Sample Category Title

USD/JPY Falls to Support, Setting Stage for a Potential Technical Pivot

Key Highlights

- USD/JPY started a steady decline from the 157.80 zone.

- A key declining channel is forming with resistance at 155.50 on the 4-hour chart.

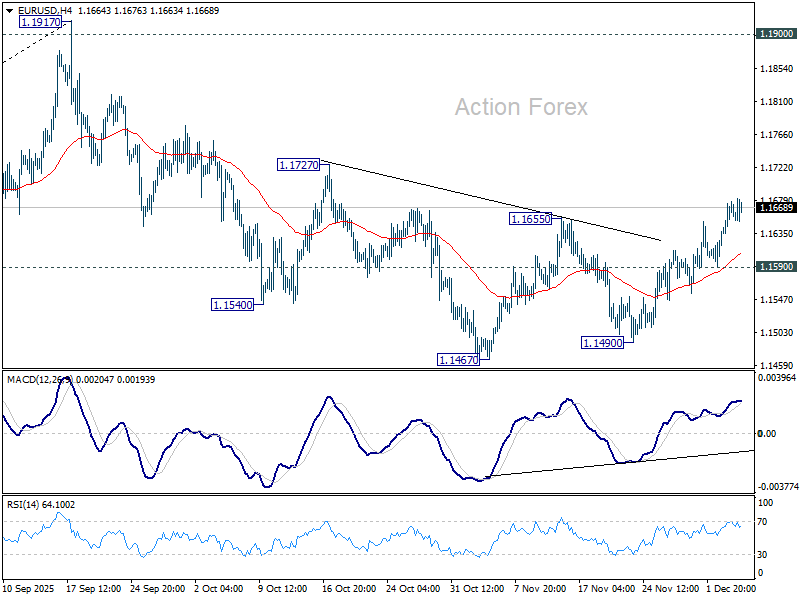

- EUR/USD started consolidating gains above 1.1625.

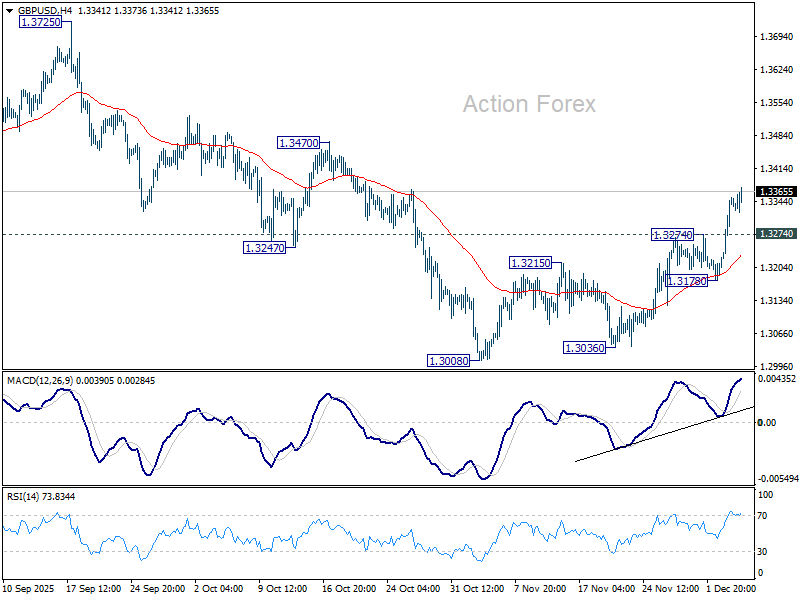

- GBP/USD could aim for more gains if it settles above 1.3350.

USD/JPY Technical Analysis

The US Dollar failed to clear 157.80 and corrected gains against the Japanese Yen. USD/JPY dipped below the 157.00 and 156.00 levels.

Looking at the 4-hour chart, the pair gained pace for a move below the 50% Fib retracement level of the upward move from the 152.81 swing low to the 157.89 high. There was a close below the 100 simple moving average (red, 4-hour), and the pair traded close to the 200 simple moving average (green, 4-hour).

On the downside, there is key support at 154.75. The next support is 154.00, and the 76.4% Fib retracement level of the upward move from the 152.81 swing low to the 157.89 high. Any more losses might call for a test of 152.80.

Immediate resistance sits near 155.20. The first key hurdle is seen near 155.50. There is also a key declining channel forming with resistance at 155.50. A close above 155.50 could open the doors for a move toward 156.00. Any more gains could set the pace for a steady increase toward 156.80.

Looking at EUR/USD, the pair rallied above 1.1650 and recently started a consolidation phase. The main support sits at 1.1600.

Upcoming Key Economic Events:

- US Personal Income for Sep 2025 (MoM) - Forecast +0.4%, versus +0.4% previous.

- Michigan Consumer Sentiment Index for Dec 2025 (Prelim) – Forecast 52.0, versus 51.0 previous.

USD Rebounds: Technical Overview for EUR/USD, USD/CAD and USD/CHF

Despite a rough monthly open, the US Dollar is currently trading within a key technical range, a factor that holds FX Markets firmly in balance despite some individual breakouts seen in pairs like NZD/USD or GBP/USD.

As is often the case ahead of pivotal events like the FOMC, the Dollar may test relative extremes, but it rarely poses definitive breakout situations.

The best example of this was ahead of the September Fed Meeting, where the Dollar rushed to make new lows but was inevitably constrained by the bounds of its previous yearly support zones.

The catalyst for the current downside came from NY Fed President John Williams' speech on November 21, which fundamentally shook markets by reintroducing rate cut hopes.

His dovish comments took the 25 basis point cut pricing from 20% all the way to the current stable 87%. This rapid repricing triggered a swift selloff in the Dollar over the past two weeks of trading.

Dollar Index (DXY) 8H Chart. December 4, 2025– Source: TradingView

But, as mentioned in our recent in-depth analysis of the Greenback, the Dollar Index is still maintaining a broad range on the bigger picture, having tested its 200-period Moving Average (and range lows) and currently bouncing above 99.00.

The range highs on the Dollar Index is located at the 100.00 level.

Today, we will look at three key FX Majors and their intraday timeframes to see how the range in the Dollar Index affects their own currency pairs: EUR/USD, USD/CHF, and USD/CAD.

