Sample Category Title

China RatingDog PMI slips into contraction at 49.9 as production, demand stall

China’s RatingDog PMI Manufacturing fell back into contraction in November, dropping from 50.6 to 49.9 and missing expectations of 50.5. Founder Yao Yu said both production and demand slowed to levels near stagnation. While new export orders improved, the pickup was not enough to offset sluggish domestic demand, leaving overall new orders almost flat.

The loss of momentum weighed on hiring, purchasing activity, and inventory decisions. Manufacturers scaled back their workforce and procurement while adopting more cautious stock management. Inventories of raw materials and finished goods both declined, with the average inventory level hitting its lowest point in nearly three years. Also, raw material inventories fell for the first time in seven months. Pricing indicators also highlighted pressure on margins, with input prices rising while output prices continued to fall.

Official data released over the weekend offered mixed signals. NBS PMI Manufacturing edged up from 49.0 to 49.2, in line with expectations, hinting at modest stabilization. However, Non-Manufacturing PMI slipped from 50.1 to 49.5—the sector’s first contraction since December 2022—showing that weakness is now spreading beyond factories and reinforcing concerns about China’s softer near-term growth path.

Ueda signals December hike debate as BoJ reviews wage momentum

BoJ Governor Kazuo Ueda said the board will actively debate the “pros and cons” of raising interest rates at its December 18–19 meeting. He emphasized that the bank is now focused on whether firms’ "active wage-setting behavior" will persist, calling it a key determinant of the timing of the next hike.

Ueda noted that even with an increase, real interest rates would remain deeply negative, meaning policy would still be accommodative—more akin to “easing off the accelerator” than “applying the brakes.”

On the Yen, Ueda said Monday that further weakness is likely to push consumer inflation higher, a development that requires close monitoring when setting policy.

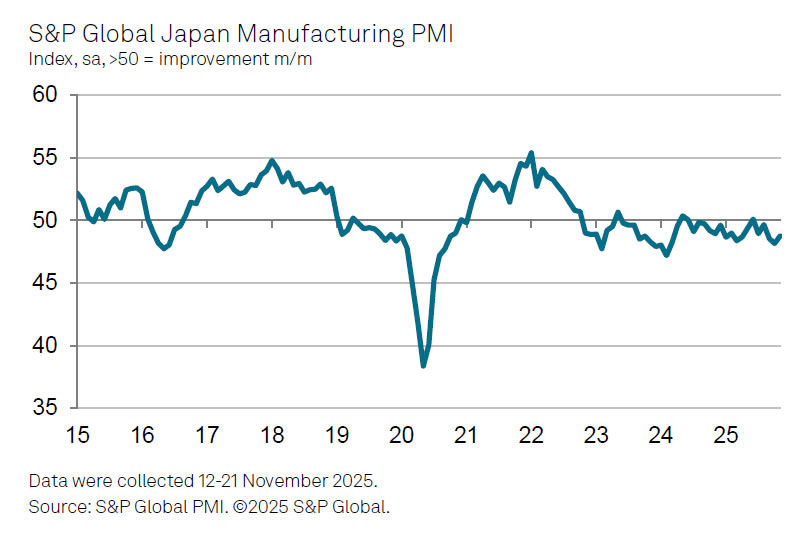

Japan’s PMI manufacturing finalized at 48.7, contraction eases and confidence hits year high

Japan’s Manufacturing PMI was finalized at 48.7 in November, slightly above October’s 48.2, but still pointing to contraction. S&P Global’s Annabel Fiddes noted that conditions remained challenging, with firms reporting “another solid decline” in new business as demand stayed weak across both domestic and external markets..

Despite the soft order flow, sentiment improved meaningfully. Business confidence rose to the strongest level since the start of the year, supported by expectations that market conditions will begin stabilizing in 2026. That optimism translated into a further rise in employment, with firms hiring in anticipation of a longer-term recovery in activity.

