Sample Category Title

Nasdaq 100: Post-FOMC Gains Wiped Out, But Technicals Still Bullish

Key takeaways

Post-FOMC optimism faded fast, with S&P 500 and Nasdaq 100 futures reversing sharply on renewed US–China tensions and concerns over AI-related export violations tied to DeepSeek.

Sentiment worsened after Oracle’s 11.5% after-hours plunge, as weak revenue reignited worries over stretched AI valuations and dragged index futures lower.

Despite the pullback, Nasdaq 100 technicals remain constructive, with improving market breadth and key supports holding, keeping the medium-term bullish reversal bias intact.

MP OEL_MultiAsset_Variant2

The post-FOMC rally quickly fizzled in today’s Asia session, with S&P 500 and Nasdaq 100 E-mini futures falling -0.8% and -1.1%, effectively wiping out Wednesday’s gains.

The pullback appears driven by renewed US-China geopolitical tension after reports that Chinese AI firm DeepSeek obtained smuggled Nvidia Blackwell chips, hardware banned for export to China, to build its next-generation model.

Sentiment was further hit by an 11.5% plunge in Oracle’s after-hours trading following weaker-than-expected Q2 revenue, reigniting concerns over stretched AI valuations and feeding into index futures weakness.

Despite the current intraday weak sentiment in the US futures, technicals are not suggesting the potential start of a medium-term downtrend phase for the Nasdaq 100.

Let’s dive deeper into several technical elements that are still constructively bullish.

Nasdaq 100 market breadth has improved in the past three weeks

Fig. 1: Percentage of Nasdaq 100 component stocks trading above 20-day & 50-day moving averages as of 10 Dec 2025 (Source: TradingView)

Based on the percentage of Nasdaq 100 component stocks that are trading above their respective 20-day and 50-day moving averages, there has been a significant improvement since 17 November 2025, after the three-week down move seen in the Nasdaq 100 from its current all-time high in late October 2025, triggered by AI bubble fears and weakness in the share price of Nvidia ex-post earnings.

The share of Nasdaq 100 component stocks trading above their 20-day moving average has surged to 65%, up sharply from 23% on 17 November 2025.

Similarly, the proportion trading above the 50-day moving average has risen to 56%, from 28% on 17 November 2025, though at a more gradual pace (see Fig. 1).

Peferred trend bias (1-3 weeks) – Bullish reversal remains intact

Fig. 2: US Nasdaq 100 CFD Index medium-term trend as of 11 Dec 2025 (Source: TradingView)

The potential bullish reversal that has taken form on the Nasdaq 100 CFD Index (a proxy of the Nasdaq 100 E-mini futures) since the 21 November 2025 low of 23,840 remains intact.

Medium-term pivotal support rests on 25,165 to maintain the bullish bias, and a clearance above 25,745 potential upside trigger level, is likely to increase the odds of a new bullish impulsive up move sequence to retest the current all-time high at 26,288 before the next medium-term resistance comes in at 26,480/26,545 (Fibonacci extension) (see Fig. 2).

Key elements

- Price actions of the Nasdaq 100 CFD Index continue to trade above its rising 20-day and 50-day moving averages since 26 November 2025.

- The 4-hour RSI momentum indicator has pulled back and just staged a rebound right above a key ascending support, which suggests a potential medium-term bullish momentum revival for the Nasdaq 100 CFD Index.

Alternative trend bias (1 to 3 weeks)

Failure to hold at the 25,165 key medium-term pivotal support invalidates the bullish scenario to kick-start a deeper corrective decline on the Nasdaq 100 CFD Index to retest the next medium-term supports at 24,540 and 24,000 (critical swing low areas of 10 October 2025 and 21 November 2025).

GBP/USD Approaches Local High, Bolstered by BoE Stance

The GBP/USD pair advanced to 1.3367 on Thursday, stabilising near its highest level since 22 October. Sterling is drawing support from a confluence of factors: a broadly weaker US dollar and a market reassessment that has scaled back expectations for additional Bank of England (BoE) monetary easing in 2026.

This follows yesterday’s Federal Reserve meeting, where the US central bank delivered a widely anticipated 25-basis-point rate cut. Crucially, the Fed signalled a potential pause in its easing cycle as early as January, emphasising the need for more economic data before determining the next steps.

