Sample Category Title

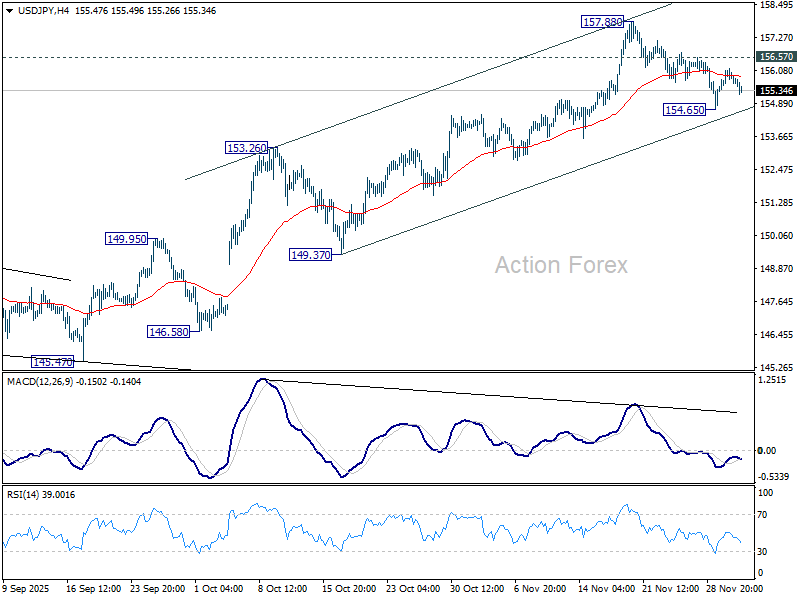

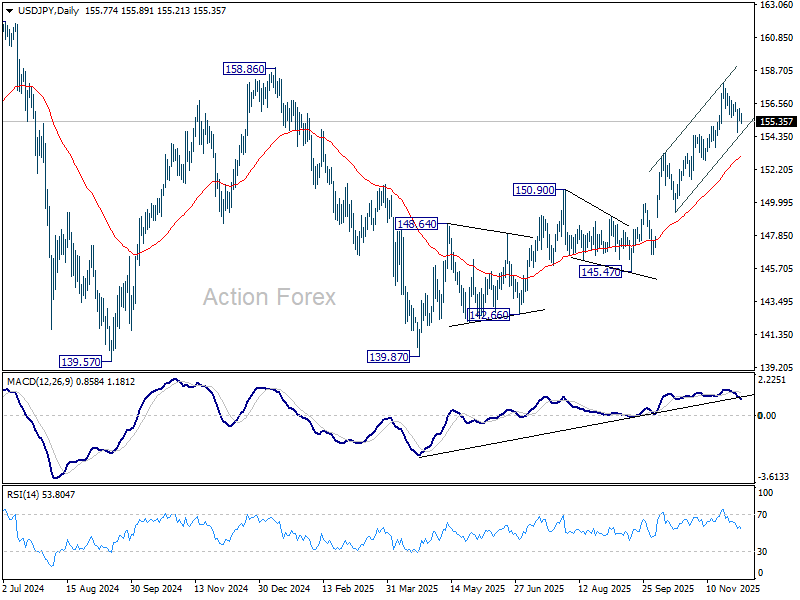

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.47; (P) 155.83; (R1) 156.22; More...

Outlook in USD/JPY remains unchanged and intraday bias stays neutral. With near term rising channel floor intact, further rally is expected. Above 156.57 minor resistance will bring retest of 157.88. Further break there will resume the whole rally from 139.87. Next target is 158.86 structural resistance, and then 161.94 high. However, sustained break of the channel support will bring deeper correction to 55 D EMA (now at 153.06), and raise the chance of near term trend reversal.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

