Sample Category Title

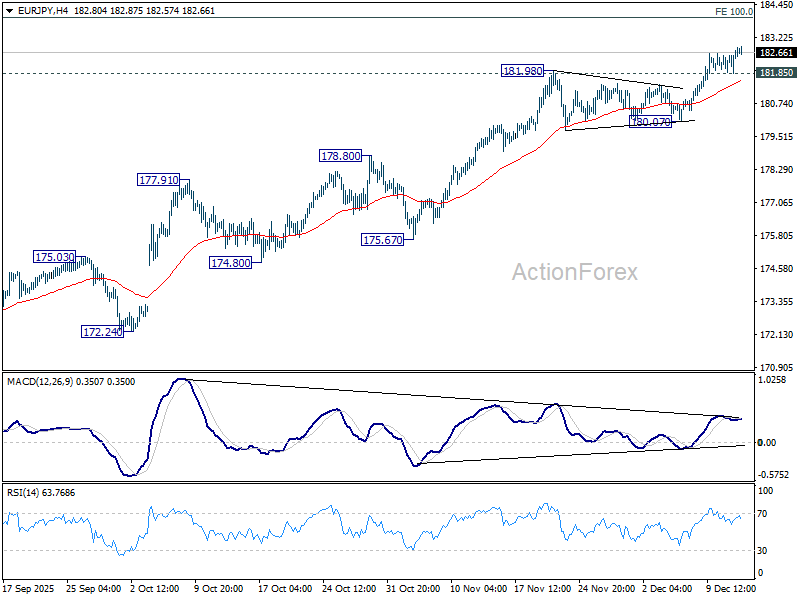

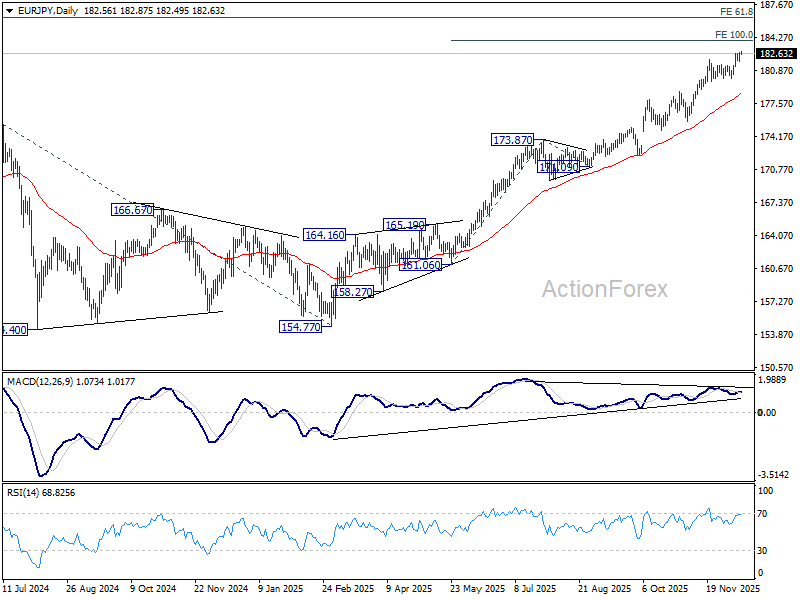

EUR/JPY Daily Outlook

Daily Pivots: (S1) 182.08; (P) 182.42; (R1) 182.95; More...

EUR/JPY's rally is still in progress and intraday bias stays on the upside. Current up trend should target 100% projection of 161.06 to 173.87 from 171.09 at 183.90. On the downside, below 181.85 minor support will turn intraday bias neutral first. But outlook will remain bullish as long as 180.07 support holds, in case of retreat.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, considering bearish divergence condition in D MACD, upside should be capped by 186.31 on first attempt. Outlook will continue to stay bullish as long as 55 W EMA (now at 170.25) holds, even in case of deep pullback.

