Sample Category Title

GBP/USD Weekly Outlook

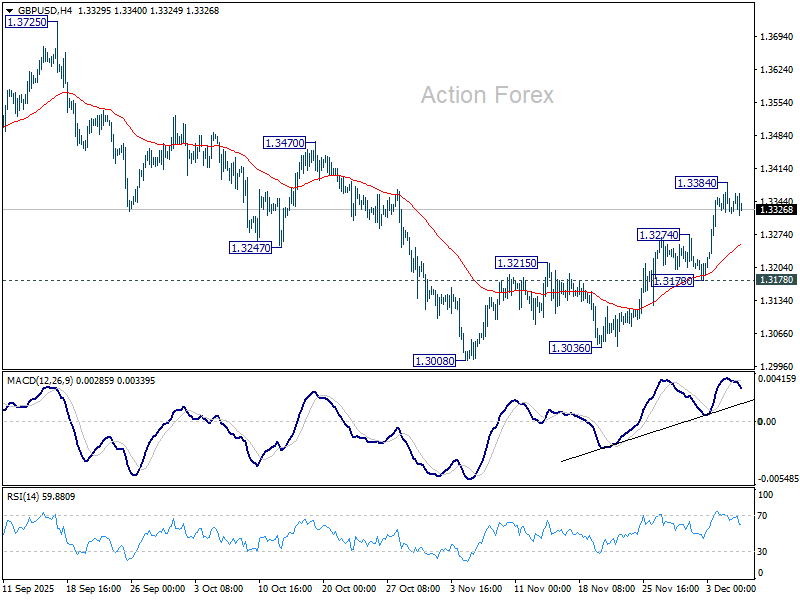

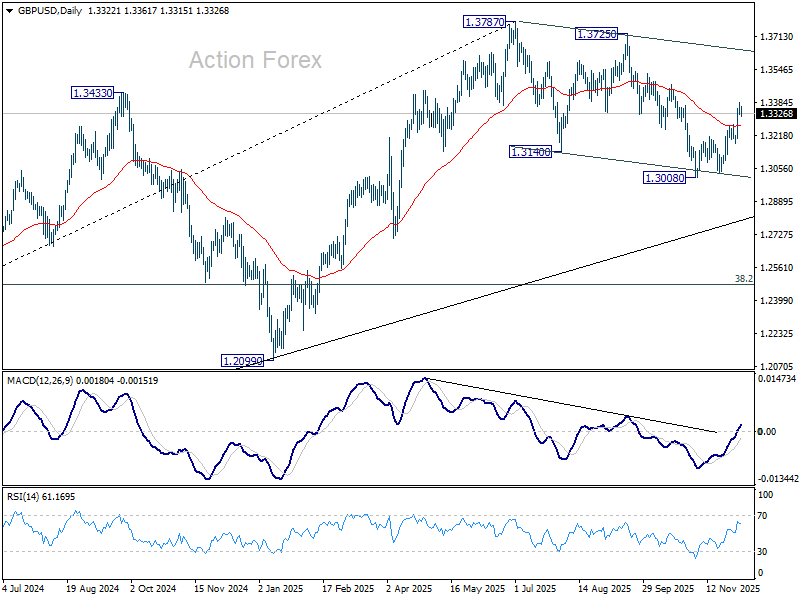

GBP/USD's rebound from 1.3008 resumed last week but retreated after hitting 1.3384. Initial bias remains neutral this week for some consolidations. But further rally is expected as 1.3178 support holds. Current development suggests that fall from 1.3787 has completed as a three-wave correction to 1..3008. Above 13384 will target 1.3470 resistance. Decisive break there will bring retest of 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.

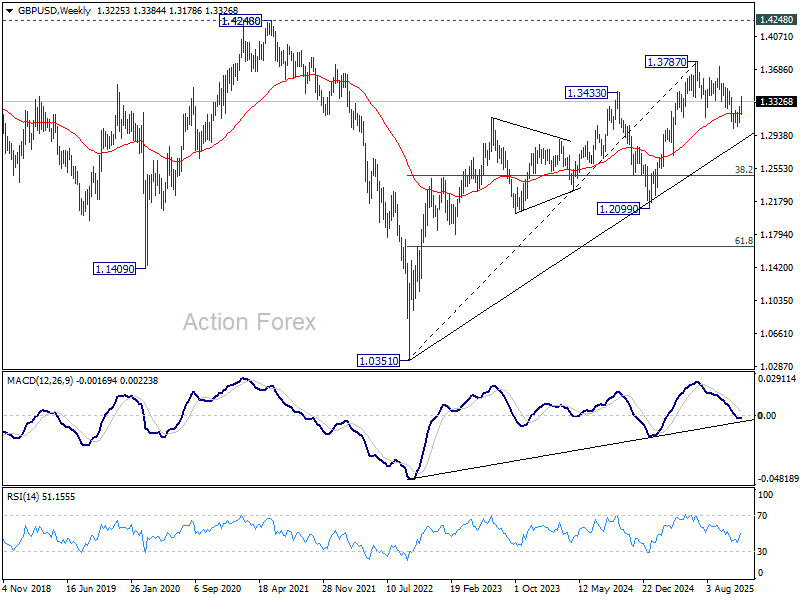

In the long term picture, as long as 1.4248/4480 resistance zone holds (38.2% retracement of 2.1161 to 1.0351 at 1.4480), the long term outlook will remain bearish. That is, price actions from 1.3051 are seen as a corrective pattern to down trend from 2.1161 (2007 high) only. Nevertheless, decisive break of 1.4248/4480 will be a strong sign of long term bullish reversal.

