Sample Category Title

Sunset Market Commentary

Markets

The October Empire Manufacturing Business Survey is one of those sole data points we get from the US with the government shutdown interfering with most of the data releases since the start of the month. The NY manufacturing index from the NY Fed unexpectedly reversed last month steep drop, rising back from -8.7 in September to 10.4 (11.9 in August). Details showed improvements across the board, both for the actual subindex and the one projecting sentiment 6 months ahead and both on the activity (eg new orders, shipments, but also employment) and the price front (paid & received). The outlook for prices paid approached the highest levels since 2022. The notoriously volatile Empire Manufacturing Survey didn’t impact trading though. At the margin, it helped US yields away from key support areas (eg US 2-yr 3.46% and 10-yr 4%). In this respect, it’s striking that yesterday’s Fed Powell speech didn’t have any more impact. He sealed the deal for October (25 bps rate cut) as downside employment risks rise faster than upside inflation risks and simultaneously called an end to the quantitative tightening cycle in coming months. Tonight, the Fed still releases its Beige Book, a summary of regional economic conditions which serves as a preparatory document for the FOMC meeting and is often overlooked. This time around, it could obviously grab some more attention though its hard to impact market pricing. The euro tried to build on yesterday’s intraday comeback but the move didn’t reach far. EMU bond markets fall back on the dovish reflex which dominated the period between US Liberation Day and the EU/US trade deal. They start erring more significantly in the direction of another ECB rate cut over the next 12 months. Daily changes on the German yield curve range between 2.2 bps (2-yr) and 4.4 bps (30-yr). France meanwhile remains stuck between a rock (budgetary crisis) and a hard place (legislative elections) as PM Lecornu tries to win confidence votes tomorrow. Despite support from leadership of French Socialists and Republicans, it remains to be seen whether they can rally all of their MP’s behind the party line. The margin for error is thin. Markets take the optimistic approach today with French assets outperforming. The CAC40 rebounds 2.1% with strong company earnings helping out as well. The EuroStoxx 50 currently recovers 1.15% with key US indices opening with 0.6%-0.9% gains. The 10-yr OAT-swapspread narrowed from 84 bps yesterday morning to currently 77 bps.

News & Views

The Norwegian (minority) government today published a draft budget for next year. The budget from the Labour government needs approval from smaller parties, which currently hold some non-addressed demands. The draft foresees NOK 579bn of the spending to be covered by funds of the Government Pension Fund Global (GPFG). This represents 2.8% of the value of the fund (capped at 3%) and represents about 27% of the budget expenditure. The government believes that 2026 fiscal policy will have an approximately neutral effect on the economy. Amongst others, the draft proposes NOK 4bn in income tax cuts and a NOK 11.5bn allocation to electricity support. The budget is estimated to raise defense spending to 3.4% of GDP. Government projections expect the mainland economy to grow by 2.1% next year from 2% this year. CPI-ATE inflation is expected to ease to 2.5% next year from 2.9% this year. At the its September 17 meeting the Norges bank cut the policy rate to 4% from 4.25%, but indicated that further easing might develop slower as the economy is holding relatively resilient. With respect to fiscal policy, the NB in September also assessed the structural non-oil public deficit at 2.7% this year and 2.8% next year. The krone today rebounds from EUR/NOK 11.79 to 11.715 today, but this is mainly due to a better risk overall sentiment.

In an interview with Bloomberg TV, the chief economist of the Reserve Bank of New Zealand, Paul Conway, indicated that after reducing the official cash interest rate by 50 bps to 2.5% the policy rate now is at the lower end of the neutral range. The RBNZ is still prepared to further cuts if data warrant so. According to Conway, the 0.9% Q/Q contraction in Q2 raised the possibility of a more prolonged period of excess capacity in the NZ economy and might cause less medium term inflation pressures. The RBNZ wanted to reacted to that, even as inflation currently still holds near the top of the RBNZ’s 1-3% target range. It is confident that this relatively high inflation will dissipate. NZD gains about 2.3% YTD against USD, but this places it as the laggard compared to G10 peers.

