Sample Category Title

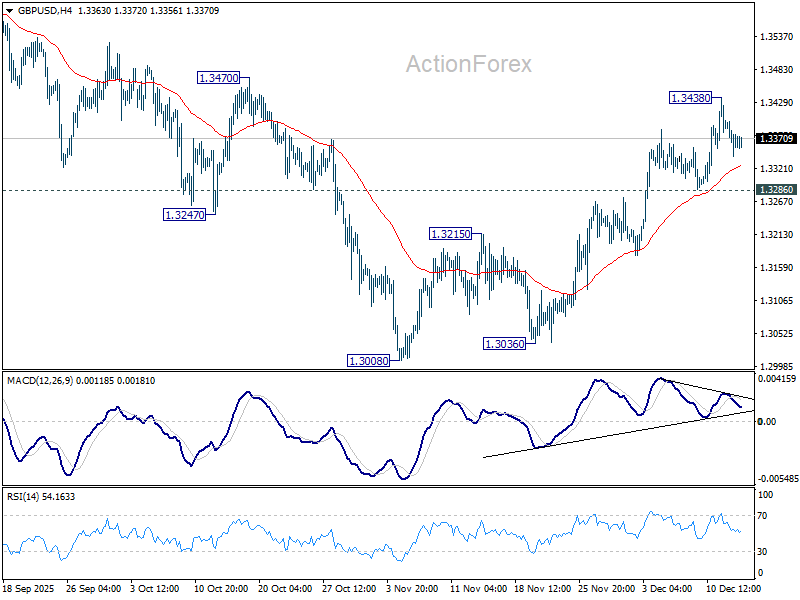

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3342; (P) 1.3371; (R1) 1.3400; More...

Intraday bias in GBP/USD remains neutral and further rally is expected as long as 1.3286 support holds. As noted before, fall from 1.3787 should have completed as a three-wave correction to 1.3008. Above 1.3428 and firm break of 1.3470 resistance will pave the way back to retest 1.3787 high. However, sustained break of 1.3286 support will mix up the near term outlook.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

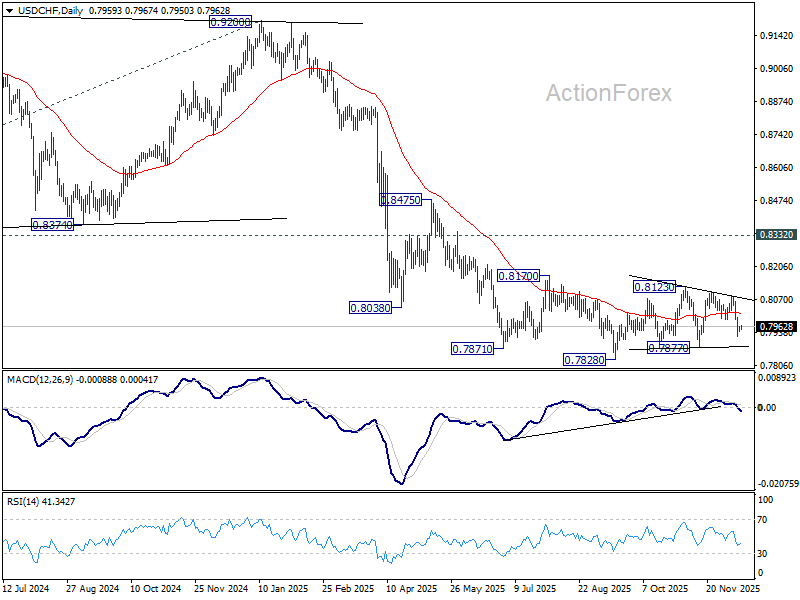

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7946; (P) 0.7955; (R1) 0.7970; More…

Intraday bias in USD/CHF remains neutral for the moment. Overall outlook is unchanged that corrective pattern from 0.7828 is still extending. On the downside, below 0.7923 will target 0.7877 support. On the upside, though, break of 0.7990 support turned resistance will bring stronger rebound towards 0.8084.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