A key focus now shifts to the government’s newly announced stimulus package—the largest since the pandemic—which aims to accelerate investment in strategic sectors such as AI. Its success in lifting demand will be critical in determining whether the manufacturing sector can move out of contraction after a long period of subdued momentum.

S&P 500 (SPX) Elliott Wave: Buying the Dips in a Blue Box

Hello fellow traders,

As our members know we have had many profitable trading setups recently. In this technical article, we are going to present another Elliott Wave trading setup we got in S&P 500 Index . SPX completed this correction precisely at the Equal Legs zone, referred to as the Blue Box Area. In the following sections, we will delve into the specifics of the Elliott Wave pattern observed , discuss the trading setup and present targets.

SPX Elliott Wave 4 Hour Chart 11.18.2025

The current view suggests that SPX is forming a Double Three correction (WXY red) . The price action is reaching blue box at 6577.688-6395.668 where we are looking to re-enter as buyers. We recommend members to avoid selling SPX . As the main trend remains bullish, we anticipate at least a 3-wave bounce from this Blue Box area. Once the price touches the 50 fibs against the X red connector, we’ll make positions risk-free and set the stop loss at breakeven and book partial profits. On other hand, breaking below the 1.618 Fibonacci extension level at 6395.668 would invalidate the trade.

Official trading strategy on How to trade 3, 7, or 11 swing and equal leg is explained in details in Educational Video, available for members viewing inside the membership area.

Quick reminder on how to trade our charts :

Red bearish stamp+ blue box = Selling Setup

Green bullish stamp+ blue box = Buying Setup

Charts with Black stamps are not tradable. 🚫

SPX Elliott Wave 1 Hour Chart 11.27.2025

The index has found buyers in the anticipated Blue Box. SPX is now showing a solid bounce from this key Buying Zone. The current reaction has reached the 50% Fibonacci level relative to the X‑red connector. As a result, any long positions initiated from the Blue Box should now be considered risk-free. Our stop loss has been moved to breakeven, and we’ve already locked in partial profits.

We consider the correction completed at the 6523 low. As long as SPX remains above this level, the index has potential to target the 7013+ area next.

