Sample Category Title

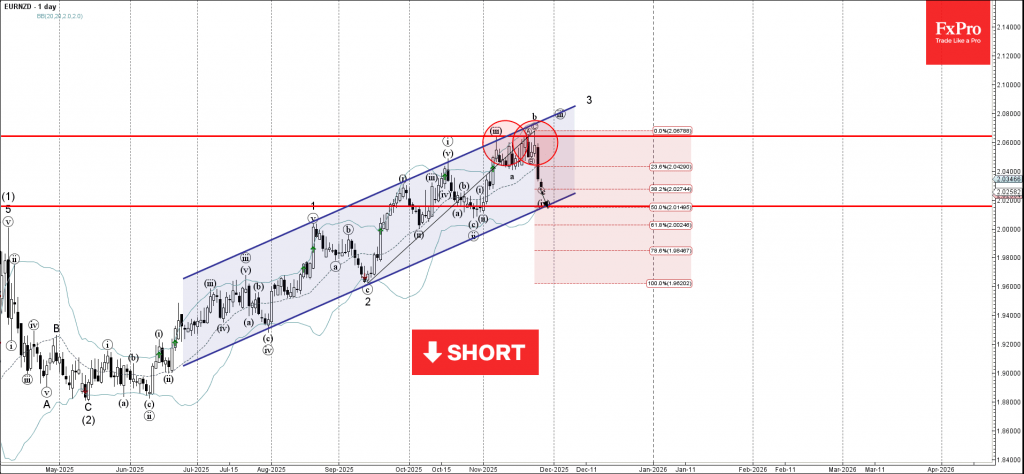

EURNZD Wave Analysis

EURNZD: ⬇️ Sell

- EURNZD reversed from resistance area

- Likely to fall to support level 2.015

EURNZD currency pair recently reversed from resistance area between the key resistance level 2.065 (which stopped the previous minor impulse wave iii), upper daily Bollinger Band and the resistance trendline of the daily up channel from June.

The downward reversal from this resistance area started the active short-term correction iv.

Given the strength of the resistance level 2.065 and the bearish US dollar sentiment seen today, EURNZD can be expected to fall to the next support level 2.015 (target price for the completion of the active correction iv).

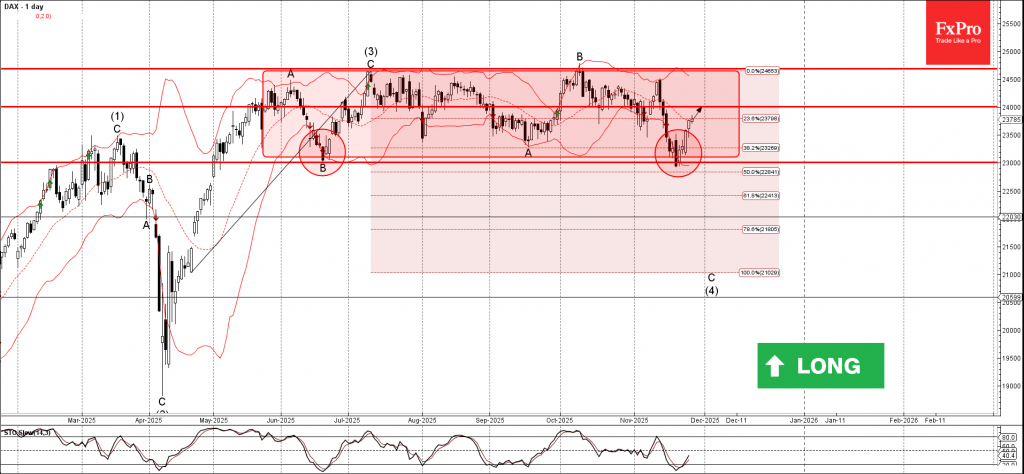

DAX Wave Analysis

DAX: ⬆️ Buy

- DAX reversed from support area

- Likely to rise to resistance level 24000.00

DAX index recently reversed from support area between the support level 23000.00 (lower border of the sideways price range inside which the price has been moving from June) and the lower daily Bollinger Band.