Expectations for the BoE’s meeting next week remain firmly anchored. The market continues to price in an 84% probability of a 25-basis-point cut, largely overlooking recent data showing accelerating wage growth and persistent inflationary pressures. Furthermore, investors are almost fully pricing in a second rate cut by June, with a 75% chance assigned to an initial move as soon as April.

Market focus now shifts to the UK’s monthly GDP report, due on Friday, which could prompt a final adjustment to monetary policy expectations ahead of the BoE decision.

Technical Analysis: GBP/USD

H4 Chart:

On the H4 chart, GBP/USD exhibits a strong upward bias, trading just below the key technical resistance at 1.3392. The pair’s position firmly above the middle Bollinger Band confirms the dominance of buyers. The expansion of the upper band signals rising volatility and suggests the market is building momentum for another attempt to breach this barrier.

A decisive breakout and close above 1.3392 would be a significant bullish development, opening the path towards the next resistance zone of 1.3420–1.3452. Should a reversal occur, the nearest notable support is at 1.3280. A breach of this level would indicate a deeper corrective phase, likely targeting the lower Bollinger Band.

H1 Chart:

On the H1 chart, the pair is undergoing a near-term correction following its impulsive rise to the 1.3390–1.3392 resistance zone. It is currently finding support above 1.3360, a level from which a prior recovery originated.

The upper Bollinger Band has flattened after a period of sharp expansion, indicating short-term overbought conditions and increasing the likelihood of a consolidation or shallow pullback. Despite this, the overall H1 structure remains bullish, with the price above the middle band and the lower band providing dynamic support.

A sustained break above 1.3392 would signal a resumption of the uptrend, targeting 1.3420 and potentially 1.3450. Conversely, a loss of the 1.3360 support would be the first technical sign of weakening bullish momentum, potentially triggering a correction towards the next demand zone in the 1.3300–1.3280 range.

Conclusion

GBP/USD is trading with conviction, supported by shifting central-bank dynamics that have turned modestly in sterling’s favour. The technical setup is bullish but faces a critical test at the 1.3392 resistance level. A successful breakout would validate the strength of the current move, while a rejection could see the pair retreat to consolidate recent gains. The upcoming UK GDP data will provide the final fundamental cue before the highly anticipated BoE meeting next week.

Dollar Index Chart Analysis After the Fed Decision

Following yesterday’s FOMC interest rate decision and Jerome Powell’s press conference, the US Dollar Index (DXY) dropped sharply to point A.

On one hand, the 0.25% rate cut makes the dollar less attractive for capital preservation and yield. On the other, the prospect of a pause before further cuts provides some support.

Thus, the current level represents the market’s attempt to establish a fair valuation for the US currency.

Technical Analysis of the DXY Chart

Three days ago, we:

→ updated the system of two trend channels;

→ noted signs of seller dominance;

→ highlighted the formation of a consolidation zone.

Yesterday’s decline prompted an extension of the blue upward channel formed in October–November. Key insights from recent price action include:

→ the consolidation zone (marked by black lines) was broken after the median of the red channel acted as resistance (indicated by the arrow);

→ the price fell to the lower boundary of the red channel;

→ the former support around 98.78 acted as resistance this morning (marked by the second arrow);

→ the RSI indicator is near oversold levels, reflecting ongoing selling pressure.

Considering the above, a scenario of further downward movement along the lower boundary of the red channel seems plausible. If this develops, the price may fall to the lower boundary of the blue channel, which could serve as a key support level.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Nasdaq 100 Chart Analysis After the Fed Decision

The Nasdaq 100 index (US Tech 100 mini on FXOpen) showed sharp volatility yesterday following the interest rate announcement. The market action can be interpreted as follows:

→ First, the FOMC decision was released: as expected, the Federal Funds Rate was cut from 4.00% to 3.75% (a bullish catalyst), which pushed the index up towards point A.

→ However, half an hour later Jerome Powell’s press conference began, and his tone was noticeably hawkish (a bearish catalyst). The Fed Chair signalled that the rate-cutting cycle has been paused because inflation remains elevated and additional labour-market data is needed. As a result, the index fell sharply from point A to the low at point B.

Meanwhile, Donald Trump criticised the Fed’s decision, arguing that rates should be cut far more aggressively. This adds to uncertainty, especially given expectations that Powell will leave his post in May 2026.

