Sample Category Title

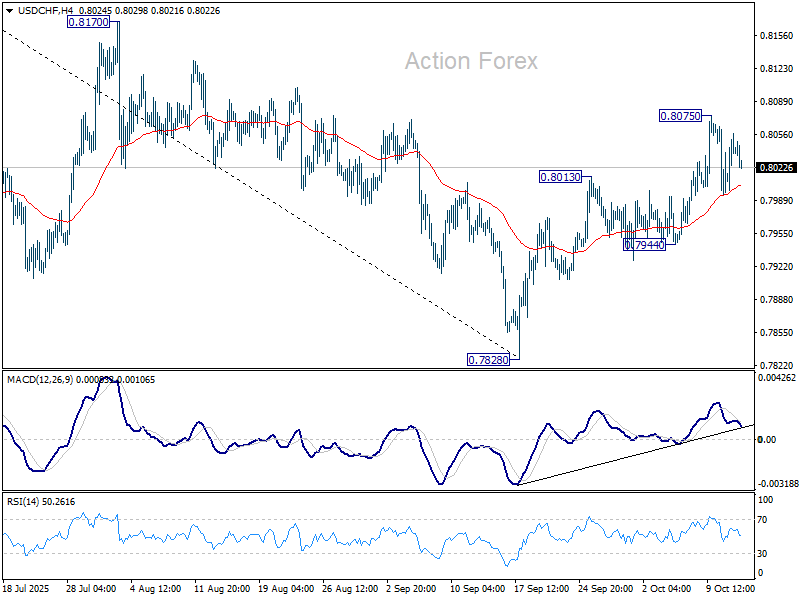

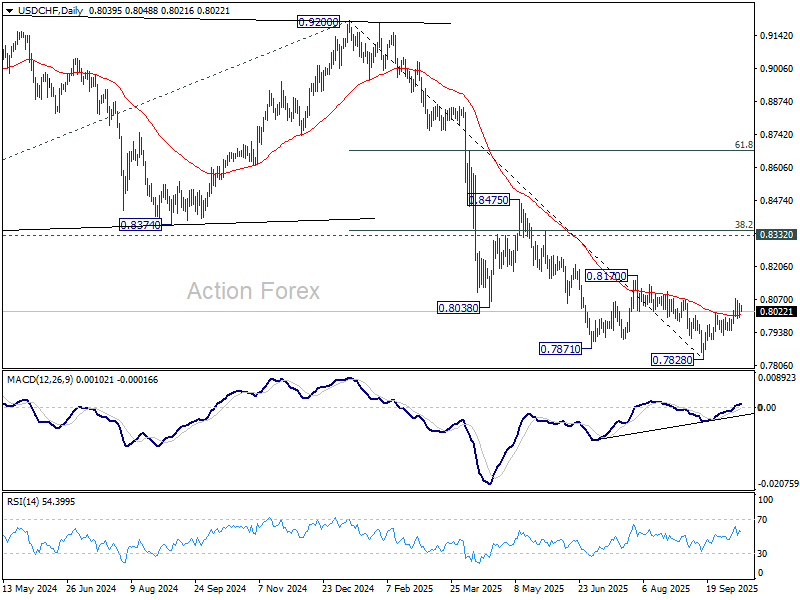

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8009; (P) 0.8033; (R1) 0.8067; More…

Intraday bias in USD/CHF remains neutral and more consolidations could be seen below 0.8075. Price actions from 0.7828 are currently seen as correcting whole fall from 0.9200. Above 0.8075 will target 0.8170 resistance next. On the downside, though, break of 0.7944 support will bring retest of 0.7828 low instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

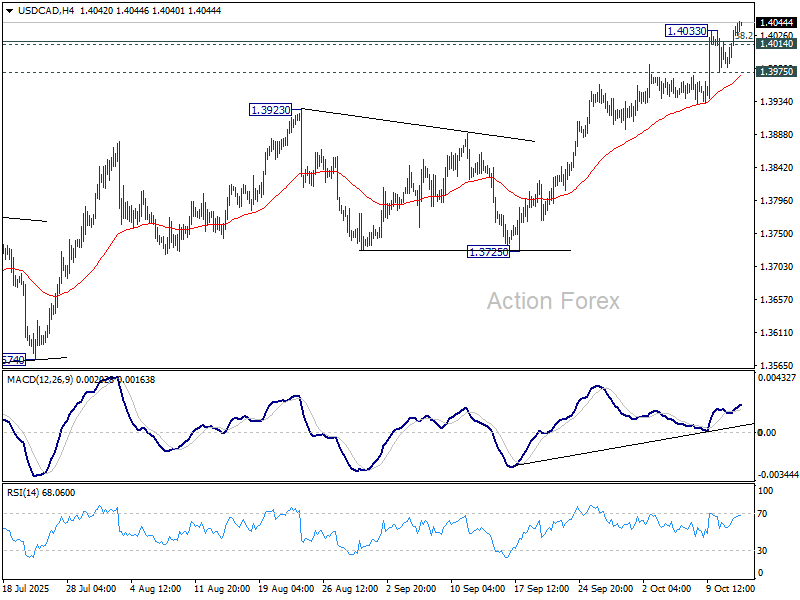

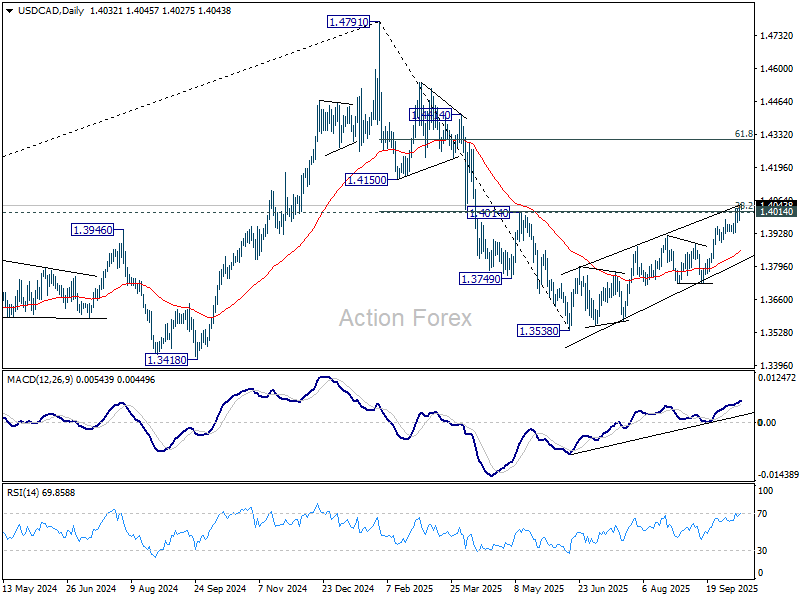

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4002; (P) 1.4021; (R1) 1.4059; More...