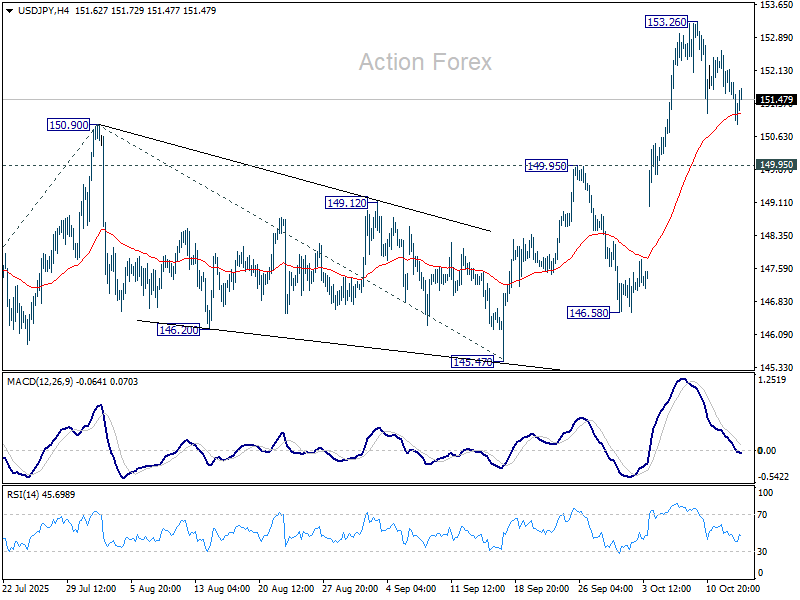

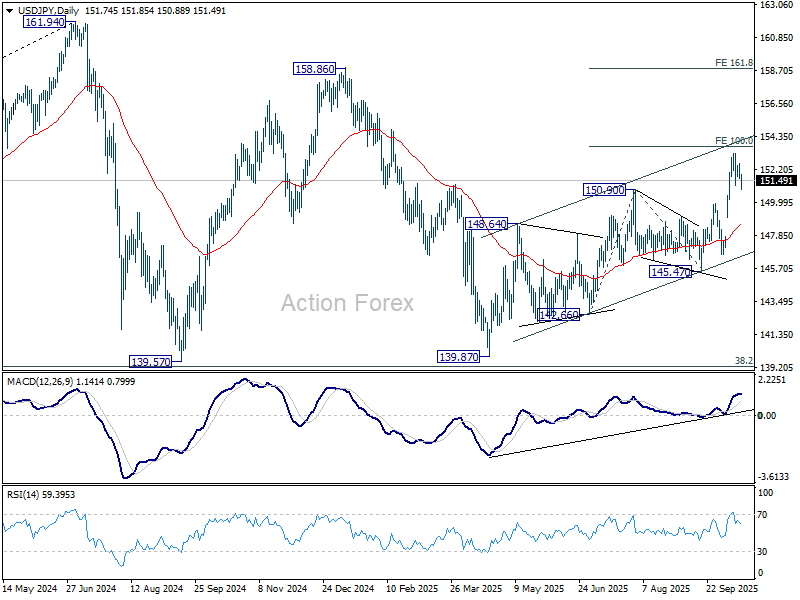

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.41; (P) 152.01; (R1) 152.42; More...