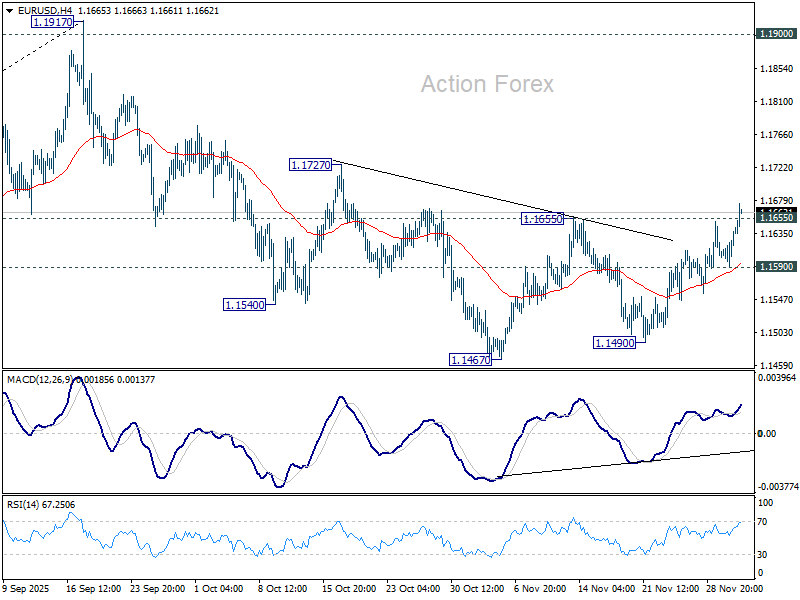

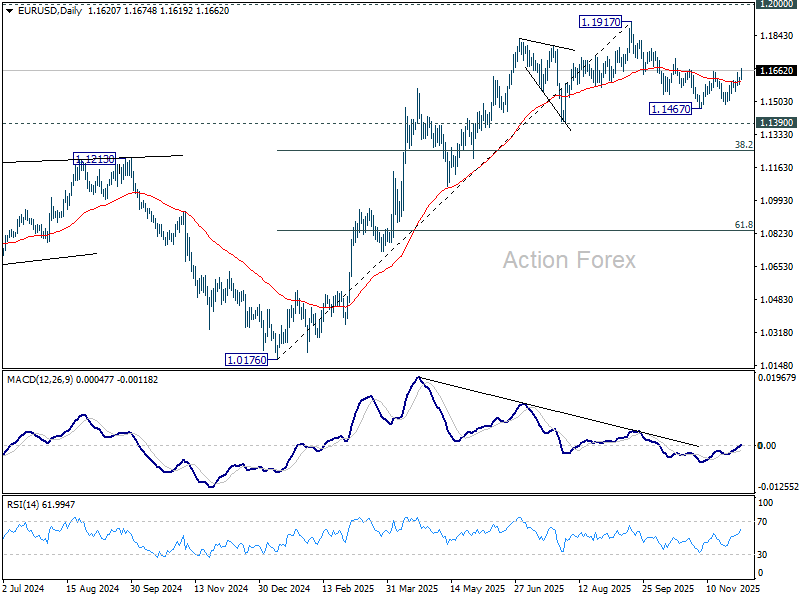

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1602; (P) 1.1615; (R1) 1.1638; More….

EUR/USD's break of 1.1655 resistance argues that fall from 1.1917 has completed at 1.1467 as a correction. This is supported by the head and shoulder bottom pattern (ls: 1.1540, h: 1.1467, rs: 1.1490). Intraday bias is back on the upside for 1.1727 resistance. Firm break there will bring retest of 1.1917 high. Nevertheless, below 1.1590 minor support will mix up the outlook and turn bias neutral again.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1345) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

Dollar Extends Losses on Deepening Labor Weakness, Euro Leads Weekly Gains

Dollar selling intensified again in early US session after another weak ADP employment report, marking the fourth decline in private payrolls over the past six months. The series of negative prints is now being viewed as a clear sign of deterioration in the labor market, prompting markets to extend their bearish repricing of the greenback ahead of next week’s FOMC meeting.

The latest ADP miss pushed the probability of a 25bps Fed rate cut this month to nearly 90%, with investors now treating a December move as all but baked in. Whether the Fed continues easing in Q1 remains less certain. Officials will have to weigh the ADP weakness against the upcoming official nonfarm payrolls report in two weeks—data that will arrive after the December policy decision and may heavily influence early-2026 expectations.

Adding to the uncertainty is speculation surrounding the Fed leadership transition. While not formally confirmed, markets widely expect US President Donald Trump to nominate his top economic adviser Kevin Hassett to replace Jerome Powell. Trump has suggested a formal announcement will come early next year, but traders are already gaming out the implications for forward guidance and institutional independence.

One emerging theme is the notion that Hassett could act as a “shadow Fed Chair” for several months before formally taking over, with markets potentially reacting as strongly to his comments as to those of Powell. If so, communication risks may rise into mid-2026 as investors adjust to a new center of gravity in policy messaging.

In FX, the Dollar sits firmly at the bottom of the weekly performance table for now, followed by Loonie and Kiwi. Euro leads, with Aussie and Sterling also posting gains. Yen and Swiss Franc are trading mid-range.

In Europe, at the time of writing, FTSE is down -0.14%. DAX is up 0.13%. CAC is flat. UK 10-year yield is down -0.025 at 4.448. Germany 10-year yield is down -0.015 at 2.740. Earlier in Asia, Nikkei rose 1.14%. Hong Kong HSI fell -1.28%. China Shanghai SSE fell -0.51%. Singapore Strait Times rose 0.36%.

US ADP jobs shock with -32k drop as small businesses cut deeply

US ADP private employment fell –32k in November, a sharp downside surprise versus expectations for 19k gain and marking one of the weakest readings of the year. Hiring declined in both major sectors, with goods-producing industries shedding -19k jobs and services losing -13k, highlighting broad cooling in labor demand.

The breakdown by firm size underscored the strain on smaller companies. Small businesses cut -120k jobs, overwhelmingly driving the headline decline, while medium-sized firms added 51k and large employers added 39k.