USD/CAD's rally resumed by breaking through 1.4033 and intraday bias is back on the upside. Sustained trading above 1.4014/7 will suggest that USD/CAD is already reversing the whole fall from 1.4719, and target 61.8% retracement at 1.4312. On the downside, below 1.3975 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. However sustained trading above 1.4014 will suggest that it's more likely just a correction, and the larger up trend would be in favor to resume through 1.4791 at a later stage.

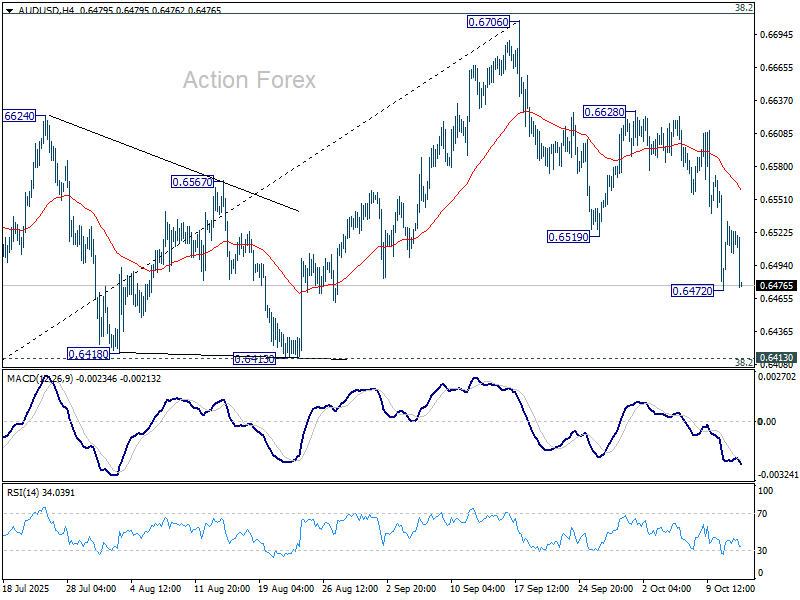

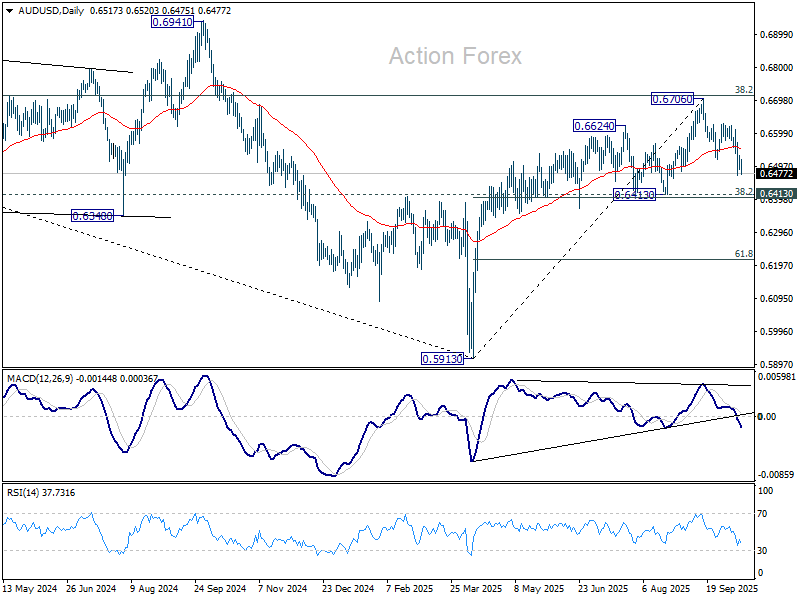

AUD/USD Daily Report

Daily Pivots: (S1) 0.6492; (P) 0.6513; (R1) 0.6534; More...

AUD/USD falls sharply today but stays above 0.6472 temporary low. Intraday bias remains neutral first and more consolidations could be seen. Still, risk will remain on the downside as long as 0.6628 resistance holds. Current development suggests rejection by 0.6713 fibonacci resistance. Below 0.6472 will resume the fall from 0.6706 to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

Nikkei Slumps as Investors Question Full Return of Abenomics Under Takaichi, Commodity Currencies Sink

Sentiment soured sharply in Asian markets, led by a steep selloff in Japan where the Nikkei reversed early gains to fall more than 3%. The downturn reflected a mix of political uncertainty in Tokyo and renewed caution over U.S.–China trade tensions. After months of strong gains, Japanese equities appear to have reached a point where investors are pausing to reassess the outlook amid rising volatility and shifting policy expectations.

The source of anxiety lies partly in Japan’s unfolding leadership transition. While LDP leader Sanae Takaichi remains widely expected to become Japan’s next prime minister, her path to confirmation has been complicated by the breakup with coalition partner Komeito. The split has introduced a small but symbolic risk that an opposition figure could be elected by parliament later this month — a scenario still viewed as unlikely but unsettling enough to spark caution among investors.

Adding to the uncertainty, Finance Minister Katsunobu Kato emphasized today that “inflation, rather than deflation, has become a challenge for us now.” He emphasized the need for policies suited to this new environment, implying that Japan is unlikely to return to a full-fledged “Abenomics” reflationary stance even if Takaichi takes office. The remarks reinforce expectations that fiscal and monetary policies may remain more balanced, tempering hopes for aggressive stimulus measures that had previously fueled market optimism.

Beyond domestic politics, escalating U.S.–China trade tensions also weighed on investor sentiment. With Washington and Beijing trading fresh barbs over tariffs and rare earth restrictions, Japanese exporters face renewed headwinds. After a strong rally since April, profit-taking was perhaps overdue, and today’s selloff appears to reflect a broader correction rather than a fundamental shift in outlook.

Overall in the currency markets, Aussie led declines, followed by Kiwi and Loonie, all under pressure from the deterioration in sentiment and weaker equities. In contrast, the safe-haven trio, Yen, Swiss Franc and Euro, gained. Dollar and British Pound held in mid-range.

In Asia, at the time of writing, Nikkei is down -2.68%. Hong Kong HSI is down -0.19%. China Shanghai SSE is up 0.21%. Singapore Strait Times is down -0.22%. Japan 10-year JGB yield is down -0.00at 1.663. Overnight, DOW rose 1.29%. S&P 500 rose 1.56%. NASDAQ rose 2.21%.

RBA minutes signal caution as board flags risk of hotter Q3 inflation

RBA’s September meeting minutes confirmed a steady hand on policy, with members concluding there was “no need for an immediate reduction” in the cash rate. The Board agreed that the economic data and forecasts since August supported maintaining the current level of restrictiveness, while emphasizing that decisions will remain “cautious and data dependent.”

Discussions focused heavily on inflation risks, particularly after stronger readings in the monthly CPI indicators for July and August. While acknowledging that these data are partial and volatile, members noted that upside surprises in market services and housing costs suggest the September quarter CPI could come in higher than expected in August forecasts.

