Sample Category Title

Summary 12/15 – 12/19

Monday, Dec 15, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Nov | 48.7 | |

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | 15 | 14 |

| 23:50 | JPY | Tankan Non - Manufacturing Index Q4 | 35 | 34 |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q4 | 13 | 12 |

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q4 | 28 | 28 |

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | 12.00% | 12.50% |

| 02:00 | CNY | Industrial Production Y/Y Nov | 5.00% | 4.90% |

| 02:00 | CNY | Retail Sales Y/Y Nov | 2.90% | 2.90% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Nov | -2.30% | -1.70% |

| 04:30 | JPY | Tertiary Industry Index M/M Oct | 0.20% | 0.30% |

| 07:30 | CHF | Producer and Import Prices M/M Nov | 0.10% | -0.30% |

| 07:30 | CHF | Producer and Import Prices Y/Y Nov | -1.70% | |

| 08:00 | CHF | SECO Economic Forecasts | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | 0.10% | 0.20% |

| 13:15 | CAD | Housing Starts Y/Y Nov | 248K | 233K |

| 13:30 | CAD | CPI M/M Nov | 0.10% | 0.20% |

| 13:30 | CAD | CPI Y/Y Nov | 2.20% | |

| 13:30 | CAD | CPI Median Y/Y Nov | 2.90% | 2.90% |

| 13:30 | CAD | CPI Trimmed Y/Y Nov | 2.90% | 3.00% |

| 13:30 | CAD | CPI Common Y/Y Nov | 2.80% | 2.70% |

| 13:30 | CAD | Manufacturingles M/M Oct | -1.10% | 3.30% |

| 13:30 | USD | Empire State Manufacturing Dec | 10.6 | 18.7 |

| 15:00 | USD | NAHB Housing Market Index Dec | 38 | 38 |

| 22:00 | AUD | Manufacturing PMI Dec P | 51.6 | |

| 22:00 | AUD | Services PMI Dec P | 52.8 | |

| 23:30 | AUD | Westpac Consumer Confidence Dec | 12.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Nov | |

| Forecast: | Previous: 48.7 | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | |

| Forecast: 15 | Previous: 14 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Index Q4 | |

| Forecast: 35 | Previous: 34 | ||

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q4 | |

| Forecast: 13 | Previous: 12 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q4 | |

| Forecast: 28 | Previous: 28 | ||

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | |

| Forecast: 12.00% | Previous: 12.50% | ||

| 02:00 | CNY | Industrial Production Y/Y Nov | |

| Forecast: 5.00% | Previous: 4.90% | ||

| 02:00 | CNY | Retail Sales Y/Y Nov | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Nov | |

| Forecast: -2.30% | Previous: -1.70% | ||

| 04:30 | JPY | Tertiary Industry Index M/M Oct | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 07:30 | CHF | Producer and Import Prices M/M Nov | |

| Forecast: 0.10% | Previous: -0.30% | ||

| 07:30 | CHF | Producer and Import Prices Y/Y Nov | |

| Forecast: | Previous: -1.70% | ||

| 08:00 | CHF | SECO Economic Forecasts | |

| Forecast: | Previous: | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 13:15 | CAD | Housing Starts Y/Y Nov | |

| Forecast: 248K | Previous: 233K | ||

| 13:30 | CAD | CPI M/M Nov | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 13:30 | CAD | CPI Y/Y Nov | |

| Forecast: | Previous: 2.20% | ||

| 13:30 | CAD | CPI Median Y/Y Nov | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 13:30 | CAD | CPI Trimmed Y/Y Nov | |

| Forecast: 2.90% | Previous: 3.00% | ||

| 13:30 | CAD | CPI Common Y/Y Nov | |

| Forecast: 2.80% | Previous: 2.70% | ||

| 13:30 | CAD | Manufacturingles M/M Oct | |

| Forecast: -1.10% | Previous: 3.30% | ||

| 13:30 | USD | Empire State Manufacturing Dec | |

| Forecast: 10.6 | Previous: 18.7 | ||

| 15:00 | USD | NAHB Housing Market Index Dec | |

| Forecast: 38 | Previous: 38 | ||

| 22:00 | AUD | Manufacturing PMI Dec P | |

| Forecast: | Previous: 51.6 | ||

| 22:00 | AUD | Services PMI Dec P | |

| Forecast: | Previous: 52.8 | ||

| 23:30 | AUD | Westpac Consumer Confidence Dec | |

| Forecast: | Previous: 12.80% | ||

Tuesday, Dec 16, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Dec P | 48.8 | 48.7 |

| 00:30 | JPY | Services PMI Dec P | 53.2 | |

| 07:00 | GBP | Claimant Count Change Nov | 22.3K | 29.0K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Oct | 5.10% | 5% |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | 4.40% | 4.80% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | 4.60% | |

| 08:15 | EUR | France Manufacturing PMI Dec P | 48.2 | 47.8 |

| 08:15 | EUR | France Services PMI Dec P | 51.3 | 51.4 |

| 08:30 | EUR | Germany Manufacturing PMI Dec P | 48.5 | 48.2 |

| 08:30 | EUR | Germany Services PMI Dec P | 53 | 53.1 |

| 09:00 | EUR | Eurozone Manufacturing PMI Dec P | 49.9 | 49.6 |

| 09:00 | EUR | Eurozone Services PMI Dec P | 53.9 | 53.6 |

| 09:30 | GBP | Manufacturing PMI Dec P | 50.3 | 50.2 |

| 09:30 | GBP | Services PMI Dec P | 51.6 | 51.3 |

| 10:00 | EUR | Eurozone Trade Balance (EUR Oct | 18.7B | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | 40 | 38.5 |

| 10:00 | EUR | Germany ZEW Current Situation Dec | -76.2 | -78.7 |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | 26.3 | 25 |

| 13:30 | USD | Retail Sales M/M Oct | 0.20% | 0.20% |

| 13:30 | USD | Retail Sales ex Autos M/M Oct | 0.30% | 0.30% |

| 13:30 | USD | Nonfarm Payrolls Oct | 50K | 119K |

| 13:30 | USD | Nonfarm Payrolls Nov | 35K | |

| 13:30 | USD | Unemployment Rate Nov | 4.40% | 4.40% |

| 13:30 | USD | Average Hourly Earnings M/M Oct | 0.20% | |

| 14:45 | USD | Manufacturing PMI Dec P | 52.2 | |

| 14:45 | USD | Services PMI Dec P | 54.1 | |

| 15:00 | USD | Business Inventories Sep | 0.20% | 0.00% |

| 21:45 | NZD | Current Account (NZD) Q3 | -7.65B | -0.97B |

| 23:50 | JPY | Trade Balance (JPY) Nov | -0.21T | 0.00T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Dec P | |

| Forecast: 48.8 | Previous: 48.7 | ||

| 00:30 | JPY | Services PMI Dec P | |

| Forecast: | Previous: 53.2 | ||

| 07:00 | GBP | Claimant Count Change Nov | |

| Forecast: 22.3K | Previous: 29.0K | ||

| 07:00 | GBP | ILO Unemployment Rate (3M) Oct | |

| Forecast: 5.10% | Previous: 5% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | |

| Forecast: 4.40% | Previous: 4.80% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | |

| Forecast: | Previous: 4.60% | ||

| 08:15 | EUR | France Manufacturing PMI Dec P | |

| Forecast: 48.2 | Previous: 47.8 | ||

| 08:15 | EUR | France Services PMI Dec P | |

| Forecast: 51.3 | Previous: 51.4 | ||

| 08:30 | EUR | Germany Manufacturing PMI Dec P | |

| Forecast: 48.5 | Previous: 48.2 | ||

| 08:30 | EUR | Germany Services PMI Dec P | |

| Forecast: 53 | Previous: 53.1 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Dec P | |

| Forecast: 49.9 | Previous: 49.6 | ||

| 09:00 | EUR | Eurozone Services PMI Dec P | |

| Forecast: 53.9 | Previous: 53.6 | ||

| 09:30 | GBP | Manufacturing PMI Dec P | |

| Forecast: 50.3 | Previous: 50.2 | ||

| 09:30 | GBP | Services PMI Dec P | |

| Forecast: 51.6 | Previous: 51.3 | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR Oct | |

| Forecast: | Previous: 18.7B | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | |

| Forecast: 40 | Previous: 38.5 | ||

| 10:00 | EUR | Germany ZEW Current Situation Dec | |

| Forecast: -76.2 | Previous: -78.7 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | |

| Forecast: 26.3 | Previous: 25 | ||

| 13:30 | USD | Retail Sales M/M Oct | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Oct | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 13:30 | USD | Nonfarm Payrolls Oct | |

| Forecast: 50K | Previous: 119K | ||

| 13:30 | USD | Nonfarm Payrolls Nov | |

| Forecast: 35K | Previous: | ||

| 13:30 | USD | Unemployment Rate Nov | |

| Forecast: 4.40% | Previous: 4.40% | ||

| 13:30 | USD | Average Hourly Earnings M/M Oct | |

| Forecast: | Previous: 0.20% | ||

| 14:45 | USD | Manufacturing PMI Dec P | |

| Forecast: | Previous: 52.2 | ||

| 14:45 | USD | Services PMI Dec P | |

| Forecast: | Previous: 54.1 | ||

| 15:00 | USD | Business Inventories Sep | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 21:45 | NZD | Current Account (NZD) Q3 | |

| Forecast: -7.65B | Previous: -0.97B | ||

| 23:50 | JPY | Trade Balance (JPY) Nov | |

| Forecast: -0.21T | Previous: 0.00T | ||

Wednesday, Dec 17, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Nov | 0.11% | |

| 07:00 | GBP | CPI M/M Nov | 0.40% | |

| 07:00 | GBP | CPI Y/Y Nov | 3.50% | 3.60% |

| 07:00 | GBP | Core CPI Y/Y Nov | 3.40% | 3.40% |

| 07:00 | GBP | RPI M/M Nov | 0.30% | |

| 07:00 | GBP | RPI Y/Y Nov | 4.30% | 4.30% |

| 07:00 | GBP | PPI Input M/M Nov | -0.30% | |

| 07:00 | GBP | PPI Input Y/Y Nov | 0.50% | |

| 07:00 | GBP | PPI Output Y/Y Nov | 3.60% | |

| 07:00 | GBP | PPI Output M/M Nov | 0% | |

| 07:00 | GBP | PPI Core Output M/M Nov | 0.10% | |

| 07:00 | GBP | PPI Core Output Y/Y Nov | 3.60% | |

| 09:00 | EUR | Germany IFO Business Climate Dec | 88.5 | 88.1 |

| 09:00 | EUR | Germany IFO Current Assessment Dec | 86 | 85.6 |

| 09:00 | EUR | Germany IFO Expectations Dec | 91 | 90.6 |

| 10:00 | EUR | Eurozone CPI Y/Y Nov F | 2.20% | 2.20% |

| 10:00 | EUR | Eurozone Core CPI Y/Y Nov F | 2.40% | 2.40% |

| 15:30 | USD | Crude Oil Inventories (Dec 12) | -1.8M | |

| 21:45 | NZD | GDP Q/Q Q3 | 0.80% | -0.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Westpac Leading Index M/M Nov | |

| Forecast: | Previous: 0.11% | ||

| 07:00 | GBP | CPI M/M Nov | |

| Forecast: | Previous: 0.40% | ||

| 07:00 | GBP | CPI Y/Y Nov | |

| Forecast: 3.50% | Previous: 3.60% | ||

| 07:00 | GBP | Core CPI Y/Y Nov | |

| Forecast: 3.40% | Previous: 3.40% | ||

| 07:00 | GBP | RPI M/M Nov | |

| Forecast: | Previous: 0.30% | ||

| 07:00 | GBP | RPI Y/Y Nov | |

| Forecast: 4.30% | Previous: 4.30% | ||

| 07:00 | GBP | PPI Input M/M Nov | |

| Forecast: | Previous: -0.30% | ||

| 07:00 | GBP | PPI Input Y/Y Nov | |

| Forecast: | Previous: 0.50% | ||

| 07:00 | GBP | PPI Output Y/Y Nov | |

| Forecast: | Previous: 3.60% | ||

| 07:00 | GBP | PPI Output M/M Nov | |

| Forecast: | Previous: 0% | ||

| 07:00 | GBP | PPI Core Output M/M Nov | |

| Forecast: | Previous: 0.10% | ||

| 07:00 | GBP | PPI Core Output Y/Y Nov | |

| Forecast: | Previous: 3.60% | ||

| 09:00 | EUR | Germany IFO Business Climate Dec | |

| Forecast: 88.5 | Previous: 88.1 | ||

| 09:00 | EUR | Germany IFO Current Assessment Dec | |

| Forecast: 86 | Previous: 85.6 | ||

| 09:00 | EUR | Germany IFO Expectations Dec | |

| Forecast: 91 | Previous: 90.6 | ||

| 10:00 | EUR | Eurozone CPI Y/Y Nov F | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 10:00 | EUR | Eurozone Core CPI Y/Y Nov F | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 15:30 | USD | Crude Oil Inventories (Dec 12) | |

