Sample Category Title

The Weekly Bottom Line

Canadian Highlights

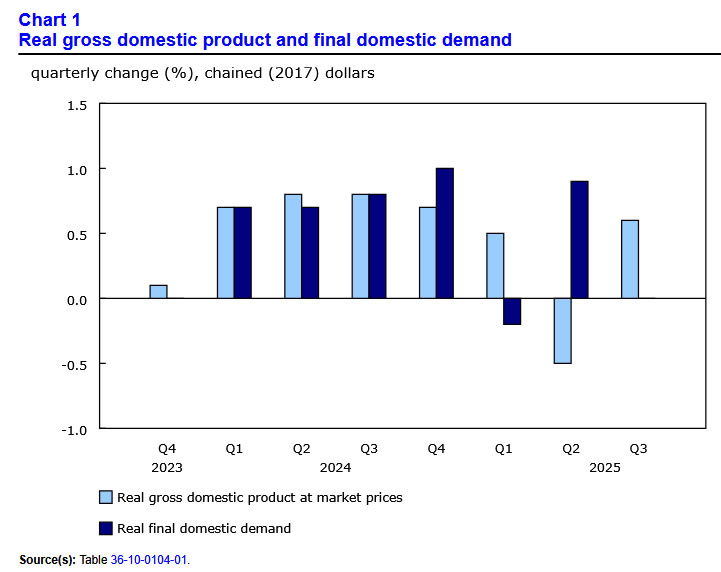

- GDP growth rebounded sharply in Q3, but the composition points to soft domestic demand. Revisions back to 2022 indicate that the economy was stronger than previously thought.

- Industry GDP posted a modest gain in September, but points to a contraction in October. Export-reliant sectors continue to lag.

- Tangible benefits from the two new government announcements will take some time to materialize. For now, the economy is tracking in line with the BoC’s estimates, suggesting the policy rate will remain on hold.

U.S. Highlights

- Market expecta k provided further anecdotal evidence that growth in the U.S. economy remains sluggish.

Canada – The Economy is Still Playing Andante

The third quarter GDP report spilled plenty of black ink, giving Black Friday week a literal twist. Markets reacted positively with the S&P/TSX building on previous gains, rising by 3.5% and long-term rates holding close to 3.1%. The loonie firmed by a full cent to $0.72

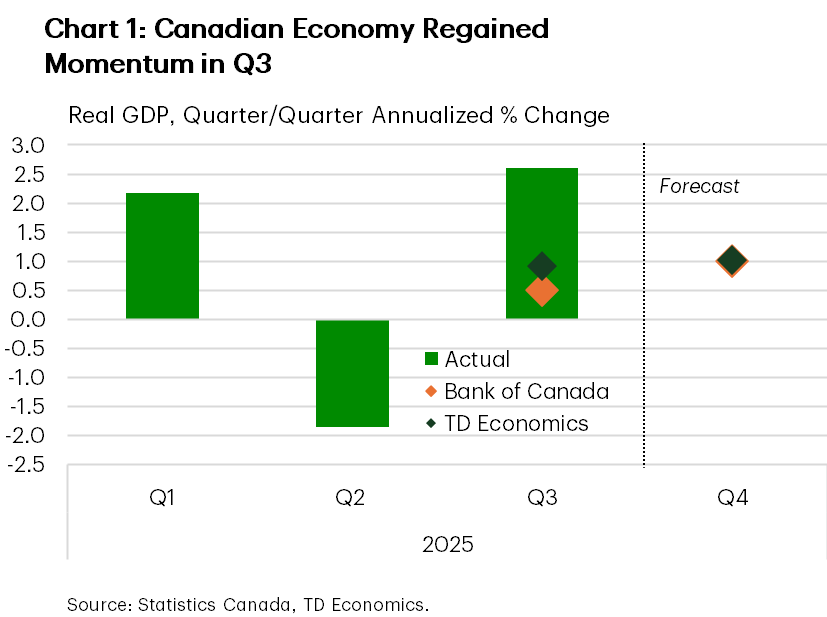

GDP growth rebounded sharply in Q3, rising by 2.6% quarter-on-quarter (q/q), annualized - far above the consensus call of 0.5% and our tracking of 0.9% (Chart 1). The upward surprise was tempered slightly by revisions. The second-quarter contraction was marked down from -1.6% to -1.8%, reflecting weaker personal consumption expenditures.

The composition tells an interesting story. Exports were basically flat last quarter after falling sharply in Q2, while business investment continued to slide amid still elevated trade uncertainty. Meanwhile, the pillar that carried the economy earlier in the year – household spending and inventories – slowed considerably. This kept underlying domestic demand soft, even as government spending surged by an eye-catching 12.2% (annualized), driven almost entirely by a massive increase in spending on weapon systems.

The GDP release also incorporated revisions from the Provincial and Territorial Economic Accounts. These updates showed stronger consumer spending and a substantial upgrade to non-residential investment. The latter added $135 billion to the level of GDP over the past two years, suggesting that Canada’s productivity performance – while still troubling – may not be as weak as previously thought.

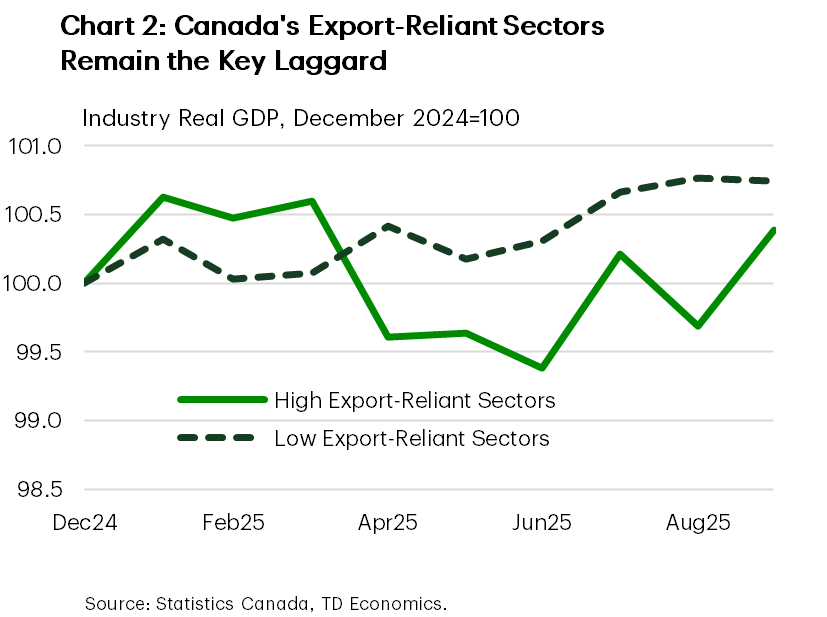

We also received figures on GDP by industry for September, which showed a modest pick-up in activity. It offered a clearer view on how the ongoing trade tensions are filtering through supply chains. Industries most affected by tariffs, such as manufacturing, rebounded but remain a laggard and still face a difficult path forward (Chart 2). But even outside of trade exposed sectors, the rest of the economy is not convincingly expanding either, with several sectors that had shown strength earlier in the year, now contracting. The advance estimate points to a decline in October.

On the musical spectrum, the economy is still playing andante: faster than adagio but far from allegro –a slow, steady walk rather than a spirited march. In this otherwise muted symphony, the federal government added two notable accents. First, a suite of measures aimed at protecting and transforming Canada’s industry by redirecting demand towards domestically-produced steel and lumber. Second, Ottawa and Alberta reached an agreement to advance a new pipeline connecting oil production to the West Coast, conditional on achieving a 75% reduction in emissions over the next decade.

As with all major infrastructure projects, tangible economic impacts will take years to materialize. For now, the underlying rhythm of the economy remains broadly aligned with the Bank’s forecast for growth just above 1% through 2026, with existing slack already embedded in the outlook. A future rate cut cannot be fully ruled out but would require a pace of growth far closer to largo – a more meaningful cooling relative to the already subdued outlook.

U.S. – Equity Markets Gobble Up Prospects for a December Rate Cut

U.S. equity markets traded higher through the holiday shortened week, boosted by expectations for a December rate cut and renewed enthusiasm for the AI trade. Meanwhile, economic data out this week reinforced the narrative that some sluggishness has materialized in the U.S. economy. The S&P 500 is looking to end the week higher by over 3%, more than erasing last week’s losses and is now up 16% year-to-date. Treasury yields dipped by a few basis points on the week, with the 10-year currently hovering around 4%.