The minutes revealed growing concern that if this pattern continues, the Bank’s assumptions about the balance between aggregate demand and supply could be too optimistic. Members also referenced lessons from abroad, where services inflation has proven stubbornly elevated, as a warning for domestic policy calibration.

Still, the Board recognized that risks remain "two-sided". On the upside, consumption could recover faster than assumed, or capacity pressures could prove stronger. On the downside, members highlighted the drag from weak consumer sentiment, slower employment growth, and subdued wage indicators.

The balance of views suggests the RBA will tread carefully in coming months, awaiting confirmation from the full Q3 inflation report before deciding whether further policy easing remains justified at the November meeting.

New Philly Fed chief Paulson backs gradual easing toward neutral policy

New Philadelphia Fed President Anna Paulson used her debut speech to call for a balanced approach to monetary policy as the economy navigates rising labor market risks and uncertain inflation dynamics.

She said policy should move toward a “more neutral stance,” stressing that the Fed must weigh both sides of its mandate. While she noted that the job market remains solid overall, she warned that conditions are “moving in the wrong direction” and that risks are “noticeably” increasing.

Paulson indicated she supports a measured pace of rate cuts consistent with the Fed’s latest projections, which outlined a quarter-point reduction last month and an additional 50 basis points of easing before the end of 2025, followed by further cuts in subsequent years.

On inflation, Paulson acknowledged that the recent tariff hikes could lift prices modestly, but said she does not expect those effects to persist. Still, she cautioned against rushing into deeper rate reductions given uncertainty over where the neutral rate truly lies.

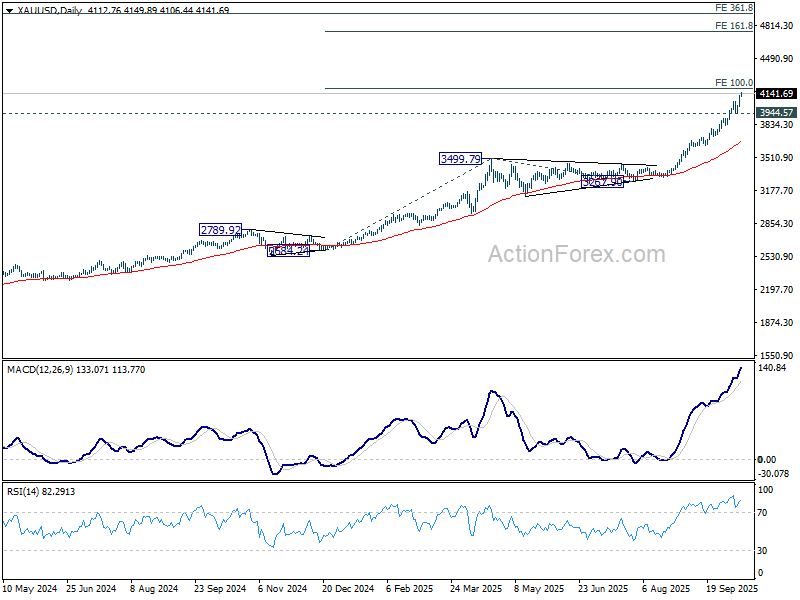

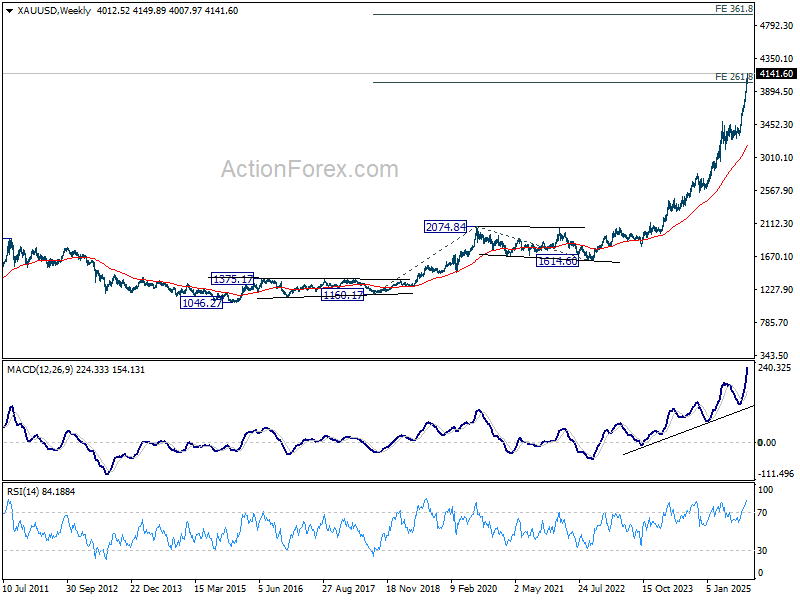

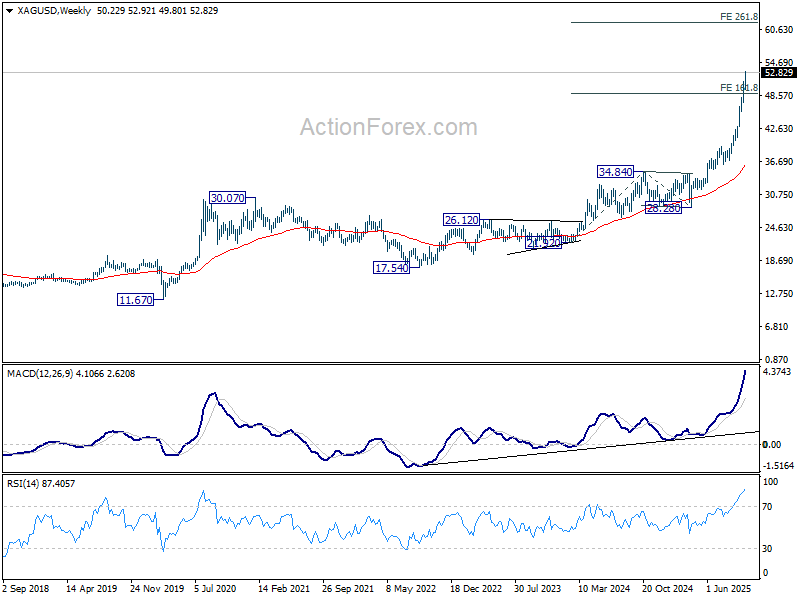

Gold and Silver shatter key barriers as bull run accelerates - 5000 and 60 next

The precious metals rally showed no sign of fatigue, with Gold surging beyond 4,000 and Silver clearing 50 in a powerful continuation of their uptrend. Neither milestone proved a deterrent, as safe-haven demand strengthened amid renewed global uncertainty. Although initial market reactions to the latest U.S.–China trade tensions were subdued, investors have steadily rotated back into metals, betting that geopolitical instability will sustain demand well into 2026.

