Sample Category Title

Crypto Market Tries to Form an Uptrend

Market Overview

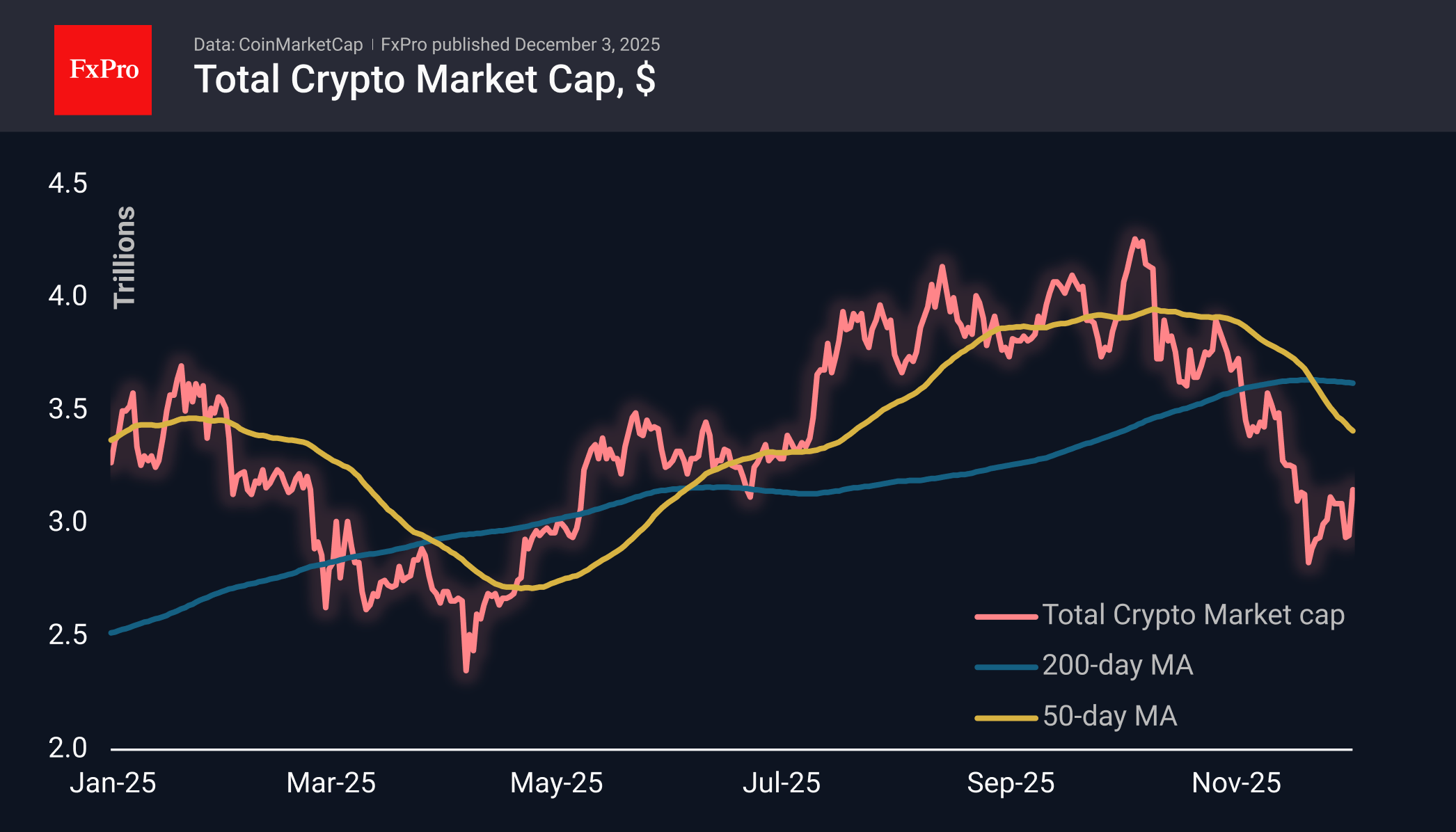

The crypto market soared by almost 7% over the past day, reaching a capitalisation of $3.15T and forming a higher local peak compared to Sunday. The mood on the crypto market was buoyed by moves from institutional giants Vanguard and Bank of America to open access to digital assets for their clients. Combined with the fact that the low point on December 1st is higher than the lows on November 21st, we are seeing a series of vital signs of an upward trend forming. However, a conservative view suggests that fluctuations below $3.38T are a correction from the previous decline.

