Sample Category Title

Canada CPI unchanged at 2.2% in November, services inflation cools

Canada’s inflation data came in softer than expected in November. Headline CPI was unchanged at 2.2% yoy, undershooting expectations for an uptick to 2.4% and suggesting inflation remains comfortably contained near target.

The moderation was led by services inflation, which slowed to 2.8% yoy from 3.2% in October. That deceleration more than offset firmer goods prices, where grocery inflation accelerated sharply to 4.7% from 3.4%, the strongest pace since December 2023.

Gasoline prices also fell at a slower annual pace, declining -7.8% yoy compared with a -9.4% drop previously. Stripping out gasoline, CPI rose 2.6% year over year for a third consecutive month, pointing to stability rather than renewed inflation momentum.

Core measures reinforced that message. CPI Median slowed to 2.8% from 3.0%, while CPI Trim eased to 2.8% from 2.9%, both coming in below expectations. CPI Common edged up slightly to 2.8%, matching forecasts.

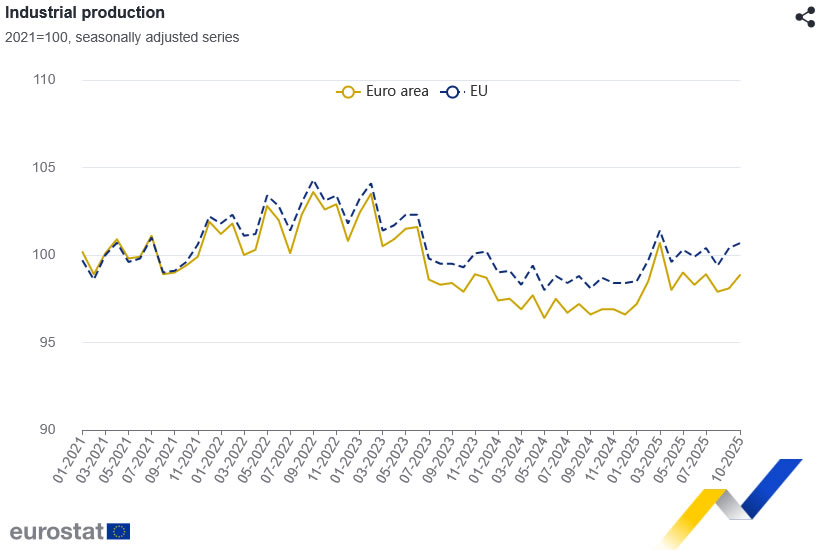

Eurozone industrial production rises 0.8% mom in October, beats expectations on broad-based gains

Eurozone industrial production delivered a modest upside surprise in October, rising 0.8% mom and beating expectations for a 0.7% increase.

The gains in the Eurozone were broad-based across sectors. Output of energy rose 1.1% mom, capital goods increased 0.5%, and intermediate goods edged up 0.3%. Consumer-related categories were firmer, with durable consumer goods jumping 2.0% and non-durable goods rising 1.2%, suggesting some resilience in downstream demand.

Across the wider EU, industrial production increased 0.3% mom, masking sharp country-level divergences. Ireland (4.0%), Luxembourg (3.6%), and Croatia (3.1%)posted the strongest gains, while Sweden (-6.5%), Belgium (-3.4%), and Denmark (-3.2%) recorded steep declines.

SECO upgrades 2026 GDP forecast, downgrades inflation

Swiss economic prospects have improved modestly, with the Federal Government Expert Group on Business Cycles revising up its 2026 growth forecast. GDP adjusted for sporting events is now seen expanding 1.1%, up from 0.9% projected in October, bringing the outlook broadly back in line with June forecasts when US tariffs stood at 10%. The reduction in US tariffs has improved conditions for exposed sectors and eased pressure on foreign trade.

Foreign demand is expected to provide a positive, though still "moderate", contribution next year. Domestic demand, however, remains the "main driver of growth", supported by resilient consumption and a gradual pickup in investment as capacity utilization improves. SECO expects investment activity to strengthen slightly as firms respond to firmer underlying demand.

Low inflation remains a key support. Consumer prices are forecast to rise just 0.2% in both 2025 and 2026 (down from 0.5%0, helping preserve real incomes and underpin solid private consumption.

Looking further ahead, growth is expected to normalize at 1.7% in 2027 as global conditions improve, though the outlook assumes tariffs remain at current levels and uncertainty around trade policy remains elevated.