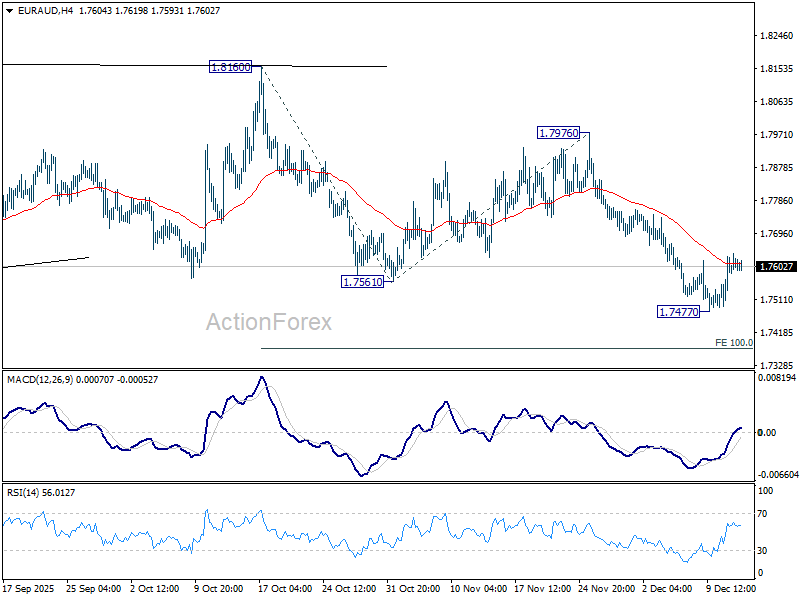

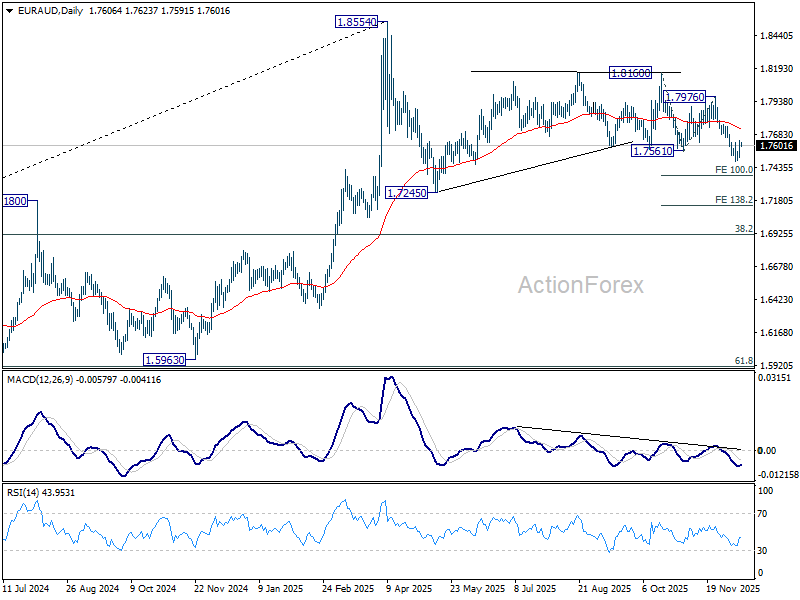

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7528; (P) 1.7585; (R1) 1.7671; More...

Intraday bias in EUR/AUD remains neutral as consolidations continue above 1.7477 temporary low. Outlook is unchanged that fall from 1.8160 is seen as the third leg of the pattern from 1.8554. Below 1.7477 will target 100% projection of 1.8160 to 1.7561 from 1.7976 at 1.7377. This will remain the favored case as long as 55 D EMA (now at 1.7726) holds.

In the bigger picture, as long as 55 W EMA (now at 1.7456) holds, price actions from 1.8554 could still be a correction to rise from 1.5963 only. However, sustained break of the EMA will argue that it's already correcting the whole up trend from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922.

Fed Has Reappointed All But One of the 12 Regional Branches

Markets

(US) markets yesterday continued the constructive reaction after Wednesday Fed policy meeting. (The pace of) any further easing has become highly depended on US data update starting next week and continuing in January. Even as Fed Chair Powell indicated that a follow-up rate cut in January isn’t evident, markets still keep the option open that some more precautionary easing is still might come relatively soon in case of softer labour market data. Early in US dealings, yields extended Wednesday’s decline. A jump in weekly jobless (from an extremely low of 192k to an very high 236k) was probably was too much distorted due to Thanksgiving to provide any additional insight on the status of the US labour market. The US yield-decline slowed as the session proceeded and even reversed. US yield finished the day marginally higher (2-y +0.2 bp; 30-y +1.3 bp). A $ 22 bln 30-y Treasury auction went ‘neutral’ and had little impact on trading. EMU yields entered a consolidation modus after recent rise. Markets after recent positive ECB comments on growth have now fully embraced the scenario that the ECB is done with its easing cycle. The debate on the timing of a potential first hike (turn of 2026/2027?) has started. Next week’s EMU PMI’s and the new growth forecasts in December ECB staff projections in this respect are next potential input for EMU interest rate markets to shape their view/expectations. (US) equity markets (except for the Nasdaq) closed near (S&P 500) or even at record levels (Dow Jones +1.34%). The (productivity driven) growth upgrade in the Fed dots probably still was a supportive factor. The EuroStoxx 50 also added 0.8% and is only about 1% away from the mid-November top. The mild US interest rate markets, a risk-on sentiment and the likes of the ECB or the BOJ moving in a different direction compared to the Fed, finally pushed the dollar below some first minor support levels. DXY closed at 98.35. EUR/USD regained the 1.17 big figure (close 1.1738). USD/JPY eased to 155.6, but the yen underperformed the euro, with EUR/JPY still setting minor now all-time highs (currently 182.8).