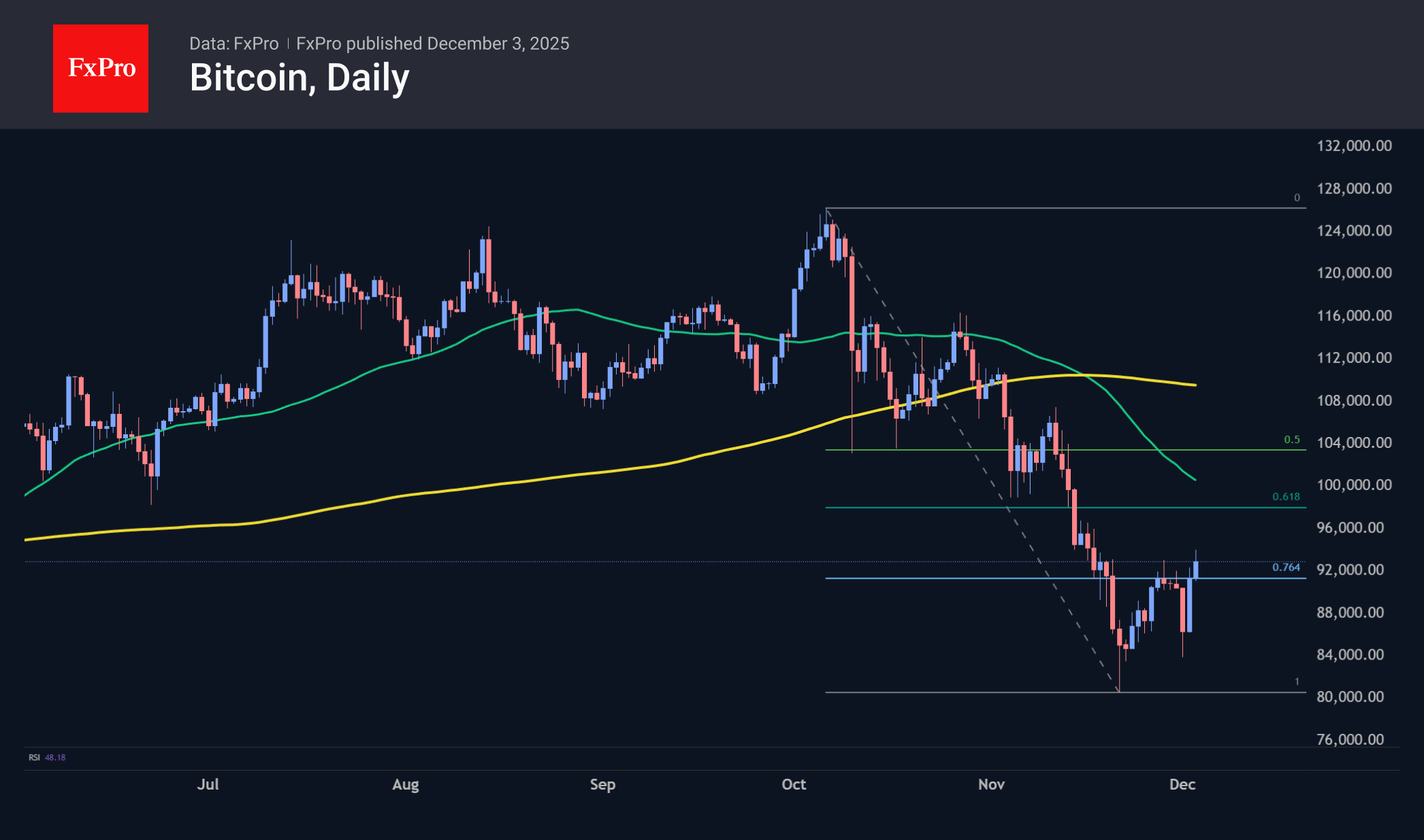

Bitcoin approached $94K on Wednesday morning, recovering half of its losses from the sell-off between November 11th and 21st. Considering the entire decline from its October peak, BTCUSD remains trading below $ 98K as part of the correction. The $98-100K range contains three psychologically significant levels: the 50-day average, early November support, and 61.8% of the decline from the peak. Consolidation above this level could convince buyers that crypto winter has not arrived.

News Background

Vanguard, the world’s second-largest investment company by assets, will open access to crypto ETF trading for its clients on December 2nd. The company had previously stated that it would avoid Bitcoin funds because cryptocurrency is an “immature asset class” and does not fit with the company’s philosophy.

Bank of America, one of the largest banks in the United States, has recommended that its institutional clients allocate 1% to 4% of their portfolios to cryptocurrencies. Previously, investors were unable to access cryptocurrencies because advisors were prohibited from recommending such instruments.