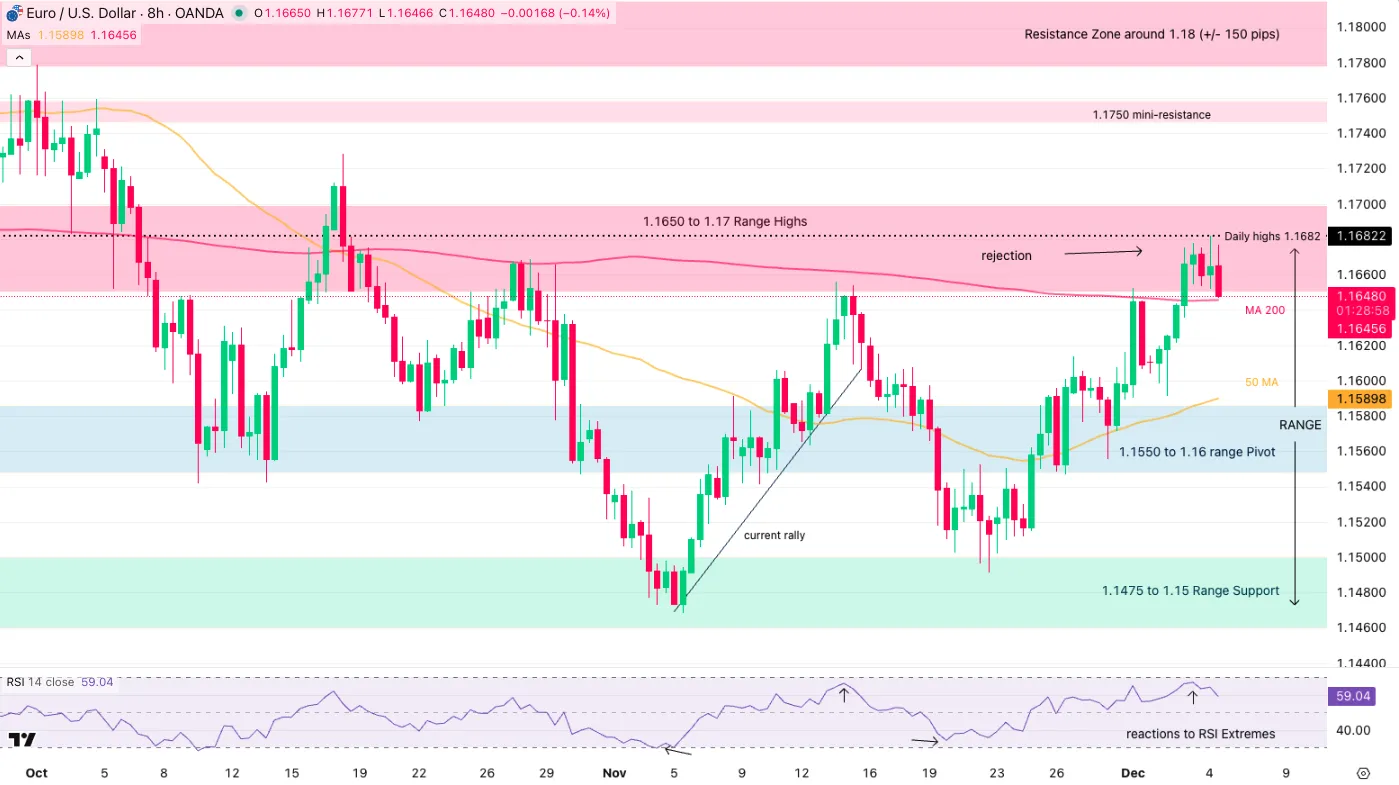

EUR/USD 8H Chart and Technical Levels

EUR/USD 8H Chart. December 4, 2025– Source: TradingView

As mentioned in our November 25 post (On the US Dollar rejecting its range highs), EUR/USD is maintaining a wide Range between 1.15 to 1.17.

As often, the range gets confirmed with:

- Rejection of price after reaching overbought/oversold levels in the RSI

- Flatlining Moving Averages, particularly the MA 200

Currently rejecting its highs, the current setup is one of a sell with a potential stop at range extremes (Above 1.17).

Sellers are currently pushing below the 200-period Moving Average (1.16455), the rejection confirms with a 1H Close below.

Levels of interest for EUR/USD Trading

Resistance levels

- 1.1630 to 1.1670 Pivot zone (range Highs)

- 1.1750 mini-resistance

- Resistance Zone around 1.18 (+/- 150 pips)

- Sep 2021 Highs – Resistance 1.19 to 1.1950 Zone

- Weekly highs 1.1656

Support levels

- 1.1470 to 1.15 range support

- 4H MA 200 Mini-support 1.16190

- 1.1475 to 1.15 Support Zone

- 1.1350 to 1.14 Support

- Session lows 1.14966

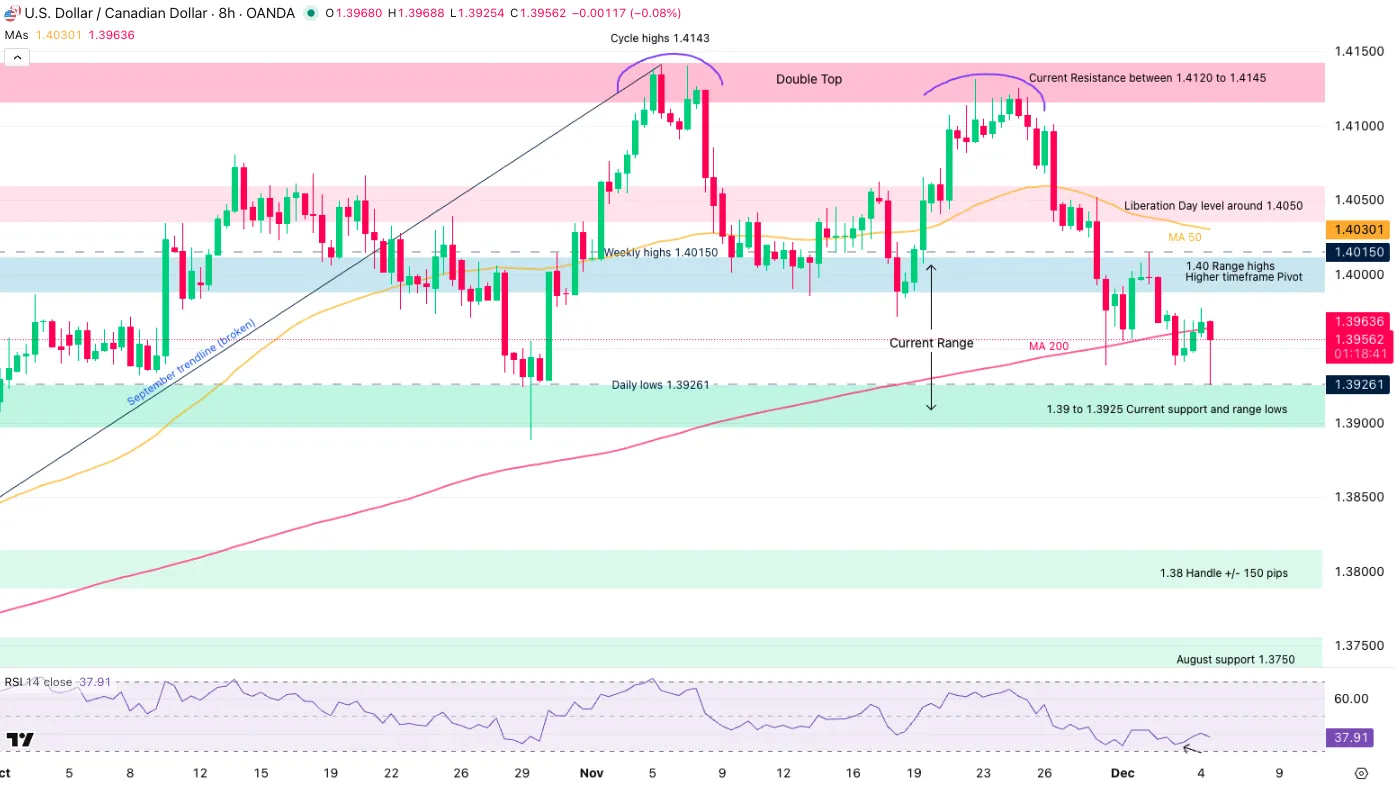

USD/CAD 8H Chart and Technical Levels

USD/CAD 8H Chart. December 4, 2025– Source: TradingView

The rangebound characteristics of USD/CAD are less obvious, but taking a step back, the North American pair has stopped trending since reaching its November and cycle highs.

Holding firmly between 1.39 and 1.40, the currency pair has been seesawing within the 1,000 pip range since the final days of November.

With traders not knowing what to do with the US-Canada deal (it seems like the Canadian government also doesn't know), rangebound conditions also make fundamental sense.

In the case of a break, watch for a daily close above or below to avoid getting trapped.

Note to traders that news on a trade-deal might move things in a flash.

Levels of interest for USD/CAD Trading

Resistance Levels

- 1.40 Major Pivot acting as resistance

- Cycle highs 1.4143 and Double top

- Resistance between 1.4120 to 1.4145

- Key resistance 1.4250

Support Levels

- 1.39 to 1.3925 Higher timeframe pivot, current support

- 1.38 Major support +/- 150 pips

- August range support 1.3750

- 1.3550 Main 2025 Support

USD/CHF 8H Chart and Technical Levels

USD/CHF 8H Chart. December 4, 2025– Source: TradingView

USD/CHF is also stuck within two ranges – A large half-year range between 0.7850 to 0.8140 and another, smaller one but more active: 0.80 to 0.81

We will focus on the smaller timeframe consolidation, also 1,000 pip large.

