Sample Category Title

AUD/USD: Advances for the Eleventh Straight Day

AUD/USD holds in steep uptrend for the eleventh consecutive day and on track for the second straight weekly gain, mainly driven by weaker US dollar on growing expectations of Fed rate cut, but also holding firm tone against other major currencies.

The pair hit new 2 ½ month high on Friday and cracked strong barriers at 0.6640 (200WMA / Fibo 76.4% of 0.6706/0.6421 descend) where bulls may face headwinds, as daily studies are overbought and Friday’s profit-taking may also contribute to potential price easing.

Investors await release of (delayed) US Sep PCE price index, one of Fed’s inflation gauges, which is to provide additional information to US policymakers ahead of next week’s policy meeting.

Firmly bullish daily studies (multiple MA bull-crosses / strong positive momentum) underpin the action, with dips to ideally find ground above 0.6600 zone (broken Fibo 61.8% / hourly higher low / top of hourly Ichimoku cloud), while potential deeper pullback should be contained by top of daily cloud / broken Fibo 50% (0.6560) to still mark a healthy correction and provide better levels to re-enter strong bullish market for push towards 0.6706 (2025 peak, posted on Sep 17).

Res: 0.6660; 0.6688; 0.6706; 0.6730.

Sup: 0.6630; 0.6600; 0.6560; 0.6541.

Canada’s Unemployment Rate Tumbles as Employment Jumps, Again

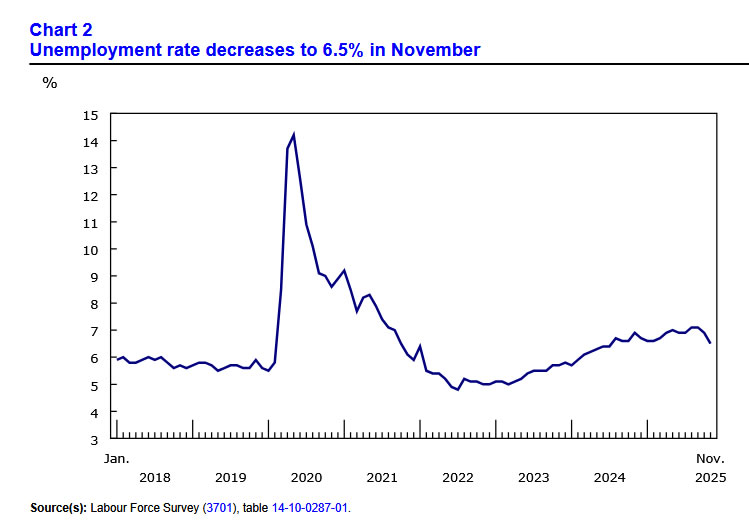

Canada's economy added another 54k jobs in November (+0.3% month/month), 57k more than consensus expectations for a 2.5k decline. The details weren't quite as strong with full-time positions falling 9k, while part time added 63k.

The unemployment rate tumbled to 6.5% from 6.9% in October (consensus expectations were for a rise to 7.0%). Even better, the job finding rate (19.6%) was slightly elevated relative to last year and Statistics Canada noted that, "increases in the unemployment rate earlier in the year had been associated with lower job finding rates". The unemployment rate was helped lower by 26k workers who left the labour force. The labour force participation rate fell 0.2 ppts.

Job gains were concentrated in health care and social assistance (+46k), accommodation and food services (+14k), and natural resources (+11k). The biggest losses were in wholesale and retail trade (-34k).

Wage growth ticked higher in November, with average hourly wages up 3.6% versus a year ago (3.5% in October).

Key Implications

Oh boy, that's a pleasant surprise. Sure, the details suggest that part-time work is leading the charge on employment these past few months, but it's impossible to ignore that the jobless rate has fallen from 7.1% in September to 6.5% as of last month. The takeaway has to be that the Canadian labour market is in better shape than most had thought. That said, this situation can't be characterized as "good". The unemployment rate is still elevated, and job gains have been concentrated in part-time work. So, while this is an improvement, there is still room for recovery.

The Bank of Canada's next decision is due next week, and the past few employment reports have painted an encouraging picture of where the economy stands. However, there is still slack in the labour market and the trade picture heading into next year remains highly muddled. Our view is with the inflation rate expected to continue moderating, the Bank will remain on the sidelines next week and continue to look for signs that a sustained recovery is in the works.