The four-year cycle theory has ceased to work, so Bitcoin has a chance to reach new highs in 2026, according to Grayscale. Analysts believe there are already some signs that Bitcoin has likely bottomed out.

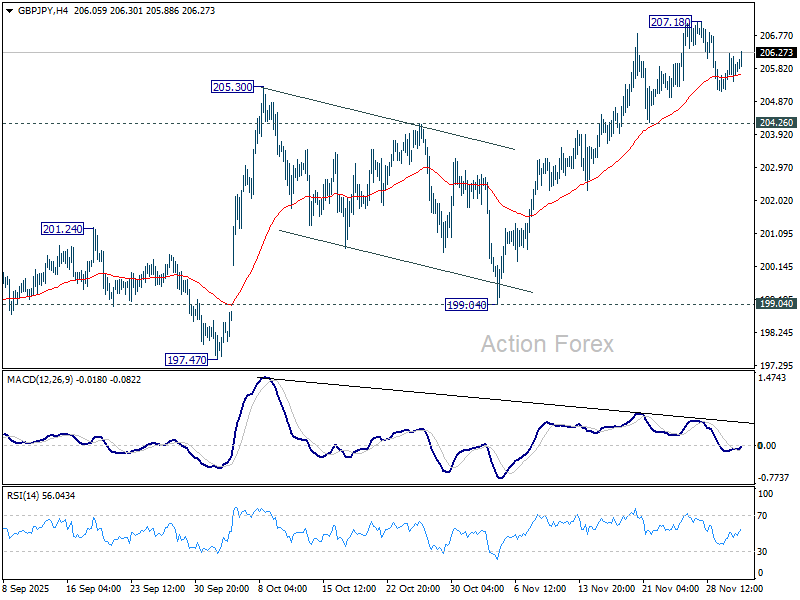

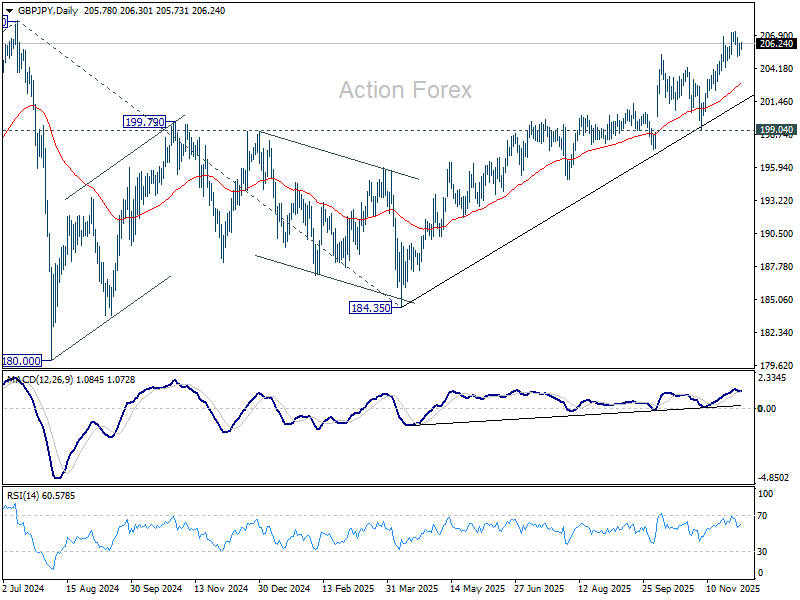

GBP/JPY Daily Outlook

Daily Pivots: (S1) 205.43; (P) 205.85; (R1) 206.36; More...

GBP/JPY is extending consolidations below 207.18 and intraday bias stays neutral. Further rally is expected as long as 204.26 support holds. Above 207.18 will resume larger rise to retest 208.09 high. Firm break there will confirm long term up trend resumption. However, decisive break of 204.26 will bring deeper pullback to 55 D EMA (now at 202.94).

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 199.04 support will dampen this view and extend the corrective pattern with another fall.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 180.58; (P) 180.97; (R1) 181.59; More...

EUR/JPY is still bounded in sideway consolidations below 181.98 and intraday bias stays neutral. While deeper retreat cannot be ruled out, downside should be contained by 178.80 resistance turned support to bring another rally. On the upside, break of 181.98 will target 100% projection of 161.06 to 173.87 from 171.09 at 183.90 next. However, firm break of 178.80 will argue that deeper correction is already underway towards 55 D EMA (now at 177.62).

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Outlook will continue to stay bullish as long as 55 W EMA (now at 169.87) holds, even in case of deep pullback.

