Sample Category Title

EUR/USD Holds Ground Amid Firm Focus on Fed Policy

The EUR/USD pair retreated to 1.1612 on Tuesday, pulling back from a recent two-week high. The catalyst for the move was a significant repricing of US interest rate expectations following weak manufacturing data. The ISM Manufacturing Index confirmed a ninth consecutive month of contraction, with the pace of decline the fastest in four months.

This data solidified market expectations for a Federal Reserve rate cut. Futures markets now imply an 88% probability of a 25-basis-point reduction at next week's FOMC meeting.

In related news, President Donald Trump announced he has selected a candidate for the next Fed Chair. Media reports suggest the leading contender is Kevin Hassett, the current head of the White House National Economic Council.

Investor attention is now focused on an upcoming speech by current Chair Jerome Powell later today, which may offer further clues on the Fed's policy trajectory.

Technical Analysis: EUR/USD

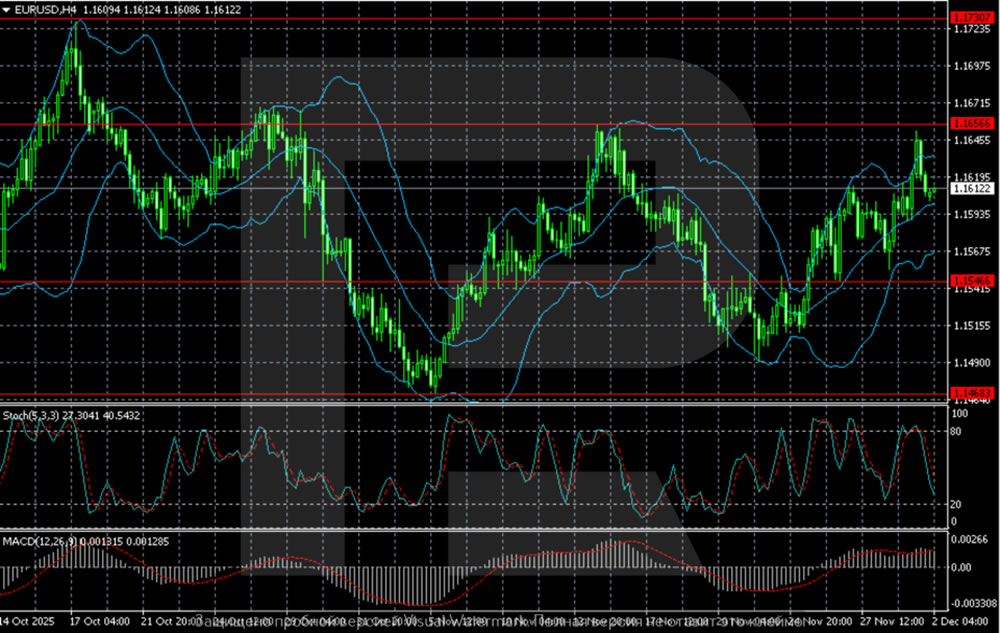

H4 Chart:

On the H4 chart, EUR/USD continues to trade within an established ascending channel. The pair is currently testing a key resistance zone at 1.1655, where buying momentum has met significant selling pressure. A decisive breakout above this level would open the path towards the next major resistance at 1.1730.

The Stochastic Oscillator is rising from the middle zone, indicating sustained bullish momentum without overbought conditions. The MACD remains above its zero line, maintaining a stable, albeit weak, buy signal. Conversely, a break and close below the key support at 1.1545 would signal a deeper correction, likely targeting the lower boundary of the current range near 1.1468.

