Sample Category Title

Markets Weekly Outlook – FOMC Rate Cut Countdown, Economic Projections May Hold the Key

Week in Review: Markets Buoyed Ahead of FOMC Meeting

The week draws to a close with risk assets largely buoyed by the prospect of an interest rate cut from the Federal Reserve.

On Friday, the main US stock market indexes all moved slightly higher. The Dow Jones gained 236.46 points (a 0.49% rise), the S&P 500 increased by 31.44 points (a 0.46% gain), and the Nasdaq rose by 131.27 points (a 0.56% increase).

Looking ahead to next week, Federal Reserve officials are scheduled to have a significant debate: should they lower interest rates, or keep them steady? The core issue is that while prices remain difficult to control (stubborn inflation) and the job market is still surprisingly strong (resilient), some Fed members are hesitant to cut rates.

Other employment-related data still does not suggest a quick slowdown in hiring, which gives those who prioritize fighting inflation (the "hawks") a stronger argument. Despite this internal debate, investors in the market still anticipate that the Fed will go ahead and cut rates by another quarter-point sometime by June 2026.

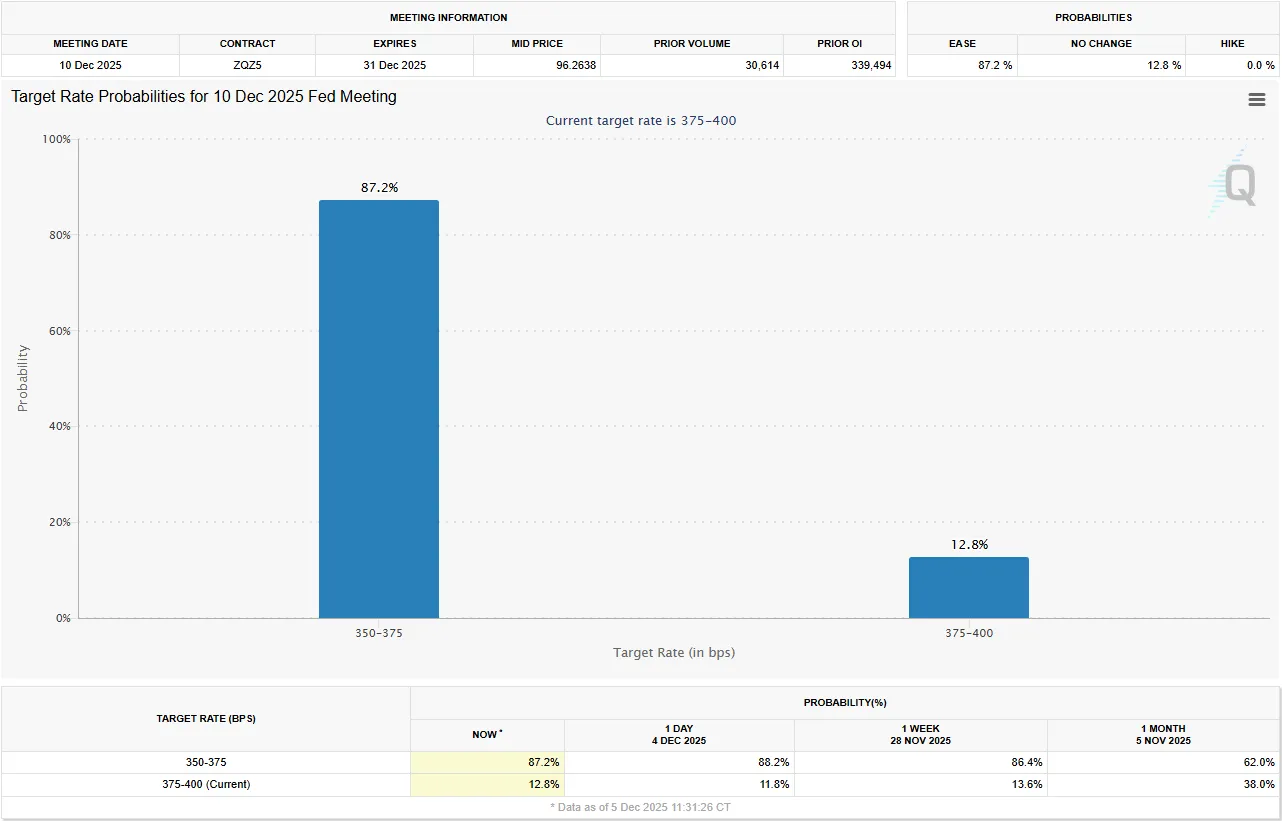

Source: CME FedWatch Tool

Heading into the decision, Wall Street indexes are all near all-time highs with the hope that the Federal Reserve meeting will serve as a catalyst for fresh all-time highs to be printed. Will such a move materialize?

How Did the US Dollar and FX Perform?

The US dollar was slightly weaker on Friday but generally stayed within its recent trading range against other major currencies.

The dollar's strength index (DXY) dipped 0.2%, landing at 98.906, which is close to its weakest point in the past five weeks.

Meanwhile, the euro gained slightly, reaching 1.1651 against the dollar.

The Japanese yen remained mostly unchanged on Friday at 155.15 per dollar, taking a pause after recent days of strength driven by speculation that the Bank of Japan (BOJ) might raise its interest rates later this month. Reports from both Bloomberg and Reuters suggested that BOJ officials are indeed prepared to raise rates on December 19th unless there is a significant unexpected economic event.

The Canadian dollar strengthened by the most in six months against its US counterpart on Friday and bond yields jumped, as stronger-than-expected domestic jobs data boosted bets the Bank of Canada would begin raising interest rates next year.

Finally, the British pound (Sterling) also rose 0.2%, trading at 1.335 and nearing its highest level in six weeks.

The Week Ahead - Fed in Focus, RBA & BoC Rate Decisions Ahead

The week ahead will see market focus on the Federal Reserve rate decision. There is also rate decisions from Canada and Australia but given the stature of the US economy and its ability to affect overall market sentiment, the RBA and BoC decisions will likely be overshadowed.

Asia Pacific Markets

The Reserve Bank of Australia (RBA) is expected to keep its main interest rate unchanged at 3.6% next Tuesday. Since recent reports showed that both inflation and economic growth were stronger than expected, it's now much less likely that the RBA will cut interest rates again. This suggests that the central bank might be finished with its current cycle of lowering rates.

China's trade activity is expected to grow only moderately. Although the recent trade agreement and reduced tariffs from the U.S. should help Chinese exports, the way the numbers are calculated (base effects) will keep the growth rate low. For November, I forecast exports to grow by 3.3% and imports by 3.4%, resulting in a trade surplus of about $100.3 billion.

Separately, China’s inflation rate is predicted to continue its recovery, rising to 0.5% for the year, which is a positive sign after it recently moved back above zero. This is largely because the falling price of food is no longer dragging down the overall inflation number, and the prices of non-food items are starting to rise. While inflation remains quite low, it is important to prevent a sustained period of falling prices (deflation) to keep long-term spending and investment healthy. Since inflation is still low, it will likely not be a major factor in the People's Bank of China's interest rate decisions.

FOMC to Steal the Show

The Federal Reserve (US) is expected to cut its interest rate by $0.25\%$ this Wednesday. While some worry that new tariffs could keep prices high (inflation), the main reason for the cut is the growing concern about the weakness in the job market, which important Fed members have recently noted. Along with the decision, the Fed will release new predictions, which are likely to suggest only one more rate cut in 2026.

However, this long-term outlook might not significantly affect the market's expectations which currently price in two or three cuts for 2026 because the composition of the Fed's voting committee and leadership (including the Chair, Jerome Powell) could change drastically under the new administration.

