Sample Category Title

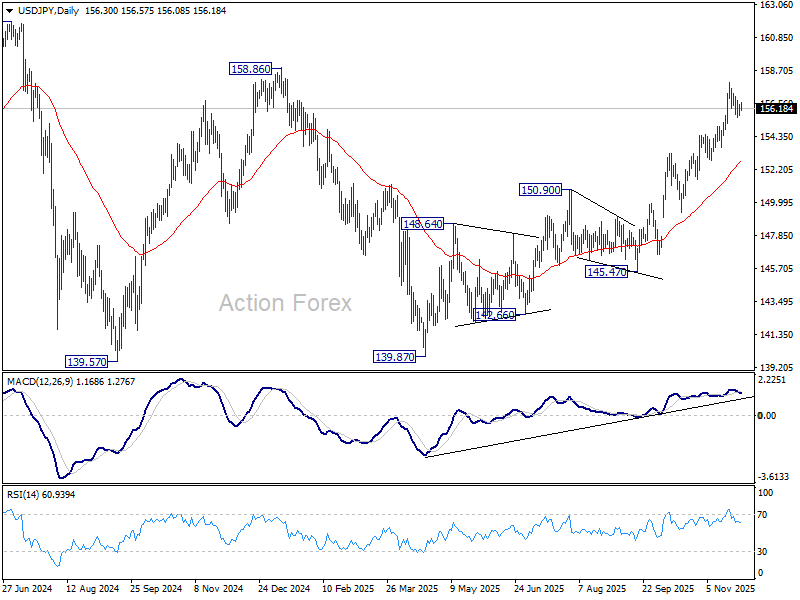

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.85; (P) 156.17; (R1) 156.63; More...

No change in USD/JPY's outlook as consolidations continue below 157.88. Intraday bias stays neutral at this point. Downside should be contained by 154.47 resistance turned support. On the upside, break of 157.88 will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high. However, firm break of 154.47 will bring deeper correction to 55 D EMA (now at 152.63).