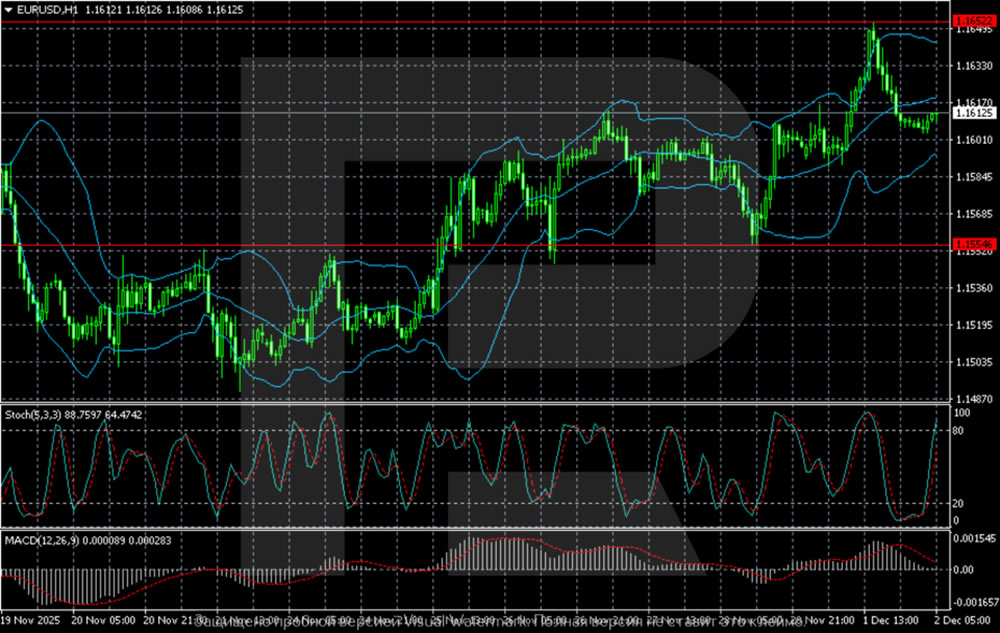

H1 Chart:

On the H1 chart, the pair is undergoing a correction after being rejected from local resistance at 1.1652. Buyers are currently defending the price above the middle Bollinger Band, suggesting short-term bullish control remains intact.

The Stochastic Oscillator is in overbought territory (above 80) and is turning down, pointing to a near-term corrective pullback. However, the MACD remains in positive territory, supporting the broader upward bias. This technical picture suggests a brief downward pause is likely, with a potential retest of support in the 1.1600–1.1585 zone. A successful hold above this area would increase the probability of a fresh upward impulse, targeting a renewed test of 1.1652 and an eventual push towards 1.1700.

Conclusion

EUR/USD remains confidently bid, supported by growing expectations of Fed easing. While a short-term technical correction is underway, the broader structure on both the H4 and H1 charts remains constructive. The key for continued upside is a successful defence of the 1.1600–1.1585 support zone. A break above 1.1655 would be a significant bullish confirmation, while a failure to hold support could trigger a deeper pullback towards 1.1545.

S&P 500 Index: Early December Chart Analysis

December is traditionally a favourable month for the S&P 500 (US SPX 500 mini on FXOpen):

→ Since the 1950s, December has ended higher in over 70% of years.

→ Average monthly gain is around +1.0%.

Will the index rise in 2025? Much depends on the Federal Reserve meeting on 10 December, as well as other factors, including geopolitical developments. Interest is also piqued by an upcoming statement from Trump at the White House (today, 22:00 GMT+3), though the topic remains undisclosed.

Technical Analysis of the S&P 500 Chart

Demand-side perspective:

→ The rebound from November’s low was aggressive, rising roughly +5% in 10 days.

→ Price climbed above the blue trendline that has acted as support since summer.

→ The recent dip (marked by the red trajectory) could be a temporary correction, forming a Bull Flag pattern.

Supply-side perspective:

→ The red trajectory has not yet been breached.

→ Recent price movements show a strong bearish Head and Shoulders pattern, along with signs of a Quasimodo formation, emerging around the attempt to break the upper boundary.