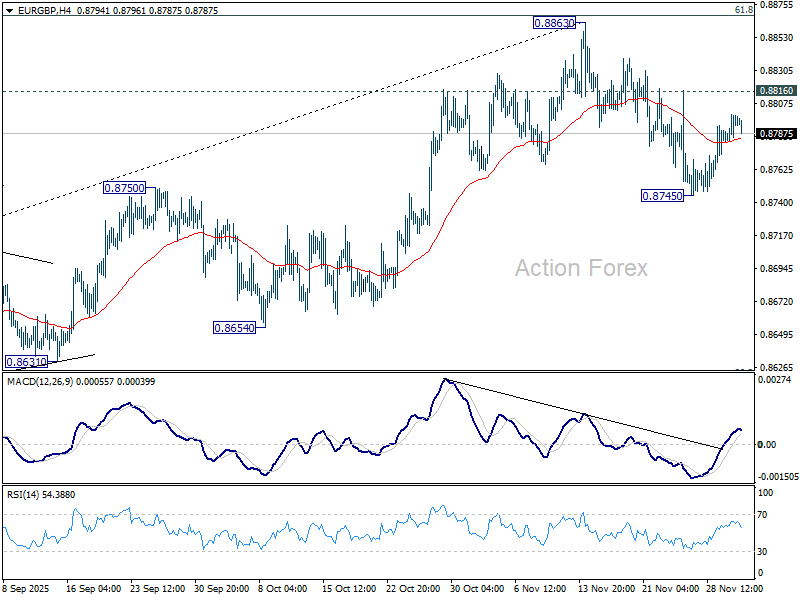

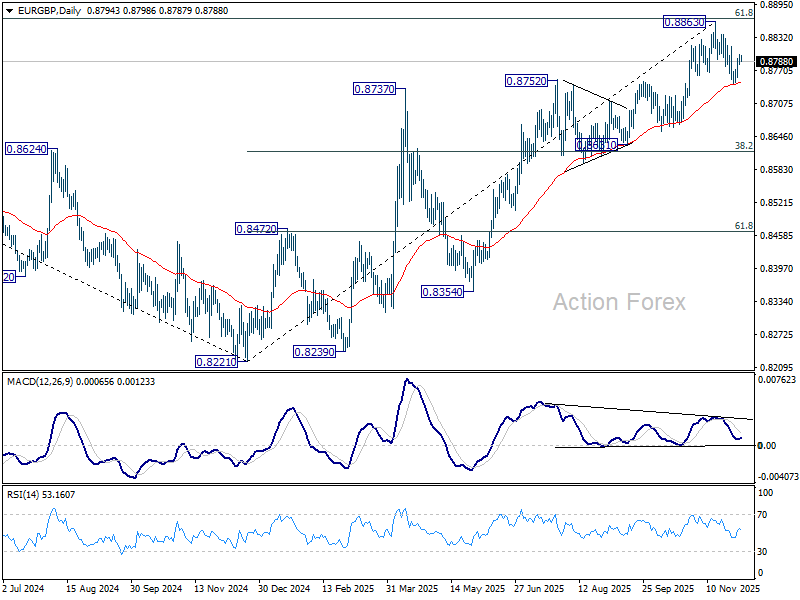

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8785; (P) 0.8794; (R1) 0.8806; More…

Intraday bias in EUR/GBP remains neutral outlook is unchanged. Considering bearish divergence condition in D MACD, sustained trading below 55 D EMA (now at 0.745) will solidify the case of bearish reversal. Deeper fall should then be seen to 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618). However, break of 0.8816 minor resistance will bring stronger rebound to retest 0.8863 high instead.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8600) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

