1.9%) in 2027. The long-term outlook remained unchanged at 1.8%.

- The median year-end unemployment forecast for 2025 and 2026 were unchanged at 4.5%, and 4.4%, respectively, while 2027 was nudged lower to 4.2% (previously 4.3%).

- Core PCE inflation – the Fed's preferred inflation gauge – was revised a touch lower to 3.0% for 2025 (previously 3.1%) and to 2.5% in 2026 (previously 2.6%) but was unchanged at 2.1% for 2027.

- Lastly, the median projection for the federal funds rate was kept unchanged and suggest just one additional quarter-point cut in both 2026 and 2027.

Nine of the twelve FOMC members voted in favor of today's decision. Stephen Miran (again) dissented in favor of a larger 50 bps cut, while Jeffrey Schmid and Austan Goolsbee voted for no change to the policy rate this meeting. The last time there were three dissenters at a policy decision was in 2019.

Key Implications

A lot of ink had been spilt leading up to today's announcement of whether the Fed would or would not cut rates for a third consecutive meeting. While the FOMC ultimately decided to push forward with another cut, the statement and accompanying projections had a hawkish tilt, suggesting a higher bar for future rate cuts. This view is likely to be further reinforced by Chair Powell at the press conference, which will start at 2:30 PM ET.

Fed futures were little changed following the announcement, with the next cut not fully priced until June – a view that aligns to our forecast. But it's hard to have much conviction in that call in the absence of timely economic data. November's employment and CPI reports (to be released on December 16th and 18th, respectively) will shed some much-needed light on recent hiring and inflation trends and could materially shift our view and market pricing on the extent and timing of further policy easing. Stay tuned!

FOMC cuts as expected; dot plot shows only one cut per year through 2027

The Fed cut interest rates by 25bps to 3.50–3.75%, fully in line with expectations. The decision was done by a three way split. Governor Stephen Miran again voting for a larger 50bps reduction. Meanwhile Chicago Fed Austan Goolsbee and Kansas City Fed Jeffrey Schmid voted for no change. All other policymakers supported the quarter-point move.

The new projections signaled remarkable continuity. The federal funds rate path was left unchanged, with policymakers still expecting the policy rate to fall to 3.4% by the end of 2026, then 3.10% by the end of 2027, and remain there through 2028. This implies one 25bps cut per year in both 2026 and 2027.

Growth expectations, however, were revised meaningfully higher. GDP is now projected to expand 2.3% in 2026, up from 1.8% previously, and to grow 2.0% in 2027 and 1.9% in 2028. Labor-market projections were largely steady, with unemployment expected to be 4.4% in 2026, unchanged from prior forecasts. The rate for 2027 was nudged down from 4.3% to 4.2%, with 2028 left at 4.2%. Policymakers continue to signal a soft-landing baseline, where job markets cool without a material rise in unemployment.

Inflation projections were modestly lowered. Headline PCE is now expected at 2.4% in 2026, down from 2.6%, while the forecasts for 2027 and 2028 remain at 2.1% and 2.0%. Core PCE was trimmed to 2.5% for 2026 and left unchanged thereafter.

(FED) Federal Reserve Issues FOMC Statement

Available indicators suggest that economic activity has been expanding at a moderate pace. Job gains have slowed this year, and the unemployment rate has edged up through September. More recent indicators are consistent with these developments. Inflation has moved up since earlier in the year and remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook remains elevated. The Committee is attentive to the risks to both sides of its dual mandate and judges that downside risks to employment rose in recent months.

In support of its goals and in light of the shift in the balance of risks, the Committee decided to lower the target range for the federal funds rate by 1/4 percentage point to 3-1/2 to 3‑3/4 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

The Committee judges that reserve balances have declined to ample levels and will initiate purchases of shorter-term Treasury securities as needed to maintain an ample supply of reserves on an ongoing basis.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Philip N. Jefferson; Alberto G. Musalem; and Christopher J. Waller. Voting against this action were Stephen I. Miran, who preferred to lower the target range for the federal funds rate by 1/2 percentage point at this meeting; and Austan D. Goolsbee and Jeffrey R. Schmid, who preferred no change to the target range for the federal funds rate at this meeting.