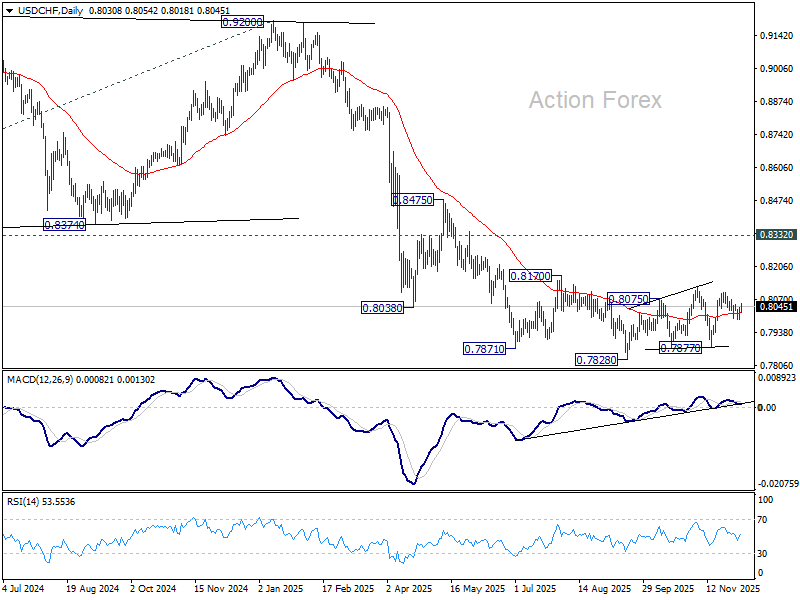

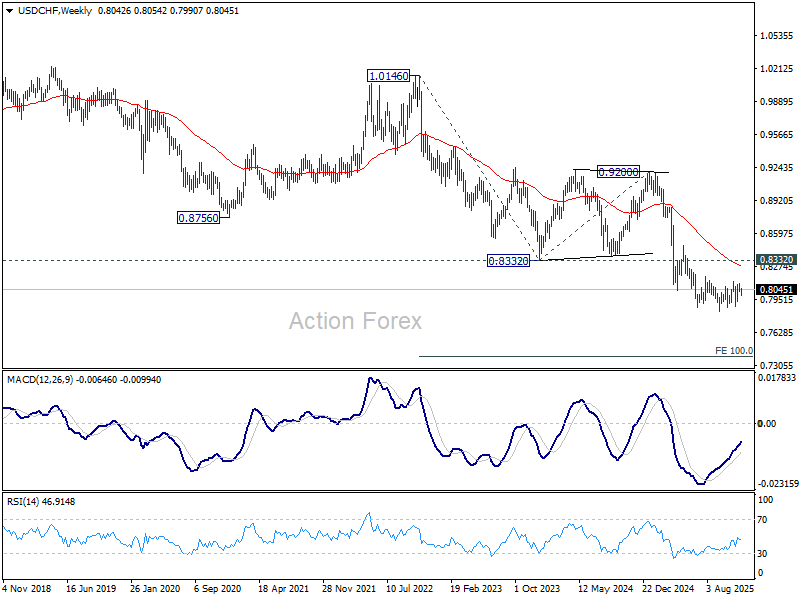

USD/CHF Weekly Outlook

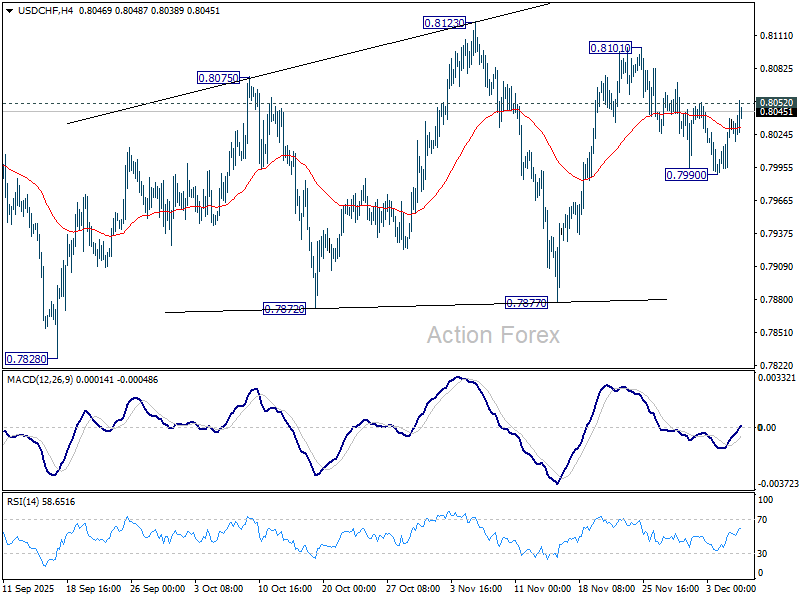

USD/CHF retreated to 0.7990 last week but recovered since then. Initial bias stays neutral this week first. Overall outlook is unchanged that price actions from 0.7828 are developing into a corrective pattern. On the upside, break of 0.8052 will bring stronger rise to 0.8101, and then 0.8123 resistance. On the downside, though, break of 0.7990 will extend the fall from 0.8101 towards 0.7877 support instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

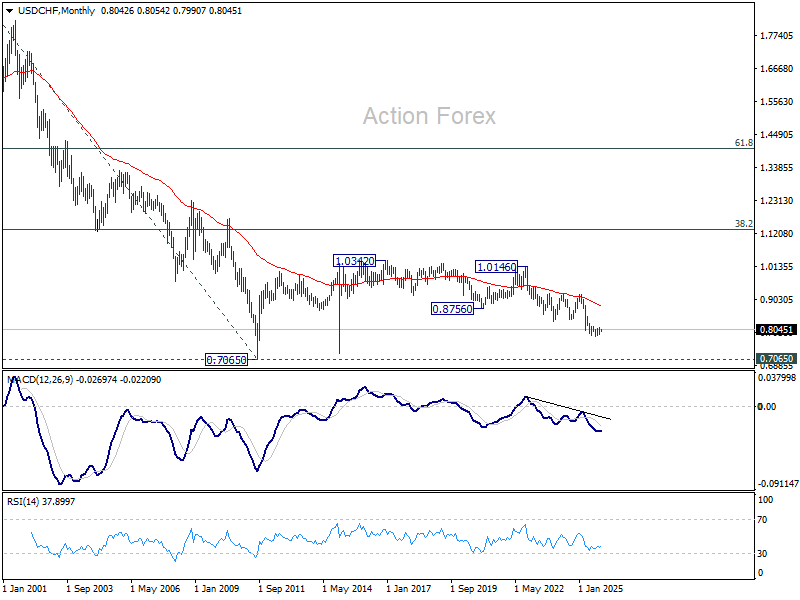

In the long term picture, price action from 0.7065 (2011 low) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the downtrend. But in either case, outlook will stay bearish as long as 0.8756 support turned resistance holds (2021 low). Retest of 0.7065 should be seen next.

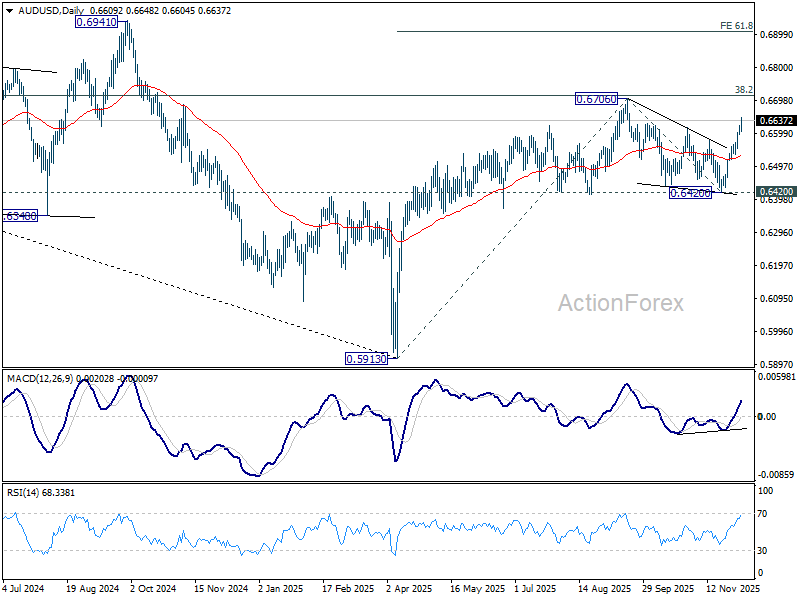

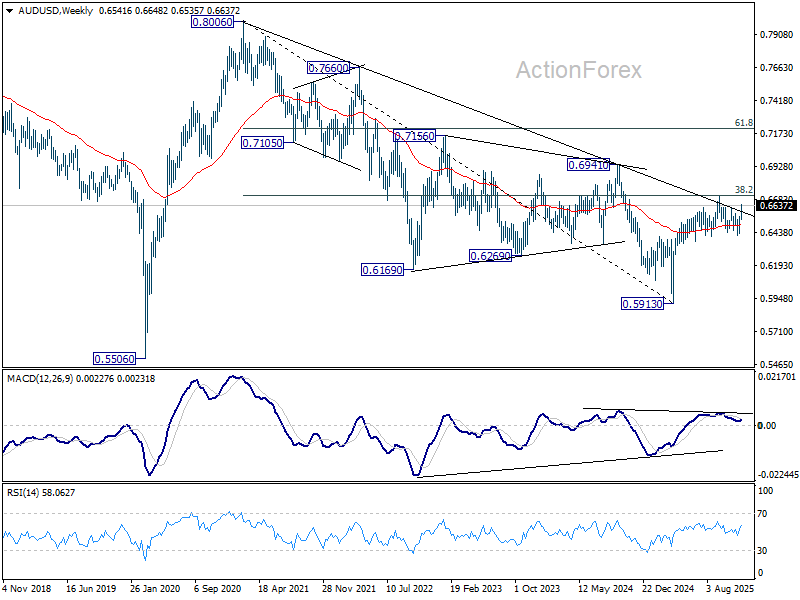

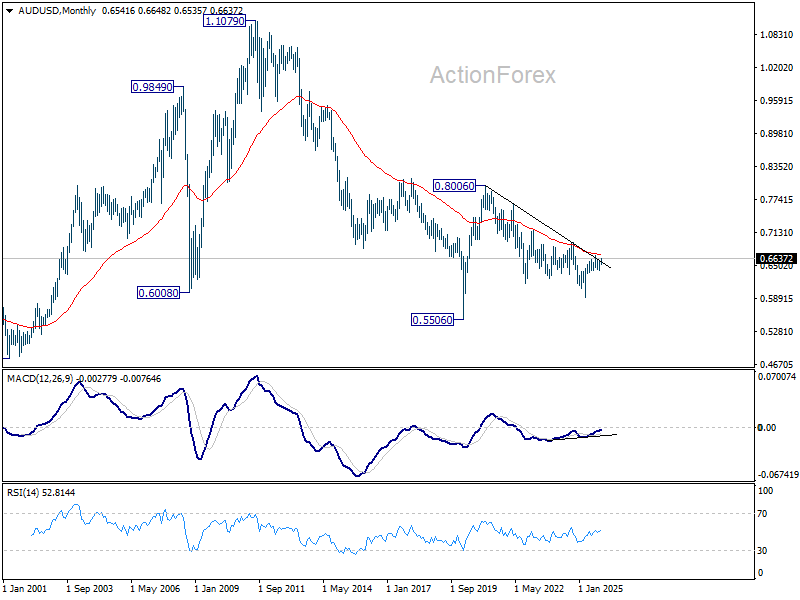

AUD/USD Weekly Report

AUD/USD's strong rise last week suggests that corrective pattern from 0.6706 has already completed with three waves to 0.6420. Rise from 0.5913 might be ready to resume. Initial bias stays on the upside this week for retesting 0.6706 first. Firm break there will pave the way to 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910. On the downside, below 0.6604 minor support will turn intraday bias neutral and bring consolidations, before staging another rise.

