Sample Category Title

Taking Temperature on Euro Area Credit Growth

In focus today

In the euro area, focus turns to data on credit growth for October. Loan growth to non-financial corporations increased to 2.1% y/y in September but the momentum has lowered recently in a signal of a smaller boost to economic activity.

In Denmark, retail sales for October are released. Our Spending Monitor showed a 0.6% m/m decline in real retail spending in October. We expect the figures from Statistics Denmark to reflect the same trend in October.

In Sweden we have the NIER release, where confidence indicators and price plans will be important for evaluating the economic recovery in Sweden. We anticipate a gradual improvement in today's data. Aside from the growth indicators, we will also pay attention to firms' pricing and employment plans.

Half an hour later, the Swedish National Debt Office will present an updated forecast and borrowing plan, where we expect an upward revision of the borrowing requirement by SEK 70-80bn for next year.

Overnight, a big batch of Japanese data is released. We highlight the November Tokyo inflation and October retail sales. Price pressures have increased again recently as inflation hovers around 3%, although for the wrong reasons. High food prices and a weak yen is driving inflation instead of consumer demand.

Economic and market news

What happened overnight

In China, industrial profit growth for October dipped into the red with a reading of -5.5% y/y. The reading followed strong gains in the late summer with +21.6% y/y in September. The decline was due to low domestic demand and exports, which were hit by US tariff threats.

What happened yesterday

In the UK, the Autumn Budget was announced. In a surprise turn of events, the Office for Budget Responsibility (OBR) report was leaked before Chancellor Reeves could present the budget. The budget raised tax rates to post war highs, with the Chancellor asking "ordinary people to pay a little bit more". A GBP22bn fiscal headroom provides a bigger buffer against future excess debt issuance than consensus expectations for GBP15bn and the budget delivered less near-term fiscal tightening than expected. The GBP strengthened on the release. The absence of VAT hikes paves the way for more near-term easing from the BoE, and markets are now pricing above 90% chance of an interest rate cut at the BoE December meeting.

In Norway, mainland GDP up 0.1% q/q in Q3 (cons: 0.2%). The details were mixed after the strong pick-up in H1, with continued solid growth in private consumption and mainland exports. Meanwhile, residential investments were flat, mainland investments were down, oil-investments and public demand were also down. Hence, growth is somewhat lower than Norges Bank's estimate from the September MPR of 0.4%, which in isolation should contribute to a downward adjustment of the rate path at the December meeting. The figures are far from weak enough to trigger a December cut but could open the door for a cut in March.

Equities: Equities rose for a fourth consecutive session on Wednesday. The S&P 500 gained 0.7% and Stoxx 600 advanced 1.1%. This was not a classic "risk-on" session, as gains were evenly distributed across both cyclical and defensive sectors. Instead, it appeared as a broad catch-up session, with most sectors moving higher and an unusual mix of materials, utilities, and technology leading the advance. Within tech, the "Google competition" trade reversed, with recent AI laggards (Nvidia, Oracle) outperforming recent winners (Alphabet).

Implied market volatility has already concluded that the selloff is over, with the VIX sliding again yesterday, approaching its 10-year median. Equity market has a little more to go with S&P 500 roughly 1% below the peak, Nordic markets 2% below while Europe is only decimals away from October highs.

FI and FX: The USD weakened modestly overnight vs rest of G10 with EUR/USD at the 1.16 mark and equities continued their advance, seemingly driven by Fed cut expectations. Fed futures continue to price in a c. 80% probability for a December cut. US10y dropped below 4.0% for the first time since late October. MSCI ACWI rose for the fifth straight session. Tech stocks led the rally in the US where SPX rose 0.7% ahead of Thanksgiving. Asia is in green, and futures indicates a positive opening today. EUR/SEK and EUR/NOK remain stable around 11.00 and 11.80, respectively. Today, the SNDO presents an updated forecast and borrowing plan for 2026-2027.