In the short term, the former resistance at 6785 may now act as support. Overall, the S&P 500 (US SPX 500 mini on FXOpen) is likely to adopt a wait-and-see stance, adjusting as economic news, delayed by the government shutdown, is released.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

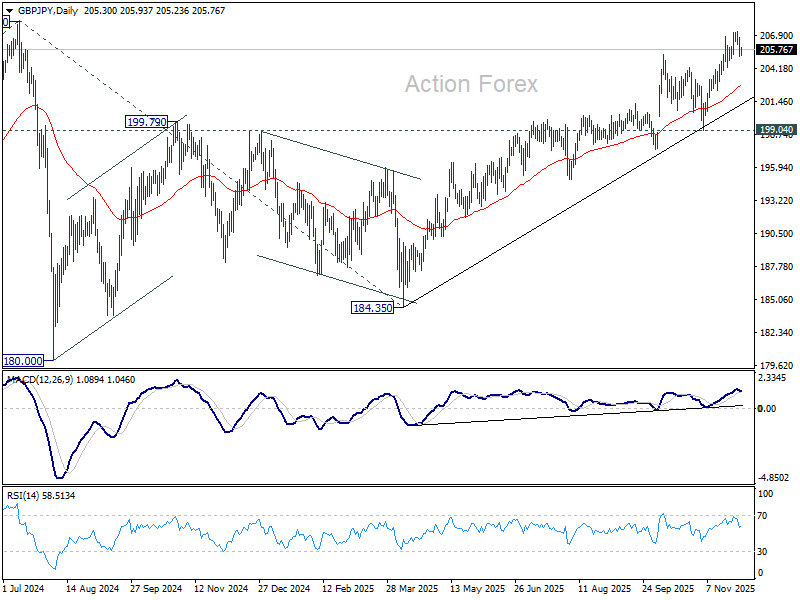

GBP/JPY Daily Outlook

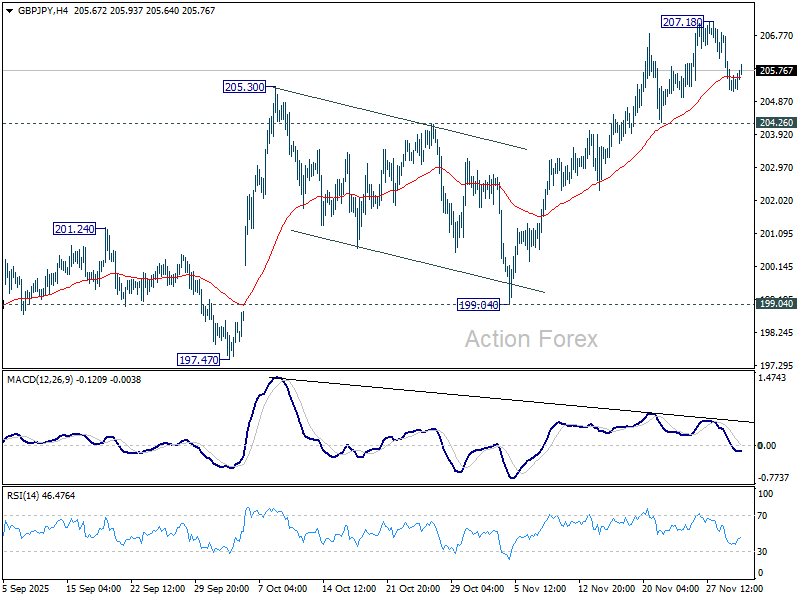

Daily Pivots: (S1) 204.83; (P) 205.80; (R1) 206.40; More...

Intraday bias in GBP/JPY stays neutral and more consolidations could be seen below 207.18. Further rally is expected as long as 204.26 support holds. Above 207.18 will resume larger rise to retest 208.09 high. Firm break there will confirm long term up trend resumption. However, decisive break of 204.26 will bring deeper pullback to 55 D EMA (now at 202.81).

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 199.04 support will dampen this view and extend the corrective pattern with another fall.