Intraday bias in USD/JPY remains as consolidation continues below 153.26. Downside should be contained above 149.95 resistance turned support. Break of 153.26 will target 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there will pave the way to 161.8% projection at 158.80. However, decisive break of 149.95 will bring deeper pullback to 55 D EMA (now at 148.58) instead.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

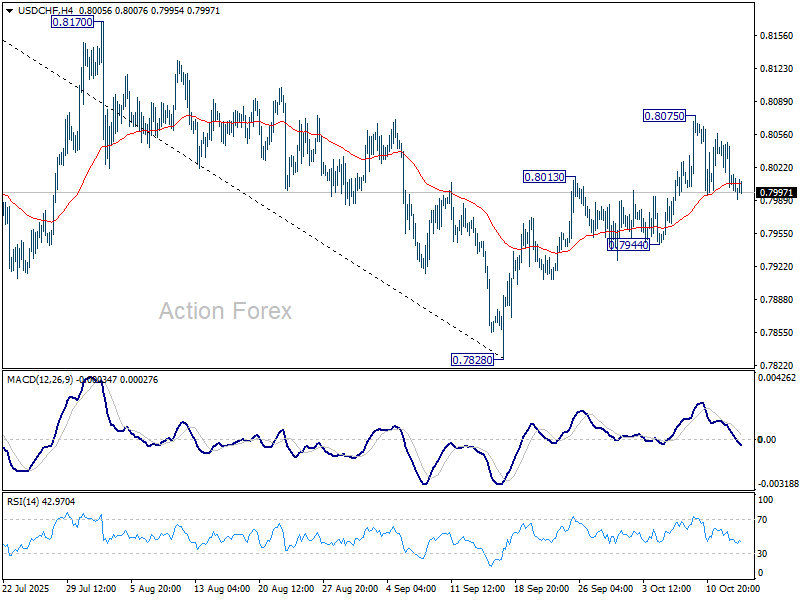

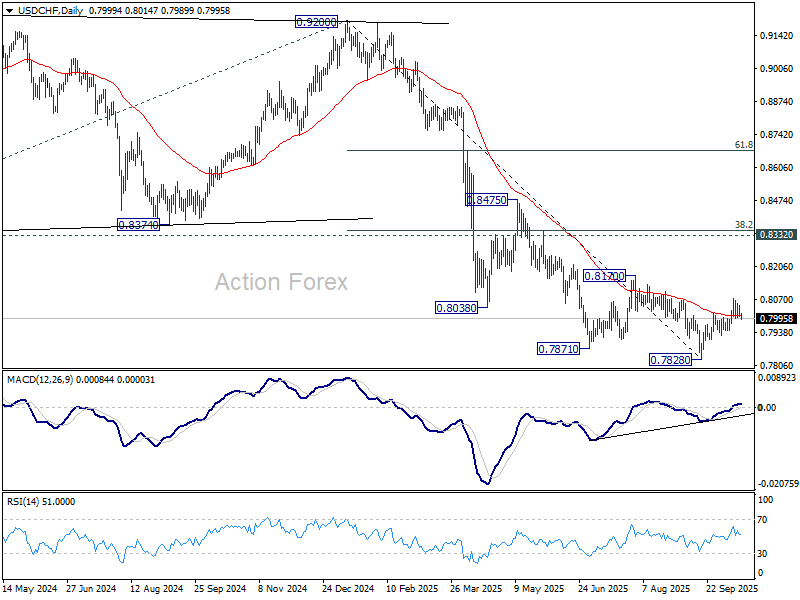

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7993; (P) 0.8021; (R1) 0.8040; More…

Intraday bias in USD/CHF remains neutral for consolidations below 0.8075. Price actions from 0.7828 are currently seen as correcting whole fall from 0.9200. Above 0.8075 will target 0.8170 resistance next. On the downside, though, break of 0.7944 support will bring retest of 0.7828 low instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