Risk sentiment in Asia remains constructive this morning, with indices often showing gains of 1%+. The eco calendar in the US and EMU is almost empty. We keep an eye at the first comments from individual Fed members in the wake of this week’s meeting. Today Fed’s Paulson, Fed’s Hammack and Fed Goolsbee (additional dissenter at this week’s decision) are scheduled to speak. Even after Fed Powell’s cautious guidance on the room for further easing, we still err to the side that US yields and the dollar stay vulnerable to softer than expected US activity data. This morning, UK October monthly GDP (-0.1% M/M) and other activity data (Industrial production +1.1% M/M, but services activity -0.3%) were little inspiring. Sterling (and UK gilts) got some reprieve after the release of the UK budget end last month, but a (technical insignificant) rebound of sterling (against the euro) this week ran into resistance in the EUR/GBP 0.872 area. Ongoing weak data and the prospect of further BoE easing probably might keep sterling in the defensive. EUR/GBP gains marginally further this morning (0.877).

News & Views

Bulgarian prime minister Zhelyazkov resigned yesterday after being in office for less than a year. Zhelyazkov’s minority government’s proposed 2026 budget which included tax rises and increased spending sparked widespread anti-corruption protests. While the budget was eventually withdrawn, the protests continued. Parliament was due to hold a vote of confidence, the sixth one since being in power, just minutes before Zhelyazkov’s announcement. The leader of the ruling Gerb party now has a chance to appoint a new premier, but already signaled that he won’t. It’s then up to the second-largest faction to give it a shot but that’s unlikely to so succeed in gathering enough support. Instead new elections are the most plausible outcome. That would be the eighth over the past four years. The political chaos doesn’t thwart Bulgaria’s approved and planned accession to the euro zone on January 1.

The Fed has reappointed all but one (Bostic, due to early retirement next year) of the 12 regional branches for new five-year terms starting March 1. The decision was made unanimous. The process usually gets little attention but this time around was different. The reappointment needs approval from the Board of Governors, which US president Trump had been trying to get a majority in with hand-picked candidates. That could in theory have blocked and steered the reappointment process in favour of candidates that are more Trump-minded. The NY regional chief has a permanent vote on monetary policy while of the remaining 11, four receive annually alternating voting seats.