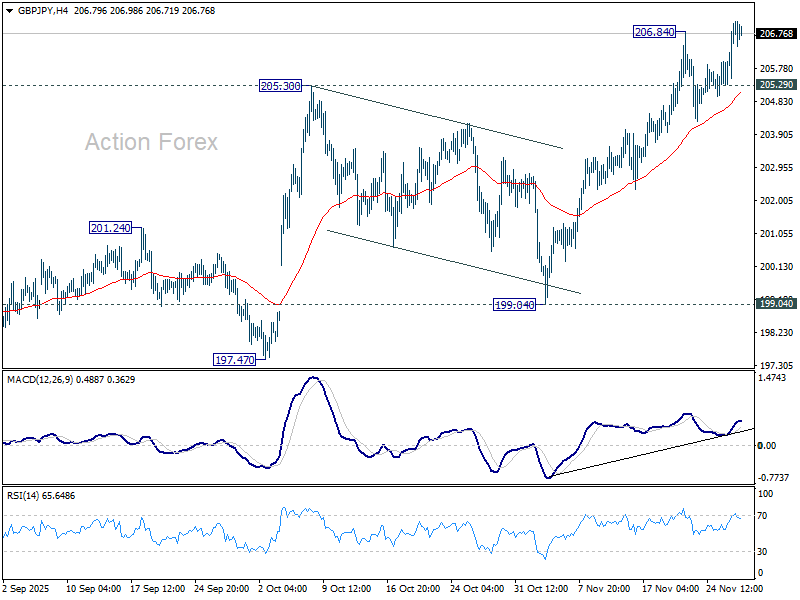

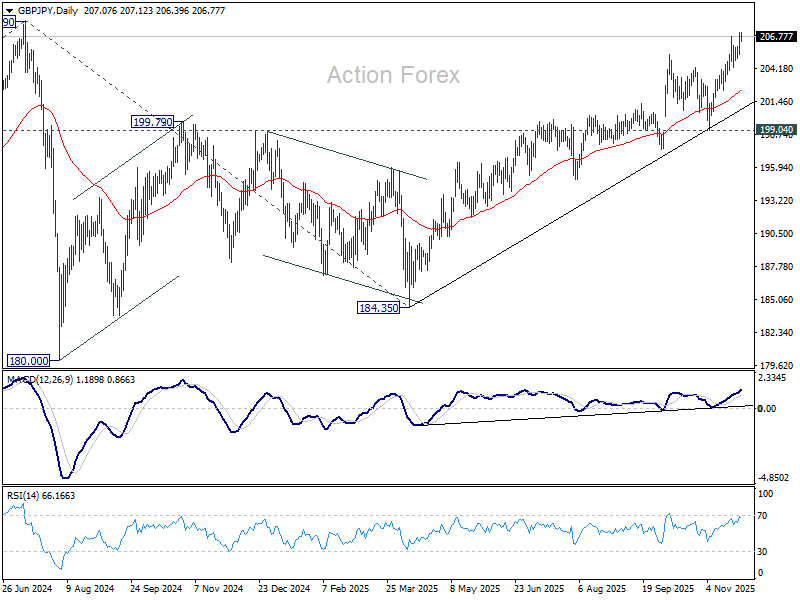

GBP/JPY Daily Outlook

Daily Pivots: (S1) 205.92; (P) 206.56; (R1) 207.85; More...

Intraday bias in GBP/JPY is back on the upside with break of 206.84 temporary top. Current rally from 184.35 should target a retest on 208.09 high. Firm break there will confirm larger up trend resumption. On the downside, below 205.29 minor support will turn bias neutral again.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 199.04 support will dampen this view and extend the corrective pattern with another fall.