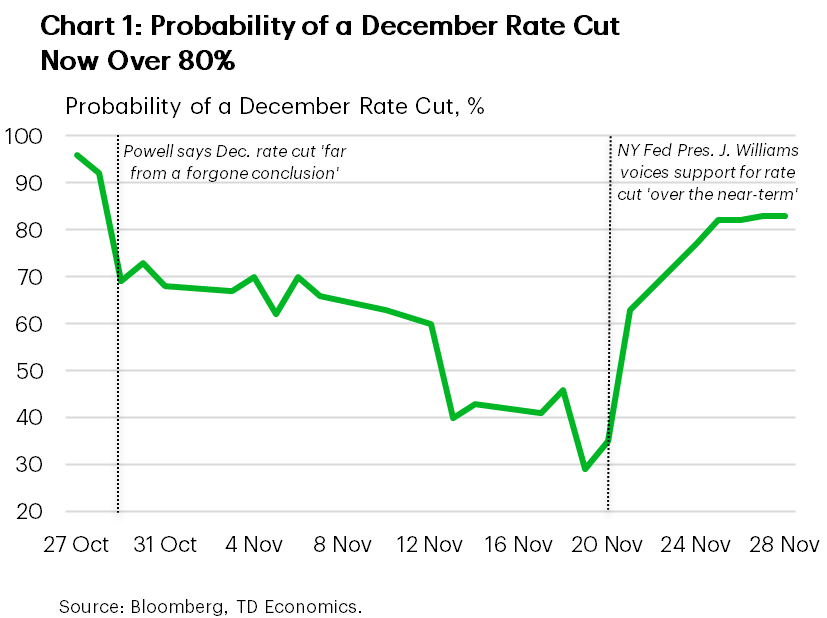

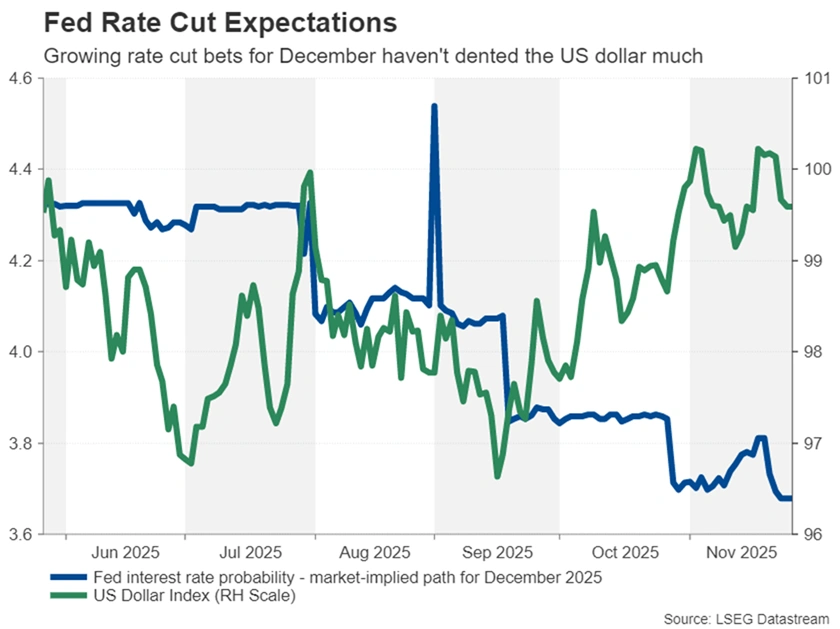

Fed futures have been on a wild ride recently. Just over a week ago, markets attached a roughly one-third probability to a December rate cut. But since then, two Fed officials who hew closely to Chair Powell, including NY Fed President John Williams and San Francisco Fed President Mary Daly (non-voting member) voiced support for a December rate cut. Pricing has since swung back to over 80% (Chart 1). The Fed doesn’t tend to fight the market and with the decision just over a week away, a further trimming in the policy rate looks to be a safe bet. Though if ADP employment data were to surprise to the upside next week, odds may yet shift again.

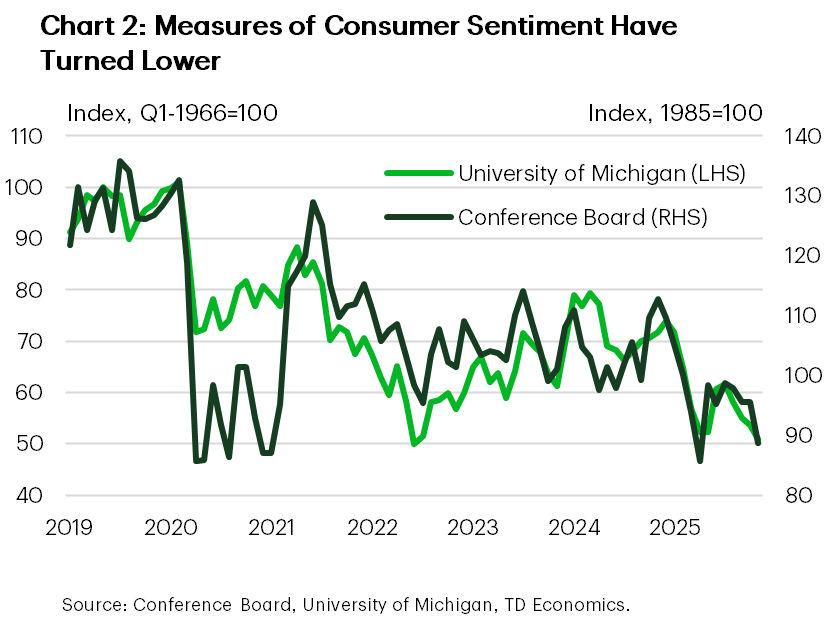

Turning to this week’s economic data releases, retail figures for September showed that spending slowed at the end of the third quarter – putting Q4 on a shakier footing. The softening in September spending isn’t entirely surprising. Measures of consumer sentiment have nosedived recently, with the Conference Board’s November reading slipping to its lowest level since April and second lowest reading since the depths of the 2020 Global Pandemic (Chart 2). Survey details show that consumers’ assessment of job availability is particularly downbeat, as are prospects for making ‘larger purchases’ over the next six months. While shifts in consumer confidence metrics have proven to be a less reliable predictor of spending patterns post-pandemic, the steady downward trend across multiple measures suggests the direction of travel is likely to be lower over the near-term.

This was further confirmed in the Fed’s Beige Book, which noted that overall consumer spending had ‘declined further’ in recent months, even though higher-end retail spending remained resilient. The Fed’s contacts chalked some of the weakness up to the government shutdown, and a pullback in EV sales following the expiration of the federal tax credit. However, the softening labor market also likely had some influence, with the majority of Districts seeing a decline in hiring and about half noting weaker labor demand. Importantly, employers across most Districts reported limiting headcounts using hiring freezes, ‘replacement-only’ hiring and attrition rather than through layoffs.

This reinforces the ‘low hire, low fire’ narrative’. But it’s a precarious balance, and one where the downside risks have the potential to materialize very quickly. While this supports the case for a bit more easing in the fed funds rate, still elevated inflation and a policy stance that is quickly closing in on neutral are important considerations that can’t be overlooked. Bringing the policy rate much lower runs the risk of putting the Fed out of position in the event the labor market were to firm in the months ahead.

Week Ahead – US Data to Stay in the Limelight as Fed Bets Gather Pace

- Flurry of US data to test dovish Fed expectations as next meeting looms.

- ISM PMIs, ADP employment and PCE inflation may yet upset rate cut hopes.

- Eurozone CPI, Australian GDP, Canadian employment also on tap.

December rate cut not a done deal yet

After a string of hawkish remarks by numerous Fed speakers, the doves made a comeback during the past 10 days, putting a rate cut at the December meeting back on the table. This lifted the odds of a 25-bps reduction on December 10 from around a quarter to almost 80%, in a dramatic reversal that reverberated across financial markets. Treasury yields sank, the US dollar not so much, but risk assets were propelled higher, with Wall Street and cryptocurrencies in particular recouping a chunk of their November losses.

This sudden turnaround wasn’t just on the basis of two new doves joining the rate-cut bandwagon, most notably one of them being influential New York Fed chief John Williams. The more recent data has raised fresh question marks about the strength of the US economy.

However, Chair Powell’s argument that policymakers won’t have access to the latest labour market and inflation indicators in time for the December policy decision still stands. In light of the missing and somewhat conflicting data, next week’s releases will be monitored very closely, as there’s plenty on the calendar that could push the odds either back towards 50% or closer to 100%.