BoC Done With Rate Cuts, Expects 2% Inflation to Persist

The Bank of Canada delivered a well-telegraphed, widely-expected hold today, keeping the overnight rate at 2.25%—the bottom of the neutral range and where we expect it will remain through the end of 2026.

The decision was after upward GDP revisions in the Q3 GDP release dating back to 2022, and a string of positive labour market surprises that saw a key indicator of the output gap, the Canadian unemployment rate, drop from 7.1% in September to 6.5% in November.

As much as recent data has been encouraging, we see it as reaffirming our cautiously optimistic base case rather than a fundamental shift in the Canadian economic outlook, and continue to expect a gradual recovery in the economy and labour market supported by the 275 bp rate reduction from the BoC since June 2024.

That outlook broadly aligns with the BoC's. Governor Macklem said in the press conference to expect modest growth and slow absorption of economic slack, while reiterating its holding bias.

Looking back, Canadian economic growth has already tracked toward the more optimistic end of the range of possibilities that the BoC projected in April, thanks to a combination of CUSMA exemptions shielding the bulk of goods exports to the U.S., and underlying resilience in household spending.

With that, we think the BoC is done with rate cuts, and that the next change in interest rates is more likely to be a hike. Our base case assumes this won't occur until 2027, but risks are tilted toward an earlier move.

What are the risks that could lead inflation to deviate from 2%?

BoC’s assessment that today’s policy rate is “at the right level” rests on a key assumption that “ongoing economic slack to roughly offset cost pressures associated with the reconfiguration of trade”, leaving inflation tracking around the 2% target.

We agree with that assessment, but have also argued that robust consumer demand growth could keep underlying price pressures elevated next year.

By most measures, the economy still has excess supply—it can produce more than is currently demanded. This creates downward pressure on inflation as businesses compete for limited demand. Still, recent data already suggests a smaller (albeit still negative) output gap than previously expected.

Consumer purchases have also broadly held onto resilience this year and could remain a source of strength if not upside risks to our growth and inflation forecast in 2026, following improvements in labour market conditions. That could lessen the disinflationary pressures relative to what was expected.

Offsetting that is the cost of "trade reconfiguration"—Canadian producers are not directly paying tariffs, but still face cost increases for managing trade complications, investing in alternative sources or partners, and absorbing higher prices from U.S. counterparts through integrated supply chains.

On both fronts, we see risks mostly tilted towards more inflationary pressures, not less. If either of those risks were to materialize more tangibly, risks of BoC rate hikes as early as H2 2026 rise.

Bitcoin (BTC), Ethereum (ETH), and Solana (SOL) Levels for FOMC

Cryptocurrencies have traded up and down over the past week following a rough correction across the board.

*By the way, the Bank of Canada Press Conference is currently ongoing for those interesting, you can access it right here – No Cut for the BoC, 2.25% rate unchanged*

While key long-term support levels arrested the steep decline and dip-buyers stepped in, the market failed to hold its highs despite a strong session yesterday.

This afternoon's event will be critical for all asset classes, including crypto. Here is why:

FOMC events often trigger sharp swings between risk-on and risk-off sentiment.

As risk assets, cryptocurrencies often correlate with equities.

For example, during the 2023 hiking cycle, risk assets dumped lower, triggering massive selloffs in the crypto market.

Rate-cutting cycles typically boost non-yielding assets like Gold and Bitcoin.

On a straightforward basis, a cut should support higher prices, though the reaction will depend heavily on whether the Fed's guidance for 2026 is dovish.

If today's (highly probable) rate cut fuels risk appetite, Bitcoin and its peers should rise.

If sentiment becomes ecstatic, expect memecoins and altcoins to outperform; if the mood is positive but measured, look for market leaders like Bitcoin (BTC) , Ethereum (ETH), and Solana (SOL) to lead the charge.