Separately, Canada is likely to take a break from its recent series of interest rate cuts this Wednesday. Stronger-than-expected recent growth and employment figures support this pause, though we still anticipate one final cut early in 2026 due to ongoing trade risks with the US.

Finally, for the UK, I expect to see an improvement in the monthly Gross Domestic Product (GDP) data on Friday. The previous drop in September was mainly because a cyberattack stopped production at a major car company, but since that production has restarted, October's GDP numbers should bounce back.

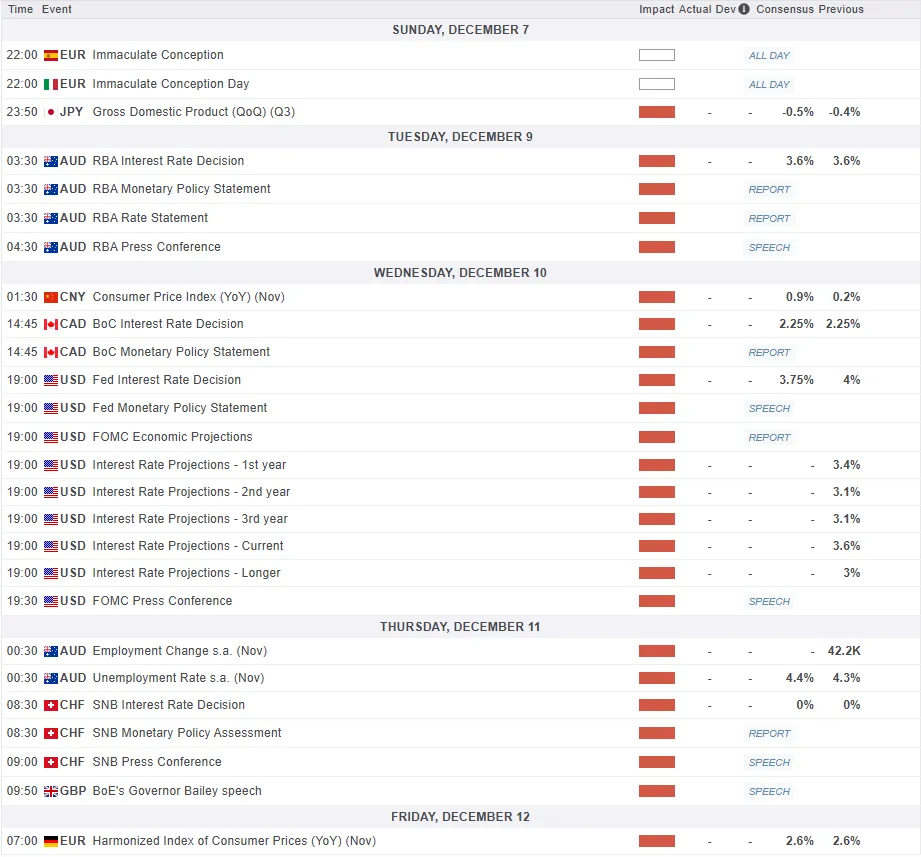

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. GMT time (click to enlarge)

Chart of the Week - US Dollar Index

This week's Chart of the week is the US Dollar Index (DXY)

From a technical perspective, the DXY has had a change in structure having taken out the November 14 swing low around the 99.00 handle.

Thursdays daily candle closed as a hammer offering bulls some hope. However, as has been the case of late any attempt at a bullish move has been met by swift selling pressure.

The period-14 RSI remains below the 50 mark which is a sign of bearish momentum.

Immediate support is provided by the 100-day MA which rests at the 98.58 before the 98.00 and 97.70 handles come into focus.

Upside resistance may be found at the 200-day MA around 99.51 before the 100.00 psychological level and the 100.61 level come into focus.

The Dollar Index trajectory may depend on the economic projections for 2026. Any sign that the Fed see more than one rate cut in 2026 could send the DXY sliding with a test of the YTD low a possibility depending on how dovish the Fed outlook is.

Alternatively, a hawkish stance could have the opposite impact. This would be similar to what we witnessed after the previous Fed meeting in October.

US Dollar Index (DXY) Daily Chart - October 17, 2025

Source:TradingView.Com (click to enlarge)

Be Nimble and Trade Safe.

The Weekly Bottom Line: Fed to Play Santa, Cut Policy Rate

Canadian Highlights

- Canada’s job market defied expectations again in November, pushing the unemployment rate down to a 16-month low.

- The labour market is demonstrating some resiliency, but slack still exists, and the short-term trajectory is marked by significant uncertainty.

- The Bank of Canada will make their final rate announcement of the year next week. We expect the Bank to hold rates steady at 2.25%.

U.S. Highlights

- Real consumer spending was flat in September, ending the third quarter on a soft note. Consumption for the third quarter was up 2.7% (q/q annualized).

- The Fed’s preferred inflation gauge – the core PCE deflator – rose by 0.2% month-on-month in September, as expected. That is still above the Fed’s target at 2.8% year-on-year, but down slightly from 2.9% in August.

- Combined with somewhat soft employment data in November’s ADP report, the Fed looks set to check off markets’ wish list for a rate cut next week.

Canada – Jobs Bringing on the Winter Heat

An update to Canada’s labour market was the sole event in an otherwise quiet start to December. And unlike the recent weather, the data brought some heat. Forecasters were caught flat-footed as Canada’s economy generated 54k jobs, against expectations for modest employment losses. Alongside a contraction in labour force growth, the national unemployment rate legged down to 6.5%, putting it back in line with mid-2024 levels. Other details were more mixed but upbeat on the margin. Part-time jobs drove the entirety of the gain, while job growth was concentrated in the private sector. To add, wage growth and hours worked both ticked higher on the month. In the wake of the news, the Loonie gained to 72 cents/USD, while yields are up a few basis points (bps), continuing their march higher on the week.

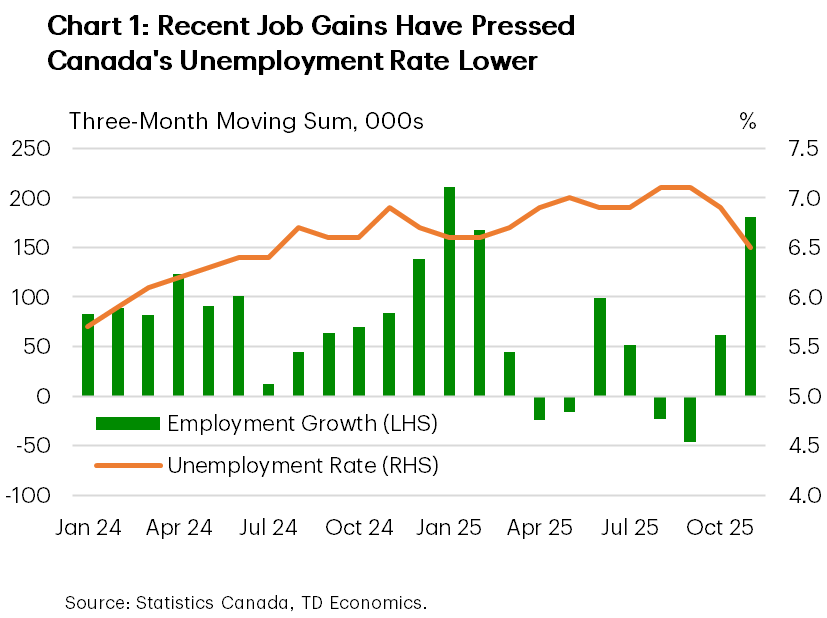

So, what do we make of all this, especially given the Labour Force Survey (LFS) has been particularly noisy in recent months? On one hand, Canada’s labour market is certainly displaying some resiliency. Job creation since tariffs took effect in March has averaged around 16k, roughly in line with historical average steady-state employment gains. That’s a great outcome considering the economy is facing one of the largest external trade shocks on record. What’s more, the Canadian economy gained a staggering 180k jobs over the last three months, which has helped put the unemployment rate on a downward trend (Chart 1).