Yen Gains Strength Ahead of Crucial Bank of Japan Meeting

The Japanese yen strengthened on Monday, approaching 155 per dollar to reach its highest level in over a week. This appreciation reflects heightened investor anticipation ahead of the Bank of Japan's (BoJ) pivotal monetary policy meeting on Friday.

Markets widely expect the central bank to raise its benchmark interest rate by 25 basis points, bringing it to 0.75%. However, the primary focus will be on the forward guidance provided by Governor Kazuo Ueda in his post-meeting commentary. His remarks will be scrutinized for signals regarding the pace and extent of monetary tightening expected throughout 2025.

Analysts now project the BoJ's policy rate could reach 1.0% by July 2026. This hawkish outlook is underpinned by resilient domestic economic data, particularly consumer inflation, which remains stubbornly above the BoJ's historical targets.

Notably, political resistance to tightening appears to be fading. Prime Minister Sanae Takaichi's administration is unlikely to oppose a rate hike, as the prolonged weakness of the yen - partly a consequence of delayed policy normalization - has exacerbated import costs and contributed to inflationary pressures.

Technical Analysis: USD/JPY

H4 Chart:

On the H4 chart, USD/JPY has completed the first leg of a decline to 154.34, followed by a corrective rebound to 156.93. We now anticipate the development of a new wave of decline targeting 154.73. Following this, the pair is likely to form a consolidation range around this level. A subsequent downward breakout from this range would signal a continuation of the broader downtrend, opening the path towards 152.58. This bearish view is supported by the MACD indicator, whose signal line is positioned below zero and pointing decisively downward.