| Forecast: | Previous: -1.8M | ||

| 21:45 | NZD | GDP Q/Q Q3 | |

| Forecast: 0.80% | Previous: -0.90% | ||

Thursday, Dec 18, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Dec | 4.50% | |

| 07:00 | CHF | Trade Balance (CHF) Nov | 5.32B | 4.32B |

| 12:00 | GBP | BoE Interest Rate Decision | 3.75% | 4.00% |

| 13:15 | EUR | ECB Deposit Rate | 2.00% | 2.00% |

| 13:15 | EUR | ECB Main Refinancing Rate | 2.15% | 2.15% |

| 13:15 | EUR | ECB Monetary Policy Statement | ||

| 13:30 | USD | Initial Jobless Claims (Dec 12) | 231K | 236K |

| 13:30 | USD | CPI M/M Nov | 0.30% | |

| 13:30 | USD | CPI Y/Y Nov | 3% | |

| 13:30 | USD | CPI Core M/M Nov | 0.20% | |

| 13:30 | USD | CPI Core Y/Y Nov | 3% | |

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Dec | 2.2 | -1.7 |

| 13:45 | EUR | ECB Press Conference | ||

| 15:30 | USD | Natural Gas Storage (Dec 12) | -177B | |

| 21:45 | NZD | Trade Balance (NZD) Nov | -1542M | |

| 23:30 | JPY | National CPI Y/Y Nov | 3% | |

| 23:30 | JPY | National CPI Core Y/Y Nov | 3% | 3% |

| 23:30 | JPY | National CPI Core-Core Y/Y Nov | 3.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Dec | |

| Forecast: | Previous: 4.50% | ||

| 07:00 | CHF | Trade Balance (CHF) Nov | |

| Forecast: 5.32B | Previous: 4.32B | ||

| 12:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 3.75% | Previous: 4.00% | ||

| 13:15 | EUR | ECB Deposit Rate | |

| Forecast: 2.00% | Previous: 2.00% | ||

| 13:15 | EUR | ECB Main Refinancing Rate | |

| Forecast: 2.15% | Previous: 2.15% | ||

| 13:15 | EUR | ECB Monetary Policy Statement | |

| Forecast: | Previous: | ||

| 13:30 | USD | Initial Jobless Claims (Dec 12) | |

| Forecast: 231K | Previous: 236K | ||

| 13:30 | USD | CPI M/M Nov | |

| Forecast: | Previous: 0.30% | ||

| 13:30 | USD | CPI Y/Y Nov | |

| Forecast: | Previous: 3% | ||

| 13:30 | USD | CPI Core M/M Nov | |

| Forecast: | Previous: 0.20% | ||

| 13:30 | USD | CPI Core Y/Y Nov | |

| Forecast: | Previous: 3% | ||

| 13:30 | USD | Philadelphia Fed Manufacturing Survey Dec | |

| Forecast: 2.2 | Previous: -1.7 | ||

| 13:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 15:30 | USD | Natural Gas Storage (Dec 12) | |

| Forecast: | Previous: -177B | ||

| 21:45 | NZD | Trade Balance (NZD) Nov | |

| Forecast: | Previous: -1542M | ||

| 23:30 | JPY | National CPI Y/Y Nov | |

| Forecast: | Previous: 3% | ||

| 23:30 | JPY | National CPI Core Y/Y Nov | |

| Forecast: 3% | Previous: 3% | ||

| 23:30 | JPY | National CPI Core-Core Y/Y Nov | |

| Forecast: | Previous: 3.10% | ||

Friday, Dec 19, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | 0.50% | ||

| 00:00 | NZD | ANZ Business Confidence Dec | 67.1 | |

| 00:00 | NZD | ANZ Activity Outlook Dec | 53.1 | |

| 00:01 | GBP | GfK Consumer Confidence Dec | -18 | -19 |

| 00:30 | AUD | Private Sector Credit M/M Nov | 0.70% | |

| 06:30 | JPY | BoJ Press Conference | ||

| 07:00 | GBP | Retail Sales M/M Nov | 0.40% | -1.10% |

| 07:00 | EUR | Germany GfK Consumer Confidence Jan | -23 | -23.2 |

| 07:00 | EUR | Germany PPI M/M Nov | 0.10% | 0.10% |

| 07:00 | EUR | Germany PPI Y/Y Nov | -1.80% | |

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Nov | 10.2B | 17.4B |

| 09:00 | EUR | Eurozone Current Account (EUR) Oct | 23.1B | |

| 13:30 | CAD | New Housing Price Index M/M Nov | 0.00% | -0.40% |

| 13:30 | CAD | Retail Sales M/M Oct | 0.00% | -0.70% |

| 13:30 | CAD | Retail Sales ex Autos M/M Oct | 0.00% | 0.20% |

| 15:00 | USD | Existing Home Sales M/M Nov | 4.15M | 4.10M |

| 15:00 | USD | UoM Consumer Sentiment Dec F | 53.3 | 53.3 |

| 15:00 | USD | UoM 1-Yr Inflation Expectations Dec F | 4.10% | |

| 15:00 | EUR | Eurozone Consumer Confidence Dec P | -14 | -14 |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: | Previous: 0.50% | ||

| 00:00 | NZD | ANZ Business Confidence Dec | |

| Forecast: | Previous: 67.1 | ||

| 00:00 | NZD | ANZ Activity Outlook Dec | |

| Forecast: | Previous: 53.1 | ||

| 00:01 | GBP | GfK Consumer Confidence Dec | |

| Forecast: -18 | Previous: -19 | ||

| 00:30 | AUD | Private Sector Credit M/M Nov | |

| Forecast: | Previous: 0.70% | ||

| 06:30 | JPY | BoJ Press Conference | |

| Forecast: | Previous: | ||

| 07:00 | GBP | Retail Sales M/M Nov | |

| Forecast: 0.40% | Previous: -1.10% | ||

| 07:00 | EUR | Germany GfK Consumer Confidence Jan | |

| Forecast: -23 | Previous: -23.2 | ||

| 07:00 | EUR | Germany PPI M/M Nov | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 07:00 | EUR | Germany PPI Y/Y Nov | |

| Forecast: | Previous: -1.80% | ||

| 07:00 | GBP | Public Sector Net Borrowing (GBP) Nov | |

| Forecast: 10.2B | Previous: 17.4B | ||

| 09:00 | EUR | Eurozone Current Account (EUR) Oct | |

| Forecast: | Previous: 23.1B | ||

| 13:30 | CAD | New Housing Price Index M/M Nov | |

| Forecast: 0.00% | Previous: -0.40% | ||

| 13:30 | CAD | Retail Sales M/M Oct | |

| Forecast: 0.00% | Previous: -0.70% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Oct | |

| Forecast: 0.00% | Previous: 0.20% | ||

| 15:00 | USD | Existing Home Sales M/M Nov | |

| Forecast: 4.15M | Previous: 4.10M | ||

| 15:00 | USD | UoM Consumer Sentiment Dec F | |

| Forecast: 53.3 | Previous: 53.3 | ||

| 15:00 | USD | UoM 1-Yr Inflation Expectations Dec F | |

| Forecast: | Previous: 4.10% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Dec P | |

| Forecast: -14 | Previous: -14 | ||

From the FOMC to NFP and CPI – Markets Weekly Outlook

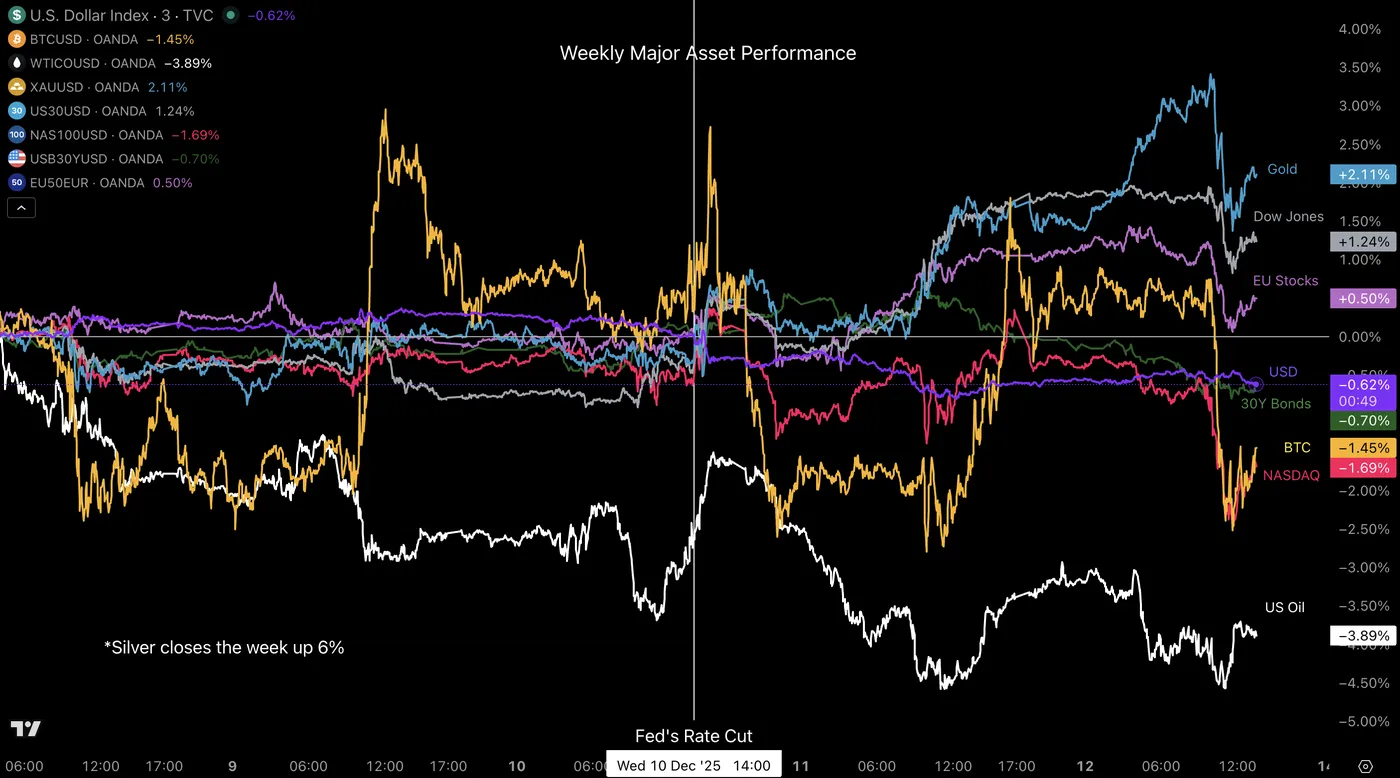

Week in review – The Debasement Trade shines again after the Fed Cut

Markets were salivating for the FOMC rate decision, and they got exactly what they wanted.

The Fed delivered a highly expected 25 bps cut on Wednesday, taking rates from the 3.75%-4.00% range down to 3.50%-3.75%, officially shutting the door on the 4% policy rate era.

While Chair Powell presented neutral remarks overall, investors interpreted them with optimism.

The Dow Jones traded at new all-time highs in consecutive sessions, marking a strong shift higher. Its record price is now at 48,886.

However, the rising tide did not lift all boats.

The US Dollar took a huge hit following the cut, despite the lack of explicitly dovish signals and lower projections in 2026.