Wage growth also eased: pay for job-stayers slowed to 4.4% yoy from 4.5%, while job-changers saw pay growth fall to 6.3% yoy from 6.7%, continuing the trend of decelerating compensation pressures.

ADP’s Dr. Nela Richardson said the hiring backdrop has become increasingly uneven, citing “cautious consumers and an uncertain macroeconomic environment.” She emphasized that while the slowdown was widespread, the contraction was driven primarily by small businesses—often the most sensitive to shifts in demand and credit conditions.

Eurozone PMI composite finalized at 30-month high, mild Q4 acceleration expected

Eurozone Services PMI final rose to 53.6 in November from 53.0, marking a 30-month high and reinforcing the sector’s position as the main driver of regional growth. Composite PMI also improved to 52.8 from 52.5—another 30-month high—indicating that services strength more than compensated for continued manufacturing softness.

Country-level PMI Composite showed broad participation: Ireland led with a 42-month high at 55.8, while Italy also hit a 31-month high at 53.8. Germany (52.34) and Spain (55.1) softened slightly, and France returned to expansion at 50.4.

Hamburg Commercial Bank Chief Economist Cyrus de la Rubia said the data show “clear signs of recovery” across the services sector. The improvement was strong enough to lift overall Eurozone output, supporting expectations of a “slight acceleration” in Q4 growth. Though the headline index remains “far from a boom,” De la Rubia described the overall performance as “relatively robust,” underpinned by encouraging geographical breadth.

Price indicators delivered mixed but generally favorable signals for policymakers. Services selling-price inflation—which the ECB monitors closely—“weakened significantly” again, while wage growth c is gradually easing. Taken together, the data are likely to strengthen the ECB’s conviction in keeping interest rates on hold at the upcoming meeting.

UK PMI services finalized at to 51.3; Client caution and margin pressures build

UK Services PMI was finalized at 51.3 in November down from October's 52.3. Composite PMI eased to 51.2 from 52.2, marking a clear loss of momentum after several months of improvement. S&P Global’s Tim Moore said the data show an “abrupt end” to the gradual recovery in order books seen since summer, with demand weakening in both domestic and export markets.

Lower workloads fed through to a slowdown in business activity growth, pushing expansion well below the post-pandemic trend. Firms also cut staffing levels at the fastest pace since February, pointing to an increasingly cautious operating environment. Survey respondents cited fragile client confidence, rising risk aversion and elevated policy uncertainty in the run-up to the Autumn Budget, with many delaying major spending decisions.

Competitive pressures intensified as firms struggled with weak sales pipelines. While input cost inflation accelerated—largely due to higher wages—selling price inflation rose at the slowest pace in nearly five years, signaling a squeeze on margins.

Swiss CPI back at 0.0% as broad price declines in November

Swiss inflation softened in November, with headline CPI falling -0.2% mom, in line with expectations, while annual inflation slowed from 0.1% yoy to 0.0%, undershooting forecasts of 0.1%. Core CPI also dipped, falling -0.1% yoy, with the annual rate easing from 0.5% yoy to 0.4%. The data highlight Switzerland’s continued weak inflation, keeping price growth far below levels seen elsewhere in Europe.

Both domestic and imported prices contributed to the decline. Domestic products fell -0.2% mom, while imported goods dropped a sharper -0.4% mom. On a yearly basis, domestic inflation cooled from 0.5% yoy to 0.4%, and imported prices remained deeply negative at -1.3% yoy. The persistent weakness in imported goods continues to anchor Swiss inflation near zero.

RBA’s Bullock warns inflation persistence may require renewed tightening

RBA Governor Michele Bullock told the Senate Economics Legislation Committee that the bank remains on high alert for renewed inflation pressure and is prepared to act if price gains prove "more persistent" than expected. She noted that upcoming data in the next few months will be crucial in determining whether demand pressures are easing, adding that officials may still have to pivot back toward tightening if inflation shows signs of regaining strength.

Facing questions on past budget and inflation mis-projections, Bullock conceded the RBA “hasn’t done it yet” in bringing inflation sustainably back to target, and must continue working toward that objective. She stressed that the board must “keep working on this”.

With national debt set to exceed AUD 1 trillion and a deficit of AUD 42 billion projected, she noted that lower public and private savings—if paired with unchanged investment—could "put upward pressure on the neutral rate,” she said."

But she added that that such an outcome is possible but contingent on both domestic and global forces. She emphasized that while the RBA can respond to domestic dynamics, but we don’t control global factors."

Australia Q3 GDP misses forecast at 0.4%, per capita output stagnates

Australia’s economy expanded 0.4% qoq in Q3, below expectations for 0.7% and marking a softer outcome despite a 2.1% yoy rise from a year earlier. The headline result reflected steady domestic activity supported by private investment and household consumption. However, GDP per capita was flat, suggesting growth is tracking population gains rather than delivering broad-based improvement in living standards.