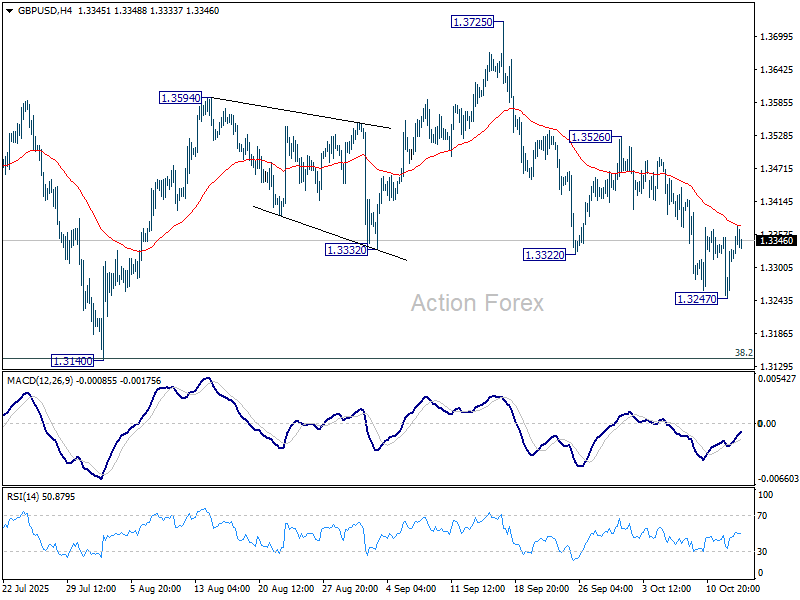

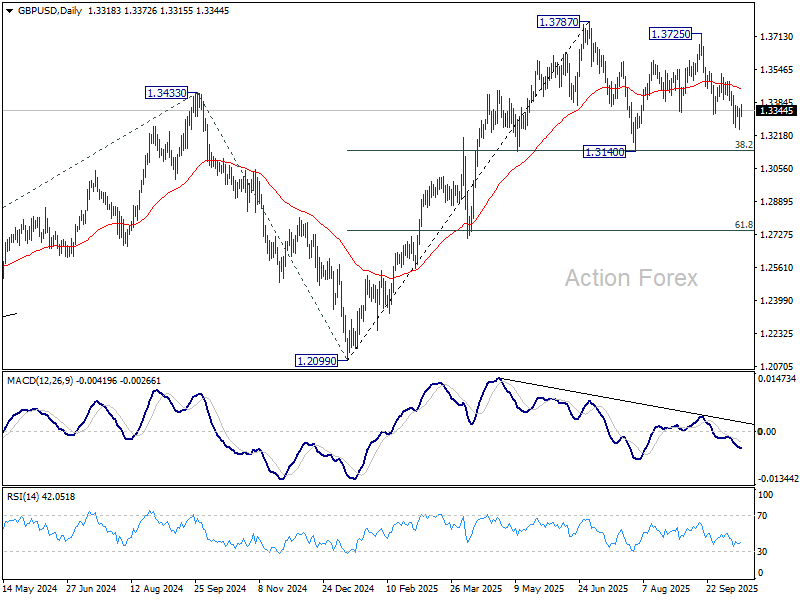

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3262; (P) 1.3307; (R1) 1.3366; More...

Intraday bias in GBP/USD stays neutral for the moment. On the downside, below 1.3247 will resume the fall from 1.3725 to 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected from there to complete the corrective pattern from 1.3787. On the upside, break of 1.3526 will bring stronger rally back to 1.3725/87 resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3173) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