The upward reversal from this support area stopped the previous minor impulse wave C of the intermediate ABC correction (4) from July.

Given the clear daily uptrend, DAX index can be expected to rise to the next resistance level 24000.00.

Sunset Market Commentary

Markets

Global markets developed as one could expect with US markets closed for Thanksgiving. A lack of guidance from US markets and too little ‘new news’ on this side of the Atlantic resulted in technical, order-driven trading. Minutes of the October 29-30 ECB policy meeting didn’t bring much directional insights. The ECB looks very happy to hold on to a status quo scenario. Minor short-term shocks/surprises, if they were to occur, probably won’t steer the policy rate away from the 2% equilibrium level. Inflation has moved close to 2%. A technical dip is possible in 2026, but inflation is expected to stay close to target over the policy horizon. On activity, the ECB assesses that the economy continues to grow despite the challenging global environment. The robust labour market, solid private sector balance sheets and past interest rate cuts are mentioned as sources of resilience. Even a rather elevated level of uncertainty “justifies keeping interest rates unchanged. Maintaining policy rates at their current levels would allow for more information to become available”. “The current level of policy rates should be seen as sufficiently robust for managing shocks, in view of the two-sided inflation risks and taking into account a broad range of possible scenarios”. As said, the bar to deviate from the current 2% level remains (very) high. EMU/German yields understandably are going nowhere, changing 1 bp or less across the curve. After this week’s rebound, European equites held on to recent gains, but without US guidance, momentum dwindled (Eurostoxx 50 perfectly unchanged). Similar story on FX, EUR/USD yesterday/this morning tried a test of the 1.16 big figure, but in the end the status quo. (EUR/USD 1.159) was unavoidable. In the UK, there was also no ‘new news’, but investors had time to give a second look at yesterday’s UK budget announcement. This second opinion at least doesn’t lead to follow-through market enthusiasm. Yesterday’s easing in UK risk premia already came to a standstill. The higher budgetary buffer provides some breathing space, but doesn’t profoundly improve the overall picture, as illustrated by the decline in trend growth from the OBR. UK yields add 1.5-3.5 bps across the curve. It will be interesting to see first comments from the BoE post-budget. A softer inflation due to some subsidies/price caps shouldn’t change the BoE’s LT view on the neutral policy rate, but helps the short term narrative to err on the dovish side. Sterling also runs into resistance after yesterday’s rebound. At EUR/GBP 0.876, the pair still struggles to clear first minor support (uptrend line since June).

News & Views

Belgian headline inflation accelerated from 0.36% M/M in October to 0.56% M/M in November. The most significant price increases last month were registered for travels abroad and city trips (+11.7%), domestic appliances and repairs (+9.1%), motor fuels (+1.9%), information processing equipment (+14.6%), electricity (+1.4%), smartphones (+18.2%) as well as bread and cereals (+0.8%). However, plane tickets (-13.8%), holiday villages (-5%) and natural gas (-0.8%) have had a decreasing effect on the index. Annual inflation increased from 2% to 2.4%, the highest level since April. Core inflation accelerated from 2.58% Y/Y to 3.1% Y/Y. Energy prices fell by 2.15% Y/Y (from -1.85%). Rent inflation was broadly stable at 3.91% Y/Y while food price inflation went up from 2.68% to 3%. Services inflation surged from 3.62% to 4.52%.

The European Commission’s EMU economic confidence indicator remained broadly stable (97 from 96.8) in November. Details showed employment expectations improving, but remaining below the long term average (98.8 vs 100). On a sectoral level, more upbeat confidence in services (broad-based), retail trade (significantly better backward looking view) and construction (employment) was almost entirely offset by lower confidence in industry. Industrial managers’ confidence worsened significantly when it comes to product expectations and the current overall level of order books (both intern & extern). Selling price expectations picked up in all four business sectors, exceeding long-term average in all of them and most so in services. EC consumer confidence was confirmed at -14.2.