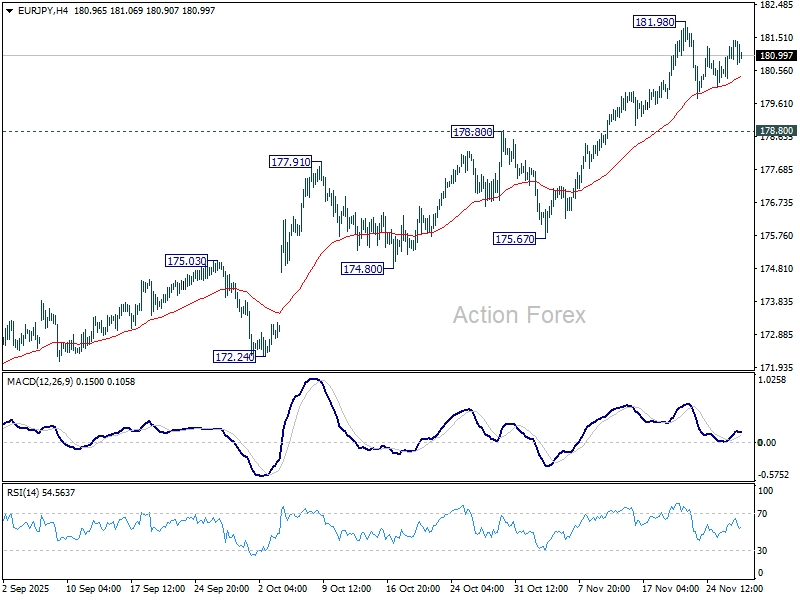

EUR/JPY Daily Outlook

Daily Pivots: (S1) 180.67; (P) 181.07; (R1) 181.84; More...

Intraday bias in EUR/JPY remains neutral and more consolidations could be seen below 181.98. Deeper retreat cannot be ruled out, but downside should be contained by 178.80 resistance turned support to bring another rally. On the upside, break of 181.98 will target 100% projection of 161.06 to 173.87 from 171.09 at 183.90 next. However, firm break of 178.80 will argue that deeper correction is already underway towards 55 D EMA (now at 177.09).

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Outlook will continue to stay bullish as long as 55 W EMA (now at 169.42) holds, even in case of deep pullback.