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

Bitcoin Stalled at a Critical Resistance

Market Overview

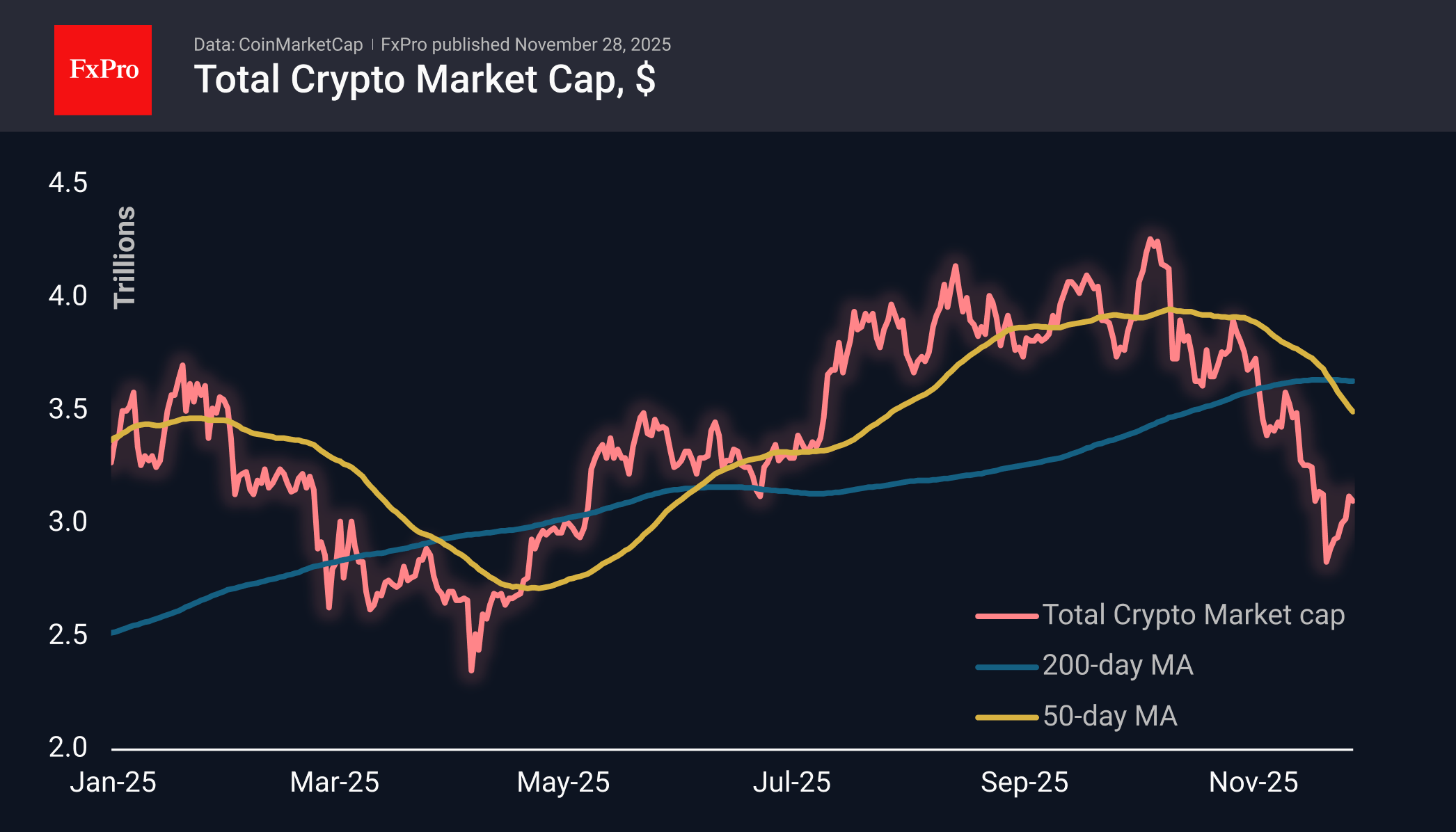

The crypto market cap corrected by 0.4% to $3.10T, pausing the cautious rebound from last Friday. Yet we can’t talk about the rebound running out of steam, as there was strong growth the day before. But we do not see any increase in optimism, as just about one in seven coins has gained in the last 24 hours, compared to a decline for most.

The sentiment index rose to 25, the threshold for exiting the territory of extreme fear, despite the latest round of weakness. The index’s dynamics are likely to attract buyers who were eager to enter the market but were waiting for a discount after the highs were set in early October.

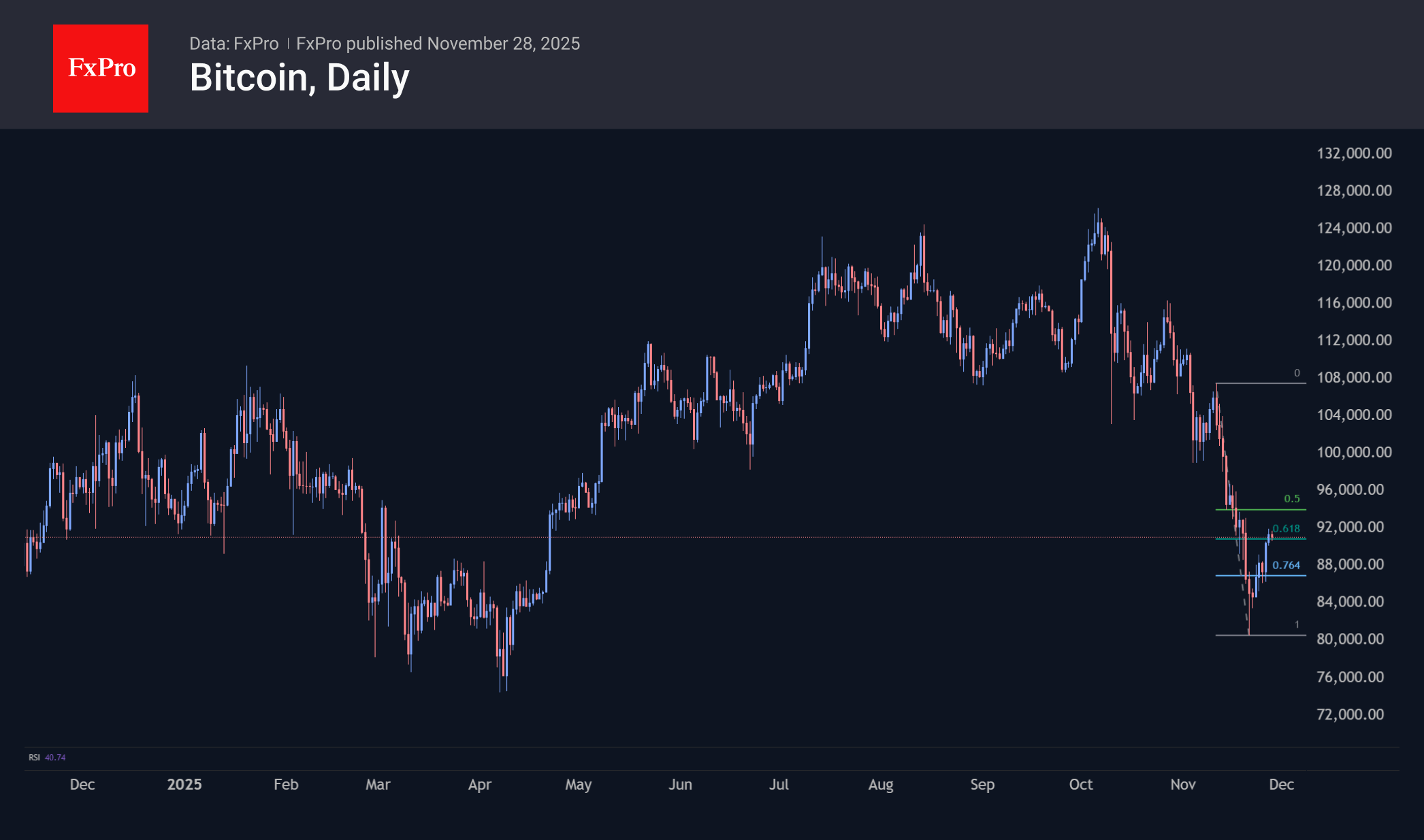

Bitcoin has fallen below $ 91K, stabilising near the 61.8% Fibonacci retracement level of the decline since November 11th. The area near $90K was significant for the market about a year ago, serving as support for the correction after the growth momentum in early November. There is some risk that it will now act as resistance, reinforcing the bearish signal of a possible end to the rebound. A rise above $95K would signal a victory for the bulls and a return to a bull market, while a decline below $87K could open the way to $80K, driving the market into a depression.