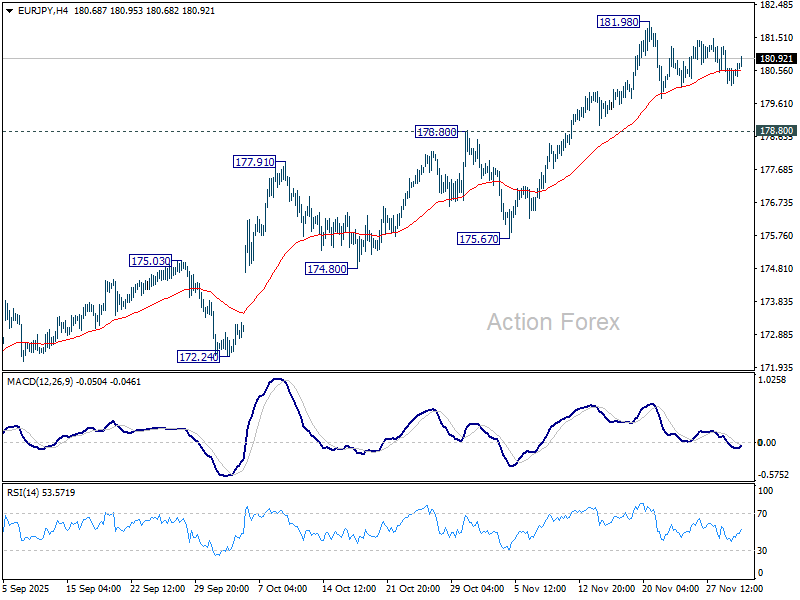

EUR/JPY Daily Outlook

Daily Pivots: (S1) 180.04; (P) 180.60; (R1) 181.07; More...

Intraday bias in EUR/JPY remains neutral as consolidations from 181.98 is still extending. While deeper retreat cannot be ruled out, downside should be contained by 178.80 resistance turned support to bring another rally. On the upside, break of 181.98 will target 100% projection of 161.06 to 173.87 from 171.09 at 183.90 next. However, firm break of 178.80 will argue that deeper correction is already underway towards 55 D EMA (now at 177.48).

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Outlook will continue to stay bullish as long as 55 W EMA (now at 169.45) holds, even in case of deep pullback.