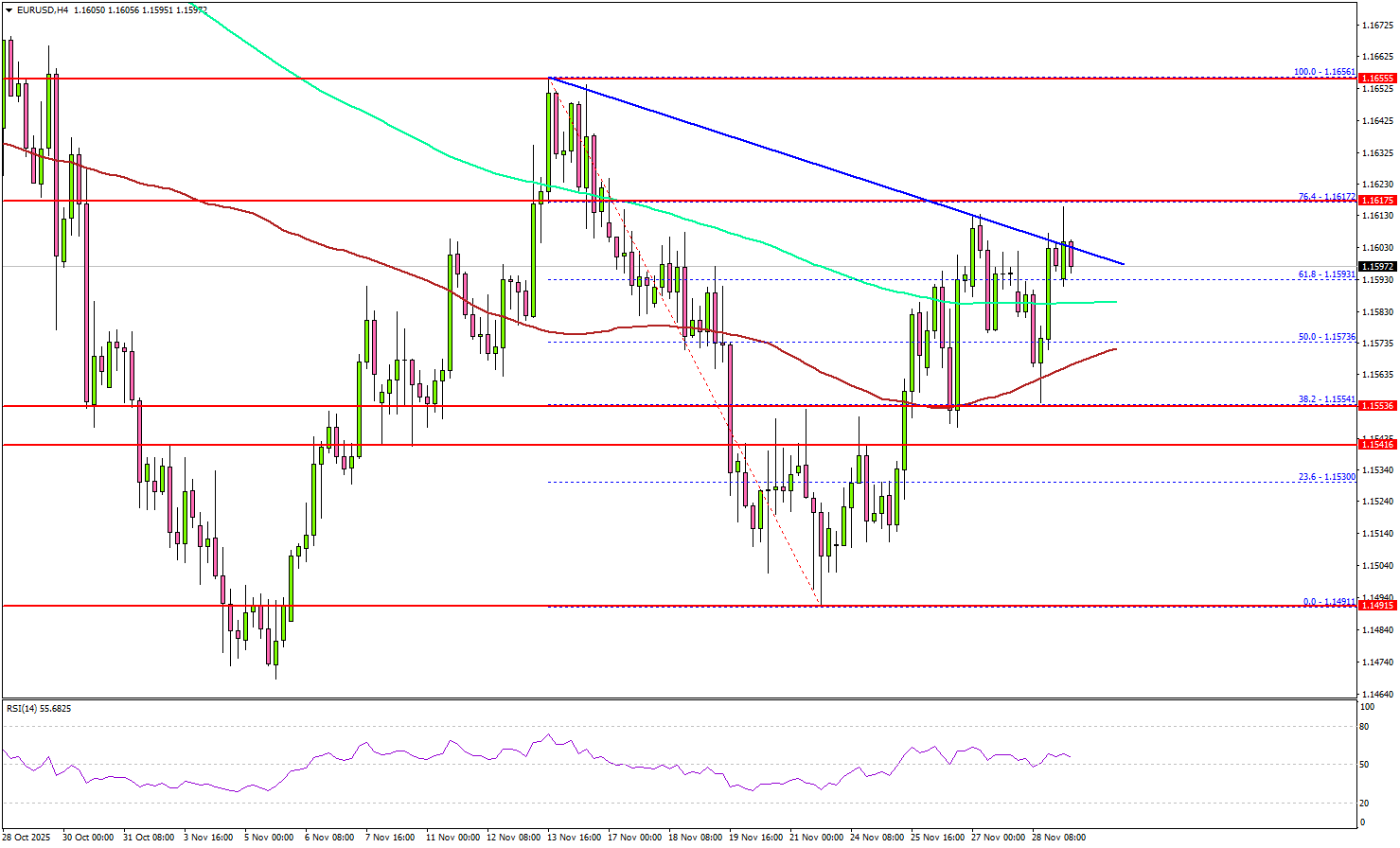

EUR/USD Hits Heavy Resistance, Sparking Questions Over Bullish Continuation

Key Highlights

- EUR/USD started a decent increase above the 1.1550 resistance.

- A key bearish trend line is forming with resistance at 1.1600 on the 4-hour chart.

- GBP/USD started a recovery wave above 1.3200.

- USD/JPY is correcting gains and might test 155.00.

EUR/USD Technical Analysis

The Euro formed a base and climbed above 1.1520 against the US Dollar. EUR/USD even cleared the 1.1550 resistance before the bears appeared.

Looking at the 4-hour chart, the pair climbed above the 50% Fib retracement level of the downward move from the 1.1656 swing high to the 1.1491 low. The pair settled above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

However, the bears are protecting gains above 1.1600. There is also a key bearish trend line forming with resistance at 1.1600. The first key hurdle sits at 1.1610 and the 76.4% Fib retracement level of the downward move from the 1.1656 swing high to the 1.1491 low.

The next area of interest for the bulls could be 1.1650. Any more gains could set the pace for a steady increase toward 1.1700.

On the downside, there is key support at 1.1575. The next support is 1.1550, below which the pair could start a steady decline to 1.1500.

Looking at GBP/USD, the pair remains in a positive zone, but it must surpass 1.3250 to continue higher in the near term.

Upcoming Key Economic Events:

- ECB's Nagel speech.

- Fed's Chair Powell speech.