The rally has now reached a stage where institutional forecasts are catching up to price reality. On Monday, Bank of America became the first major institution to lift its long-term targets, projecting Gold at 5,000 per ounce in 2026 and Silver at 65.

Silver remains the outperformer, up about 80% year-to-date, compared with a 55% rise in gold. However, the surge has not come without risks. Some analysts caution that as liquidity improves and industrial demand fluctuates, volatility could increase in the near term. The latest spike has also been fueled by a temporary shortage in physical supply, which is expected to ease soon.

Technically, Gold’s next immediate focus lies at 100% projection of 2,584.24 to 3,499.79 from 3,267.90 at 4,183.45. Resistance could emerge there, prompting some profit-taking on first test. Break below 3,944.57 support would signal short-term topping and consolidation. However, sustained strength above 4,183.45 would pave the way toward 161.8% projection at 4,749.25 next.

In the broader view, now that 261.8% projection of 1,160.17 to 2,074.84 from 1,614.60 at 4,009.21 is cleared, Gold could be heading towards 361.8% projection at 4.923.87, which is close to 5000 psychological level. The technical setup aligns closely with the latest upward revisions from institutional forecasts.

For Silver, near term outlook will stay bullish as long as 48.35 support holds. Next target is 161.8% projection of 28.28 to 39.49 from 36.93 at 55.06. Firm break there will target 200% projection at 59.35, which is close to 60 psychological level.

In the bigger picture, the up trend remains in acceleration phase, and could further stretch to 261.8% projection of 21.92 to 34.84 from 28.28 at 62.10 in the medium term.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6492; (P) 0.6513; (R1) 0.6534; More...

AUD/USD falls sharply today but stays above 0.6472 temporary low. Intraday bias remains neutral first and more consolidations could be seen. Still, risk will remain on the downside as long as 0.6628 resistance holds. Current development suggests rejection by 0.6713 fibonacci resistance. Below 0.6472 will resume the fall from 0.6706 to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

Gold and Silver shatter key barriers as bull run accelerates – 5000 and 60 next

The precious metals rally showed no sign of fatigue, with Gold surging beyond 4,000 and Silver clearing 50 in a powerful continuation of their uptrend. Neither milestone proved a deterrent, as safe-haven demand strengthened amid renewed global uncertainty. Although initial market reactions to the latest U.S.–China trade tensions were subdued, investors have steadily rotated back into metals, betting that geopolitical instability will sustain demand well into 2026.

The rally has now reached a stage where institutional forecasts are catching up to price reality. On Monday, Bank of America became the first major institution to lift its long-term targets, projecting Gold at 5,000 per ounce in 2026 and Silver at 65.

Silver remains the outperformer, up about 80% year-to-date, compared with a 55% rise in gold. However, the surge has not come without risks. Some analysts caution that as liquidity improves and industrial demand fluctuates, volatility could increase in the near term. The latest spike has also been fueled by a temporary shortage in physical supply, which is expected to ease soon.

Technically, Gold’s next immediate focus lies at 100% projection of 2,584.24 to 3,499.79 from 3,267.90 at 4,183.45. Resistance could emerge there, prompting some profit-taking on first test. Break below 3,944.57 support would signal short-term topping and consolidation. However, sustained strength above 4,183.45 would pave the way toward 161.8% projection at 4,749.25 next.

In the broader view, now that 261.8% projection of 1,160.17 to 2,074.84 from 1,614.60 at 4,009.21 is cleared, Gold could be heading towards 361.8% projection at 4.923.87, which is close to 5000 psychological level. The technical setup aligns closely with the latest upward revisions from institutional forecasts.

For Silver, near term outlook will stay bullish as long as 48.35 support holds. Next target is 161.8% projection of 28.28 to 39.49 from 36.93 at 55.06. Firm break there will target 200% projection at 59.35, which is close to 60 psychological level.

In the bigger picture, the up trend remains in acceleration phase, and could further stretch to 261.8% projection of 21.92 to 34.84 from 28.28 at 62.10 in the medium term.