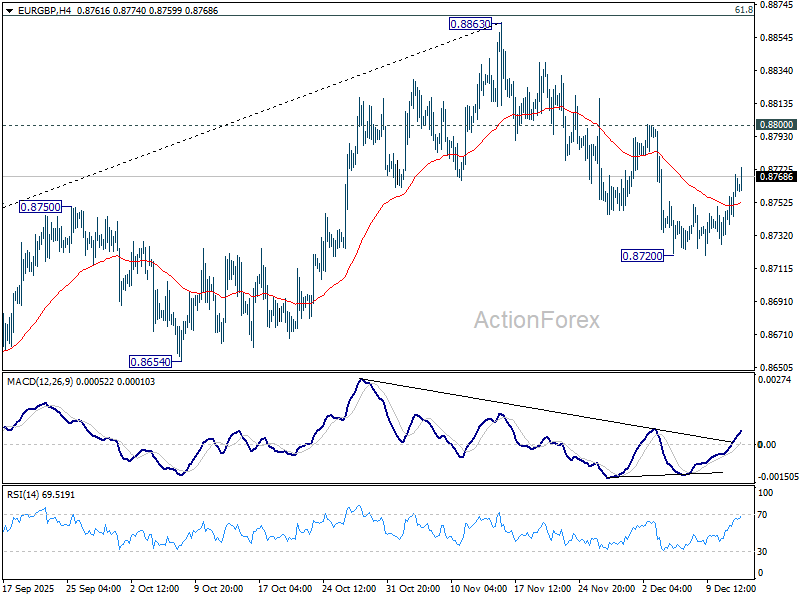

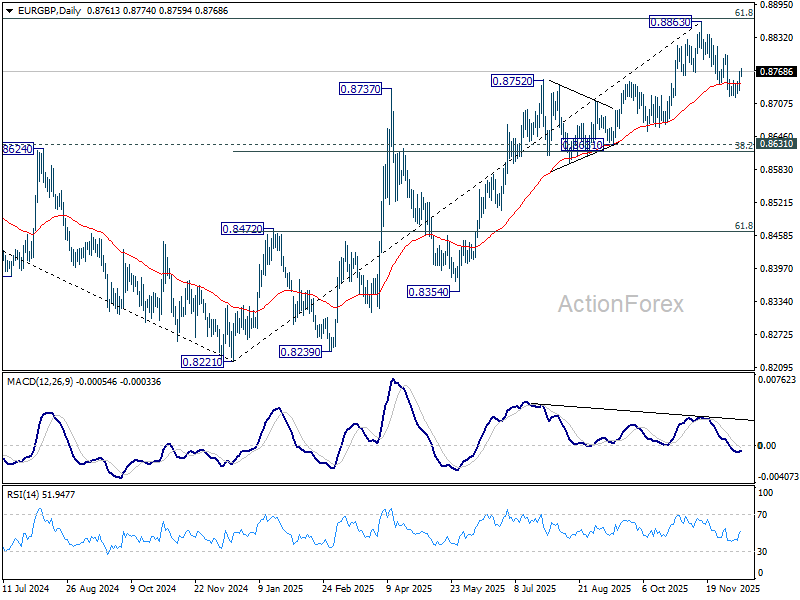

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8745; (P) 0.8759; (R1) 0.8783; More…

EUR/GBP's recovery from 0.8720 extends higher today but stays below 0.8800 resistance. Intraday bias remains neutral for the moment, and further decline is still expected. Fall from 0.8863 should at least be a correction to the up trend from 0.8221, with risk of bearish reversal. Below 0.8720 will target 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618). However, break of 0.8800 will turn bias back to the upside for retesting 0.8863.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8600) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

Sterling Softens After GDP Miss; Dollar Remains Under Pressure

Sterling edged lower after the UK GDP release disappointed again, a adding to a run of soft growth signals and left the Pound mildly on the defensive into European session. The pre-Budget weakness is strengthening the case for the BoE to resume rate cuts at next week’s meeting. While the MPC remains clearly divided, resistance to a measured easing pace looks limited. The delay from October to December was only driven by November’s Budget timing rather than a fundamental shift in the policy outlook.

A quarterly pace of cuts remains the path of least resistance for now, but beyond that the outlook is uncertain. The policy debate inside the MPC polarized, particularly around how restrictive current settings really are and how persistent inflation risks might prove in 2026. On the hawkish side, Deputy Governor Clare Lombardelli has warned this week about upside inflation risks and suggested the BoE may be nearing the end of its cutting cycle. She has also questioned how restrictive policy actually is, hinting that the room for further easing could be more limited than markets assume.

In contrast, dovish voices remain active. Deputy Governor Dave Ramsden, who argued for a rate cut in November, said he sees no evidence that inflation will fail to fall as the BoE expects. He reiterated that a gradual removal of policy restraint remains appropriate, allowing the MPC to reassess risks as new data arrive.

Elsewhere, Dollar remains broadly weak as post-FOMC softness persists, particularly against Euro and Swiss Franc. Investors appear comfortable with the Fed’s easing trajectory, a stance that has helped propel traditional stocks to fresh record highs even as debate over AI valuations lingers. Underlying risk-on sentiment continues to cap any meaningful Dollar rebound.

For the week so far, Yen sits at the bottom of the FX performance table, followed by Dollar and then Loonie. Swiss Franc leads, followed by Euro and Kiwi, while Sterling and Aussie trade in the middle of the pack.

In Asia, Nikkei rose 1.37%. Hong Kong HSI is up 1.58%. Shanghai SSE rose 0.41%. Singapore Strait Times is up 1.27%. Japan 10-year JGB yield rose 0.021 to 1.952. Overnight, DOW rose 1.34%. S&P 500 rose 0.21%. NASDAQ fell -0.25%. 10-year yield fell -0.023 to 4.141.