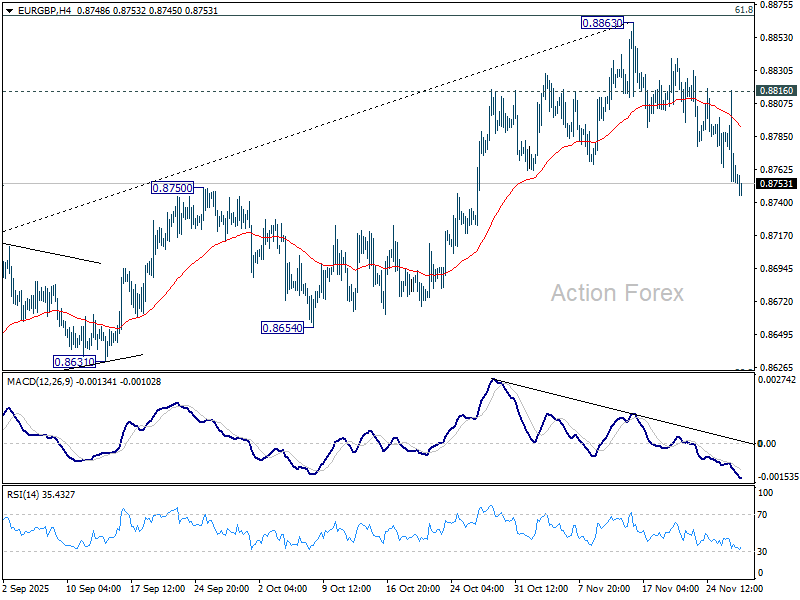

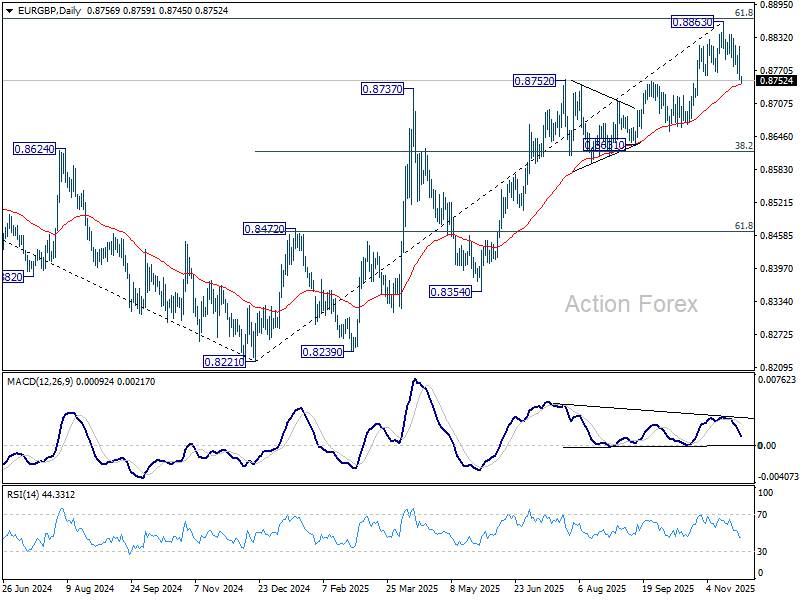

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8735; (P) 0.8777; (R1) 0.8798; More…

Intraday bias in EUR/GBP remains on the downside for the moment. Sustained trading below 55 D EMA (now at 0.8743) will be an early sign of bearish trend reversal. Deeper fall should then be seen to 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618. However, break of 0.8816 minor resistance will bring stronger rebound to retest 0.8863 high instead.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8588) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