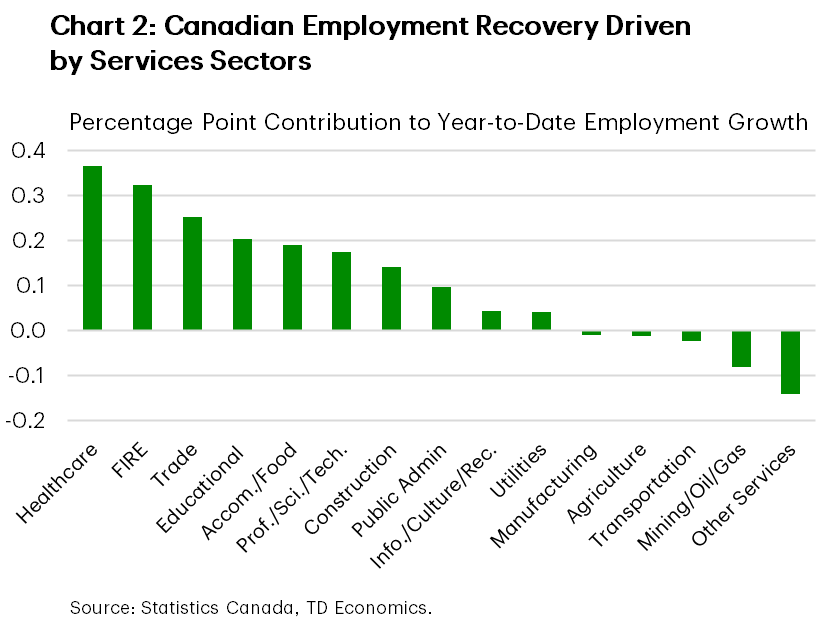

On the other hand, we are cautious to declare this a victory. Job conditions are showing signs of improvement, but the jobless rate is still elevated, and Canada’s payroll survey (SEPH) is painting a much weaker picture of labour conditions, albeit in data only up to September. The composition of employment gains this year has also been skewed, with almost 90% of job creation coming from the services sector (Chart 2). This result is unsurprising as the goods side of the economy is facing more of a disproportional hit from trade-related headwinds, but it still creates a wedge in the employment recovery narrative.

The Bank of Canada’s (BoC) will hold its final policy decision of the year next week. Prior to November’s employment report, it was already expected that interest rates would stay unchanged, and today’s update confirms this view. More important is how Governing Council guides the outlook. They are likely to recognize progress in employment while highlighting ongoing slack in the labour market and considerable uncertainty, especially as Canada and the U.S. enter complex USMCA renegotiation talks. We also expect the BoC will reaffirm that inflation will continue moderating. All told, we expect the Bank to maintain its current stance through 2026 and continue to look for signs that a sustained economic recovery is in the works.

We will finally get an update on how Canada’s exports are faring in the face of U.S. tariffs, as Statistics Canada will publish September’s international trade data on December 11th. Trade data was delayed due to the U.S. government shutdown, with October and November’s data to be released in January.

U.S. – Fed to Play Santa, Cut Policy Rate

Markets are convinced that the Fed will deliver an early holiday gift – a rate cut – next week. Odds of a December cut have hung near 90% ever since shifting up in late November, following support for more easing from Fed Presidents Williams (NY) and Daly (San Fran.). Economic data out this week, while mixed, did not perturb that balance. Equities managed to trek modestly higher, with S&P 500 up 1.1% from last week’s close.

September’s personal income and spending report provided a snapshot of spending and inflation trends before the government shutdown. Spending was flat in real terms in September, ending the third quarter on a soft note. Consumption for the quarter was up 2.7% (q/q annualized) – below expectations but still an improvement from 2.5% in the second quarter. September provides a soft handoff to the fourth quarter, which coupled with the government shutdown, slowing job growth, and weak consumer confidence, suggests spending will slow further at the end of the year. Early data from Thanksgiving weekend suggests holiday shopping was healthy but likely grew at a pace slightly below that of last year. Online sales continued to lead the way, with Cyber Week spending up nearly 8% year-over-year (y/y) according to Adobe. In-store gains were softer, with closely watched indicators pointing to growth in the low single-digits. AI tools helped boost retail site traffic, while a growing Buy-Now-Pay-Later (BNPL) trend also played an important role in propping up spending.

Core PCE inflation rose 0.2% month-over-month (m/m) in September, and 2.8% in y/y terms – a modest easing from 2.9% in the prior two months. The ISM services price index recorded a notable pullback in November – marking a modest positive post-shutdown signal with respect to inflationary pressures. Nonetheless, Cleveland Fed Inflation Nowcasting puts core PCE at 0.23% (m/m) for both October and November, 2.8% and 2.9% in y/y terms respectively – still well above target.