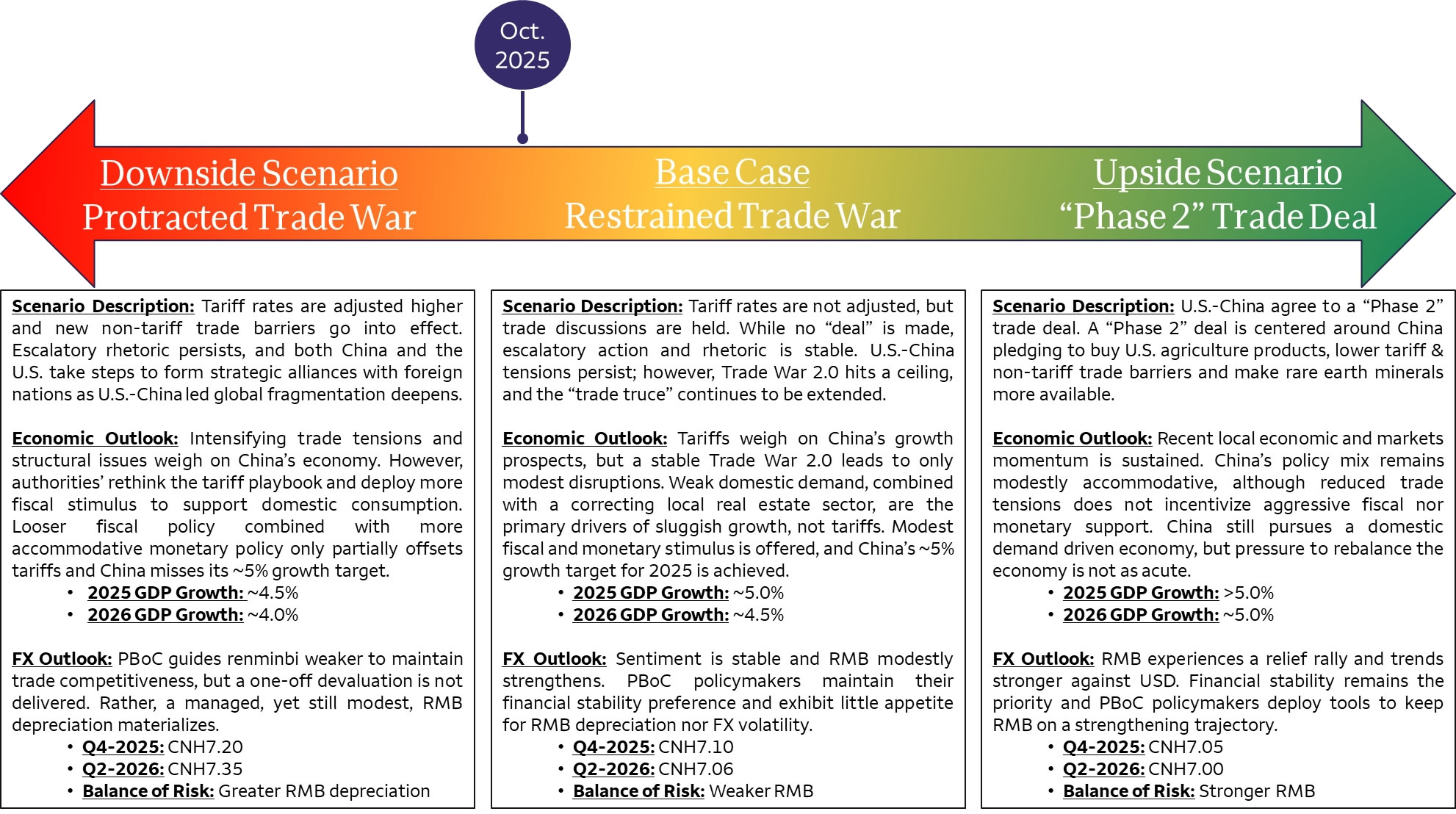

U.S.-China Trade War 2.0 Scenario Analysis Update

Summary

U.S.-China trade tensions are again front and center following the developments of late last week. China's plan to impose strict export controls, especially on rare earth minerals, were matched by new tariff threats from President Trump. While rhetoric eased this past weekend, a November 1 target date for the imposition of Chinese export restrictions and higher U.S. imposed tariffs elevate the probability of the U.S. and China slipping into a downside trade war scenario. In the context of U.S.-China tensions, mid-October to November 1 is a lot of time with many potential twists and turns along the way. In that sense, we updated our U.S.-China Trade War 2.0 scenarios for how China's economy and currency could perform should relations deteriorate, improve, or hold steady. For now, we believe the U.S. and China will remain in our "restrained trade war" base case scenario, although risks are tilted toward our downside scenario materializing.

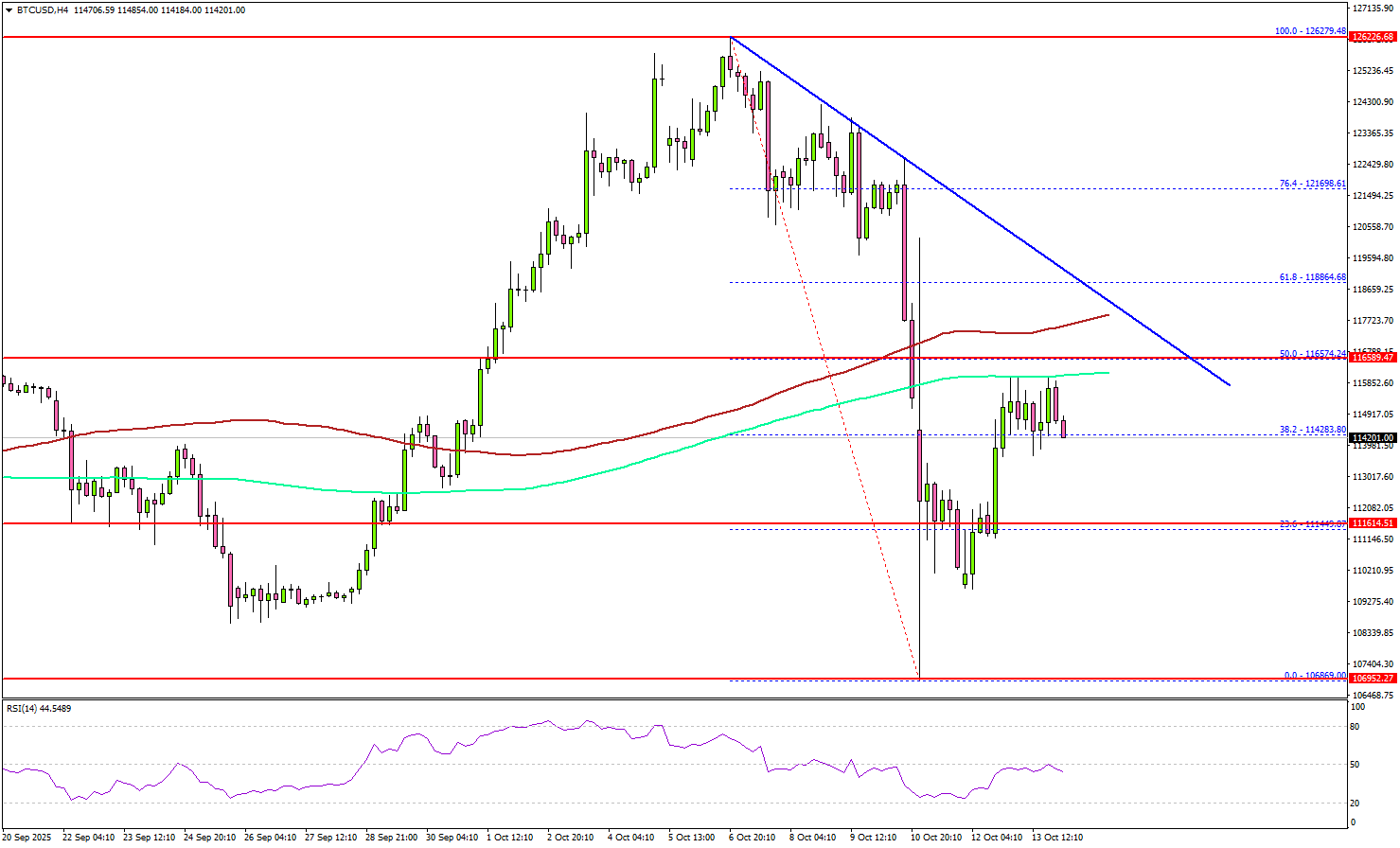

Bitcoin Rebounds After Selloff – But Bulls Struggle To Hold Onto Gains

Key Highlights

- Bitcoin started a recovery wave above $112,000 after a major crash.

- BTC/USD is still below a key bearish trend line with resistance at $117,800 on the 4-hour chart.

- Ethereum also started a decent increase above $4,000.

- XRP price is back above $2.20 but faces hurdles near $2.650.

Bitcoin Price Technical Analysis

Bitcoin price started a major decline below $115,000 against the US Dollar. BTC dived below $112,000 and $110,000 before the bulls took a stand.

Looking at the 4-hour chart, the price traded as low as $106,869 on TitanFX and recently started a steady recovery wave. The price climbed above the $112,000 resistance zone. There was a move above the 38.2% Fib retracement level of the downward move from the $126,279 swing high to the $106,869 low.

However, the price is still below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). There is also a key bearish trend line forming with resistance at $117,800.

Immediate support sits at $112,500. A downside break below $112,500 might start another decline. The next major support is $111,600. Any more losses might call for an extended decline toward the $108,000 support zone.

On the upside, the price now faces resistance near the $116,000 level and the 200 simple moving average (green, 4-hour). The main hurdle is now forming near $117,500. A successful close above $117,500 might start another steady increase. In the stated case, the price may perhaps rise toward the $118,800 level. Any more gains might call for a test of $120,000.