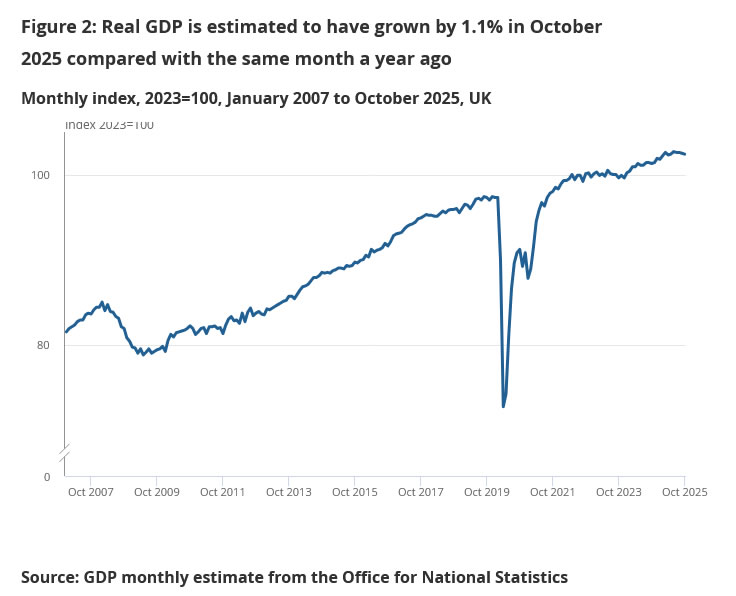

UK GDP contracts -0.1% mom in October as services drag deepens

UK GDP contracted by -0.1% mom in October, undershooting expectations for a 0.1% gain and marking a third consecutive month of stagnation or contraction. The economy had already shrunk by -0.1% in September after flat growth in August, reinforcing concerns that momentum is fading as the year draws to a close.

The monthly breakdown was weak across key domestic sectors. Services output fell -0.3% mom and construction declined -0.6%, offsetting a 1.1% rise in production. The continued softness in services is particularly concerning given its dominant share of UK economic activity.

On a three-month basis, GDP fell -0.1% in the period to October compared with the previous three months. Services recorded no growth, extending the recent trend of slowing activity, while production output dropped -0.5% due largely to weaker motor vehicle manufacturing. Construction also declined by -0.3%.

New Zealand BNZ manufacturing improves to 51.1, but momentum still modest

New Zealand’s BNZ Performance of Manufacturing Index edged up from 51.2 to 51.4 in November, remaining in expansionary territory but still below the long-run average of 52.4.

Production strengthened from 52.0 to 52.8, while employment rebounded sharply from contractionary 48.3 to 52.4, suggesting manufacturers are becoming more confident about staffing needs. That said, new orders softened notably, slipping from 54.5 to 51.9, highlighting lingering caution about the sustainability of demand beyond the seasonal boost.

Survey commentary was more encouraging. The share of negative comments fell to 45.6% from 54.1% in October and 60.2% in September. Respondents cited stronger Christmas-related demand, improving economic conditions, rising customer confidence, and a pickup in both domestic and overseas orders, alongside firmer construction activity and new product launches.

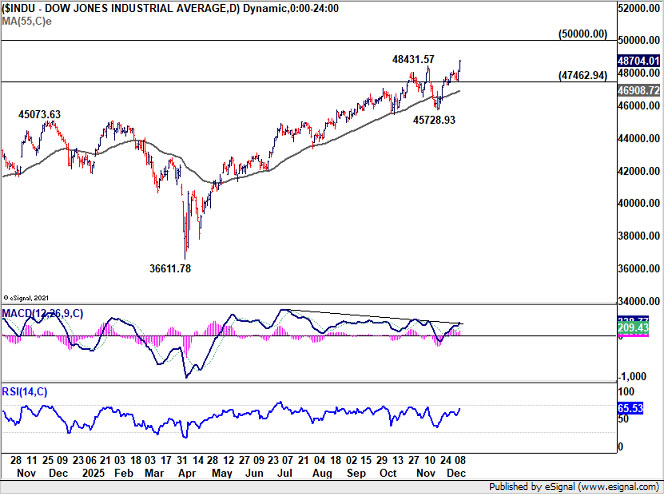

DOW eyes 50k as Fed easing fuels broad-based equity breakout, except tech

DOW decisively to a new record high yesterday, reinforcing the view that the Santa rally is firmly in force after clearly this week's FOMC risk. With momentum accelerating, the index is now on track to challenge the 50,000 psychological level before year-end, a milestone that reflects renewed confidence in the outlook for growth and monetary policy.