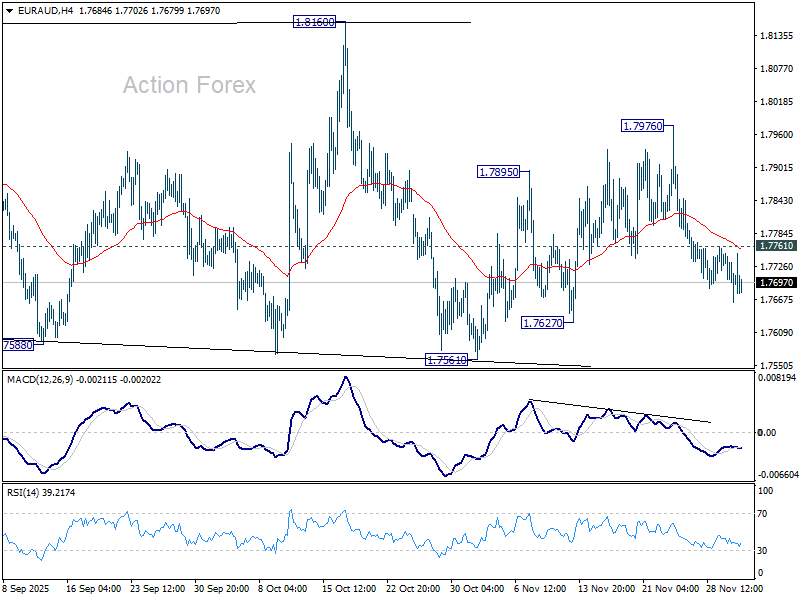

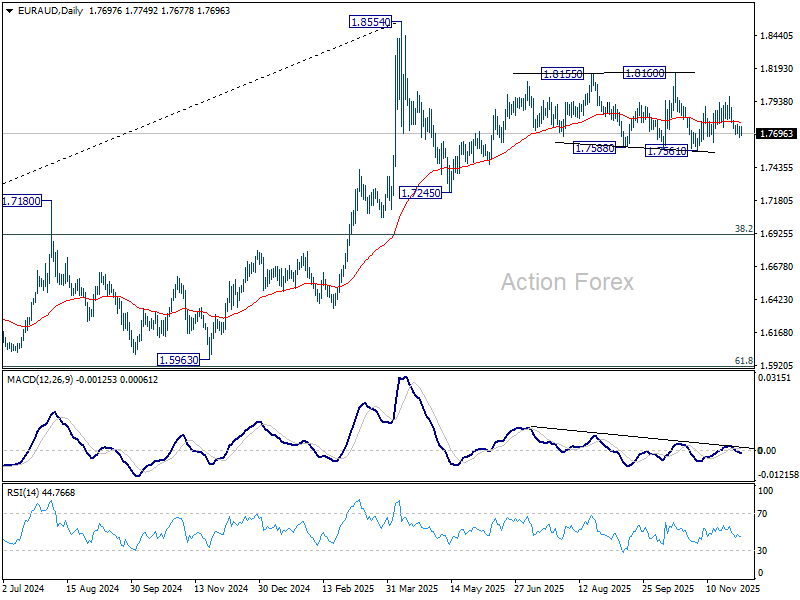

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7660; (P) 1.7711; (R1) 1.7757; More...

Intraday bias in EUR/AUD remains mildly on the downside for 1.7627 support. Firm break there will argue that decline from 0.8160 is ready to resume through 1.7561 support next. On the upside, above 1.7794 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Sustained break of 55 W EMA (now at 1.7426) will suggest that it's correcting the whole rally from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922. Nevertheless, strong rebound from 55 W EMA will likely bring resumption of the up trend sooner.