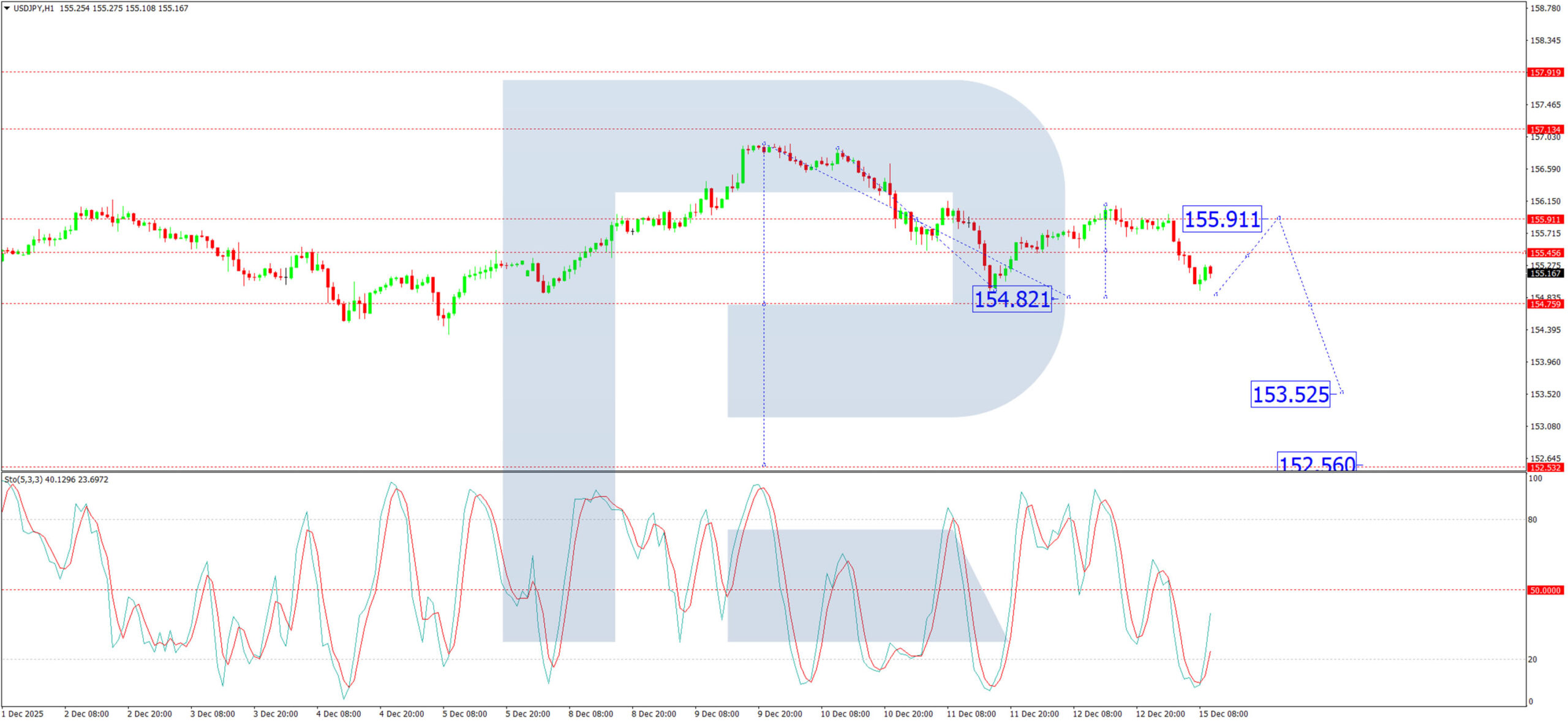

H1 Chart:

On the H1 chart, the pair is forming a declining wave with an immediate target at 154.82. Upon reaching this level, a corrective upward move towards 155.45 is anticipated. A further extension of this correction to 155.91 cannot be ruled out. However, following this relief rally, we expect the primary downtrend to resume, driving the pair lower towards 153.52. The Stochastic Oscillator aligns with this near-term corrective view, as its signal line has turned up from the 20 level and is rising towards 50, indicating that a temporary bounce is likely before selling pressure reasserts itself.

Conclusion

The yen is firming as markets position for a landmark BoJ rate hike and a shift away from its long-held ultra-loose policy stance. Technically, USD/JPY is exhibiting a clear bearish structure across multiple timeframes. While a short-term corrective bounce is possible, the overall trajectory points towards further weakness, with key downside targets at 154.73 on H4 and 153.52 on H1. Governor Ueda's guidance on Friday will be the ultimate determinant of whether this technical correction evolves into a sustained trend reversal.