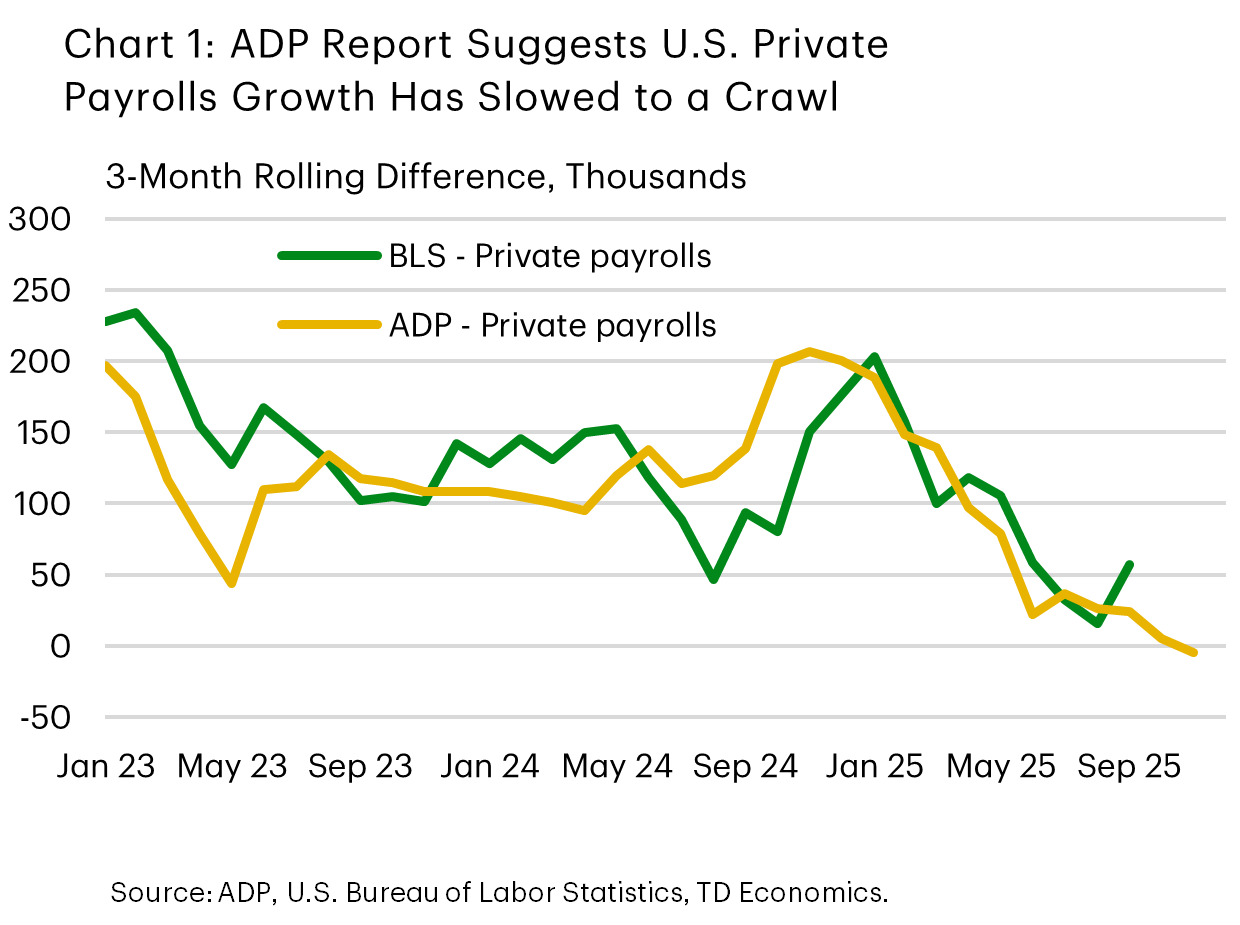

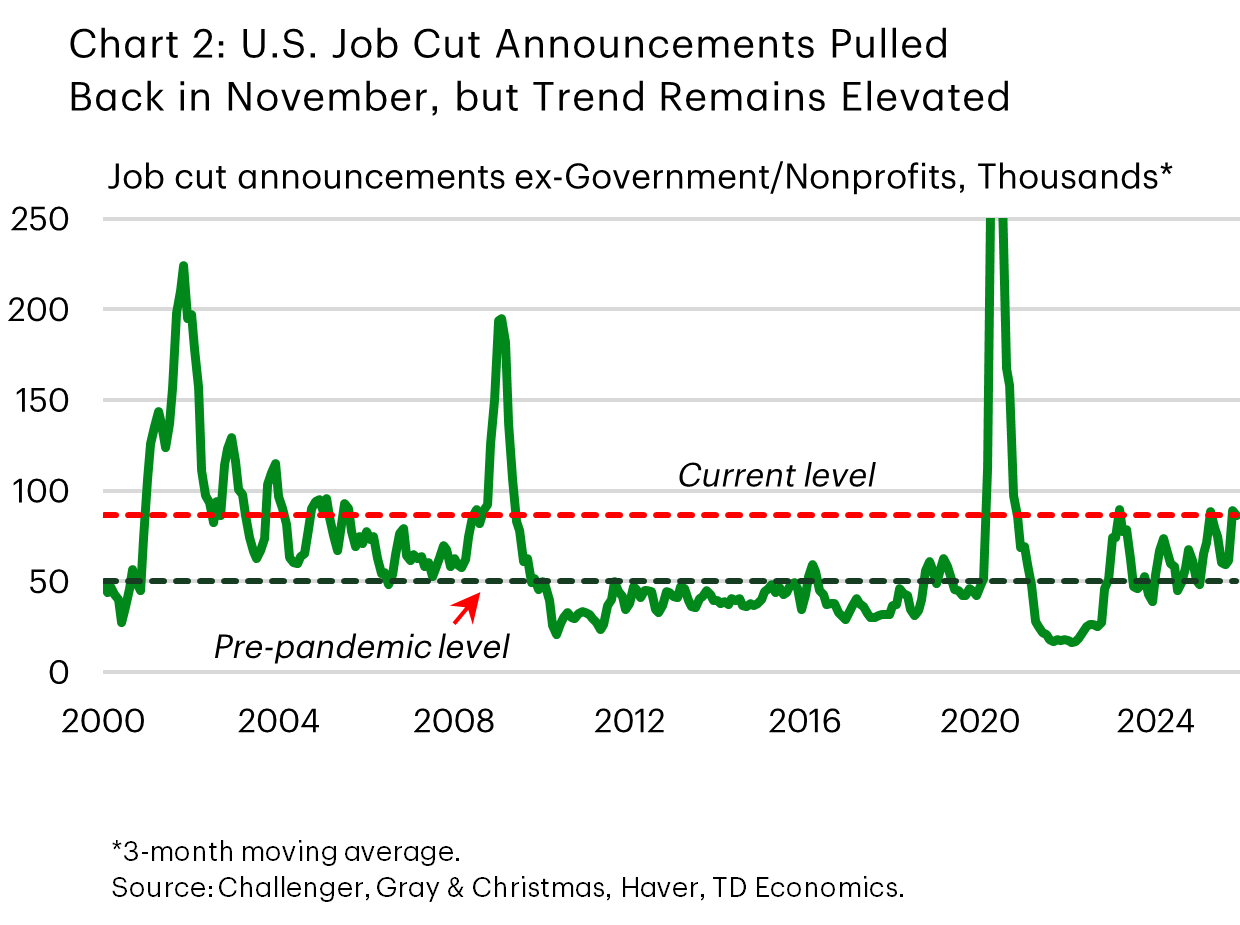

Employment data was mixed. Initial jobless claims dropped to a three-year low of 191k at November’s end. The Thanksgiving holiday may have distorted the data. But even prior to that last week, initial claims were still trending lower. Conversely, the ADP report showed private payrolls fell by 32k in November. Its three-month average, which is more closely aligned with the BLS equivalent, turned slightly negative too (Chart 1). Job cut announcements, meanwhile, also pointed to continued challenges. Layoff announcements in November were cut in half from their October tally, coming in at 71k. But even when looking past the weakness in the government sector, the trend in layoff announcements remains elevated (Chart 2). Overall, markets seemingly expect the Fed to focus on signs of labor market softness and maintain a cautious policy stance.

Our reading is that the Fed won’t disappoint market expectations next week. But in the New Year, the bar for additional cuts may be higher. Having delivered some insurance cuts, the Fed will likely take time to digest delayed economic reports and carefully assess post-shutdown data to form a clearer picture of the economy’s health.

Weekly Economic & Financial Commentary: A Split Committee and Steady Dots

Summary

United States: Consumers Still Carry the Torch, but the Glow Is Fading

- As Powell heads into one of his four remaining meetings as Fed Chair, strength in services and lingering consumer resilience contrast with manufacturing weakness, reinforcing expectations for a December rate cut.

- Next week: JOLTS (Tue.), ECI (Wed.), FOMC Meeting (Wed.)

International: Global Crosswinds: Sticky Prices and Softer Signals

- Eurozone inflation rose more than expected in November, reinforcing the case for the European Central Bank to keep rates on hold. Australia’s Q3 GDP came in below consensus with underlying details showing modest resilience. And in emerging markets, the Reserve Bank of India cut its policy rate and signaled a dovish bias while maintaining a neutral stance.

- Next week: Japan Labor Cash Earnings (Mon.), Bank of Canada Policy Rate (Wed.)

Topic of the Week: A Split Committee and Steady Dots

- The FOMC heads into its December meeting with a rare degree of internal division. Regional presidents—particularly those with a vote—have signaled greater skepticism toward further easing, setting the stage for opposition in both directions of the policy decision, though the more dovish governors are likely to provide the critical mass of support needed for another 25 bps rate cut.