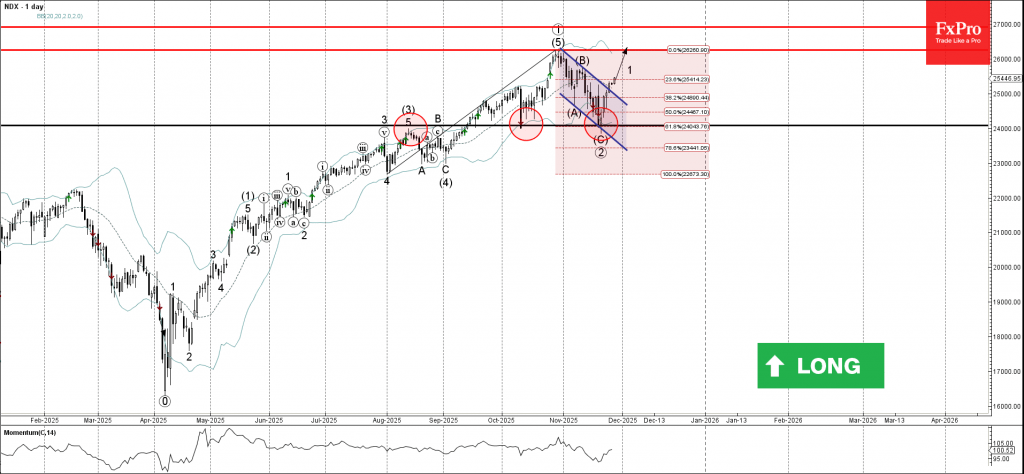

Nasdaq-100 Wave Analysis

Nasdaq-100 index: ⬆️ Buy

- Nasdaq-100 broke resistance zone

- Likely to rise to resistance level 0.3000

Nasdaq-100 index recently broke the resistance zone between the round resistance level 25000.00 and the resistance trendline of the daily down channel from October (which encloses the previous primary ABC correction 2).

The breakout of this resistance zone accelerated the active short-term impulse wave 1 of the intermediate impulse wave (1) from November.

Given strong daily uptrend, Nasdaq-100 index can be expected to rise to the next resistance level 26250.00 (former top of wave (5) from October).

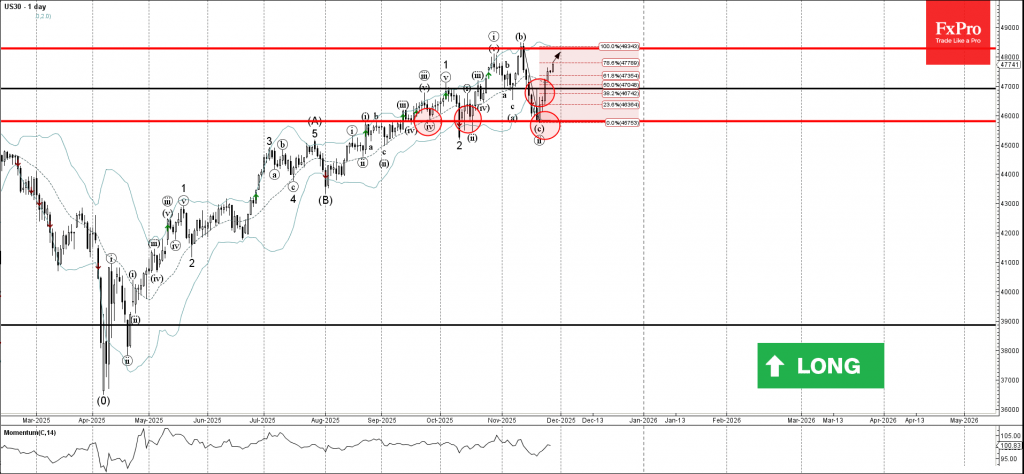

Dow Jones Wave Analysis

Dow Jones: ⬆️ Buy

- Dow Jones broke resistance zone

- Likely to rise to resistance level 48300.00

Dow Jones index recently broke the resistance zone between the resistance level 47000.00 and the 50% Fibonacci correction of the downward impulse c from the start of November.

The breakout of this resistance zone accelerated the active short-term impulse wave (iii).