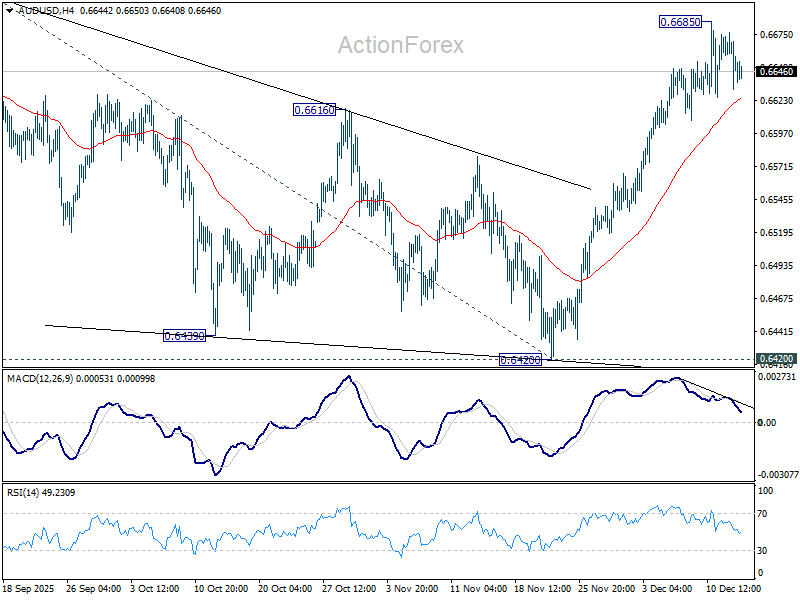

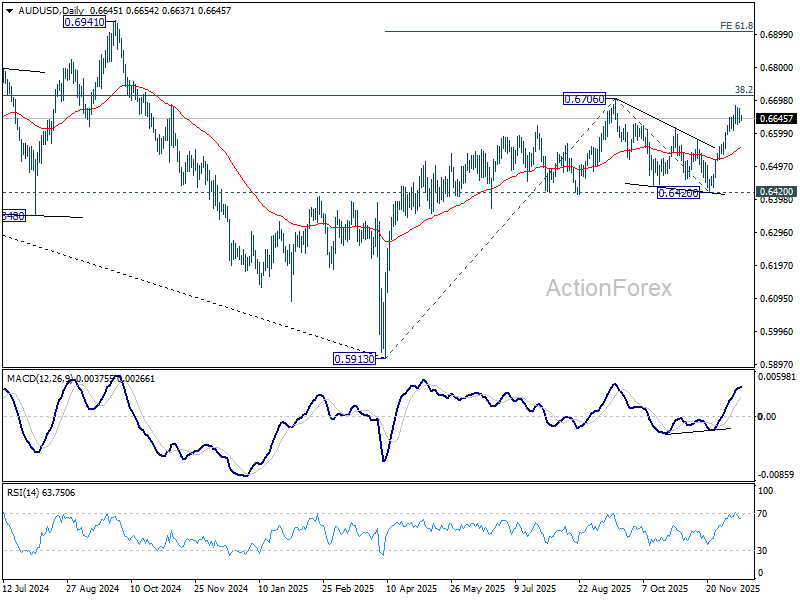

AUD/USD Daily Report

Daily Pivots: (S1) 0.6632; (P) 0.6655; (R1) 0.0.6676; More...

Intraday bias in AUD/USD stays neutral and some more consolidations could be seen below 0.6685. On the upside, firm break of 0.6706 will confirm resumption of whole rise from 0.5913. Next target is 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. However, break of 55 D EMA (now at 0.6556) will extend the corrective pattern from 0.6706 with another falling leg.

In the bigger picture, the break of multi-year falling trend line resistance suggests that rise from 0.5913 is possibly reversing whole down trend from 08006 (2021 high). Decisive break of 38.2% retracement of 0.8006 to 0.5913 at 0.6713 will solidify this case, and bring further rally to 61.8% retracement at 0.7206. On the downside, however, firm break of 0.6420 support will suggest rejection by 0.6713 and retain medium term bearishness.