As a matter of fact, let's explore the intraday charts and levels for these three crypto leaders to prepare for the rate decision, coming up in about three hours.

Bitcoin, Solana and Ethereum Technical Analysis

Bitcoin 8H Chart and levels

Bitcoin (BTC) 8H Chart, December 10, 2025 – Source: TradingView

Bitcoin rallied a strong 14% since reaching its $80,563 lows on November 21, bringing back intermediate momentum into balance (from heavily bearish).

Still, the chart doesn't point to immediate bullish domination – The RSI is going sideways. This arises particularly as sellers appeared at the highs of the bear channel, keep an eye on this one.

The dip-buying was a technical one, with the Crypto Leader retest its long-term support levels as seen in our previous analysis.

Things might change today however

FOMC Scenarios:

- A daily close above $94,000 points to a continued break higher. If the rest of the Market follows suit, a new uptrend might be found. A yearly close above $100,000 confirms the return of a long-term bullish environment.

- Hanging close within the $88,000 to $92,000 maintains the current hesitant picture.

- Close below $88,000 however may relaunch the bearish trend which can be dangerous for the Market outlook.

Levels of interest for BTC trading:

Support Levels

- $88,000 to $92,000 major support turned Pivot (testing

- November lows $80,563

- $85,000 mini Support (+/- $500)

- Liberation Day Support $75,000 to $80,000

Resistance Levels

- mini-resistance around $94,000

- Swing highs from yesterday $94,657 and highs to break

- $98,000 to $100,000 Main Resistance

- Resistance at previous ATH $106,000 to $108,000

- Current ATH Resistance $124,000 to $126,000

Ethereum (ETH) 8H Chart and levels

Ethereum (ETH) 8H Chart, December 10, 2025 – Source: TradingView

The idea is the same for Ethereum, but the breakout has been even-more solid.

Hence, traders may expect ETH outperformance if today's FOMC is bullish.

In a bearish case, ETH and other altcoins should outperform.

FOMC Scenarios:

- In a bullish session, a close above $3,400 continues the more bullish momentum found recently. Keep track of the upward trendline in this case.

- In a balanced FOMC session, prices should maintain between $3,000 to $3,300 indicating that traders will be looking to learn more – Rangebound action in this case.

- In a bearish session, ETH should close below $3,000 and relaunch the bearish prospects.

Levels of interest for ETH trading:

Support Levels

- $3,000 Psychological level and Pivot (+ 50 MA)

- $2,500 to $2,700 June Key Support (recent rebound)

- $2,620 Recent Lows

- $2,100 June War support

- $1,385 to $1,750 2025 Support

- 2025 Lows $1,384

Resistance Levels

- $3,400 Tuesday highs

- $3,500 (+/- $50) Resistance and Descending Channel highs

- $3,800 September lows

- $4,000 to Dec 2024 top Higher timeframe Resistance zone

- $4,950 Current new All-time highs

Solana (SOL) 8H Chart and levels

Solana (SOL) 8H Chart, December 10, 2025 – Source: TradingView

Solana has rebounded but still struggles to find upside momentum, holding its mid-October downwards channel.

The third largest crypto maintains a rangebound price action between $125 to $145.

FOMC Scenarios:

- Bullish case: Solana closes above $145 which would imply a return in the Crypto, and should increase odds of a channel breakout ($155 is the level to look)

- Neutral case: The crypto holds its ongoing range, not so bad considering how bearish the previous momentum was. It also holds the line for a future rebound

- Bearish case: Solana closes at the lows of its range, which may trigger a further selloff.

Levels to keep on your SOL Charts:

Support Levels

- Main Support $125 to $130 (Range lows)

- $110 to $115 Support

- Weekly lows $123

- Support 3: $100 to $105

Resistance Levels

- $140 to $150 Major Pivot (Range Highs)

- Channel highs and October Pivot resistance $165 to $170

- $180 to $190 Resistance

- Psychological level $200 to $205

- $253 Cycle highs

Safe Trades!