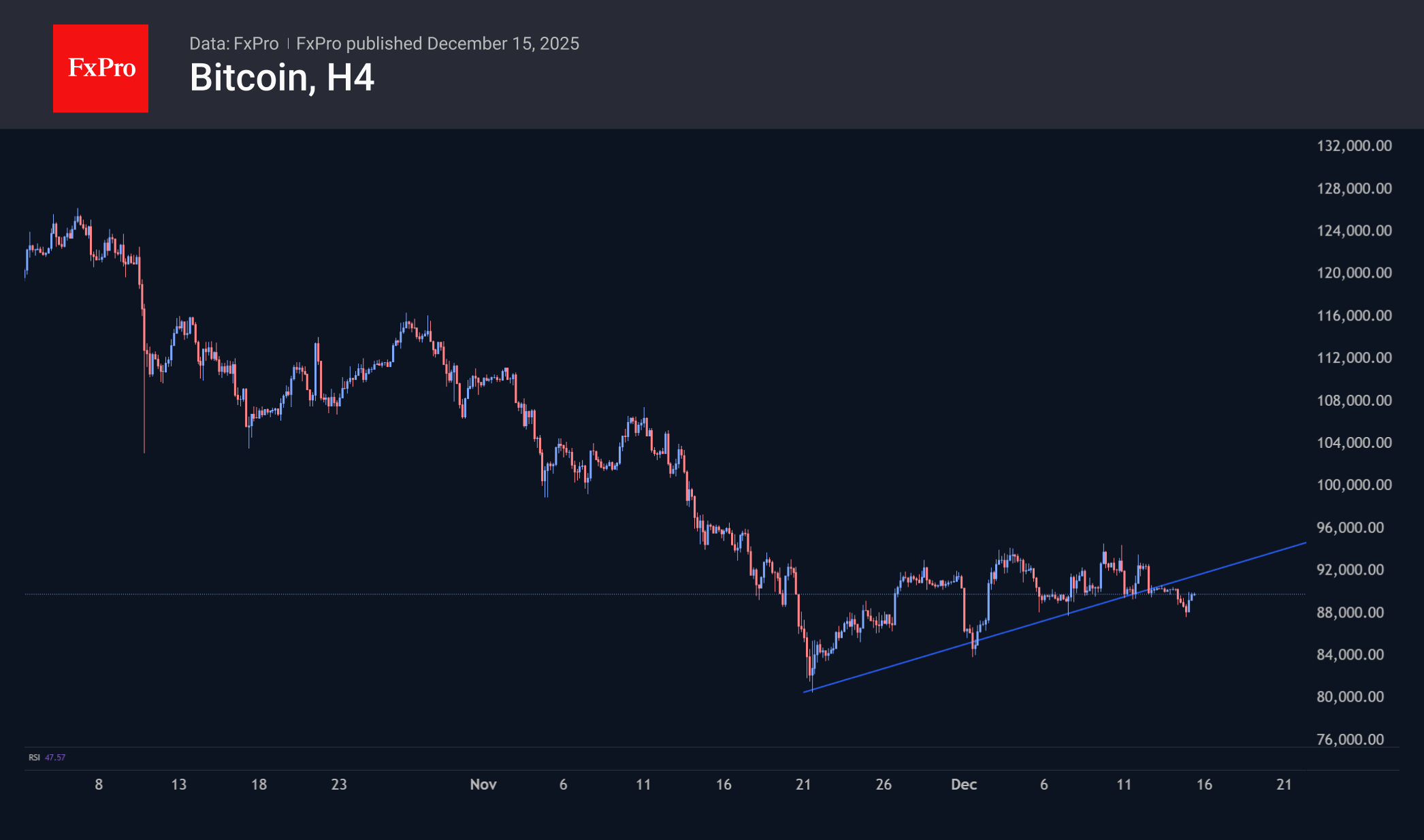

Crypto Market Holds at $3T Amid Broken Uptrend

Market Overview

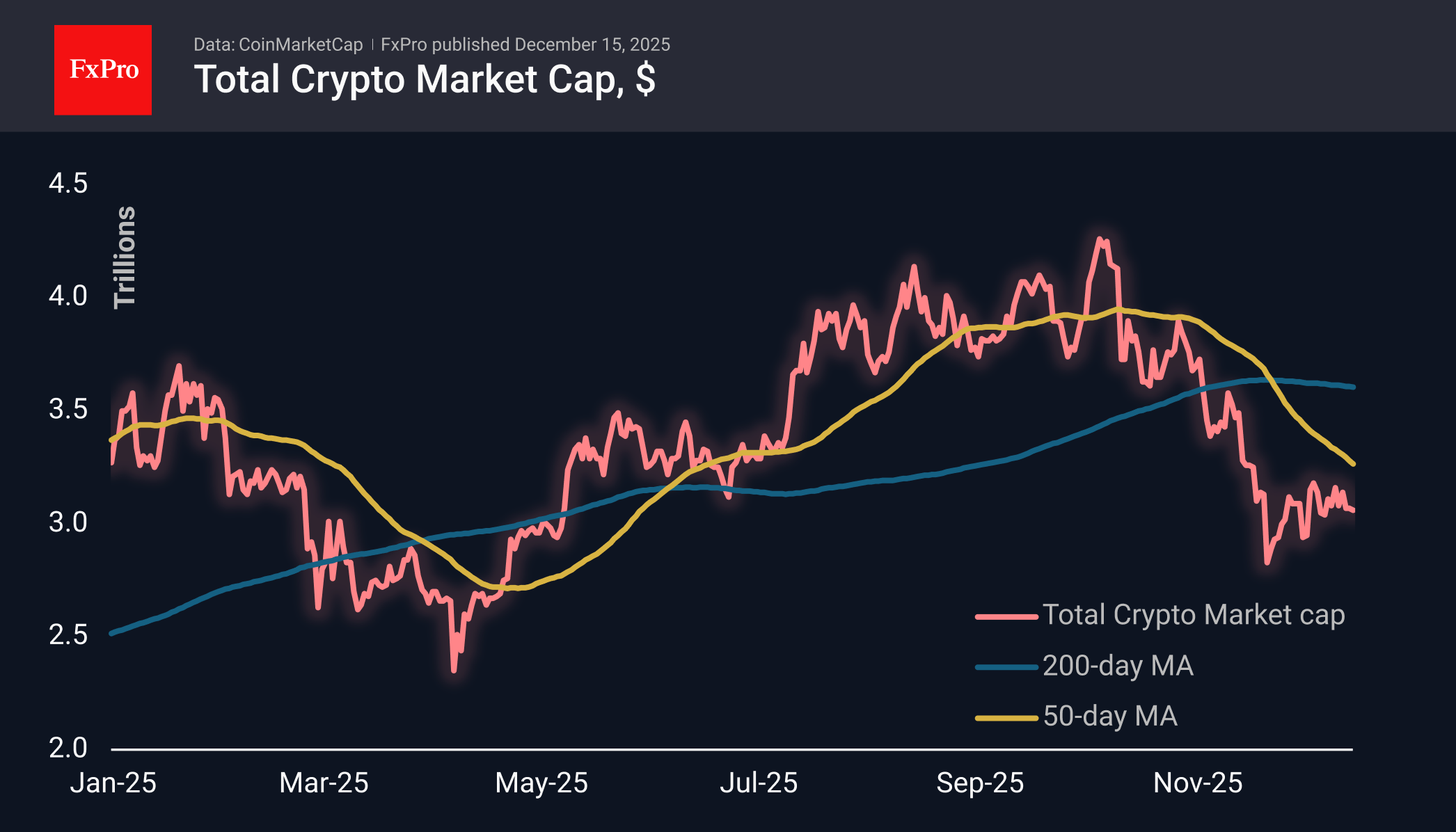

The crypto market capitalisation decreased by 0.2% in 24 hours and 2.2% in a week to $3.06 trillion. Overnight, the market managed to withstand the bears’ test of the $3.0T level, a level below which the bulls have not allowed it to settle for the last 10 days. At the same time, the transition from an upward trend to horizontal support is not the best signal for buyers.

The sentiment index has fallen to 16, its lowest level in almost three weeks. This return is another indication of the cyclical weakness of the crypto market. Without an obvious driver, as was the case in April, the market’s current prolonged stay in extreme fear is reminiscent of what we saw at the end of 2021.

Bitcoin slipped below $87.5K in early trading on Monday but is now recovering to levels close to $90K. Selling pressure since the end of last week has broken the upward trend that had been forming since the end of November. Now, the formal baseline scenario is a return to $81K. However, bulls still have some hope for a more protracted consolidation and subsequent growth, rather than an immediate sell-off.

News Background

According to SoSoValue, net inflows into spot BTC ETFs amounted to $286.6 million, the highest in the last seven weeks. Total inflows since the approval of Bitcoin ETFs in January 2024 have increased to $57.90 billion. Net inflows into spot Ethereum ETFs in the US amounted to $208.9 million for the week, bringing the cumulative net inflows since the ETF’s launch in July 2024 to $12.88 billion. Inflows into the recently launched spot Solana ETFs in the US totalled $36 million for the week, continuing for all seven weeks since their launch, amounting to $675 million. Inflows into the spot XRP ETFs, launched on November 14 in the US, have continued for almost a month and exceeded $974 million.

The total capitalisation of the crypto market has fallen by 15% in 30 days, indicating that it is entering a phase of deep correction, according to Binance Research. December is considered less liquid than other months, and market volatility is likely to increase.