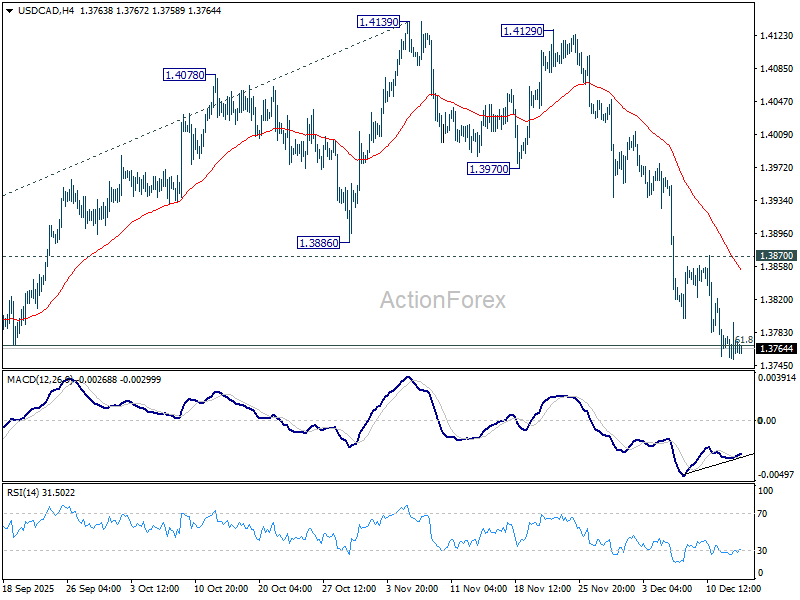

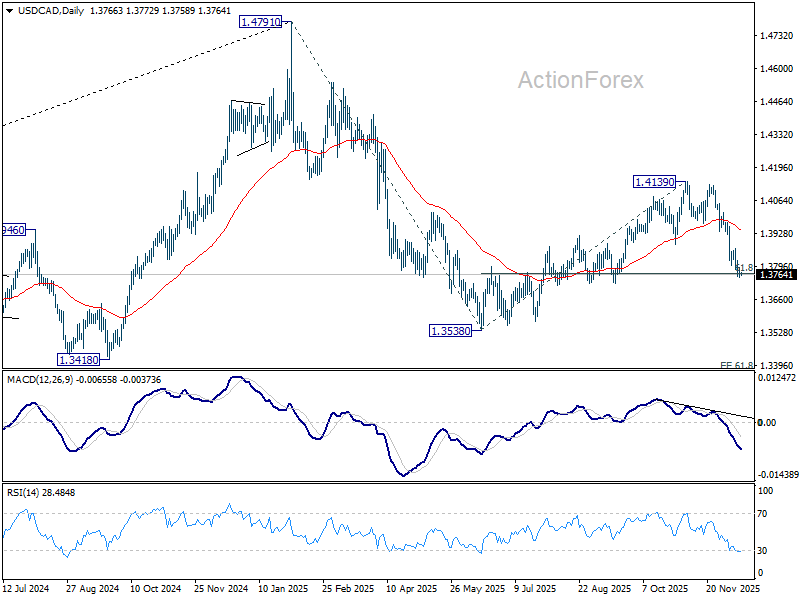

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3752; (P) 1.3773; (R1) 1.3793; More...

Intraday bias in USD/CAD stays mildly on the downside for the moment. Sustained trading below 61.8% retracement of 1.3538 to 1.4139 at 1.3768 will argue that whole decline form 1.4791 might be ready to resume and targets a retest on 1.3538 low. On the upside, however, break of 1.3870 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it's just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.

