Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.86; (P) 152.16; (R1) 152.59; More...

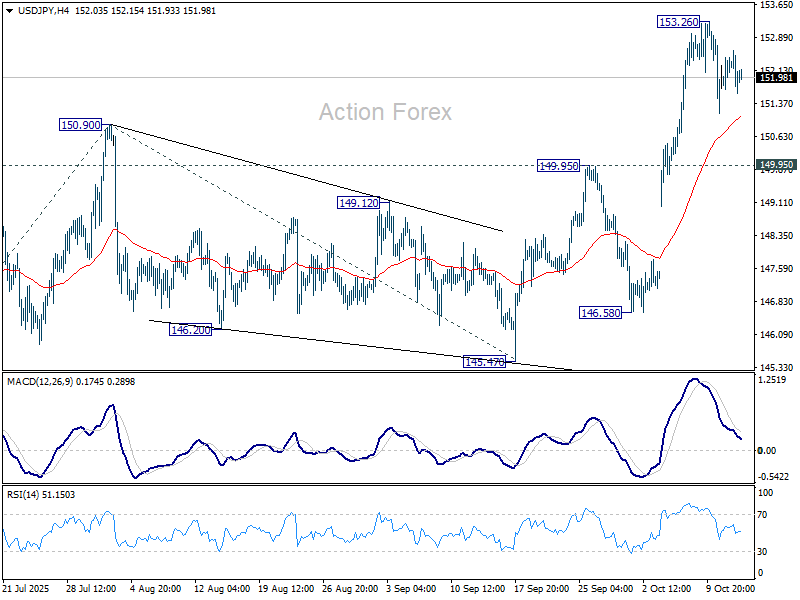

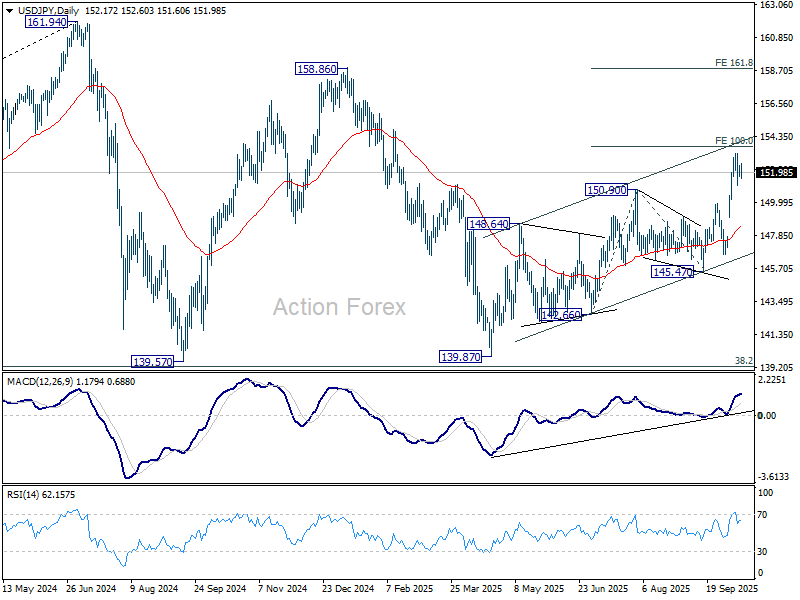

USD/JPY is staying in consolidations below 153.26 and intraday bias stays neutral. Downside should be contained above 149.95 resistance turned support. Break of 153.26 will target 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there will pave the way to 161.8% projection at 158.80. However, decisive break of 149.95 will bring deeper pullback to 55 D EMA (now at 148.48) instead.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8009; (P) 0.8033; (R1) 0.8067; More…