XAG/USD: Silver Hits New Record High Above $60

Silver hit new record high ($61.59) on Wednesday, in extension of Tuesday’s strong acceleration higher which resulted in a daily gain of 4.5% and break through psychological $60 barrier.

Silver continues to benefit from strong demand for safe haven, as well as an evident disbalance between industrial demand and supply.

Silver’s sharp rise in past six months was steeper than advance of gold that continued to push gold – silver ratio lower (in June, one ounce of gold was buying around a hundred ounces of silver, while today only 69 ounces of silver were needed to buy an ounce of yellow metal.

Today’s slight easing from new all-time high could be seen rather as positioning for further advance than as stronger pullback, as markets widely expect 25 basis rate cut by Fed and many anticipate that the US policymakers may adopt more dovish stance on rates in coming months (due to significant weakening in the labor sector and also that further easing in monetary policy is President Trump’s preferred scenario).

Broken $60 level now reverted to solid support which so far holds today’s action, with potential deeper dips to find firm ground above $58 (rising 10DMA) to keep bulls intact.

The price currently rides on the third wave of five-wave cycle from $45.53 (Oct 28 low) and probed through 138.2% Fibonacci expansion ($60.95).

Bulls eye targets at $62 (psychological) and $63.05 (Fibo 161.8% expansion).

Res: 61.59; 62.00; 63.05; 64.00

Sup: 60.00; 58.98; 58.00; 57.54

Bank of Canada Holds as Expected

The Bank of Canada (BoC) held its policy rate at 2.25%, in line with market expectations.

The opening statement highlighted that while tariffs and trade uncertainty continue to weigh on business investment, the economy has proven to be relatively resilient. However, it noted that measures of hiring intentions remain "subdued" despite the recent improvements in the labour market.

The Bank expects that inflation will continue to moderate in the coming months. There was emphasis that there could be some "choppiness" in inflation in the months ahead. Nonetheless this is expected to be temporary and there was again emphasis that underlying inflation remains “around 2.5%”.

Importantly the release maintained the statement that "[i]f inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment".

Key Implications

A sequence of strong employment reports lead to markets repricing the risk of a rate hike from the BoC next year. Dismissing the economy's resilience would be a mistake, however, the outlook remains challenging and the risks from trade uncertainty remain high.

The hold here was widely expected, and we maintain the view that the balance of risks to the outlook will have the Bank on hold in the coming months. Of course, uncertainty remains sky-high and with discussions about the renewal of the CUSMA trade agreement set to pick up (along with some delayed data), we expect the Bank of Canada to maintain its data dependent approach.

Sunset Market Commentary

Markets

The European morning session contained little more than the long-drawn waiting exercise that often precedes a Fed policy decision. EMU yields resumed their recent journey ‘north’ that accelerated on comments from ECB board member Schnabel on Monday. She ‘approved’ market pricing taking a rate hike as the ‘base case’ for the next ECB rate move. Market participants who still weren’t convinced as Schnabel is considered to be on the hawkish side of the ECB spectrum, got some more ‘neutral’ confirmation today. ECB Simkus, usually on the dovish side, also agrees that interest rates don’t have to be lowered any further as both inflation and growth recently printed stronger than expected and as risks on both have become fairly balanced. ECB Chair Lagarde in an interview at an FT event, agreed that the EMU economy had been more resilient than expected in the wake of the US tariff announcement in spring. The ECB already upgraded 2025 growth in September (from 0.9% to 1.2%) and might repeat that at next week’s staff projections. ECB’s Kazaks repeated that the bank is in a good place with inflation near 2% but warned that sticky core and services inflation ‘requires continued monitoring’. The ECB tomorrow enters its silent period ahead of the December 18 decision tomorrow. EMU (swap) yields currently trade off the intraday highs, but still add up to 2.5+ bps (2 & 5-y). The 2-y swap in this respect returned to the levels reached after German fiscal announcement early March. Longer maturities, affected by rising (fiscal) premia, even returned to the mid-2024 peak levels. As was often the case of late, the impact of moves in interest rate markets only had little impact on equities (Eurostoxx 50 -0.25%) or FX (EUR/USD little changed at 1.1635).