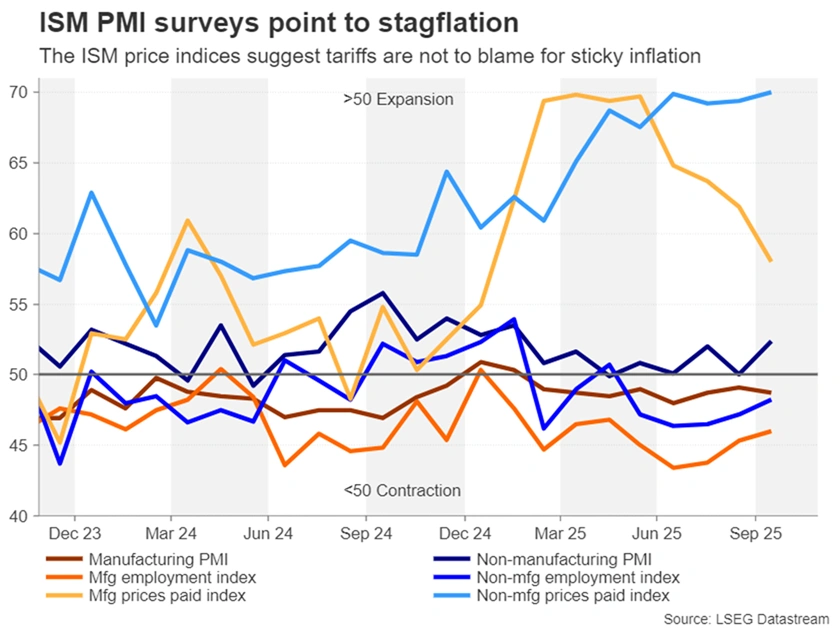

Will the ISM PMIs pose a stagflation dilemma?

First on the agenda is the ISM manufacturing PMI for November on Monday. The services PMI is released a couple of days later. The US manufacturing sector has been contracting since March according to the ISM survey, amid the tariff-related uncertainty and possible retaliatory backlash against American goods from international buyers.

Employment has also been declining, with the sub-index printing below 50 since February. However, the price index has plunged from close to 70.0 to 58.0 in October, casting doubt on the claim that tariffs have been inflationary. What’s worrying, though, is that the equivalent gauge for the services sector has stayed elevated near 70.0, suggesting that domestic price pressures are to blame for the country’s inflation rate being stuck within the 3.0% vicinity.

The overall PMI for services edged up to 52.4 in October, helped by a jump in new orders, while the manufacturing PMI declined to 48.7. Another healthy rise in services activity in November would bolster the hawks at the Fed, whereas a sudden drop to 50.0 or lower would back the case for an immediate rate cut.

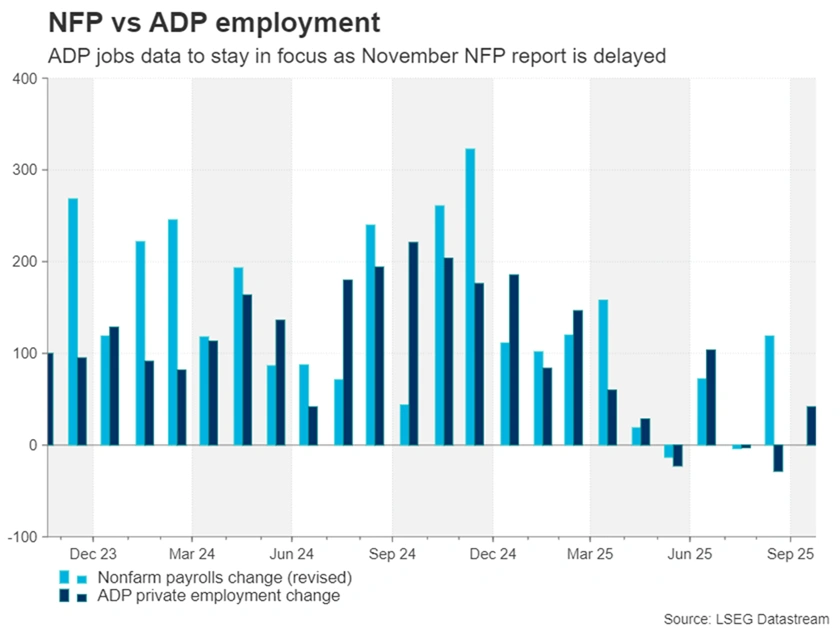

ADP in focus as November NFP delayed

Just as important will be Wednesday’s ADP employment report. The official November payrolls report isn’t due until December 16, and with the October one cancelled, the ADP’s employment survey for the private sector will offer a vital update on the labour market. In October, there were 42k jobs added, which was more than expected. As with the ISM PMIs, any surprises in either direction pose a symmetrical risk to easing expectations, as well as the US dollar.

More jobs data will follow on Thursday with the Challenger Layoffs. Even though most Fed officials haven’t sounded too worried about the recent round of job-cut announcements, any jump in layoff numbers in November could fuel concerns that the US labour market is in trouble.

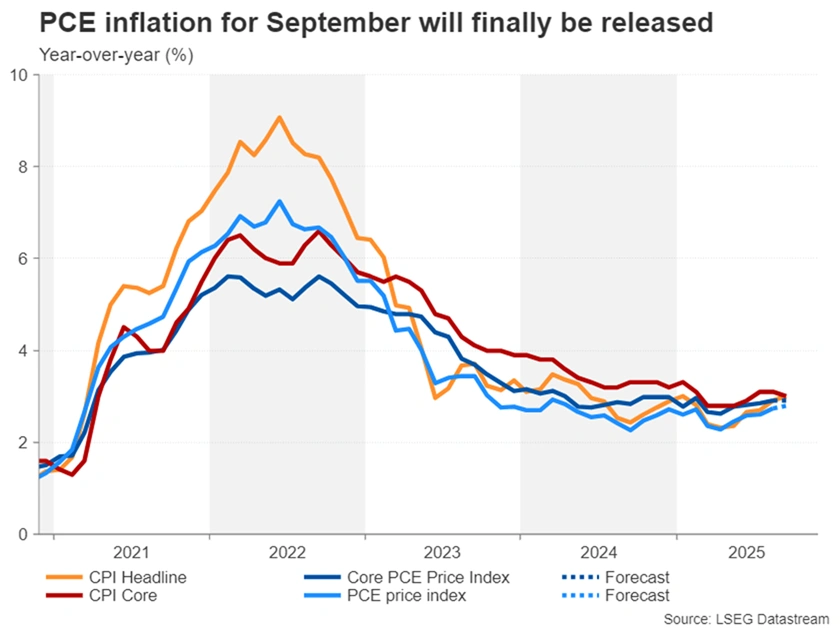

September PCE inflation might not matter

Moving to Friday, the focus will shift to the PCE inflation and personal consumption indicators for September. Although the Fed will be more eager to see the November stats, whose release date hasn’t been confirmed yet, the September report will still be watched for some guidance, especially if the incoming data continues to give mixed messages on the state of the economy.

Headline PCE is forecast to have inched up to 2.8% y/y in September from 2.7%, while the all-important core PCE price index is projected to have stayed unchanged at 2.9% y/y.

Other releases will include industrial production on Wednesday, and factory orders and the University of Michigan’s preliminary consumer sentiment survey on Friday.

Should December rate cut bets take a hit from a broadly strong set of figures, Wall Street’s rebound would be put at risk, potentially dashing hopes of a Santa rally this year, at least before the Fed meeting.

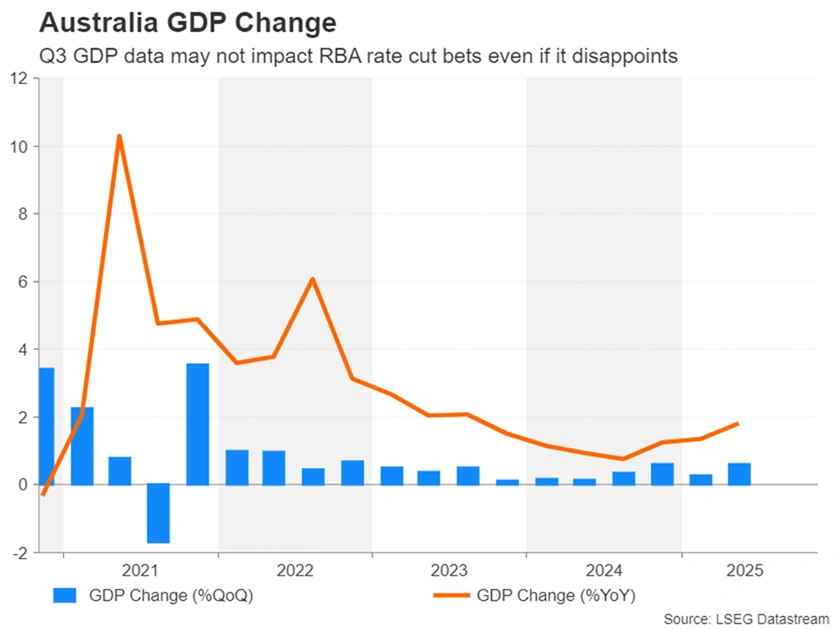

Aussie might shrug off GDP data

In Australia, the latest inflation readings couldn’t have been more decisive for the Reserve Bank of Australia where rate cut expectations have completely evaporated. The consumer price index rose by a more than-forecast 3.8% y/y in October, well above the RBA’s upper target band of 3.0%.