Bearish pressure on the tech index intensified further after Oracle’s earnings release — see yesterday’s post for details. The results disappointed investors, fuelling renewed talk of an AI bubble, and ORCL shares plunged around 11% in after-hours trading.

Technical Analysis of the Nasdaq 100 Chart

Looking at recent price action in the Nasdaq 100 (US Tech 100 mini on FXOpen), the index appears to be forming a bearish Rounding Top pattern:

→ The peak at point A resembles a bull trap, as the price only slightly exceeded the December highs before reversing — in SMC terms, a sign of a bearish liquidity grab.

→ The price then broke support from several recent sessions around 25,570 after forming a large bearish candle (marked by the arrow). This indicates strong selling pressure (a market imbalance) and the area may now act as resistance.

It is possible that bulls will attempt to recover some of yesterday’s losses today. However, if any rebound stalls near this resistance zone, the Nasdaq 100 (US Tech 100 mini on FXOpen) may continue to drift lower along a rounding downward trajectory.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

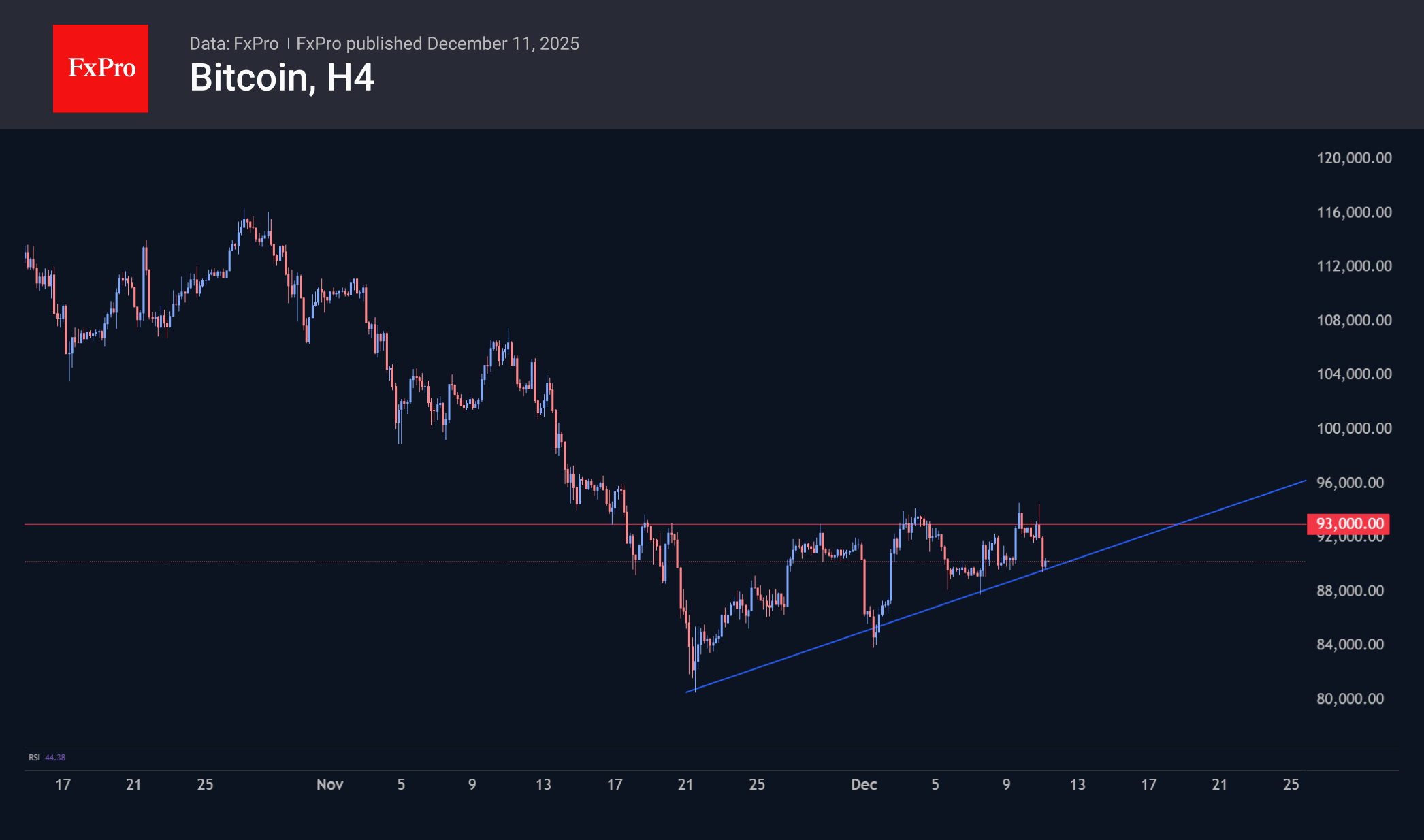

Bitcoin Attempts to Break the Short Uptrend

Market overview

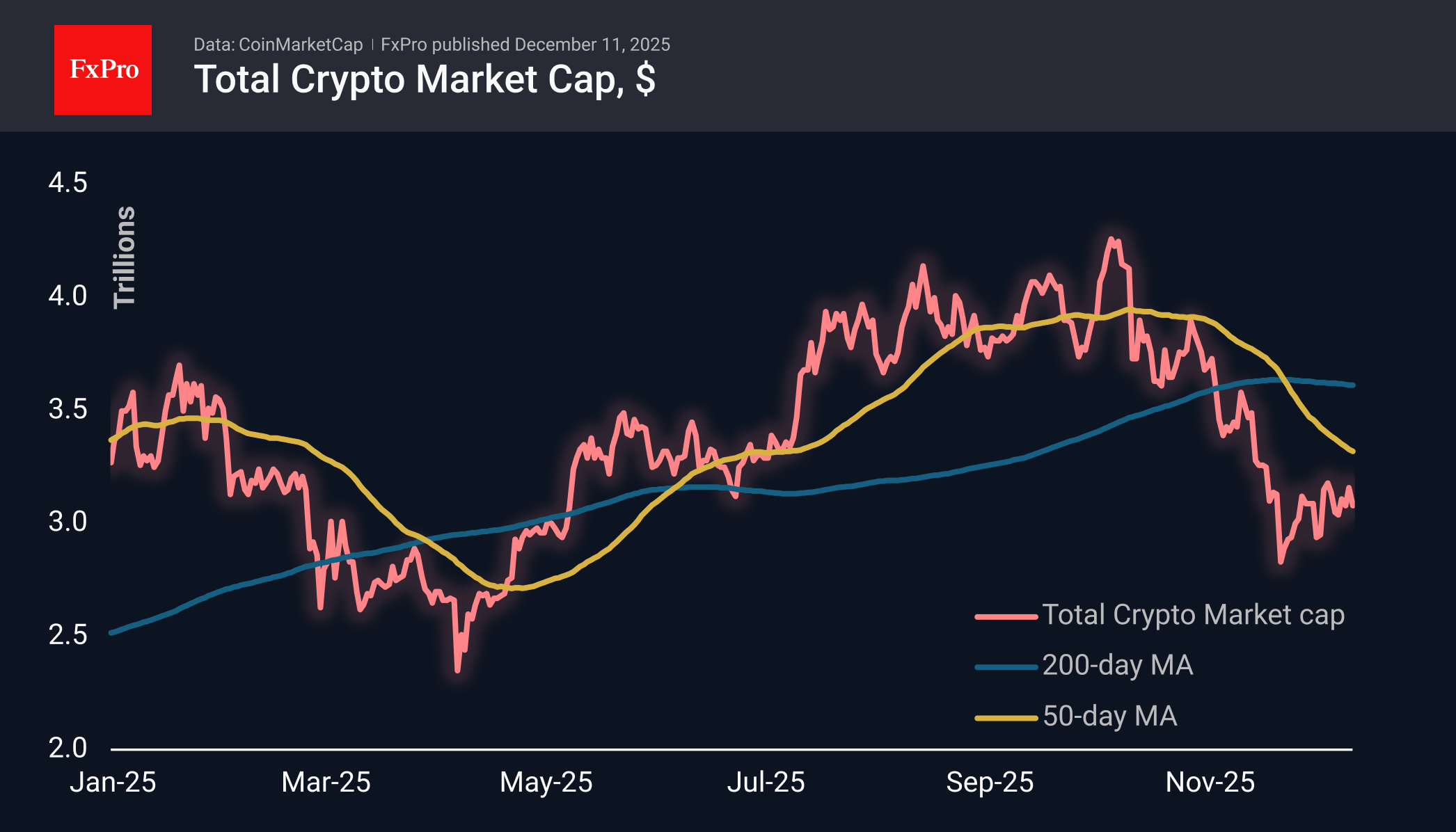

The crypto market cap has been in a see-saw pattern over the past three weeks, exhibiting a gentle uptrend that has returned to the $3.08 trillion level during a consolidation phase. With no clear trend, crypto traders have reduced their activity in altcoins, waiting for the trend to recover in the first cryptocurrency and key stock indices.