US Dollar Index (DXY) Slips as Rate Cut Bets Remain Unchanged Post US PCE and University of Michigan Data

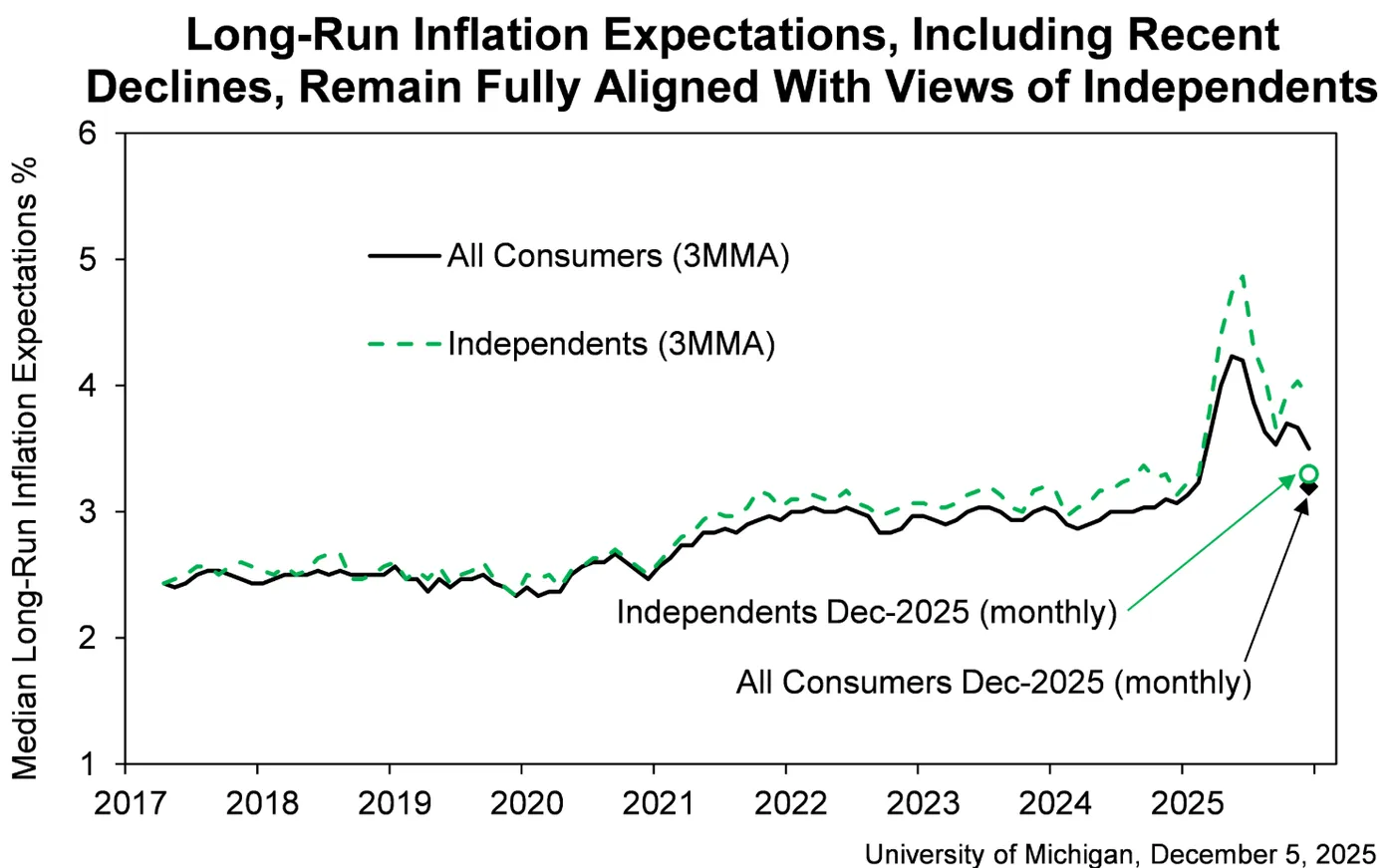

American consumers felt slightly better about the economy in early December, according to a survey released on Friday.

The Consumer Sentiment Index from the University of Michigan went up to 53.3 this month, an improvement from 51.0 in November, and slightly better than what economists expected.

However, the overall mood remains gloomy. The main problem is that consumers are still very worried about high prices (inflation) and are not very optimistic about the job market.

On a positive note, consumers expect price increases to slow down slightly: they now anticipate inflation will be 4.1% over the next year, down from 4.5%, and 3.2% over the next five years, down from 3.4%.

Source: UofM

PCE Data Release for September 2025

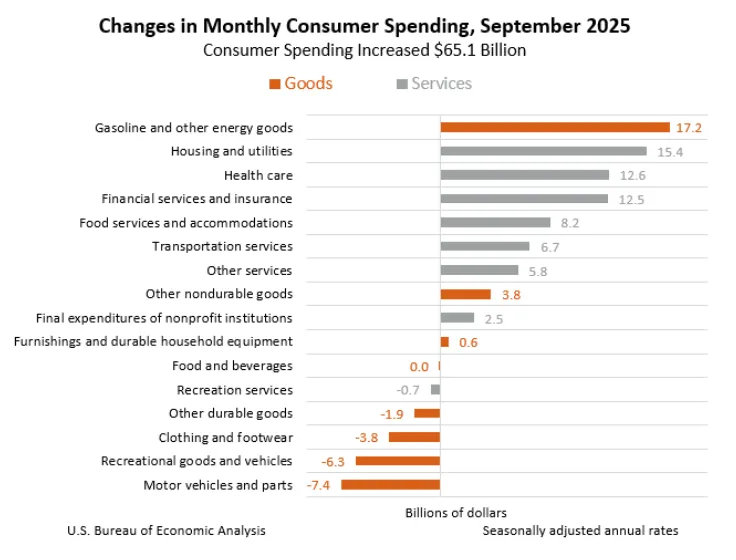

In September 2025, Americans spent 0.3% more than they did in August, which was a total increase of about $65.1 billion. This increase was exactly what financial experts had predicted.

The main reason for this spending growth was a large jump in spending on services (up by $63.0 billion), especially on housing, utilities, healthcare, and financial services. Spending on physical goods saw only a small increase (up by $2.1 billion).

This small gain was due to a sharp rise in the cost of gas and other energy; otherwise, spending would have fallen, as people spent less money on things like cars, recreational items, and clothes.

Source: US Bureau of Economic Analysis

Market Impact & US Dollar Index (DXY) Reaction

The data was not really a huge surprise and heading into the release i did not expect it to have a major impact on the Interest rate outlook moving forward for the Federal Reserve.

Those assumptions have been proved correct with rate cut expectations remaining relatively unchanged for next week's Federal Reserve meeting. Markets are still pricing in around an 87% probability of a 25bps rate cut next week.

Heading into next week's Fed meeting, I still believe that the economic projections may hold more weight than the actual decision by the Fed. This is unless the Fed defy market expectations and hold rates steady. Any rate cut may receive a lukewarm response.

However the 2026 economic projections and particularly those around how many rate cuts the Fed sees in 2026 could stoke significant volatility.

At the previous meeting the Fed's economic projections only showed one 25 bps rate in 2026. Any dovish or hawkish tilt in this regard could send market volatility soaring.

Following today's data, the US dollar index slipped further as pressure continues to mount on the greenback.

Immediate support rests at 98.72 before the 100-day MA at 98.58 and the 98.00 handles come into focus.

On the upside, resistance may be found at the 200-day MA resting at 99.51 before the psychological 100.00 becomes an area of focus once more.

US Dollar Index Daily Chart, December 5, 2025

Source: TradingView

Trade Safe.

BoC to Leave Interest Rate Unchanged After Cuts in October and September

Dual central bank interest rate decisions from the U.S. Federal Reserve and the Bank of Canada on Wednesday top the week’s calendar, with the BoC expected to hold rates, while a third consecutive 25 basis point cut from the Fed looks highly likely.

Our base case forecast a month ago did not assume a December cut from the Fed, given inflation in the U.S. remains above the central bank’s 2% target, and Chair Jerome Powell’s comments at the last meeting about cautiously proceeding in a foggy environment.