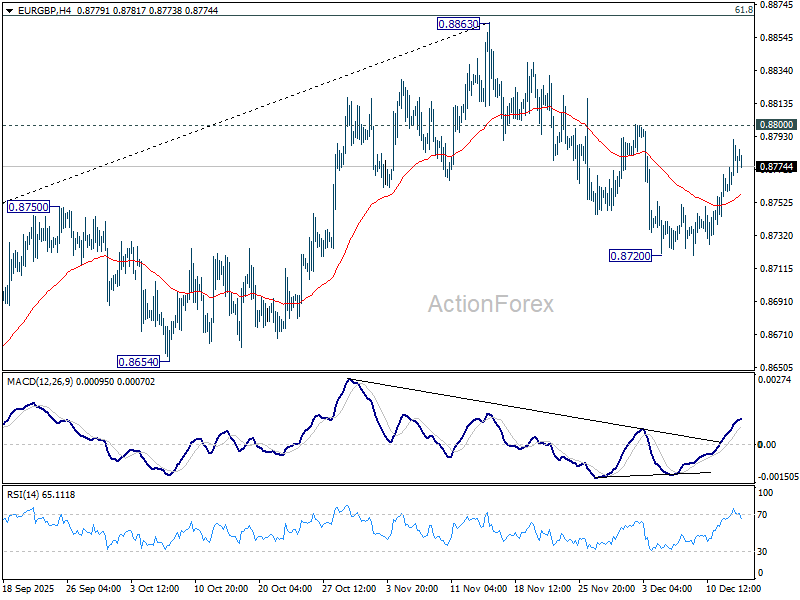

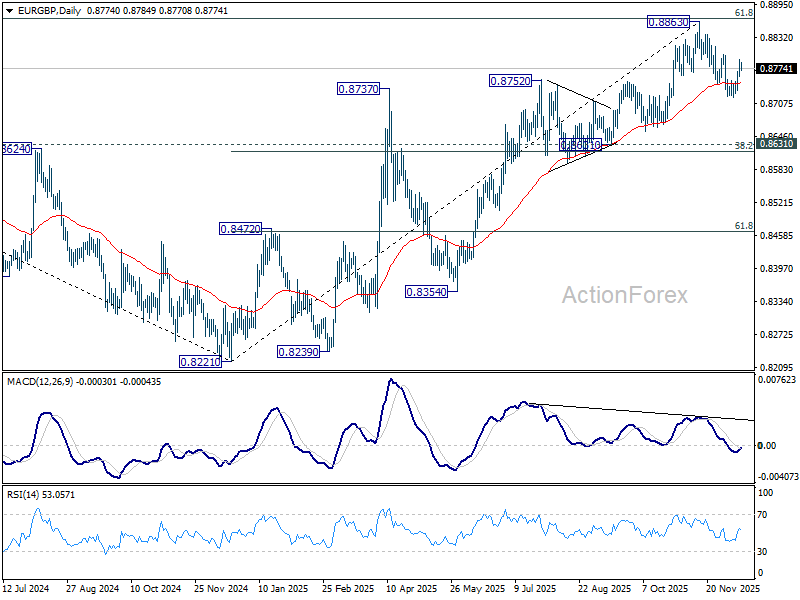

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8763; (P) 0.8777; (R1) 0.8794; More…

Intraday bias in EUR/GBP stays neutral at this point. With 0.8800 resistance intact, further decline is mildly in favor. Below 0.8720 will target 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618). However, break of 0.8800 will turn bias back to the upside for retesting 0.8863.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8605) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