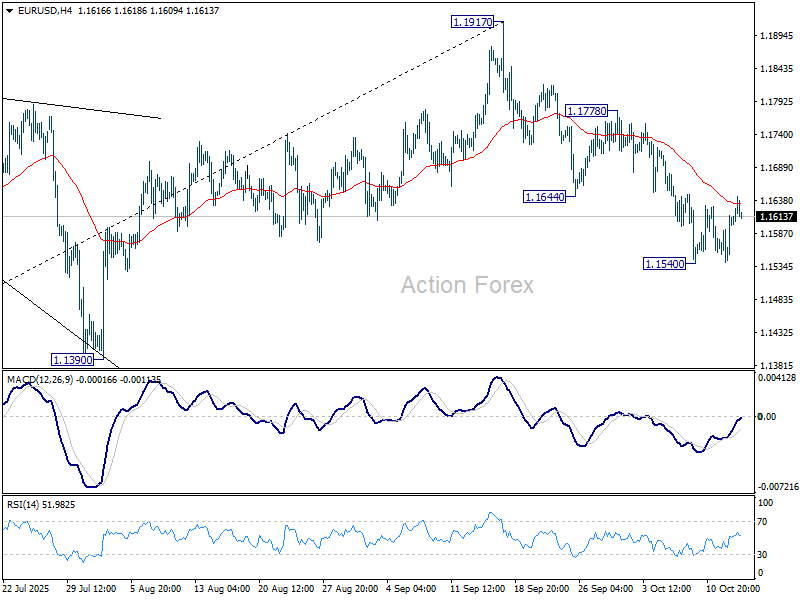

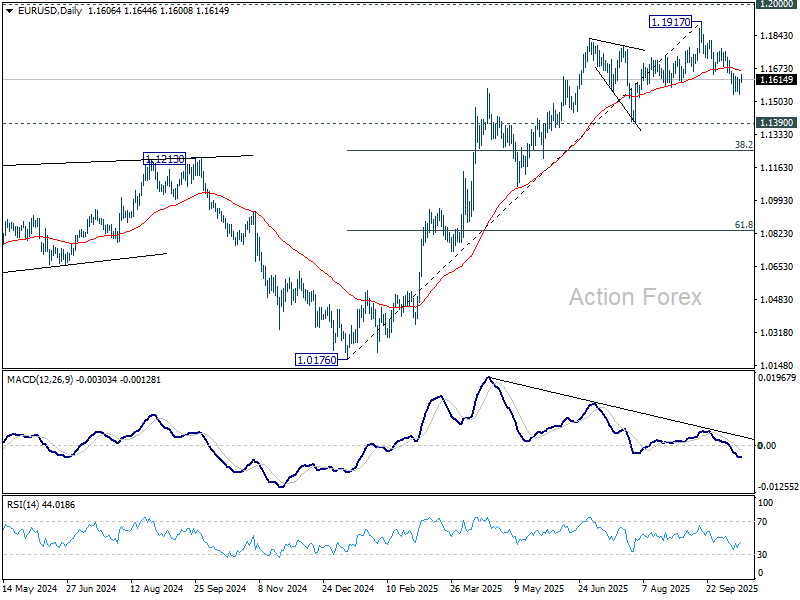

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1562; (P) 1.1588; (R1) 1.1634; More…

EUR/USD recovers mildly today as consolidations continue. Intraday bias remains neutral first. Deeper decline is expected as long as 1.1778 resistance holds. On the downside, break of 1.1540 will resume the fall from 1.1917 to 1.1390 , or further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1274) holds, the up trend from 0.9534 (2022 low) is still extended to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

Markets Calm as U.S.–China Trade Tensions Simmer, France’s Political Reprieve Lifts Sentiment

Global markets traded with a steady and cautious tone today, as investors balanced persistent U.S.–China trade tensions with signs of easing political risk in Europe.

Despite the looming November 1 deadline for Washington’s threatened 100% tariffs on Chinese imports, traders appeared hopeful for de-escalation, judging that both sides have incentives to avoid a severe disruption before year-end. Volatility has eased slightly after a turbulent start to the week, reflecting a shift toward defensive but stable positioning. Still, rhetoric from U.S. officials remains uncompromising. Treasury Secretary Scott Bessent told CNBC that the administration would not alter its negotiating stance toward Beijing, regardless of market swings.

In Europe, however, a measure of political stability returned after a tense week in Paris. French Prime Minister Sébastien Lecornu, reinstated after his brief resignation, announced that the government would suspend President Emmanuel Macron’s pension reform—the signature measure to raise the retirement age from 62 to 64—until January 2028. The decision represents a major concession aimed at restoring unity and calming public discontent.