News Background

Kronos Research describes the current dynamics as a classic rebound from oversold conditions. The market has cleared out excess long positions, creating room for growth, according to Presto Research.

Futures and options data point to a return of bullish sentiment. The market is ‘ready for growth’ after speculative longs were closed over the past two weeks, according to GSR.

According to CryptoQuant, in November, the Binance crypto exchange increased its stablecoin reserves to a record $51.1 billion. The growth of this indicator can be seen as a positive factor for the crypto market.

The potential exclusion of Strategy from the S&P 500 index and continued outflows from spot crypto ETFs could bring back bearish sentiment and trigger sell-offs, warns QCP Capital.

Bolivia will include cryptocurrencies and stablecoins in its national financial system to modernise it. Cryptocurrencies will be allowed to be used as a means of payment, savings accounts, credit products and loans. The authorities’ decision is a result of the country’s challenging economic situation.

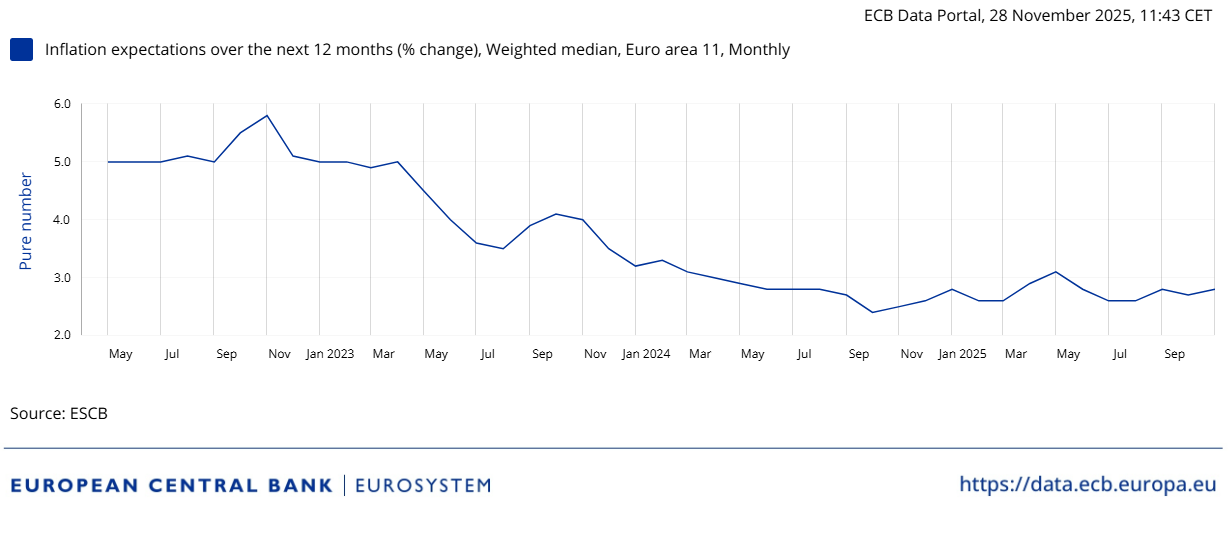

ECB survey shows slight rise in 12-month inflation expectations to 2.8%

The ECB Consumer Expectations Survey for October showed a small uptick in near-term inflation expectations, with the median 12-month outlook rising to 2.8% from 2.7% in September.

Longer-term expectations remained stable, with the three-year horizon unchanged at 2.5% and the five-year measure anchored at 2.2%. Inflation uncertainty was likewise steady, indicating consumers do not see a significant shift in the underlying trend.

On the economic front, consumers grew slightly more optimistic about growth. Expectations for GDP over the next 12 months improved to -1.1%, up from -1.2% previously. However, labor-market expectations worsened. Consumers now expect the unemployment rate to reach 11.0% in 12 months, up from 10.7% in September.

GBP/USD Regains Footing, but Underlying Doubts Persist

The GBP/USD pair is edging higher, trading around 1.3239, following a pause in its five-day rally. While the pair has returned to positive territory, investor focus has shifted to the underlying health of the UK economy and the credibility of the newly announced budget measures.

The fundamental headwinds for sterling remain significant. Weak growth prospects, stubbornly low productivity, and persistent inflationary pressures continue to cap the currency's long-term potential.

The UK government bond market experienced a short-lived rally after Chancellor Rachel Reeves unveiled a larger-than-expected fiscal reserve and reaffirmed her commitment to strict spending control. Thirty-year gilt yields initially fell by over 10 basis points but subsequently pared these losses.

A key concern for investors is the government's fiscal trajectory. By postponing most of its proposed tax measures until after 2029 – beyond the current parliamentary cycle – the government has raised questions about its fiscal credibility. This long-dated approach leaves the pound vulnerable to future weakness, as the necessary budgetary tightening remains a distant and uncertain prospect.