Canada employment jumps 53.6k in October, unemployment rate falls sharply to 6.5%

Canada’s labor market delivered a major upside surprise in November, adding 53.6k jobs versus expectations of a small -1.5k decline. The strength came almost entirely from part-time positions, which rose by 63k, offsetting a modest dip in full-time work. The gain pushed the employment rate up 0.1% to 60.9%, marking a notable stabilization after a year of softening labor momentum.

The unemployment rate dropped sharply from 6.9% to 6.5%, defying expectations for a rise to 7.0%. This reverses part of the labor market deterioration seen through most of 2025, when unemployment climbed to 7.1% in September—its highest level since 2016. The improvement suggests that labor demand remains healthier than previously believed, even in a slowing economic environment.

Wage data also supported the stronger labor picture. Average hourly earnings rose 3.6% yoy in November, up slightly from October’s 3.5% yoy, reaching CAD 37.00.

Gold Price Analysis: Market Awaits Key Updates

The ADX indicator on the 4-hour XAU/USD chart has dropped to a multi-month low, signalling the absence of a clear trend.

At the same time, a technical assessment of price movements allows for the construction of a symmetrical triangle pattern with a central axis around $4,205 — indicating that the current price reflects an equal balance of major drivers, including:

→ Weakening conditions in the US labour market. According to media reports, ADP recorded an unexpected decline of 32,000 private-sector jobs, while Challenger reported 71,000 layoffs in November, bringing the total number of job cuts since the start of the year close to 1.17 million.

→ Rumours that White House economic adviser Kevin Hassett may replace Federal Reserve Chair Jerome Powell in May — a development that has strengthened expectations of more aggressive policy easing in 2026.

It is worth noting that on 1 December, gold briefly rose above the November high — a move that coincided with silver reaching an all-time record (as suggested in our analysis on 27 November). However, the bulls failed to hold the price above $4,245, indicating a lack of sufficient buying interest. It appears that traders require stronger justification to purchase gold at such elevated levels.

Most likely, market participants have adopted a wait-and-see stance ahead of key releases:

→ Personal Consumption Expenditure (PCE) data for September, whose publication was delayed by the shutdown;

→ Next week’s FOMC decision (10 December).

Although the market currently appears balanced, XAU/USD may be functioning like a “compressed spring”. Be prepared for bursts of volatility.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Gold Steady Near 4,200 USD as Markets Await Key Data

Gold prices held close to 4,200 USD per ounce on Friday, with investors focused on a significant, delayed inflation report ahead of next week’s Federal Reserve policy decision.

All attention is on the release of the September Personal Consumption Expenditures (PCE) index, the Fed’s preferred inflation gauge. The data could be decisive in shaping expectations for the timing and scale of upcoming monetary easing.

Earlier in the week, further signs of a cooling labour market emerged. ADP reported an unexpected decline of 32,000 in private sector payrolls, while the Challenger report recorded 71,000 layoffs in November – bringing the year-to-date total to nearly 1.17 million.

This combination of soft employment figures has reinforced investor conviction that the Fed will cut rates as early as next week, with the market-implied probability now standing at approximately 87%.

Adding to the dovish narrative are reports that White House economic adviser Kevin Hassett may succeed Jerome Powell as Fed Chair in May. Markets interpret this as a potential tilt towards more aggressive policy easing.

Despite a moderately lower weekly close, gold remains well-supported heading into the critical data release.

Technical Analysis: XAU/USD

H4 Chart:

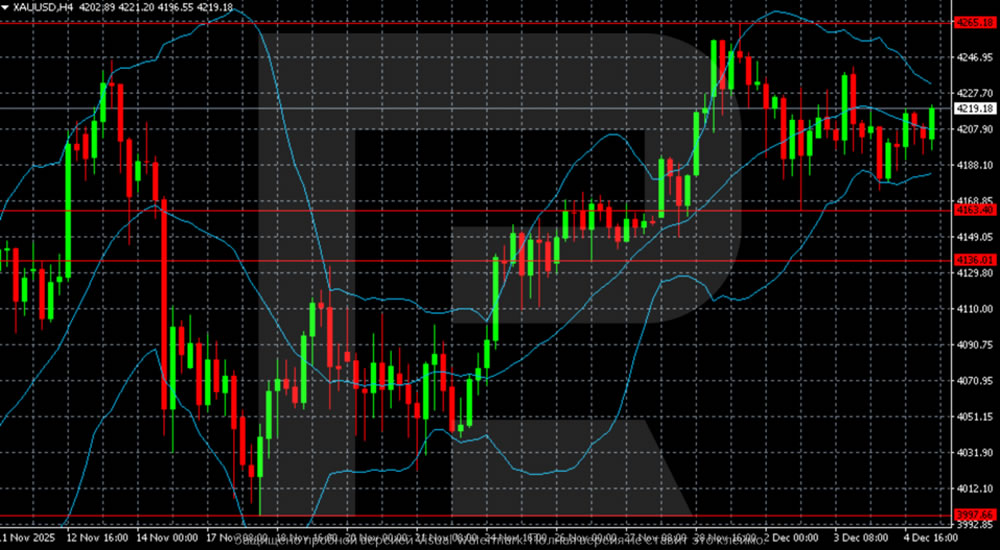

On the H4 chart, gold (XAU/USD) is consolidating after its recent advance toward 4,220–4,230 USD. The price remains above the middle Bollinger Band, with the upper band turning slightly upward, suggesting an attempt to recover from recent weakness.

Key resistance is around 4,265 USD, a level the market has repeatedly tested without securing a decisive breakout. A sustained move above this level would clear the path towards 4,300 USD and beyond.

Immediate support is marked at 4,163 USD. A break below this level would increase selling pressure and raise the risk of a decline towards the next demand zone near 4,136 USD. A close below 4,136 USD would signal a transition into a deeper corrective phase.

H1 Chart:

On the H1 chart, XAU/USD is trading within a tightening range between 4,188 USD and 4,220 USD, reflecting mixed short-term momentum. The middle Bollinger Band is providing near-term equilibrium, confirming the absence of a clear directional bias.

The upper Bollinger Band is capping advances near 4,220–4,225 USD, with several rejections from this zone indicating local overbought conditions. The lower band is offering support around 4,185–4,190 USD.

A sustained move above 4,220 USD would signal a resumption of bullish momentum, initially targeting 4,235–4,240 USD, and potentially 4,265 USD. Conversely, a break below 4,185 USD would open the way towards 4,163 USD. A loss of this support could intensify corrective pressure and expose the 4,136 USD level.

Conclusion

Gold remains in a holding pattern near 4,200 USD as traders await the delayed PCE inflation report. While labour market softness has bolstered expectations for Fed easing, the technical picture reflects consolidation within a defined range. A decisive reaction to today’s data is likely to set the tone ahead of next week’s FOMC meeting, with a break above 4,265 USD opening the door to further gains, while a drop below 4,163 USD risks a deeper correction.