Buyers are stepping in from the 0.80 Zone after bouncing on the 200-period Moving Average (1.79930).

The current candle is strong, with the ongoing rebound in the USD.

Check out reactions at the highs of the range.

Levels of interest for USD/CHF Trading

Resistance levels

- 0.8075 to 0.81 Range highs

- 0.81244 November highs

- Main resistance 0.8150 to 0.82

- 0.82144 June Highs

Support levels

- 0.80 Range Lows, Higher timeframe Pivot

- 0.7950 Higher timeframe Support

- 0.78575 2025 lows support

Safe Trades!

Sterling breaks key levels in EUR/GBP and GBP/CHF on stronger UK outlook

Sterling is clearly outperforming both Euro and Swiss Franc this week, as markets continue to unwind the defensive positioning built ahead of the Autumn Budget. The announcement was broadly well received, with investors encouraged by the government’s emphasis on fiscal discipline and medium-term stability. The shift has helped ease earlier concerns over the UK’s fiscal outlook while reinforcing confidence in the Pound.

Chancellor Rachel Reeves managed to assemble a broad combination of tax measures that collectively reduce the deficit by more than markets had anticipated. Crucially, the package delivered the fiscal credibility that investors had been demanding without leaning into excessively front-loaded austerity. With meaningful tightening delayed, the budget does not add pressure on the BoE to accelerate its cutting cycle in the coming year.

The UK also received a further tailwind from the OECD, which upgraded its growth outlook for 2026 to 1.2% (from 1.0%) and now sees GDP expanding 1.3% in 2027. The organization cited supportive impacts from Reeves’ budget on consumption, alongside global uncertainty that may keep inflation sticky enough to limit aggressive policy easing. For markets, the upgraded profile reinforces the idea that the UK may outperform its European peers over the next two years.

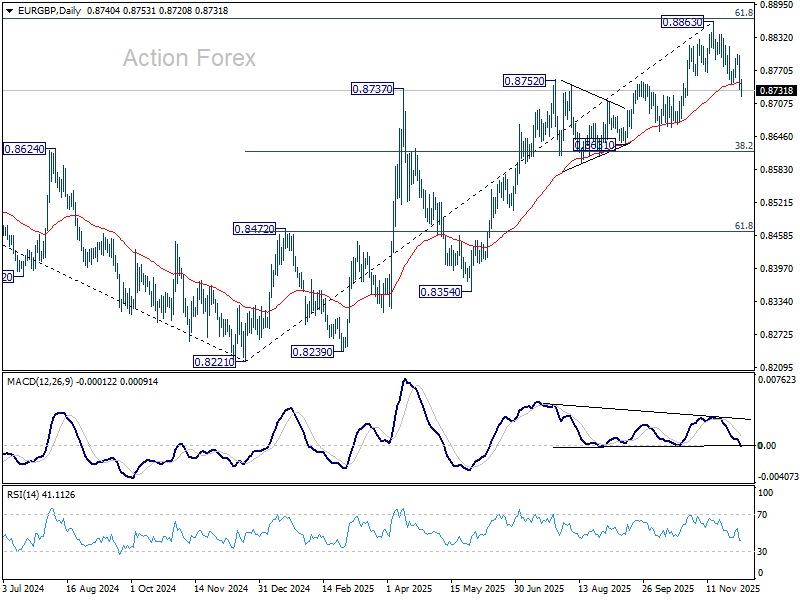

On the technical side, EUR/GBP’s break below the 55 D EMA confirms rejection at the long-term 61.8% retracement of 0.9267 to 0.8221 at 0.8867. With clear bearish divergence on D MACD, the cross should have set a medium-term top at 0.8633.

Deeper fall is now in favor back to 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618), even if the decline from 0.8863 is just a correction to the up trend from 0.8221 (2024 low).

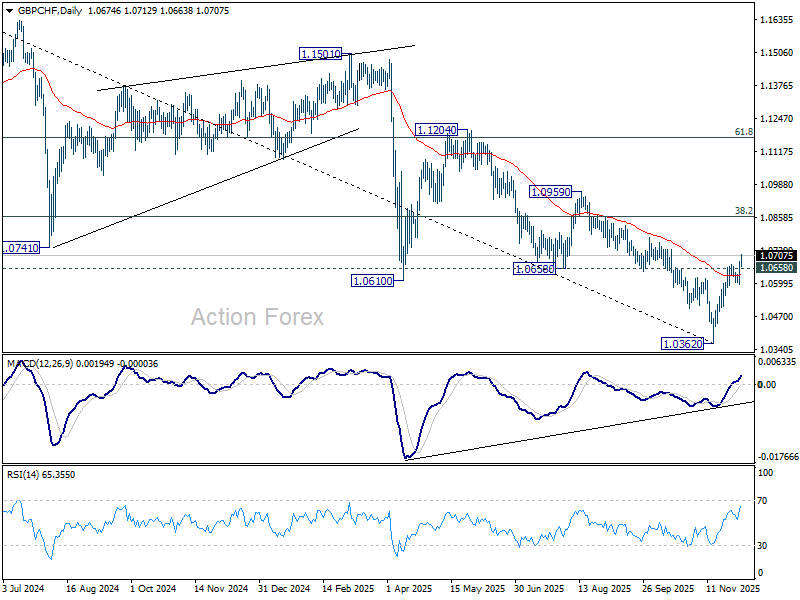

GBP/CHF is also turning structurally higher after breaking above 1.0658 (previous support turned resistance) and 55 D EMA, confirming a medium-term bottom at 1.0362. Bullish convergence in the D MACD supports the upside case, with next targets at the 38.2% retracement of 1.1675 to 1.0362 at 1.0864, and potentially 55 W EMA (now at 1.0906) if momentum continues.

Flashlight for the December FOMC Blackout Period: A Contentious Cut

Summary

- We expect the FOMC to reduce the fed funds rate by another 25 bps to 3.50%-3.75% at its December 10 meeting. The FOMC will not have the October and November Employment Situation and CPI reports as initially planned, but the latest available data suggest continued softening in labor market conditions and receding inflationary pressures outside of tariffs.

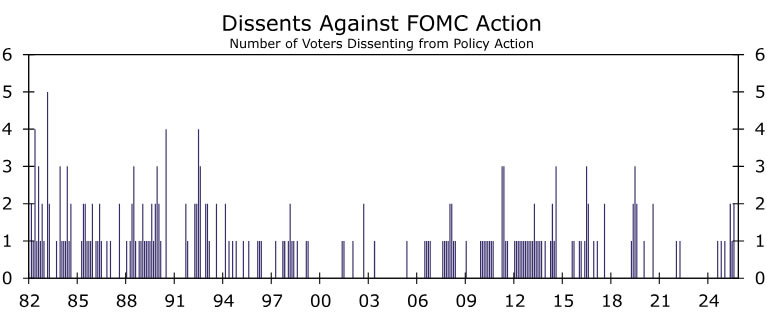

- The FOMC has grown increasingly split over its near-term course of action. Generally speaking, the Board of Governors has a dovish skew, while the regional Fed presidents—who do not all vote—lean more hawkish. Multiple dissents seem likely. While we expect opposition in both directions of the policy decision again, more dissents are likely to be in favor of keeping the policy rate unchanged.

- A more hawkish post-meeting statement could be used to limit the total number of dissents. We expect the statement to signal a higher bar to additional rate cuts and to hint that a hold in January is most Committee members' working assumption.