A key drag came from external accounts. Inventory rundown—used to support export volumes—subtracted meaningfully from growth, while net trade also weighed as imports rose faster than exports. The pattern highlights ongoing pressure on Australia’s trade balance even as domestic demand remains resilient.

Grace Kim, ABS head of National Accounts, described Q3 performance as “steady,” noting growth matched the post-pandemic quarterly average. Kim added that per capita GDP stagnation reflected population dynamics rather than outright weakness in activity, with the measure still 0.4% above its level a year earlier.

Japan PMI services holds strong at 53.2, optimism hits year high

Japan’s Services PMI was finalized at 53.2 in November, edging up from 53.1 in October. Composite PMI also improved, rising to 52.0 from 51.5. S&P Global’s Annabel Fiddes noted “a number of positive developments,” with the sector consistently driving overall activity since mid-year.

Forward-looking indicators strengthened notably. Business optimism and hiring intentions both climbed to their highest levels since early 2025. New orders also accelerated modestly, the first pickup in three months, signaling a gradual improvement in underlying demand even if the pace remains mild. However, the positive momentum was accompanied by firmer inflation pressures. Input costs rose at the fastest rate since May, prompting another solid increase in selling prices as firms sought to protect margins.

With Japan’s new stimulus package now approved—aimed at supporting growth and offsetting rising costs—markets will be watching closely to see whether demand and output continue to improve in the coming months.

China's RatingDog PMI services falls to 52.1, expansion loses pace, employment and margins under pressure

China’s RatingDog Services PMI eased in November, slipping from 52.6 to 52.1, while Composite PMI fell from 51.8 to 51.2. Both measures remained in expansionary territory, but the decline signaled moderation in growth momentum heading into year-end.

Yao Yu, Founder of RatingDog, said the services sector remained “relatively stable,” though November’s reading marked the weakest level since Q2. External demand showed mild improvement and offered “marginal support,” but domestic conditions were less encouraging.

Employment contracted again, profit margins came under pressure, and business expectations weakened—factors Yao described as the “main constraints” on the sector.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1602; (P) 1.1615; (R1) 1.1638; More….

EUR/USD's break of 1.1655 resistance argues that fall from 1.1917 has completed at 1.1467 as a correction. This is supported by the head and shoulder bottom pattern (ls: 1.1540, h: 1.1467, rs: 1.1490). Intraday bias is back on the upside for 1.1727 resistance. Firm break there will bring retest of 1.1917 high. Nevertheless, below 1.1590 minor support will mix up the outlook and turn bias neutral again.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1345) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

US ADP jobs shock with -32k drop as small businesses cut deeply

US ADP private employment fell –32k in November, a sharp downside surprise versus expectations for 19k gain and marking one of the weakest readings of the year. Hiring declined in both major sectors, with goods-producing industries shedding -19k jobs and services losing -13k, highlighting broad cooling in labor demand.

The breakdown by firm size underscored the strain on smaller companies. Small businesses cut -120k jobs, overwhelmingly driving the headline decline, while medium-sized firms added 51k and large employers added 39k.

Wage growth also eased: pay for job-stayers slowed to 4.4% yoy from 4.5%, while job-changers saw pay growth fall to 6.3% yoy from 6.7%, continuing the trend of decelerating compensation pressures.

ADP’s Dr. Nela Richardson said the hiring backdrop has become increasingly uneven, citing “cautious consumers and an uncertain macroeconomic environment.” She emphasized that while the slowdown was widespread, the contraction was driven primarily by small businesses—often the most sensitive to shifts in demand and credit conditions.

Dollar Weakening, as Set by Seasonality

- December, a seasonally weak month for the dollar, coincided with expectations of aggressive easing by the Fed.

- Divergence in monetary policy is helping the Yen and the Australian dollar.

The first step is the hardest! At the start of winter, the dollar’s decline accelerated, a trend consistent with seasonal patterns. December is traditionally a bearish month for the US currency — over the past 25 years, the dollar has declined on 18 occasions. The repatriation of profits by non-residents from investments in US stocks and bonds requires USD sales. Given the record demand for US securities from foreign investors, this process could give new impetus to the EURUSD rally.