Furthermore, the rotation flows that boosted the Dow came at a cost to the Nasdaq: since the cut, the tech-heavy index has dropped by 2%, with capital fleeing toward Industrial and traditional assets.

Weekly Performance across Asset Classes

Weekly Asset Performance – December 12, 2025 – Source: TradingView

But concerns remain, as seen throughout today's session and confirmed by Chicago Fed President Austan Goolsbee. He dissented against the cut, deeming it not urgent given that the labor situation is not dire and inflation remains way too high. He argued in favor of waiting for the inflation picture to clear before cutting further—fair remarks, considering the Federal Reserve has been "driving blind" following the month-and-a-half-long Bureau of Labor Statistics shutdown.

Some profit-taking is also normal after a relentless "Everything Rally" (or Debasement Trade). The fall in the US Dollar combined with sizzling metals brings back echoes of early 2025 flows.

Strong flows but not too surprising when considering how huge next week's data releases will be.

The question now is whether sentiment can hold after today's reality check.

Silver fell 4% in today's session right after reaching a record level of $65. Despite the drop, it is still closing the week up 6% and has surged 23% since the last week of November.

Silver (XAG/USD) 4H Chart. December 12, 2025 – Source: TradingView

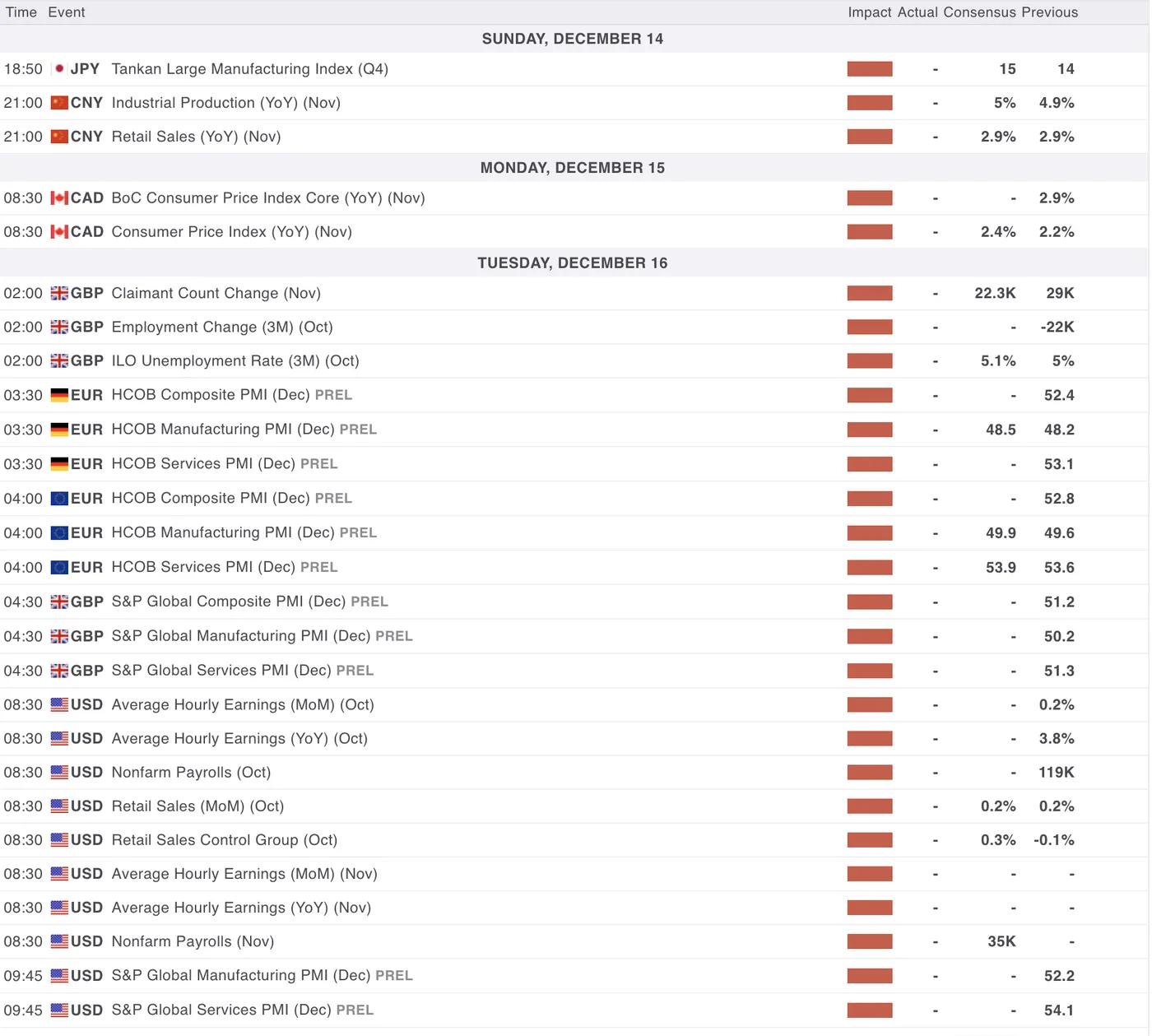

The Week Ahead – Major data is back for the US

Asia Pacific Markets – Bank of Japan in focus

Next week's action in APAC Markets will be quite interesting.

The week will start on Sunday evening (in North America) with quite a lot of interesting economic data, between Manufacturing data from Japan, Retail Sales from Japan and a Business Survey from New Zealand.

The week then officially commences with some PMI releases for Australia, more trade data for Japan on Tuesday and the Kiwi GDP on Wednesday (very important report).

With all due respect to these (key) pieces of data, they will just be acting as Entrées for Thursday evening's Bank of Japan rate decision.

High expectations for a hike have grown even higher in the past month, as the rout on the Yen has kept increasing despite JPY sellers taking somewhat of a breather last week.

Closing the week around 156.00 despite Dollar weakness, the Bank of Japan is facing quite an important test.

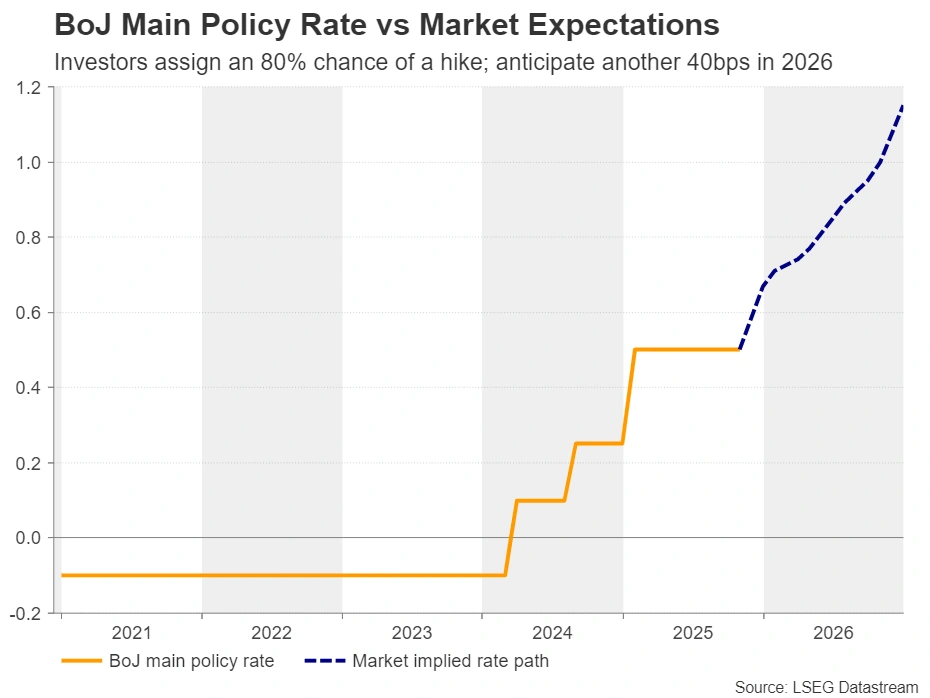

The key really will be whether the BoJ materializes some hawkish communications from their hike, if they actually provide one. The current pricing for the hike is around 75%.

Europe and UK Markets – ECB Rate Decision, UK Employment & PPI supplemented by some PMIs

Next week will also be big for Europe, particularly for the UK.

Tuesday will start with their Employment numbers expected at +22K, releasing in the Tuesday overnight session at 2:00 A.M. and facing some important tests.

The Bank of England now holds the highest interest rates of OECD nations and have about 60 bps of cuts priced in through 2026.

The Pound actually was one of the best performers against the dollar these past few weeks and may stand on top for a moment, particularly if UK data comes in strong.

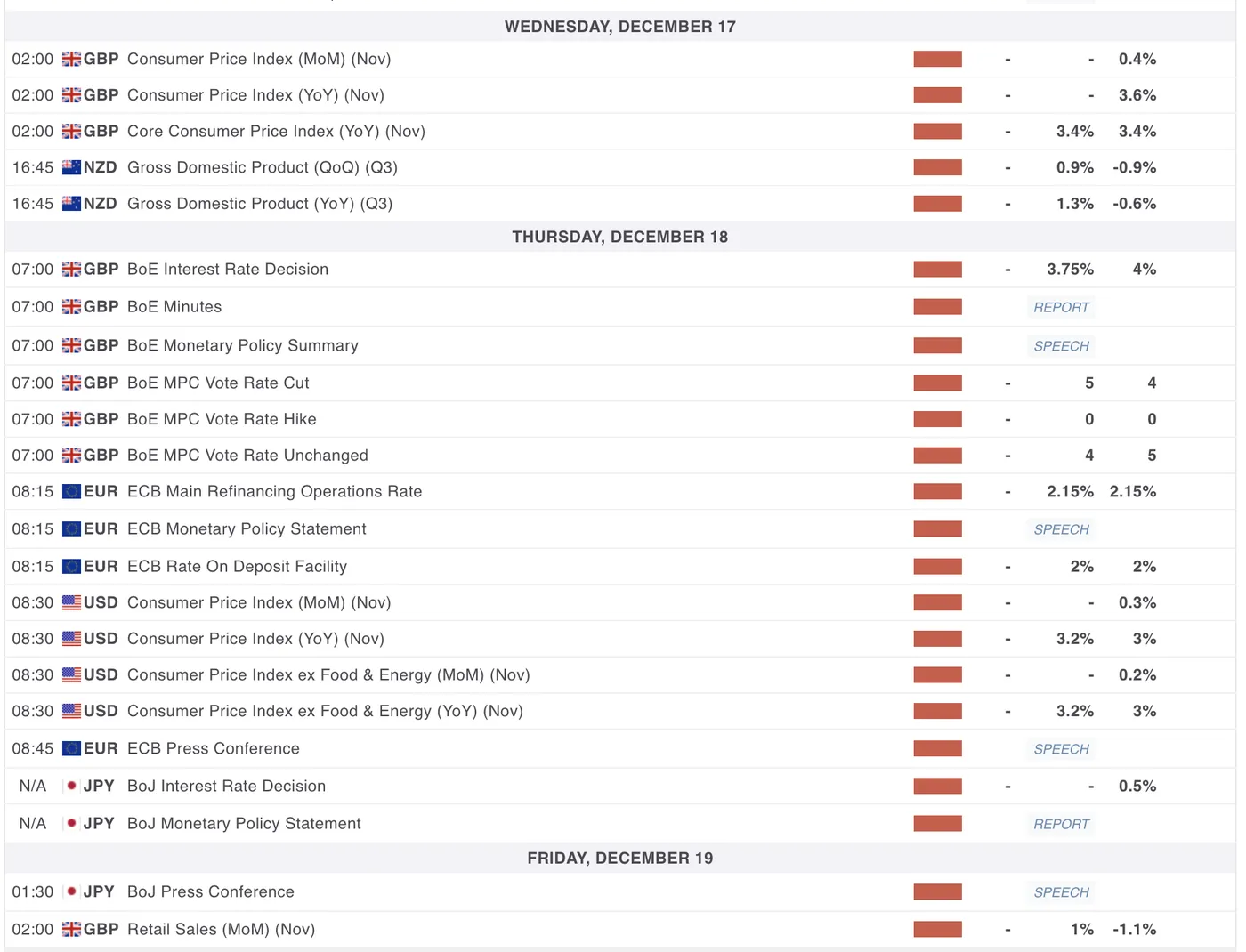

Thursday will also be quite important for GBP traders as they will also get some inflation data, with the UK PPI and Retail Price Index reports. And I was about to forget the Bank of England rate decision, with a 25 bps cut largely expected.