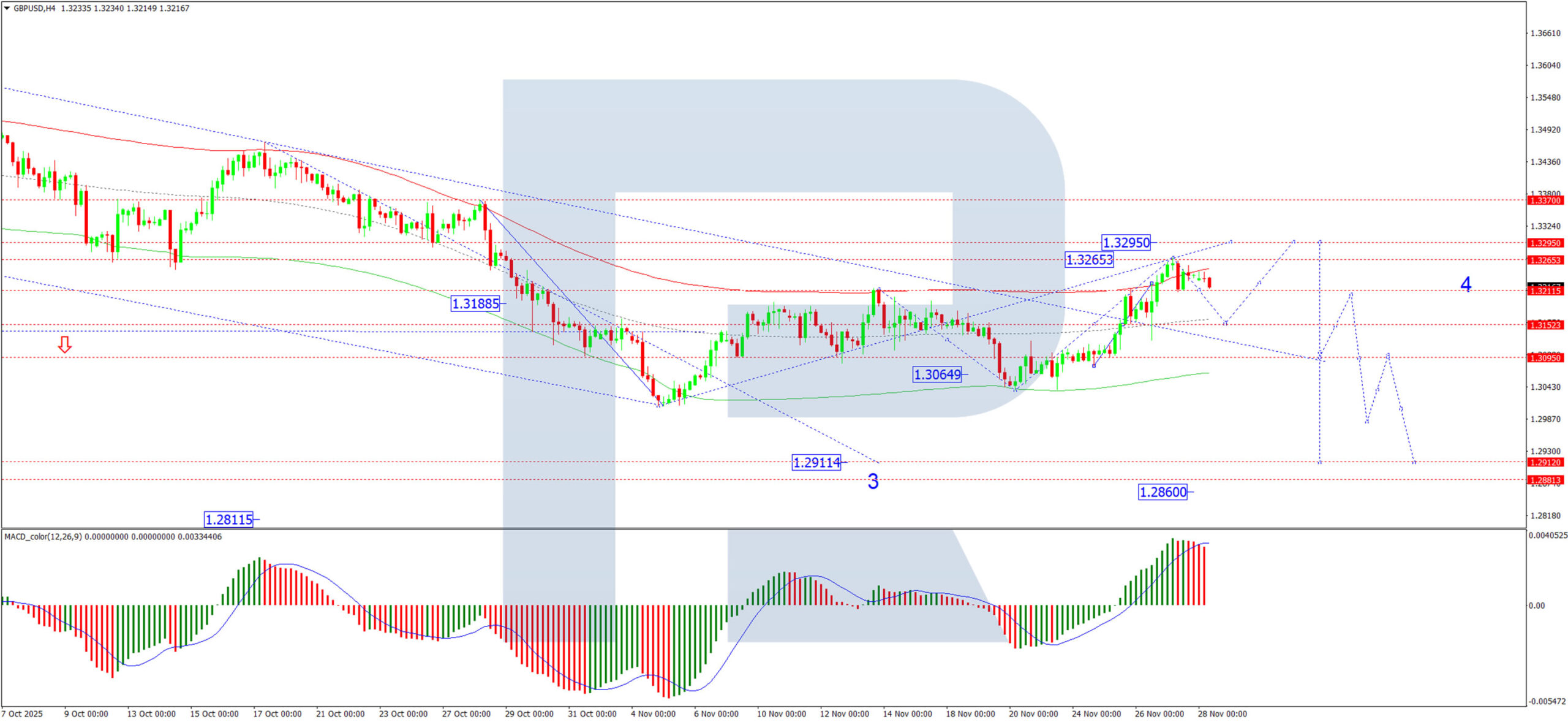

Technical Analysis: GBP/USD

H4 Chart:

On the H4 chart, GBP/USD has completed a growth wave to 1.3265 and is now likely to form a consolidation range below this peak. A decisive decline and break below the 1.3210 support would trigger a corrective move towards 1.3152. Following the completion of this correction, we would anticipate the formation of a new growth structure, initially targeting a return to 1.3215. A sustained break above this level would then open the path for a more significant advance towards 1.3295. The MACD indicator supports this view of an impending pullback. Its signal line is at elevated levels above zero and has diverged bearishly from its histogram, suggesting the recent upward momentum is waning.