Bitcoin is expected to close the year below the psychological mark of $100,000, according to the majority of users on the Kalshi prediction platform, where the chances of exceeding this mark are only 23%.

Large companies, governments, centralised exchanges and investment funds have concentrated 29.8% of the total volume of bitcoins in free circulation, according to Glassnode’s calculations.

The first cryptocurrency should be viewed more as a speculative collectable than a working asset, according to Vanguard. Bitcoin does not have the properties that provide income, compound interest, and cash flow.

International rating agency Moody’s has published a set of criteria for determining the credit rating of fiat-pegged stablecoins. Some experts believe that Tether’s USDT is in the crosshairs. In November, S&P Global downgraded USDT’s stability rating to the fifth-lowest level.

S&P 500 Index: Chart Analysis After Friday’s Sell-Off

Trading on 12 December was overshadowed by a sharp decline in the S&P 500 (US SPX 500 mini on FXOpen), with the session low approaching December’s previous trough.

Among the key fundamental drivers behind Friday’s drop was the market reaction to Broadcom’s quarterly report. Shares (AVGO) plunged more than 10%, possibly as investors aggressively took profits in tech stocks, concerned that the AI hype may be overheated.

A review of the 4-hour chart of the S&P 500 (US SPX 500 mini on FXOpen) suggests that Friday’s negative sentiment may have begun to ease, as the index is now recovering. Overall, this presents an interesting picture from a price-action perspective.

Technical Analysis of the S&P 500 Chart

Five days ago, we noted that an ascending channel had formed in early December, which could be interpreted as cautious optimism ahead of key news.

However, Fed-related announcements triggered a surge in volatility (as we described, “the calm before the storm”), pushing prices beyond both boundaries of the blue channel:

→ The failure to hold above the upper boundary can be seen as bulls lacking confidence to challenge the all-time high. The false break around 6929 looks like a trader trap.