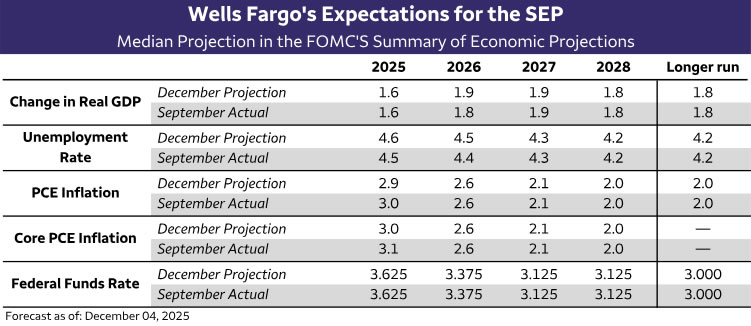

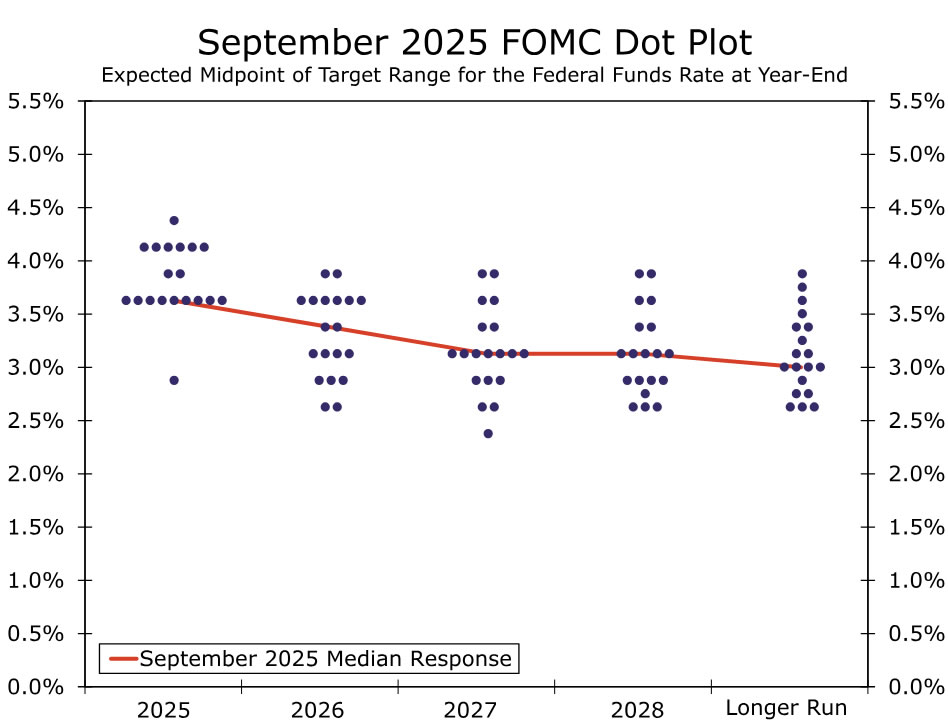

- To the extent that adjustments are coming to the Summary of Economic Projections, we suspect changes to 2025 economic forecasts will be in the direction of higher unemployment and lower inflation—consistent with another 25 bps rate cut at this meeting (see Table). Looking ahead to 2026, major changes seem unlikely. If the medians are to move, we think they are more likely to drift up a tenth or so for GDP growth and the unemployment rate, while edging down a tick for inflation.

- Our expectation is that the median dot for 2026 will remain unchanged at 3.375%. That said, it would take just one participant at the current median of 3.375% moving their dot lower for the median to fall. Given the potential for a slightly higher unemployment rate and slightly lower inflation in the 2026 projections, we see the risks to the 2026 median dot as skewed to the downside.

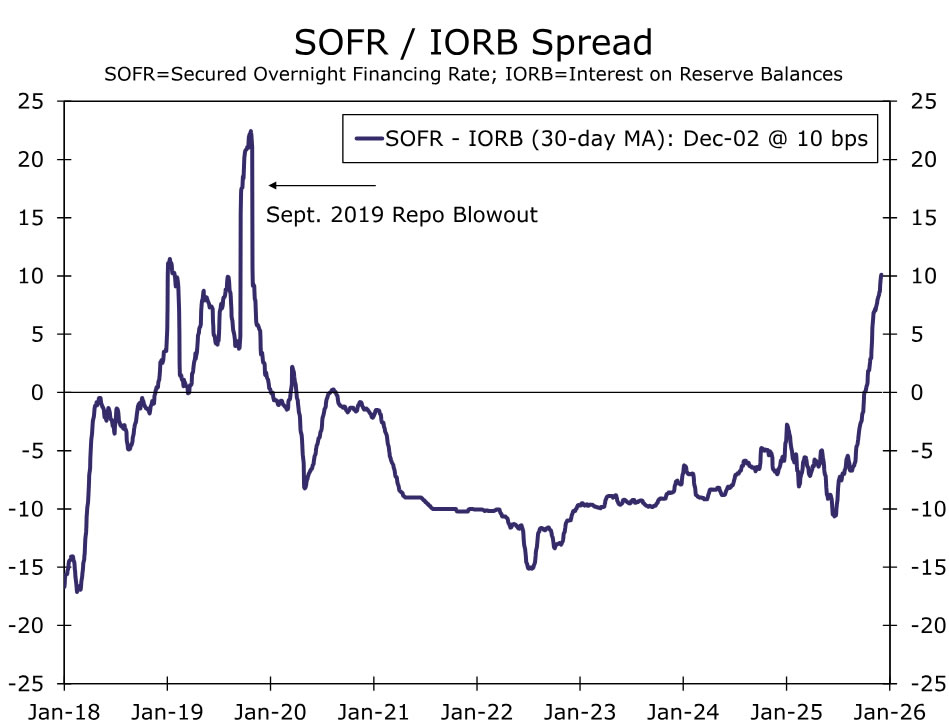

- With quantitative tightening (QT) having ended on December 1, attention has turned to when reserve management purchases will begin to preserve the Fed's ample reserve framework. We do not expect a decision at this meeting, and instead look for the start of reserve management purchases to be announced at the March 18 meeting.

Jobs Market Softness Enough to Keep FOMC on Course for Another Cut

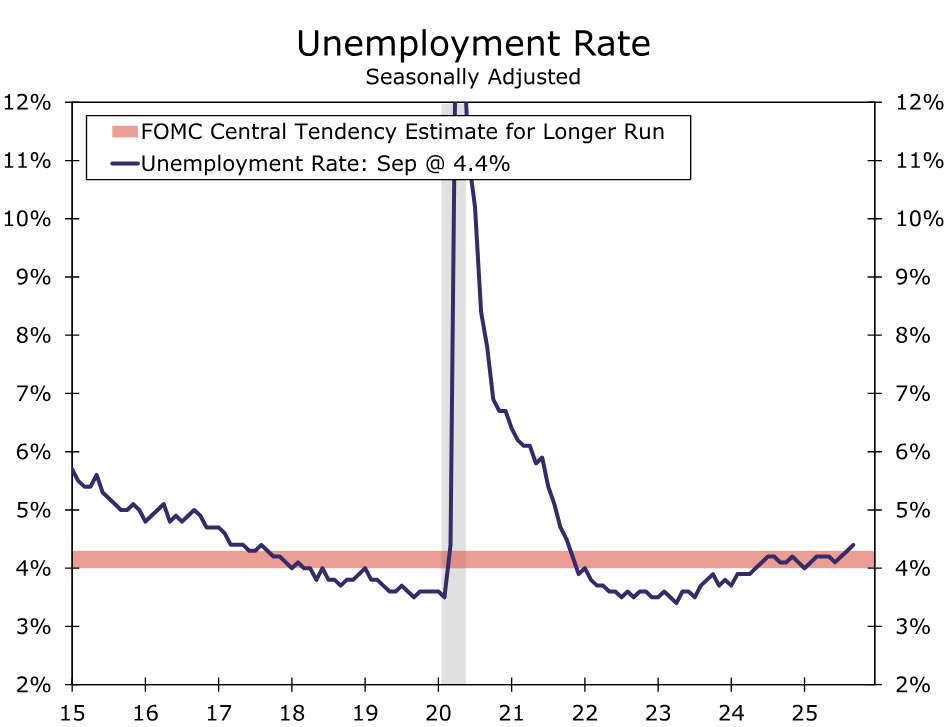

We expect the FOMC to proceed with returning policy toward a more neutral stance and reduce the fed funds rate by another 25 bps to 3.50%-3.75% at its upcoming meeting on December 9-10. Although the FOMC will not have the October and November jobs report at this meeting as initially planned, the latest available labor market data suggest that conditions have continued to slowly soften. While nonfarm payroll growth firmed in September, the unemployment rate rose to 4.44%, placing it above the Committee's central tendency range for "maximum employment." (Figure 1).