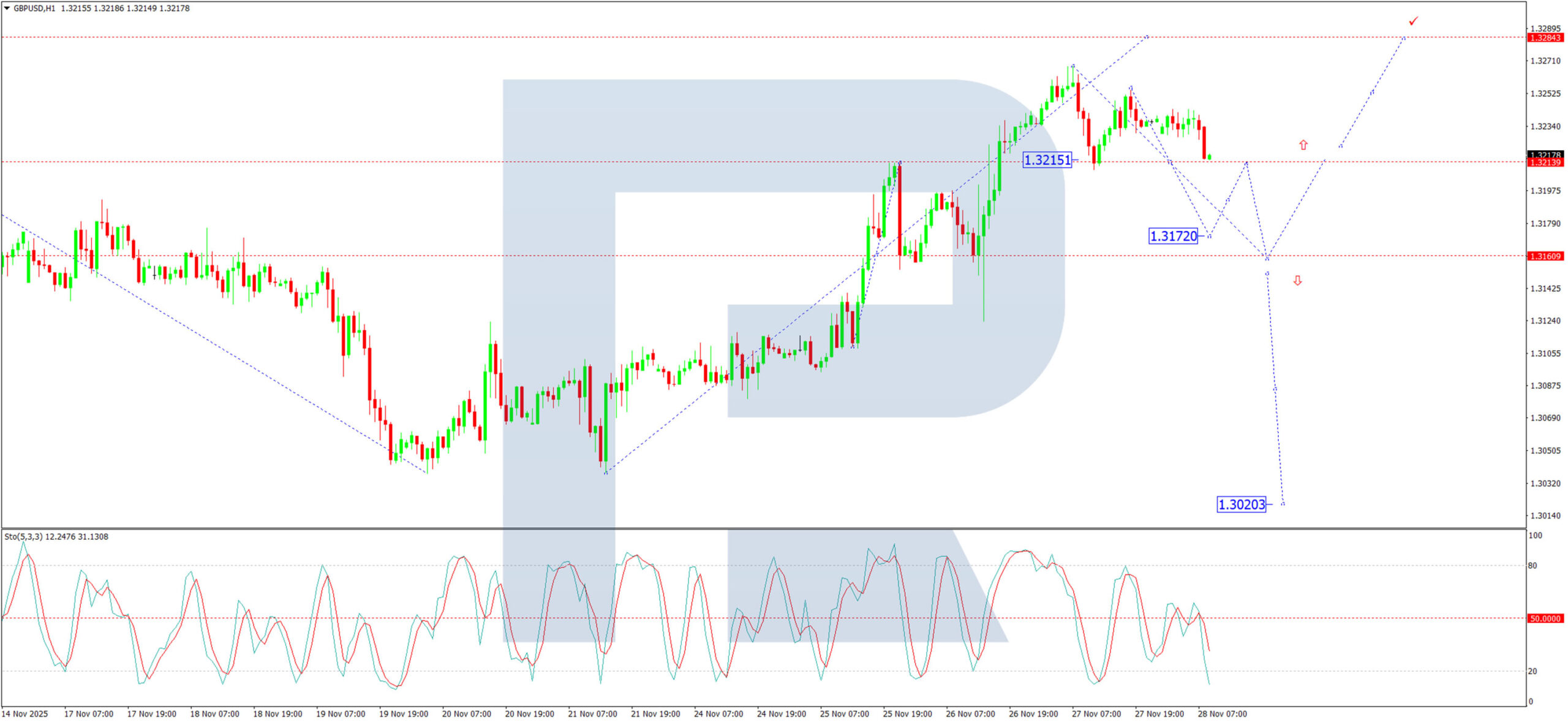

H1 Chart:

On the H1 chart, the pair formed a downward impulse to 1.3210, followed by a rebound to 1.3254. These two levels now define the boundaries of a consolidation range. We expect a downward breakout from this range, triggering a decline towards the 1.3160 target. This near-term bearish bias is confirmed by the Stochastic oscillator. Its signal line is below 50 and is trending downward towards 20, indicating that short-term selling momentum is building.

Conclusion

While GBP/USD is managing to hold onto recent gains, the rally appears to be on shaky ground. Fundamental doubts about the UK's fiscal and economic outlook are colliding with technical signals that suggest a near-term correction is likely. The key level to watch is 1.3210; a break below this support would signal a deeper pullback towards 1.3160, potentially offering a more attractive level from which to reassess the long-term directional bias. For any sustained bullish move to develop, a decisive break above 1.3295 would be required.

USD/JPY Currency Pair Has Stabilised Around 156.300 Level

The ATR indicator is sitting near its lowest readings and is trending downward. This may reflect not only reduced trading activity over the Thanksgiving period in the US, but also uncertainty among currency traders who are weighing the many factors influencing USD/JPY at the moment.

On one hand, the US dollar is being pressured by expectations of a Federal Reserve rate cut, with Fed officials delivering notably dovish comments this week.

On the other hand, the yen’s valuation is being shaped by:

→ the economic stimulus package from Prime Minister Sanae Takaichi;

→ expectations of Bank of Japan intervention to support the weakening yen;

→ geopolitical tensions between China and Japan.

Technical Analysis of USD/JPY

The chart supports the view that the market is balanced.

Using the ascending channel that began forming after USD/JPY broke above the psychological 150 level, we can see that the pair has moved into the lower half of the channel, while the median line has shifted from acting as support to working as resistance (as shown by the arrows).

At present, USD/JPY is compressing into a triangle formed by:

→ the lower boundary — the line dividing the lower half of the channel into quarters;

→ the upper boundary — the descending trendline drawn through last week’s lower highs.

A breakout from this triangle may be sudden and tricky, so the current fall in volatility should not lull USD/JPY traders into complacency. It is entirely possible that after repeated verbal warnings, the Bank of Japan could proceed with direct intervention — an action that would almost certainly break the existing upward channel.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

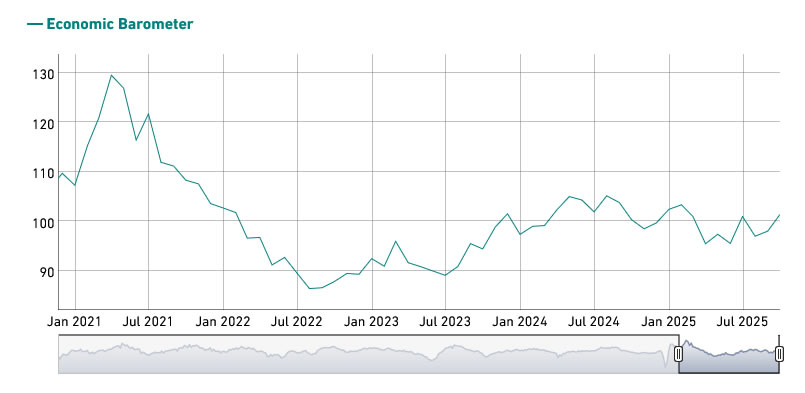

Swiss KOF barometer edges up to 101.7 on stronger demand

Switzerland’s KOF Economic Barometer ticked higher in November, rising from 101.5 to 101.7 and signaling modest improvement in the near-term economic outlook.