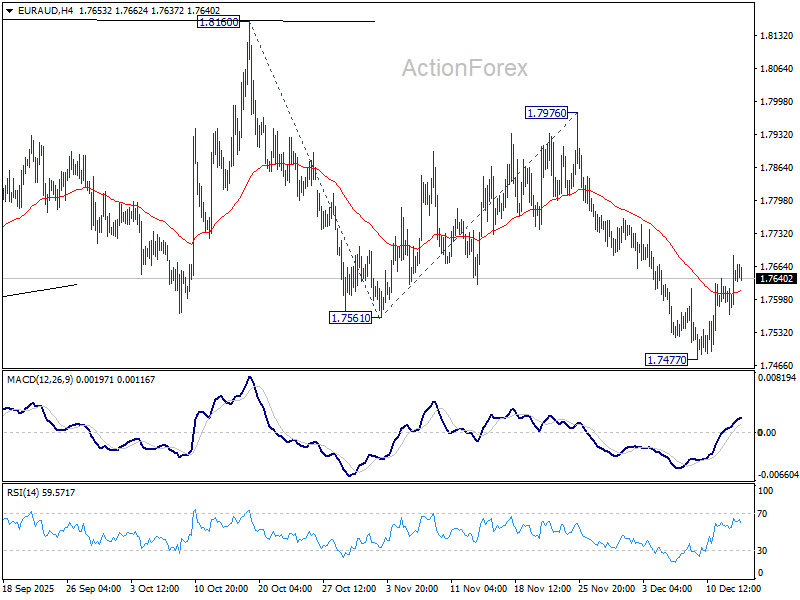

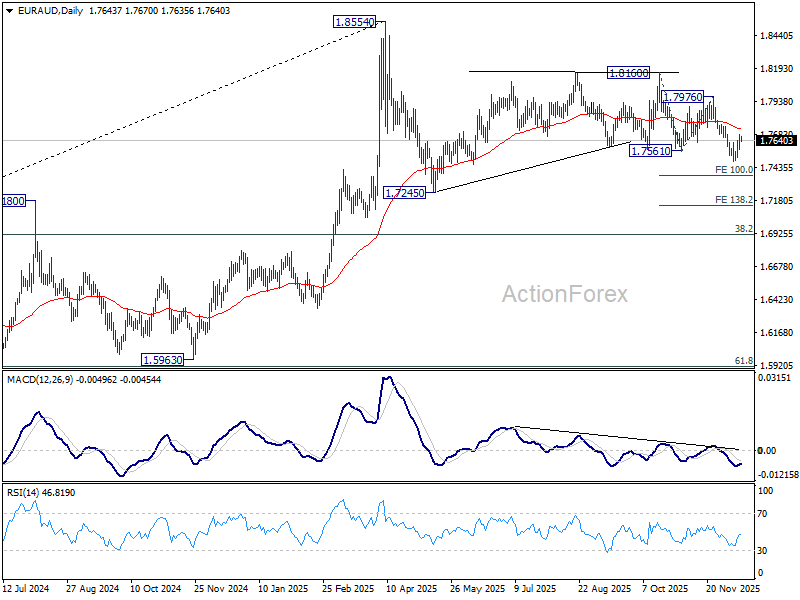

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7584; (P) 1.7636; (R1) 1.7701; More...

Intraday bias in EUR/AUD remains neutral for the moment. On the downside, below 1.7477 will extend the decline from 1.8160 to 100% projection of 1.8160 to 1.7561 from 1.7976 at 1.7377. Firm break there will pave the way to 138.2% projection at 17148. However, sustained break of 55 D EMA (now at 1.7728) will bring stronger rebound back to 1.7976 resistance.

In the bigger picture, as long as 55 W EMA (now at 1.7465) holds, price actions from 1.8554 could still be a correction to rise from 1.5963 only. However, sustained break of the EMA will argue that it's already correcting the whole up trend from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922.