Looking at Ethereum, the price was able to follow Bitcoin and climbed above the $4,000 resistance region.

Today’s Key Economic Releases

- Fed's Chair Powell speech.

- BoE's Governor Bailey speech.

RBA minutes signal caution as board flags risk of hotter Q3 inflation

RBA’s September meeting minutes confirmed a steady hand on policy, with members concluding there was “no need for an immediate reduction” in the cash rate. The Board agreed that the economic data and forecasts since August supported maintaining the current level of restrictiveness, while emphasizing that decisions will remain “cautious and data dependent.”

Discussions focused heavily on inflation risks, particularly after stronger readings in the monthly CPI indicators for July and August. While acknowledging that these data are partial and volatile, members noted that upside surprises in market services and housing costs suggest the September quarter CPI could come in higher than expected in August forecasts.

The minutes revealed growing concern that if this pattern continues, the Bank’s assumptions about the balance between aggregate demand and supply could be too optimistic. Members also referenced lessons from abroad, where services inflation has proven stubbornly elevated, as a warning for domestic policy calibration.

Still, the Board recognized that risks remain "two-sided". On the upside, consumption could recover faster than assumed, or capacity pressures could prove stronger. On the downside, members highlighted the drag from weak consumer sentiment, slower employment growth, and subdued wage indicators.

The balance of views suggests the RBA will tread carefully in coming months, awaiting confirmation from the full Q3 inflation report before deciding whether further policy easing remains justified at the November meeting.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Hybrid – 29 and 30 September 2025

Members participating

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor and Deputy Chair), Marnie Baker AM, Renée Fry-McKibbin, Ian Harper AO, Carolyn Hewson AO, Iain Ross AO, Alison Watkins AM, Jenny Wilkinson PSM

Others participating

Sarah Hunter (Assistant Governor, Economic), Brad Jones (Assistant Governor, Financial System), Christopher Kent (Assistant Governor, Financial Markets)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Meredith Beechey Osterholm (Head, Monetary Policy Strategy), Andrea Brischetto (Head, Financial Stability Department), Sally Cray (Chief Communications Officer), David Jacobs (Head, Domestic Markets Department), Michael Plumb (Head, Economic Analysis Department), Penelope Smith (Head, International Department)

Financial conditions

Members commenced their discussion of financial conditions by considering policy settings at other advanced economy central banks. The US Federal Reserve (Fed), the Bank of Canada and the Reserve Bank of New Zealand (RBNZ) had all reduced their policy rates further since the previous meeting, in large part because of softening labour markets. In the United States, the softening labour market had led the Fed to ease policy, notwithstanding some evidence of higher tariffs beginning to be passed through to consumer prices. Market participants anticipated that the Fed would ease policy further in 2026. Additional easing by the RBNZ was also anticipated. By contrast, expectations for the path of the policy rate in the United Kingdom, euro area and Japan had edged higher since the previous meeting. For the United Kingdom, this partly reflected growing concern about the persistence of inflation.

Sovereign bond yields in the United States had declined since the previous meeting, reflecting growing market expectations for additional policy easing. However, the yield curve had also steepened. Members noted that there were few signs that this reflected investor concern about external pressure on the Fed. Most notably, measures of long-term inflation expectations and term premia had been stable, though members noted that the rapid rise in the gold price and a depreciation of the US dollar were perhaps indicative of some concern about the pressure on the Fed. Members also discussed the pronounced rise in 30-year bond yields in other countries, including the United Kingdom, Germany, France and Japan. These moves had occurred amid concerns about long-term public debt sustainability and political uncertainty about how those concerns might be addressed.

Members noted that conditions in global corporate funding markets remained buoyant. Debt and equity funding were both readily available on favourable terms. Equity prices in many advanced economies had reached new highs. In part, that reflected strong US company earnings but equity risk premia were also near multi-decade lows (as were corporate bond spreads). Members noted that low risk premia continued to suggest that market participants were placing little weight on the potential for adverse outcomes from trade and geopolitical risks.

The Australian dollar had appreciated slightly since the previous meeting. This had been supported by widening yield differentials between Australia and other advanced economies. In real terms, the Australian dollar trade-weighted index was close to estimates of the equilibrium level implied by its long-run historical relationship with the forecast terms of trade and real yield differentials. Members noted that this suggested the slight appreciation of the Australian dollar was not causing financial conditions to be any tighter than already implied by the level of interest rates.

Domestically, members noted that the Board’s decision to lower the cash rate in August had eased financial conditions. Reductions in the cash rate had been passed onto bank funding costs and lending rates, and scheduled mortgage payments had declined. The transmission of monetary policy to financial conditions had been broadly in line with prior easing phases.

Members turned to consider their assessment of the overall level of restrictiveness in financial conditions. They noted that a range of indicators suggested that financial conditions had been clearly restrictive in 2024 but these now presented a less clear picture.

Members noted that the path for the cash rate implied by market pricing was well within the range of model-based estimates of the neutral cash rate. They agreed that the estimates from these models were imprecise and did not provide any direct guide to policy.

Australian equity risk premia and credit spreads remained close to multi-decade lows, as in other countries. Equity prices had been little changed since the previous meeting, partly reflecting mixed earnings results in Australia, but were still materially higher over the year. Growth in business credit had exceeded the rate of GDP growth, although measures of aggregate business leverage remained low by historical standards.

Growth in housing credit had picked up further, consistent with the easing in monetary policy since the start of the year. The pick-up had been driven by growth in lending to housing investors, which was above its post-2008 average; members noted that housing investors historically had been more responsive to declining interest rates than owner-occupiers. However, they also observed that, while overall household credit growth had picked up, household debt relative to household incomes had only just begun to stabilise following a long period of gradual decline.

Households’ mortgage payments, as a share of household disposable income, remained above their historical average. Members noted that the still-elevated level of extra mortgage payments – which were running ahead of the pace recorded in 2023 and 2024 – could suggest that households with a mortgage were still saving at a relatively high rate.

Members concluded their discussion of financial conditions by considering market participants’ expectations for the path of the cash rate. They observed that these expectations had moved higher since the previous meeting in response to some stronger-than-expected data for activity and inflation. Members noted that market participants had absorbed the Board’s prior communication that it would be guided by the incoming data and its evolving assessment of the outlook and risks when making decisions. No change in the cash rate was expected at the September meeting, according to both market pricing and economists’ expectations. Market pricing was for the cash rate to reach around 3¼ per cent by the middle of 2026, compared with 3 per cent at the time of the August meeting.

Economic conditions

Turning to economic conditions, members noted that GDP had increased by slightly more in the June quarter than the staff’s expectation in the August Statement on Monetary Policy. Growth had been led by a recovery in household consumption. Public demand had increased in the quarter but by less than expected, reflecting a decline in public investment. Members noted that these data provided further evidence that the anticipated shift in the composition of growth from the public to private sector was occurring.