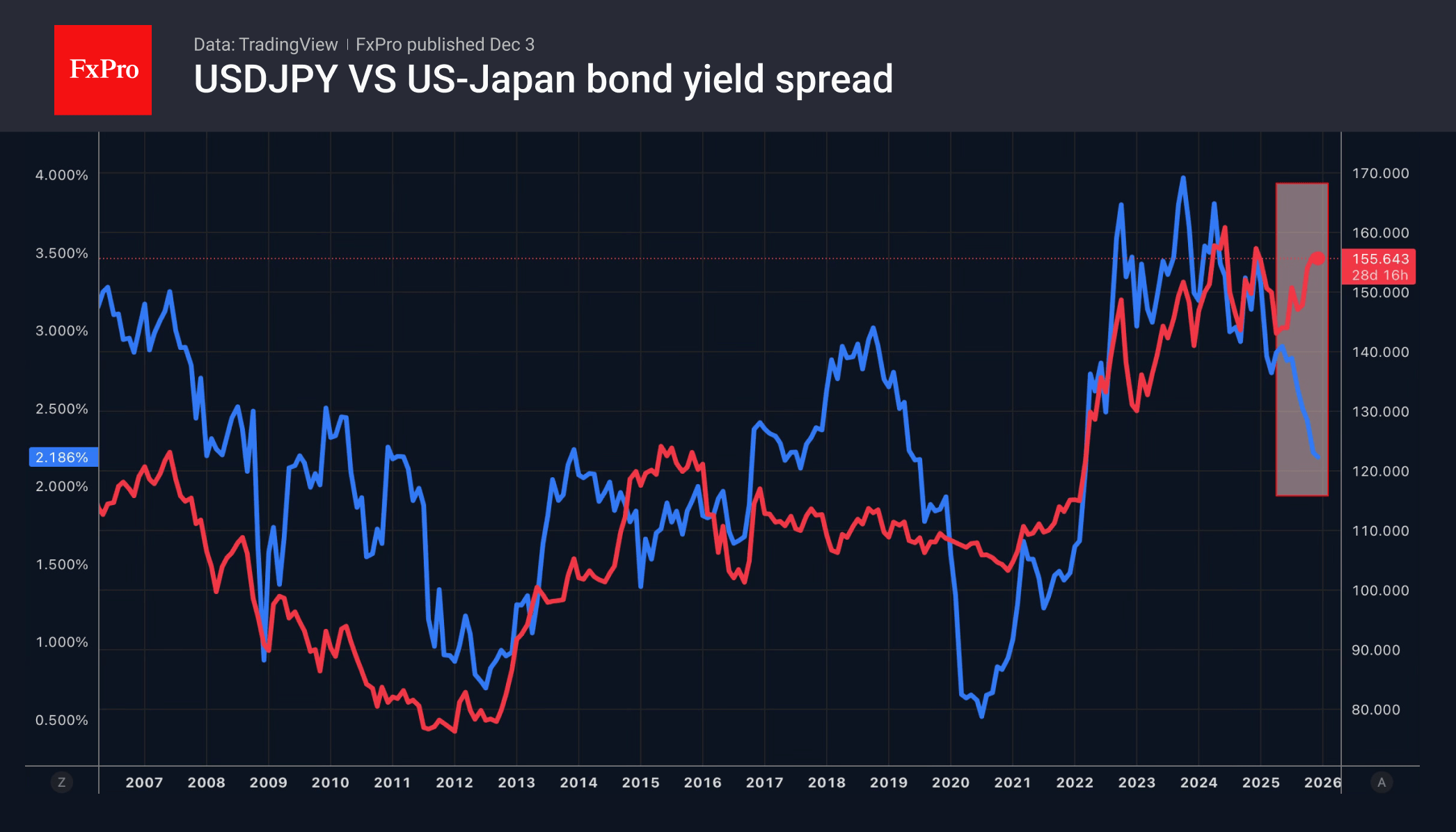

Usually in December, the US dollar performs the worst against the franc and the Swedish krona. At the same time, the struggle with the yen and the Loonie intensifies to the limit. The former looks like the favourite this time around amid expectations of a key rate hike by the Bank of Japan in December. The decline in USDJPY is developing alongside the growing chances of a rate hike from 0.5% to 0.75% on 19 December.

Investors are playing on the divergence in monetary policy. The Fed is expected to cut rates to 3% in 2026, whereas the BoJ forecasted a hike to 1.25%. The narrowing of the yield spread between these countries’ bonds shifts the balance in favour of the yen on Forex next year.

The anticipation of death is worse than death itself. Donald Trump’s statement that the new Fed chair will be announced in early 2026, rather than by Christmas as Scott Bessent had previously said, is not helping the dollar. Along with the expectation of Kevin Hassett’s arrival at the helm of the Fed, the expected scale of monetary expansion is growing. This is bad news for USD.