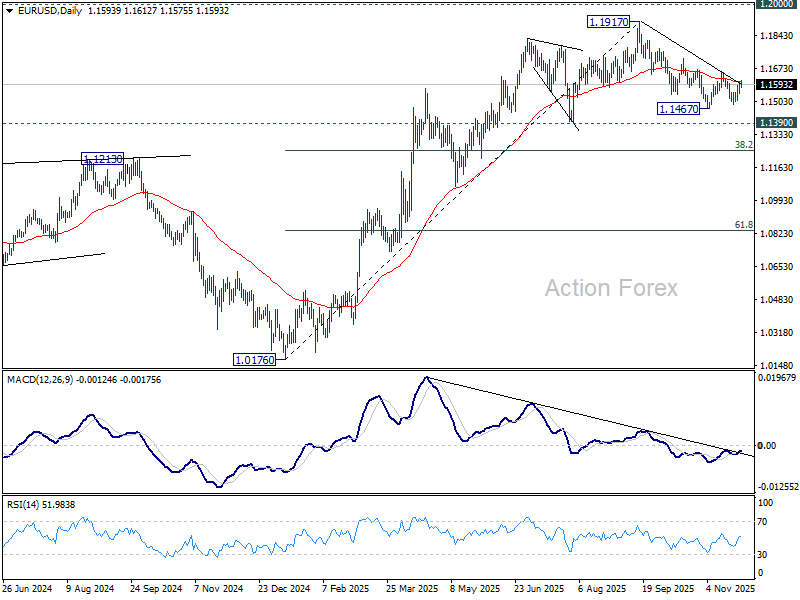

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1563; (P) 1.1582; (R1) 1.1617; More…

Intraday bias in EUR/USD stays neutral as sideway trading continues. Further decline is expected with 1.1655 resistance intact. On the downside, below 1.1490 and 1.1467 will resume the whole decline from 1.1917 high. Next targets are 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