→ Conversely, bears may have been unable to suppress buying near Friday’s low, as indicated by the long lower wicks on the candles (highlighted by the arrow).

The chart now shows a complex Megaphone pattern (marked A–F).

It is possible that the coming week will be characterised by consolidation following Wednesday–Friday’s swings, with market sentiment increasingly influenced by the approaching holiday period.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

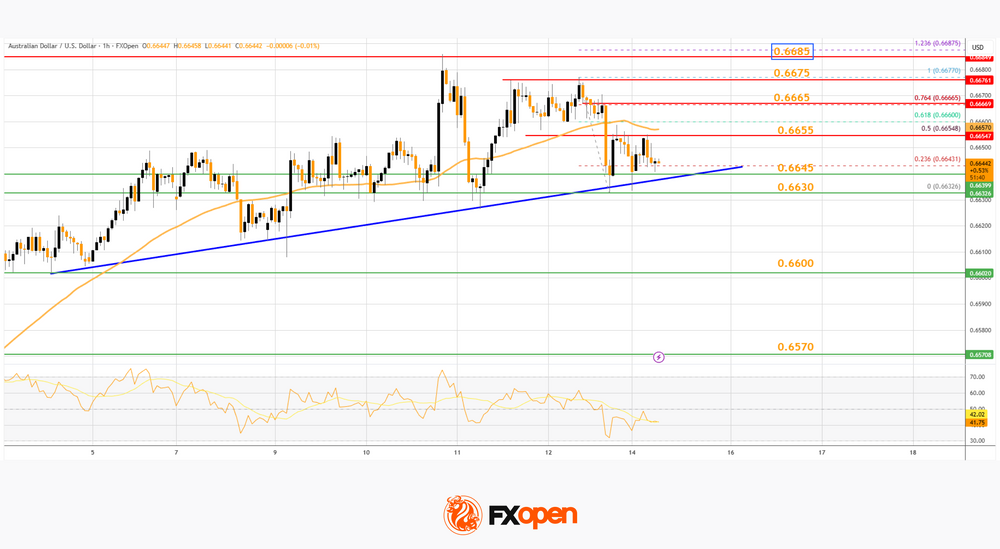

AUD/USD and NZD/USD Test Support, Break or Bounce Next?

AUD/USD is attempting a fresh increase from 0.6630. NZD/USD is consolidating and could aim for a move above 0.5800 in the short term.

Important Takeaways for AUD/USD and NZD/USD Analysis Today

- The Aussie Dollar started a minor pullback from 0.6685 against the US Dollar.

- There is a key bullish trend line forming with support at 0.6645 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD is consolidating above 0.5765 and 0.5755.

- There is a major bullish trend line forming with support at 0.5765 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair formed a base above 0.6600. The Aussie Dollar started a decent increase above 0.6630 against the US Dollar to enter a short-term positive zone.

The pair struggled above 0.6680 and recently corrected some gains. The recent low was formed at 0.6632. The pair is now consolidating and facing resistance near the 50% Fib retracement level of the downward move from the 0.6677 swing high to the 0.6632 low at 0.6655 and the 50-hour simple moving average.

The AUD/USD chart indicates that the pair could struggle to clear the 76.4% Fib retracement at 0.6665. The first major hurdle for the bulls could be 0.6685.

An upside break above 0.6685 resistance might send the pair further higher. The next major target is near the 0.6720 level. Any more gains could clear the path for a move toward 0.6750. If there is no close above 0.6665, the pair might start a fresh decline.

Immediate bid zone could be near the 0.6645 level. There is also a key bullish trend line forming with support at 0.6645. The next area of interest is 0.6630. If there is a downside break below 0.6630, the pair could extend its decline toward 0.6600. Any more losses might signal a move toward 0.6570.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair also followed AUD/USD. The New Zealand Dollar failed to stay above 0.5800 and corrected gains against the US Dollar.

The pair dipped below 0.5790 and the 50-hour simple moving average and 0.5830. A low was formed at 0.5765, and the pair is now consolidating below the 23.6% Fib retracement level of the downward move from the 0.5831 swing high to the 0.5765 low.

The NZD/USD chart suggests that the RSI is below 40, signaling a short-term negative bias. On the upside, the pair is facing resistance near the 50% Fib retracement level at 0.5800.