Awaiting this evening’s Fed decision, US yields understandably are changing less than 1 bp across the curve. The Fed is expected to proceed with another precautionary 25 bps rate cut (to 3.5%-3.75%) despite a highly divided MPC. Markets will keep a close eye at the new Summery of Economic Projections (dots) and any guidance from Fed Chair Powell. However, news from those sources will probably be highly conditional. Governors since the September forecast had little hard evidence on the labour market and even less on inflation to make substantial changes. One can expect the Fed chair to shift to an outright data-dependent narrative as the policy rate is coming closer to neutral. This puts the focus on data updates between now and Christmas (payrolls, CPI and Q3 GDP). With yields having rebounded/priced out more aggressive easing, there might again be room for some correction in case of softer data. Question is whether today’s FOMC meeting will already allow for such an interpretation/reaction.

News & Views

Norwegian inflation unexpectedly rose by 0.1% m/m in November, defying estimates for a slight 0.1% monthly drop. The annual print came in at 3% vs 2.7% expected but nevertheless a slight easing from October’s downwardly revised 3.1%. Norway’s central bank had 2.5% written down in the tables. The underlying measure on the other hand dropped a little more than analysts had penciled in, -0.3% m/m, lowering the yearly reading to 3% from 3.4%. Today’s numbers together with tomorrow’s regional business sentiment survey by the Norges Bank are the final input to next week’s monetary policy decision. With inflation still well above the 2% target, the central bank in all likelihood will keep rates steady at 4% and stick to the extremely gradual easing pace they’ve been communicating for some time now (one cut per year over the next three years). The Norwegian crown is slightly lower on the day with EUR/Nok moving towards 11.81.

The IMF in its annual review of China urged the country to make “the brave choice” in switching from an economy that’s nearing the growth limits via exports to a consumption-led model. The IMF called for additional fiscal stimulus and greater monetary easing while simultaneously take steps to rein in local debt and tackle a year’s long property crisis. It estimates the required spending for the latter to be around 5% of GDP. The IMF nevertheless upgraded its growth forecasts for China to 5% from 4.8% for this year and to 4.5% from 4.2% for 2026. Around a fifth of this year’s estimated 5% growth came on the account of net-exports, the IMF said, with a real depreciation of the Chinese currency having played a role. The IMF hasn’t formally called for China to pursue a stronger CNY, but did state that bolder stimulus could boost consumption and lift inflation (and the real CNY exchange rate) in the process.

BoC Confirms Long Pause, Markets Pivot to High-Stakes FOMC

Canadian Dollar eased modestly in early US trading after the BoC left its policy rate unchanged at 2.25%, as markets had fully expected. While the decision itself carried no surprises, the statement struck a slightly cautious tone on growth, prompting a mild pullback in CAD after its recent period of outperformance.

Policymakers reiterated that the bank has entered a long pause, but also highlighted that uncertainty surrounding the growth outlook remains elevated. Q4 GDP is expected to be weak, and the anticipated recovery in 2026 could still be derailed by trade volatility, structural headwinds and the ongoing adjustments to supply chains.

Even so, the BoC made clear it is not preparing to adjust interest rates again soon. With inflation expected to hover near target and domestic slack offsetting cost pressures tied to trade reconfiguration, policymakers see little justification for further moves unless a drastic shock emerges. That message keeps the easing cycle firmly in the rear-view mirror.

Attention now shifts to the FOMC decision later today. A 25bps cut is fully priced and universally expected, making the headline move largely irrelevant for markets. Instead, traders will focus on how the Fed shapes expectations for 2026 through the dot plot, the vote split, the statement, and Chair Jerome Powell’s press conference. With so many variables, volatility is almost guaranteed.

Away from North American monetary policy, the IMF raised its forecast for China’s 2026 economic growth by 0.3 percentage points to 4.5%, citing stronger domestic stimulus and lower-than-expected tariff effects. However, the Fund also made clear that China must accelerate its transition toward consumption-led growth.