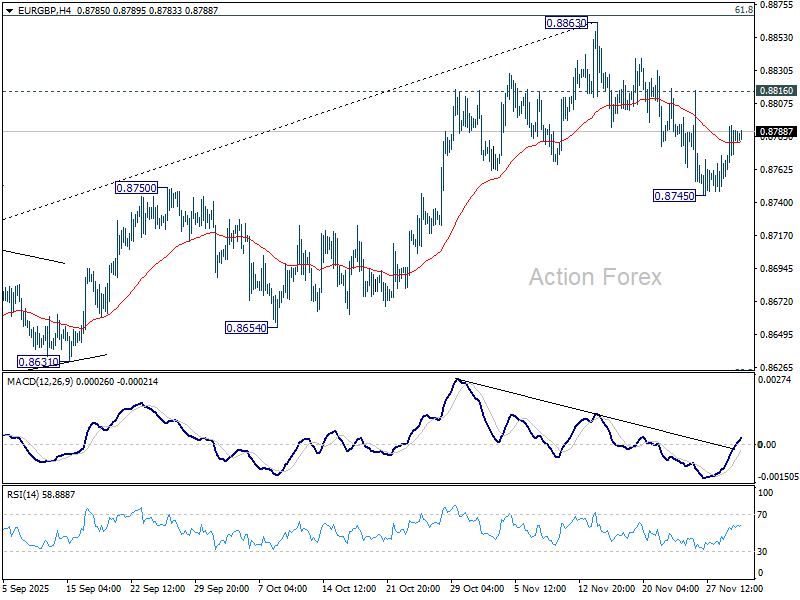

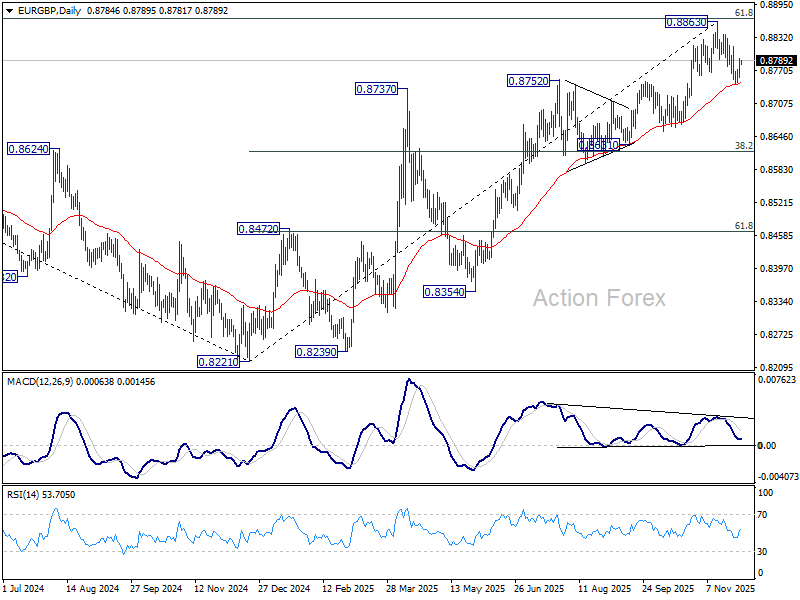

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8766; (P) 0.8780; (R1) 0.8800; More…

Intraday bias in EUR/GBP stays neutral at this point. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 0.745) will solidify the case of bearish reversal. Deeper fall should then be seen to 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618). However, break of 0.8816 minor resistance will bring stronger rebound to retest 0.8863 high instead.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8600) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

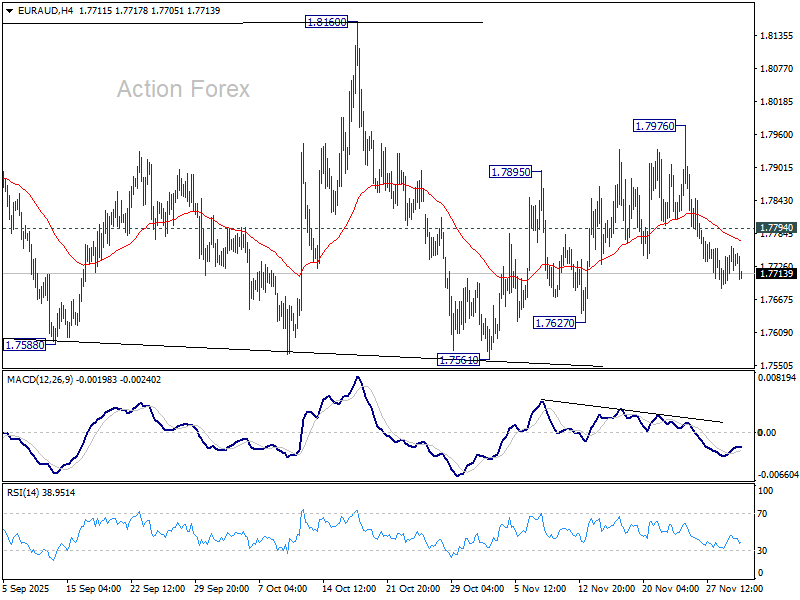

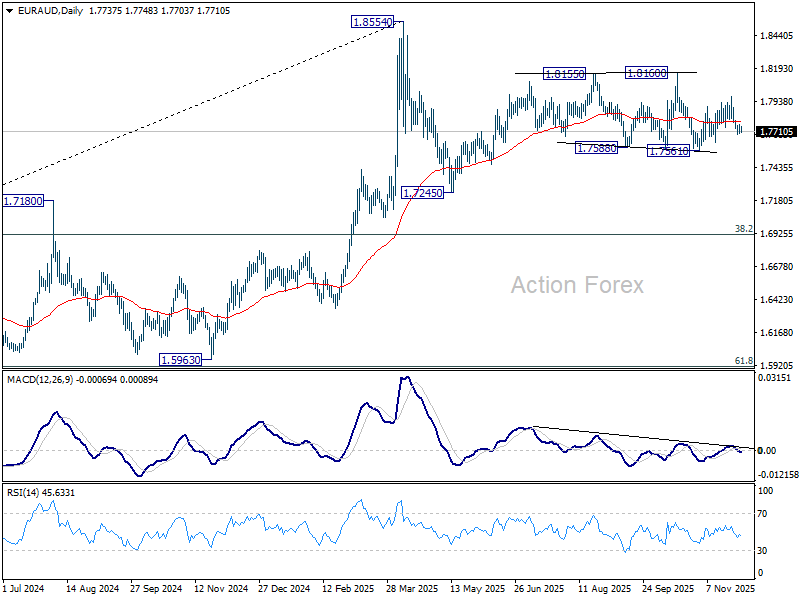

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7709; (P) 1.7737; (R1) 1.7768; More...