Lecornu also promised not to bypass parliament on the 2026 budget, in a bid to win Socialist Party support ahead of Thursday’s no-confidence votes. With this compromise, markets now see the government’s survival as likely. The prospect that France’s cost-cutting budget will pass has helped revive investor confidence.

In currencies, Aussie continues to outperform, followed by Dollar and Euro. Loonie remains the weakest for the week, trailed by Yen and Swiss Franc. Sterling and Kiwi are trading mid-pack.

In Europe, at the time of writing, FTSE is down -0.41%. DAX is down -0.11%. CAC is up 2.22%. UK 10-year yield is down -0.036 at 4.553. Germany 10-year yield is down -0.024 at 2.587. Earlier in Asia, Nikkei rose 1.76%. Hong Kong HSI rose 1.84%. China Shanghai SSE rose 1.22%. Singapore Strait Times rose 0.32%. Japan 10-year JGB yield fell -0.007 to 1.656.

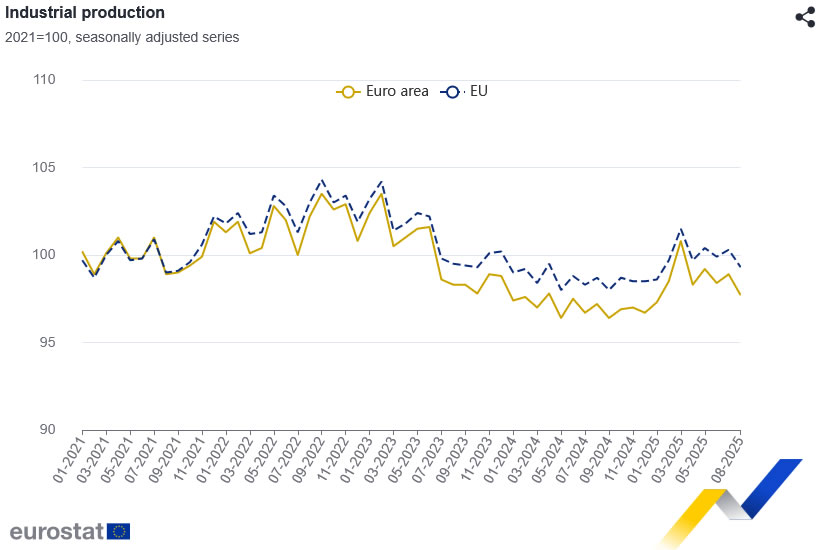

Eurozone industrial output drops -1.2% in August, Germany down -5.2%

Eurozone industrial production fell -1.2% mom in August, a smaller decline than the expected -1.8%. The data from Eurostat showed broad-based declines across key sectors, with capital goods output down -2.2%, durable consumer goods down -1.6%, energy production falling -0.6%, and intermediate goods slipping -0.2%. Only non-durable consumer goods managed a slight gain of 0.1%,.

Across the European Union as a whole, industrial output fell -1.0% mom. The regional breakdown showed significant divergence among member states: Germany, the bloc’s industrial powerhouse, suffered a sharp -5.2% decline, followed by Greece (-4.5%) and Austria (-3.1%), reflecting ongoing weakness in Europe’s core. Meanwhile, Ireland (+9.8%), Luxembourg (+4.8%), and Sweden (+3.6%) recorded the strongest gains.

RBA’s Hunter: Economy holding up, inflation still persistent in some areas

RBA Assistant Governor Sarah Hunter said in a speech on Tuesday that recent data suggest the Australian economy has been performing slightly stronger than expected, reinforcing the Bank’s decision to keep the cash rate unchanged at 3.60% at its September meeting. She noted that the RBA continues to see signs that “private demand is recovering,” “inflation may be persistent in some areas,” and that labor market conditions remain “stable.”

Hunter highlighted that GDP grew 1.8% over the year to the June quarter. “If anything, outcomes have been a little stronger than those expected in the August SMP,” she said, citing resilient private spending and steady employment as evidence that the economy remains on firmer footing than previously anticipated.