Euro traders will also be served, between rounds of PMI releases but most importantly, the final ECB rate decision for the year, also releasing Thursday.

No change is expected, but as we conclude 2025, keep a close eye on their communication for 2026.

North American Markets – US Non-Farm Payrolls and CPI make their comeback

Nothing much for North American markets... Actually that's false.

The US will get quite some attention after this week's cut, transitioning towards the return of live data.

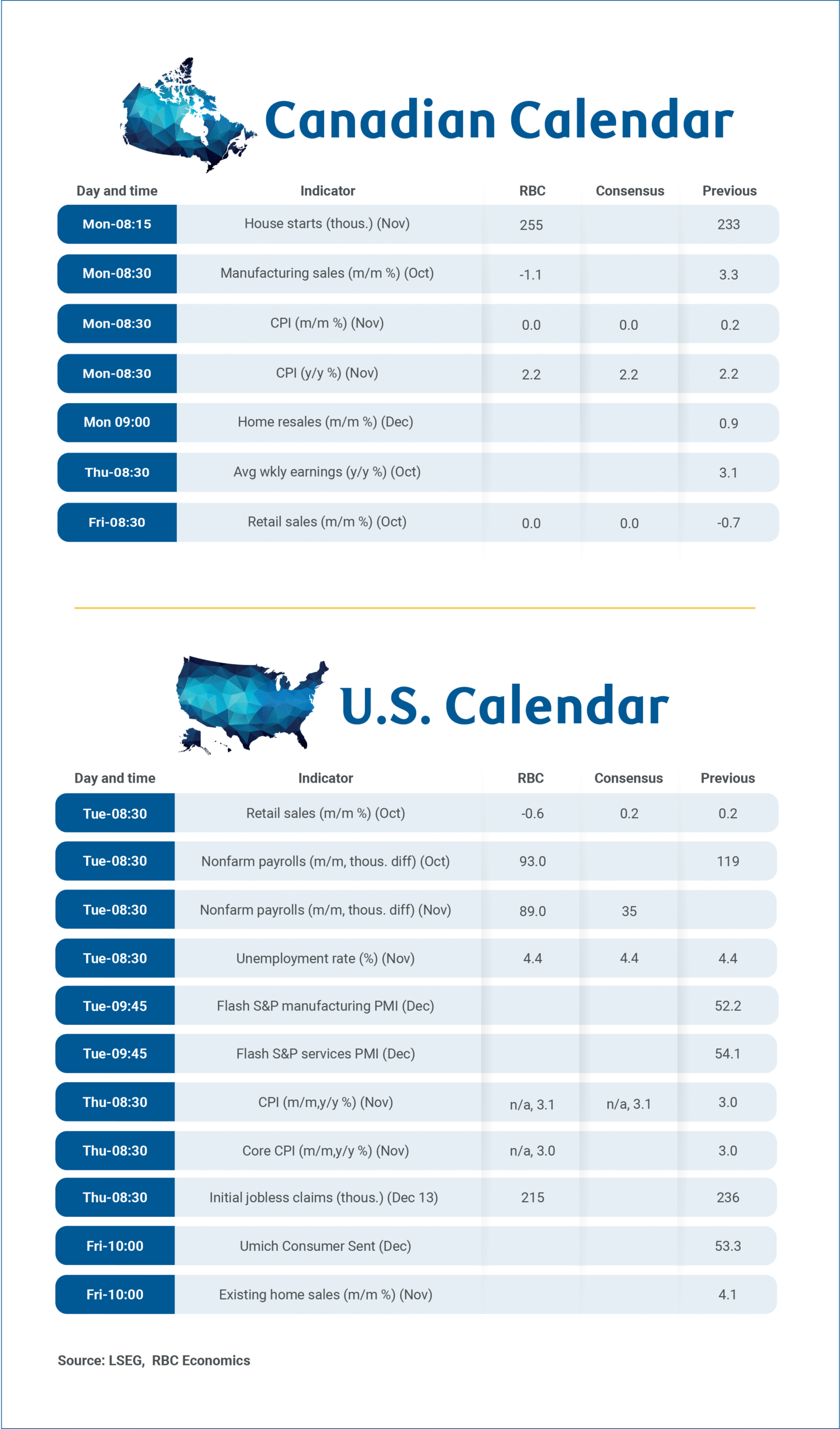

In the mix, November NFP data on December 16, CPI on December 18. Some individual reports will be released for the two quintessential releases

For Canada, they will also be releasing their inflation data on Monday to start the North American week, before only awaiting a Macklem Speech on Tuesday around noon.

Next week's calendar in two parts. Get ready for some volatile action!

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (High-tier data only)

Safe Trades and enjoy your weekend!

Weekly Economic & Financial Commentary: December Rate Cut, Options Left Open for January

Summary

United States: December Rate Cut, Options Left Open for January

- The FOMC lowered the fed funds rate 25 bps at its December meeting and left its options open for January as the Committee weighs incoming data with a wide dispersion of views. Data out this week continue to show the labor market losing steam, supporting the case for returning monetary policy to a neutral stance.

- Next week: Employment (Tue.), Retail Sales (Tue.), CPI (Thu.)

International: Global Central Banks Holding Steady

- In contrast to the FOMC’s rate cut, most global policymakers played it cool in a jam-packed week of central bank decisions, opting to hold steady. The Bank of Canada, Reserve Bank of Australia, Swiss National Bank and Brazilian Central Bank all kept policy rates unchanged. Meanwhile, outside the rate-setting arena, Mexico’s inflation surprised to the upside.

- Next week: China Industrial Production and Retail Sales (Mon.), Bank of England Policy Rate (Thu.), European Central Bank (Thu.)

Topic of the Week: A Cut to Close Out the Year

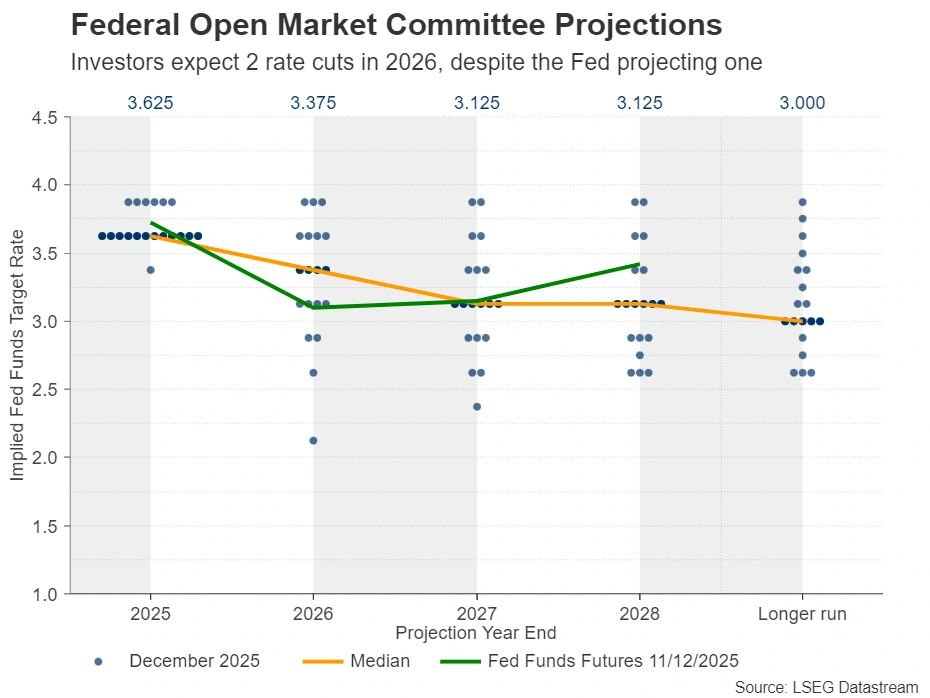

- The December FOMC meeting included the latest Summary of Economic Projections. Despite dissents and a hawkish tilt to the dot plot, the Committee maintains an easing bias.

The Weekly Bottom Line: Fed Delivers on December Cut, But Signals Slower Pace Ahead

Canadian Highlights

- The Bank of Canada kept interest rates unchanged, signaling caution about recent resilience in the Canadian economy in light of the ongoing trade uncertainty.

- The policy rate looks set to remain steady next year. Soft demand is likely to lean against inflationary pressures from increased costs associated with trade adjustments, netting out to keep inflation near target.

- Canada’s trade position improved in September, although most industries still lag be-hind last year’s performance.

U.S. Highlights

- The Federal Reserve delivered a third consecutive quarter-point rate cut this week, bringing the target range to 3.50%-3.75%.

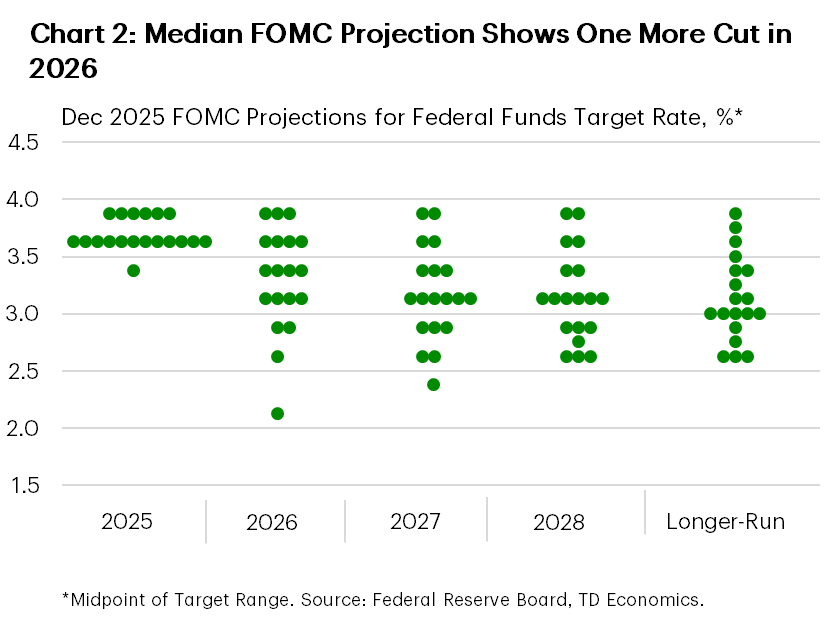

- Three voters dissented on December’s decision and there was considerable dispersion on the expected rate path for 2026, underscoring the growing divide among FOMC members.

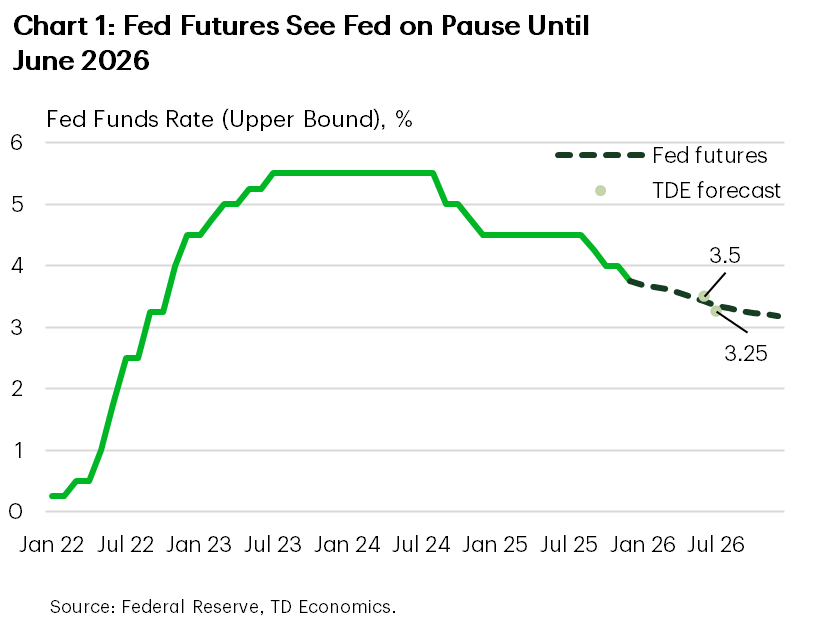

- The median FOMC projection on the federal funds rate suggests just one additional cut in 2026. For now, we think the Fed is on hold until June.