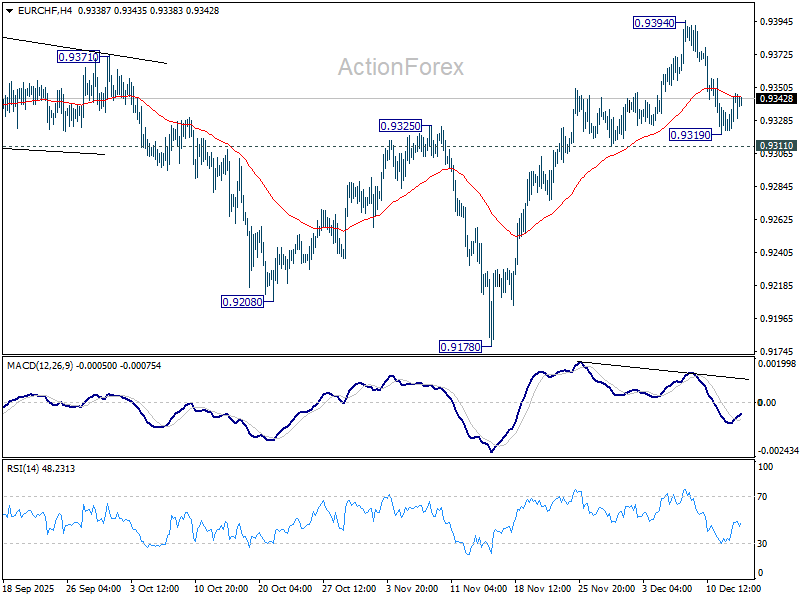

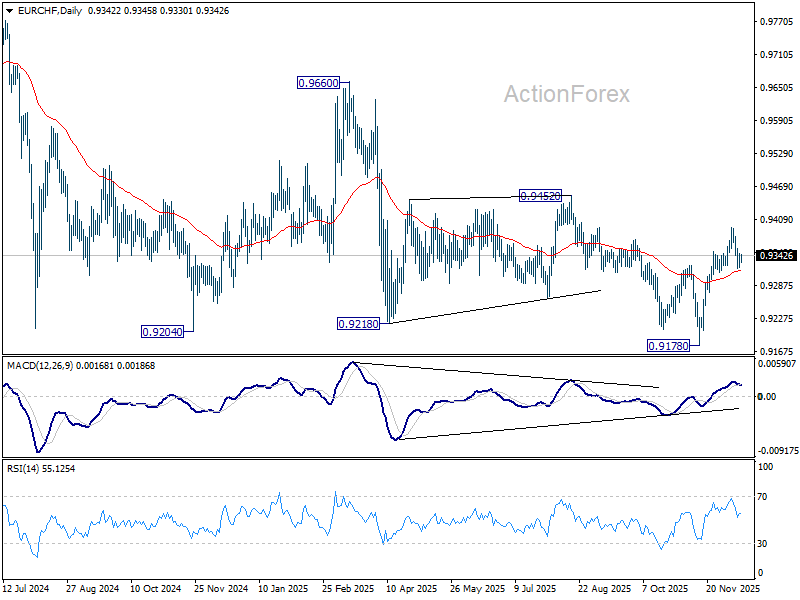

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9329; (P) 0.9338; (R1) 0.9354; More....

Intraday bias in EUR/CHF stays neutral for the moment, and more consolidations could be seen. On the upside, break of 0.9394 will resume the rebound from 0.9178 to 0.9452 structural resistance. Decisive break there will carry larger bullish implications. However, firm break of 0.9311 support will argue that the rebound has completed, and turn bias back to the downside for retesting 0.9178 low.

In the bigger picture, EUR/CHF has breached long term falling channel resistance as the rebound from 0.9278 extends. Considering bullish convergence condition in W MACD, sustained trading above 55 W EMA (now at 0.9316) will indicate medium term bottoming at 0.9178, and suggests that it's already in larger scale rebound. Further break of 0.9452 resistance will bring stronger medium term rally towards 0.9928 resistance next. Nevertheless, rejection by 55 W EMA will retain bearishness for another fall through 0.9278 at a later stage.

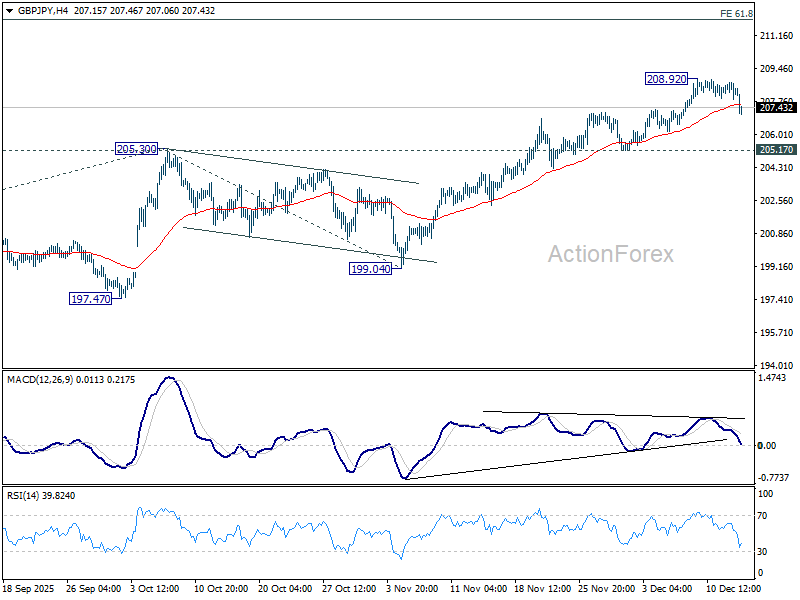

GBP/JPY Daily Outlook

Daily Pivots: (S1) 207.91; (P) 208.33; (R1) 208.78 More...

Intraday bias in GBP/JPY stays neutral as more consolidations would be seen below 208.92. Further rally is expected as long as 205.17 support holds. ON the upside, break of 208.92 will resume larger up trend and target 61.8% projection of 184.35 to 205.30 from 199.04 at 211.98 next.

In the bigger picture, up trend from 123.94 (2020 low) is resuming. Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. On the downside, break of 199.04 support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.