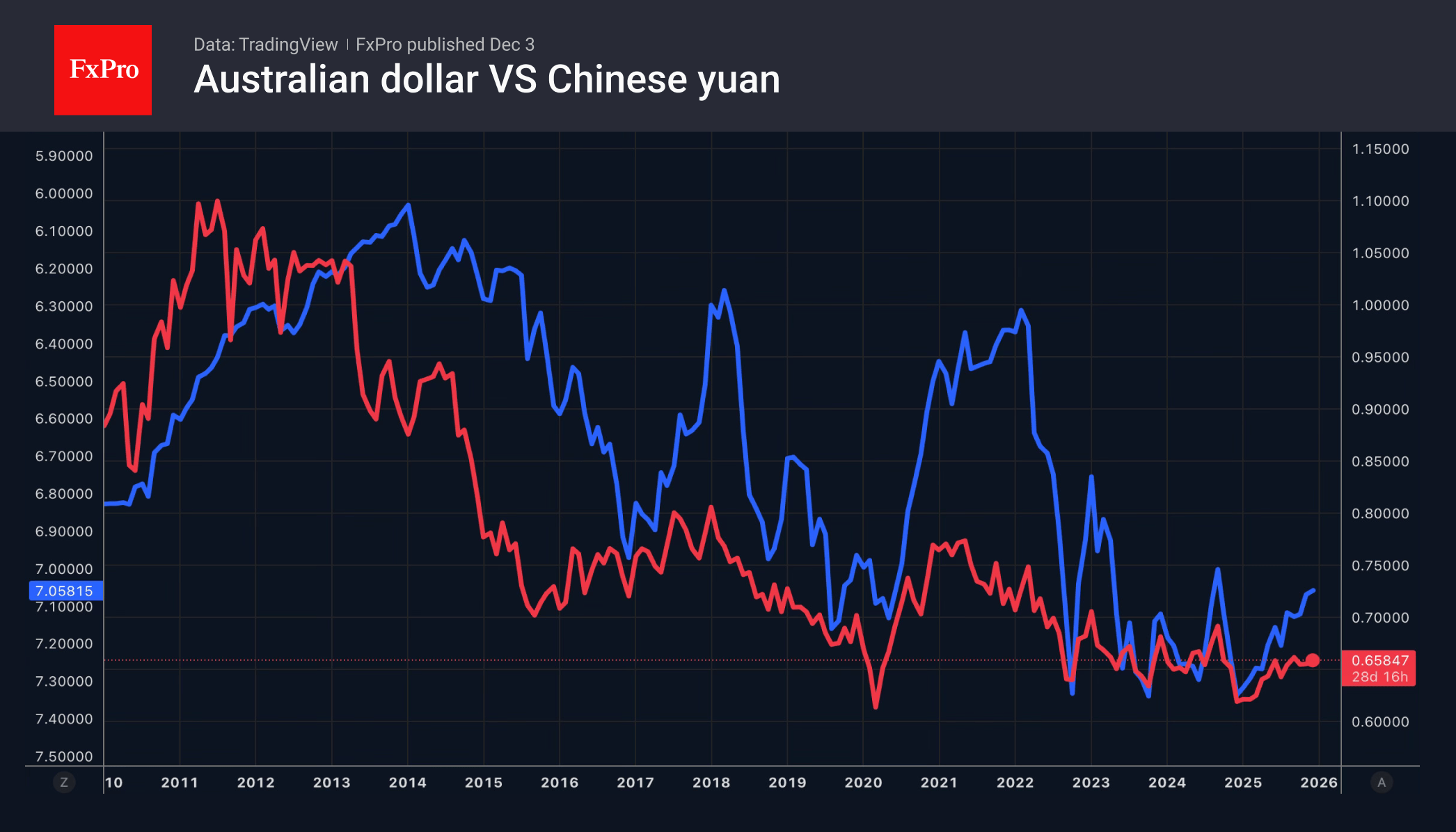

Other currencies are taking advantage of the greenback’s weakness. AUDUSD rose to a 5-week high on growing chances of an RBA base rate hike next year due to accelerating inflation. The rally in US stock indices supports the Aussie, as well as the associated improvement in global risk appetite, and the most significant strengthening of the Chinese yuan since 2020. Unlike the first trade war, when USDCNH soared by 13%, this time the tariffs did not scare off the bears.

Bitcoin Price Analysis: Chart Shows Bullish Signals

Today, Bitcoin is trading above the psychological $90,000 mark – its highest level in over ten days.

Following a severe drop of more than 30% from October’s highs, the market had been lacking positive momentum. Confidence was boosted by:

→ investment giant Vanguard allowing clients to purchase spot Bitcoin ETFs on its platform;

→ news from Strategy Inc (we covered MSTR shares yesterday), which holds around 650,000 bitcoins and confirmed it has no plans to sell them in “emergency mode,” avoiding a flood of supply that could further depress the market.

Technical Analysis of BTC/USD

Since the summer, Bitcoin has been moving within a descending channel (shown in red), with:

→ the 21 November low (A) marking the lower boundary of the channel;

→ yesterday’s breakout above the QL line (which divides the lower half into quarters) accelerating price growth.

The formation of lows A and B suggests bullish potential, as they:

→ resemble a “Cup with Handle” pattern;

→ indicate aggressive demand.

However, further upside may be constrained by the channel’s median. As shown by the black segments, this line previously acted as support, so traders should consider the possibility that it may now function as resistance.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

USD/JPY Declines as Market Focus Shifts to Bank of Japan Policy

The USD/JPY pair fell to 155.67 on Wednesday, recovering part of the previous session’s sharp losses. The decline was driven by renewed pressure on the US dollar, as market expectations for a deeper Federal Reserve easing cycle gained traction.