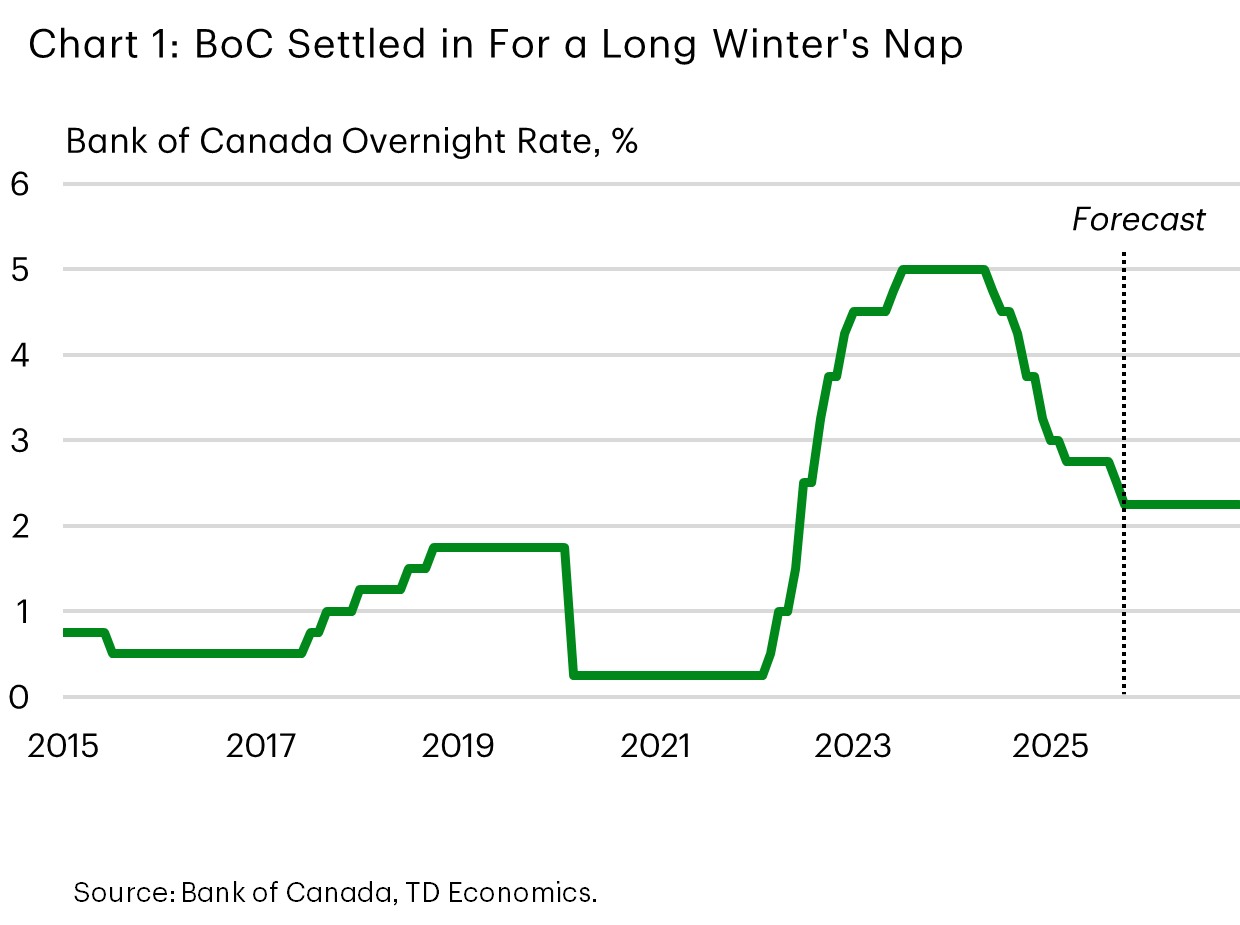

Canada – Bank of Canada Brings Tidings of Comfort (But Not Joy)

We are in the home stretch before Canadian economy watchers can kick back with a festive beverage and reflect on 2025. This past week featured the Bank of Canada’s last interest rate decision of the year and an overdue report on Canada’s trade picture. Overall, the week’s events confirm that Canada’s economy is holding up well despite global uncertainties. This was echoed in the Bank of Canada’s (BoC) interest rate announcement, which brought tidings of comfort, if not exactly joy.

Governor Macklem did not bring any surprises down the chimney, leaving the policy rate unchanged as expected. The central bank acknowledges ongoing concerns about tariffs and trade uncertainty, which continue to dampen business investment intentions. Despite improvements in the labor market, hiring remains subdued, signaling that employers are not yet eager to expand their workforce.

Inflation also remains a key focus for the BoC. While some volatility is anticipated in the coming months, the Bank expects underlying inflation to remain steady near 2.5%. The Governing Council believes that the current interest rate is appropriate to keep inflation close to target and to help the economy adapt to ongoing shifts.

Looking ahead, recently robust employment reports have prompted markets to price in the likelihood of one rate hike next year. However, with trade uncertainties persisting and the review of the CUSMA (USMCA) trade agreement approaching, the BoC is committed to a data-driven approach. For now, Canadians should expect the policy rate to be settled in for a long winter’s nap, unless significant changes in economic indicators warrant a shift (Chart 1).

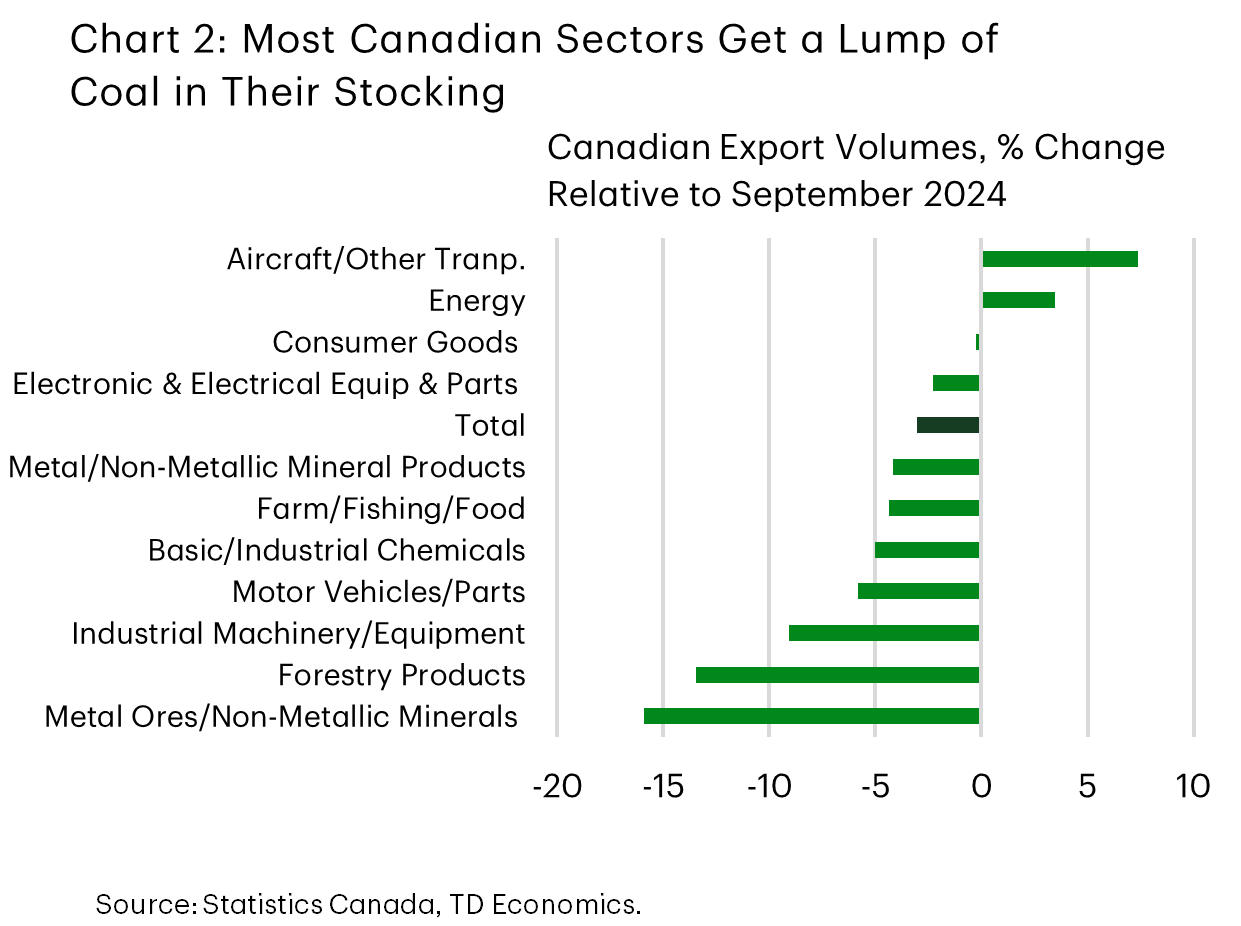

The key piece of data this week was international trade data for September, which had been delayed by the U.S. government shutdown. Canada’s trade position strengthened notably, moving from a $6.4 billion deficit in August to a $153 million surplus. Exports surged by 6.3% month-over-month, with gains distributed across most product categories, especially unwrought gold, crude oil, and aircraft/transportation equipment. That is good news, but looking at exports relative to a year ago, most industries are still in the not-so-festive red (Chart 2).

The latest figures confirm that net trade contributed positively to real GDP growth in the third quarter and suggest a potential upward revision to Q3 GDP figure. While some volatility may remain, the most severe impacts of tariffs appear to be in the rearview, though the future of trade relations will depend on the outcome of the USMCA review.

As Canadians get ready to sip some egg nogg and reflect on 2025, what stands out is the economy’s continued resilience despite global uncertainties. Interest rates have stabilized at a lower level and trade is recovering. The trajectory will depend on how these trends evolve, but for now, the week brings tidings of cautious comfort, in the economy’s underlying strength.

U.S. – Fed Delivers on December Cut, But Signals Slower Pace Ahead

The main event this week was the Federal Reserve’s much anticipated interest rate announcement. While policymakers elected to push ahead with a third consecutive quarter-point rate cut – bringing the target range to 3.50%-3.75% – the move came amid an increasingly divided FOMC (Chart 1). Uncertainty over the extent and timing of future rate cuts didn’t stop the S&P 500 from briefly notching a new all-time high but pared those gains towards the end of the week. The yield curve steepened by roughly 10 bps, with the 10-year currently sitting at 4.19%.

Accompanying the statement, the FOMC also released a revised set of economic forecasts, known as the Summary of Economic Projections (SEP). The SEP represents the median of the individual forecasts submitted by FOMC participant. Relative to the September projection, economic growth for 2025 saw a very modest upgrade (1.7% vs. 1.6%), while there was a notable upward revision to 2026 (2.3% vs. 1.8%). The expected trajectory for the unemployment rate was unchanged, while the inflation forecast is expected to remain above the 2% target through 2027 despite being nudged a tick lower in both 2025 and 2026. Importantly, the median projection on the federal funds rate remained unchanged at 3.6% for 2026 and 3.1% for 2027 – suggesting just one additional cut in each of the next two years (Chart 2). However, there was considerable dispersion across those projections, with the range of estimates for the appropriate level of the policy rate by the end of 2026 spanning 175 bps – a wider range than in September.

The growing divide among policymakers was further underscored by the fact that three participants dissented against December’s decision. Regional Fed Presidents Schmid and Goolsbee favored keeping the policy rate unchanged, while Governor Miran voted for a larger 50 bps cut. But as seen in Chart 2, there were a total of four Fed members who came into the meeting thinking a cut was not required.