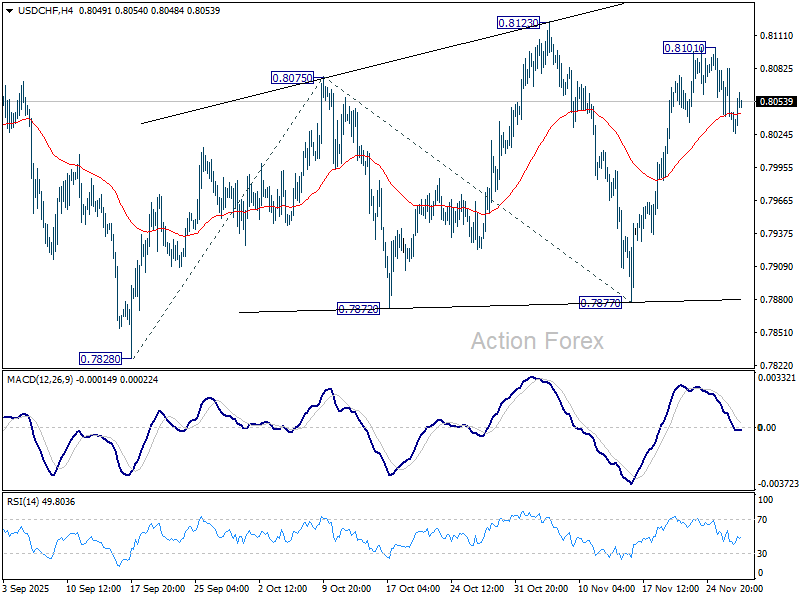

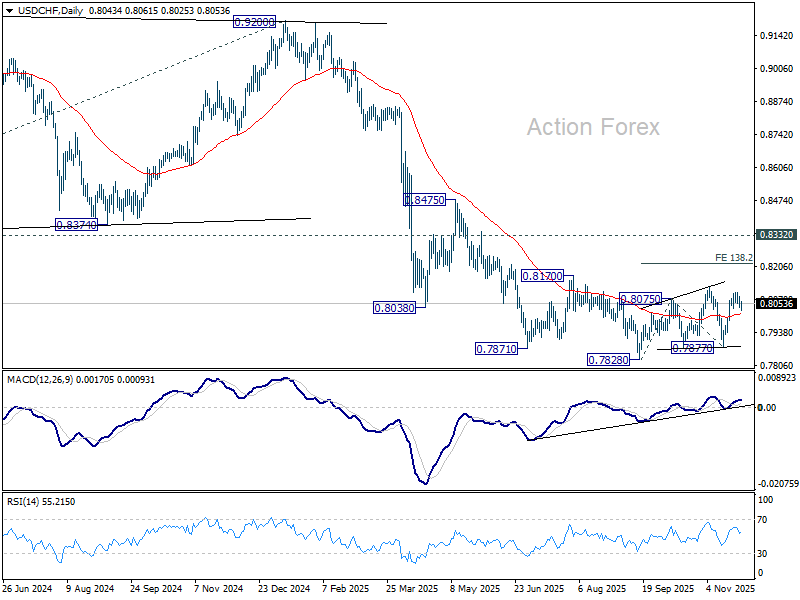

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8027; (P) 0.8055; (R1) 0.8072; More…

Intraday bias in USD/CHF stays neutral at this point. Outlook is unchanged that current rise from 0.7877 is still seen as the third leg of the corrective pattern from 0.7828 low. Above 0.8101 will target 0.8123 resistance, and then 138.2% projection of 0.7828 to 0.8075 from 0.7877 at 0.8218. However, sustained break of 55 D EMA (now at 0.8012) will bring deeper fall back to 0.7877 support instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