The next major hurdle for buyers could be 0.5815. A clear move above 0.5815 might even push the pair toward 0.5830. Any more gains might clear the path for a move toward the 0.5880 pivot zone in the coming sessions.

On the downside, there is support forming near the 0.5765 zone and a bullish trend line. If there is a downside break below 0.5765, the pair might slide toward 0.5740. Any more losses could lead NZD/USD into a bearish zone to 0.5710.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

USD/JPY Slides Towards Key Support

A Bank of Japan monetary policy meeting is due this week, and expectations around the decision are supporting the yen today. Traders increasingly believe that the central bank may raise its policy rate by 25 basis points to 0.75%.

Moreover, according to Trading Economics, analysts expect the interest rate to reach 1% by July 2026. Senior officials in Prime Minister Sanae Takaichi’s cabinet are also unlikely to oppose tighter policy, as an excessively weak yen could drive up import costs and fuel inflation.

Technical Analysis of the USD/JPY Chart

The chart shows USD/JPY moving lower today towards the important support level at ¥155 per dollar. Earlier this month, bears attempted to break below this level but failed to gain leading momentum.

Notably, market fluctuations since October have formed an ascending channel. Within this framework:

→ the channel median has twice acted as resistance, a bearish signal;

→ the price is currently near the lower boundary of the channel, which may serve as strong support.

Given these factors, it is reasonable to assume that expectations of tighter monetary policy could lead to a break below the combined support formed by the lower channel boundary and the key 155.00 level. If this occurs, the area could turn into resistance, opening the way for USD/JPY to move towards the next major support near ¥150 per dollar.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

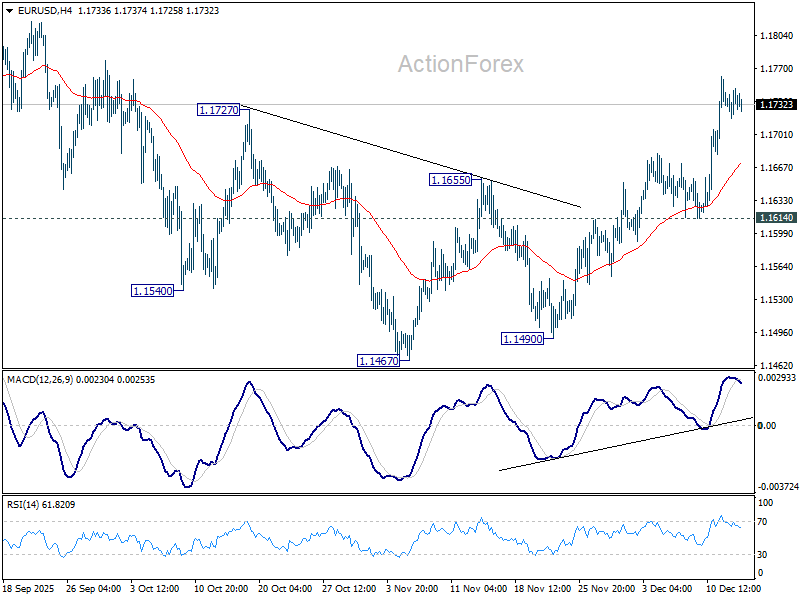

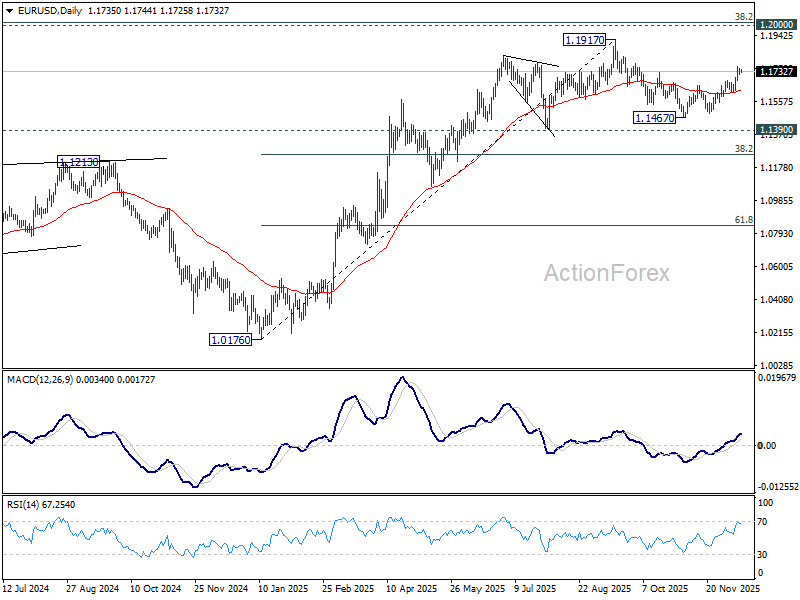

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1723; (P) 1.1737; (R1) 1.1753; More….