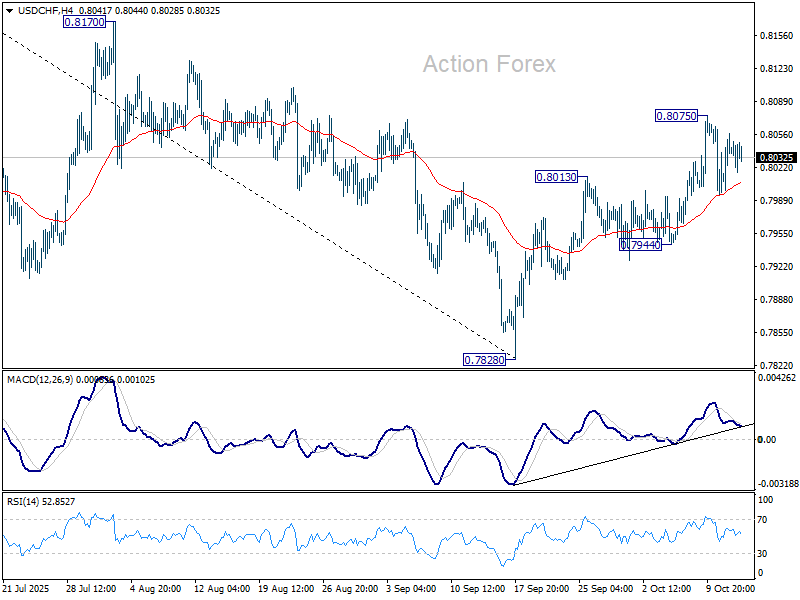

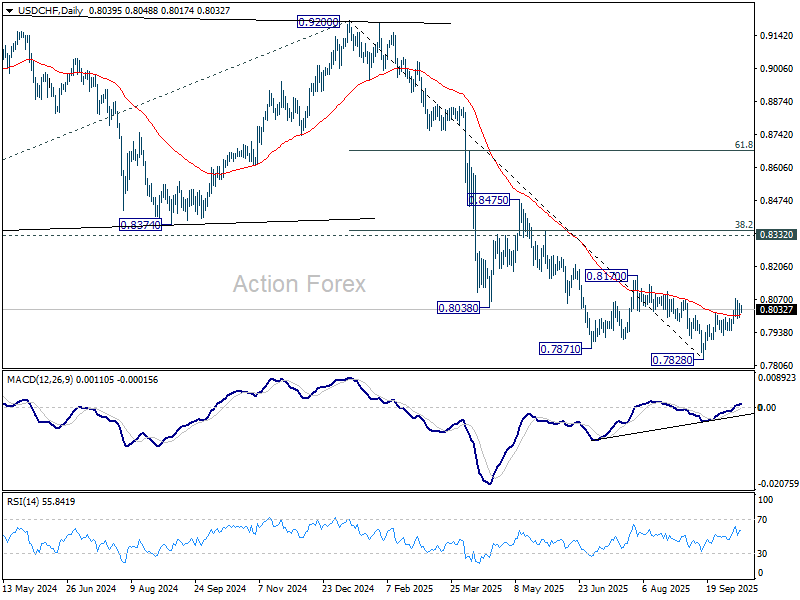

USD/CHF is staying in consolidations below 0.8075 and intraday bias stays neutral. Price actions from 0.7828 are currently seen as correcting whole fall from 0.9200. Above 0.8075 will target 0.8170 resistance next. On the downside, though, break of 0.7944 support will bring retest of 0.7828 low instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

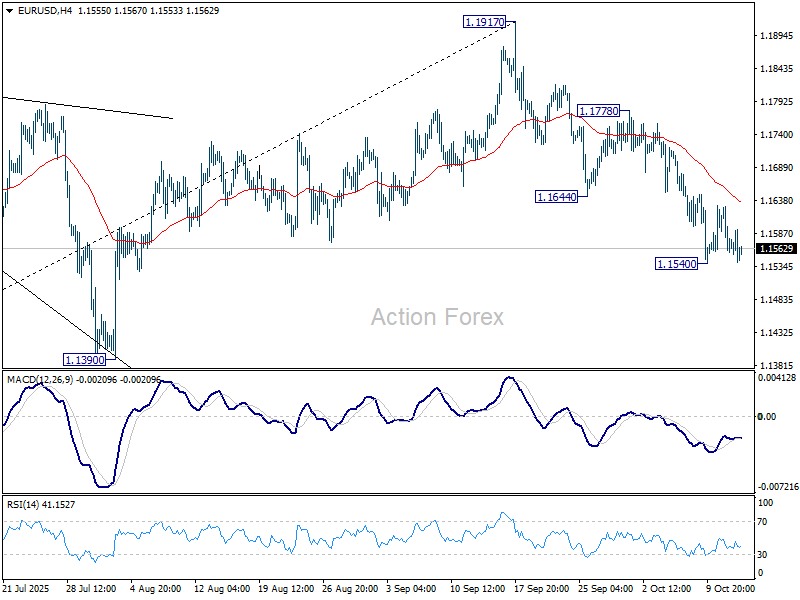

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1542; (P) 1.1586; (R1) 1.1614; More…

EUR/USD is staying in range above 1.1540 and intraday bias stays neutral. Deeper decline is expected as long as 1.1778 resistance holds. On the downside, break of 1.1540 will resume the fall from 1.1917 to 1.1390 , or further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1274) holds, the up trend from 0.9534 (2022 low) is still extended to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