The subtle shift in the dots wasn’t lost on market participants. Come January, the four regional presidents who are currently voting FOMC members (Goolsbee, Schmid, Collins, and Musalem) will be replaced by Paulson of Philadelphia, Hammack of Cleveland, Kashkari of Minneapolis and Logan of Dallas. While we don’t know for certain if any of the incoming Fed Presidents ‘quietly’ opposed the December cut, recent speeches by both Logan and Hammack have struck a more hawkish tone. Moreover, Kashkari had advocated for a pause on rate cuts ahead of the October meeting. This suggests that the hawkish tilt from Fed presidents isn’t going away despite the turnover in voting members.

However, this needs to be balanced against a new Fed Chair, who will be in seat May 2026, and is likely to have a more dovish policy stance. Moreover, should Chair Powell elect to not serve out the remaining two years of his term on the board of governors, it will create another vacancy for which President Trump can appoint a new board member. The takeaway from all this is that the division among FOMC members is only likely to deepen next year, putting in question both the timing and extent of further policy easing.

Forward Guidance: Canada’s Inflation Likely Held Steady as We See More Delayed U.S. Data

A busy week of key data releases ahead of the holidays includes Canadian inflation, housing, and employment, while the U.S. will see delayed releases on jobs and inflation.

Canada’s inflation on Monday is expected to have held steady in November with growth in the headline Consumer Price Index remaining at 2.2%, unchanged from October after slowing from 2.4% in September. Gasoline prices rose moderately in November, but were still about 8% below a year ago, thanks to the end of consumer carbon surcharges in April. That leaves energy inflation tracking well below zero.

Food prices, on the other hand, likely continued to grow faster year-over-year, at above 3%, consistent with rising agricultural commodity prices over the first half of 2025.

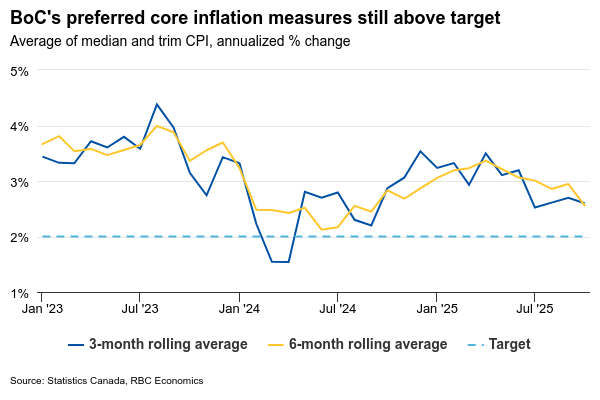

Excluding food and energy, we look for inflation to have held steady at 2.7%. Annual growth in the Bank of Canada's core measures—CPI trim and CPI median—is likely to tick lower but will stay close to the upper end of the 1% to 3% target range for inflation.

We continue to expect no additional BoC rate cuts in the year ahead with underlying inflation persistently above target and economic conditions improving.

Reductions of 275 basis points since mid-2024 should lead to gradual improvements in home resales into 2026. Regional details show more divergence than usual, but abundant supply in key markets means it will likely take a while for prices to start rising.

On Thursday, we'll watch the Survey of Employment, Payrolls and Hours (SEPH) closely for contradicting signs to the consecutive employment increases in the Labour Force Survey (LFS). As of September, employment in SEPH was essentially unchanged versus a 228,000 increase (excluding self-employed workers) in the LFS.

Job vacancies from SEPH already ticked higher in September, and we expect that persisted in October, following increases in Indeed job postings.

More clarity on U.S. jobs and inflation post shutdown

We'll get the long overdue U.S. inflation for November, and labour market reports for October/November for a glimpse of the state of the economy right after the prolonged government shutdown. Our forecast expects little deterioration in labour conditions or inflation over that period.

Payrolls on Tuesday are expected to show roughly 90,000 per month growth in October and November and the unemployment rate is expected to have held at 4.4% in November, unchanged from September.

On Thursday, we look for core U.S. CPI unchanged at 3% year-over-year from September, while headline measure ticked slightly higher to 3.1%, driven by slight accelerations in food and energy prices.

The Federal Reserve sounded cautious about whether additional interest rate cuts would be needed after a 25-basis-point cut in December. If the data broadly evolves as we expect, we think the Fed will deliver just one more 25-basis-point cut in January before pausing for the rest of 2026.

The October surveys that produce the unemployment rate and CPI data were unable to be collected by the Bureau of Labour Statistics during the shutdown, and will not be released.

Week ahead data watch:

Week Ahead – US NFP and CPI, BoE, ECB and BoJ Mark a Busy Week

- After Fed decision, dollar traders lock gaze on NFP and CPI data.

- Will the BoE deliver a dovish interest rate cut?

- ECB expected to reiterate “good place” mantra.

- Will a BoJ rate hike help the yen recover some of its massive losses?

Less-hawkish-than-expected Fed hurts the Dollar

The highly anticipated December Fed decision is behind us, leaving a taste of extreme division among its members, and prompting investors to sell the US dollar. The Committee decided to cut interest rates by 25bps as was widely anticipated, but the updated dot plot pointed to only one single quarter-point reduction for next year.

At first glance this could be characterized as a hawkish cut, especially with two members voting for interest rates to remain on hold, and six officials placing their dot for this year to signal their preference for an unchanged rate.

That said, the dots for 2026 were widely and evenly spread, with four members advocating for no rate cuts in 2026, four favoring one prediction, and four wanting two. So, the median for 2026 did not represent a majority opinion; rather, it was the average of those three equally supported levels.

More importantly, the Committee announced that it will begin purchasing short-term Treasury bills as part of its reserve management operations, with the aim of supporting market liquidity and maintaining control over interest rates.

Combined with a less-hawkish-than-expected press conference by Fed Chair Powell, who highlighted slowing jobs growth and uncertainty about the labor market, this may have been the main reason behind the dollar’s slide, with investors remaining convinced that the Fed may need to cut twice next year.

NFP and CPI inflation to impact Fed rate bets

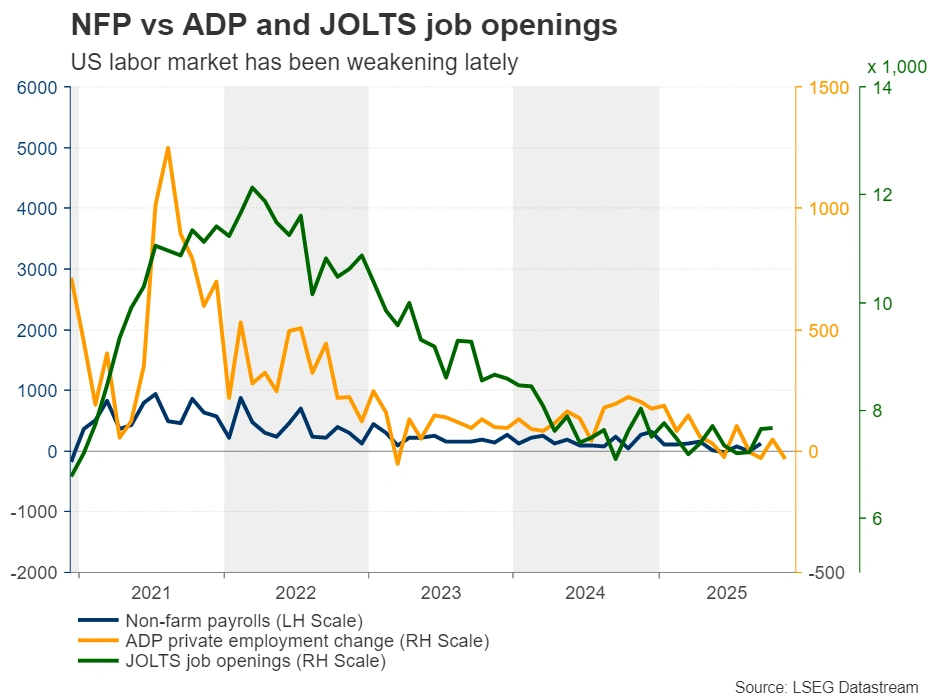

This week, the spotlight is likely to fall on the shutdown-delayed NFP report for November, due out on Tuesday and the CPI numbers for the same month, due out on Thursday. The ADP report for November revealed that the private sector lost 32k jobs, missing analysts’ estimate of a 5k gain, which tilts the risks to the NFP report to the downside.

Even if the CPI data reflects further stickiness in inflation, the Fed seems to be prioritizing the labor market for now, with Powell noting on Wednesday that the current overshooting of the 2% inflation goal is mostly due to tariffs and that it is likely to be a “one-time price increase.” Therefore, the inflation numbers are unlikely to fully reverse any dollar weakness ignited by Tuesday’s NFP report.

The preliminary S&P Global PMIs for December and the retail sales figures for November will also be released on Tuesday and Wednesday, respectively.

BoE to lower rates – Will it signal more cuts for 2026?

Besides the aftermath of the Fed and the key NFP and CPI data out of the US, investors will also have to digest three more central banks this week: The BoE and ECB on Thursday, and the BoJ on Friday.

Getting the ball rolling with the BoE, British policymakers kept rates unchanged in November but via a 5-4 vote, with the 4 dissenters favoring a rate cut and Governor Bailey being the only one of the five who supported the on-hold decision noting that overall inflation risks had moved down. This was probably interpreted as a signal by Bailey that he will join those wanting a rate cut at Thursday’s decision.

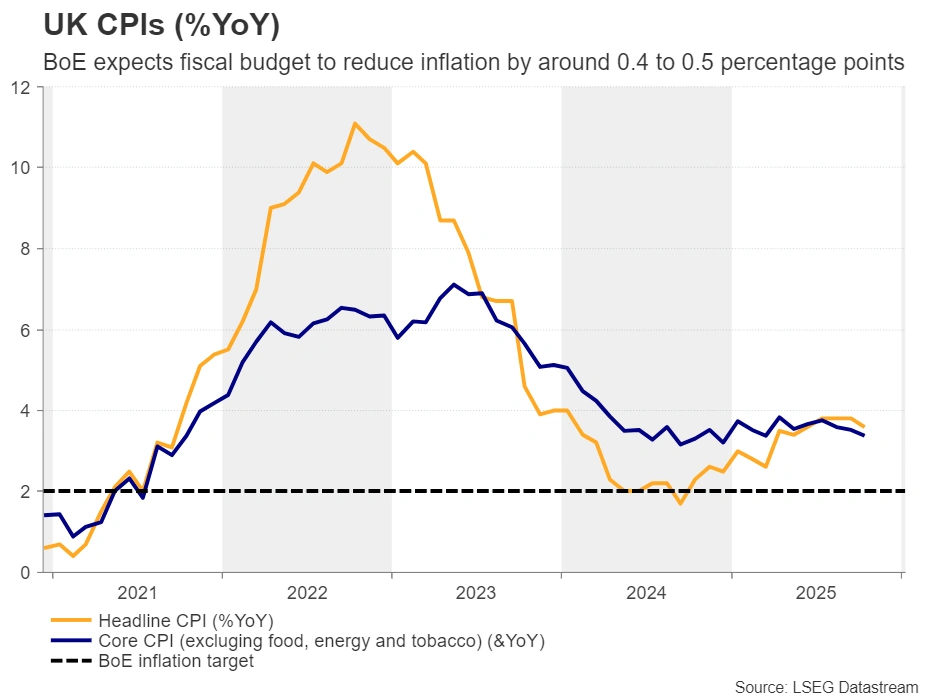

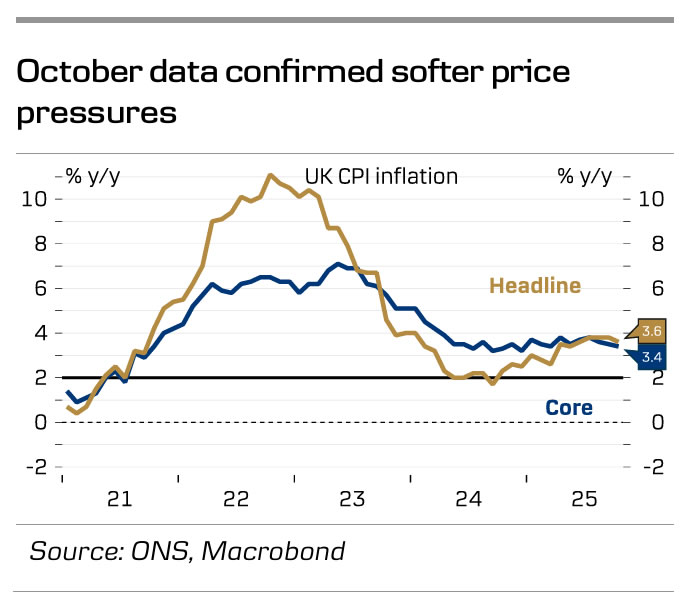

Since the prior meeting, data showed that the unemployment rate for September moved up to 5.0% from 4.8%, economic growth slowed to 0.1% in Q3 from 0.3%, and both the headline and core CPI rates moved slightly lower, although they both remain above 3%.