Combined with signs of a recovery in the labour market, there’s very little prospect of the RBA trimming rates again anytime soon. Hence, Wednesday’s GDP figures for the third quarter are unlikely to alter those expectations much even if they disappoint.

The Australian dollar will probably shrug off the growth data and will instead be driven by global risk sentiment, as well as by PMI numbers out of China on Sunday (official government), Monday (S&P Global manufacturing) and Wednesday (S&P Global services).

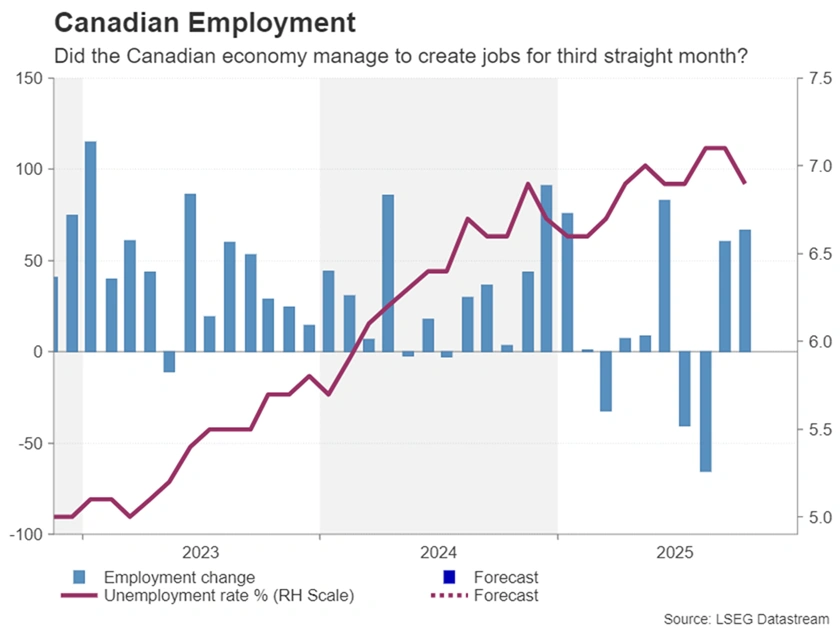

Loonie bulls hoping for jobs lift

The Bank of Canada is another central bank that’s had to adopt a more neutral tone lately. Although the Canadian economy continues to reel from President Trump’s tariffs, employment conditions appear to be stabilizing and underlying inflation measures remain sticky.

Yet, in the absence of Washington and Ottawa striking a trade agreement over the next few months, further rate cuts cannot be ruled out. But the bar is high as the BoC has already slashed rates to 2.25% so policymakers are likely preserving some firepower for a rainier day.

Along with inflation, the labour market will be key for the BoC in determining the need for additional easing. If Friday’s employment numbers show that the economy added jobs for the third month in a row, expectations of a 25-bps reduction will probably fade further, boosting the Canadian dollar.

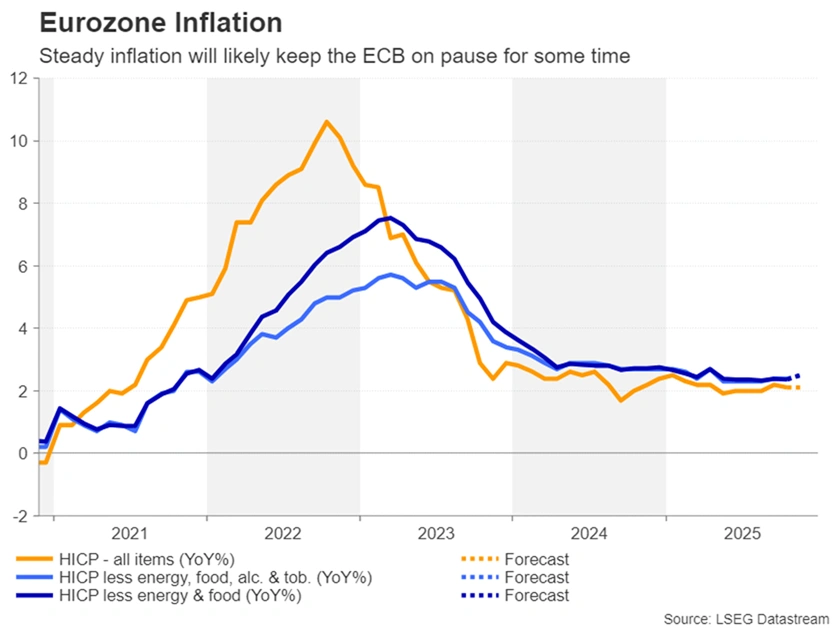

Eurozone CPI could be a non-event

Inflation is a lesser concern in the Eurozone where the European Central Bank has no plans to adjust policy anytime soon. The data backs the ECB’s firmly neutral stance.

The headline rate of CPI has been hovering around 2.0% since spring. The flash estimates for November due on Tuesday are expected to maintain the flat picture, with headline CPI holding steady at 2.1%. On Friday, no change is anticipated in revised estimates of Q3 GDP when the economy expanded by 0.2% q/q.

German industrial orders and French industrial production might also move the euro on Friday. But on the whole, Fed policy and US-EU trade relations will be a bigger driver for the single currency in the short-to-medium term.

Yen and Oil in search for a boost

In contrast, the dollar/yen pair is expected to remain somewhat more volatile, where the diverging monetary policies of the Fed and Bank of Japan are not quite having the desired effect. Although the yen has steadied over the past week following increased Fed easing bets and some unexpectedly hawkish comments from BoJ policymakers, it’s still trapped within the intervention zone.

Monday’s revised capital expenditure figures for Q3 out of Japan and Friday’s household spending numbers for October could provide some additional support to the yen if they bolster the odds of a December rate hike.

Finally, OPEC+ countries are widely anticipated to keep production quotas unchanged on Sunday, reaffirming their decision to pause output increases during the first three months of 2026. Oil traders will therefore likely be paying more attention to any updates on the Trump administration’s efforts to get Ukraine and Russia to agree to a peace plan.

Forward Guidance: Canada’s Job Growth to be Flat in November, Unemployment Rate Unchanged

Canadian labour markets will be the focus with the scheduled release of Canadian international trade data delayed by the U.S. government shutdown, while the release of U.S. employment and trade data was also pushed further back into December.

The November employment report on Friday will be the last major data release ahead of the Bank of Canada’s interest rate decision on Dec.10.

We expect employment growth to be in flat in November, following larger-than-expected 67,000 and 60,000 increases in October and September, respectively. Slower population growth is expected to limit the number of new entrants into labour markets, leaving the unemployment rate unchanged at 6.9% from October after 7.1% in September and August.

Canadian labour markets are still soft with the unemployment rate still roughly one percentage point above levels we expect would be consistent with a “normal” backdrop. However, a steady 6.9% in November would mark the first month since May 2023 that there wasn’t a rise on a year-over-year basis.

Employment in heavily trade exposed sectors like manufacturing and transportation and warehousing have still underperformed broader trends, but showed significant improvement in October. Underperformance in trade exposed sectors have yet to spread broadly across the economy. Layoffs have been limited with the rise in the unemployment rate in October mostly reflecting longer job search times for new entrants. Canada’s employment count overall was up 299,000 in October from a year ago.

Industry data like job openings from indeed.com continued to show signs of stabilization in hiring demand. And, business confidence measures have improved as some of the more damaging international trade scenarios from earlier this year have not materialized.

Additionally, we’ll be watching hours worked closely. A decline in October (despite a gain in employment) was reportedly largely due to a teacher’s strike in Alberta, and should reverse in November. Wage growth unexpectedly ticked higher in October, but we expect it will broadly continue to edge lower in the near term with business surveys still suggesting planned wage increases to be smaller.

In October’s interest rate cut, the BoC clearly signalled that interest rates had now been adjusted to about where they should be (lower end of the estimated “neutral range” where they’re not significantly adding to inflation pressures), making additional reductions unlikely without significant downside surprises in growth, and/or inflation.