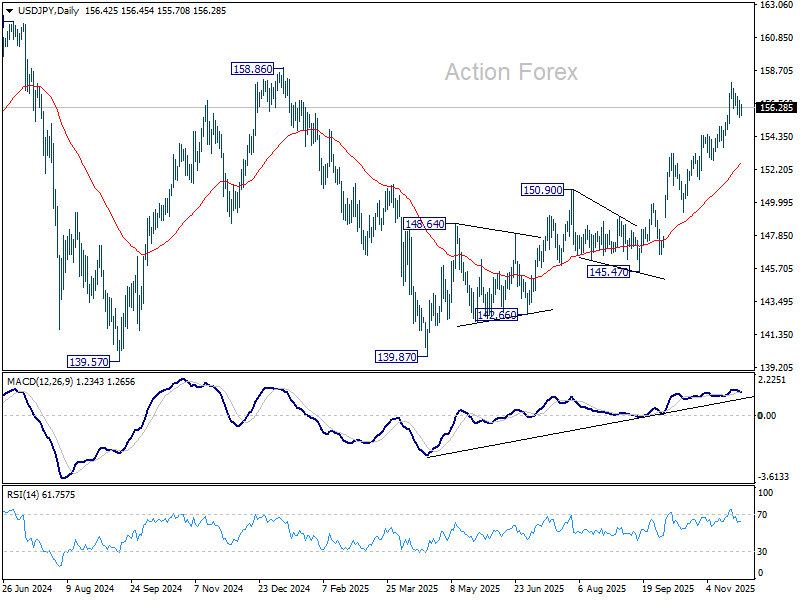

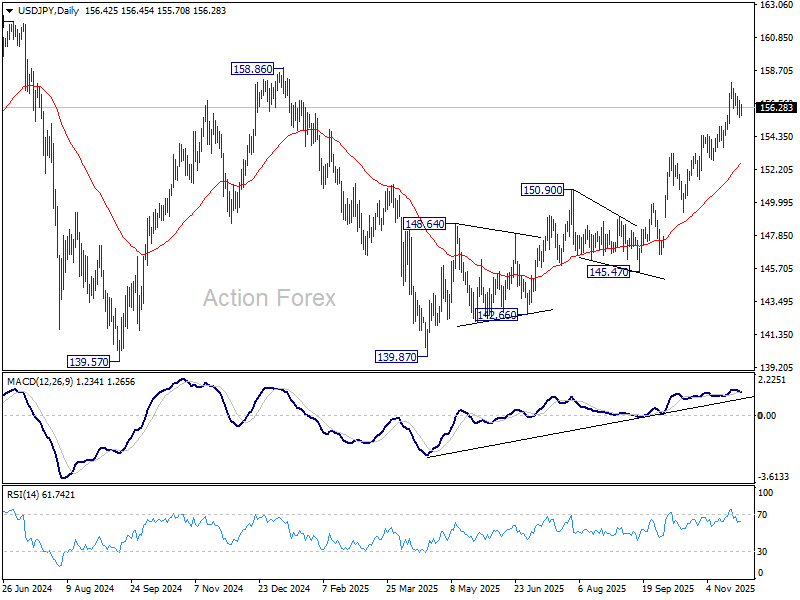

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.82; (P) 156.28; (R1) 156.91; More...

Intraday bias in USD/JPY stays neutral at this point, as consolidation is still in progress. Downside should be contained by 154.47 resistance turned support. On the upside, break of 157.88 will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

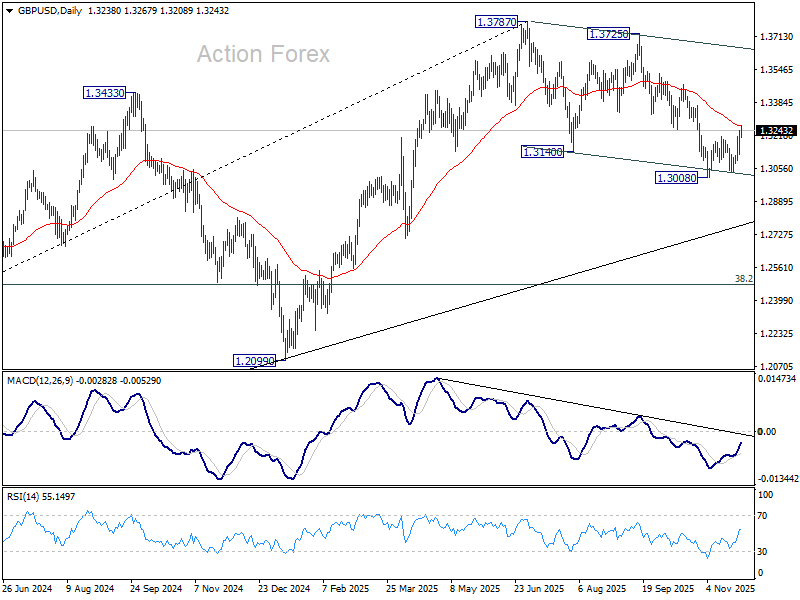

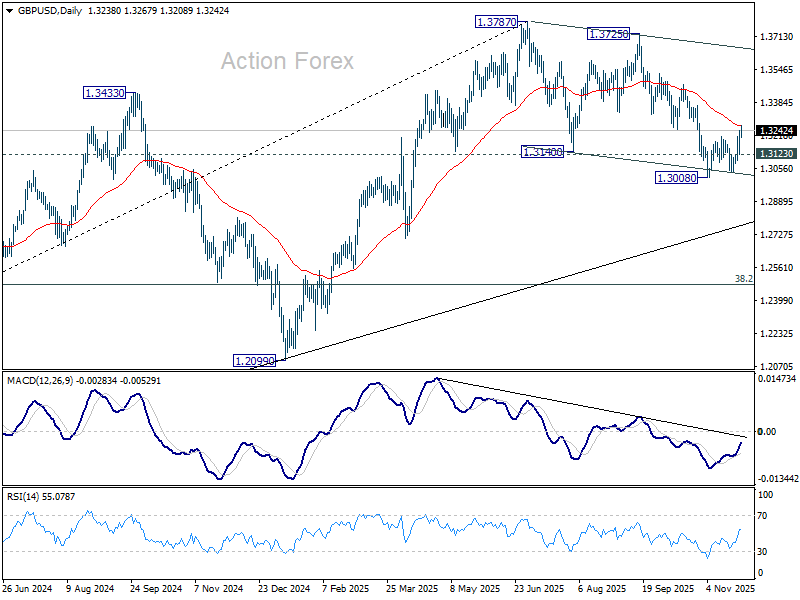

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3162; (P) 1.3204; (R1) 1.3282; More...