In the bigger picture, the break of multi-year falling trend line resistance suggests that rise from 0.5913 is possibly reversing whole down trend from 08006 (2021 high). Decisive break of 38.2% retracement of 0.8006 to 0.5913 at 0.6713 will solidify this case, and bring further rally to 61.8% retracement at 0.7206. On the downside, however, firm break of 0.6420 support will suggest rejection by 0.6713 and retain medium term bearishness.

In the long term picture, fall from 0.8006 is seen as the second leg of the corrective pattern from 0.5506 long term bottom (2020 low). Hence, in case of deeper decline, strong support should emerge above 0.5506 to contain downside to bring reversal. On the upside, firm break of 0.6941 will argue that the third leg has already started back to 0.8006 and above.

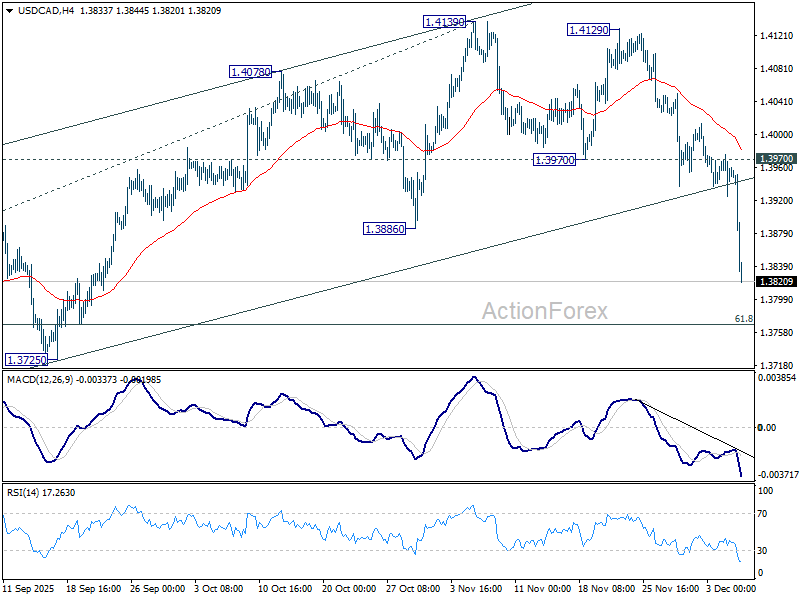

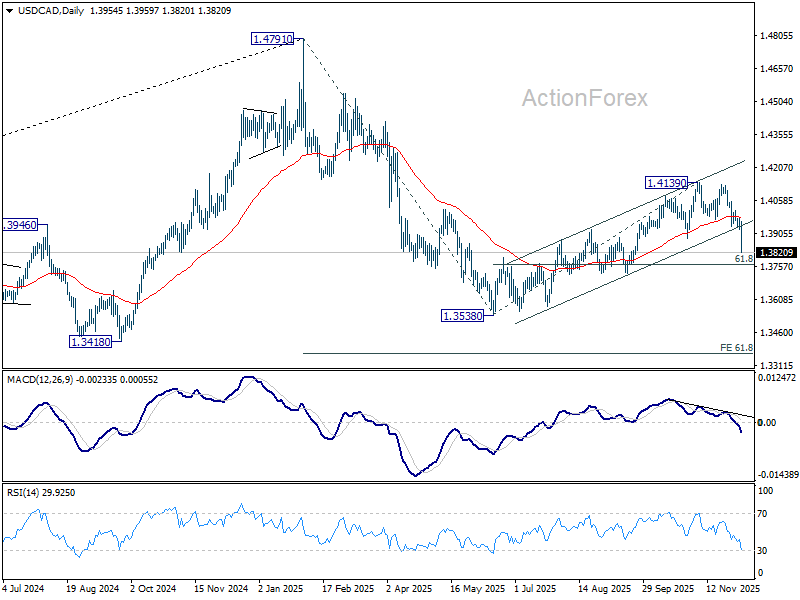

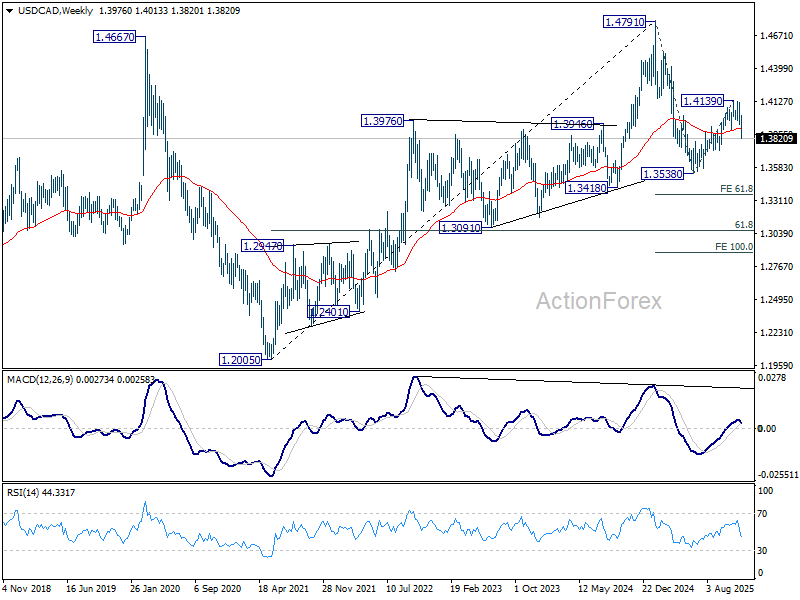

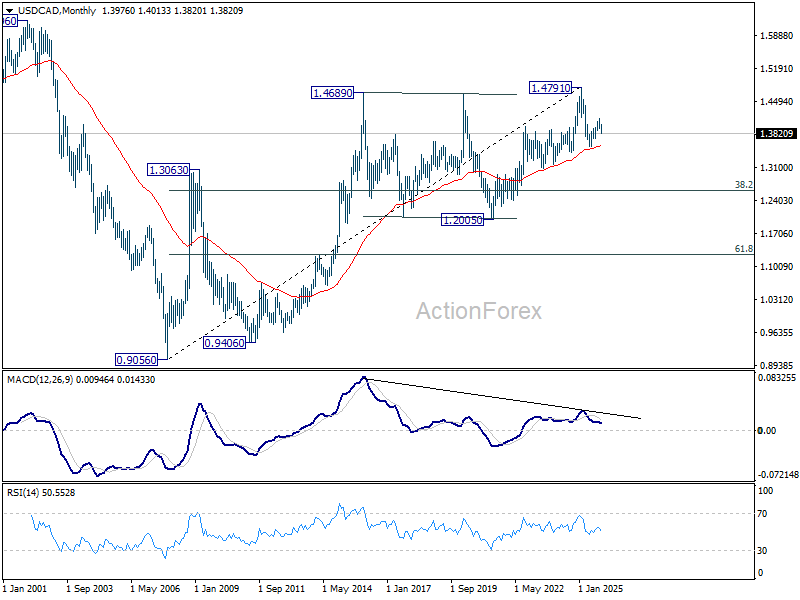

USD/CAD Weekly Outlook

USD/CAD's steep decline last week suggests that rise from 1.3538 has already completed at 1.4139. Initial bias remains on the downside this week for 61.8% retracement of 1.3538 to 1.4139 at 1.3768. Firm break there will argue that whole decline form 1.4791 might be ready to resume through 1.3538 low. For now, risk will stay on the downside as long as 1.3970 support turned resistance holds, in case of recovery.