However, with an unusually divided FOMC committee, next week’s decision was always going to be a very close call. Fed communication over the last few weeks has also been leaning in the direction of a cut. With some softer data during the blackout, we doubt the hawks will put up a major fight.

A hold by the BoC in comparison should be relatively uncontroversial. After October’s rate cut, policymakers signaled that “the current policy rate is about the right level” to deliver low, steady inflation while supporting growth through uncertainty.

Delayed September Canadian trade data next week would need to show a 3.4% increase in merchandize export volume from August, and a 3.1% decrease in goods import volume in order to match the details in the third quarter GDP data from last week.

More important still are the trade details from U.S. census bureau on whether CUSMA exemptions have continued to hold up to support Canadian exports to the U.S. in September.

How the labour market plays into the BoC decision

BoC’s holding bias was contingent on the central bank’s forecast for soft but positive economic growth. Gross domestic product growth in Q3 surprised on the upside with a 2.6% annualized increase versus the BoC’s 0.5 % projection, with mixed details.

But labour markets have also shown more signs of stabilizing with employment rising 54,000 in November after already firm increases in September and October. The (less-volatile) unemployment rate dropped to 6.5% in November from 7.1% in September. Weakness still exists among tariff-exposed manufacturing sectors, but economy-wide layoffs have remained low.

As a result, household spending has broadly remained resilient this year despite a tick lower in Q3. Spending was, in part, supported by earlier BoC rate cuts that have reduced debt service pressures. Financial market gains have bolstered net worth, adding to aggregate purchasing power.

We expect those trends will have persisted in Q3, and next week’s national balance sheet data to show little changes in households’ debt service ratio from Q2 level that was already below 2019, and further gains in financial assets and net wealth.

Today, underlying inflation pressures are running above the BoC’s 2% inflation target, and could prove stickier than the central bank would like in the future thanks to stronger-than-expected consumer and government spending in 2026. Our base case assumes per-capita growth will slowly improve in 2026 with no additional interest rate cuts from the central bank.

Week ahead data watch:

The Q3 national balance sheet account details next Thursday should show rising household net worth with asset expansion outpacing growth in liabilities. Robust stock market gains in Q3 (the TSX index were up 11.8% and the S&P 500 up 10.3%) were partially offset by lower home equity given an 1.8% drop in home prices. Households’ debt service ratio is expected to remain little changed at 14.4%, as debt payments continued to rise at a similar pace as disposable income.

The release of September Canadian (and U.S.) international trade data delayed by the U.S. government shutdown should show a narrowing in the Canadian trade deficit. But the magnitude of the improvement will be watched closely after Statistics Canada needed to impose imputed placeholders on Canadian export data to compile the contribution of net trade to Canada’s Q3 GDP report. Most of a 3.1 percentage point (annualized rate) add to GDP growth in Q3 came from a pullback in imports that was not impacted by the U.S. shutdown. But the quarterly GDP data also implied a 3 1/2% increase in September merchandise export volumes.

US: Consumer Spending Stalls in September

Personal income rose 0.4% month-over-month (m/m), on par with the prior month. On an inflation adjusted basis, personal income was up just 0.1% m/m.

Consumer spending grew 0.3% m/m in nominal terms. This was in line with market expectations, which called for growth to slow from the 0.5% m/m pace seen in August. However, September's gain was entirely due to higher prices, as spending remained flat after adjusting for inflation. Looking at the broad categories, consumers dialled back their spending on goods (-0.4% m/m), led by reduced spending on motor vehicles and parts, as well as recreational goods and vehicles. Spending on services edged higher (+0.25% m/m).

With nominal spending growing at a similar pace to income, the personal savings rate held steady at 4.7% but is down a percentage point from April.

There was little change on the inflation front. Core PCE – the Fed's preferred inflation gauge – rose by 0.2%, on par with the pace seen over the previous two months. In annual terms, core PCE inflation was up 2.8% year-over-year, down slightly from the 2.9% pace in August.

Key Implications

Today's data indicate that both consumer spending and income growth slowed to close out an otherwise strong quarter. Inflation-adjusted spending grew by 2.7% annualized in Q3 – up slightly from 2.5% in Q2. However, September's weaker performance, combined with the recent pullback in consumer confidence metrics and softening labor market, suggest spending is likely to slow to a sub-1% pace in Q4.

Although the Fed's preferred inflation measure remains above its target, it has not accelerated and has stayed relatively stable over the past five months. Softer spending momentum and steady inflation should provide further reassurance to the Fed, solidifying the case for another quarter-point rate cut at next week's FOMC meeting.

Week Ahead – Rate Cut or Market Shock? The Fed Decides

- Fed rate cut widely expected; dot plot and overall meeting rhetoric also matter.

- Risk appetite is supported by Fed rate cut expectations; cryptos show signs of life.

- RBA, BoC and SNB also meet; chances of surprises are relatively low.

- Dollar weakness could linger; both the aussie and the yen best positioned to gain further.

- Gold and oil eye Ukraine-Russia developments; a peace deal remains elusive.

Fed meeting in focus

With risk assets, including the ailing cryptocurrencies, remaining bid this week, mostly on the back of ballooning Fed rate cut expectations, the countdown to the most critical event until year-end is almost over. On Wednesday, at 19:00 GMT, the Fed will announce its rate decision, with the market appearing confident about another 25bps rate cut.

Aggressively hawkish Fedspeak, the minutes of the October meeting revealing a strong barrier to another cut, and the absence of clean data due to the federal government shutdown made the Fed rate cut look extremely unlikely during November. Everything changed, though, after New York Fed President Williams’ remarks on November 21, supported by the few data releases for November – particularly Wednesday’s weak ADP report – with the probability of the rate cut jumping to 86%.

On Wednesday, the focus will also be on the dot plot and overall meeting rhetoric. In September, the dot plot projected three rate cuts by the end of 2026, one more cut than in June. With the market currently pricing in 63bps of easing during 2026, there is a decent chance of the three rate cuts penciled for next year, making it the baseline scenario for the Fed.

While any dot plot adjustments might be easy to justify, Chair Powell will have some serious explaining to do if a rate cut is indeed announced, after stating in the October press conference that one should slow down when driving in the fog. Using the “weaker labour market” argument will probably be seen as a shallow justification, once again damaging the Fed’s low credibility.

Notably, these two factors – the dot plot and the meeting’s overall rhetoric – might prove less important for the 2026 policy outlook than usual, since Trump has probably picked Powell’s replacement. NEC Director Hassett appears to be the chosen one to lead the Fed into the future (of lower rates).

Markets have been preparing for the Fed meeting

It has been a relatively quiet period, with one-month volatility easing across the board, but this could change dramatically next week. Confirmation of Fed rate cut expectations, along with balanced-to-dovish rhetoric and the dot plot pointing to three rate cuts, would support the current prevailing, but fragile, risk-on sentiment. Both equities and gold are expected to rally, with the dollar finding it difficult to reverse the current weakness. A strong move above 1.1700 in euro/dollar, resulting in a fresh higher high, would confirm the current short-term bullish trend.

The most acute market moves will probably take place in the unlikely scenario of the Fed keeping rates unchanged, a major upset to the current expectations. The initial aggressive risk-off reaction, with stocks tumbling and the US dollar strengthening, might only be tempered by an overly dovish Powell press conference and the dot plot projecting four rate cuts in 2026. Even then, markets might still feel betrayed, maintaining the bearish momentum. A drop below 1.1572 in euro/dollar would be important, but only a move below the key 1.1500 zone would negate the current short-term bullish trend.