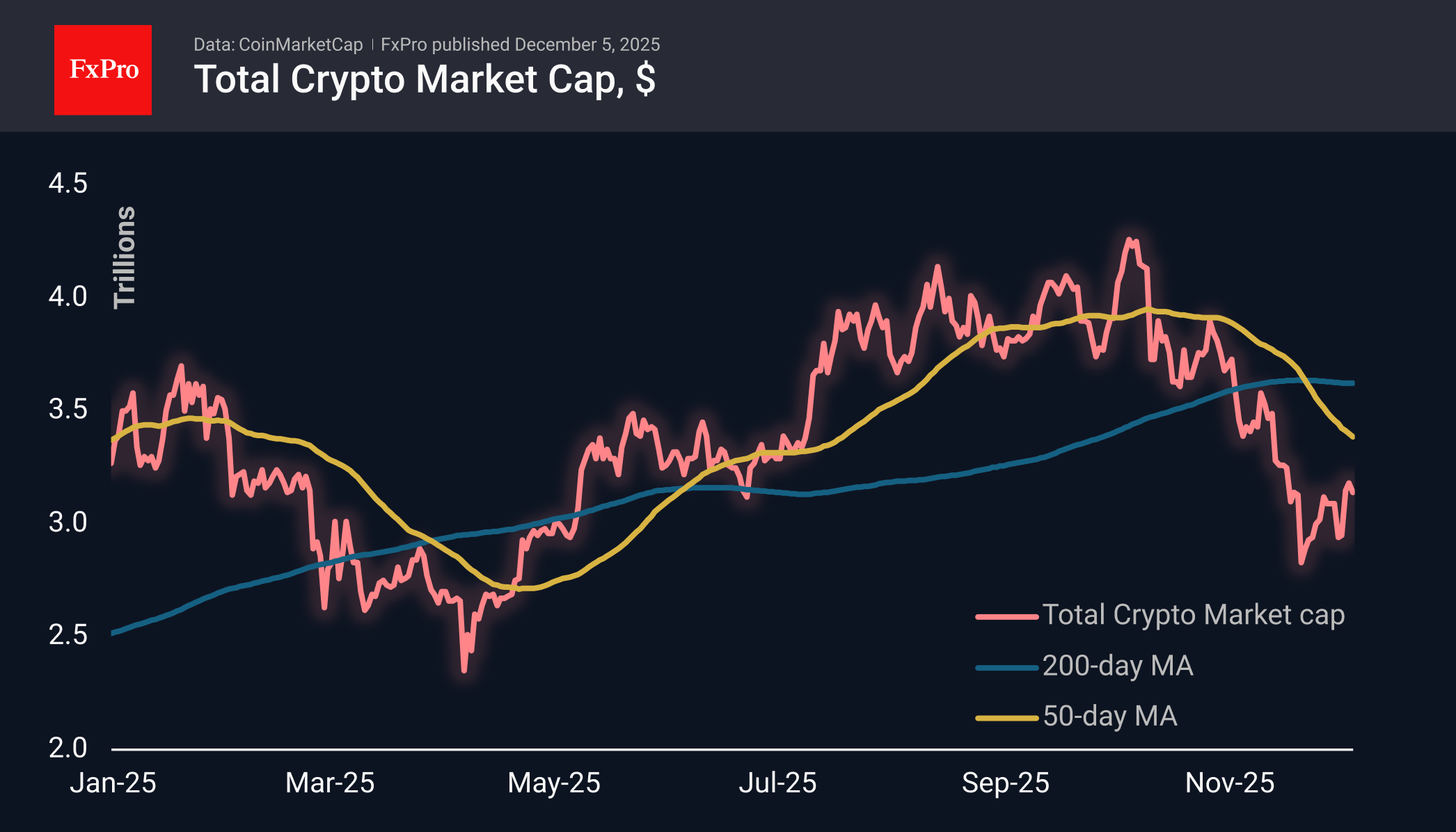

Bear Market Rebound in Crypto is Likely to Continue

Market Overview

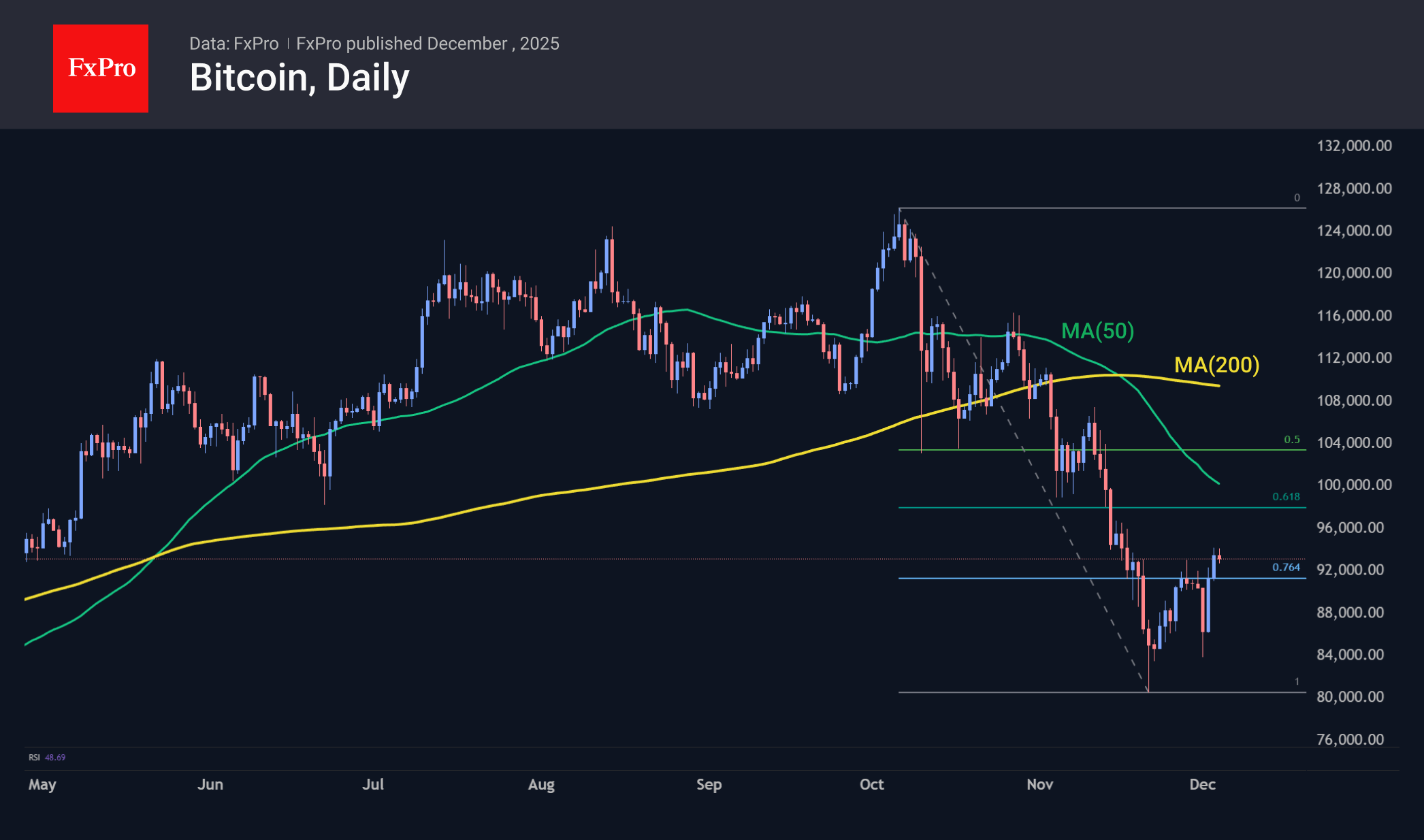

The crypto market capitalisation fell by 1% to $3.14 trillion over the past 24 hours, retreating from local highs but maintaining a relatively optimistic mood. Among the popular coins for the day, Zcash is once again in the lead, adding 10% and exceeding $400, while XRP loses 3.6% to $2.09. However, we still classify this as a rebound from oversold conditions, with doubts about the ability to renew October highs in the next couple of years. We also saw attempts to push the market up at the end of 2017 and in 2021. The capitalisation of the crypto market reached new highs during these pre-New Year rallies, but this is a dangerous game in which one needs to choose instruments more carefully than usual.

Bitcoin’s recovery slowed down, facing resistance from sellers in the $ 94,000 range. However, we view this as a pause rather than an exhaustion of the corrective rebound, which may well develop into the $98-100K range in the next few days. Nevertheless, we adhere to the 4-year cycle pattern, as the opposite has not yet been proven. In addition, we have seen a significant pullback from the highs of the previous two months, which is consistent with what happened in 2013, 2017 and 2021.

News Background

The Bull Score index developed by CryptoQuant fell to zero for the first time since January 2022, signalling a bearish market phase. CryptoQuant acknowledges that next year, Bitcoin is expected to fall to the $55K-$70K range.

Most of Bitcoin’s on-chain indicators are bearish, notes CryptoQuant CEO Ki Young Ju. According to him, without an influx of liquidity, the crypto market will enter a bearish phase of the crypto cycle.

K33 draws attention to several emerging medium-term factors that could form the basis for market growth. By February 2026, US regulators are expected to issue new rules for 401(k) retirement savings, which could potentially open up a $9 trillion market for Bitcoin.

Ethereum developers have successfully activated the Fusaka hard fork on the ETH mainnet. The update is designed to implement fundamental improvements to increase the scalability, efficiency and security of the Ethereum network.

BlackRock has announced the transformation of the financial system, influenced by cryptocurrencies and the growth of US public debt. Stablecoins are increasingly being used for cross-border payments and have become a bridge between the digital and traditional economies.