In the bigger picture, current development suggests that price actions from 1.4791 is developing into a deeper, larger scale correction. In the less bearish case, it's just correcting the rise from 1.2005 (2021 low). But even so, break of 1.3538 will pave the way to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. This will remain the favored case as long as 1.4139 resistance holds, in case of rebound.

In the long term picture, rising 55 M EMA (now at 1.3567) remains intact. Thus, up trend from 0.9056 (2007 low) should still be in progress. However, considering bearish divergence condition M MACD, sustained trading below 55 M EMA will argue that the up trend has completed with five waves up to 1.4791, and turn medium term outlook bearish for correction. to 38.2% retracement of 0.9056 to 1.4791 at 1.2600.

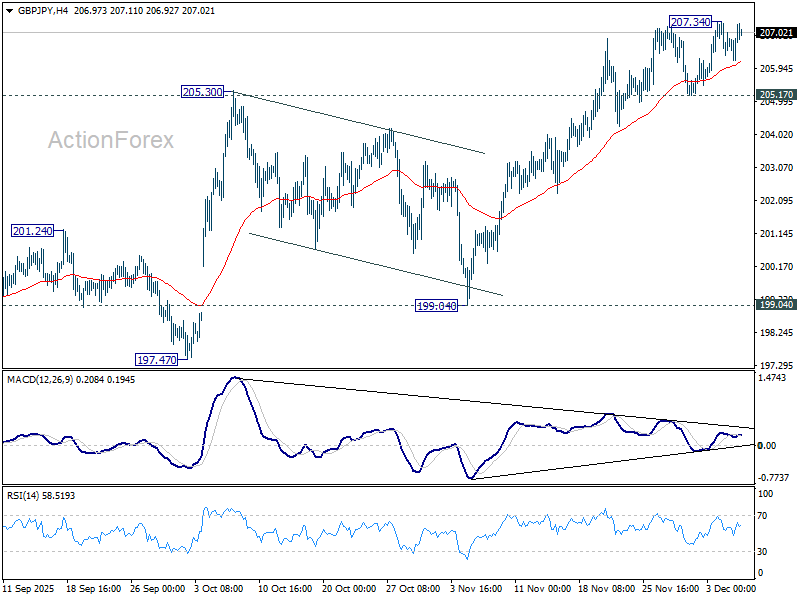

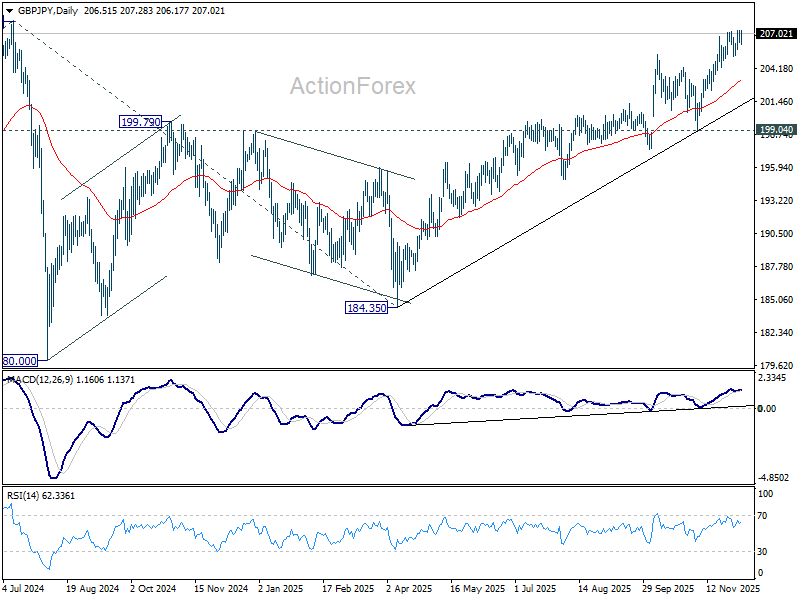

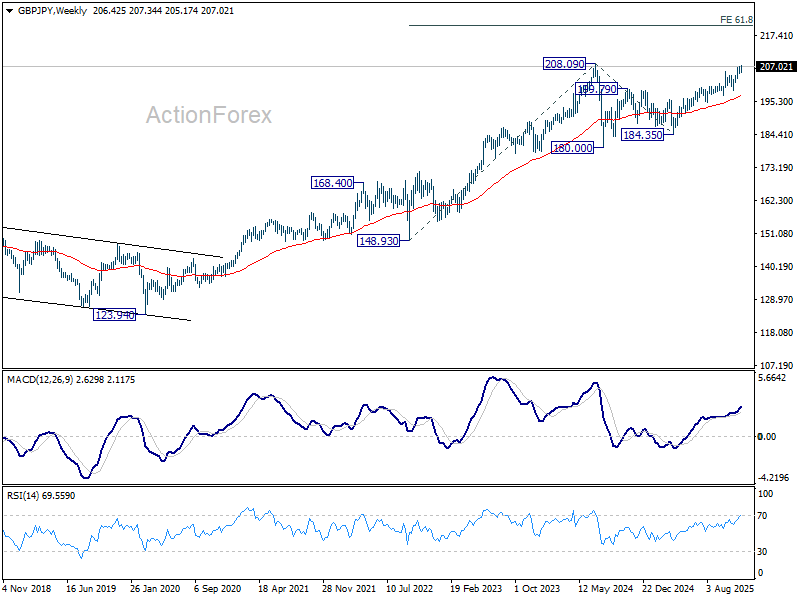

GBP/JPY Weekly Outlook

GBP/JPY edged higher to 207.34 but quickly retreated. Initial bias stays neutral this week first, but further rise is expected as long as 205.17 support holds. Break of 207.34 will resume the rally from 184.35 and target 208.09 high. However, break of 205.17 support will turn bias to the downside for deeper pullback, possibly to 55 D EMA (now at 203.25).

In the bigger picture, price actions from 208.09 (2024 high) are seen as a corrective pattern which might have completed at 184.35. Firm break of 208.09 high will resume the up trend from 123.94 (2020 low). Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. However, decisive break of 199.04 support will dampen this view and extend the corrective pattern with another fall.

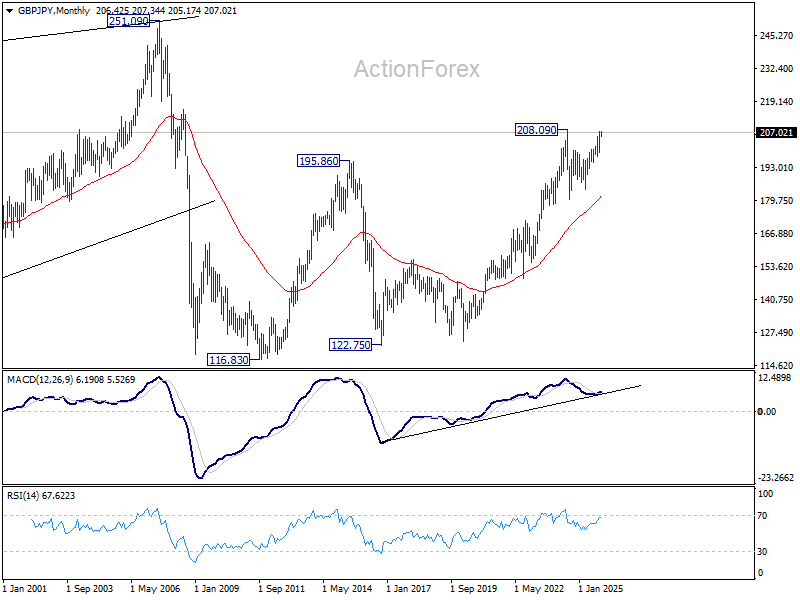

In the long term picture, there is no sign that the long term up trend from 122.75 (2016 low) has concluded. But firm break of 208.09 is needed to confirm resumption. Otherwise, more medium term range trading could still be seen.