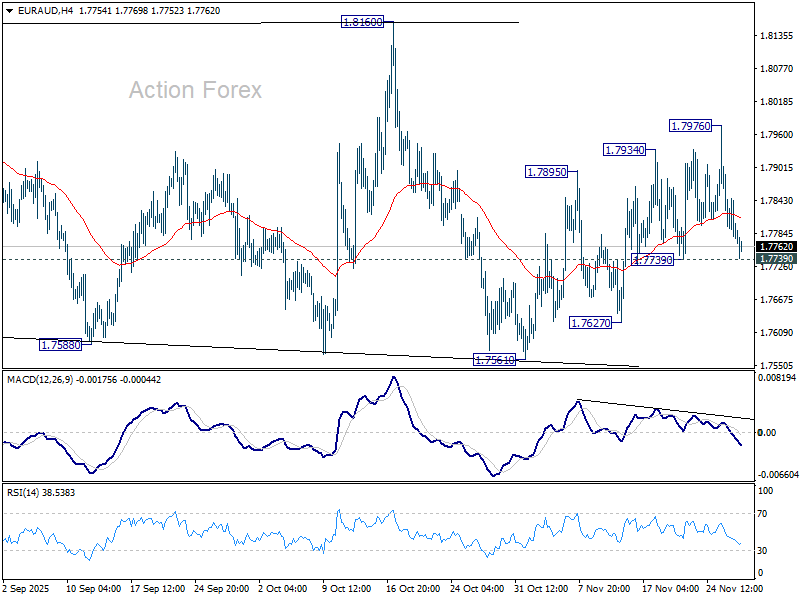

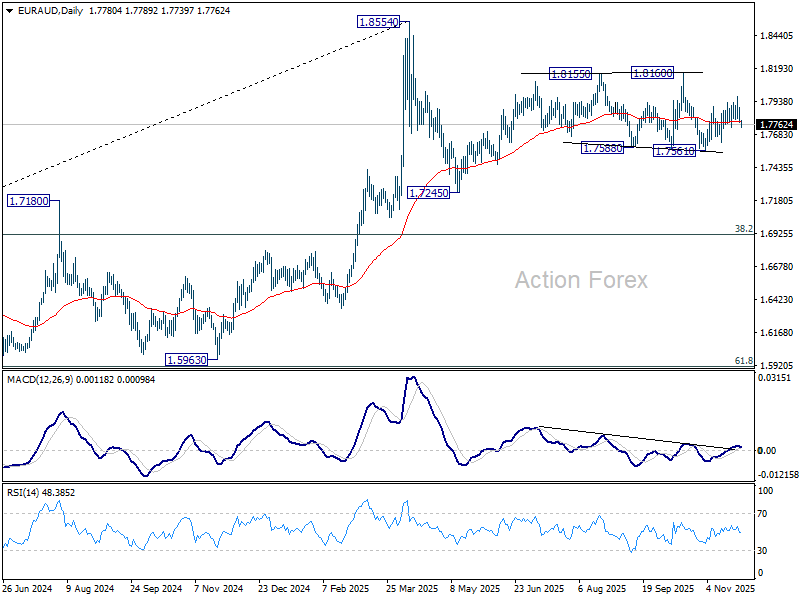

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7750; (P) 1.7823; (R1) 1.7864; More...

Intraday bias in EUR/AUD remains neutral for the moment. On the downside, firm break of 1.7739 support will argue that rebound from 1.7561 has completed, and turn bias back to the downside for this support. On the upside, above 0.7976 will resume the rebound towards 0.8160 resistance.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Sustained break of 55 W EMA (now at 1.7426) will suggest that it's correcting the whole rally from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922. Nevertheless, strong rebound from 55 W EMA will likely bring resumption of the up trend sooner.

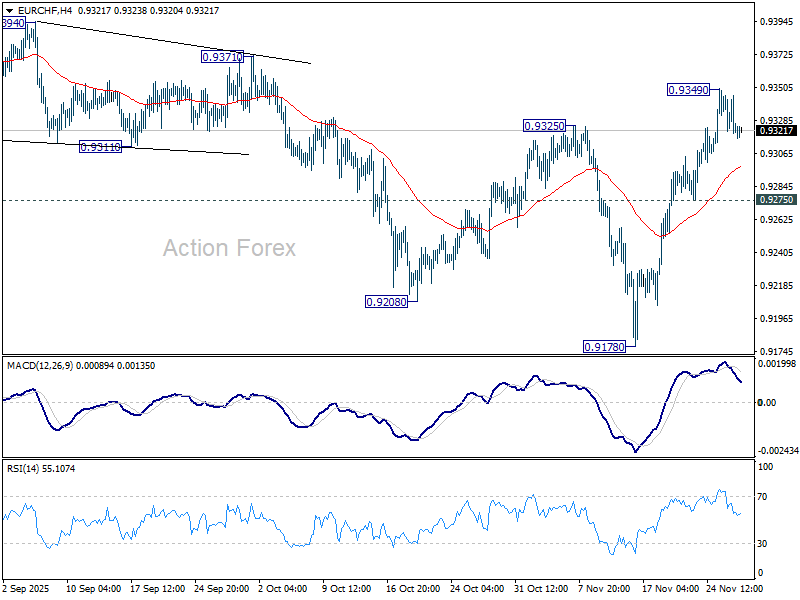

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9316; (P) 0.9331; (R1) 0.9342; More....

Intraday bias in EUR/CHF is turned neutral with current retreat, and some consolidations would be seen below 0.9349. Still, fall from 0.9660 could have completed at 0.9178, on bullish convergence condition in D MACD. Above 0.9349 will target 0.9452 resistance next. However, break of 0.9275 will turn bias back to the downside for 0.9178 low instead.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9377). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish in case of strong rebound.