She also pointed to high-frequency indicators showing that underlying inflation in the September quarter is likely to be stronger than anticipated, suggesting that economic and labor market conditions remain “a bit tighter than we had assessed.” However, she acknowledged that employment growth has slowed "slightly" more than expected, while "elevated" global uncertainty continues to cloud the outlook.

Hunter concluded that the RBA will “continually reassess” its view on the economy and adjust policy as appropriate.

China’s CPI still negative at -0.3% in September as food prices drag

China’s consumer inflation remained in negative territory in September, highlighting continued weakness in domestic demand even as underlying price pressures showed tentative signs of improvement. Headline CPI rose from –0.4% yoy to –0.3% yoy, missing expectations of –0.2% yoy.

The National Bureau of Statistics said lower food and energy prices were the main contributors to the decline, with food prices down -4.4% yoy and consumer goods prices falling -0.8% yoy, partly offset by a 0.6% yoy increase in service prices.

However, the data also showed hints of stabilization beneath the surface. Core CPI, which excludes food and energy, rose 1.0% yoy from a year earlier, its highest level since February 2024, suggesting that domestic price momentum is slowly recovering in service sectors and other non-food categories.

Meanwhile, factory-gate prices continued to contract, with PPI rising from –2.9% yoy to –2.3% yoy, in line with expectations. This marks the 36th consecutive month of producer deflation, underscoring persistent cost pressures in manufacturing. NBS statistician Dong Lijuan said recent capacity management efforts in several industries have helped narrow the pace of decline, noting that market competition has improved as industrial supply and demand slowly rebalance.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1562; (P) 1.1588; (R1) 1.1634; More…

EUR/USD recovers mildly today as consolidations continue. Intraday bias remains neutral first. Deeper decline is expected as long as 1.1778 resistance holds. On the downside, break of 1.1540 will resume the fall from 1.1917 to 1.1390 , or further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1274) holds, the up trend from 0.9534 (2022 low) is still extended to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

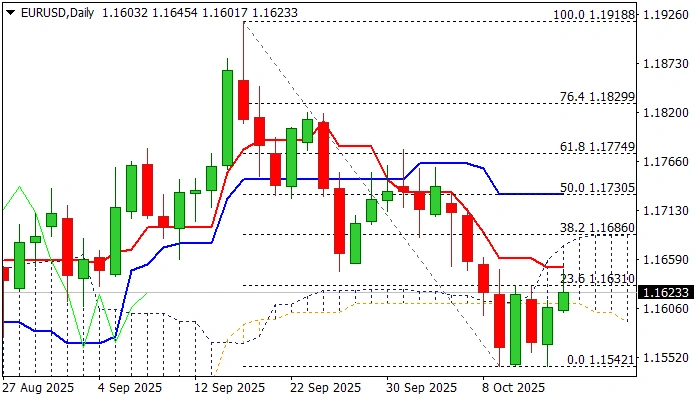

EUR/USD: Fresh Recovery Needs to Close Above Daily Cloud to Brighten Near-Term Outlook

The Euro edged higher on Wednesday morning, underpinned by weaker dollar on the latest remarks from Fed chief Powell which markets saw as more dovish and contributing to strong expectations for two rate cuts by the end of the year.

Fresh gains penetrated daily cloud (spanned between 1.1610 and 1.1686) and attempt to break above recent congestion (top lays at 1.1650 and is reinforced by daily Tenkan-sen), which acts as solid resistance and caps recovery so far.

Break of 1.1650 is seen as minimum requirement to keep recovery in play, with lift above daily cloud top (1.1680. also Fibo 38.2% of 1.1918/1.1542) to confirm signal and open way for further gains towards 1.1730 (daily Kijun-sen / 50% retracement) and 1.1774 (Fibo 61.8% / Oct 1 lower top) in extension.

However, predominantly bearish structure of daily technical studies warns of potential recovery stall, with slight bullish bias expected while the price stays above cloud base, but fresh negative signal to be expected in case on repeated daily close below daily cloud.