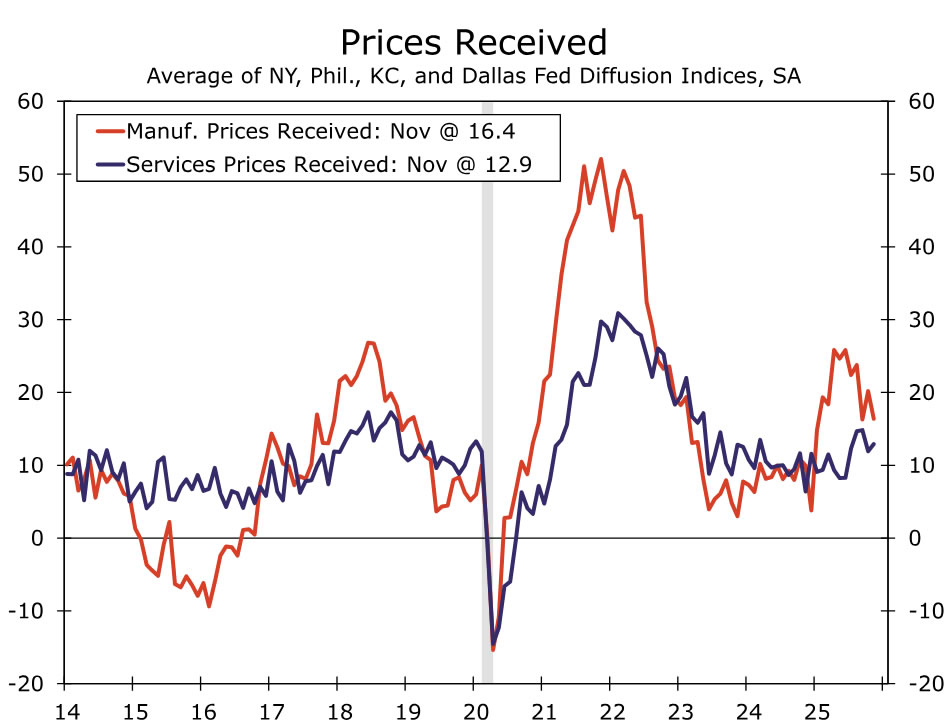

Fresh data on inflation since the FOMC last met have been more limited. The Committee will receive the September PCE price index prior to its upcoming meeting. The PPI and CPI data for that month point to the Fed's preferred measure of inflation rising 2.8% in the 12 months through September on both a headline and core basis, largely unchanged from the readings seen over the summer. While still frustratingly above target, there are few signs of inflationary pressures bubbling up further, in our view. Average hourly earnings growth is generally consistent with 2% inflation, while the September PPI showed the pickup in inflation this year remains limited to the goods sector. Inflation expectations generally remain well-anchored, and businesses also appear to be raising prices a bit more slowly over the past month or so. Fewer firms in the NFIB survey have been reporting higher prices, while the latest regional Fed PMIs show prices received moderating (Figure 2).

A Fed Divided

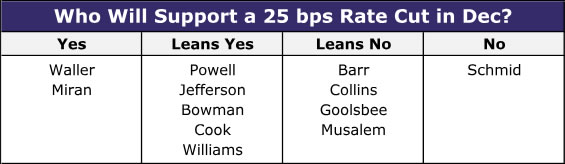

With inflation continuing to run above target and the FOMC having already cut 50 bps since the summer, the Committee has grown increasingly split on its next course of action. The public comments from FOMC officials in recent weeks reflect this unusually deep divide. Governors Miran and Waller have explicitly stated their support for rate cuts at the December meeting. Governors Jefferson, Bowman and Cook have not been quite as explicit in their support, but their public remarks in recent months lead us to believe they also will support another 25 bps rate cut in December. If there is a hawk lurking on the Board, it is probably Governor Barr. Governor Barr expressed some concern that "we're seeing inflation still at around 3% and our target is 2%" in comments on November 20.

In contrast, the voting regional Fed presidents have sounded more hawkish. Kansas City Fed President Jeffrey Schmid dissented against cutting rates in October and seems likely to do so again in December. Boston Fed President Susan Collins recently expressed no "urgency" for more accommodative monetary policy, while St. Louis Fed President Alberto Musalem said there was "limited room for further easing without monetary policy becoming overly accommodative." Even the oft-dovish Chicago Fed President Austan Goolsbee has sounded more skeptical of additional rate cuts in his recent public remarks. Yet, there was one key exception to the hawkish tilt of regional Fed presidents recently. New York Fed President John Williams stated on November 21 that he sees room for another rate adjustment "in the near term," a key signal that this leader on the FOMC seems likely to support a December cut. Conspicuously quiet in recent weeks has been Chair Powell, who has not made any public comments on monetary policy since the last FOMC meeting on October 29-30.

We believe that, on net, there will be a critical mass of support for a 25 bps rate cut in December, particularly among the FOMC's leadership (Figure 3). That said, there is clearly disagreement within the ranks. Should the Committee cut rates like we expect, we can easily envision three or four votes against the action, with dissents once again possible in both directions of the policy decision. Governor Miran in particular could dissent in favor of a 50 bps cut if his vote is not needed to lock in 25 bps. The last time there were three dissents was September 2019, while four dissents last occurred in October 1992 (Figure 4).

The Statement Will Be Used to Limit Hawkish Dissents

We believe the ultimate number of dissents will depend on the guidance the Committee provides about future policy adjustments in its post-meeting statement. To help appease voters who are reluctant to cut again at this particular meeting, we expect the statement to signal a higher bar of additional rate cuts. This could be done by saying, "In considering the timing and extent of any additional adjustments to the target range for the federal funds rate...", with the italicized portion an insertion to the current statement text. Additional emphasis on returning inflation to the FOMC's 2% target could also help muster support from some hawks frustrated by inflation's lengthy overshoot of target.

In the opening paragraph on recent economic conditions, we expect the statement to be unchanged except in reference to the labor market. We could see the sentence on the jobs market truncated to merely state that "Job gains have slowed this year, and the unemployment rate has edged up but remains low." The acknowledgment of the labor market's ongoing cooling would be consistent with the Committee moving forward with another cut at this meeting.

SEP: No Change to the Median Dots

The upcoming FOMC meetings will include an update to the Summary of Economic Projections (SEP). The median projections in the current SEP, last updated in September, still look about right for 2025, in our view. A 4.5% unemployment rate for 2025 is in line with our most recent forecast from November 19, although September's upside surprise of 4.4% opens the door to the median edging up to 4.6%. The median SEP projections for headline and core PCE inflation of 3.0% and 3.1%, respectively, are modestly above our latest projections of 2.8% and 3.0%, respectively, but they are not dramatically out of line either. Although the government shutdown has clouded the outlook, the economic data appear to have been moving in line with the median participant's 2025 projections from back in September.

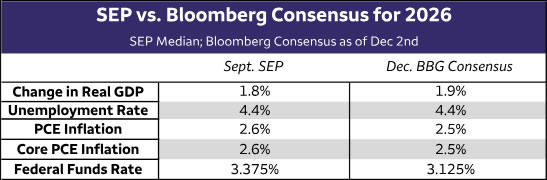

Looking ahead to 2026, we do not see much reason for the economic projections to change materially. The median projections from September are broadly in line with the latest Bloomberg consensus forecasts for 2026 (Figure 5). If the medians are to move, we think they are more likely to drift up a tenth or so for GDP growth and the unemployment rate, while edging down a tick for inflation. (Table).