IMF Managing Director Kristalina Georgieva argued that China is now too large an economy to rely on export-driven expansion. “Continuing to depend on export-like growth risks furthering global trade tensions,” she said, adding that accelerating the shift toward domestic demand would be “beneficial for China” and for the global economy.

Her comments coincided with a stark warning from the European Union Chamber of Commerce in China. The group said European companies are accelerating diversification away from Chinese supply chains as Beijing’s self-reliance agenda and export controls deepen uncertainty. The EU trade imbalance with China has widened to 1:4 in container terms, from 1:2.7 in 2019, exacerbated by persistent deflation and Yuan depreciation.

EU Chamber President Jens Eskelund highlighted that China has now recorded 37 consecutive months of factory-gate deflation. “When we have this gap between deflation in China and inflation in Europe, that adds to the imbalance in currency,” he said.

For the week so far, Swiss Franc is currently the best performer, followed by Kiwi, and then Dollar. Yen is still the weakest, followed by Loonie, and then Aussie. EUro and Sterling are positioning in the middle.

In Europe, at the time of writing, FTSE is up 0.25%. DAX is down -0.52%. CAC is down -0.40%. 10-year yield is up 0.022 at 4.526. Germany 10-year yield is up 0.011 at 2.868. Earlier in Asia, Nikkei fell -0.10%. Hong Kong HSI rose 0.42%. China Shanghai SSE fell -0.23%. Singapore Strait Times fell -0.03%. Japan 10-year JGB yield fell -0.001 to 1.963.

BoC holds steady, points to weak Q4 GDP and balanced inflation outlook

The BoC kept the overnight rate unchanged at 2.25% today, in line with expectations. The most notable element of the statement was the Governing Council’s assessment that, if inflation and economic activity evolve broadly as projected in October, the current policy rate is “about the right level.” This marks a clear signal that the easing cycle has effectively ended and that the bank has entered a long period of steady policy barring major surprises.

The statement acknowledged mixed growth dynamics heading into year-end. The Bank expects final domestic demand to expand in Q4, but weakness in net exports will leave overall GDP “likely weak.” Growth is projected to firm in 2026, though policymakers warned that uncertainty remains elevated and that swings in trade flows could continue to create quarter-to-quarter volatility.

Employment has posted solid gains over the past three months and the unemployment rate declined to 6.5% in November. However, job markets in trade-sensitive sectors “remain weak,” and economy-wide hiring intentions are still "subdued"—reflecting the broader drag from structural trade reconfiguration.

Despite these pressures, BoC expects the ongoing economic slack to counterbalance cost increases associated with shifting trade patterns. As a result, CPI inflation is still anticipated to stay close to the 2% target, providing the BoC with scope to maintain a steady hand for the foreseeable future.

China CPI hits 21-month high, but weak demand keeps PPI in deep negative

China’s November inflation data paint a picture of an economy showing modest signs of surface-level improvement while still grappling with entrenched deflationary pressures.

CPI accelerated from 0.2% yoy to 0.7% yoy, matching expectations and marking a 21-month high. The gain was driven primarily by food prices, which rose 0.2% yoy after a -2.9% yoy drop in October. Core inflation held steady at 1.2% yoy, while energy prices slid -3.4% yoy—an even deeper decline than the prior month.

On a monthly basis, CPI fell -0.1% mom after October’s 0.2% mom increase, contrary to expectations for another rise.

PPI slipped from –2.1% yoy to –2.2% yoy, extending China’s factory-gate deflation streak into a fourth year. Manufacturers continue to cut prices aggressively to clear excess supply, a sign that domestic and external demand remain too weak to absorb output.

Coal mining prices tumbled -11.8% yoy, while the oil and gas extraction sector saw a -10.3% yoy decline—deep drops that suggest little improvement in industrial profitability.