Markets have looked past persistent debate over AI valuations, focusing instead on the Fed’s less-hawkish-than-expected rate cut earlier this week. The shift has favored cyclical and traditional sectors. Russell 2000’s surge to a record close adds further confirmation. Smaller companies are typically more sensitive to changes in borrowing costs, and their leadership highlights expectations that easing financial conditions will filter through to the real economy.

Technically, near-term outlook for DOW remains bullish as long as 47,462.94 support holds. The current uptrend is targeting 78.6% projection of 28,660.94 to 45,071.29 from 36,611.78 at 49,510.32, with scope to stretch above 50,000 handle. Attention now turns to whether S&P 500 joins the breakout to confirm momentum, even as NASDAQ's participation remains less certain.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8745; (P) 0.8759; (R1) 0.8783; More…

EUR/GBP's recovery from 0.8720 extends higher today but stays below 0.8800 resistance. Intraday bias remains neutral for the moment, and further decline is still expected. Fall from 0.8863 should at least be a correction to the up trend from 0.8221, with risk of bearish reversal. Below 0.8720 will target 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618). However, break of 0.8800 will turn bias back to the upside for retesting 0.8863.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8600) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

Big Week Ends With Big Doubts

The S&P 500 continued to push higher yesterday as the US 2-year yield wavered around the 3.50% mark following a Federal Reserve (Fed) rate cut earlier this week that was ultimately perceived as not that hawkish after all. The cut is especially boosting the non-tech pockets of the market. The S&P 500’s equal-weight index is catching up with the tech-heavy, market-cap-weighted version, suggesting further upside potential from a rotation out of growth and into value. Normally, the tech and growth-heavy sectors react more to changes in borrowing costs because more of their future revenue gets discounted to today. But sky-high valuations in tech mean they’ve become less reactive to the rate cut. Investors clearly have bigger concerns.

The Nasdaq 100 failed to eke out gains after the Fed cut, as a more-than-10% slump in Oracle shares dampened sentiment across tech and dragged broader AI names lower. Nvidia, for example, lost more than 1.5% on worries about the circularity of AI deals — and for being situated at the centre of the largest AI loop to date: the one surrounding OpenAI.

If it’s any comfort, OpenAI announced a $1bn deal with Disney yesterday. Under the agreement, Disney will invest $1bn in OpenAI, and OpenAI will allow Sora users to generate short videos using more than 200 Disney, Marvel, Pixar and Star Wars characters. You might remain sceptical, but this is an interesting revenue channel for OpenAI, as content creators may be willing to spend more on Sora — which has faded somewhat since launch — because these characters can boost engagement and monetisation on platforms like YouTube.

This announcement is encouraging for those wondering how companies will monetise AI without relying heavily on advertising. The OpenAI–Disney partnership offers an alternative to flooding chatbots with ads — something that would make them feel as annoying as Facebook’s feed. It doesn’t have the same scale as ad revenue (Facebook earned $51.24 bn last quarter, with roughly $50.1 bn coming from advertising), but it does illustrate how OpenAI turns its models into dollars. The company has commercial deals across a wide range of industries. There is Microsoft, where Copilot uses OpenAI’s intelligence. There is Eli Lilly — a major pharma company — working with OpenAI on AI-enabled R&D and drug discovery. There are commerce-related partnerships, such as Walmart’s integration that lets users buy products through ChatGPT’s conversational interface. OpenAI previously supported Shopify and Etsy with chat-commerce capabilities in exchange for fees. And it has an enterprise partnership with Databricks to embed OpenAI models into its platform. OpenAI needs a continuous flow of such deals to justify its lofty valuation and those of its partners, but the negative press often feels disproportionate for a company that fundamentally changed how we interact with machines only three years ago.

Now, none of this answers whether “this is a bubble”. The internet outlived the dot-com crisis even as countless companies disappeared. But it does show how far AI capabilities can extend across industries and clients — from Microsoft and Eli Lilly to Walmart and Disney — and how productivity gains, in blue-collar sectors, could support long-term demand.

Turning to individual earnings, Broadcom reported very strong results yesterday. Revenue jumped 28% to $18 bn, and earnings surpassed expectations thanks to surging AI-chip demand. The company disclosed $73 bn in AI-related orders already booked, issued an upbeat Q1 revenue outlook of $19 bn, and raised its dividend by 10%. Not bad. The problem is that expectations were simply too high, and after an initial uptick the stock fell more than 4% in after-hours trading as investors focused on margin pressures and profit dynamics in AI.