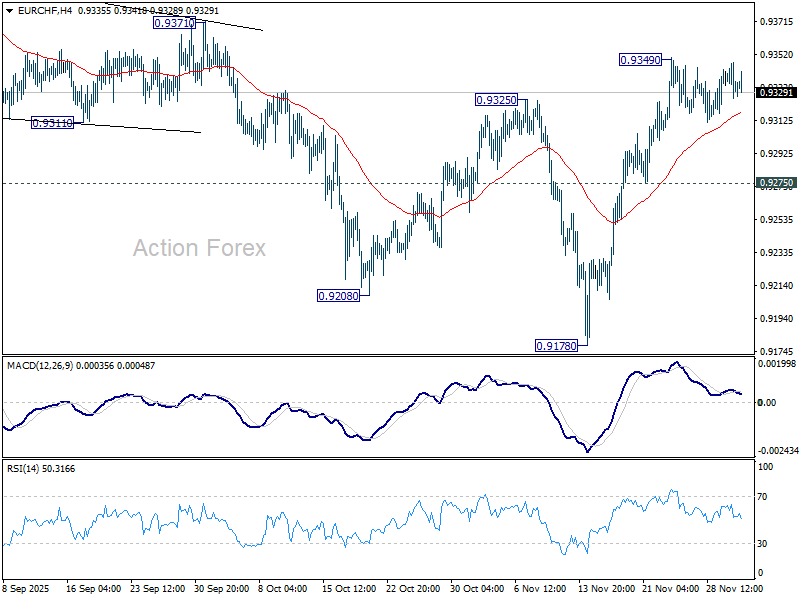

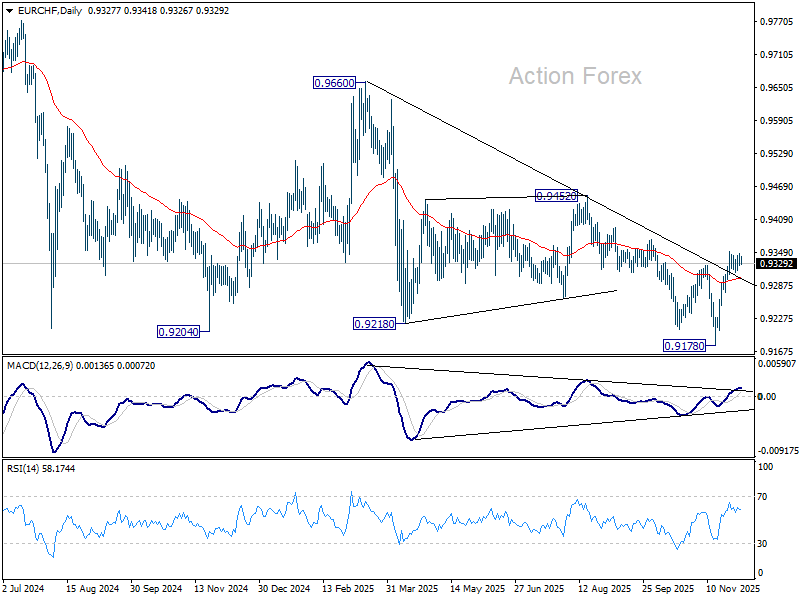

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9322; (P) 0.9335; (R1) 0.9348; More....

Sideway trading continues in EUR/CHF and intraday bias remains neutral. As noted before, fall from 0.9660 could have completed at 0.9178, on bullish convergence condition in D MACD. Above 0.9349 will resume the rise from 0.9178, and target 0.9452 resistance next. However, break of 0.9275 will turn bias back to the downside for 0.9178 low instead.

In the bigger picture, outlook remains bearish with EUR/CHF staying well inside long term falling channel after multiple rejection by 55 W EMA (now at 0.9371). Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Break of 0.9452 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish in case of strong rebound.

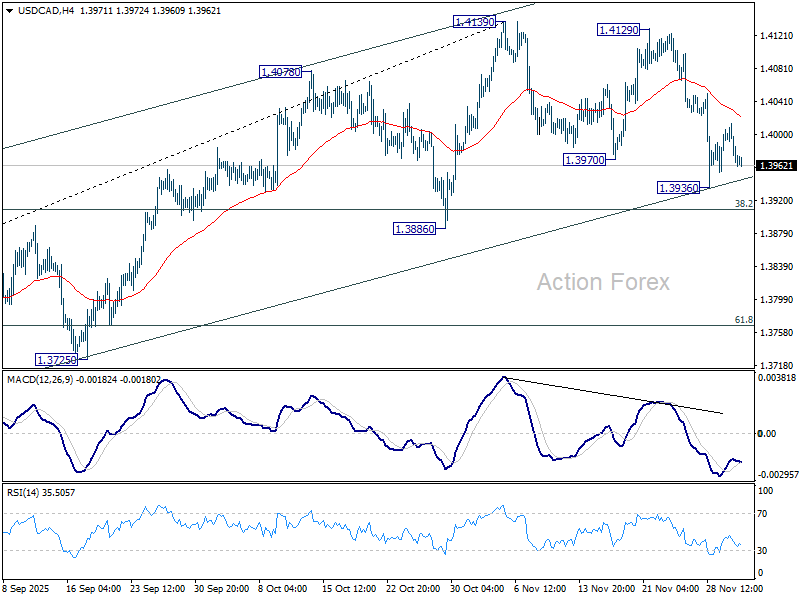

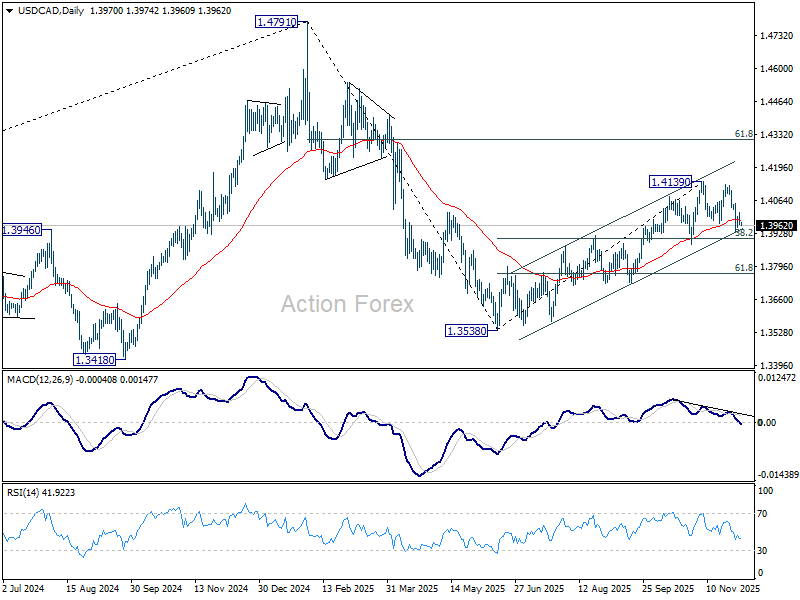

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3952; (P) 1.3984; (R1) 1.4000; More...