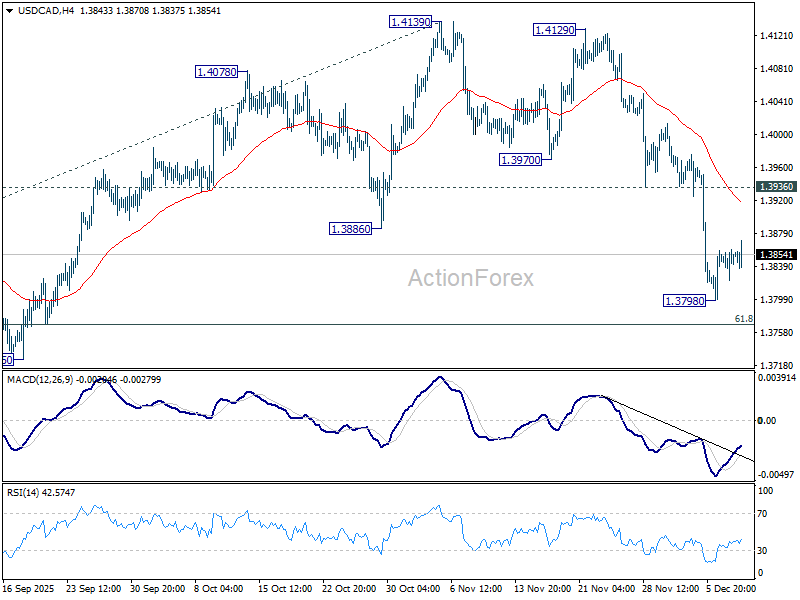

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3826; (P) 1.3844; (R1) 1.3863; More...

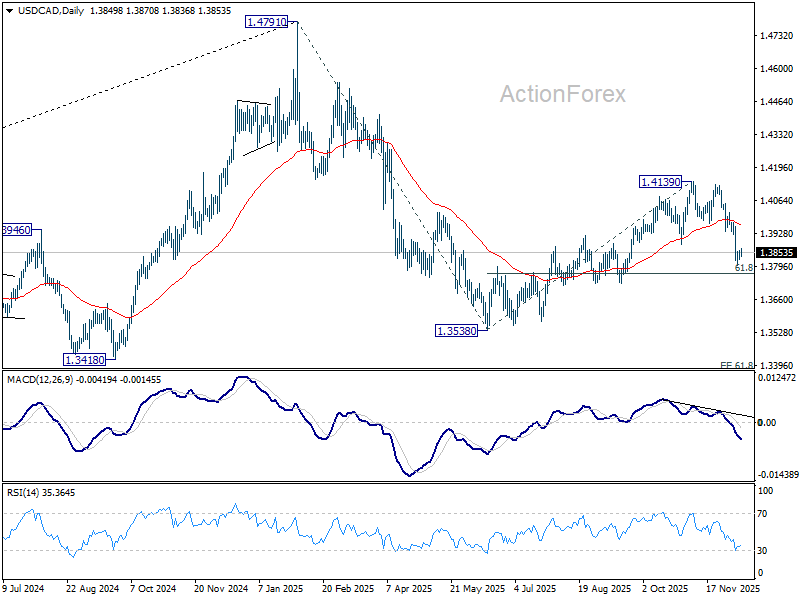

USD/CAD recovers mildly in early US session but outlook is unchanged. Intraday bias stays neutral and more consolidations could be seen. Upside of recovery should be limited below 1.3936 support turned resistance. On the downside, break of 1.3798 will resume the fall from 1.4139 to 61.8% retracement of 1.3538 to 1.4139 at 1.3768. Firm break there will argue that whole decline form 1.4791 might be ready to resume through 1.3538 low.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it's just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3826; (P) 1.3844; (R1) 1.3863; More...

USD/CAD recovers mildly in early US session but outlook is unchanged. Intraday bias stays neutral and more consolidations could be seen. Upside of recovery should be limited below 1.3936 support turned resistance. On the downside, break of 1.3798 will resume the fall from 1.4139 to 61.8% retracement of 1.3538 to 1.4139 at 1.3768. Firm break there will argue that whole decline form 1.4791 might be ready to resume through 1.3538 low.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it's just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.