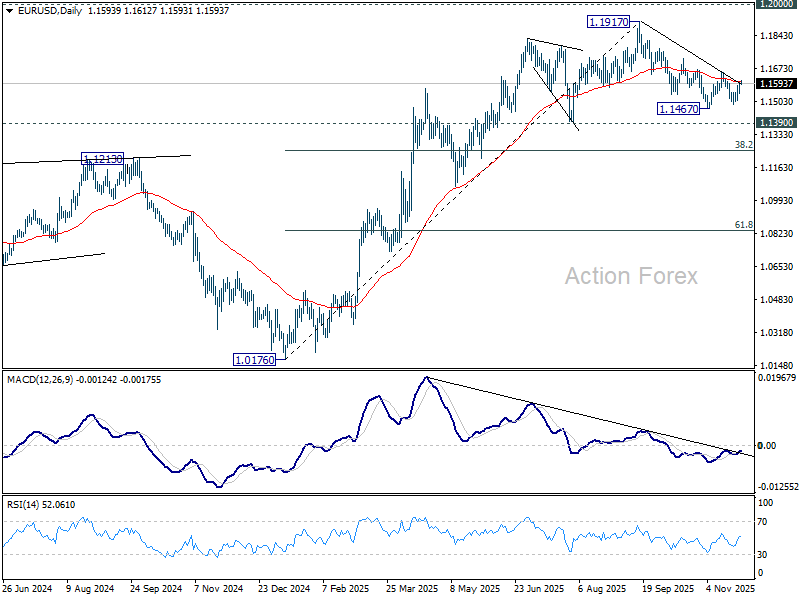

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1563; (P) 1.1582; (R1) 1.1617; More…

No change in EUR/USD's outlook as sideway trading continues. Intraday bias remains neutral. Further decline is expected with 1.1655 resistance intact. On the downside, below 1.1490 and 1.1467 will resume the whole decline from 1.1917 high. Next targets are 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

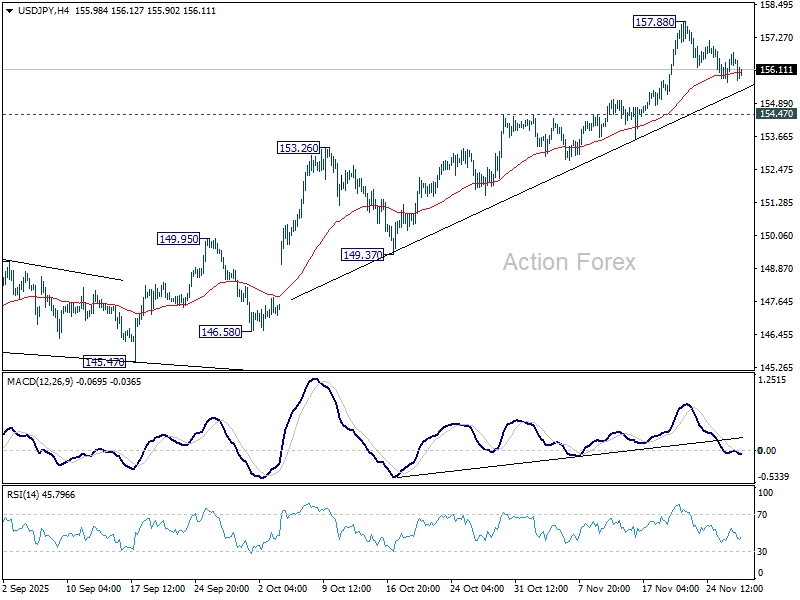

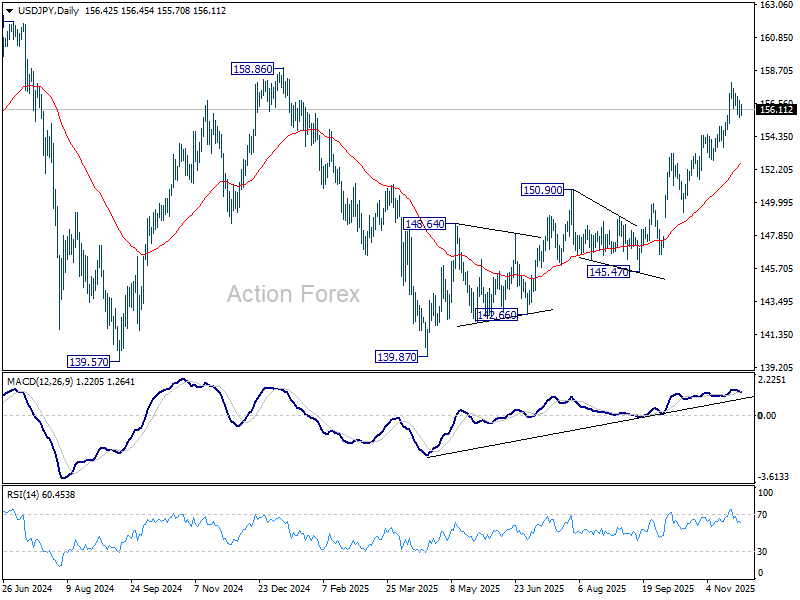

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.82; (P) 156.28; (R1) 156.91; More...