Domestically, investor attention remains firmly fixed on the likelihood of a Bank of Japan (BoJ) interest rate hike at its December meeting. This possibility has been underscored by recent hawkish signals from certain BoJ officials, creating a contrast with market perceptions that Prime Minister Sanae Takaichi’s government favours more accommodative monetary conditions.

This week, Finance Minister Satsuki Katayama sought to downplay any perceived policy rift, stating there is no discrepancy between the government’s and the central bank’s economic assessments. This remark underscores the continued official emphasis on coordination between fiscal and monetary policy.

Her comments followed a speech by BoJ Governor Kazuo Ueda, who expressed confidence in Japan’s economic outlook and confirmed the central bank will carefully weigh the advantages and disadvantages of a rate increase at its December policy review.

Technical Analysis: USD/JPY

H4 Chart:

On the H4 chart, USD/JPY remains in a downward correction phase following its accelerated rally in mid-November. The pair is trading below the key resistance level of 156.76, forming a potential reversal structure near the lower Bollinger Band. Selling pressure persists, as evidenced by the market’s failure to sustain a move above the indicator’s middle band.

A decisive break below the 154.66 support level would signal a deeper correction, targeting the area of previous local lows. Conversely, a sustained recovery and close above 156.76 would provide the first technical signal of a potential recovery, opening a path for the pair to retest the 157.90–158.00 resistance zone.

H1 Chart:

On the H1 chart, USD/JPY is undergoing an upward correction after rebounding from support at 157.91. However, the upside appears constrained by the upper Bollinger Band. While buyers are attempting to push above the intermediate resistance at 158.40, price action remains choppy and lacks clear directional conviction.

The technical picture suggests a phase of sideways consolidation with a downside bias. Maintaining the price below 158.45 increases the likelihood of a retest of 157.91. A break below this level would strengthen the bearish scenario, targeting the lower boundary of the current range. For a confirmed bullish shift, a sustained move above 158.45, followed by a breakout towards 158.80–159.00, would be required.

Conclusion

USD/JPY is consolidating its recent decline amid a tug-of-war between a softer US dollar and evolving expectations for BoJ policy. The technical structure across both timeframes suggests a cautious, range-bound environment with a current tilt towards the downside. The immediate directional catalyst will likely be the BoJ’s December meeting, but in the near term, traders should watch for a break outside the 156.76–154.66 range on the H4 chart for a clearer signal on the pair’s next significant move.

GBP/USD Maintains Upward Bias, EUR/GBP Gains Strength

GBP/USD is showing bullish signs above the 1.3180 zone. EUR/GBP is gaining pace and might extend its upward move above 0.8800.

Important Takeaways for GBP/USD and EUR/GBP Analysis Today

- The British Pound is gaining pace above 1.3200 against the US Dollar.

- There is a declining channel forming with support at 1.3180 on the hourly chart of GBP/USD at FXOpen.

- EUR/GBP started a fresh increase above 0.8765 and 0.8775.

- There is a major bearish trend line forming with resistance at 0.8800 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair remained in a positive zone above 1.3080. The British Pound formed a base and started a fresh increase against the US Dollar, as mentioned in the previous analysis.

The pair gained pace for a move above 1.3130 and 1.3180. The pair even settled above 1.3200 and the 50-hour simple moving average. A high was formed at 1.3275 before there was a downside correction.

The pair dipped below the 23.6% Fib retracement level of the upward move from the 1.3038 swing low to the 1.3275 high. However, the bulls are active above 1.3180. There is also a declining channel forming with support at 1.3180.

On the upside, the GBP/USD chart indicates that the pair is facing resistance near 1.3250. The next key hurdle sits at 1.3275. If the RSI moves above 70 and the pair climbs above 1.3275, there could be another rally. In the stated case, the pair could rise toward 1.3350 or even 1.3400.

On the downside, there is a major support forming near 1.3180. If there is a downside break below 1.3180, the pair could accelerate lower. The next area of interest might be 1.3130, below which the pair could test 1.3080. Any more losses could lead the pair toward 1.3035.

EUR/GBP Technical Analysis

On the hourly chart of EUR/GBP at FXOpen, the pair started a fresh increase from 0.8745. The Euro traded above 0.8765 to move into a positive zone against the British Pound.

The EUR/GBP chart suggests that the pair settled above the 50-hour simple moving average and 0.8780. There was a clear move above the 61.8% Fib retracement level of the downward move from the 0.8818 swing high to the 0.8745 high.

Immediate resistance is near 0.8800 and a bearish trend line. The next breakout zone sits near the 0.8815 level. A close above 0.8815 might accelerate gains. In the stated case, the bulls may perhaps aim for a test of 0.8830.

Any more gains might send the pair toward 0.8850 in the coming days. Immediate support sits near the 50-hour simple moving average at 0.8790.