Bitcoin jumped to $94.5K on Wednesday evening in response to the Fed’s announcement of a bond-buying programme and a key rate cut. But this link to stocks played a cruel joke. The fall in Oracle shares dragged the Nasdaq-100 to eight-day lows, and BTC rolled back to $90K. The market is testing the strength of the modest uptrend that has been forming since 21 November. A drop below $88K would break this trend, bolster bearish sentiment and confirm the end of the recovery rally.

News background

Public and private companies have increased their Bitcoin reserves by 448% since the beginning of the year to 1.08 million BTC, according to Glassnode. The corporate sector remains a key driver of demand for digital gold.

ARK Invest CEO Cathie Wood believes that large companies buying cryptocurrency for long-term storage could prevent BTC from falling 75-90% as it has in the past.

Strategy founder Michael Saylor announced the company’s plans to acquire as much Bitcoin as possible. Mayside Partners believes that such plans are economically unsound. This is not innovation, but cascading leverage on speculative collateral — a model that has failed time and time again.

The American Federation of Teachers (AFT) has called on the US Senate to withdraw the cryptocurrency bill on ‘responsible financial innovation,’ which will be considered next week. The organisation pointed to the risks to pension savings and the country’s economy.

Twenty One Capital, a big Bitcoin holder, has entered the stock market. The company’s shares fell 20% on their first day of trading on the NYSE. The firm ranks third among public holders of the first cryptocurrency with 42,000 BTC (~$3.9 billion).