Growth in household consumption in the June quarter had been stronger than expected. Members noted that this had been supported by some temporary factors (the impact on measured household consumption of unwinding electricity subsidies, end-of-financial-year promotions and a rebound from weather disruptions in Queensland and New South Wales in the March quarter). Moreover, the size of the increase in the June quarter and the fact that consumption had picked up across a wide range of categories over the preceding year suggested that the recovery in household consumption was likely to persist. This assessment was also supported by early indicators for the September quarter, including the ABS Household Spending Indicator for July and information from liaison. Members noted the role of the recovery in household disposable income in this pick-up. Real disposable income had risen strongly over the preceding year, supported by ongoing strength in employment, growth in real wages and the Stage 3 tax cuts. In per capita terms, real disposable income had been back above its pre-pandemic level since late 2024. Despite this, measures of consumer sentiment remained quite low. Members considered how best to interpret this weakness in consumer sentiment and the extent to which it reflected the persistent rise in the price level over prior years, noting that consumer sentiment had been low for some time in many economies.

Members considered the impact on the economy of the easing in monetary policy this year. There were signs that this was contributing to stronger housing market conditions. However, given the lags in policy transmission, it was too early to have discerned the expected effect on broader private sector activity. Past reductions in the cash rate would therefore provide further support for GDP growth in the year ahead, at least partly offsetting the diminishing impetus to growth from the Stage 3 tax cuts and growth in public demand.

Turning to the labour market, members assessed conditions to remain a little tight, though there was considerable uncertainty around this assessment. The unemployment rate was 4.2 per cent in August, unchanged from July. The underemployment rate had edged lower while other measures of labour underutilisation had been broadly stable. Business surveys and liaison suggested that availability of labour had been little changed. Half of the firms that mentioned the labour market in liaison described labour availability as tight.

Members discussed the signal to take from the slightly larger-than-expected easing in employment growth in August. While some easing in employment growth had been forecast in August as population growth slowed, the employment-to-population ratio and participation rate had also edged lower (but remained close to historical highs). Members noted that most indicators of labour demand had been broadly stable or eased only slightly, and that leading indicators (such as job advertisements and vacancies) continued to point to healthy labour demand in the near term. An easing in labour supply may also have played a part, if some individuals had become less inclined to participate in the workforce as their cost-of-living pressures became less acute.

Members also considered the evolving composition of employment growth. The bulk of employment growth over the first half of 2025 had been in the market sector, following strong growth in non-market sector employment in 2024. This was broadly consistent with the shifting driver of momentum in economic activity more generally. Such a shift, if it persisted, would be consistent with some slowing in overall employment growth (as had been forecast in the August Statement on Monetary Policy), given that the market sector is generally less labour intensive. Members also discussed variations in employment outcomes across industries and states.

Growth in the private sector wage price index had been broadly steady over preceding quarters (after adjusting for administered decisions). Members noted that preliminary information from liaison, together with some timely indicators of wages, pointed to a risk that private sector wages growth could ease a little faster than expected in the near term. However, it was too early to assess the implications of these indicators for future wages growth, and the staff continued to assess that a material moderation in quarterly wages growth was unlikely while labour market conditions remained a little tight. Members noted that growth in unit labour costs remained high, in part because labour productivity growth was still weak.

Turning to prices, recent data suggested that inflation in the September quarter may be higher than had been expected in the August Statement on Monetary Policy. The monthly CPI indicator for July and August, while partial and volatile, had pointed to stronger-than-expected outcomes in the September quarter. Most notably, outcomes for the new dwellings and market services inflation components – which contain important information for the quarterly outcome – had both been stronger than expected. Shifts in the timing of electricity rebates were also expected to contribute to stronger-than-expected headline inflation in the September quarter. More broadly, members observed that services inflation was proving surprisingly persistent in several other economies, which may hold lessons for Australia. Members noted that it would be important to see how all these developments are revealed in the September quarterly data and the implications they hold for their assessment of the supply capacity of the economy.

Turning to the global economy, members noted that risks remained heightened. Higher tariff rates imposed by the United States were now in effect for many economies, but there was still considerable uncertainty about their macroeconomic effects (given their scale and potential for further change as the United States continues negotiations with its three largest trading partners).

On the upside, global trade had remained at a high level, in part reflecting significant shifts in global trade patterns in response to the higher tariffs. GDP growth in Australia’s trading partners had also remained resilient and stronger than expected in the June quarter. Economic activity in the United States had been surprisingly robust, though employment growth had slowed over preceding months and GDP growth was expected to slow as well. Members noted that the slowing in US employment growth could, at least in part, reflect changes in US immigration policy and measures to reduce the number of federal government employees. Higher tariffs were also contributing a little to US inflation.

In China, growth in domestic demand had slowed by more than expected in July and August. The slowing had been particularly pronounced for fixed asset investment. Members noted that infrastructure and manufacturing investment had been affected by the fading impact of supportive policies announced in late 2024, adverse weather conditions, uncertainty over tariffs and a strengthening in authorities’ resolve to curb excess capacity. They also observed that the long-term slowdown in China’s real estate sector may have accelerated somewhat. Notwithstanding these developments, bulk commodity prices had increased slightly. Iron ore and coking coal prices had been supported by resilient underlying demand from Chinese steel mills. The staff’s assessment was still that any material slowing in activity in China would prompt incremental fiscal stimulus from the authorities to support growth.

Financial stability assessment

Members turned to considering the staff’s semi-annual assessment of financial stability risks. They noted that the main risks to financial stability in Australia came from abroad, and discussed ways that an international shock could spill over to the Australian economy and financial system. Domestically, credit growth had picked up, but lending standards had remained sound and household indebtedness had stabilised after a long period of gradual decline. The staff also assessed that the Australian financial system remains financially resilient and well placed to weather most shocks, including those emanating from abroad. Overall, therefore, members observed that there were no immediate implications for monetary policy arising from domestic financial stability considerations.

Turning to the considerations supporting this assessment, members discussed several vulnerabilities in the global financial system that stood out as having the potential to affect financial stability in Australia significantly. Concerns about fiscal sustainability had become more prominent in several advanced economies, including because of the absence of credible frameworks to constrain fiscal deficits over the medium term. Aggregate supply and demand imbalances in key sovereign debt markets also increased the risk of disruptions in financial markets in periods of stress; these have the potential to be compounded in the longer run if stablecoin issuance becomes systemically important. Longstanding vulnerabilities in China’s financial and property sectors have the potential to constrain long-run growth in China, even in the absence of a discrete shock to the financial system.