KOF noted that the improvement is concentrated on the demand side. Indicator bundles tied to foreign demand and private consumption strengthened, suggesting both external orders and household activity are on firmer footing.

On the production side, however, parts of the economy remain under pressure. Indicators for financial and insurance services, as well as construction, deteriorated, revealing a mixed underlying picture.

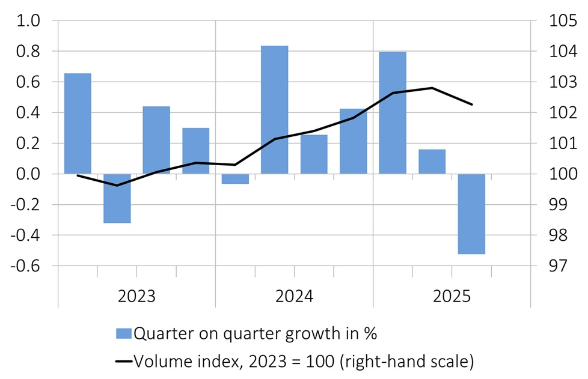

Swiss GDP contracts -0.5% in Q3, pharma and chemicals lead decline

Swiss GDP fell -0.5% qoq in Q3, marking a sharp reversal driven almost entirely by the chemical and pharmaceutical sector. After strong momentum earlier in the year, the industry saw output plunge -7.9%, erasing prior gains and dragging the broader economy into contraction.

Authorities noted that the downturn reflects recent volatility in foreign trade. Earlier quarters saw a surge in pharma exports, partly driven by front-loading ahead of U.S. trade-policy changes. Those temporary boosts have now unwound, resulting in a "compensatory decline" that weighed heavily on Q3 activity.