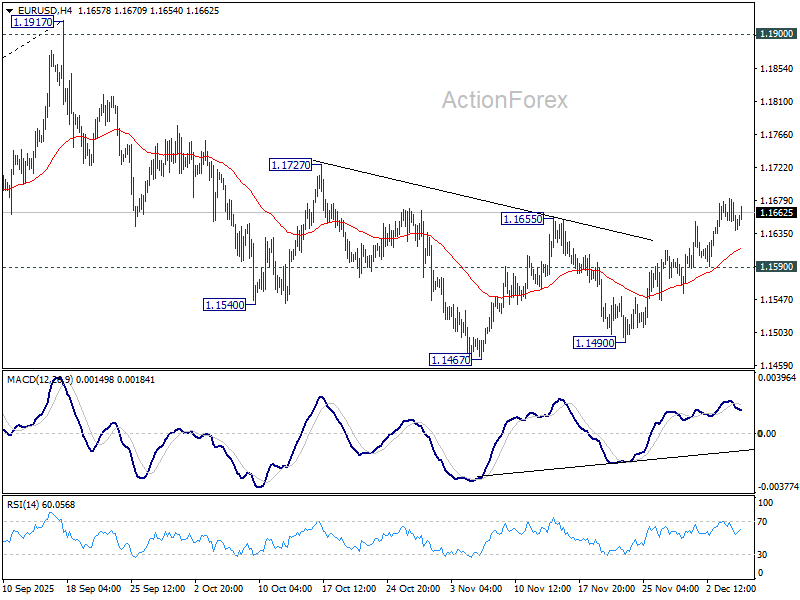

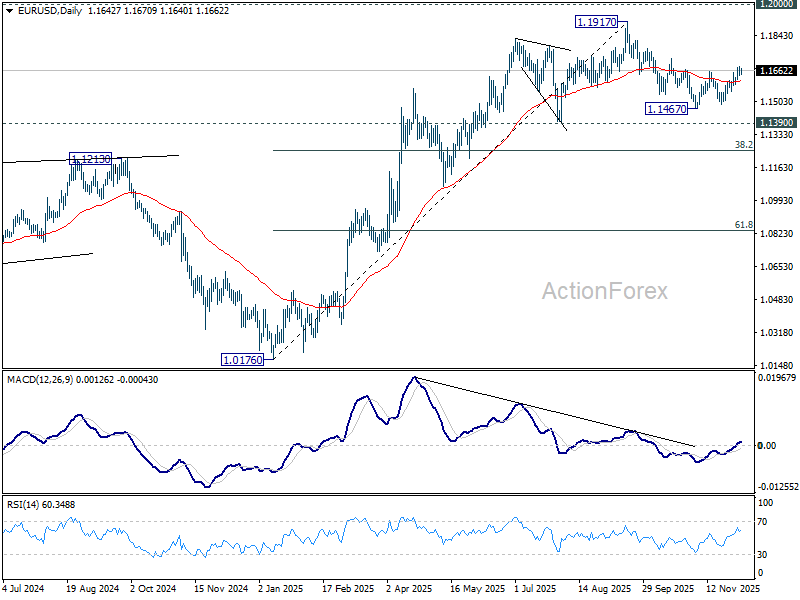

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1629; (P) 1.1656; (R1) 1.1670; More….

Intraday bias in EUR/USD stays mildly on the upside for the moment. Fall from 1.1917 should have completed at 1.1467. Further rise should be seen to 1.1727 resistance first. Firm break there will bring retest of 1.1917 high. Nevertheless, below 1.1590 minor support will mix up the outlook and turn bias neutral again.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1345) holds, the up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