Intraday bias in GBP/USD stays mildly on the upside at this point. Corrective fall from 1.3787 could have completed with three waves down to 1.3008. Sustained trading above 55 D EMA (now at 1.3268) should confirm and target a retest on 1.3725/3787 resistance zone. Nevertheless, break of 1.3123 minor support will revive near term bearishness, and bring retest of 1.3008.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

Dollar Stays Soft Into Thanksgiving Lull

Trading turned subdued as markets moved into the U.S. session, with activity expected to slow further as Thanksgiving approaches. Liquidity conditions were already thinning in early trade, and the muted tone across majors reflects a market unwilling to take fresh positions before the long weekend. Despite the quieter backdrop, broader directional themes remain unchanged.

Dollar attempted a modest recovery earlier in the day but lacked momentum, with the prospect of a December Fed rate cut still acting as a cap on any sustained rally. Much of the intraday movement appears to be position-squaring rather than a shift in sentiment, with traders closing shorts and reducing exposure ahead of the holiday. The underlying bias remains tilted against the greenback.

Yen also tried to firm but struggled to gain traction. Falling U.S. yields provides some support, yet these gains are partially offset by expectations that BoJ could hold in December. By contrast, Kiwi and Aussie remain among the stronger performers, supported by both constructive risk sentiment and supportive domestic developments.

For the week so far, Kiwi remains the best performer, with Sterling now overtaking Aussie for second place. Dollar is anchored at the bottom of the pack, followed by Yen and Swiss Franc. Euro and Loonie sit in the middle.

In Europe, at the time of writing, FTSE is down -0.10%. DAX is up 0.26%. CAC is up 0.11%. UK 10-year yield is up 0.036 at 4.464. Germany 10-year yield is up 0.009 at 2.683. Earlier in Asia, Nikkei rose 1.23%. Hong Kong HSI rose 0.07%. China Shanghai SSE rose 0.29%. Singapore Strait Times rose 0.17%. Japan 10-year JGB yield fell -0.017 to 1.802.

ECB accounts show unified hold, but debates on future cut threshold

ECB meeting accounts from October showed unanimous agreement to keep all three key interest rates unchanged, with policymakers noting that both the inflation outlook and incoming activity data had broadly aligned with September’s baseline. The economy was still expanding despite global headwinds, giving the Governing Council confidence that the current stance remained appropriate.

Members highlighted that December will bring critical new information, including a fresh set of staff projections extending to 2028 for the first time. These forecasts will offer a "clearer picture of the outlook at that horizon".

However, the accounts revealed differing views on whether the rate-cutting cycle has fully run its course. Some members argued that the favorable outlook meant that "should not be fine-tuned" in response to "moderate and temporary fluctuations" of inflation.

Others cautioned that the Governing Council must remain “entirely open-minded,” noting that another rate cut could be justified if downside risks intensified or if projected inflation undershoots persisted. That viewpoint stressed that the bar for action should be “no higher than normal”.

Eurozone economic sentiment marks mild gains, but stay below long-term average

EU and Eurozone posted only marginal improvements in sentiment in November, with the Economic Sentiment Indicator rising 0.2 points in both regions to 96.8 and 97.0. While the Employment Expectations Indicator saw a more meaningful lift—up to 98.8 in the EU and 97.8 in the Eurozone. Both gauges remain below their historical averages of 100.

Sector trends again showed uneven dynamics. Services, retail and construction recorded higher confidence. But industry confidence weakened further, nearly cancelling out those gains and keeping the overall ESI flat. Consumer sentiment was little changed,.