Intraday bias in USD/JPY remains neutral and more consolidations could be seen below 157.88. Downside should be contained by 154.47 resistance turned support. On the upside, break of 157.88 will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

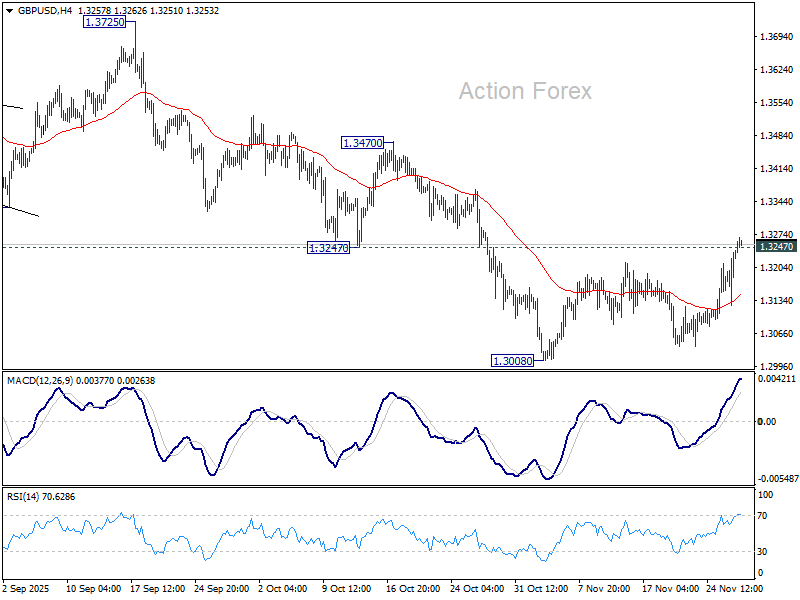

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3162; (P) 1.3204; (R1) 1.3282; More...

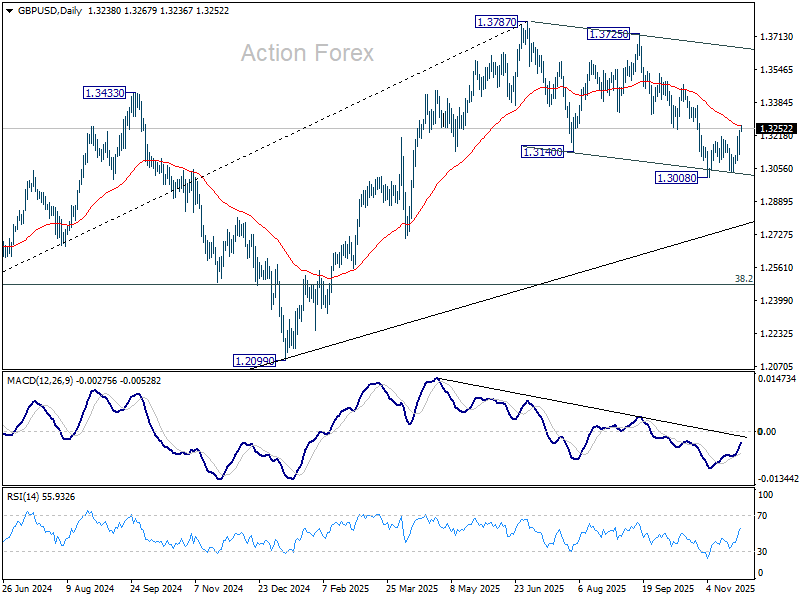

GBP/USD's break of 1.3247 support turned resistance suggests that fall from 1.3787 has completed as a three-wave correction at 1.3008. Intraday bias is back on the upside. Sustained break above 55 D EMA (now at 1.3268) should confirm and target a retest on 1.3725/3787 resistance zone. For now, risk will remain on the upside as long as 1.3008 support holds, in case of retreat.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