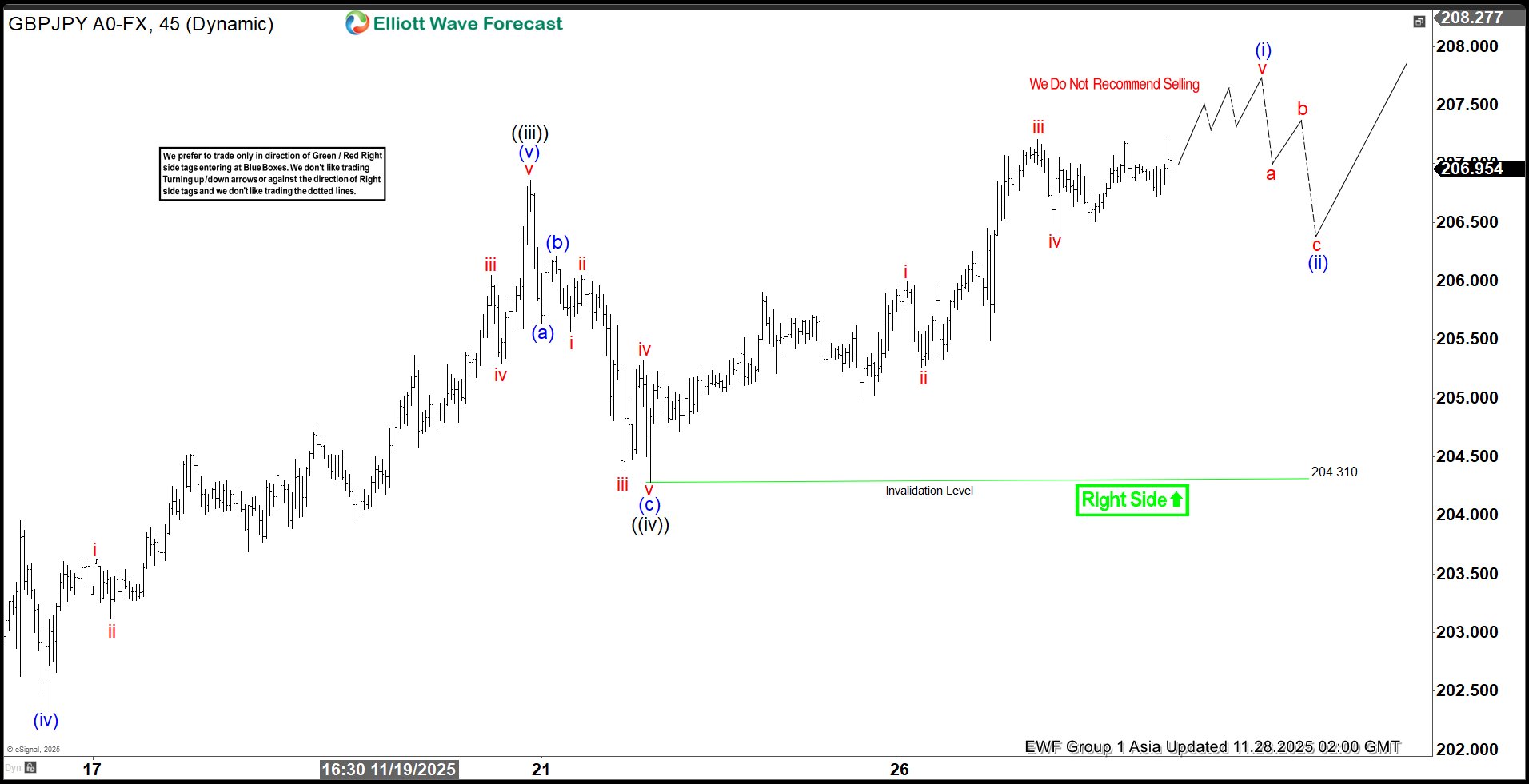

GBPJPY Buyers Hold Command, Eye Multi Decade Highs

The short-term Elliott Wave outlook in GBPJPY indicates that the cycle from the October 2, 2025 low remains in progress as a five-wave diagonal structure. From that date, wave ((i)) concluded at 205.3, followed by a corrective pullback in wave ((ii)) that reached 199.05. The pair then advanced in wave ((iii)), achieving 206.85, as reflected in the 45‑minute chart. Subsequently, wave ((iv)) unfolded in the form of a zigzag pattern. Within this correction, wave (a) ended at 205.63, wave (b) terminated at 206.21, and wave (c) completed at 204.31. This final leg also marked the completion of wave ((iv)) at a higher degree.

From that point, the pair resumed its upward trajectory in wave ((v)), which developed as an impulse structure of lesser degree. Rising from wave ((iv)), wave i concluded at 206, while wave ii corrected to 205.26. The advance continued with wave iii reaching 207.2, before wave iv pulled back to 206.41. The current expectation is that the pair will soon complete the cycle from the November 21 low in wave v of (i). Following this, a corrective phase in wave (ii) should emerge to balance the preceding advance before the rally resumes.

As long as the pivot at 204.31 remains intact, dips are anticipated to find support. These supports are likely to appear in sequences of three, seven, or eleven swings, reinforcing the broader bullish outlook. The structure suggests that the market retains a constructive bias, with corrections offering opportunities for continuation rather than signaling exhaustion.

GBPJPY 45-Minute Elliott Wave Chart From 11.28.2025

GBPJPY Elliott Wave Video:

https://www.youtube.com/watch?v=n2uqgmqZLBc

Weak Yen Might Become Ever Bigger Factor in BoJ’s Assessment

Markets

US markets were closed for Thanksgiving yesterday and second tier EMU eco data failed to impress. The result was a dull, low volume, trading session. Minutes of the previous ECB meeting confirmed the central bank’s current comfortable position with the bar being very high to change that. EC November economic confidence data printed near consensus. Russian president Putin signaled willingness to negotiate a peace deal by saying that US President Trump’s proposals for end the war could be the basis for future agreements. No final version exists yet with US official heading to Moscow next week for further discussions. He was happy to learn that the US took into account Russia’s position as discussed when the two presidents met in Alaska. European stock markets closed almost unchanged after a day of treading water near opening levels. German bond yields added 1 bp across the curve while EUR/USD remained stuck at 1.16. EUR/GBP also went nowhere at 0.8758. The “relief” rally following UK Chancellor Reeves’ Autumn budget proved short-lived. We stressed before that it might be a battle won by the UK government, but the fight ain’t over.

US markets close early today with traded volumes traditionally lower the (Black) Friday after Thanksgiving. Eco data are confined to Europe with national inflation readings in Spain, France, Italy and Germany. Yesterday’s numbers released in Belgium showed a significant acceleration, but that doesn’t necessarily mean that we’ll get the same today as national policies obviously can play an important role. Taken into account the firm ECB stance, EMU eco data generally lost market-moving potential. It leaves general risk sentiment as today’s main global market driver. Stock markets crawled back this week, avoiding a sell-on-upticks pattern. We’ll see how much dash is left going into the weekend.

News & Views

Japanese data published this morning at least confirm that conditions are falling into place for the Bank of Japan to make a next step in the process of policy normalization in the near future. November Tokyo CPI inflation, seen as pointer for national data to be published next month, remained well above the BoJ’s 2% inflation target. Headline inflation eased marginally from 2.8% to 2.7%. Core measures (ex fresh food & ex fresh food and energy) were both unchanged at 2.8%. Food price inflation slowed to 0.3% M/M and 5.5% Y/Y (from 5.8%). Utility prices again rose a solid 4.1% M/M (2.4% Y/Y). Services prices inflation eased slightly to 1.5% Y/Y from 1.6%. Price rises for goods were still a strong 4% Y/Y. In this respect, the weak of level of the yen might become an ever bigger factor in the BoJ’s assessment. Aside from the price data, activity indictors also showed resilience with both October production growth (1.4% M/M and 1.5% Y/Y) and retail sales (1.6% M/M) substantially beating expectations. The unemployment rate remained unchanged at 2.6%. The next BoJ policy decision is scheduled for December 19. The market currently discounts a probability of a rate hike of about 60%. The yen whipsawed but holds basically unchanged near USD/JPY 156.35.