With all that in mind, investors are now assigning a 90% chance of a rate cut next week, while another quarter-point reduction is more-than-fully priced in by December 2026. It is also worth noting that the Bank of England projected that the latest budget plan announced by finance minister Reeves will reduce the annual inflation rate by around 0.4 to 0.5 percentage points from around the second quarter until the end of 2026.

Thus, a rate cut accompanied by a dovish message could prompt investors to bring forward the timing of the next rate cut and perhaps add some more basis points worth of reductions to their bets for next year. Such an outcome could weigh on the British pound.

Ahead of the decision, a barrage of UK data will be released. The employment report for October and the flash PMIs for December will come out on Tuesday, followed by the CPI and retail sales data on Wednesday and Friday, respectively. A back-to-back slowdown in inflation could solidify the notion of a dovish hold the next day and may trigger a pound slide, even ahead of the BoE decision announcement.

ECB to stay sidelined, upward GDP revisions likely

Around an hour or so after the BoE announcement, it will be the ECB’s turn to make its monetary policy decision public. At the prior meeting, ECB policymakers kept interest rates unchanged, reiterating the view that policy was in a “good place” as the economy was showing signs of health and inflation was close to target.

This week, on Wednesday, ECB President Lagarde said that the resilience of the Eurozone economy to trade tensions and its near-potential growth could prompt the Bank to proceed with upwardly revised GDP projections at next week’s gathering. Taking things a little bit further, ECB Board member Isabel Schnabel told Bloomberg News on Monday that the Bank’s next move may be a rate hike, though it will not happen in the near future.

With all that in mind, investors expect the ECB to stand pat next week, and they are factoring in a respectable 36% chance of a rate hike by the end of next year. Therefore, a reiteration of an upbeat message could help Euro/Dollar march higher, especially if the flash S&P Global PMIs on Tuesday corroborate the notion that the Euro area economy is faring well.

BoJ prepares to raise rates; forward guidance to be scrutinised

Last but not least, the BoJ is now seen raising interest rates with a chance of 75%. As for next year, investors are penciling in another 40 basis points worth of hikes, which translates into another quarter-point reduction and a 60% probability of a third.

Following the election of fiscal dove Sanae Takaichi as Japan’s new Prime Minister, investors scaled back their bets about a potential December hike, but recent remarks by Governor Ueda, as well as reports by Bloomberg and Reuters, revived speculation about action. Yet, the yen failed to massively capitalize on the increasing hawkish expectations.

Therefore, should the Bank press the hike button as largely anticipated, the focus will quickly shift to hints and clues about how the Bank is planning to proceed in 2026. If policymakers fail to match the market’s latest hawkish shift, the yen is likely to resume its prevailing downtrend. However, as dollar/yen moves closer to the psychological zone of 160.00, Finance Minister Katayama may become vocal again in expressing concerns about the yen’s slide and perhaps mention the probability of intervention. All this means that upside risks surrounding the yen are unlikely to vanish, even if the BoJ disappoints market participants on Friday.

Weekly Focus – At Cut, a Hike and a Hold

Solid macro data and hawkish comments from ECB's Schnabel have moved investors' perception of the ECB's next move from cut to hike. This has triggered a further move higher in European bond yields this week. French bonds did experience some tailwinds, though, as the parliament narrowly approved next year's social security budget. Challenges remain ahead with the main budget up for debate next week. It has faced tougher opposition.

A not-so hawkish message from Fed chair Powell also dampened the upward trend in bond yields a bit. USD lost some ground in a week where equity markets edged higher, following the Fed communication. The Fed cut rates as widely expected and Powell made it clear that they are in no hurry to ease further. He also (against ours and markets' expectations) refrained from clearly pushing back against the market pricing, which currently sees slightly more than 50bp of additional cuts for the coming year. The JOLTS report indicated robust labour demand. Details were less rosy, though, as voluntary quits and hires declined, while involuntary layoffs increased.

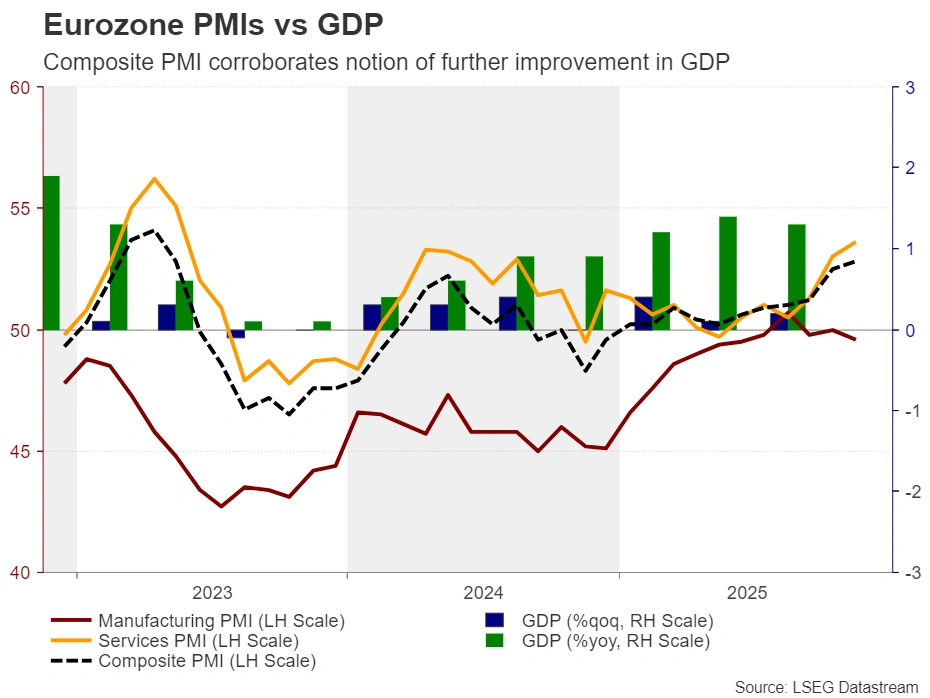

In Germany, industrial production was significantly stronger than expected in October and Sentix data indicates that investors and analysts have become slightly less pessimistic on the euro area economic recovery in December. We expect PMIs will confirm the picture of decent activity next week.

More central banks will be busy taking a stance on their monetary policy. We expect to see a cut, a hike and a hold decision. The ECB will take the latter decision and reiterate that they are in a good place and signal that they will be on hold for a while. We see rates steady for the coming two years. We expect The Bank of England will deliver the cut as we have seen softer inflation, steeper job losses and GDP decline recently. The policy committee is divided, though, and we get fresh CPI data and a labour market report ahead of the meeting.

We count on the Bank of Japan to deliver the hike. In Japan, wages continue to struggle compensating for inflation with real earnings down 0.7% y/y. Besides that, the economy looks solid, though, and tightening is due to avoid further yen slide, which would be unconstructive for the aim of reeling in cost-push inflation. Ahead of the meetings, we will know more of the current shape of the respective economies with the Tankan business survey published in Japan and PMI data released for all three economies.

The data highlight of the week will be the delayed October/November jobs report from the US, where we believe the slowdown in labour supply growth will reflect in a modest 20K/50K job growth. US November CPI data will also be very interesting after the October data was cancelled. We expect core inflation steady at 3.0% yoy.

China releases their big monthly batch of data. We expect it to show more of the same, i.e. still weak consumer spending and housing market but decent increase in industrial production supported by robust exports.

Bank of England Preview – Slowdown Paves Way for Rate Cut

- We expect the Bank of England to cut the Bank Rate by 25bp to 3.75% in line with market expectations. The MPC is split in half, and we expect a 5-4 vote.

- Although key data releases ahead of the meeting could change circumstances, we believe a significantly hawkish surprise is needed to put a rate cut in jeopardy.

- With a divided MPC, we will need more disinflationary signs before we get the final rate cut in April. This will also most likely be reiterated in the guidance.

- If we are right, we expect slightly weaker GBP on announcement.

We expect the Bank of England (BoE) to cut the Bank Rate to 3.75% on Thursday 18 December, which is also largely priced in by investors. At the November meeting, the MPC decided to keep rates unchanged by a narrow 5-4 vote. Governor Bailey casted the deciding vote for hold with the view: "Rather than cutting Bank Rate now, I would prefer to wait and see if the durability in disinflation is confirmed in upcoming economic developments this year". We believe it has been confirmed.

CPI inflation declined to 3.6% in October in line with BoE projections with service inflation slightly lower than consensus. This was not in itself a low print, but it confirmed that the soft September print was not just a blip. On the labour market, job losses have accelerated in the fall with most recent data, showing a 32K decline in September and October. The unemployment rate increased to 5% and wage growth has been edging lower in September. GDP data for October also disappointed with another 0.1% mom contraction driven by a weak service sector. The economy has not grown since June.

The fiscal stance laid out in the 2026 budget was mildly contractionary with no new inflation headaches from VAT hikes but with modest cuts to energy bills. We think the news since the November meeting will suffice for Governor Bailey to journey into the camp voting for a rate cut, although the labour market report and CPI data released in the days ahead of the meeting is a joker. According to November PMIs it does not look like, these releases will change the dovish picture much. They suggest, price pressures have eased further, and job losses have accelerated.

BoE call. Considering the recent tunes from the most hawkish members of the MPC, we see neither Lombardelli, Pill, Mann or Greene voting for a rate cut any time soon. Parti-cularly not to 3.50%. Thus, rate cuts need to be taken with a slim 5-4 decision. Ramsden, who voted for cut in November, has also stressed the need for gradual cuts to borrowing costs. We think Bailey will take a cautious approach and listen to both sides when timing the next rate cut and that a majority will vote for a final rate cut at the April meeting.

Market reaction. We expect slightly weaker GBP on announcement. More broadly, we stay negative on GBP FX on a relatively weak growth outlook and a positive correlation to a USD negative environment.

Gold (XAU/USD) Price Outlook: 1% to All-Time Highs, getting Jealous of Silver

As highlighted in our overnight session rewind, Gold has quickly breached above $4,300 and is now racing towards new all-time highs.

The Fed's cutting cycle and overall 2025 US Exceptionalism from the Trump Administration have had a considerable effect on the demand for non-fiat assets, and Gold is the primary beneficiary of such demand.