More notably, the median Committee participant projects 25 bps less easing than the Bloomberg consensus and our own forecast for 2026 (Figures 5 and 6). Our expectation is that the median dot for 2026 will remain unchanged at 3.375% in a sign that most participants on the Committee have not materially changed their minds about the appropriate stance of monetary policy next year. An unchanged median dot in 2026 also would be another nod to the simmering hawkish sentiment among some participants on the Committee. That said, it would take just one participant at the current median of 3.375% moving their dot lower for the median to fall. Given the potential for a slightly higher unemployment rate and slightly lower inflation in the 2026 projections, we see the risks to the 2026 median dot as skewed to the downside.

We expect the median dots beyond 2026 to remain unchanged as well. The dots for 2027 and 2028 are more clustered around the median and, being so close to neutral, seem less likely to move. The longer run median seems primed to rise by 12.5 bps or 25 bps at some point given the skew, but we have no reason or cause to believe it will occur at this meeting.

Likely No Changes to Balance Sheet Policy in December

At its previous meeting, the FOMC announced the end of quantitative tightening (QT) effective December 1. The end of QT has sparked a debate about when the Federal Reserve will begin growing its balance sheet again in the form of reserve management purchases. Reserve management purchases are a staple tool of the ample reserve framework used by the Federal Reserve to maintain interest rate control and ensure the smooth functioning of financial markets. It is important to understand that reserve management purchases are distinct from quantitative easing (QE) asset purchases meant to stimulate the economy. The latter involve the central bank buying longer-dated Treasury securities and mortgage-backed securities, putting downward pressure on longer-term interest rates and mortgage spreads and thus easing financial conditions. These purchases also often have a signaling effect as markets anticipate that rate hikes remain a long way off while QE is happening.

In contrast, reserve management purchases involve swapping one riskless asset (bank reserves) for another essentially riskless asset (Treasury bills) to ensure bank reserves remain ample. Federal Reserve officials have been very clear (see here and here as examples) that these purchases would be the next phase of reserve management policy and in no way represent a change in the stance of monetary policy. We agree with this assessment, and the beginning of reserve management purchases will have no bearing on our view of the stance of monetary policy.

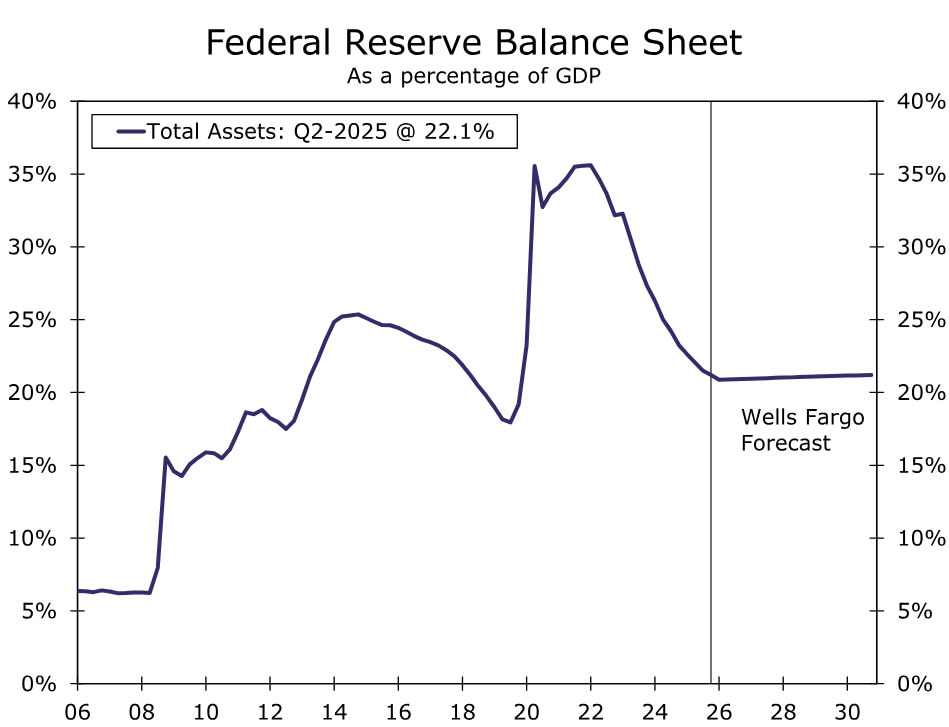

Our expectation is that the FOMC will announce the start of reserve management purchases at the March meeting, with purchases beginning April 1. If realized, the Fed's balance sheet would start to grow again in nominal terms, although it would be roughly unchanged as a share of GDP (Figure 8). We estimate that these purchases will total approximately $25 billion per month and be comprised entirely Treasury bills. The FOMC may not immediately begin with purchases of this size and instead might phase them in similar to how QT was tapered down.

We think the risks are skewed toward an earlier start date for reserve management purchases, e.g., announced at the January meeting for a February start. We will be watching money market conditions closely into year-end as we fine tune our forecast. Repo rates have risen sharply relative to the interest rate the Fed pays banks on its reserves, a sign that funding conditions have tightened notably (Figure 9). If year-end goes relatively smoothly, we likely will be inclined to stick with this timing, whereas if it is a sloppy year-end, we would be inclined to pull-forward our forecast for the start of reserve management purchases.

USD/JPY Drops Below 155.00: Has 2025 Yearly Top Been Reached?

After two months of a relentless rout in the Yen, the Japanese currency is finally finding some stable ground.

The core of the current reversal lies in the clash between the administration’s fiscal policy and the central bank’s monetary response: fiscal recklessness has finally been met with monetary soundness.

Prime Minister Takaichi has been pushing to implement massive stimulus packages, while also pressuring the Bank of Japan to keep rates low to support these projects.

Still, Markets don't get by the "cheap money" concept, which has led to a precipitous 5% to 8% move in the JPY against most majors since the beginning of October.

To balance things out, a round of increasingly hawkish tones from Bank of Japan Governor Kazuo Ueda has reversed the course over the past few weeks, winning his first showdown against Takaichi – as provided by a Reuters Headline.

Ueda confirmed overnight that current policy remains "accommodative" even after recent adjustments, underscoring the necessity of a planned exit from ultra-loose policy – The next BoJ Meeting is on December 19.

The Central Bank is actively working to narrow its estimate of the neutral rate (the level that is neither stimulative nor restrictive).

This rhetoric has created a strong market expectation for a December rate hike, supplemented by strong Japanese Inflation reports.

Complemented by some renewed weakness in the US Dollar, the Yen’s resurgence has led to a top being found in USD/JPY, which has plunged more than 2% off its November highs.

Let's examine the charts to see if technicals suggest a definite top or a temporary resistance.

USD/JPY Multi-Timeframe Analysis

Daily Chart

USD/JPY Daily Chart. December 4, 2025 – Source: TradingView

Since the change in tone from the Bank of Japan, the sky-high prices have been rejected in a daily tight bear channel formation (Where no green candle overlaps the preceding red bar – A sign of seller strength).

Falling 3,000 pips from its highs, the pair has broken below the key 155.00 psychological level but remains above its Daily Pivot Zone, decisive for long-term bull/bear strength.

Looking at the Daily RSI, it's currently crossing the neutral zone which confirms the shift in trend but isn't yet in bearish territory.

Traders will have to consider tomorrow's US Core PCE release, but barring any major crazy beat, the path for USD/JPY is towards some downside.