For now, further fall remains in favor in EUR/AUD for 1.7627 support. Firm break there will argue that decline from 0.8160 is ready to resume through 1.7561 support next. On the upside, above 1.7794 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Sustained break of 55 W EMA (now at 1.7426) will suggest that it's correcting the whole rally from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922. Nevertheless, strong rebound from 55 W EMA will likely bring resumption of the up trend sooner.

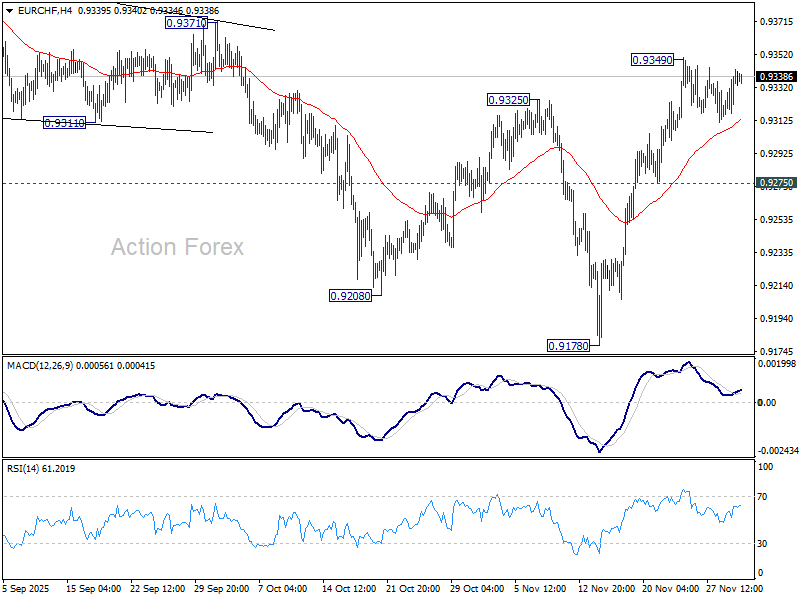

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9325; (P) 0.9335; (R1) 0.9353; More....

Intraday bias in EUR/CHF stays neutral as consolidations continue below 0.9349 temporary top. As noted before, fall from 0.9660 could have completed at 0.9178, on bullish convergence condition in D MACD. Above 0.9349 will resume the rise from 0.9178, and target 0.9452 resistance next. However, break of 0.9275 will turn bias back to the downside for 0.9178 low instead.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9371). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish in case of strong rebound.

Solid 10-Yr Japanese Bond Auction Eases Sell-off with Treasuries

Markets

Bonds suffered in a global bear steepening move yesterday. Bank of Japan’s Ueda was widely considered to have started the fire by giving a clear nod towards a December rate hike. At 0.75% (from 0.5% today), Ueda added, the BoJ would also indicate how far the normalization cycle could go. And by comparing another hike by lifting the foot of the accelerator rather than hitting the brakes, markets soon concluded that December wouldn’t be the final move, considering that inflation remains well above the 2% target. Japanese yields rose with the 2-yr yield topping 1% for the first time since 2008 and long(er) tenors either testing or hitting new (record) highs. Japanese yields are looking ever more attractive and increasingly offer an alternative to higher-yielding assets such as Treasuries. Along with the expected heavy corporate issuance this week (and month) it helps explain core bonds losing ground yesterday. US rates rallied between 4 bps (2-yr) to 7.3 bps (30-yr). The US money market segment (<1 year) grabs some attention with interbank rates such as the SOFR being fixed (on Friday) at rates well above the Fed’s upper bound target (4%). US banks yesterday at the same time drew a substantial amount from the Fed’s repo facility ($26 bln), indicating some kind of funding pressures going into the new month. German yields added 3.5-6.2 bps. The 10-yr European swap rate ended at a 1.5 year high, the 30-yr at a 2-yr (+) high. The Japanese yen unsurprisingly outperformed on FX markets but finished off the intraday highs. USD/JPY dropped as low as 154.67 before recovering to 155.46 into the close. The euro lost most of its upper hand against the USD when US investors began to join. EUR/USD pared earlier gains to 1.165 to around 1.161. Sterling slid to EUR/GBP 0.8786.