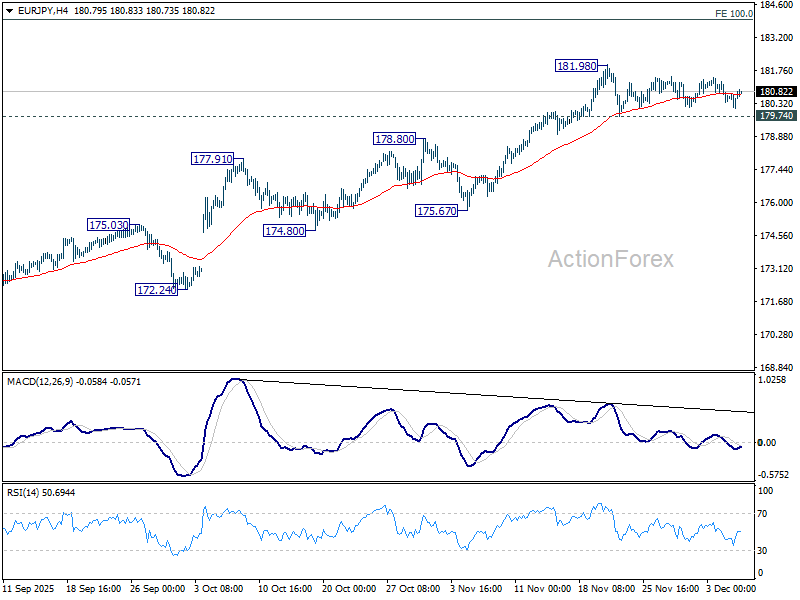

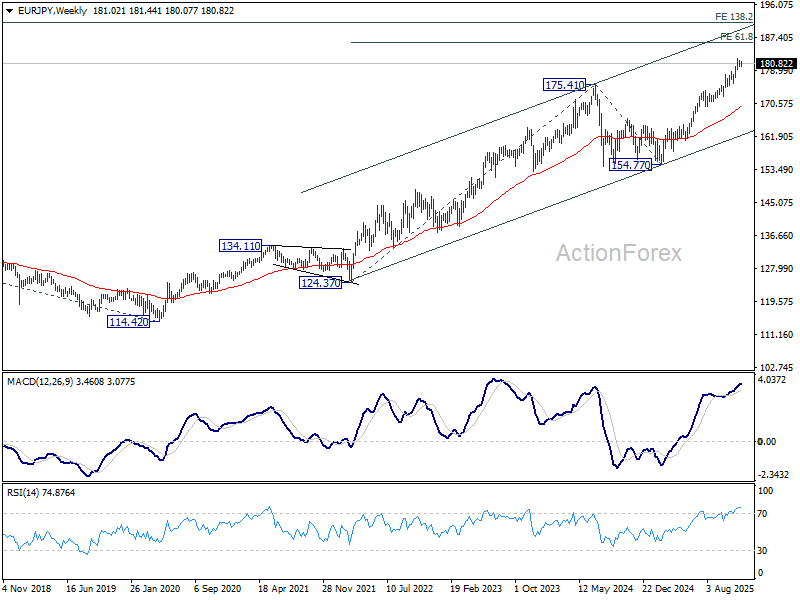

EUR/JPY Weekly Outlook

EUR/JPY stayed in established range below 181.98 last week and outlook is unchanged. Initial bias remains neutral this week first, and further rally is expected with 179.74 support intact. On the upside, break of 181.98 will resume larger up trend to 100% projection of 161.06 to 173.87 from 171.09 at 183.90 next. However, firm break of 178.80 will argue that deeper correction is already underway towards 55 D EMA (now at 177.84).

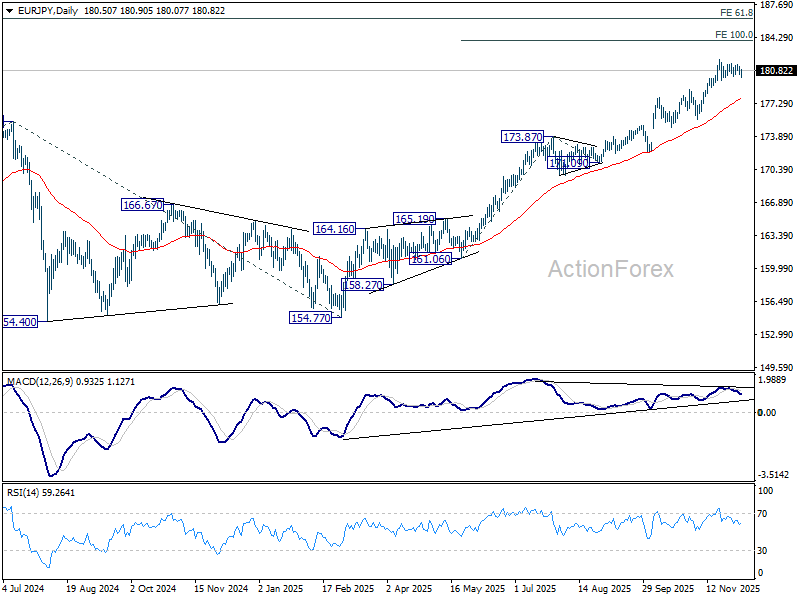

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. However, considering bearish divergence condition in D MACD, upside should be capped by 186.31 on first attempt. Outlook will continue to stay bullish as long as 55 W EMA (now at 169.87) holds, even in case of deep pullback.

In the long term picture, up trend from 94.11 (2021 low) is in progress. Next target is 138.2% projection of 94.11 to 149.76 (2014 high) from 114.42 (2020 low) at 191.32. This will remain the favored case as long as 154.77 support holds.