Given strong multi-month uptrend, Dow Jones index can be expected to rise to the next resistance level 48300.00, which stopped the previous waves i and b.

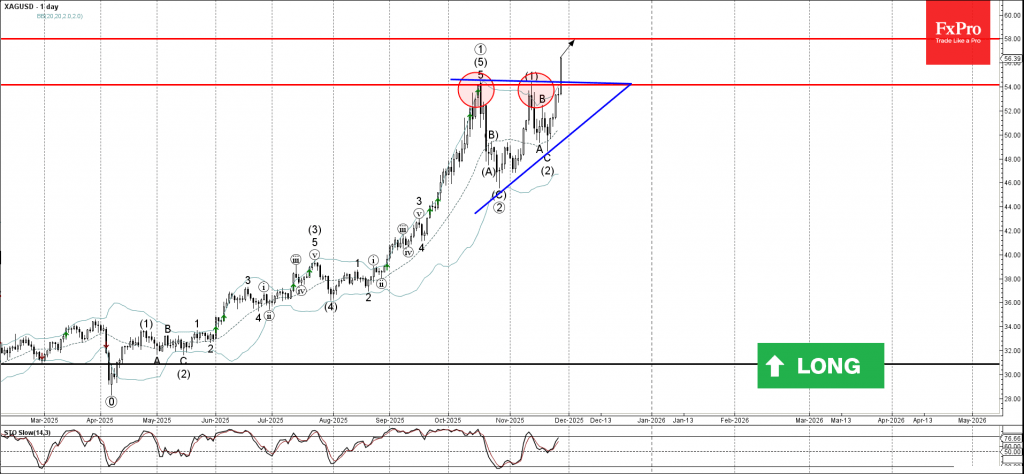

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver broke key resistance level 54.00

- Likely to rise to resistance level 58.00

Silver recently broke the resistance zone between the key resistance level 54.00 (which stopped the previous sharp impulse wave (5) in October) and the resistance trendline of the ascending triangle from October.

The breakout of this resistance zone accelerated the active intermediate impulse wave (3).

Given the clear daily uptrend, Silver can be expected to rise to the next resistance level 58.00, target price for the completion of the active impulse wave (3).

The Week Ahead of the December FOMC – Markets Weekly Outlook

Week in review – Were the past few weeks just a farce?

Markets rebounded as if nothing happened – Nvidia (NVDA) earnings came to save the trend as the narrative was switching to a general AI-Bubble scare.

The earnings brought back confidence into the Market, and this feeling got exacerbated by a brand new dovish repricing after last Friday's speech by NY Fed President John Williams, who signaled his "support for a rate cut in the near-term".

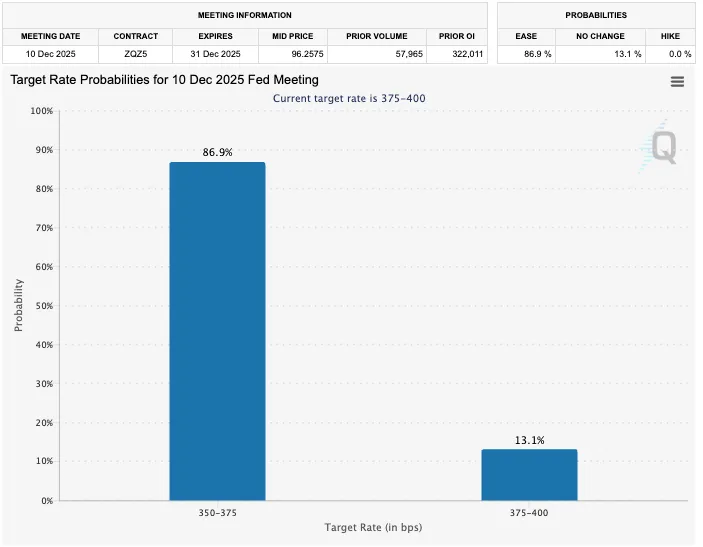

Pricing for the December 10 FOMC Meeting – Source: FedWatch Tool

This sentiment was further confirmed by not-so-hot (late) September US PPI and Retail Sales and honestly weak Weekly Private Jobs data from ADP.