Intraday bias in USD/CAD remains neutral and some more consolidations could be seen above 1.3936. Risk will stay on the downside as long as 55 4H EMA(now at 1.4021) holds. Below 1.3936 will target 38.2% retracement of 1.3538 to 1.4139 at 1.3909. Sustained break there will indicate that whole rise from 1.3538 has completed. Deeper fall should then be seen to 61.8% retracement at 1.3768 next. However, firm break of 55 4H EMA will retain near term bullishness, and bring retest of 1.4139 high.

In the bigger picture, price actions from 1.4791 medium term top is likely just unfolding as a correction to up trend from 1.2005 (2021 low), with rise from 1.3538 as the second leg. A third leg should follow before up trend resumption. That is, range trading is set to extend for the medium term. For now, this will remain the favored case as long as 1.3886 support holds. However, firm break of 1.3886 will revive the case that fall from 1.4791 is indeed a larger scale correction.

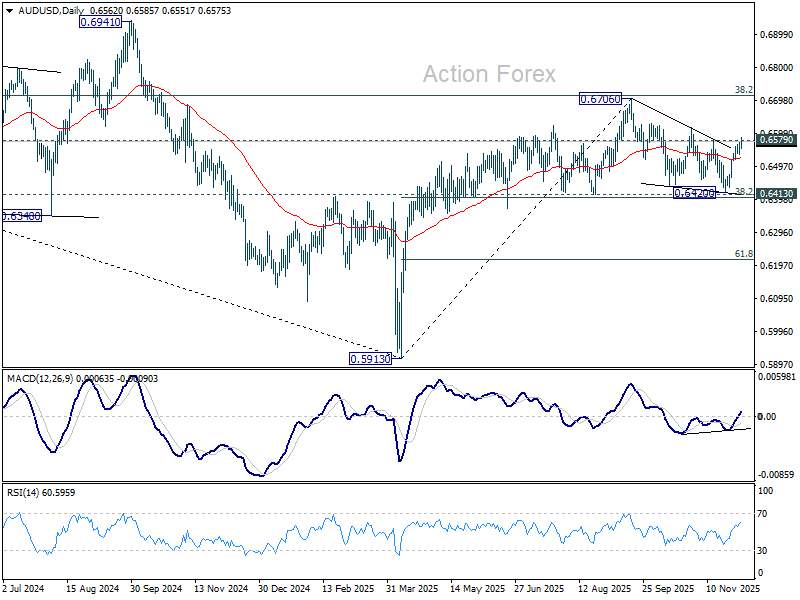

AUD/USD Daily Report

Daily Pivots: (S1) 0.6544; (P) 0.6558; (R1) 0.6578; More...

Intraday bias in AUD/USD stays on the upside at this point. Decisive break of 0.6579 resistance should confirm that whole fall from 0.6706 has completed as a three wave correction. Stronger rally should then be seen back to retest 0.6706. However, below 0.6519 minor support will turn intraday bias back to the downside for 0.6413 key support.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Break of 0.6413 support will suggest rejection by 0.6713 and solidify this bearish case. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

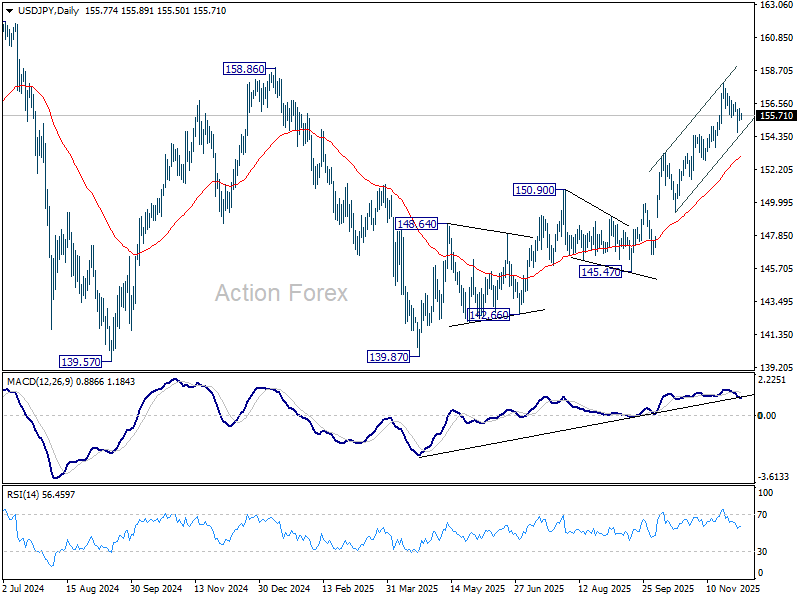

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.47; (P) 155.83; (R1) 156.22; More...