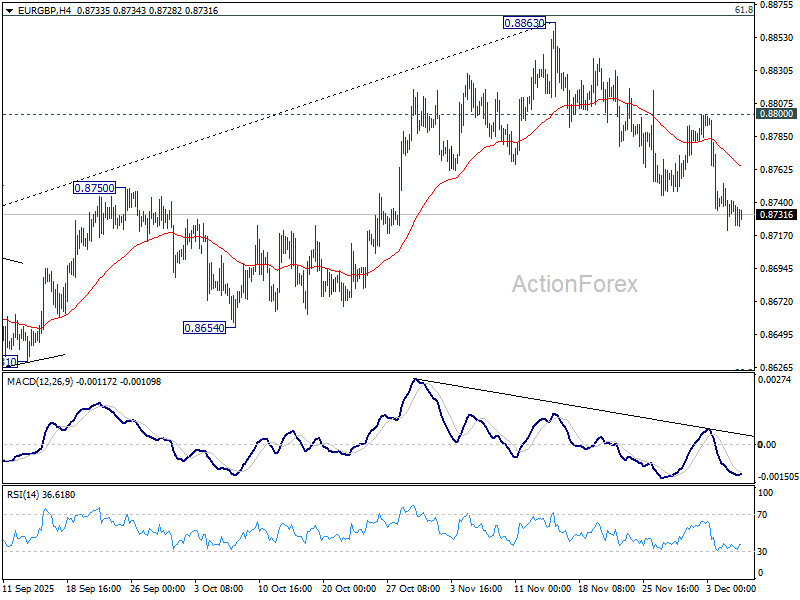

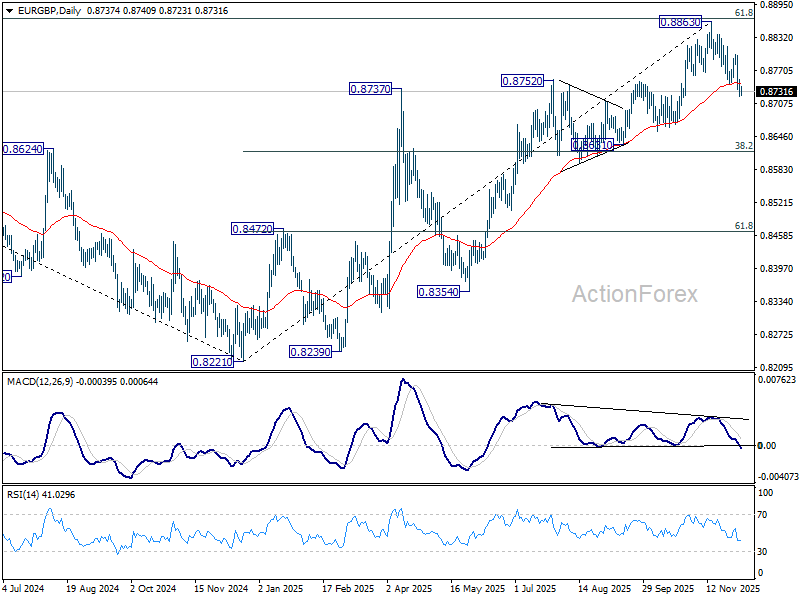

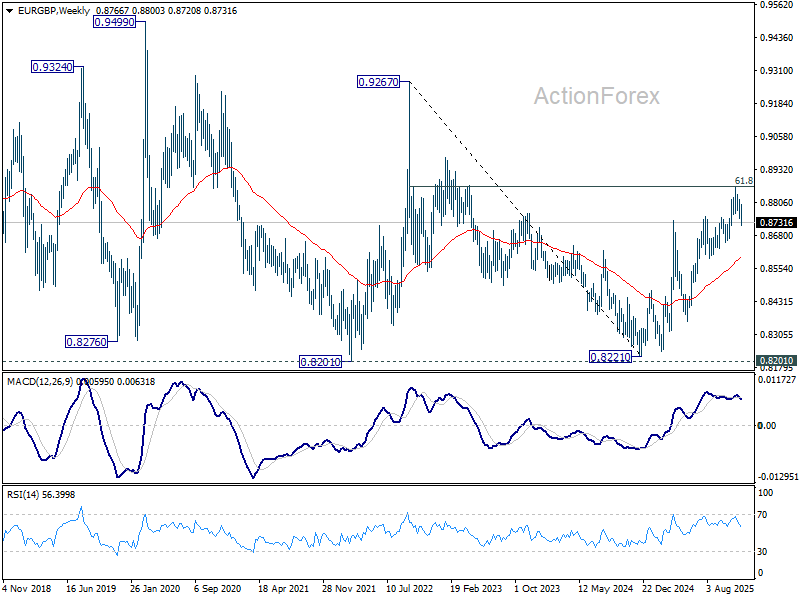

EUR/GBP Weekly Outlook

EUR/GBP's fall from 0.8863 extended last week and the break of 55 D EMA (now at 0.8745) should confirm rejection by 0.8867 key fibonacci level. Initial bias stays on the downside this week for 0.8631 cluster (38.2% retracement of 0.8221 to 0.8663 at 0.8618). For now, risk will stay on the downside as long as 0.8800 resistance holds, in case of recovery.

In the bigger picture, rise from 0.8221 medium term bottom is still seen as a corrective move. Upside should be limited by 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Sustained trading below 55 W EMA (now at 0.8600) should confirm that this corrective bounce has completed. However, decisive break of 0.8867 will suggest that EUR/GBP is already reversing whole decline from 0.9267 (2022 high). That should pave the way back to 0.9267.

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

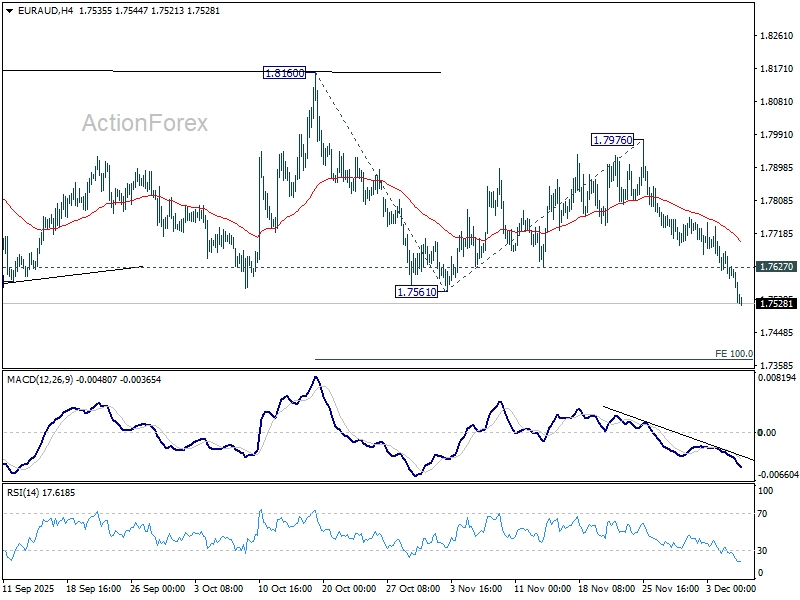

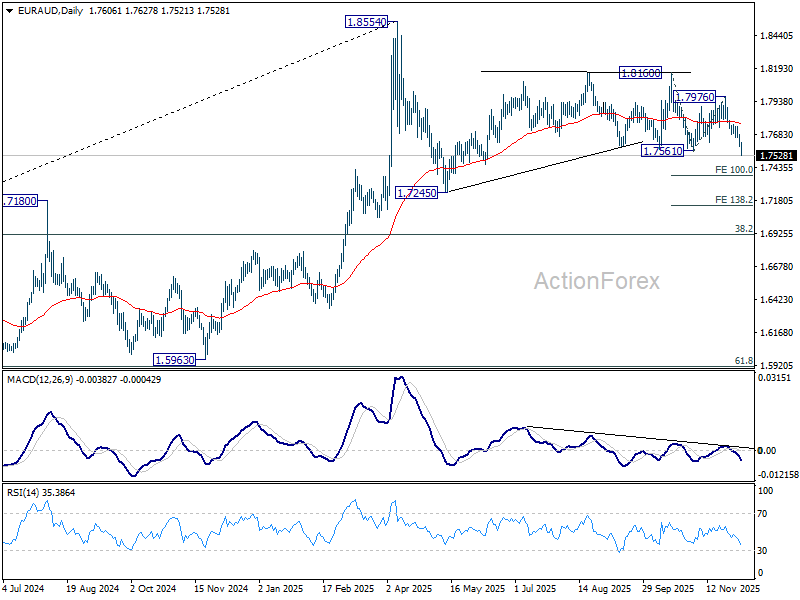

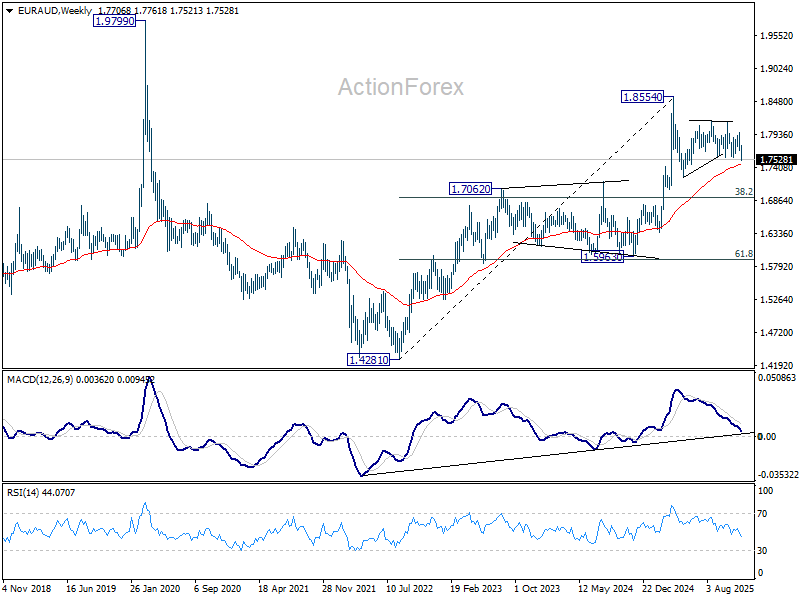

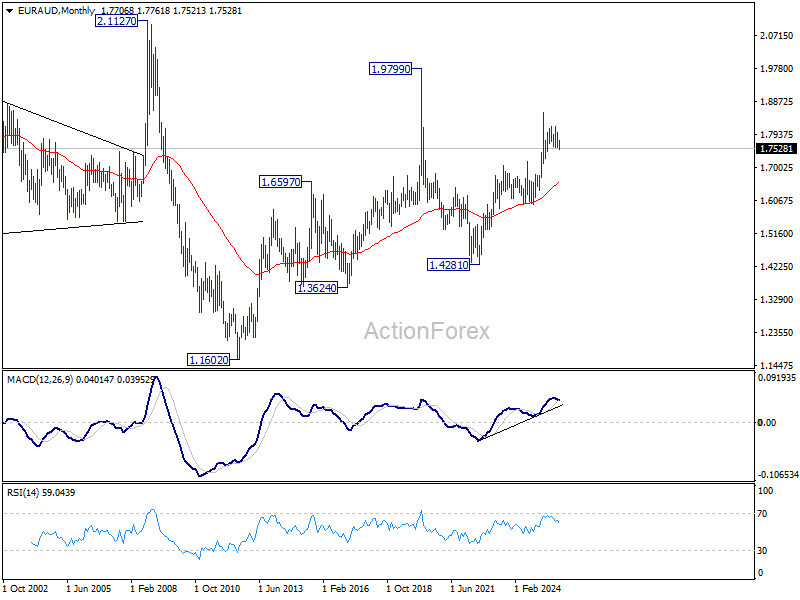

EUR/AUD Weekly Outlook

EUR/AUD's steep decline and solid break of 1.7561 support confirms resumption of fall from 1.8160. More importantly the whole pattern from 1.8554 should now be in its third leg. Initial bias stays on the downside this week for 100% projection of 1.8160 to 1.7561 from 1.7976 at 1.7377. Firm break there will pave the way to 138.2% projection at 17148. On the upside, above 1.7627 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, as long as 55 W EMA (now at 1.7449) holds, price actions from 1.8554 could still be a correction to rise from 1.5963 only. However, sustained break of the EMA will argue that it's already correcting the whole up trend from 1.4281 (2022 low). In this case, deeper decline would be seen to 38.2% retracement of 1.4281 to 1.8554 at 1.6922.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6579) holds, this second leg could still extend higher.