We’re keen to find out how yesterday’s opening moves to the week play out further. A solid 10-yr Japanese bond auction this morning for now eases the sell-off with Treasuries and Bunds steading too. Asian stock markets trade mixed, offering little guidance for the European open later (futures flat). The underling market dynamics in any case won’t be derailed by the economic calendar. Based on last week’s national releases, European inflation figures should more or less match the bar set at -0.3% m/m and 2.1% y/y for headline CPI. Core inflation is expected at 2.4%. Implications for the ECB are close to zero: president Lagarde just last week reiterated the current 2% is the correct level to have in place. Yesterday’s US manufacturing ISM barely made a dent in markets. It further slipped into contraction territory (48.2 from 48.7) with new orders and employment details unconvincing either. But markets are more interested in tomorrow’s services edition as well as other releases including the ADP job report and PCE deflators. The OECD’s new economic outlook is worth mentioning too.

News & Views

The British Retail Consortium’s (BRC) shop price index showed prices falling for a second consecutive month. Overall prices fell by 0.1% M/M with lower food prices (-0.3% M/M) again responsible for the setback. Non-food prices were stable compared with October. On an annual level, it’s still the other way around. The overall 0.6% Y/Y increase (down from 1% in October) is due to higher food prices compared to November 2024 (+3% Y/Y vs +3.7% in October; slowest pace since May 2025). Non-food price deflation went from -0.4% Y/Y to -0.6%. BRC CEO Dickinson said that retailers are hoping that consumer confidence rebounds in this crucial trading period with Budget uncertainty behind us. After kicking off Black Friday deals earlier than expected, they will continue doing everything to keep prices down going into Christmas. 2026 looks less bright with headwinds including rising employment costs and consequences for both prices and consumer confidence.

Multiple officials confirmed that the ECB won’t provide a backstop for a €140bn loan (against frozen Russian central bank assets) to cover Ukraine’s 2026-2027 financing needs. The ECB concluded that the European Commission proposal violated its mandate (prohibiting monetary financing). The EC wanted EU countries to provide state guarantees to ensure the repayment risk of the loan is shared. The ECB would have a role as a lender of last resort to Euroclear bank to mitigate any liquidity risk. The EC is now looking for other solutions, but almost all of them include (a way of) joint EU debt issuance.

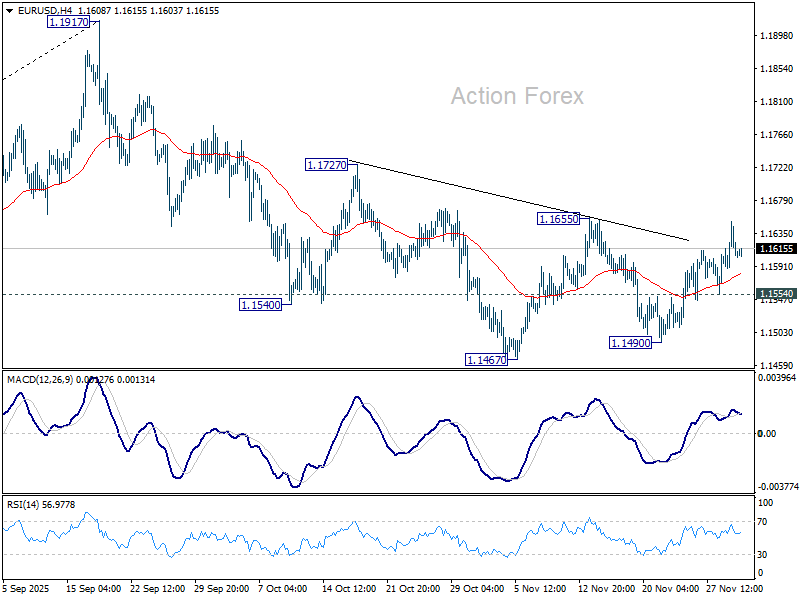

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1582; (P) 1.1617; (R1) 1.1644; More…