Week ahead data watch:

- We'll get delayed U.S. personal spending data for September next Friday. We expect spending to increase 0.2% month-over-month. Retail sales for September came in below consensus, but the services component appeared strong, offsetting weakness in goods spending.

- We anticipate personal income will rise 0.4% month-over-month, matching August.

Summary 12/1 – 12/5

Monday, Dec 1, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | CNY | NBS Non-Manufacturing PMI Nov | 50 | 50.1 |

| 01:30 | CNY | NBS Manufacturing PMI Nov | 49.2 | 49 |

| 21:45 | NZD | Building Permits M/M Oct | 7.20% | |

| 23:50 | JPY | Capital Spending Q3 | 5.90% | 7.60% |

| 00:00 | AUD | TD-MI Inflation Gauge M/M Nov | 0.30% | |

| 00:30 | JPY | Manufacturing PMI Nov F | 48.8 | 48.8 |

| 01:45 | CNY | RatingDog Manufacturing PMI Nov | 50.5 | 50.6 |

| 07:30 | CHF | Real Retail Sales Y/Y Oct | 1.20% | 1.50% |

| 08:30 | CHF | Manufacturing PMI Nov | 49 | 48.2 |

| 08:50 | EUR | France Manufacturing PMI Nov F | 47.8 | 47.8 |

| 08:55 | EUR | Germany Manufacturing PMI Nov F | 48.4 | 48.4 |

| 09:00 | EUR | Eurozone Manufacturing PMI Nov F | 49.7 | 49.7 |

| 09:30 | GBP | Manufacturing PMI Nov F | 50.2 | 50.2 |

| 09:30 | GBP | Mortgage Approvals Oct | 64K | 66K |

| 09:30 | GBP | M4 Money Supply M/M Oct | 0.40% | 0.60% |

| 14:30 | CAD | Manufacturing PMI Nov | 49.6 | |

| 14:45 | USD | Manufacturing PMI Nov F | 51.9 | 51.9 |

| 15:00 | USD | ISM Manufacturing PMI Nov | 49 | 48.7 |

| 15:00 | USD | ISM Manufacturing Prices Paid Nov | 59.5 | 58 |

| 15:00 | USD | ISM Manufacturing Employment Nov | 46 | |

| 15:00 | USD | Construction Spending M/M Oct | -0.10% | 0.20% |

| 21:45 | NZD | Terms of Trade Index Q3 | 0.30% | 4.10% |

| 23:50 | JPY | Monetary Base Y/Y Nov | -8.50% | -7.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | CNY | NBS Non-Manufacturing PMI Nov | |

| Forecast: 50 | Previous: 50.1 | ||

| 01:30 | CNY | NBS Manufacturing PMI Nov | |

| Forecast: 49.2 | Previous: 49 | ||

| 21:45 | NZD | Building Permits M/M Oct | |

| Forecast: | Previous: 7.20% | ||

| 23:50 | JPY | Capital Spending Q3 | |

| Forecast: 5.90% | Previous: 7.60% | ||

| 00:00 | AUD | TD-MI Inflation Gauge M/M Nov | |

| Forecast: | Previous: 0.30% | ||

| 00:30 | JPY | Manufacturing PMI Nov F | |

| Forecast: 48.8 | Previous: 48.8 | ||

| 01:45 | CNY | RatingDog Manufacturing PMI Nov | |

| Forecast: 50.5 | Previous: 50.6 | ||

| 07:30 | CHF | Real Retail Sales Y/Y Oct | |

| Forecast: 1.20% | Previous: 1.50% | ||

| 08:30 | CHF | Manufacturing PMI Nov | |

| Forecast: 49 | Previous: 48.2 | ||

| 08:50 | EUR | France Manufacturing PMI Nov F | |

| Forecast: 47.8 | Previous: 47.8 | ||

| 08:55 | EUR | Germany Manufacturing PMI Nov F | |

| Forecast: 48.4 | Previous: 48.4 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Nov F | |

| Forecast: 49.7 | Previous: 49.7 | ||

| 09:30 | GBP | Manufacturing PMI Nov F | |

| Forecast: 50.2 | Previous: 50.2 | ||

| 09:30 | GBP | Mortgage Approvals Oct | |

| Forecast: 64K | Previous: 66K | ||

| 09:30 | GBP | M4 Money Supply M/M Oct | |

| Forecast: 0.40% | Previous: 0.60% | ||

| 14:30 | CAD | Manufacturing PMI Nov | |

| Forecast: | Previous: 49.6 | ||

| 14:45 | USD | Manufacturing PMI Nov F | |

| Forecast: 51.9 | Previous: 51.9 | ||

| 15:00 | USD | ISM Manufacturing PMI Nov | |

| Forecast: 49 | Previous: 48.7 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Nov | |

| Forecast: 59.5 | Previous: 58 | ||

| 15:00 | USD | ISM Manufacturing Employment Nov | |

| Forecast: | Previous: 46 | ||

| 15:00 | USD | Construction Spending M/M Oct | |

| Forecast: -0.10% | Previous: 0.20% | ||

| 21:45 | NZD | Terms of Trade Index Q3 | |

| Forecast: 0.30% | Previous: 4.10% | ||

| 23:50 | JPY | Monetary Base Y/Y Nov | |

| Forecast: -8.50% | Previous: -7.80% | ||

Tuesday, Dec 2, 2025

| GMT | Ccy | Events | Consensus | Previous | |

|---|---|---|---|---|---|

| 00:01 | GBP | BRC Shop Price Index Y/Y Nov | 1.10% | 1% | |

| 00:30 | AUD | Current Account (AUD) Q3 | -13.4B | -13.7B | |

| 00:30 | AUD | Building Permits M/M Oct | -4.80% | 12% | |

| 05:00 | JPY | Consumer Confidence Nov | 36.3 | 35.8 | |

| 10:00 | EUR | Eurozone Unemployment Rate Oct | 6.30% | 6.30% | |

| 10:00 | EUR | Eurozone CPI Y/Y Nov P | 2.10% | 2.10% | |

| 10:00 | EUR | Eurozone Core CPI Y/Y Nov P | 2.40% | 2.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | BRC Shop Price Index Y/Y Nov | |

| Forecast: 1.10% | Previous: 1% | ||

| 00:30 | AUD | Current Account (AUD) Q3 | |

| Forecast: -13.4B | Previous: -13.7B | ||

| 00:30 | AUD | Building Permits M/M Oct | |

| Forecast: -4.80% | Previous: 12% | ||

| 05:00 | JPY | Consumer Confidence Nov | |

| Forecast: 36.3 | Previous: 35.8 | ||

| 10:00 | EUR | Eurozone Unemployment Rate Oct | |

| Forecast: 6.30% | Previous: 6.30% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Nov P | |

| Forecast: 2.10% | Previous: 2.10% | ||

| 10:00 | EUR | Eurozone Core CPI Y/Y Nov P | |

| Forecast: 2.40% | Previous: 2.40% | ||

Wednesday, Dec 3, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q3 | 0.70% | 0.60% |

| 01:45 | CNY | RatingDog Services PMI Nov | 51.9 | 52.6 |

| 07:30 | CHF | CPI M/M Nov | -0.20% | -0.30% |

| 07:30 | CHF | CPI Y/Y Nov | 0.10% | |

| 08:50 | EUR | France Services PMI Nov F | 50.8 | 50.8 |

| 08:55 | EUR | Germany Services PMI Nov F | 52.7 | 52.7 |

| 09:00 | EUR | Eurozone Services PMI Nov F | 53.1 | 53.1 |

| 09:30 | GBP | Services PMI Nov F | 50.5 | 50.5 |

| 10:00 | EUR | Eurozone PPI M/M Oct | 0.20% | -0.10% |

| 10:00 | EUR | Eurozone PPI Y/Y Oct | -0.20% | |

| 13:15 | USD | ADP Employment Change Nov | 19K | 42K |

| 13:30 | CAD | Labor Productivity Q/Q Q3 | -1% | |

| 13:30 | USD | Import Price Index M/M Sep | 0.10% | 0.30% |

| 14:45 | USD | Services PMI Nov F | 55 | 55 |

| 15:00 | USD | ISM Services PMI Nov | 52 | 52.4 |

| 15:30 | USD | Crude Oil Inventories (Nov 28) | 2.8M |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q3 | |