BoJ’s Quarterly Tankan Survey Shows a Constructive Picture

Markets

AI valuation stress kicks in for the second time this quarter after industry giant Broadcom’s sales outlook failed to live up to (outsized) expectations. Earlier last week, Oracle got punished for delay in completing data centers. The high beta part of the market sold off with the S&P and Nasdaq losing 1.1% and 1.7% respectively. Both key indices failed to take out the October highs in the run-up to the correction lower on Friday, in what might be a further completion of a technical head-and-shoulders formation with necklines around 6550 and 22 000. Technical pictures in the small-cap Russell 2000 or industrial Dow Jones look different (both set new highs last week), suggesting that the equity move at least for now is buffered by some rotation rather than being a broad-based market sell-off.

The equity market set-up is something to take into account as we start a jampacked week. German Chancellor Merz and Ukrainian President Zelenskyy meet today to continue peace talks. Zelenskyy yesterday said that he is ready to give up demands for NATO membership in exchange for security guarantees from the US and Europe. It’s a new tweak to the US peace proposal under discussion. There’s no breakthrough on the most thorniest issue today, territory concession. On Thursday, EU leaders also meet to decide on how to morph the frozen Russian assets at Euroclear into two year of financing for Ukraine. Focus turns to the eco data tomorrow with US November payrolls and October retail sales. Global PMI surveys (December) and UK labour market are due as well. For US payrolls we see asymmetric risks with (the front end) of the US yield curve reacting more strongly in case of data weakness compared to solid numbers. Markets were attentive to Fed Chair Powell’s suggestion that recent data overstated US labour market strength and were keen to respond to it (raising Q1 rate cut bets). For Europe, we see asymmetric risks (to PMI’s) as well but in the opposite direction. This creates space for EUR/USD to further explore the upper part of the sideways trading channel in place since summer. The YtD high (EUR/USD 1.1919) serves as key reference. ECB Schnabel opened to door for a rate hike last week (after a long pause) while more dovish ECB member shut the door to more rate cuts. This view should be backed by upward revisions to GDP forecasts at Thursday’s ECB gathering. Downward revisions to 2027 CPI forecasts might be ignored and downplayed as a technical issue related to the delay of the EU’s Emissions Trading System 2 (ETS2). For UK labour market data (and UK CPI numbers on Wednesday) we’re back in the US situation where markets will be keen to err on the dovish side of expectations. The Bank of England convenes on Thursday as well and is set to lower its policy rate from 4% to 3.75%. The EUR/GBP YtD high and reference stands at 0.8865.

News & Views

The BoJ’s Quarterly Tankan survey shows a constructive picture on the state of the economy. The closely watched large manufacturers’ sentiment index improved from 14 to 15, the best level since end 2021. The index measuring sentiment on large non-manufacturing companies held at the same level as in Q3 (34), but still hovers near the strongest levels since the 1990’s. The outlook also improved at large manufacturers (15 from 12) and remained unchanged for large non-manufacturers. Large industry capex is expected to growth at 12.6% this fiscal year. Companies expect overall global prices rises to hold near a pace of 2% over a 5-y horizon. The data strengthen the view that the BoJ will continue its policy normalization cycle with a 25 bps rate hike on Friday. Bloomberg also suggests this morning a likely start to selling ETF’s from January on. This process is expected to develop in a very gradual way in order not to disturb markets and might take decades. (starting pace of JPY 330bn/year).

Friday’s government bond issuance plan for 2026 by Slovak debt agency Ardal, shows gross issuance to be around €10bn next year. Two new syndicated deals are part of the plans. The agency intends to issue a new bond line with fixed coupon and time to maturity from 12 to 20 years (expected in H1 2026) and a new bond line with fixed coupon and time to maturity of 10 years (expected in H2 of 2026). The total expected amount to be sold via syndicated sales is EUR 5bn, regardless of the number of transaction. Aside from the syndicated sales it also intends to issue two new retail bonds lines with maturities up to 5 years. Other bond lines (including foreign currency) can be opened based on debt management requirements and investor’s demand.

Tech Disappetite

Last week ended on a mixed note for equities. Looking at global index performance, the message was fairly clear: investor appetite is waning for AI-related technology stocks, while non-tech and more value-oriented pockets of the market are benefiting from the latest Federal Reserve (Fed) rate cut.