EUR/USD is still staying in range below 1.1655 and intraday bias remains neutral. On the upside, decisive break of 1.1655 will complete a head and should bottom pattern (ls: 1.1540, h: 1.1467, rs: 1.1490). That would argue that whole fall from 1.1917 has completed as a correction. Further rise should then be seen to 1.1727 resistance first. On the downside, though, below 1.1554 will turn bias to the downside for 1.1490 support first.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1345) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

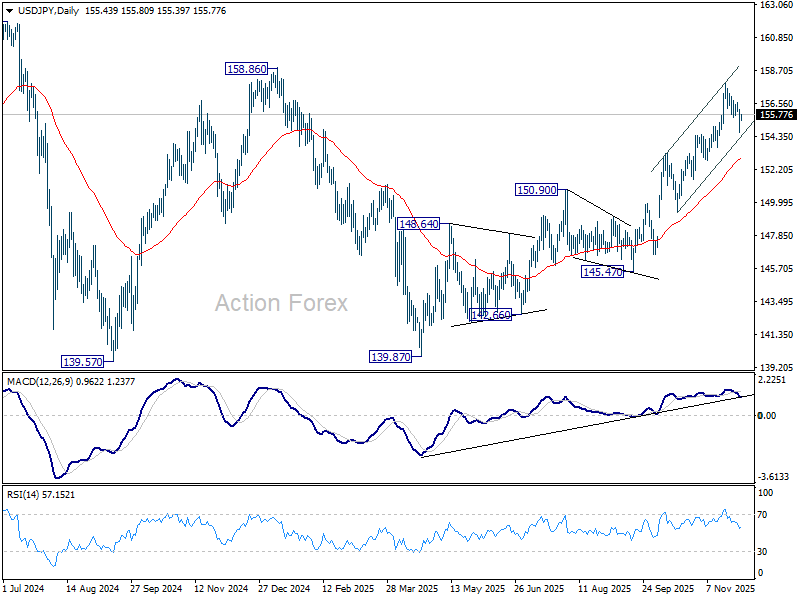

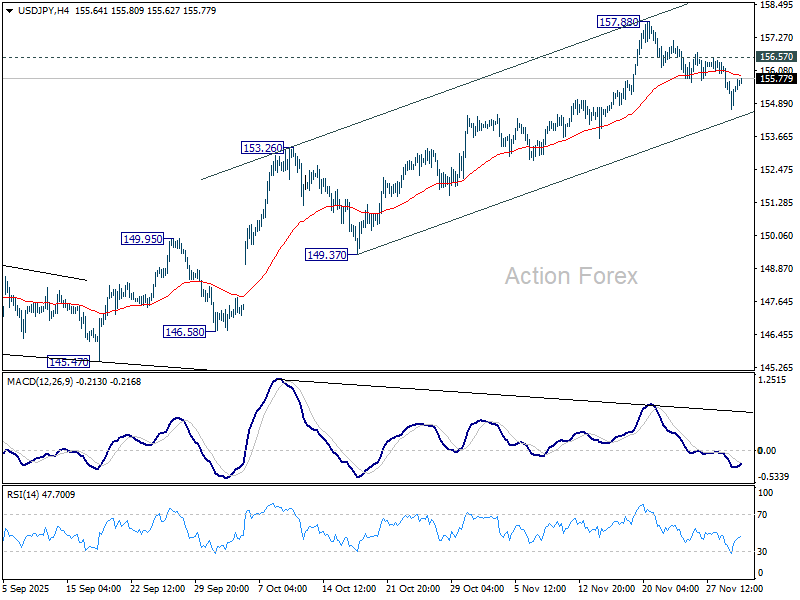

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.71; (P) 155.43; (R1) 156.21; More...

Intraday bias in USD/JPY remains mildly on the downside with focus on near term rising channel support (now at 154.44). Strong support could be seen there to bring rebound. Above 156.57 minor resistance will bring retest of 157.88. Further break of 157.88 will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high. However, sustained break of the channel support will bring deeper correction to 55 D EMA (now at 152.86), and raise the chance of near term trend reversal.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.