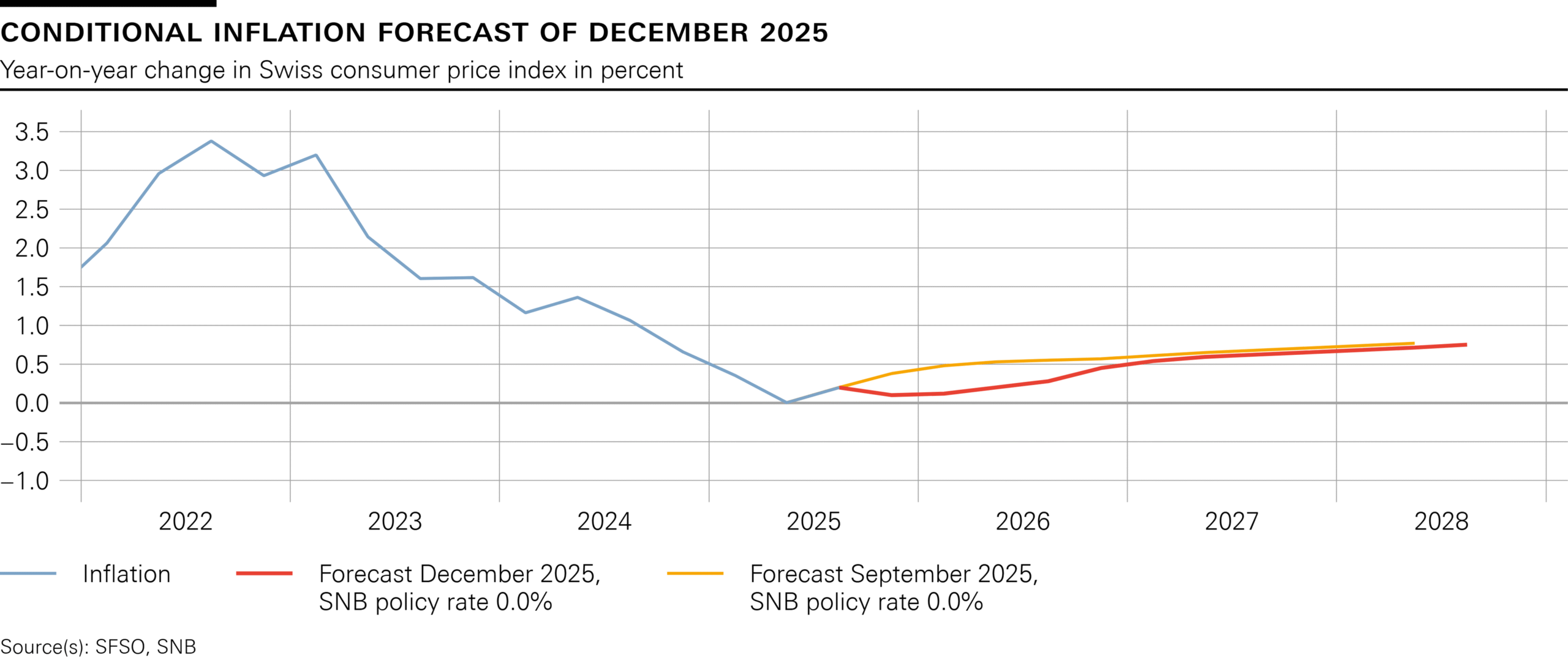

SNB holds at 0.00%, medium term inflation outlook virtually unchanged.

SNB left its policy rate unchanged at 0.00%, as widely expected, and reiterated its readiness to intervene in foreign exchange markets if necessary. The hold reflects the bank’s assessment that current conditions do not justify a shift, even as inflation undershot expectations.

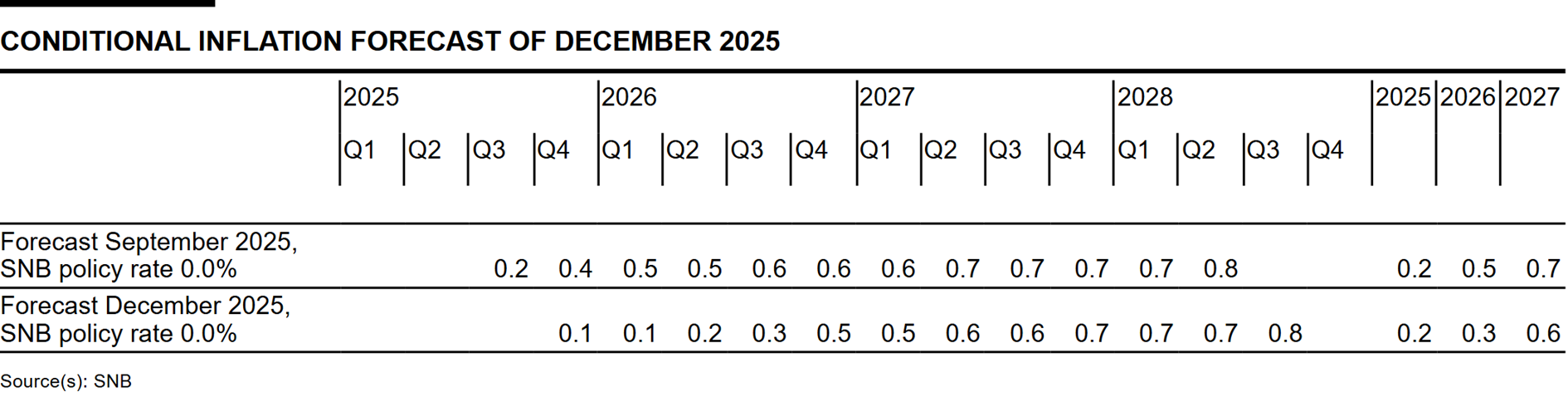

In its statement, the SNB noted that inflation has been slightly weaker than anticipated in recent months, but emphasized that medium-term pressures are “virtually unchanged” compared with September. The conditional inflation forecast is marginally lower in the near term but shows little change beyond that. The Bank now sees inflation averaging 0.2% in 2025, 0.3% in 2026 and 0.6% in 2027, based on the assumption of a 0% policy rate throughout the forecast horizon.

The economic outlook for Switzerland has "improved slightly", helped by reduced U.S. tariffs and a modestly better global backdrop. SNB now expects GDP to grow just under 1.5% in 2025 and around 1% in 2026, though it cautioned that unemployment is likely to edge higher.

(SNB) Swiss National Bank leaves SNB policy rate unchanged at 0%

The Swiss National Bank is leaving the SNB policy rate unchanged at 0%. Banks' sight deposits held at the SNB will be remunerated at the SNB policy rate up to a certain threshold. The discount for sight deposits above this threshold still stands at 0.25 percentage points. The SNB remains willing to be active in the foreign exchange market as necessary.