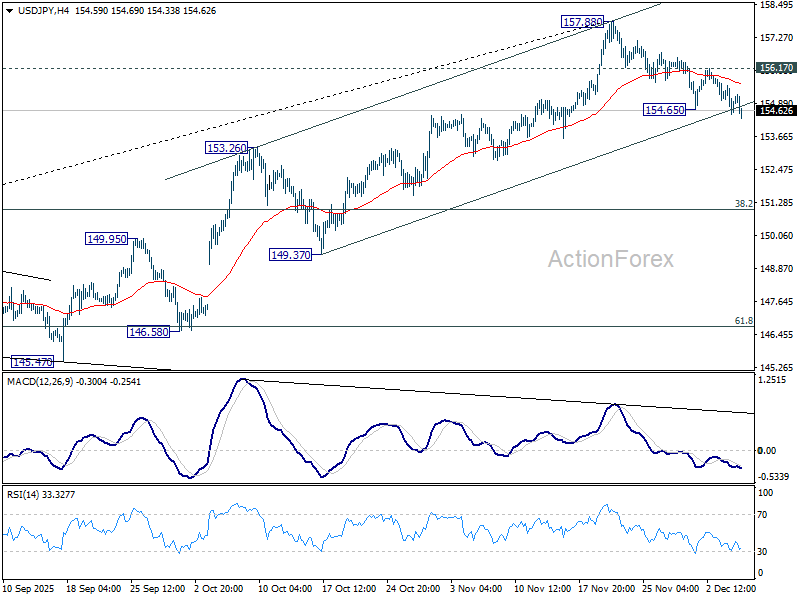

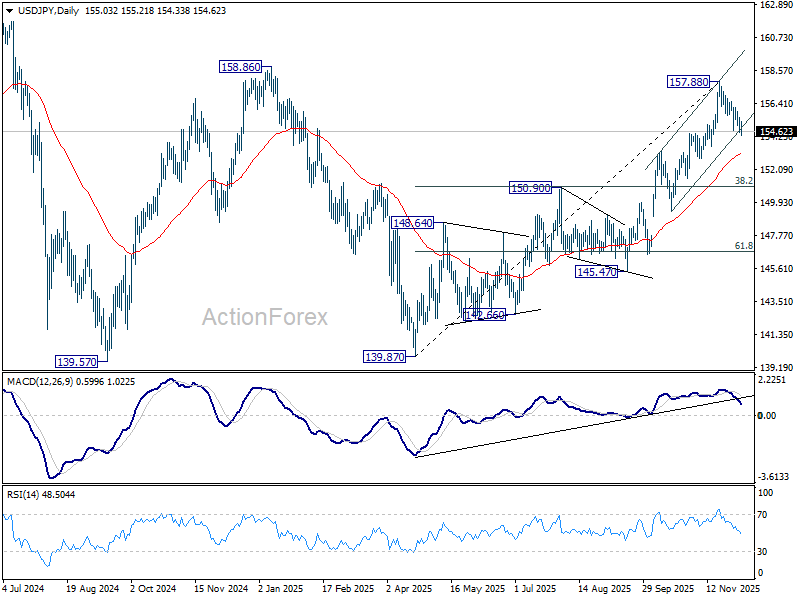

USD/JPY Daily Outlook

Daily Pivots: (S1) 154.57; (P) 155.05; (R1) 155.60; More...

USD/JPY's fall from 157.88 is resuming by breaking through 154.65 temporary low and intraday bias is back on the downside. Sustained trading below channel support should bring deeper correction to 55 D EMA (now at 153.11). Firm break there will bring deeper fall to 150.90 cluster (38.2% retracement of 139.87 to 157.88 at 151.00). For now, risk will stay on the downside as long as 156.17 resistance holds, in case of recovery.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.

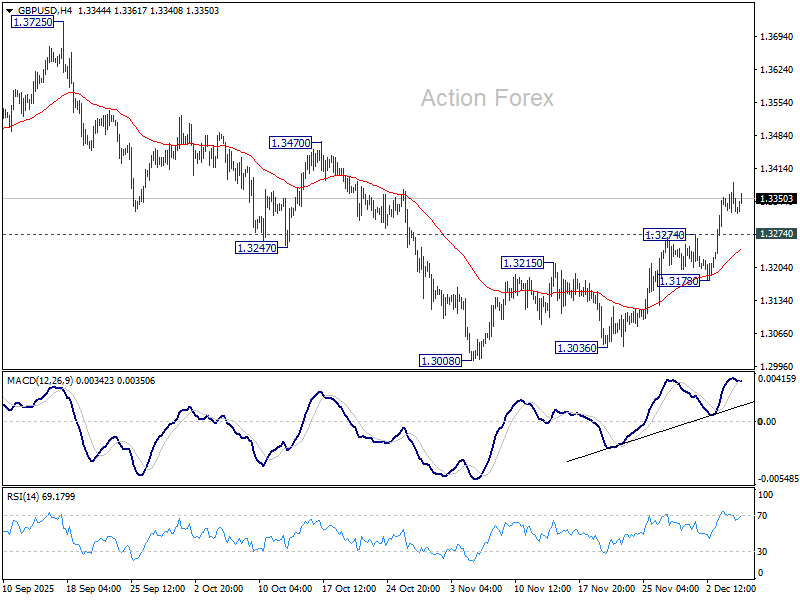

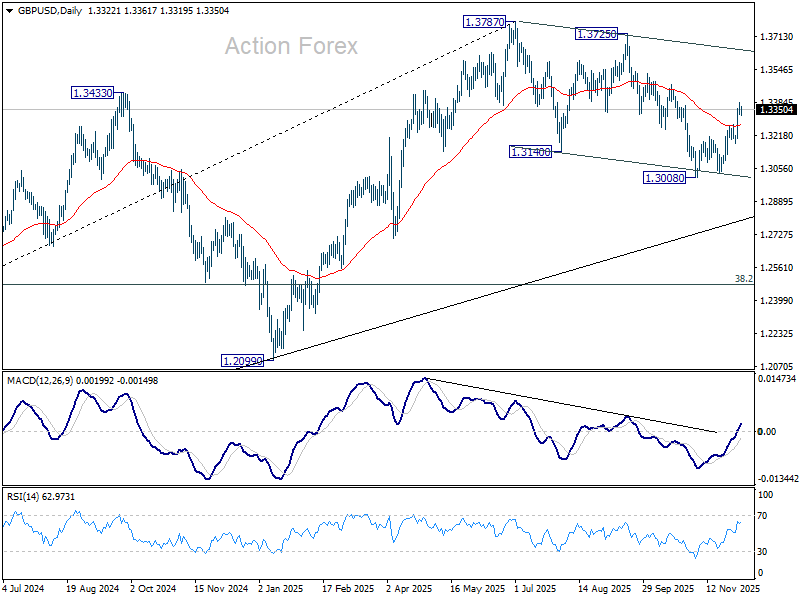

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3303; (P) 1.3344; (R1) 1.3369; More...