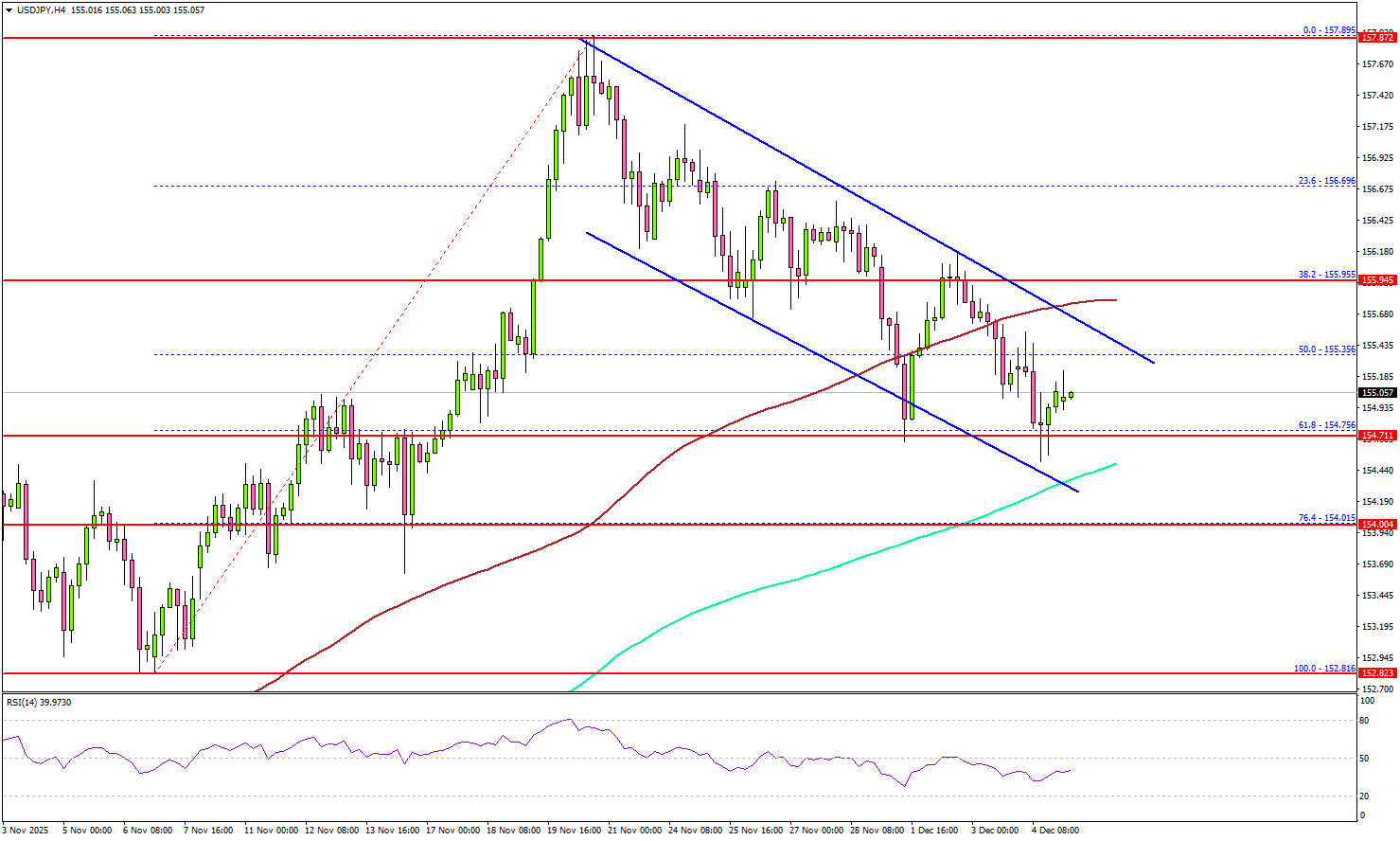

4H Chart and Technical Levels

USD/JPY 4H Chart. December 4, 2025 – Source: TradingView

USD/JPY technical levels of interest:

Support Levels:

- Session Lows 154.50 and Short-timeframe support

- 153.00 to 154.00 Key Resistance now Pivot

- 50-Day MA 153.00

- 150.00 Psychological Support and 50-Week MA

- 146.00 August Range Main Support

Resistance Levels:

- December 1 highs 156.15 (short-term resistance – 156.00 to 156.30)

- 156.90 to 157.95 recent peak resistance

- 2025 Highs and April 2024 peaks 158.80 to 160.00

- 1990 and July 2024 Peak 161.00 to 162.00

1H Chart

USD/JPY 1H Chart. December 4, 2025 – Source: TradingView

Looking closer to the 1H Timeframe, we spot prices evolving within a downward channel and remaining below the two key 50 and 200-period Moving Averages, the intermediate trend is bearish.

Still, the corrective move may have reached a temporary bottom with the RSI reaching oversold and a rebound attempt is ongoing.

For interesting levels to join the trend, monitor two levels:

Reactions at 155.00 (+/- 100 pips) to spot if the level attract further movement towards the channel lows

On further mean-reversion higher, look at 155.40 which is the 50-H Moving average.

For bulls, look at a break and close above the channel (155.50)

Expect traders to wait for Core PCE for decisive moves.

Safe Trades!

Sunset Market Commentary

Markets

FI, once again, is where most of the market attention went to today. It originated, once again, from Japan where a more than solid demand for a 30-yr JGB auction failed to prevent yields rising in maturities up to 20 year. A Reuters report that the Takaichi government is said to tolerate a BoJ rate hike this month added a little fuel to the fire. Such a move still isn’t fully discounted even though the stars are aligning. The market implied probability did rise from <60% on Friday to 80% in recent days on BoJ governor Ueda’s speech on Monday and further to 89% today. Japan’s 10-year yield hit the highest level since 2007 at 1.94%. The closely watched reference is now 6 bps away from the pre-GFC highs. The Japanese yield situation warrants close monitoring with higher local yields pulling back or keeping capital at home (reversing the long-popular carry trade). Less huge (foreign) buyer of particularly long term bonds – next to central banks and traditional buyers such as pension funds and life insurers – comes at a tricky time when huge supply (government deficits) is already competing for demand. JGBs reaffirmed their importance for global bond markets by dragging Bunds and Treasuries down with them. US yields today add between 2 and 3.5 bps. The front-to-middle segment underperforms marginally following a steep drop in US jobless claims. The 219k reading was the lowest since September 2022. The holiday-shortened week ending Nov 29 came with some Thanksgiving-related distortions that some say help explain the low reading. It won’t alter the Fed’s intentions for next week though. German yields add 0.5-2 bps across the curve. Bunds underperform vs swap with market chatter growing about a potential demise of Merz’ seven months old government. A group of Merz’ own CDU lawmakers rebelled against a pension bill. The 18 that did effectively exceed the CDU/SPD’s majority of 12. Should the group continue to do so in tomorrow’s final vote and the Left party does not abstains (as they said they would), the SPD co-leader Bas said earlier this week it could spell the end of the coalition. New elections according to the polls would favour the extremes, the far right in particular. It wouldn’t come at a worse time after French politics this week also rearing its head again when coalition partner Les Horizons said it wouldn’t support the social security budget bill in December 9’s vote. French OAT/swap spreads have been trending higher all week and trade back above Italy’s. The euro doesn’t want to frontrun any German or French political upheaval for now with EUR/USD holding steady around a 1.5 month high of 1.167 but it’s a tense situation. JPY outperforms, pushing USD/JPY back below 155 for a second time this week. EUR/JPY is also down on the day but remains near the record highs north of 180.

News & Views

Czech inflation unexpectedly fell by 0.3% M/M in November (+0.1% consensus), bringing the annual number down to 2.1% Y/Y instead of the expected stabilization at 2.5%. Gauges for core inflation slowed from 3.2%/3.3% Y/Y to 2.9%/3% Y/Y. Details showed steep drops in goods (-0.6% M/M and +0.6% Y/Y from 1.3%) and food prices (-0.8% M/M & +2.8% Y/Y from 3.9%). Within food subcategories, it were processed food, alcohol & tobacco prices that fell while unprocessed food prices still increased (+0.8% M/M & +1.9% Y/Y from 3.3%). Energy prices were 0.1% lower compared with October and 3.8% lower versus November of last year. Services inflation (+0.1% M/M) held steady at 4.6% Y/Y. The Czech Statistical Office also released Q3 wage data today. Nominal wages increased by 7.1% Y/Y (from +7.6% Y/Y in Q2) with real wage growth coming in at 4.5% Y/Y (from 5.1% Y/Y in Q2), almost matching expectations (+4.6%). The Czech koruna lost ground after inflation numbers with EUR/CZK rising from 24.10 to 24.22. CZK swap yields lose 7 to 9 bps across the curve in a slight bull steepening move.