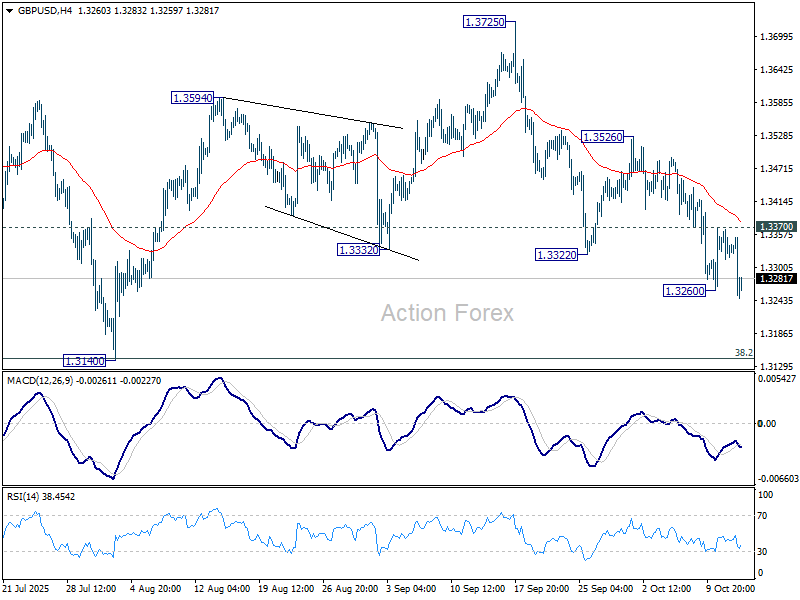

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3309; (P) 1.3338; (R1) 1.3360; More...

Breach of 1.3260 suggests that GBP/USD's fall is resuming. Intraday bias is back on the downside for 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected from there to complete the corrective pattern from 1.3787. On the upside, above 1.3370 minor resistance will turn intraday bias neutral first.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3173) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

Risk-Off Mood Deepens as U.S.–China Trade War Expands to Shipping

Global markets turned sharply defensive today as renewed U.S.–China trade tensions reignited fears of broader economic disruption. Equities fell across Asia and Europe, while safe-haven demand lifted Yen and Dollar. The latest flashpoint emerged at sea, where both countries introduced new port charges on ocean shipping firms, adding a fresh dimension to the ongoing trade confrontation.

Beijing announced that it would begin collecting special charges on U.S.-owned, operated, built, or flagged vessels. Washington, in turn, rolled out its own fees on Chinese-linked shipping companies. In another retaliatory step, China also sanctioned five U.S.-linked subsidiaries of South Korea’s Hanwha Ocean, accusing them of aiding a U.S. investigation into Chinese trade practices.

The risk-off tone spread swiftly through financial markets. Investors rotated into safe-haven currencies, with the Yen leading gains, followed by Dollar and Swiss Franc, while risk-sensitive units — Aussie, Kiwi and Sterling — underperformed. Euro and Canadian Dollar held to mid-range positions.

Adding to Sterling’s weakness, U.K. labor market data showed further signs of cooling. The combination of softer wage growth and rising unemployment gave the report a dovish tilt. However, policymakers are unlikely to pivot toward immediate easing yet. Despite the cooling trend, total pay growth remains elevated, and inflation is expected to tick higher to 4% in September, keeping the BoE cautious.

In Europe, at the time of writing, FTSE is down -0.45%. DAX is down -1.23%. CAC is down -1.00%. UK 10-year yield is down -0.066 at 4.594. Germany 10-year yield is down -0.03 at 2.607. Earlier in Asia, Nikkei fell -2.58%. Hong Kong HSI fell -1.73%. China Shanghai SSE fell -0.62%. Singapore Strait Times fell -0.80%. Japan 10-year JGB yield fell -0.033 to 1.663.

German ZEW edges higher to 39.3, but Eurozone sentiment slips on French turmoil

Germany’s ZEW Economic Sentiment Index rose modestly in October to 39.3, up from 37.3 but below expectations of 41.7. Current Situation Index deteriorated further from -76.4 to –80.0, undershooting forecasts of –75.0.

ZEW President Achim Wambach noted that experts “are still hoping for an upturn in the medium term,” but persistent global uncertainties and questions over Berlin’s state investment program continue to weigh on confidence.

Sectorally, expectations improved in several export-oriented industries after a recent slump in shipments to China. However, the automotive sector—long Germany’s industrial backbone—remains an exception with "slightly deteriorating indicator."