Gold and oil also eye geopolitical developments

The Fed meeting is not the only game in town next week, as both gold and oil await developments on the Ukraine-Russia front. While the first round of meetings with Trump’s representatives was characterized as fruitful, sticky points – particularly the frozen Russian assets and the occupied eastern Ukraine regions – could derail the current effort.

Gold continues to hover near $4,200, with a dovish Fed meeting and a high-profile breakdown in the Ukraine-Russia negotiations creating a dual tailwind that could drive the precious metal towards the all-time high of $4,381.

Similarly, despite the confirmation of the current production quotas until end-March 2026 by the OPEC+ alliance, oil has been unable to rally meaningfully above a key downward sloping trendline. Positive progress, in the form of preparations for a trilateral meeting between US, Russian and Ukrainian leaders, could push oil towards the October trough of $56.36, close to the four-year low of $55.60.

How hawkish could the RBA sound?

Following three rate cuts during 2025, the chances of a dovish surprise on Tuesday are almost zero. Inflation has been stubbornly high, with the October CPI edging higher to 3.8%, and the trimmed mean following suit. Despite the weaker Q3 GDP report, partly due to softer consumption, RBA Governor Bullock is focused on the elevated inflationary pressures and the tightness in the labour market.

Externally, despite the numerous support programmes and the upbeat GDP projections for 2026, the world’s second largest economy continues to face deflation. Improved economic momentum in China would benefit Australia, potentially adding pressure for a more restrictive stance ahead.

The divergence in rhetoric between the Fed and RBA has been playing a pivotal role in the aussie/US dollar rally towards the 0.6610 zone. Confirmation of this central bank divergence next week could fuel a move towards the 0.6680 region, particularly if Fed Chair Powell opens the door to a January 2026 rate cut. That said, a more balanced message from Bullock et al. might result in a decline towards the 0.6550 area.

The BoC is expected to keep it powder dry

Following 100bps of easing so far in 2025, the BoC is expected to stand pat on Wednesday. However, excluding the surprisingly strong Q3 GDP report, the positive news is scarce, as seen in this week’s S&P Global PMI surveys. But the main headwind for the Canadian economy remains the stalled negotiations with the US over tariffs, mostly regarding products currently not covered by the USMCA agreement.

With additional tariffs hanging over their heads like Damocles’ sword, Governor Macklem et al. will probably remain slightly dovish and repeat their readiness to respond if the outlook changes dramatically. Unsurprisingly, dollar/loonie has been trading sideways, mostly due to the greenback’s weakness. The combination of a dovish Fed meeting and a more balanced BoC rhetoric could open the door to a decline towards the late-October low of 1.3887.

Unchanged SNB set to remain vigilant

The SNB is treading on thin ice as consumer price inflation continues to flirt with negative territory. The negative annual growth in PPI, following an especially weak Q3 GDP report, is seriously clouding the outlook, increasing the pressure for a dovish tilt on Thursday.

That said, not everything is bleak, as the recent PMI surveys and October retail sales managed to produce upside surprises. More importantly, the US and Switzerland have reached a trade agreement, with the US rate dropping from 39% to 15% and Switzerland committing to a $200bn investment until end-2028.

SNB President Schleger has recently repeated the high bar for negative rates, hoping that the SNB’s projection for inflation acceleration in 2026 will be confirmed. Notably, markets have not been indifferent to the negative rate remarks, with the Swiss franc stabilizing lately against both the euro and the dollar. Pending a dovish tilt on Thursday, the Franc’s short-term reaction will mostly depend on the dollar’s performance. Interestingly, the convergence of simple moving averages in dollar/franc are pointing to increased volatility ahead.

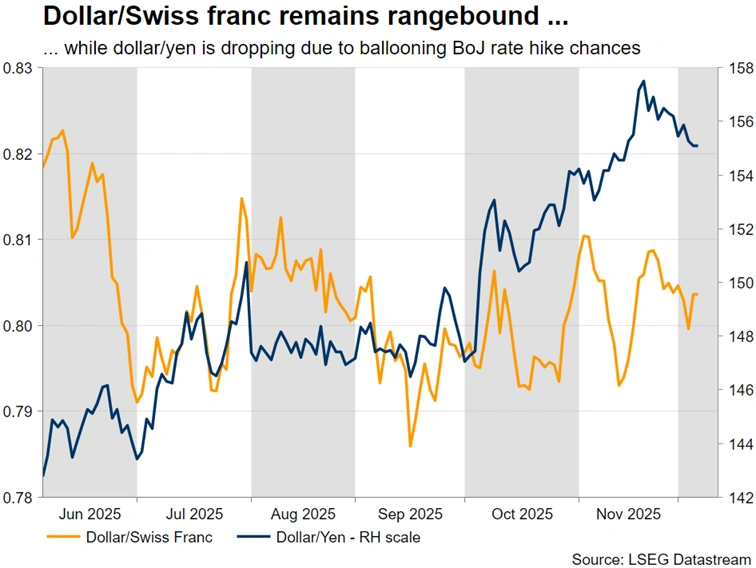

Is the BoJ on the cusp of the much-anticipated rate hike?

Since mid-November, there has been a hawkish tilt in BoJ commentary, with the latest reports suggesting that the government has agreed to the BoJ rise. Armed with elevated inflation and some initial positive wage growth demands, the BoJ is ready to take a leap of faith, hoping that this move won’t backfire down the line. Dollar/yen continues to decline, also taking advantage of the greenback’s weakness, with the first support expected in the 153.20-154.50 area.

Weekly Focus – US to Cut Rates Despite High Inflation

Over the last month, market expectations have increasingly turned towards a 25bp rate cut when the Fed makes its decision on Wednesday next week. This has been driven by lower inflation expectations and weaker forward-looking economic data, such as the balance between orders and inventories in the PMI and ISM surveys for November - private sector data that is still coming in a timely manner while the aftereffects of the government shutdown continue to hamper official data. Opinions clearly differ among members of the rate-setting committee, but we now see it as most likely that they will chose to do as the market expects and deliver the rate cut next week even though inflation is clearly above target. Arguably, even if rates are cut to 3.5% - 3.75%, they will still be high enough to dampen the economy and inflation pressures. However, with wider financial conditions still supportive and fiscal policy to be eased in 2026, we see a good case for the Fed to signal a cautions stance where future rate cuts will come at a slow pace. Ahead of the rate decision, we will get the much-delayed data on job openings in September.

President Trump has flagged that he has made a decision about who will be the next Fed chairman, and betting markets overwhelmingly expect it to be Trump loyalist Kevin Hassett, who will presumably push for more rate cuts. However, the usual rotation of regional Fed presidents as voting committee members could likely push in a more hawkish direction next year.

In the euro area, wage growth was 4.0% y/y in Q3 according to the compensation per employee measure which is the one the ECB prefers. In the ECB's staff projection, the number had been forecast at 3.2%, so this is a data point that speaks clearly against another rate cut in 2026. In the same direction, GDP growth for Q3 was revised up from 0.2% to 0.3% q/q and inflation for November came in slightly higher than expected at 2.2%. For both GDP and inflation though, the upside surprises were really due to rounding up from a slightly higher second decimal so in reality, they were very small surprises.

Chinese PMI data again came in weaker than expected, with the index for new orders declining from 50.5 to 50.1 in the private sector RatingDog version and staying below the 50-threshold in the official NBS version. This came despite a clear increase in the export orders index, which suggest that the weak export data we saw in October was a one-off caused by the short-lived escalation in the trade war with the US we saw in that month. This is likely to be confirmed by the foreign trade data for November that will be released on Monday. The NBS PMI for employment declined to 46.7. This index often correlates with consumer spending in China. Together with the weakness in domestic orders, the clear picture is that domestic demand remains subdued despite the recovery in exports.