Members noted again that risk premia in global equity and credit markets had remained low, and sovereign bond term premia were only around long-term averages, despite these vulnerabilities and a backdrop of heightened geopolitical tensions. Members observed that any reassessment of the likelihood of key risks materialising, or of their potential consequences, could cause sharp adjustments in international financial markets. Highly leveraged trading strategies employed by hedge funds in fixed income markets, liquidity mismatches among open-ended fixed-income funds, concentration in equity markets, herding behaviour among passive funds and interlinkages across the global financial system each were judged as having the potential to amplify any such adjustments.

A significant increase in risk aversion in global financial markets was viewed as having the potential to increase financing costs sharply and constrain access to funds, including in Australia. Members noted the extent of concentration of ownership in key Australian debt securities markets, as was the case in some other international fixed income markets, which make it important for these investors to assess carefully their potential liquidity needs for stress scenarios. At the same time, members noted the reduction over time in Australian banks’ reliance on offshore funding markets and the steps they had taken to mitigate their exposure to global shocks, including by building significant liquidity buffers.

In considering the financial position of Australian households and businesses, members noted that most were in a relatively strong financial position. Cash flow pressures for households had eased as real wages had risen and interest rates had declined. Most households with mortgages had maintained their repayments and large savings buffers. Most businesses also had solid financial buffers. While the share of companies entering insolvency remained high in the retail, hospitality and construction industries, particularly for smaller firms, the insolvency rate across the economy was around its longer run average. Members also noted that banks remain well placed to continue lending and supporting the economy in the event of a significant economic downturn. This reflected their ongoing high levels of capital and liquidity, prudent lending standards and loan loss provisioning.

Members discussed the financial stability implications of the recent pick-up in housing credit growth, particularly for investors. The pick-up to date had been within the range of previous experience in monetary policy easing cycles. Credit growth in the period ahead would likely be supported to an extent by the expansion of the Home Guarantee Scheme. Importantly, members also noted that riskier types of housing borrowing – such as high loan-to-value, high debt-to-income and interest-only lending – had not picked up. Members noted their earlier observation that business credit had continued to grow strongly, with banks and non-banks competing vigorously for market share, but that overall corporate leverage remained low in Australia. Looking ahead, members noted that it was important that lending standards remain sound for housing and business borrowing, across the bank and non-bank sectors, to forestall any build-up of vulnerabilities in the financial system. In this context, members noted their support for the work being done with industry by the Australian Prudential Regulation Authority, as the macroprudential policy authority, to ensure that a range of macroprudential policy tools could be deployed in a timely manner if needed.

Finally, members discussed the importance of individual institutions, and the wider Australian financial system, strengthening resilience to geopolitical and operational risk. Advancing digitalisation across the financial system had increased the prospect that cyber-attacks and operational incidents could have systemic implications. Members noted the growing risk that financial and operational stress events could coincide in the future, which would complicate the nature of any crisis response and the scope of coordination required across regulators, government and industries. Members noted the significant program of work being led by the Council of Financial Regulators in this area.

Considerations for monetary policy

Turning to considerations for the monetary policy decision, members noted that the forecasts in the August Statement on Monetary Policy were for inflation to return to around the midpoint of the 2–3 per cent target range and for conditions in the labour market to be little changed at around full employment over the forecast period. They observed that these forecasts were based on the technical assumption that the cash rate follows the market path, which at that time implied three further 25 basis point cuts (including in August) over the year ahead.

Since the August meeting, private demand had recovered a little more quickly than expected given outcomes from the June quarter national accounts and early indicators for growth in demand in the September quarter. In the labour market, employment growth had slowed in August but the unemployment rate had been steady, and conditions overall appeared to be little changed. Members judged that the labour market was still a little tight and noted that forward-looking indicators were not signalling any material change in the near term.

Internationally, there continued to be considerable uncertainty about the outlook. Recent information suggested that momentum in the Chinese economy had been weak, although the staff’s judgement was that Chinese authorities would be likely to respond to any persistent weakness with additional fiscal stimulus. Members also noted that economic activity in the United States appeared to be growing at a steady rate, despite the softening labour market. The likelihood of higher tariffs having a pronounced adverse near-term effect on the world economy had diminished since April.

Members discussed the implications to be drawn from the monthly CPI indicator outcomes for July and August. While noting the partial and volatile nature of these data, members observed that the outcomes for certain components of the indicator – including market services and housing – suggested that the September quarter inflation outcome might be higher than the staff had expected in August. Members noted that the combination of potentially higher-than-expected inflation and broadly stable labour market conditions, if sustained, could imply that the staff’s assumption regarding the balance between aggregate demand and potential supply was incorrect. They also highlighted the potential lessons for Australia from the experience of some other countries where services inflation has been elevated.

Members observed that monetary policy was probably still a little restrictive but acknowledged the extent of restriction was difficult to determine. Financial conditions had eased further with the reduction in the cash rate target in August, and the pick-up in housing price and credit growth over prior months was indicative of the easing in monetary policy earlier in the year having an impact. Moreover, it would be some time before the full effect of the monetary policy easing flowed through the economy.

Regarding the risks to the outlook, members agreed that there were still risks on both sides of the forecast and debated their relative importance. On the upside, it was possible that the August forecasts had underestimated the strength of the recovery in consumption or had underestimated the extent of capacity pressures in the economy at present. But, on the downside, it was possible that the forecasts were not taking sufficient signal from the persistent weakness in consumer sentiment, the recent softness in employment or some timely indicators of wages growth.

Members agreed that financial stability considerations were not a constraint on their monetary policy decision at this meeting.

In light of these considerations, members agreed that it was appropriate to leave the cash rate unchanged at this meeting. They agreed that the flow of information since the previous meeting, the forecasts from August and their judgement about the extent of policy restrictiveness collectively implied that there was no need for an immediate reduction in the cash rate target. Looking ahead, members noted that it was appropriate for the Board’s decisions to remain cautious and data dependent.

In finalising its statement, the Board affirmed the importance of being attentive to the data and the evolving assessment of the outlook and risks when making its decisions. Members committed to pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board will remain focused on its mandate to deliver price stability and full employment and will do what it considers necessary to achieve that outcome.

The decision

The Board decided unanimously to leave the cash rate target unchanged at 3.60 per cent.

New Philly Fed chief Paulson backs gradual easing toward neutral policy

New Philadelphia Fed President Anna Paulson used her debut speech to call for a balanced approach to monetary policy as the economy navigates rising labor market risks and uncertain inflation dynamics.

She said policy should move toward a “more neutral stance,” stressing that the Fed must weigh both sides of its mandate. While she noted that the job market remains solid overall, she warned that conditions are “moving in the wrong direction” and that risks are “noticeably” increasing.

Paulson indicated she supports a measured pace of rate cuts consistent with the Fed’s latest projections, which outlined a quarter-point reduction last month and an additional 50 basis points of easing before the end of 2025, followed by further cuts in subsequent years.

On inflation, Paulson acknowledged that the recent tariff hikes could lift prices modestly, but said she does not expect those effects to persist. Still, she cautioned against rushing into deeper rate reductions given uncertainty over where the neutral rate truly lies.