So we’re back to square one. Taken together, Oracle and Broadcom reminded the market that while AI demand remains strong, leveraged investments and uncertain monetisation paths are preventing investors from adding exposure at current valuations.

Investors instead seem to prefer gold, silver, and copper. Gold is back in a solid uptrend after the October correction, supported by lower US yields and a softer dollar. Silver and copper benefit from the same bullish factors— plus tight supply conditions. Oil bulls, by contrast, remain impossible to cheer up. Despite earlier geopolitical tensions, WTI continues to test the $58 level on the downside, pressured by ample supply from the US, OPEC, and non-OPEC producers, even as the US dollar index falls below its 100-day moving average.

This week ends on a dovish note for the Fed, a positive one for Treasuries, metals, and value stocks, and a negative one for the dollar, oil, and tech stocks. Next week’s US CPI release — the first one since the shutdown — will either confirm or challenge the post-Fed trend. The last headline figure pointed to 3% inflation, still above the Fed’s 2% target. A sufficiently soft CPI print would likely reinforce the recent price action into year-end and could deliver fresh all-time highs in some indices, especially the smaller and non-tech ones. A stronger reading could cool risk appetite and revive concerns that the Fed may not be able to cut rates next year if inflation remains sticky.

UK GDP contracts -0.1% mom in October as services drag deepens

UK GDP contracted by -0.1% mom in October, undershooting expectations for a 0.1% gain and marking a third consecutive month of stagnation or contraction. The economy had already shrunk by -0.1% in September after flat growth in August, reinforcing concerns that momentum is fading as the year draws to a close.

The monthly breakdown was weak across key domestic sectors. Services output fell -0.3% mom and construction declined -0.6%, offsetting a 1.1% rise in production. The continued softness in services is particularly concerning given its dominant share of UK economic activity.

On a three-month basis, GDP fell -0.1% in the period to October compared with the previous three months. Services recorded no growth, extending the recent trend of slowing activity, while production output dropped -0.5% due largely to weaker motor vehicle manufacturing. Construction also declined by -0.3%.

Swedish Labour Force Survey Concludes the Week

In focus today

In Sweden, the Swedish labour force survey (LFS) for November is set to be released. We anticipate the unemployment rate to come in at 7.90% (8.80% seasonally adjusted). Recent indicators, including the Sweden's Public Employment Servies (SPES), has continued to show an improvement of the Swedish labour market. As SPES typically serves as a leading indicator for the LFS, we might see some improvement today. However, it could well be too early for significant changes to appear.

In Germany, we receive the final inflation data for November. While CPI was unchanged at 2.3% y/y there was a large upside surprise in the HICP index which rose to 2.6% y/y. HICP services inflation was the culprit behind the surprise as it rose to 4.2% y/y (prior: 3.6%) and the final print will shed more light on the drivers.

In the UK, October GDP data is released. After a couple of weak prints, job losses becoming more prominent, and inflation edging somewhat lower, the Bank of England looks ready to cut rates again next week.

In Japan, the Bank of Japan (BoJ) releases its extensive quarterly Tankan business survey on Sunday night. This will be scrutinised by the BoJ ahead of its rate decision Friday next week. Business sentiment is strong in Japan, particularly in the service sector, where tourism is contributing to solid demand.

Also, early Monday, China brings the release of the monthly batch of data for retail sales, industrial production, housing and investments. We expect it to show more of the same, i.e. still weak consumer spending, low home sales, further declines in home prices but decent increase in industrial production supported by robust exports. China is a two-speed economy with strong exports and tech development but weak demand in domestic demand.

Have a good weekend!

Economic and market news

What happened yesterday

In the US, the Federal Reserve has unanimously reappointed its 11 regional presidents in a vote held every five years. While this process typically attracts little attention, scrutiny from the Trump administration and debates about central bank independence raised concerns that some terms could have been blocked.

In Norway, Norges Bank Regional Survey showed that the aggregated production index for next quarter (Q1/26) dropped to 0.3, marginally lower than Norges Bank's expected growth in the September MPR. More importantly, capacity utilization fell from 35% to 33% and the indicator for labour shortage dropped from 25% to 22%. Combined with lower inflation and higher unemployment, this points to a lower rate path in the MPR published next week. Lastly, wage growth this year fell from 4.5% to 4.4%, a bit lower than Norges Bank expected in September.