The next hurdle for the bears might be 0.8765. A downside break below 0.8765 might call for more downsides. In the stated case, the pair could drop toward 0.8745. Any more losses might send the pair to 0.8720.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

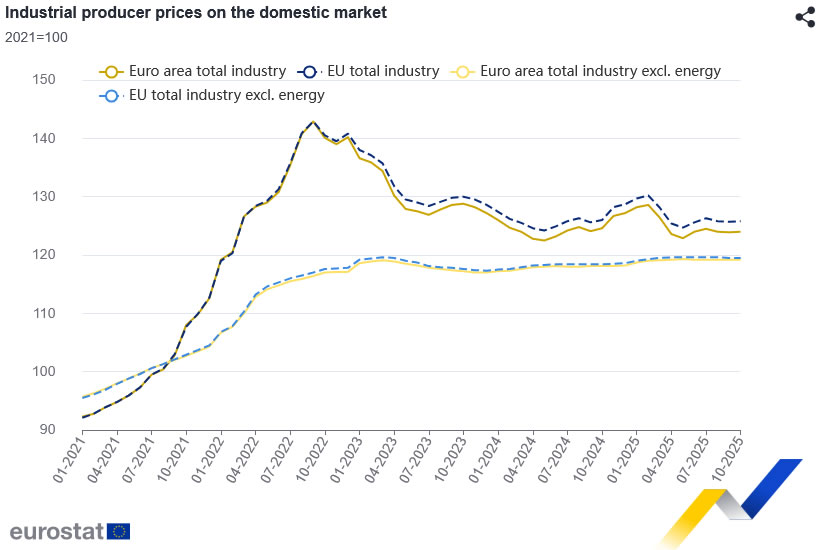

Eurozone PPI at 0.1% mom, -0.5% yoy in October, diminishing upstream inflation

Eurozone PPI edged up 0.1% mom in October but fell -0.5% yoy, coming in softer than expectations of -0.4% yoy.

The monthly gain in Eurozone PPI reflected modest increases across most major categories, including intermediate goods, energy, capital goods and durable consumer goods, each rising 0.1%. Non-durable consumer goods were the exception, slipping -0.2% and weighing slightly on the headline.

In the wider EU, PPI also rose 0.1% mom but was down -0.2% yoy. Price movements across member states were uneven. Bulgaria recorded the sharpest monthly increase at 4.6%, followed by Ireland (1.4%) and Estonia (1.3). Meanwhile, Slovakia (-1.0%), Poland (-0.5%) and Italy (-0.4%) saw notable declines.

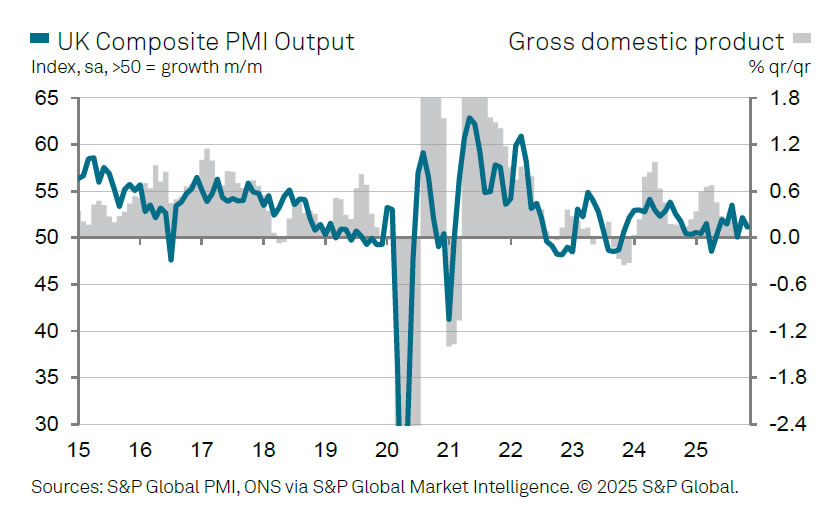

UK PMI services finalized at to 51.3; Client caution and margin pressures build

UK Services PMI was finalized at 51.3 in November down from October's 52.3. Composite PMI eased to 51.2 from 52.2, marking a clear loss of momentum after several months of improvement. S&P Global’s Tim Moore said the data show an “abrupt end” to the gradual recovery in order books seen since summer, with demand weakening in both domestic and export markets.

Lower workloads fed through to a slowdown in business activity growth, pushing expansion well below the post-pandemic trend. Firms also cut staffing levels at the fastest pace since February, pointing to an increasingly cautious operating environment. Survey respondents cited fragile client confidence, rising risk aversion and elevated policy uncertainty in the run-up to the Autumn Budget, with many delaying major spending decisions.

Competitive pressures intensified as firms struggled with weak sales pipelines. While input cost inflation accelerated—largely due to higher wages—selling price inflation rose at the slowest pace in nearly five years, signaling a squeeze on margins.