Across the broader Eurozone, confidence took a sharper turn lower. ZEW Economic Sentiment Index dropped to 22.7 from 26.1, missing expectations of 30.2. Current Situation Index plunged by -30 points to –31.8. ZEW attributed the decline largely to political instability in France and ongoing budget disputes.

BoE’s Taylor sees mounting downside risks, says trade diversion aiding disinflation

BBoE MPC member Alan Taylor, one of the committee’s most dovish voices, warned that the U.K. economy faces a “preponderance of downside risks” as growth slows and labor market slack widens.

In a speech today, he said output has fallen below potential, confidence among firms and households remains weak, and the trend of disinflation continues to deepen. Wage settlements are now expected to end the year around 3–3.5%, moving lower into 2026 — a sign, he argued, that “wage-led domestic inflation will not re-kindle an upward spiral.”

Taylor also pointed to global trade dynamics as a growing disinflationary force. He noted that U.K. import prices, particularly from Europe, have been falling for several years and are likely to decline further as “trade diversion” accelerates — a process through which supply chains shift across regions, increasing competition and reducing goods prices.

While acknowledging that the 2025 inflation hump and moderate expectations pose some upside risk, Taylor said these should fade by early 2026 as earlier tax and administered price effects roll off. With inflation fundamentals softening and external price pressures subsiding, he maintained that the balance of risks justifies a lower path for Bank Rate, consistent with his repeated dissents at recent MPC meetings.

UK payrolled employment falls -10k, but wages growth still firm

The latest U.K. labor market figures painted a mixed picture for September, highlighting a slowdown in hiring momentum alongside still-solid wage growth. Payroll employment fell by -10k. Claimant count rose sharply by 25.8k, well above expectations for a modest 10.3k increase.

At the same time, wage growth remains resilient, albeit easing from its prior peak. Median monthly pay increased by 5.5% yoy, down from 6.5% in August but still within the tight range seen since the start of the year.

Over the three months to August, unemployment rate ticked up to 4.8%, slightly higher than the expected 4.7%. Meanwhile, average earnings including bonuses rose 5.0% yoy, beating forecasts of 4.7% yoy. Pay growth excluding bonuses slowed to 4.7% yoy, in line with expectations.

Overall, the figures reinforce the view of a gradual cooling in the labor market rather than a sharp deterioration. Elevated wage pressures will remain a key concern for the BoE.

RBA minutes signal caution as board flags risk of hotter Q3 inflation

RBA’s September meeting minutes confirmed a steady hand on policy, with members concluding there was “no need for an immediate reduction” in the cash rate. The Board agreed that the economic data and forecasts since August supported maintaining the current level of restrictiveness, while emphasizing that decisions will remain “cautious and data dependent.”

Discussions focused heavily on inflation risks, particularly after stronger readings in the monthly CPI indicators for July and August. While acknowledging that these data are partial and volatile, members noted that upside surprises in market services and housing costs suggest the September quarter CPI could come in higher than expected in August forecasts.

The minutes revealed growing concern that if this pattern continues, the Bank’s assumptions about the balance between aggregate demand and supply could be too optimistic. Members also referenced lessons from abroad, where services inflation has proven stubbornly elevated, as a warning for domestic policy calibration.

Still, the Board recognized that risks remain "two-sided". On the upside, consumption could recover faster than assumed, or capacity pressures could prove stronger. On the downside, members highlighted the drag from weak consumer sentiment, slower employment growth, and subdued wage indicators.

The balance of views suggests the RBA will tread carefully in coming months, awaiting confirmation from the full Q3 inflation report before deciding whether further policy easing remains justified at the November meeting.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3309; (P) 1.3338; (R1) 1.3360; More...

Breach of 1.3260 suggests that GBP/USD's fall is resuming. Intraday bias is back on the downside for 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Strong support is expected from there to complete the corrective pattern from 1.3787. On the upside, above 1.3370 minor resistance will turn intraday bias neutral first.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3173) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

BoE’s Taylor sees mounting downside risks, says trade diversion aiding disinflation

BBoE MPC member Alan Taylor, one of the committee’s most dovish voices, warned that the U.K. economy faces a “preponderance of downside risks” as growth slows and labor market slack widens.

In a speech today, he said output has fallen below potential, confidence among firms and households remains weak, and the trend of disinflation continues to deepen. Wage settlements are now expected to end the year around 3–3.5%, moving lower into 2026 — a sign, he argued, that “wage-led domestic inflation will not re-kindle an upward spiral.”