In Sweden, final inflation figures aligned closely with the flash estimate. November CPI was 0.3% y/y and -0.4% m/m, while CPIF came in at 2.3% y/y and -0.2% m/m, slightly above the flash estimate by 0.1 percentage point. Core inflation was 2.4% y/y and -0.6% m/m. The larger-than-usual monthly decline was driven by a sharper drop in recreation and hotels. Goods prices also fell, including clothing and furniture, with clothing declining slightly more than anticipated, likely driven by earlier and more Black Friday sales. Core inflation was 0.4 percentage points below our forecast, with 0.3 percentage points explained by the unexpected dip in recreation, primarily from package holidays.

In Switzerland, The SNB kept the policy rate at 0%, as widely expected, and maintained its stance on FX intervention. Inflation forecasts were lowered due to recent weaker-than-expected inflation, and the SNB signalled continued monitoring and readiness to adjust policy if needed.

In Turkey, the Central Bank of Turkey surprised markets by lowering its key policy rate by 150 bp to 38%.

In geopolitics, Ukraine has presented its revised 20-point framework to the US, with territorial concessions remaining a key hurdle. The US proposed a 'free economic zone' in part of Donbas and potential joint governance of the Zaporizhzhia Nuclear Power Plant. The broader plan includes security guarantees, rebuilding efforts, and maintaining a strong Ukrainian military. While Washington seeks clarity by Christmas, Zelenskiy insists on a referendum for any territorial concessions.

Equities: Equities were generally higher yesterday despite some emerging weakness in the tech sector. The S&P 500 gained 0.2% but equal-weight S&P 500 0.8%, and the Stoxx 600 advanced 0.6%. The tech pullback was driven by a disappointing report from Oracle, which showed slowing revenue growth and a notable increase in spending. Had this occurred three weeks ago, the market reaction would likely have been pronounced. However, yesterday the weakness remained contained within tech. In fact, materials, financials, and industrials extended their post-Fed-meeting gains, rising another 1-2%. So, the rotation was notable. Futures are little changed this morning.

FI and FX: Norges Bank will publish their funding outlook for 2026, whereas the Riksbank is closing in on their second last nominal SGB QT-auction. The SNB left its policy rate unchanged but stands ready to act in foreign exchange markets, at the same time as they try to withstand a negative policy rate. Net movement in US and EUR rates were relatively muted during yesterday's session. EUR/USD continued to edge higher and touched 1.176 yesterday afternoon.

DOW eyes 50k as Fed easing fuels broad-based equity breakout, except tech

DOW decisively to a new record high yesterday, reinforcing the view that the Santa rally is firmly in force after clearly this week's FOMC risk. With momentum accelerating, the index is now on track to challenge the 50,000 psychological level before year-end, a milestone that reflects renewed confidence in the outlook for growth and monetary policy.

Markets have looked past persistent debate over AI valuations, focusing instead on the Fed’s less-hawkish-than-expected rate cut earlier this week. The shift has favored cyclical and traditional sectors. Russell 2000’s surge to a record close adds further confirmation. Smaller companies are typically more sensitive to changes in borrowing costs, and their leadership highlights expectations that easing financial conditions will filter through to the real economy.

Technically, near-term outlook for DOW remains bullish as long as 47,462.94 support holds. The current uptrend is targeting 78.6% projection of 28,660.94 to 45,071.29 from 36,611.78 at 49,510.32, with scope to stretch above 50,000 handle. Attention now turns to whether S&P 500 joins the breakout to confirm momentum, even as NASDAQ's participation remains less certain.

New Zealand BNZ manufacturing improves to 51.1, but momentum still modest

New Zealand’s BNZ Performance of Manufacturing Index edged up from 51.2 to 51.4 in November, remaining in expansionary territory but still below the long-run average of 52.4.

Production strengthened from 52.0 to 52.8, while employment rebounded sharply from contractionary 48.3 to 52.4, suggesting manufacturers are becoming more confident about staffing needs. That said, new orders softened notably, slipping from 54.5 to 51.9, highlighting lingering caution about the sustainability of demand beyond the seasonal boost.

Survey commentary was more encouraging. The share of negative comments fell to 45.6% from 54.1% in October and 60.2% in September. Respondents cited stronger Christmas-related demand, improving economic conditions, rising customer confidence, and a pickup in both domestic and overseas orders, alongside firmer construction activity and new product launches.