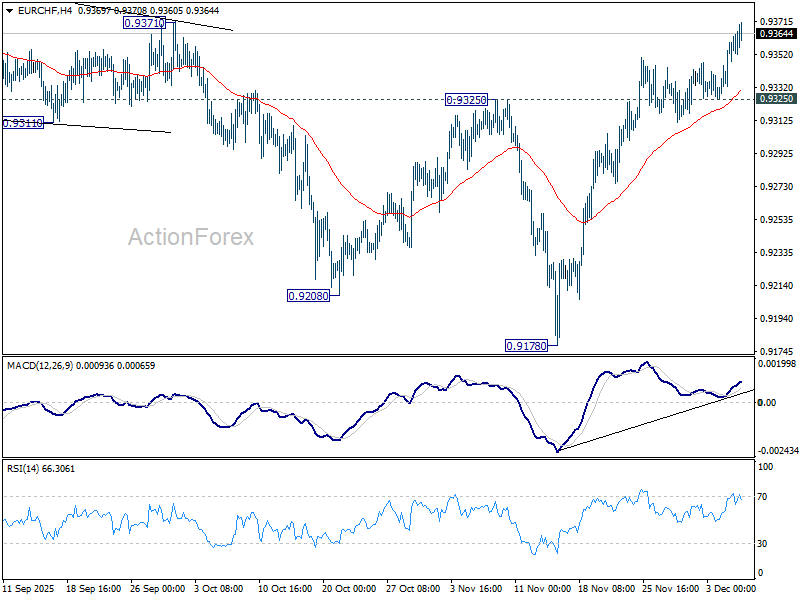

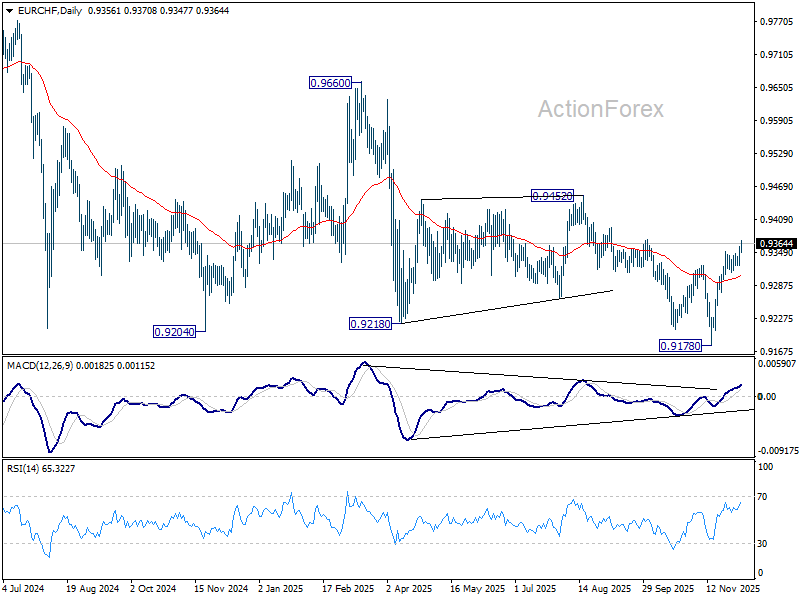

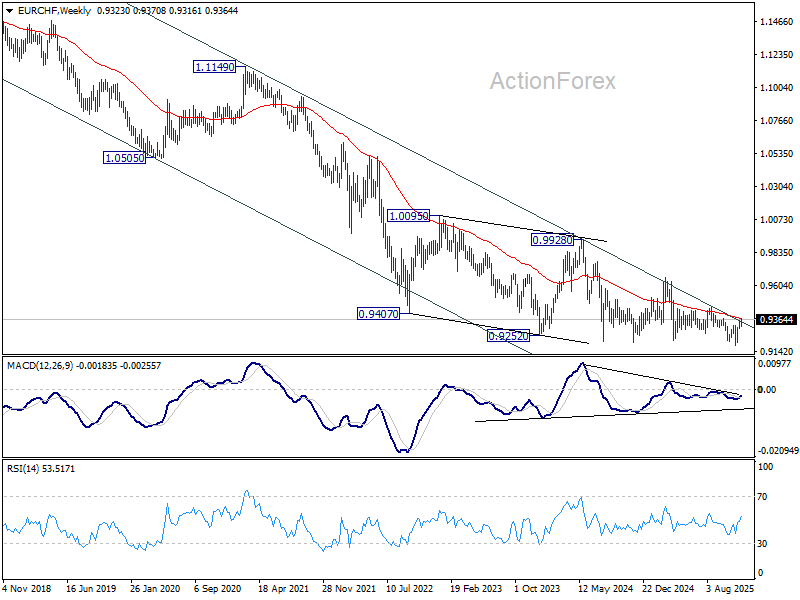

EUR/CHF Weekly Outlook

EUR/CHF's rally from 0.9278 short term bottom resumed last week and the development solidify that case that fall from 0.9660 has completed. Initial bias stays on the upside this week for 0.9452 key structural resistance. Decisive break there will carry larger bullish implications. For now, risk will stay on the upside as long as 0.9325 support holds, in case of retreat.

In the bigger picture, EUR/CHF has breached long term falling channel resistance as the rebound from 0.9278 extends. Considering bullish convergence condition in W MACD, sustained trading above 55 W EMA (now at 0.9316) will indicate medium term bottoming, and suggests that it's already in larger scale rebound. Further break of 0.9452 resistance will bring stronger medium term rally towards 0.9228 resistance next. Nevertheless, rejection by 55 W EMA will retain bearishness for another fall through 0.9278 at a later stage.

In the long term picture, overall long term down trend from 1.2004 (2018 high) is still in progress in EUR/CHF. Outlook will continue to stay bearish as long as falling 55 M EMA (now at 0.9785) holds.

Summary 12/8 – 12/12

Monday, Dec 8, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | 2.20% | 1.90% |

| 23:50 | JPY | GDP Deflator Y/Y Q3 | 2.80% | 2.80% |

| 23:50 | JPY | GDP Q/Q Q3 F | -0.50% | -0.40% |

| 23:50 | JPY | GDP Annualized Q3 F | -2.00% | -1.80% |

| 23:50 | JPY | Current Account (JPY) Oct | 3.00T | 4.35T |

| 03:00 | CNY | Trade Balance (USD) Nov | 105.0B | 90.1B |

| 05:00 | JPY | Eco Watchers Survey: Current Nov | 49.5 | 49.1 |

| 07:00 | EUR | Germany Industrial Production M/M Oct | 0.50% | 1.30% |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Dec | -6.3 | -7.4 |