A rate hike in Japan later this month is almost fully priced in. The last remaining piece of the puzzle is wage growth which remains too low to compensate for inflation, so focus could turn to the October wage data due on Monday.

Fed Preview: Hawkish Cut is the Consensus Choice

- We expect the Fed to cut its policy rate target by 25bp to 3.50-3.75% next week, in line with consensus and market pricing. We expect an equal reduction to all administered rates, but an additional 5bp cut to the IORB rate is not off the table.

- The Fed could also follow up on its October decision to end QT by announcing the start of organic balance sheet expansion in 2026, which would ease USD liquidity conditions further.

- We expect Powell to verbally push back against continuation of sequential rate cuts in early 2026. Updated dots will likely signal a range of views for 2026 rates outlook, but we expect median long-range dot to remain at 3.00-3.25%.

- Hawkish forward guidance could push UST yields higher and EUR/USD lower on Wednesday, but we maintain our upward sloping 12M EUR/USD forecast at 1.22.

Markets are pricing next week's 25bp cut to the policy rate target as largely a done deal, but 2026 outlook for both rates and liquidity remains a lot less clear. We expect Powell to push back on expectations of sequential rate cuts continuing in early 2026, echoing the message heard in October and reflecting the widely varying views within the FOMC. Knowingly delivering a 'hawkish cut' is a consensus choice.

Even though incoming macro data has not delivered decisive signals since October, we believe that the decline seen in markets' inflation expectations makes another rate cut more palatable even for the hawks (chart 1). Overall financial conditions have tightened modestly as real short rates have moved higher.

Jeffrey Schmid is likely to repeat his dissent in favour of a hold and could potentially be joined by Susan Collins and/or Alberto Musalem. Chicago Fed's Austan Goolsbee also prepared markets in November by saying he sees 'nothing wrong with dissenting'. On the other side, Trump-nominated governors Waller, Bowman and Miran together with NY Fed's John Williams form the backbone of the dovish camp.

We see a good chance of the Fed pausing its easing cycle in January, as three of the four new 2026 voters - Hammack, Kashkari and Logan - have all vocally opposed the October decision to cut. In our base case, we expect final 25bp cuts in March and June. The updated dots are likely to reflect the growing diversity of views even by the end of 2026. Macroeconomic forecasts will see more cosmetic changes; we expect a small positive revision to 2026 GDP forecast while inflation outlook will likely remain mostly unchanged.

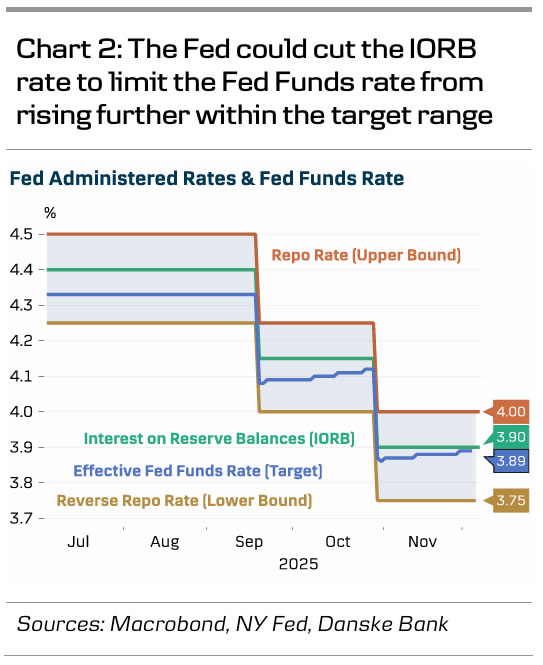

The Fed formally ended its balance sheet drawdown at the start of December, but liquidity conditions remain on the tighter side. The effective Fed Funds rate has risen modestly within the target range, and SOFR traded above the upper bound around month-end. While liquidity is not an imminent concern in our view, the Fed could pre-announce organic balance sheet expansion, or gradual QE, starting in 2026. Alternatively, the Fed could lower the interest rate of reserve balances (IORB) by additional 5bp to limit the Fed Funds rate from rising further, though we see the former more likely than the latter.

Loonie Rallies After Canada Adds 54,000 Jobs in Major Employment Beat

Some change is starting to appear for Canada after consecutive rough years.

Subject to a red-hot post-COVID boom, the Land of the Maple Syrup had severely tightened its policy rates and immigration rules, leading to a consecutive trough in activity starting in 2024.

To add to that, US President Trump’s protectionist policies placed huge tariffs on key Canadian exports, including Lumber, Aluminium, and many others, damaging demand for Canada's cyclical economy and its prospects for growth.

Given that growth prospects are essential for inciting business investment and hiring, it is clear why Canada struggled quite a bit under such pressure.

But with peak fear subsiding and in the absence of an actual trade deal, Canadian data is bouncing suddenly, and the CAD now leads its FX peers on the session.

Morning FX Performance, pre Core PCE (9:03 A.M.) December 5, 2025 – Source: TradingView

The shock came this morning with the publication of their third consecutive beat in Employment, posting a gain of +53.6K jobs (vs -5K exp).

This also dropped the Unemployment rate considerably, from 7.0% to 6.5%.

While most of the gains have been in the part-time economy, this is not entirely sub-optimal, as Canada's part-time and seasonal labor market is substantial, with winter and subsequent summer jobs solidifying Canada's labor picture.

This strong surprise combines with recent beats in GDP and Housing data.

Is Canada on the rise again, as the Bank of Canada looks to be done with its rate cuts (currently at 2.25%)?

Canadian interest rate futures are already beginning to price hike premiums in 2026!

Details of the Canadian Employment report – December 5, 2025

USD/CAD 4H Chart

USD/CAD 4H Chart. December 5, 2025– Source: TradingView

The North-American pair is reaching levels not seen since mid-September as USD/CAD was breaking higher on failed trade deal negotiations.

Since November 25, the pair has reversed harshly after forming a double top, bearish Moving Average crosses and now testing Key levels.

On the verge of breaking its 1.39 (+/- 200 Pips) Major support zone, there won't be much to support the pair on a break lower before 800 pips below at 1.38.

Momentum is a bit oversold which can lead to consolidation, so watch how things develop with the soon releasing Core PCE.

Levels of interest for USD/CAD Trading

Resistance Levels

- 1.3930 Mini-resistance

- 1.40 Major Pivot acting as resistance

- Cycle highs 1.4143 and Double top

- Resistance between 1.4120 to 1.4145

- Key resistance 1.4250

Support Levels

- Major Support 1.3870 to 1.39 (breaking)

- 1.38 Major support +/- 150 pips

- August range support 1.3750

- 1.3550 Main 2025 Support

EUR/CAD 8H Chart

EUR/CAD 8H Chart. December 5, 2025– Source: TradingView

The rally in EUR/CAD in 2025 has been relentless, particularly when looking how weak the Loonie got in recent years.

Up from 1.46 to 1.6490 (Levels not seen since 2009) in just a year, the momentum had been a one way flow.

Things are starting to change however, with the current range (1.6130 to 1.63) lasting long enough to break below the 2025 upwards trendline.

Now testing the higher timeframe pivot, EUR/CAD sellers will want to push for a weekly close below 1.6120 to confirm a break-down.

Failing to do so maintains the two week range.

Levels of interest for EUR/CAD Trading

Resistance Levels

- 1.62 Mid-range Resistance

- 1.6258 MA 50 and 200

- July 2009 Highs around 1.6350

- August 2025 Highs 1.64697

Support Levels

- 1.6150 Range lows & Higher timeframe Pivot (testing)

- 1.6050 Minor Support

- Support for higher trend 1.5950

Safe Trades!