Across major EU economies, sentiment gains were led by Spain (2.0), Italy (1.1), France (0.) and Poland (0.5), while Germany and the Netherlands were steady at -0.3.

Noguchi says BoJ can restart hikes gradually as Yen weakness turns problematic

BoJ board member Asahi Noguchi said today that the central bank could resume interest rate hikes once U.S. tariff risks recede, but emphasized that any tightening must "measured, step-by-step".

He warned that maintaining very low real interest rates for too long risks undermining the economy by pushing Yen lower and stoking undesirable inflation. A weaker currency, he said, lifts prices through import costs and boosts exports in a way that can overheat the economy .

Noguchi highlighted that Yen depreciation was once a tailwind during Japan’s deflation era, supporting exporters and helping revive demand. However, "as supply constraints intensify, the positive effects eventually disappear and are replaced by negative effects that merely push inflation higher than needed," he added.

NZ ANZ business confidence jumps to 11 year high, green shoots well established

New Zealand’s ANZ Business Confidence index jumped from 58.1 to 67.1 in November, the strongest reading in 11 years. The survey’s own-activity outlook also surged from 44.6 to 53.1, marking the highest level since 2014 and signaling a material improvement in real economic momentum rather than sentiment alone. ANZ noted that "green shoots are looking well established", with recent gains increasingly rooted in actual activity.

Inflation signals were more mixed. The share of firms planning to raise prices over the next three months climbed from 44% to 51%, the highest since March. However, expected cost increases eased slightly from 76% to 74%, and one-year-ahead inflation expectations were steady at 2.7%. The combination points to stabilizing inflation pressures, but not yet disinflation strong enough to encourage fresh easing from the RBNZ.

ANZ said the underlying improvement in conditions offers reassurance that the pickup is likely to be sustained. With the recovery underway and CPI sitting at the top of the target band, the bank sees little reason for further OCR cuts “barring unexpected developments.”

NZ retail sales surge 1.9% qoq in Q3, strongest since 2021

New Zealand retail sales delivered a strong upside surprise in Q3, rising 1.9% qoq versus expectations of 0.6%. Ex-auto sales also beat forecasts, up 1.2% qoq compared with 0.8% consensus.

Statistics New Zealand said this was the largest quarterly increase in retail activity since late 2021, with broad-based gains across the sector. Most industries recorded growth during the September.

The details showed particularly strong demand in motor vehicles and electrical and electronic goods retailing, which posted the biggest increases. Eight of the 15 retail industries reported higher volumes compared with Q2.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3162; (P) 1.3204; (R1) 1.3282; More...

Intraday bias in GBP/USD stays mildly on the upside at this point. Corrective fall from 1.3787 could have completed with three waves down to 1.3008. Sustained trading above 55 D EMA (now at 1.3268) should confirm and target a retest on 1.3725/3787 resistance zone. Nevertheless, break of 1.3123 minor support will revive near term bearishness, and bring retest of 1.3008.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

ECB accounts show unified hold, but debates on future cut threshold

ECB meeting accounts from October showed unanimous agreement to keep all three key interest rates unchanged, with policymakers noting that both the inflation outlook and incoming activity data had broadly aligned with September’s baseline. The economy was still expanding despite global headwinds, giving the Governing Council confidence that the current stance remained appropriate.

Members highlighted that December will bring critical new information, including a fresh set of staff projections extending to 2028 for the first time. These forecasts will offer a "clearer picture of the outlook at that horizon".

However, the accounts revealed differing views on whether the rate-cutting cycle has fully run its course. Some members argued that the favorable outlook meant that "should not be fine-tuned" in response to "moderate and temporary fluctuations" of inflation.

Others cautioned that the Governing Council must remain “entirely open-minded,” noting that another rate cut could be justified if downside risks intensified or if projected inflation undershoots persisted. That viewpoint stressed that the bar for action should be “no higher than normal”.