Intraday in USD/JPY remains neutral at this point. With near term rising channel floor intact, further rally is expected. Above 156.57 minor resistance will bring retest of 157.88. Further break there will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high. However, sustained break of the channel support will bring deeper correction to 55 D EMA (now at 153.06), and raise the chance of near term trend reversal.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

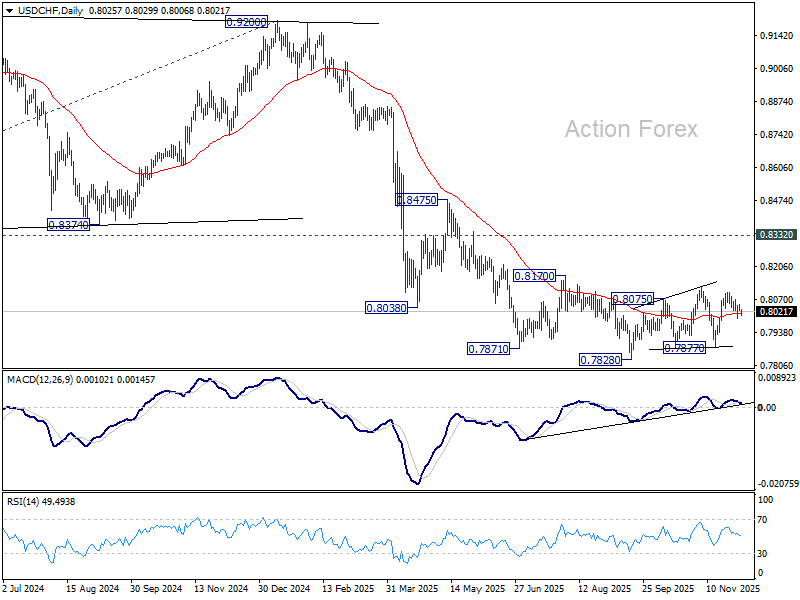

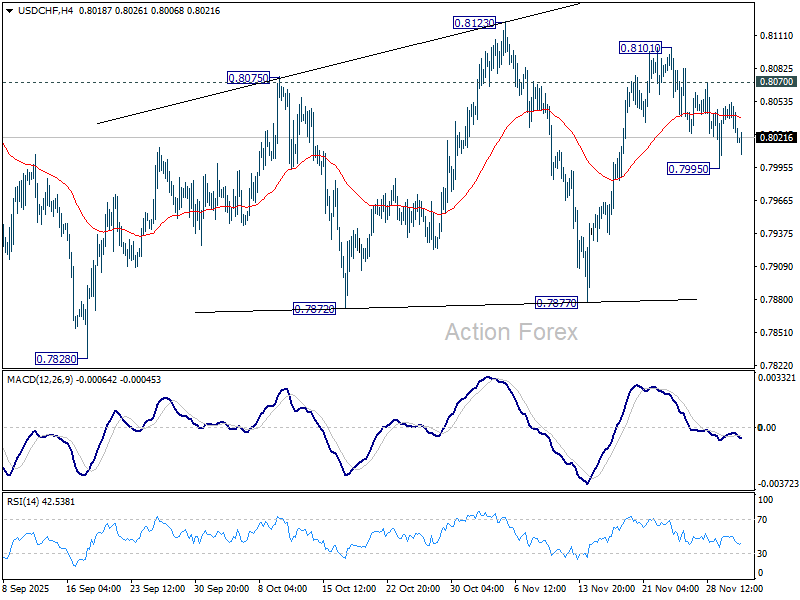

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8020; (P) 0.8036; (R1) 0.8046; More…

Intraday bias in USD/CHF remains neutral for the moment. Outlook is unchanged that price actions from 0.7828 low is seen as a corrective pattern. On the upside, above 0.8070 will indicate that pattern is still extending, and turn bias back to the upside for 0.8123 and above. On the downside, below 0.7995 will bring deeper fall back towards 0.7877 support.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).