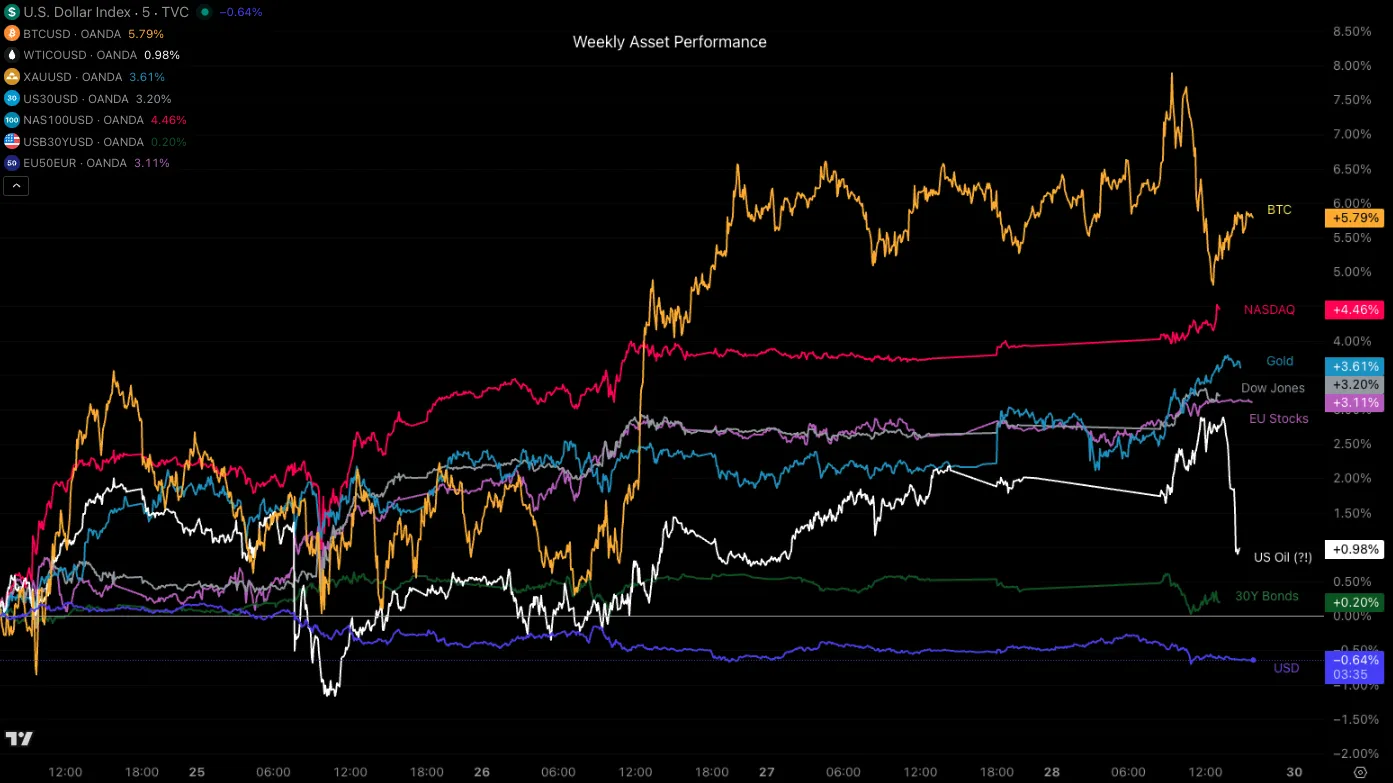

Cryptos bounced back timidly, with Bitcoin regaining the $92,000 level but rejecting it in the early afternoon, but the most impressive really were the Metals, all back to their cycle highs, and Stocks which almost erased their entire 3-week drop in the matter of a few days, with all US Indices posting gains today to close an already strong week.