Intraday bias in GBP/USD remains on the upside and rise from 1.3008 should extend to 1.3470 resistance first. Decisive break there will pave the way to retest 1.3725/3787 resistance zone. On the downside, below 1.3274 resistance turned support will turn intraday bias neutral first. But risk will stay on the upside as long as 1.3718 support holds, in case of retreat.

In the bigger picture, the break of 55 W EMA (now at 1.3184) is taken as the first sign that corrective rise from 1.0351 (2022 low) has completed. Decisive break of trend line support (now at 1.2760) will solidify this case and target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 next. Meanwhile, in case of another rise, strong resistance should emerge below 1.4248 (2021 high) to cap upside to preserve the long term down trend.

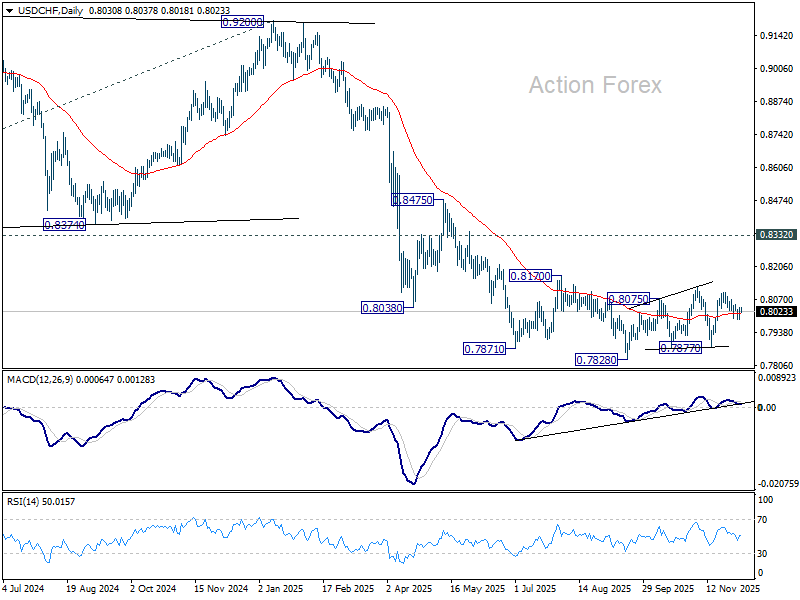

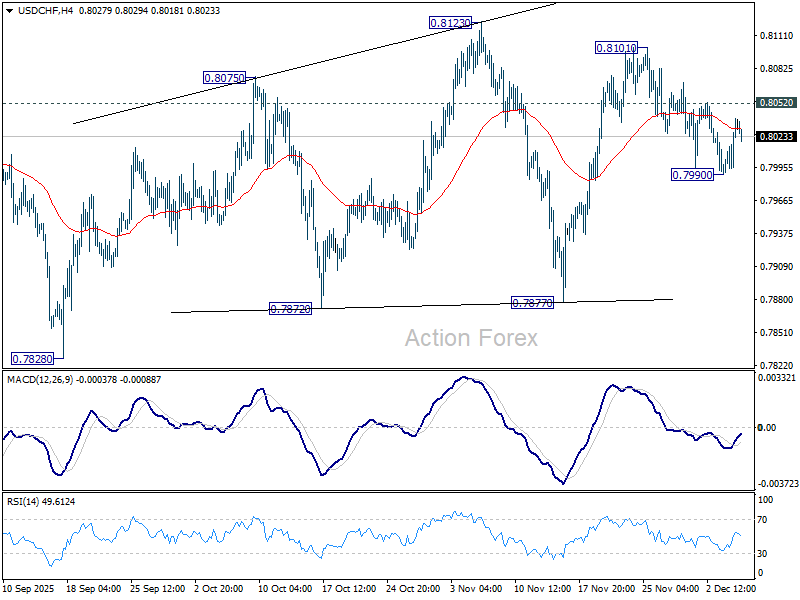

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8006; (P) 0.8023; (R1) 0.8055; More…

Intraday bias in USD/CHF remains neutral for the moment. Price actions from 0.7828 low is seen are a corrective pattern. On the upside, above 0.8052 resistance will indicate that pattern is still extending, and turn bias back to the upside for 0.8123 and above. On the downside, below 0.7990 will bring deeper fall back towards 0.7877 support.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).