| Forecast: 0.70% | Previous: 0.60% | ||

| 01:45 | CNY | RatingDog Services PMI Nov | |

| Forecast: 51.9 | Previous: 52.6 | ||

| 07:30 | CHF | CPI M/M Nov | |

| Forecast: -0.20% | Previous: -0.30% | ||

| 07:30 | CHF | CPI Y/Y Nov | |

| Forecast: | Previous: 0.10% | ||

| 08:50 | EUR | France Services PMI Nov F | |

| Forecast: 50.8 | Previous: 50.8 | ||

| 08:55 | EUR | Germany Services PMI Nov F | |

| Forecast: 52.7 | Previous: 52.7 | ||

| 09:00 | EUR | Eurozone Services PMI Nov F | |

| Forecast: 53.1 | Previous: 53.1 | ||

| 09:30 | GBP | Services PMI Nov F | |

| Forecast: 50.5 | Previous: 50.5 | ||

| 10:00 | EUR | Eurozone PPI M/M Oct | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Oct | |

| Forecast: | Previous: -0.20% | ||

| 13:15 | USD | ADP Employment Change Nov | |

| Forecast: 19K | Previous: 42K | ||

| 13:30 | CAD | Labor Productivity Q/Q Q3 | |

| Forecast: | Previous: -1% | ||

| 13:30 | USD | Import Price Index M/M Sep | |

| Forecast: 0.10% | Previous: 0.30% | ||

| 14:45 | USD | Services PMI Nov F | |

| Forecast: 55 | Previous: 55 | ||

| 15:00 | USD | ISM Services PMI Nov | |

| Forecast: 52 | Previous: 52.4 | ||

| 15:30 | USD | Crude Oil Inventories (Nov 28) | |

| Forecast: | Previous: 2.8M | ||

Thursday, Dec 4, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Oct | 4.42B | 3.94B |

| 06:45 | CHF | Unemployment Rate Nov | 3.00% | 3% |

| 09:30 | GBP | Construction PMI Nov | 44.3 | 44.1 |

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | 0.00% | -0.10% |

| 12:30 | USD | Challenger Job Cuts Nov | 175.30% | |

| 13:30 | USD | Initial Jobless Claims (Nov 28) | 220K | 216K |

| 15:00 | CAD | Ivey PMI Nov | 53.6 | 52.4 |

| 15:30 | USD | Natural Gas Storage (Nov 28) | -11B | |

| 23:30 | JPY | Household Spending Y/Y Oct | 1.10% | 1.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Oct | |

| Forecast: 4.42B | Previous: 3.94B | ||

| 06:45 | CHF | Unemployment Rate Nov | |

| Forecast: 3.00% | Previous: 3% | ||

| 09:30 | GBP | Construction PMI Nov | |

| Forecast: 44.3 | Previous: 44.1 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 12:30 | USD | Challenger Job Cuts Nov | |

| Forecast: | Previous: 175.30% | ||

| 13:30 | USD | Initial Jobless Claims (Nov 28) | |

| Forecast: 220K | Previous: 216K | ||

| 15:00 | CAD | Ivey PMI Nov | |

| Forecast: 53.6 | Previous: 52.4 | ||

| 15:30 | USD | Natural Gas Storage (Nov 28) | |

| Forecast: | Previous: -11B | ||

| 23:30 | JPY | Household Spending Y/Y Oct | |

| Forecast: 1.10% | Previous: 1.80% | ||

Friday, Dec 5, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Oct P | 109.4 | 108.6 |

| 07:00 | EUR | Germany Factory Orders M/M Oct | 0.40% | 1.10% |

| 07:45 | EUR | France Industrial Output M/M Oct | -0.10% | 0.80% |

| 08:00 | CHF | Foreign Currency Reserves (CHF) Nov | 725B | |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 F | 0.20% | 0.20% |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 F | 0.10% | 0.10% |

| 13:30 | USD | Personal Income M/M Sep | 0.30% | 0.40% |

| 13:30 | USD | Personal Spending Sep | 0.30% | 0.60% |

| 13:30 | USD | PCE Price Index M/M Sep | 0.30% | |

| 13:30 | USD | PCE Price Index Y/Y Sep | 2.70% | |

| 13:30 | USD | Core PCE Price Index M/M Sep | 0.20% | 0.20% |

| 13:30 | USD | Core PCE Price Index Y/Y Sep | 2.90% | |

| 13:30 | CAD | Net Change in Employment Nov | -7.6K | 66.6K |

| 13:30 | CAD | Unemployment Rate Nov | 7.00% | 6.90% |

| 15:00 | USD | UoM Consumer Sentiment Dec P | 52 | 51 |

| 15:00 | USD | UoM 1-Yr Inflation Expectations Dec P | 4.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Oct P | |

| Forecast: 109.4 | Previous: 108.6 | ||

| 07:00 | EUR | Germany Factory Orders M/M Oct | |

| Forecast: 0.40% | Previous: 1.10% | ||

| 07:45 | EUR | France Industrial Output M/M Oct | |

| Forecast: -0.10% | Previous: 0.80% | ||

| 08:00 | CHF | Foreign Currency Reserves (CHF) Nov | |

| Forecast: | Previous: 725B | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 F | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q3 F | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 13:30 | USD | Personal Income M/M Sep | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 13:30 | USD | Personal Spending Sep | |

| Forecast: 0.30% | Previous: 0.60% | ||

| 13:30 | USD | PCE Price Index M/M Sep | |

| Forecast: | Previous: 0.30% | ||

| 13:30 | USD | PCE Price Index Y/Y Sep | |

| Forecast: | Previous: 2.70% | ||

| 13:30 | USD | Core PCE Price Index M/M Sep | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 13:30 | USD | Core PCE Price Index Y/Y Sep | |

| Forecast: | Previous: 2.90% | ||

| 13:30 | CAD | Net Change in Employment Nov | |

| Forecast: -7.6K | Previous: 66.6K | ||

| 13:30 | CAD | Unemployment Rate Nov | |

| Forecast: 7.00% | Previous: 6.90% | ||

| 15:00 | USD | UoM Consumer Sentiment Dec P | |

| Forecast: 52 | Previous: 51 | ||

| 15:00 | USD | UoM 1-Yr Inflation Expectations Dec P | |

| Forecast: | Previous: 4.50% | ||

Canada GDP rebounds 0.6% qoq in Q3, per capita output also rises

Canada’s economy returned to growth in Q3, expanding 0.6% qoq after contracting -0.5% in Q2. The improvement was driven mainly by a stronger trade balance as imports fell and exports edged higher.

Government-led capital investment also provided support, though business investment was flat. The gains were partially offset by declines in both household and government consumption, alongside slower inventory accumulation.

On a per-capita basis, GDP rose 0.5% qoq after a -0.5% decline the previous quarter—offering some relief amid ongoing concerns about sluggish productivity and population-driven dilution of output.

Monthly data aligned with expectations, with September GDP rising 0.2% mom.

Weekly Focus – Weaker US Data and Euro Area Inflation

In the US, we received more of the delayed data following the end of the government shutdown last week. September retail sales disappointed with retail sales growing only 0.2% m/m below expectations of a 0.4% m/m rise and the control group saw spending decline by 0.1% m/m against an expected rise of 0.3% m/m. Hence, consumers lost some momentum at the end of an otherwise solid third quarter. The conference board consumer confidence indicator recorded a significant decline in November to 88.7 which is the second lowest reading in four years. Expectations for the next six months declined to the lowest level since April as consumers are increasingly concerned about higher prices and a cooling labour market. Overall, the data prints from the US added fuel to the worries surrounding the US economy and markets are now pricing about an 80% chance of an interest rate cut at the FOMC December meeting up from 60% last week.

In the euro area, we received the first inflation prints for November from France, Spain, Germany, and Italy ahead of the aggregate euro area print we get next week. Inflation came in slightly lower than expected with especially services inflation slowing in November. Consensus was looking for a rise in the euro area aggregate print from 2.1% y/y to 2.2% y/y but is likely to stay at 2.1% y/y in line with our initial forecast. Despite the slightly weaker inflation data we do think this changes the outlook for the ECB which still has a strong bias for holding the policy rate steady, which we expect they will do throughout 2026. The ECB September staff projections saw headline inflation at 2.0% in Q4, so inflation is still on track to come in higher than ECB had expected.

In the UK, the Autumn Budget was announced, raising tax rates to post war highs, with the Chancellor asking "ordinary people to pay a little bit more". The GBP strengthened on the release as the government targeted a tighter fiscal policy than markets had been expecting. This provides a bigger buffer against future excess debt issuance although the budget delivered less near-term fiscal tightening than expected. Particularly the absence of VAT hikes paves the way for more near-term easing from the Bank of England in our view, and markets now price above 90% chance of a cut from Bank of England in December.