Volumes have been low throughout the week, a classic of Thanksgiving trading.

Therefore, some of these moves might get retested as large traders coming back from their breaks may move prices quite aggressively – Things will get confirmed Monday.

Weekly Performance across Asset Classes

Weekly Asset Performance – What's going with Oil? November 28, 2025 – Source: TradingView

In terms of Central Bank communication, not much changed except for a very divided Bank of Japan, leading to another, less ardent Yen selloff.

A December rate hike becomes more and more probable (now priced at roughly 56%) as yesterday's Tokyo inflation came in hotter than expected, keeping pressure on the BoJ to normalize policy.

But markets did receive some better geopolitical headlines: The light is at the end of the tunnel for the Ukraine-Russia conflict, with talks accelerating.

Steve Witkoff, US Envoy, will travel to Moscow next week to discuss the revised peace proposal, and Zelenskyy is expecting to discuss with the US "in the near future" as negotiations progress on a new framework.

The Week Ahead – Final stretches of Economic data before the December FOMC

Asia Pacific Markets – All eyes on Bank of Japan's Ueda and the Australian GDP

Both the Australian and New Zealand Dollars have bounced higher to close this calm FX week, with Aussie and Kiwi data still tenace (particularly for Australia).

NZD/USD posts a major reversal higher after the RBNZ Cut – Technical Outlook

AUD will be on the spotlight as the latest CPI report for Australia came red-hot (3.8% y/y), with hopes for cuts flying away from the continuous strong inflation numbers.

So keep an eye on the GDP report for Australia, releasing Wednesday evening in between PMI and Trade Balance releases.

The Yen, which hasn't grabbed enough attention in the past few months, will once again also be at the center of the scene as the week won't even have begun for North Americans.

Bank of Japan Governor Ueda will appear at a Business Leaders conference in Nagoya Sunday evening, with comments regarding his recent meeting with PM Takaichi and the blushing Japanese CPI.

Europe and UK Markets – Inflation reports and EU data flood

Markets are turning the page on the UK Budget which had taken quite some attention throughout the FX space and brought some renewed demand for the Pound, back above the 1.32 Level against the US Dollar.

Inflation data throughout the European continent will put both the EUR and CHF in action.

The European HICP is taking place on Tuesday at 6:00 A.M., while the Swiss inflation (closely watched for the next SNB decision) releases on Wednesday at 3:30 A.M.

The Swiss National Bank has been reflecting on a potential cut below 0% if Swiss inflation remains subdued, once again struck with small deflation in the past months. This has led a fair weakening of the CHF.

For the rest, a lot of growth Data will also be released for the Eurozone, with their PPI, Retail Sales and GDP going back to back to back towards the end of the week.

North America – Jerome Powell, Final Data for the Fed and a return of Canadian Dollar strength?

Canada has finally began to show upside to their ever-weakening growth data, posting a gigantic 2.6% (exp at 0.5%) Annualized Q3 GDP this morning (!), the previous was at -1.8% just to put things in perspective.

This combined with pre-occuring US Dollar weakness has taken USD/CAD to new lows to close the Thanksgiving week.

With American traders coming back to their screens, we should see if this week's flows get anchored. Expect hesitation until Friday's PCE release.

For other data points, US and Canadian PMIs will occupying NA traders from Monday to Thursday. US-Canada talks are still in a limbo.

Of course, don't forget the Monthly ADP Private Jobs release on Tuesday, University of Michigan Consumer Sentiment and Canadian Employment Data releasing Friday morning.

Monday morning should be active for Markets with Fed's Powell participating in a panel discussion – Nevertheless, the FOMC is in a blackout period so he shouldn't speak much regarding the following week's decision.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (High-tier data only)

Safe Trades and enjoy your weekend!