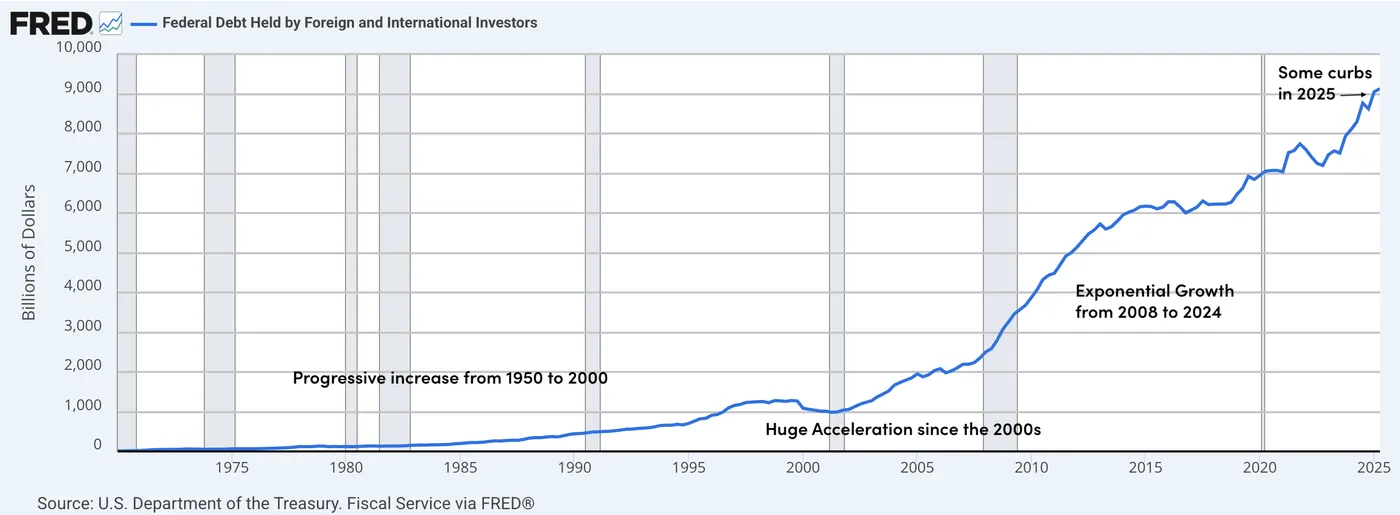

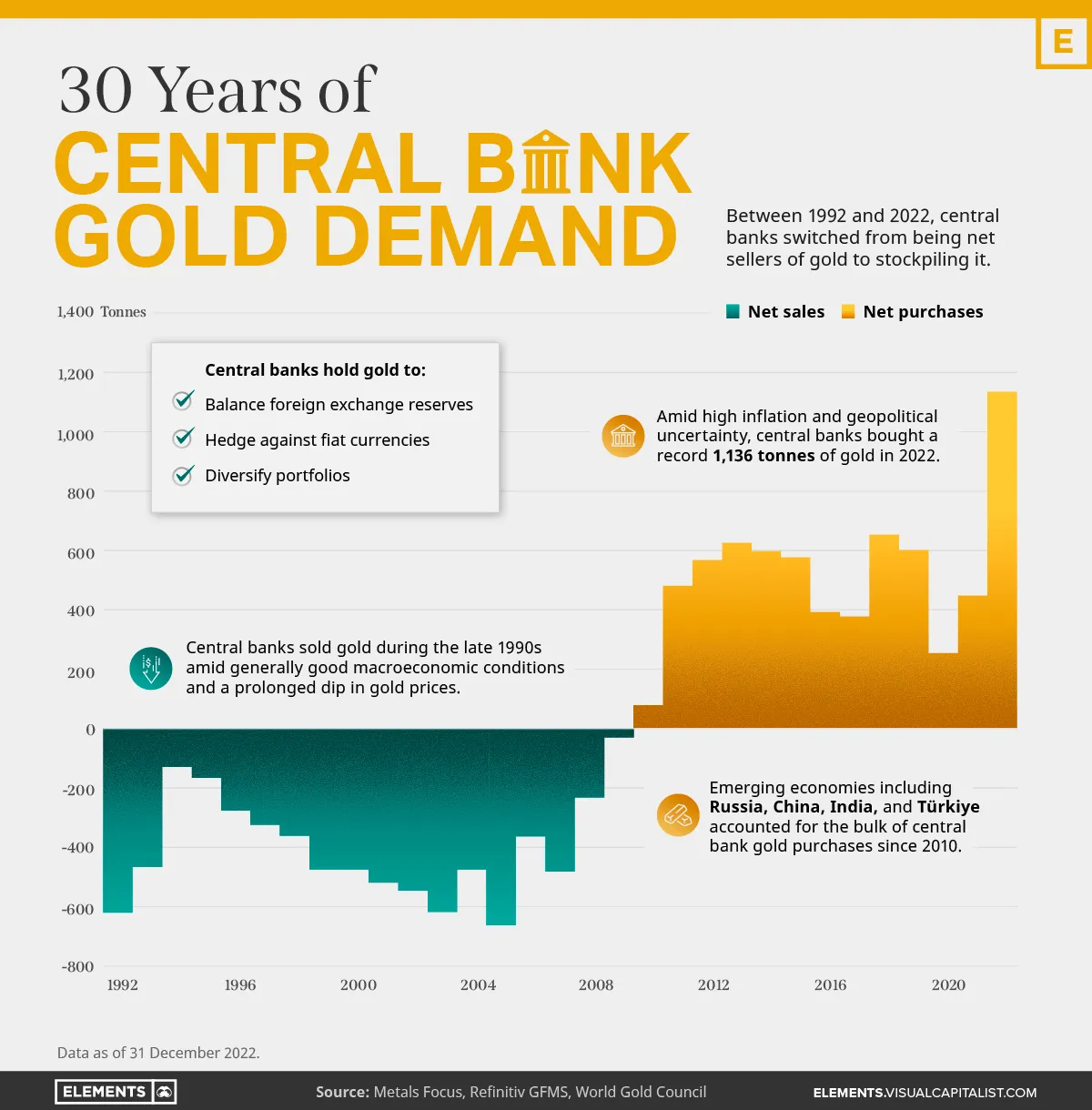

The financial world order since the early 2000s has been characterized by high demand for US Treasuries.

As the US maintained higher rates relative to others, even during the Global Financial Crisis, and consequently recovered much more solidly than its OECD peers, it absorbed the flows from the entire globe.

US Debt holdings by Foreign Investors (Central Banks and others) – Source: St. Louis Fed

Metals, on the other hand, were getting replaced by their yielding rivals - Treasuries.

Some Countries, like Canada, have emptied their gold reserves, for example, Making Questionable decisions.

However, as yields had been trending lower, particularly after the QE, demand for metals reformed again, and now, their attraction is without question.

Gold demand from 1992 to 2022 – Courtesy of Elements-VisualCapitalist.

Government deficits are ever-increasing, even with a stable global economy, and the US seemingly cannot be as trustful of a global riches reserve, given the several diplomatic heatwaves provided by Donald Trump.

Tariffs aren't the most welcomed policies if you want to retain buyers of your government bonds.

Particularly when you're cutting rates.

In any case, since reaching its COVID lows in March 2020 ($1,451), Gold is up close to 200%, and most of its gains have occurred since February 2024.

However, what is grabbing Markets' attention is how strong the acceleration has been ongoing since August 2025 and Powell's Jackson Hole speech, which may have been a turning point for global Markets.

Let's dive into a multi-timeframe Gold analysis to get a closer look on the post-FOMC rebound as the Yellow metal aims to protect its throne.

Gold (XAU/USD) Multi-Timeframe Analysis, Technical levels and Potential Price Targets

Daily Chart

Gold (XAU/USD) Daily Chart. December 12, 2025 – Source: TradingView

Our pre-FOMC Metals analysis pointed to a potential breakout in Gold after a triangle consolidation – And it is currently playing out.

Bulls used the 50-Day Moving Average as support. Keep a close eye on it as it has been serving as loyal support throughout 2025.

The rest will be to see if buyers can make the push beyond new highs.

Up 3.75% in 3 sessions, momentum is gathering some heat despite some not-so-dovish 2026 Fed Cut projections – Until more data is served for Markets (Tuesday 16 - US NFP) not much can come to stop the rally.

Metal buyers just wanted to see rates coming down, and they are getting served.

Silver and its ongoing frenzy is dragging demand for such commodities higher.

An interesting Chart: Silver to Gold Ratio

Silver to Gold Ratio – Monthly Chart. December 12, 2025 – Source: TradingView

4H Chart, Technical Levels and potential Price targets

Gold (XAU/USD) 4H Chart. December 12, 2025 – Source: TradingView

As indicated in our recent piece (link just above), a measured move higher (Yellow squares) could take prices anywhere to $4,500 to $4,575 if buyers manage to break recent highs.

Levels to watch for Gold (XAU/USD) trading:

Resistance Levels

- Current All-time High resistance $4,300 to $4,400

- $4,380 Current all-time Highs

- Fib-Induced potential new ATH resistance $4,500 to $4,575

- Session highs $4,346 (and counting)

Support Levels

- Hourly Pivot and Triangle top $4,200 to $4,240

- 50-Day MA $4,150

- Major Pivot $3,950 to $4,000 (200-period MA)

- $3,700 consolidation Support

- $3,500 Major Support

1H Chart

Gold (XAU/USD) 1H Chart. December 12, 2025 – Source: TradingView

Despite the overbought conditions on all timeframes, the rally isn't showing signs of stopping.

Watch for any stalling of momentum however.

A consolidation between $4,300 to $4,350 provides higher chances of a breakout as the RSI slows down.

A retracement however points to a more balanced price action going forward.

Safe Trades!

Sunset Market Commentary

Markets

Two of Wednesday’s dissenters at the Fed hit the wires today. Goolsbee and Schmid both favoured to keep the rate steady but it appears both had a different angle to do so. Schmid wants to keep monetary policy slightly restrictive, citing a balanced labour market but too high inflation and an economy that’s showing momentum. Goolsbee on the other hand was simply concerned on frontloading cuts too much. He wanted to wait till Q1 after some “concerning” inflation data prior to the shutdown. He went on to say he’s projecting more cuts than the median and thinks rates can come down “a significant amount” next year. Neither policymaker had a material impact on (short-term) US rates though. We do see some (natural?) bear steepening of global curves in an otherwise quiet trading session. Long-end yields rise up to 5 bps in the US and around 4 bps in Europe and the UK. European stocks inch higher with the EuroStoxx50 now just a sigh away from its November record high. Tech on WS underperforms following Broadcom’s (lofty) sales outlook miss but declines for the likes of the Nasdaq are limited to 0.3%. The dollar recovers some ground after a two-day beating. EUR/USD trades near 1.173, DXY grinds higher to 98.48. Sterling extends yesterday’s losses after a poor set of economic data this morning in which the surprising monthly GDP drop stood out. EUR/GBP recovers the previously lost support area at 0.8769.

Today’s poor economic calendar puts the spotlight on the one of the coming week. The US publishes November payrolls on Tuesday along with October retail sales and December PMIs that day. November inflation figures are scheduled on Thursday. They carry big value coming after a Fed that cut rates for a third time this week but basically moved in the dark due to the lack of economic input. They’ll certainly shape market expectations for the Fed in early 2026. We consider a weak(er than expected) batch to have the bigger moving potential (ie. lower US rates and dollar) by markets upping the ante for January. The Bank of Japan’s Q4 Tankan on Monday should convince the remaining (if any) doubters on upcoming rate hike at Friday’s policy meeting. Inflation figures are published the same day and will be an above 2% target reading for the umpteenth month running. The UK central bank meets and likely lowers rates to 3.75%. The BoE has to move cautiously though with November inflation - released on Wednesday - expected to be trending north of 3% still. UK PMI business confidence and the October labour market report is on tap Tuesday. The ECB by Thursday will also have a new set of PMIs at its disposal. President Lagarde already hinted earlier this week at another upgrade to the growth forecasts, cementing the case for a 2% deposit rate for longer. She might get grilled on the impact of the carbon tax being postponed on the inflation outlook in 2027. It could push inflation below target but we expect the central bank look through it since it is out of monetary reach. Additionally, having the tax postponed could also be considered as a positive demand shock that at least partially replaces the cost push shock.

News & Views

The Bank of England published its quarterly Inflation Attitudes Survey, conducted by Ipsos. The perception of the UK inflation rate amongst surveyed residents stood at 4.7%, slightly less than the 4.8% in August. Inflation expectations for the next 12 months, the 12 months thereafter and the long-term (5-yr) were all 0.1 ppt lower as well at respectively 3.5%, 3.3% and 3.7%. When asked about the future path of interest rates, 38% of respondents expected rates to rise over the next 12 months, up from 33%. 24% said they expected rates to stay about the same over the next twelve months (from 26%) and 25% said they expected rates to decline over the next twelve months (from 29%). Respondents were also asked to assess the way the Bank of England is ‘doing its job to set interest rates to control inflation’. The net satisfaction balance, the proportion satisfied minus the proportion dissatisfied, was -1%, down from 2% in August.

SEB research’s quarterly investor survey, targeting large Swedish institutional fixed income investors, showed all respondents expected an unchanged Riksbank policy rate at 1.75% in December and January. For December 2026, policy rate expectations shift to the upside. 40% of the respondents predict at least one rate hike, while the share expecting a rate cut have increased only slightly to 28% (from 24% in June). For December 2027, expectations for rate hikes dominate even more. A broad majority (72%) expect the policy rate to be above the current level (1.75%), while the share predicting a policy rate below declines to 12%. The median expectation for the policy rate is 2.25%.