In Germany, the Ifo Business Climate index for November declined against expectations to 88.1 (cons: 88.5) from 88.4. At the same time, the Q3 GDP growth rate was confirmed at 0.0% q/q and revealed that private consumption fell 0.3% q/q, which is the first quarterly decline recorded since 2023. Hence, the German economy is still stagnating and has yet to recover although expectations for a recovery remain intact. We will likely have to await the effects of fiscal easing to kick in before the economy records a rebound in activity.

Next week focus turns to the US ISM report and ADP employment for November as well as the September PCE inflation. In the euro area, we receive the aggregate inflation print, final PMIs, and the ECB's preferred measure of wage growth for the third quarter. Especially the wage growth will be interesting for the ECB as it is what keeps inflation from falling below target currently. In China focus turns to the PMI report for November which is expected to rebound following a sharp drop in October due to lower exports, likely driven by the threat of 100% US tariffs which never materialised.

Quiet Markets, Technical Outage, and a Dollar Still Stuck at Weekly Lows

Markets were broadly quiet today as holiday conditions dominated trading, with liquidity thinning further after a major technical issue at the Chicago Mercantile Exchange brought several platforms to a halt. The CME said trading had come to a standstill due to a cooling problem at one of its data centers. The outage affected Globex futures and options, EBS foreign-exchange trading and BMD markets, with the exchange warning that price adjustments may take time to filter through once systems fully recover.

In currencies, the Dollar attempted another modest rebound but once again struggled to build momentum. With little fresh data and most investors already looking ahead to next week’s U.S. releases—including ISM manufacturing and services—there was no catalyst to drive a meaningful shift. Many traders may simply prefer to wait even longer for the December 10 FOMC decision before committing to larger directional positions.

As a result, the weekly performance picture remains unchanged. Dollar is still the weakest performer of the week, followed by Yen and Swiss Franc. At the top end, Kiwi continues to lead, supported by a hawkish RBNZ stance, while Aussie and Sterling follow. Euro and Loonie sit squarely in the middle.

In Europe, at the time of writing, FTSE is up 0.27%. DAX is up 0.18%. CAC is up 0.25%. UK 10-year yield is down -0.02 at 4.436. Germany 10-year yield is flat at 2.685. Earlier in Asia, Nikkei rose 0.17%. Hong Kong HSI fell -0.34%. China Shanghai SSE rose 0.34%. Singapore Strait Times rose 0.32%. Japan 10-year JGB yield rose 0.005 to 1.807.

ECB survey shows slight rise in 12-month inflation expectations to 2.8%

The ECB Consumer Expectations Survey for October showed a small uptick in near-term inflation expectations, with the median 12-month outlook rising to 2.8% from 2.7% in September.

Longer-term expectations remained stable, with the three-year horizon unchanged at 2.5% and the five-year measure anchored at 2.2%. Inflation uncertainty was likewise steady, indicating consumers do not see a significant shift in the underlying trend.

On the economic front, consumers grew slightly more optimistic about growth. Expectations for GDP over the next 12 months improved to -1.1%, up from -1.2% previously. However, labor-market expectations worsened. Consumers now expect the unemployment rate to reach 11.0% in 12 months, up from 10.7% in September.

Swiss KOF barometer edges up to 101.7 on stronger demand

Switzerland’s KOF Economic Barometer ticked higher in November, rising from 101.5 to 101.7 and signaling modest improvement in the near-term economic outlook.

KOF noted that the improvement is concentrated on the demand side. Indicator bundles tied to foreign demand and private consumption strengthened, suggesting both external orders and household activity are on firmer footing.

On the production side, however, parts of the economy remain under pressure. Indicators for financial and insurance services, as well as construction, deteriorated, revealing a mixed underlying picture.

Swiss GDP contracts -0.5% in Q3, pharma and chemicals lead decline

Swiss GDP fell -0.5% qoq in Q3, marking a sharp reversal driven almost entirely by the chemical and pharmaceutical sector. After strong momentum earlier in the year, the industry saw output plunge -7.9%, erasing prior gains and dragging the broader economy into contraction.

Authorities noted that the downturn reflects recent volatility in foreign trade. Earlier quarters saw a surge in pharma exports, partly driven by front-loading ahead of U.S. trade-policy changes. Those temporary boosts have now unwound, resulting in a "compensatory decline" that weighed heavily on Q3 activity.

Tokyo core CPI holds at 2.8% in November, inflation pressures still firm

In Japan, Tokyo’s inflation profile showed little moderation in November, with both core CPI and core-core CPI staying at 2.8% yoy. The readings came in slightly firmer than expected, while headline CPI eased just one-tenth to 2.7%. The stability of these measures indicates that underlying inflation momentum remains intact.

Much of the price momentum came from food, where sharp gains continued. The cost of rice surged 38.5% yoy, coffee beans rose 63.4%, and chocolate jumped 32.5%, reflecting broad price pressures across essential and discretionary categories.

Meanwhile, goods inflation climbed 4.0% yoy. Services inflation eased only marginally to 1.5% from 1.6%.

Japan industrial production surges 1.4% mom in October on auto rebound, but fluctuation to continue

Japan’s industrial production rose 1.4% mom in October, sharply beating expectations of a -0.6% decline. The rebound was driven primarily by a 6.6% jump in motor vehicle output, a sector benefiting from the U.S. tariff rate on Japanese cars being reduced to 15% from 27.5% in mid-September. The improvement highlights how quickly Japanese automakers responded once tariff uncertainty eased.

However, the forward outlook remains soft. Based on its manufacturer survey, METI expects output to fall -1.2% in November and contract a further -2.0% in December. Despite October’s upside surprise, the ministry kept its overall assessment unchanged, saying industrial production “fluctuates indecisively” amid continued uncertainty at home and abroad.

Retail sales also surprised to the upside, rising 1.7% yoy versus expectations of 0.8%. The strength suggests domestic demand remains more resilient than many feared, even as the industrial sector continues to face uneven momentum.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1578; (P) 1.1596; (R1) 1.1615; More…

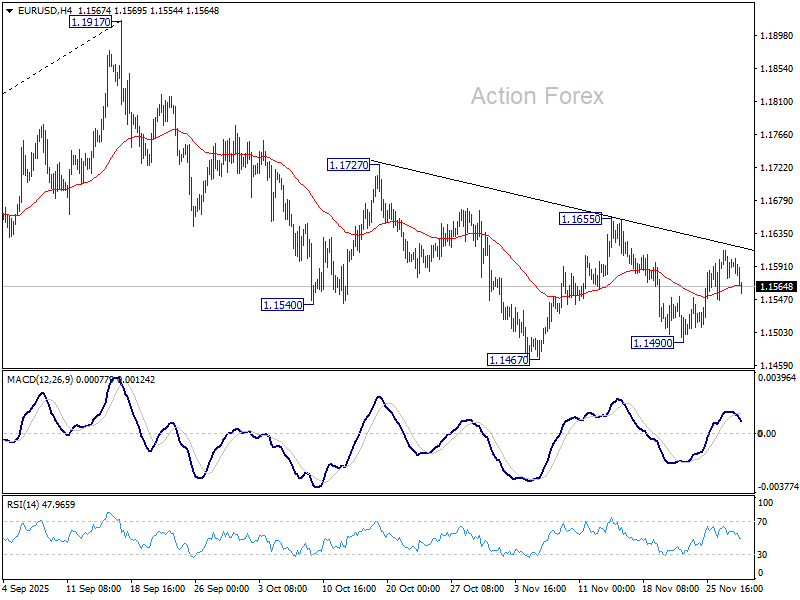

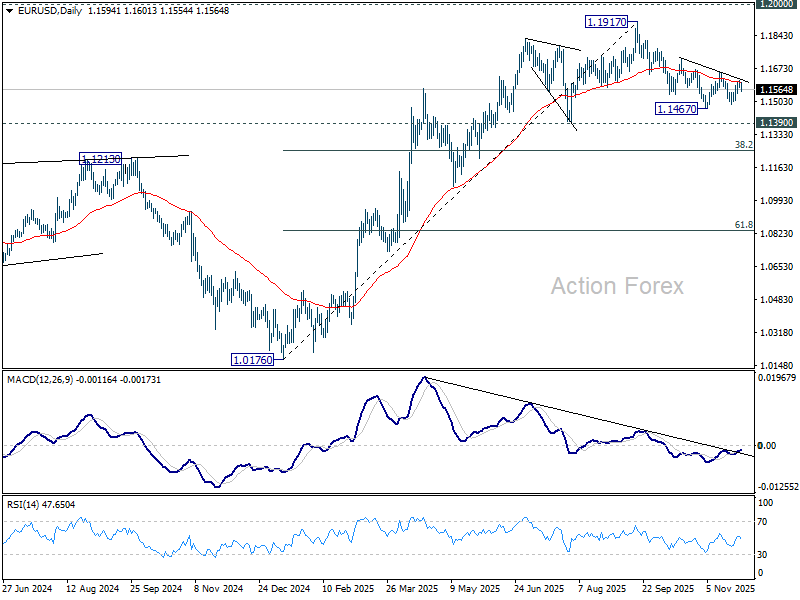

Intraday bias in EUR/USD remains neutral for the moment, as range trading continues. Further decline is expected with 1.1655 resistance intact. On the downside, below 1.1490 and 1.1467 will resume the whole decline from 1.1917 high. Next targets are 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252. However, decisive break of 1.1655 will argue that fall from 1.1917 has completed, and turn bias back to the upside for 1.1727 resistance and above.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1578; (P) 1.1596; (R1) 1.1615; More…