Intraday bias in EUR/USD remains mildly on the upside for the moment. Further rise should be seen to retest 1.1917 high. Decisive break there will resume larger up trend. For now, risk will stay on the upside as long as 1.1614 support holds, in case of retreat.

In the bigger picture, as long as 55 W EMA (now at 1.1373) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

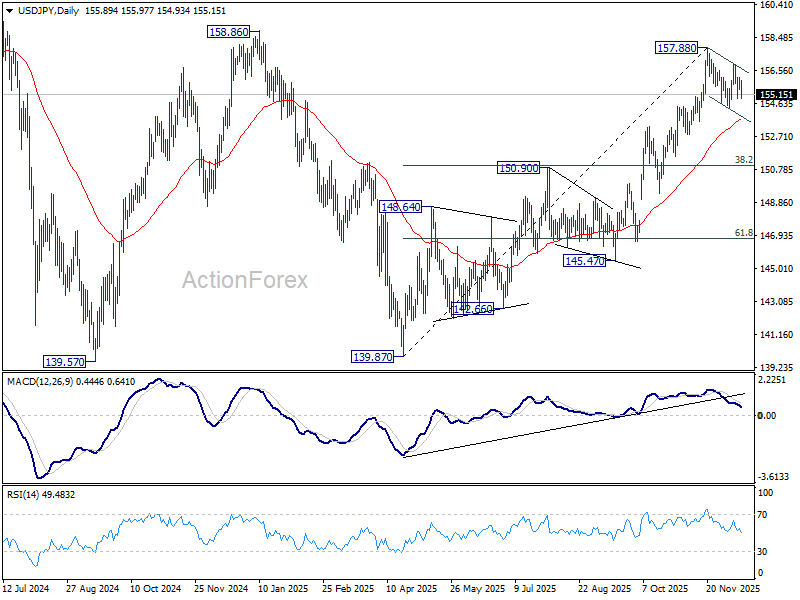

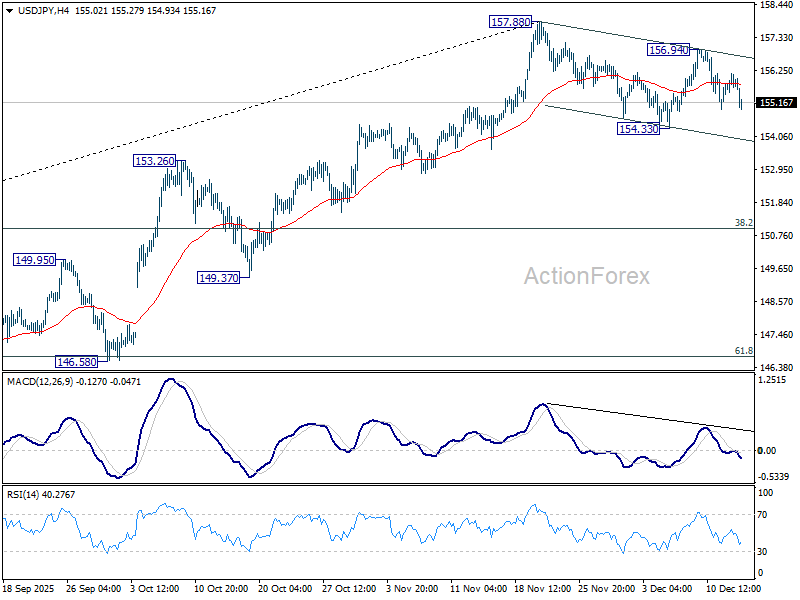

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.47; (P) 155.80; (R1) 156.15; More...

Intraday bias in USD/JPY stays neutral as consolidations from 157.88 is in progress. On the downside, break of 154.33 will target 55 D EMA (now at 153.66) and possibly below. On the upside, above 156.94 will bring retest of 157.88. Firm break there will resume whole rally from 139.87 to 158.85 key structural resistance.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.