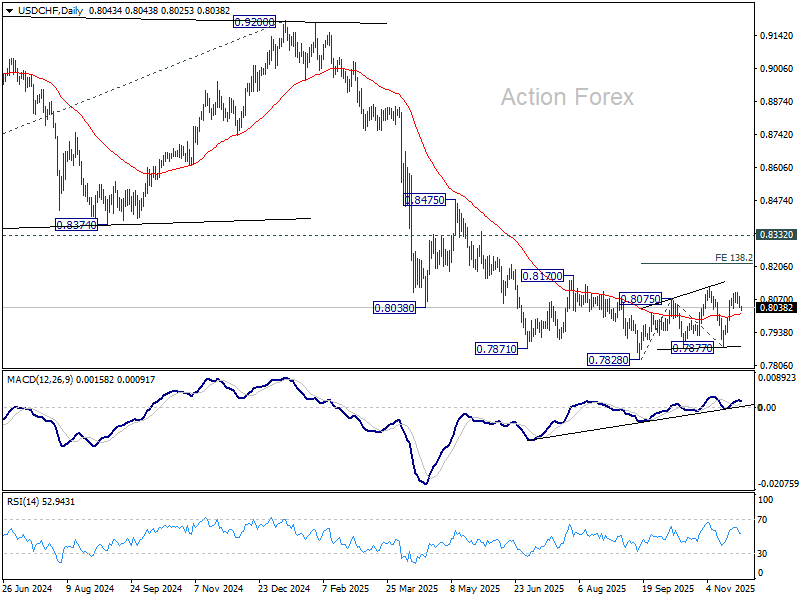

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8027; (P) 0.8055; (R1) 0.8072; More…

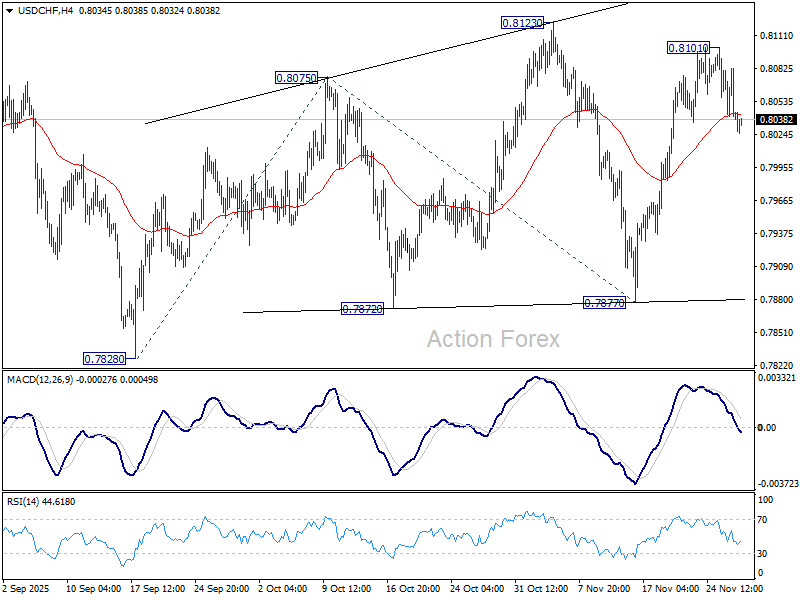

Intraday bias in USD/CHF remains neutral for the moment. No change in the outlook that current rise from 0.7877 is still seen as the third leg of the corrective pattern from 0.7828 low. Above 0.8101 will target 0.8123 resistance, and then 138.2% projection of 0.7828 to 0.8075 from 0.7877 at 0.8218. However, sustained break of 55 D EMA (now at 0.8012) will bring deeper fall back to 0.7877 support instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).