Intraday bias in EUR/USD remains neutral for the moment, as range trading continues. Further decline is expected with 1.1655 resistance intact. On the downside, below 1.1490 and 1.1467 will resume the whole decline from 1.1917 high. Next targets are 1.1390, and then 38.2% retracement of 1.0176 to 1.1917 at 1.1252. However, decisive break of 1.1655 will argue that fall from 1.1917 has completed, and turn bias back to the upside for 1.1727 resistance and above.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1328) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

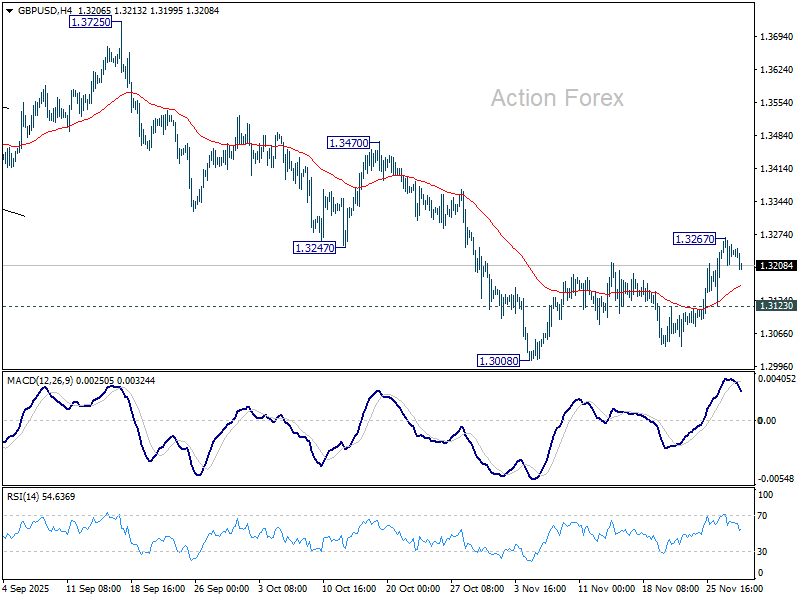

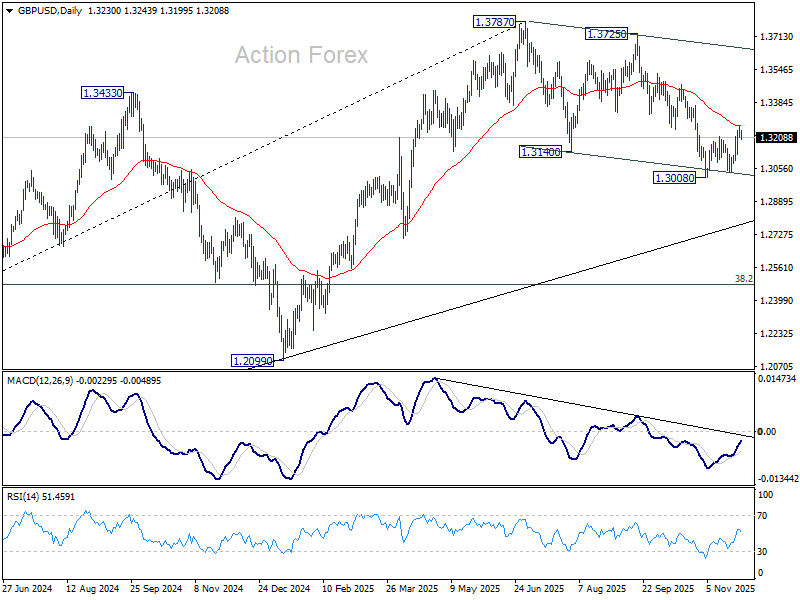

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3210; (P) 1.3240; (R1) 1.3270; More...

Intraday bias in GBP/USD is turned neutral with current retreat. On the upside, break of 1.3267 will resume the rebound from 1.3308. Sustained trading above 55 D EMA should confirm that fall from 1.3787 has completed as a correction. Further rise should then be seen to 1.3725/3787 resistance zone. Nevertheless, break of 1.3123 minor support will revive near term bearishness, and bring retest of 1.3008.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

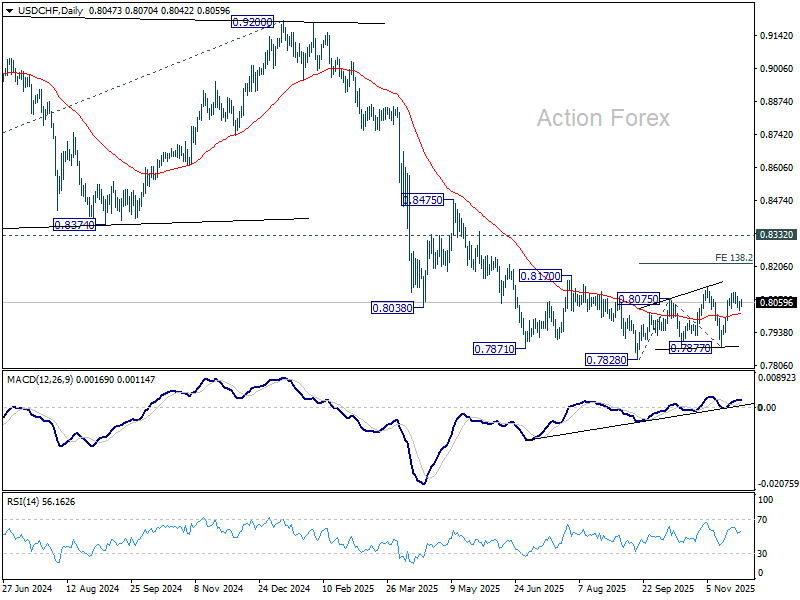

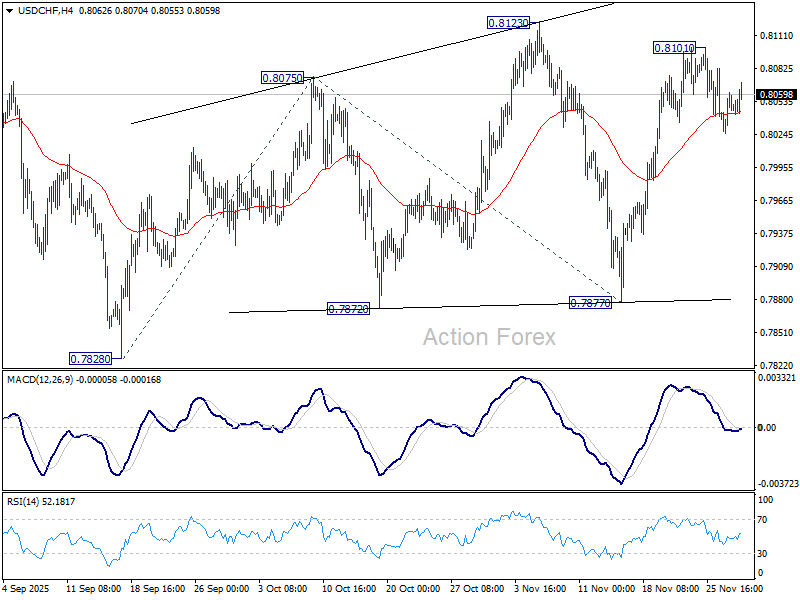

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8027; (P) 0.8048; (R1) 0.8069; More…

Intraday bias in USD/CHF remains neutral for the moment. Outlook is unchanged that current rise from 0.7877 is still seen as the third leg of the corrective pattern from 0.7828 low. Above 0.8101 will target 0.8123 resistance, and then 138.2% projection of 0.7828 to 0.8075 from 0.7877 at 0.8218. However, sustained break of 55 D EMA (now at 0.8015) will bring deeper fall back to 0.7877 support instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).