Res: 1.1650; 1.1686; 1.1700; 1.1730.

Sup: 1.1610; 1.1596; 1.1574; 1.1542.

Gold Price Falls from Above $4,200

The XAU/USD chart shows that gold recently climbed above the $4,200 mark for the first time. The upward momentum has been supported by the ongoing US government shutdown, central bank demand (with reports highlighting a sharp rise in reserves at the Reserve Bank of India), and market focus on US–China trade developments.

According to Trading Economics, on Tuesday President Donald Trump accused China of “economically hostile” behaviour, citing a halt in soybean imports, and warned of potential retaliatory measures.

After an 8% gain since the start of October, the market appears overbought, as reflected by the RSI, creating vulnerability to a correction. Today’s sharp drop from record levels (highlighted by the red arrow) may be seen in this context, yet bullish positions remain solid for several reasons.

Analysing gold price action (highlighted with bold lines), we can identify a rising channel that has remained relevant since late September. Signs of strong demand include:

→ persistent moves towards the channel’s upper boundary;

→ a steeper growth channel forming since 10 October;

→ the local $4,155 level shifting from resistance to support.

It is also notable that previous bearish attempts failed — each short-term plunge was followed by a strong rebound. Today’s correction could similarly precede further gains in gold.

Key levels to watch:

→ Psychological resistance at $4,250;

→ Boundaries of the orange channel and the blue median line.

In summary, the gold market currently appears extremely bullish, and it would likely take extraordinary events to reverse this pronounced trend.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

BTC/USD Analysis: Volatility Eases, But What’s Next?

In recent days, the cryptocurrency market has experienced extreme volatility:

A→B: Bitcoin surged sharply, partly driven by concerns around the US government shutdown, forming a historic peak above $125k.

B→C: Panic selling followed, triggered by Trump’s statements on the possible introduction of 100% tariffs on Chinese goods.

Price swings for both moves exceeded 15%. Following this “pump and dump,” crypto volatility appears to be easing, with BTC/USD consolidating between $110k and $115k.

What could happen next?

Technical Analysis of Bitcoin

Demand-side perspective:

→ BTC/USD is maintaining a long-term upward trend, highlighted by the blue channel.

→ The lower boundary (indicated by the arrow) provides solid support.

Supply-side perspective:

→ Examining price behaviour, such as the reversal from peak B, allows the construction of a descending channel (shown in red).

→ October’s record high may act as a bull trap if the August peak fails to break convincingly.

The long-term trend is supported by inflows into crypto-related ETFs, favouring the bulls. However, the A→B→C sequence reflects the characteristics of a Bearish Engulfing pattern.

As Bitcoin oscillates between the red median and the lower blue boundary, the key question remains: what will be the next move?

Assuming:

→ the market is still under the emotional impact of last Friday’s reactive sell-off;

→ the initiative may lie with the sellers.

If rebounds from the lower blue line prove weak, a bearish break could occur, potentially pushing BTC/USD down to the lower red boundary around the psychological $100k mark.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Eurozone industrial output drops -1.2% in August, Germany down -5.2%

Eurozone industrial production fell -1.2% mom in August, a smaller decline than the expected -1.8%. The data from Eurostat showed broad-based declines across key sectors, with capital goods output down -2.2%, durable consumer goods down -1.6%, energy production falling -0.6%, and intermediate goods slipping -0.2%. Only non-durable consumer goods managed a slight gain of 0.1%,.

Across the European Union as a whole, industrial output fell -1.0% mom. The regional breakdown showed significant divergence among member states: Germany, the bloc’s industrial powerhouse, suffered a sharp -5.2% decline, followed by Greece (-4.5%) and Austria (-3.1%), reflecting ongoing weakness in Europe’s core. Meanwhile, Ireland (+9.8%), Luxembourg (+4.8%), and Sweden (+3.6%) recorded the strongest gains.