Consumer confidence in New-Zealand as measured by the ANZ-Roy Morgan survey improved substantially in November, rising from 92.4 to 98.4 and reaching the best level since June. Consumers, amongst others, turned more positive on the economy, both for the next year and further out. Also ANZ business confidence jumped sharply in November from 58.1 to 67.1. This is the best level since March 2014. The release of these solid confidence data come after the RBNZ earlier this week cut the policy rate by 25 bps to 2.25%, but indicated that the bar for further easing is high as the current level of the policy rate is low enough to support activity going forward. Even so, after a sharp rebound after the RBNZ decision, the kiwi dollar this morning eases marginally to NZD/USD 0.5715. It traded below 0.56 at the start of the week.

A Delicate Setup

It’s boring when the US is not here. All the show, the drama, the buzz, the rumours stop – all of a sudden – and we are left to look back and think. So let’s think. It was a harsh month. The S&P 500 companies announced strong earnings: earnings growth came in at an impressive 13.4% for the entire index. Health care, financials and consumer discretionary were leading sectors, along with technology, of course.

Most Big Tech names reported better-than-expected earnings and stronger-than-expected guidance – including Nvidia. But instead of being the best day of the earnings season, Nvidia’s earnings day turned into drama. Investors – too used to blockbuster results – decided to dig into the reports. And the gap between accounts receivable and incoming cash, along with swelling inventories, became the focal point and added to circularity worries around the latest AI deals. Nvidia’s earnings – which were supposed to give comfort to tech investors – had the exact opposite effect. The bad press took over, and things have been quite downhill since. Earlier this week, Nvidia was trading up to 20% lower than its latest peak a month ago. Meta is accused of offloading its debt to private equity companies to keep its books clean, and the circularity of the deals around OpenAI – and OpenAI itself – is under heavy criticism.

The good news is that the Fed doves jumped in at the right time – last Friday – to make sure that the tech-led rally didn’t reverse and take global stocks down with it. The probability of a Fed cut went from below 30% to 85%, giving the world space to breathe as the US left for Thanksgiving.

Since then, nothing much. European stocks barely moved yesterday, while Asian tech stocks looked bleak, with Alibaba finding no support despite strong results and news that it has already introduced AI glasses to compete with Meta.

In vain, the HSI looks uninspiring to global investors, and the Korean Kospi and Japan’s SoftBank – a few names I watch to feel the heat in technology – are struggling.

For the S&P 500, expectations for future quarters have softened. Projections are pointing at lower revenue growth over the next five quarters, ranging between 5% and 8%. In contrast, according to FactSet, analysts expect higher earnings growth for the Mag 7 over the next four quarters, between 18% and 25%.

Meanwhile, valuations are high (above 5 and 10-year averages), and we would need a drop of a bit more than 5% to call it a correction.

So here we are. I’m already being asked whether we will see a Santa Rally. And my answer is: hard to tell. Really hard to tell because there is so much uncertainty in the market right now: uncertainty around AI valuations, uncertainty around Japanese yields as Takaichi pushes for higher spending and higher borrowing in Japan, and uncertainties, of course, regarding what the Federal Reserve (Fed) will do – and what the Fed should do.

Even though I believe the best thing for the Fed would’ve been to wait a month and deliver a rate cut when the sky is clear and the data is out, truly, given the Fed probabilities – and the wild swings we’ve seen – it would be dramatic for expectations to snap back to ‘no cut’. It would inject an incredible amount of volatility into the market and make the Fed look foolish – and they really don’t need that right now.

So, we will probably get that 25bp cut. The question is: what happens after? If the inflation report (due the week after the decision) remains as subdued as it has been for the rest of the year, the way could be cleared for a Santa Rally – because no one wants to book profits after such a stellar year, right? We could see some profit-taking in January. Or we get a hot inflation report that vanishes the dream of 2026 cuts – we’re talking about 2–4 cuts – and the selloff deepens before year end. And regarding the accuracy of US data, well, it will take time to see whether the data is being tweaked to serve the White House’s lower-rate ambitions.

The US dollar is preparing to close the week on a slightly better note, and returning above the 200-DMA should help the greenback stay on course for further recovery of this year’s losses. The downside potential in the euro is limited as the European Central Bank (ECB) is not willing to cut rates further, with policy looking – and feeling – like it is in a good place at the moment. A very rare feeling, indeed.

For Japan, the story remains the same: the USDJPY will weaken along with the rising pressure on JGBs, while sterling sees the post-Budget appetite gently wane. Gilt yields rebounded yesterday on the realization that the Budget – though eventless – didn’t necessarily hint at a sustainably better fiscal picture. And it cannot. When productivity and growth slow, the only way to get more money in is by collecting higher taxes and issuing more debt. More taxes being deflationary, the Bank of England (BoE) could get back to cutting rates in December. Cable looks good to sell.

In commodities, gold is back to gains as softening Fed expectations and lower US yields bring inflows into the yellow metal – that’s good because gold is acting as you would expect, shrugging off the impact of the speculative moves of late summer.

Crude oil, on the other hand, is better bid into the OPEC meeting weekend. OPEC is expected to reiterate its intention to pause production increases when it meets this weekend to relieve downside pressure on oil prices. Indeed, oil prices have been falling this year despite many rate cuts from major central banks and a cheaper US dollar – both fundamentally supportive of prices. That means that ample OPEC and non-OPEC supply has weighed heavier on price dynamics. So OPEC knows that if it wants to throw a floor under cheapening prices, it must restrict production. But the thing is, OPEC’s share in the global oil market has been narrowing, meaning that lower supply – even fresh supply restrictions – may not reverse the bearish trend if the US keeps “drill, baby, drill.”