Inflation in recent months has been slightly lower than expected. In the medium term, however, inflationary pressure is virtually unchanged compared to the last monetary policy assessment. The monetary policy helps to keep inflation within the range consistent with price stability and supports economic development. The SNB will continue to monitor the situation and adjust its monetary policy if necessary, in order to ensure price stability.

Inflation has declined slightly since the last monetary policy assessment. It decreased from 0.2% in August to 0.0% in November. Lower inflation in the hotel industry, as well as for rents and clothing, contributed in particular to this decline.

Inflationary pressure in the medium term is virtually unchanged compared to the previous quarter. Although the conditional inflation forecast is somewhat lower in the short term than in September, there is only little change in the medium term. The forecast is within the range of price stability over the entire forecast horizon (cf. chart). It puts average annual inflation at 0.2% for 2025, 0.3% for 2026 and 0.6% for 2027 (cf. table). The forecast is based on the assumption that the SNB policy rate is 0% over the entire forecast horizon.

Global economic growth was stronger than expected in the third quarter. Although US tariffs and trade policy uncertainty weighed on the global economy, economic development in many countries has thus far remained more resilient than had been assumed. Inflation remained elevated in the US, while in the euro area it was close to target.

In its baseline scenario, the SNB anticipates that growth in the global economy will be moderate over the coming quarters. Inflation in the US is likely to remain elevated for some time. In the euro area, on the other hand, inflation is expected to stay close to target.

Uncertainty has decreased somewhat compared to the last monetary policy assessment. That said, the baseline scenario for the global economy is still subject to significant risks. For example, US tariffs and trade policy uncertainty could yet weigh more heavily on global economic momentum than observed thus far. It is also possible that trade barriers may be raised again. At the same time, however, it cannot be ruled out that the global economy will continue to develop better than expected in the coming quarters.

Swiss GDP contracted in the third quarter. The decline was due in particular to the pharmaceuticals industry. Value added there had risen strongly in the first quarter because deliveries to the US had been brought forward in anticipation of possible tariffs. There was a countermovement in the second quarter, which continued in the third quarter. Value added rose slightly in the other manufacturing industries and in services. Owing to this subdued economic development overall, unemployment has risen further in recent months.

The economic outlook for Switzerland has improved slightly due to the lower US tariffs and somewhat better development globally. For 2025 as a whole, the SNB expects GDP growth of just under 1.5%. For 2026, it expects growth of around 1%. In this environment, unemployment is likely to continue to rise somewhat.

The main risk to the economic outlook for Switzerland is the development of the global economy.

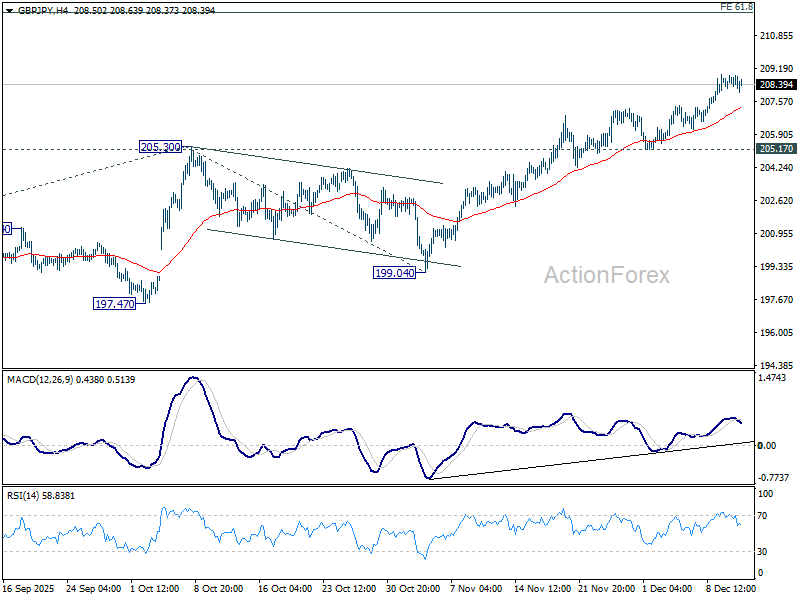

GBP/JPY Daily Outlook

Daily Pivots: (S1) 208.38; (P) 208.64; (R1) 209.04; More...