The Bank of England’s Decision Maker Panel (DMP) survey showed stable price and wage growth metrics at firms in November. Year-ahead and three-year-ahead CPI inflation expectations were unchanged at 3.4% and 3% respectively. Realized annual own-price growth and realized annual wage growth remained steady as well, at 3.8% and 4.5%. Both year-ahead measures increased by 0.1pp compared with October to 3.7% and 3.8%. Employment is contracting with realized and year ahead employment growth falling by 0.7% and 0.2% respectively. The profit margin outlook is mixed, with equal shares expecting improvement or stability (both 38%) next year.

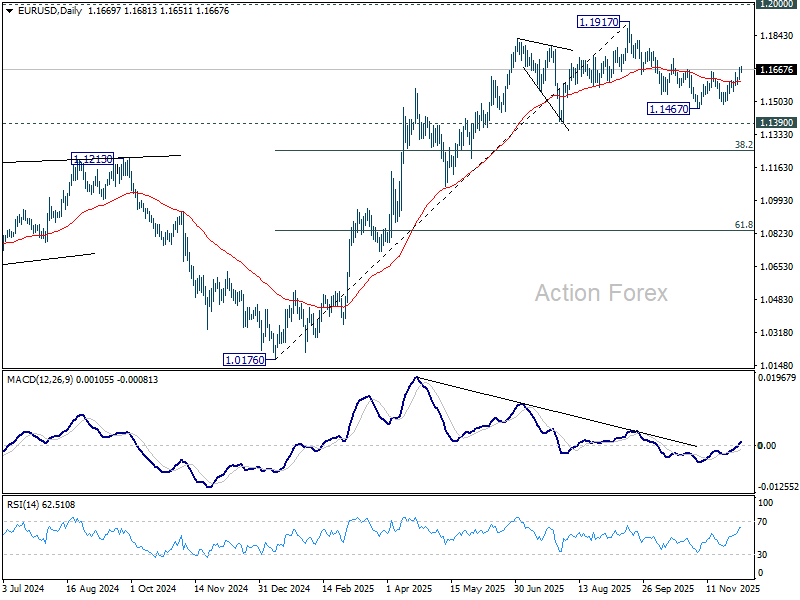

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1635; (P) 1.1657; (R1) 1.1692; More….

Intraday bias in EUR/USD remains on the upside at this point. Fall from 1.1917 should have completed at 1.1467. Further rise should be seen to 1.1727 resistance first. Firm break there will bring retest of 1.1917 high. Nevertheless, below 1.1590 minor support will mix up the outlook and turn bias neutral again.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1345) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

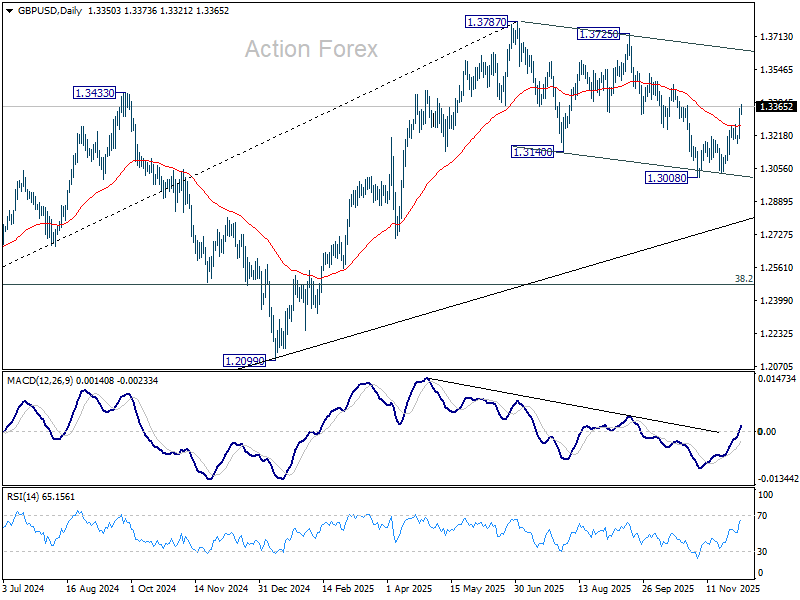

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3250; (P) 1.3303; (R1) 1.3405; More...

Intraday bias in GBP/USD remains on the upside for the moment. Fall from 1.3787 could have completed as a correction at 1.3008. Firm break of 1.3470 resistance will pave the way to retest 1.3725/3787 resistance zone. On the downside, below 1.3274 resistance turned support will turn intraday bias neutral first. But risk will stay on the upside as long as 1.3718 support holds, in case of retreat.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

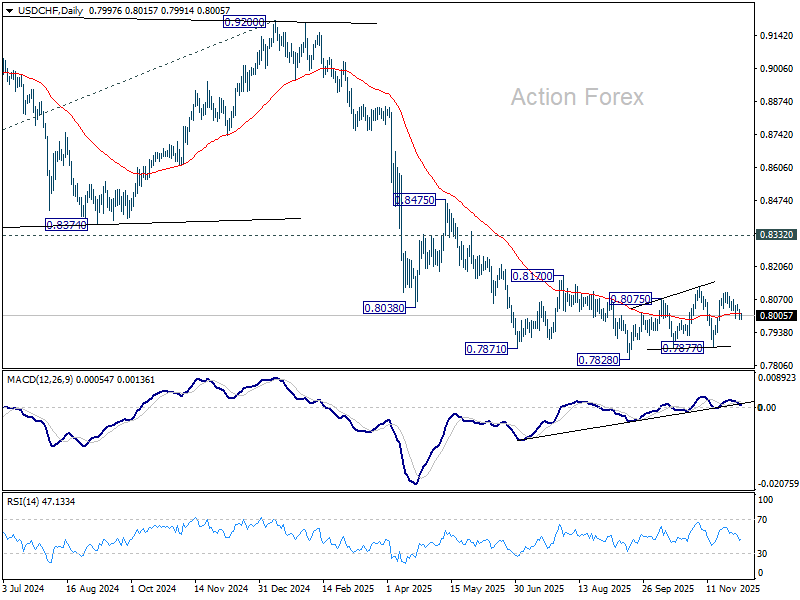

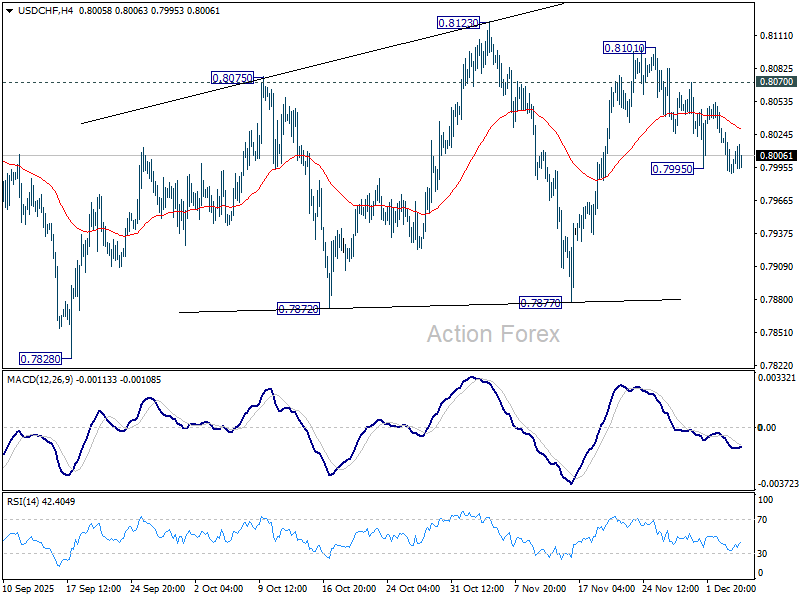

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7978; (P) 0.8010; (R1) 0.8028; More…

No change in USD/CHF's outlook and intraday bias stays neutral. Price actions from 0.7828 low is seen are a corrective pattern. On the upside, above 0.8070 will indicate that pattern is still extending, and turn bias back to the upside for 0.8123 and above. On the downside, below 0.7995 will bring deeper fall back towards 0.7877 support.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).