In the US, the Dow Jones briefly hit a fresh all-time high on Friday before retreating, while the tech-heavy Nasdaq fell 1.9%, sliding into its 50-day moving average. Earnings from Oracle and Broadcom were not strong enough to reignite enthusiasm, with investors instead focusing on high leverage, elevated debt levels and cloudy revenue visibility.

To rub salt in the wound, Oracle said it is pushing back the completion dates of some data centres developed for Nvidia from 2027 to 2028, citing labour and material shortages. That announcement proved to be the final blow: Oracle shares fell another 4.5% on Friday, after plunging more than 10% the day before following its Q3 results. Stress is also visible across related assets: Oracle’s new investment-grade bonds are trading at distressed levels, while its five-year CDS spiked to the highest level since 2009.

When the market’s AI risk barometer struggles, the sector’s kingpin is unlikely to remain unscathed. Nvidia shares fell more than 3%, despite reports that Chinese demand for its H200 chips exceeds current production capacity. Nvidia is now allowed to sell these chips to China provided a 25% cut of revenues is paid to the US government. The issue, however, is that there is no guarantee Beijing will allow Chinese firms to purchase them freely, given its determination to build domestic chip capacity. China, therefore, may not provide the safety net investors are hoping for.

More broadly, while Nvidia’s revenues continue to grow thanks to massive investment in AI infrastructure, investors increasingly want to see monetisation through AI-enabled end products, not just spending. That matters because investors ultimately finance this capex cycle through equity and bond markets. If their support fades, spending will need to be trimmed — and Nvidia would inevitably feel the impact.

Against this backdrop, Bitcoin — often seen as a bellwether of tech and risk appetite — remained under pressure over the weekend. While slightly firmer this morning, it is still trading below $90’000. Asian tech stocks also opened the week on the back foot, with SoftBank down more than 6%. If the global tech sell-off deepens, Bitcoin could retest — and potentially break — the key $80’000 support level.

Looking ahead, Micron’s earnings this week could add to the gloom for the tech sector. A deeper tech correction would likely accelerate rotation into non-tech and non-US assets. In the US, the Dow Jones could continue to attract flows, while in Europe the Stoxx 600 and FTSE 100 may benefit from their value tilt. For the UK market, a potential Bank of England (BoE) rate cut on Thursday could provide additional support. The BoE is expected to lower rates by 25bp, as it continues to support a weakening economy. Recent UK growth data were particularly poor, and upcoming budget measures are unlikely to improve the outlook in the near term.

China is also struggling. Recent growth, retail sales and industrial production data disappointed sharply, underscoring how reliant Chinese markets have become on tech optimism. The silver lining is that Beijing is likely to respond with further stimulus, which typically resonates well with investors.

Elsewhere, both the European Central Bank (ECB) and the Bank of Japan (BoJ) will deliver their final policy decisions of the year. The ECB is expected to stay on hold, arguing that policy is close to equilibrium while remaining data-dependent. In contrast, the BoJ is widely expected to hike rates. That move appears largely priced in, with Japanese yields rising sharply: the 10-year has pushed above 1.95%, while the 30-year is flirting with 3.40%, narrowing the gap with US yields. This raises the risk of Japanese investors repatriating capital from US Treasuries.

But, Keep Calm! The Federal Reserve has begun buying roughly $40bn per month of short-term Treasury bills to support bank reserves and stabilise short-term funding markets after years of quantitative tightening weighed on liquidity. Officials stress this is not QE, but a “reserve management” operation aimed at ensuring sufficient reserves to keep policy rates under control.

Better news: According to the New York Fed’s operational schedule, total transactions could exceed $54bn over the next month, including reserve-management purchases and reinvestments. And frankly, regardless of the label, $40bn of central-bank Treasury buying is still $40bn of liquidity entering the system — liquidity that tends to find its way into stocks, bonds and metals.

The final test this week will be US CPI and non-farm payrolls. Investors want soft labour data to justify further rate cuts — but not numbers too weak to signal a sharp earnings slowdown. And everyone wants inflation to continue easing toward the Fed’s 2% target. Lower inflation remains the key ingredient for sustaining risk appetite.