Intraday bias in GBP/JPY remains mildly on the upside for the moment. Current up trend should target 61.8% projection of 184.35 to 205.30 from 199.04 at 211.98. Outlook will stay bullish as long as 205.17 support holds, in case of retreat.

In the bigger picture, up trend from 123.94 (2020 low) is resuming. Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. On the downside, break of 199.04 support is needed to be the first sign of medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 182.11; (P) 182.36; (R1) 182.72; More...

Intraday bias in EUR/JPY remains on the upside for the moment. Current up trend should target 100% projection of 161.06 to 173.87 from 171.09 at 183.90. For now, outlook will remain bullish as long as 180.07 support holds, in case of retreat.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, considering bearish divergence condition in D MACD, upside should be capped by 186.31 on first attempt. Outlook will continue to stay bullish as long as 55 W EMA (now at 170.25) holds, even in case of deep pullback.

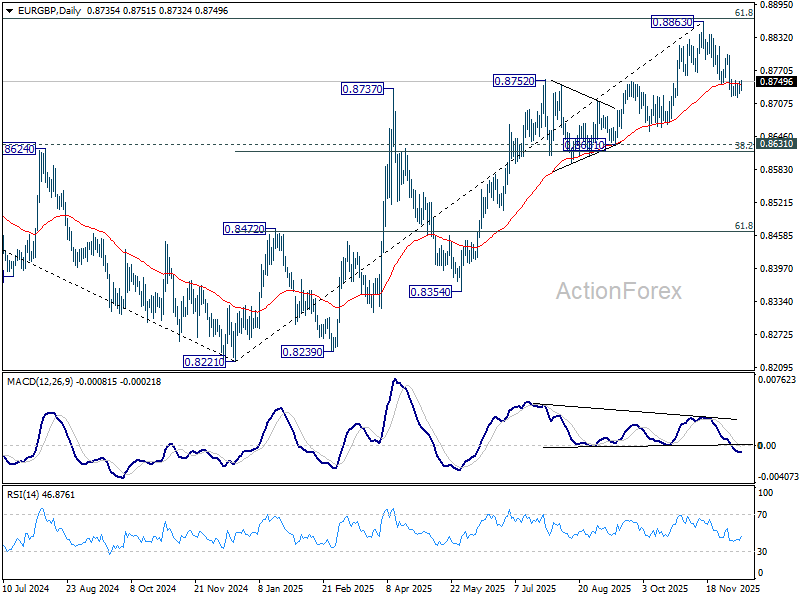

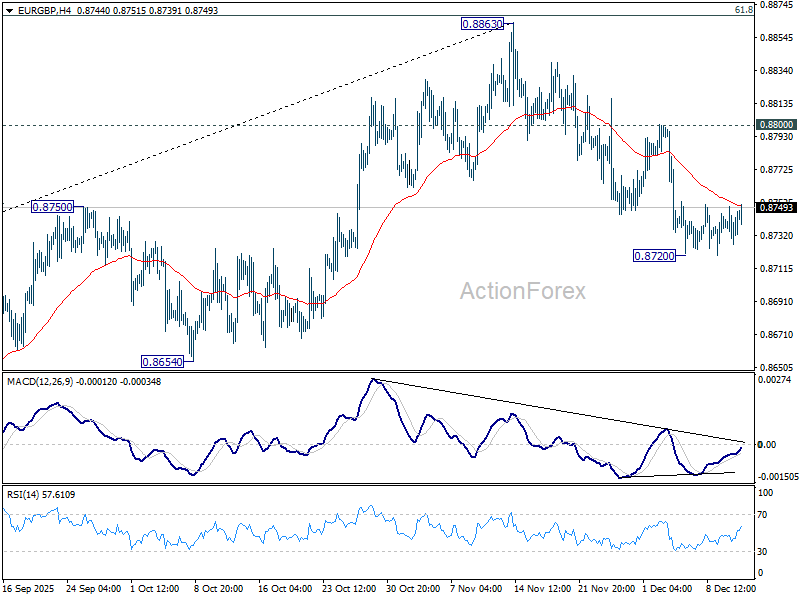

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8728; (P) 0.8740; (R1) 0.8751; More…

Intraday bias in EUR/GBP remains neutral and more consolidations could be seen. With 0.8800 resistance intact, further decline is expected. Fall from 0.8863 should at least be a correction to the up trend from 0.8221, with risk of bearish reversal. Below 0.8720 will target 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618).

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8600) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.