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | 1.40% | 1.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | |

| Forecast: 2.20% | Previous: 1.90% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q3 | |

| Forecast: 2.80% | Previous: 2.80% | ||

| 23:50 | JPY | GDP Q/Q Q3 F | |

| Forecast: -0.50% | Previous: -0.40% | ||

| 23:50 | JPY | GDP Annualized Q3 F | |

| Forecast: -2.00% | Previous: -1.80% | ||

| 23:50 | JPY | Current Account (JPY) Oct | |

| Forecast: 3.00T | Previous: 4.35T | ||

| 03:00 | CNY | Trade Balance (USD) Nov | |

| Forecast: 105.0B | Previous: 90.1B | ||

| 05:00 | JPY | Eco Watchers Survey: Current Nov | |

| Forecast: 49.5 | Previous: 49.1 | ||

| 07:00 | EUR | Germany Industrial Production M/M Oct | |

| Forecast: 0.50% | Previous: 1.30% | ||

| 09:30 | EUR | Eurozone Sentix Investor Confidence Dec | |

| Forecast: -6.3 | Previous: -7.4 | ||

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | |

| Forecast: 1.40% | Previous: 1.60% | ||

Tuesday, Dec 9, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | BRC Retail Sales Monitor Y/Y Nov | 2.40% | 1.50% |

| 00:30 | AUD | NAB Business Confidence Nov | 6 | |

| 00:30 | AUD | NAB Business Conditions Nov | 9 | |

| 03:30 | AUD | RBA Interest Rate Decision | 3.60% | 3.60% |

| 04:30 | AUD | RBA Press Conference | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | 16.80% | |

| 07:00 | EUR | Germany Trade Balance (EUR) Oct | 15.8B | 15.3B |

| 11:00 | USD | NFIB Business Optimism Index Nov | 98.4 | 98.2 |

| 23:50 | JPY | PPI Y/Y Nov | 2.70% | 2.70% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | BRC Retail Sales Monitor Y/Y Nov | |

| Forecast: 2.40% | Previous: 1.50% | ||

| 00:30 | AUD | NAB Business Confidence Nov | |

| Forecast: | Previous: 6 | ||

| 00:30 | AUD | NAB Business Conditions Nov | |

| Forecast: | Previous: 9 | ||

| 03:30 | AUD | RBA Interest Rate Decision | |

| Forecast: 3.60% | Previous: 3.60% | ||

| 04:30 | AUD | RBA Press Conference | |

| Forecast: | Previous: | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Nov P | |

| Forecast: | Previous: 16.80% | ||

| 07:00 | EUR | Germany Trade Balance (EUR) Oct | |

| Forecast: 15.8B | Previous: 15.3B | ||

| 11:00 | USD | NFIB Business Optimism Index Nov | |

| Forecast: 98.4 | Previous: 98.2 | ||

| 23:50 | JPY | PPI Y/Y Nov | |

| Forecast: 2.70% | Previous: 2.70% | ||

Wednesday, Dec 10, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Nov | 0.70% | 0.20% |

| 01:30 | CNY | PPI Y/Y Nov | -2.10% | -2.10% |

| 13:30 | USD | Employment Cost Index Q3 | 0.90% | 0.90% |

| 14:45 | CAD | BoC Interest Rate Decision | 2.25% | 2.25% |

| 15:30 | CAD | BoC Press Conference | ||

| 15:30 | USD | Crude Oil Inventories (Dec 5) | 0.6M | |

| 19:00 | USD | Fed Interest Rate Decision | 3.75% | 4.00% |

| 19:30 | USD | FOMC Press Conference | ||

| 21:45 | NZD | Manufacturingles Q3 | -2.90% | |

| 23:50 | JPY | BSI Large Manufacturing Index Q4 | 4.2 | 3.8 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Nov | |

| Forecast: 0.70% | Previous: 0.20% | ||

| 01:30 | CNY | PPI Y/Y Nov | |

| Forecast: -2.10% | Previous: -2.10% | ||

| 13:30 | USD | Employment Cost Index Q3 | |

| Forecast: 0.90% | Previous: 0.90% | ||

| 14:45 | CAD | BoC Interest Rate Decision | |

| Forecast: 2.25% | Previous: 2.25% | ||

| 15:30 | CAD | BoC Press Conference | |

| Forecast: | Previous: | ||

| 15:30 | USD | Crude Oil Inventories (Dec 5) | |

| Forecast: | Previous: 0.6M | ||

| 19:00 | USD | Fed Interest Rate Decision | |

| Forecast: 3.75% | Previous: 4.00% | ||

| 19:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

| 21:45 | NZD | Manufacturingles Q3 | |

| Forecast: | Previous: -2.90% | ||

| 23:50 | JPY | BSI Large Manufacturing Index Q4 | |

| Forecast: 4.2 | Previous: 3.8 | ||

Thursday, Dec 11, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:01 | GBP | RICS Housing Price Balance Nov | -21% | -19% |

| 00:30 | AUD | Employment Change Nov | 20.0K | 42.2K |

| 00:30 | AUD | Unemployment Rate Nov | 4.40% | 4.30% |

| 08:30 | CHF | SNB Interest Rate Decision | 0.00% | 0.00% |

| 09:00 | CHF | SNB Press Conference | ||

| 13:30 | CAD | Trade Balance (CAD) Oct | -4.9B | -6.3B |

| 13:30 | USD | Initial Jobless Claims (Dec 5) | 205K | 191K |

| 13:30 | USD | Trade Balance (USD) Sep | -65.5B | -59.6B |

| 15:00 | USD | Wholele Inventories Sep F | 0.10% | 0.00% |

| 15:30 | USD | Natural Gas Storage (Dec 5) | -12B | |

| 21:30 | NZD | Business NZ PMI Nov | 51.4 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:01 | GBP | RICS Housing Price Balance Nov | |

| Forecast: -21% | Previous: -19% | ||

| 00:30 | AUD | Employment Change Nov | |

| Forecast: 20.0K | Previous: 42.2K | ||

| 00:30 | AUD | Unemployment Rate Nov | |

| Forecast: 4.40% | Previous: 4.30% | ||

| 08:30 | CHF | SNB Interest Rate Decision | |

| Forecast: 0.00% | Previous: 0.00% | ||

| 09:00 | CHF | SNB Press Conference | |

| Forecast: | Previous: | ||

| 13:30 | CAD | Trade Balance (CAD) Oct | |

| Forecast: -4.9B | Previous: -6.3B | ||

| 13:30 | USD | Initial Jobless Claims (Dec 5) | |

| Forecast: 205K | Previous: 191K | ||

| 13:30 | USD | Trade Balance (USD) Sep | |

| Forecast: -65.5B | Previous: -59.6B | ||

| 15:00 | USD | Wholele Inventories Sep F | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 15:30 | USD | Natural Gas Storage (Dec 5) | |

| Forecast: | Previous: -12B | ||

| 21:30 | NZD | Business NZ PMI Nov | |

| Forecast: | Previous: 51.4 | ||

Friday, Dec 12, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | JPY | Industrial Production M/M Oct F | 1.40% | 1.40% |

| 07:00 | EUR | Germany CPI M/M Nov F | -0.20% | -0.20% |

| 07:00 | EUR | Germany CPI Y/Y Nov F | 2.60% | 2.60% |

| 07:00 | GBP | GDP M/M Oct | 0.10% | -0.10% |

| 07:00 | GBP | Industrial Production M/M Oct | 1.10% | -2.00% |

| 07:00 | GBP | Industrial Production Y/Y Oct | -2.50% | |

| 07:00 | GBP | Manufacturing Production M/M Oct | 1.20% | -1.70% |

| 07:00 | GBP | Manufacturing Production Y/Y Oct | -2.20% | |

| 07:00 | GBP | Goods Trade Balance (GBP) Oct | -19.1B | -18.9B |

| 13:30 | CAD | Building Permits M/M Oct | -1.20% | 4.50% |

| 13:30 | CAD | Capacity Utilization Q3 | 79.30% | 79.30% |

| 13:30 | CAD | Wholeleles M/M Oct | -0.10% | 0.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | JPY | Industrial Production M/M Oct F | |

| Forecast: 1.40% | Previous: 1.40% | ||

| 07:00 | EUR | Germany CPI M/M Nov F | |

| Forecast: -0.20% | Previous: -0.20% | ||

| 07:00 | EUR | Germany CPI Y/Y Nov F | |

| Forecast: 2.60% | Previous: 2.60% | ||

| 07:00 | GBP | GDP M/M Oct | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 07:00 | GBP | Industrial Production M/M Oct | |

| Forecast: 1.10% | Previous: -2.00% | ||

| 07:00 | GBP | Industrial Production Y/Y Oct | |

| Forecast: | Previous: -2.50% | ||

| 07:00 | GBP | Manufacturing Production M/M Oct | |

| Forecast: 1.20% | Previous: -1.70% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Oct | |

| Forecast: | Previous: -2.20% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Oct | |

| Forecast: -19.1B | Previous: -18.9B | ||

| 13:30 | CAD | Building Permits M/M Oct | |

| Forecast: -1.20% | Previous: 4.50% | ||

| 13:30 | CAD | Capacity Utilization Q3 | |

| Forecast: 79.30% | Previous: 79.30% | ||

| 13:30 | CAD | Wholeleles M/M Oct | |

| Forecast: -0.10% | Previous: 0.60% | ||