Taylor also pointed to global trade dynamics as a growing disinflationary force. He noted that U.K. import prices, particularly from Europe, have been falling for several years and are likely to decline further as “trade diversion” accelerates — a process through which supply chains shift across regions, increasing competition and reducing goods prices.

While acknowledging that the 2025 inflation hump and moderate expectations pose some upside risk, Taylor said these should fade by early 2026 as earlier tax and administered price effects roll off. With inflation fundamentals softening and external price pressures subsiding, he maintained that the balance of risks justifies a lower path for Bank Rate, consistent with his repeated dissents at recent MPC meetings.

Commodity Currencies Weaken Amid Escalating Trade Tensions

The Australian and Canadian dollars weakened after Donald Trump announced plans to impose 100% tariffs on Chinese goods. The escalation in trade tensions between the world’s two largest economies has increased market caution and weighed on risk-sensitive currencies.

Trump stated that the tariffs would come into effect from 1 November or sooner, depending on Beijing’s response. The announcement followed China’s decision to restrict exports of rare earth metals — a move that fuelled concerns over the stability of global supply chains.

Although Trump later expressed optimism about a “constructive dialogue” with China, markets interpreted his remarks as a signal for heightened volatility.

This week, traders’ focus will remain on further comments from Washington and Beijing, as well as on oil price movements, which continue to be a key driver for USD/CAD. Any softening of rhetoric could support a recovery in commodity currencies, but if the US maintains a hard line, downward pressure on the AUD and CAD may intensify.

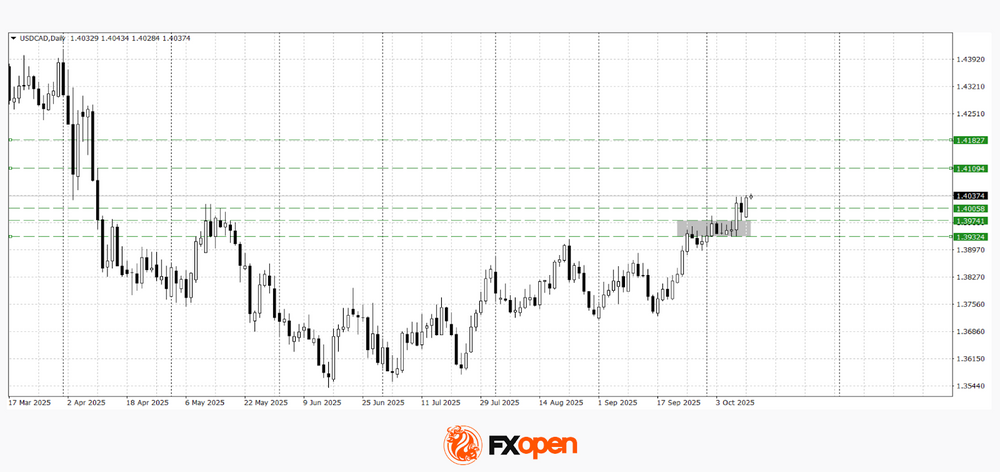

USD/CAD

News of the proposed tariffs prompted USD/CAD to break out of its medium-term range between 1.3930 and 1.3970. The pair not only pierced the upper boundary but also consolidated above the key psychological resistance level of 1.4000.

Technical indicators suggest potential for further gains towards the 1.4100–1.4180 area. However, if the price falls back below 1.4000, a retest of 1.3970 cannot be ruled out.

Key events that may influence USD/CAD trading today:

- 15:30 (GMT+3): Canadian building permits;

- 15:45 (GMT+3): speech by FOMC member Michelle Bowman;

- 18:15 (GMT+3): remarks by Bank of Canada First Deputy Governor Rogers.

AUD/USD

Late last week, the pair fell sharply, breaking below the critical 0.6500 support level. On Monday, investors showed signs of stabilisation, pushing the price back above that threshold.

Technical analysis points to the potential for a corrective rebound, as a bullish “harami” candlestick pattern has formed on the daily timeframe. Should the pair slip below 0.6500 again, last Friday’s low could be retested.

Upcoming events that may affect AUD/USD:

- 19:20 (GMT+3): speech by Fed Chair Jerome Powell;

- Tomorrow, 03:30 (GMT+3): Australia’s MI Leading Economic Index;

- Tomorrow, 22:35 (GMT+3): speech by Reserve Bank of Australia Governor Michele Bullock.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Silver Price Reaches Record High

The previous peak was set in 1980, but this week the price of silver rose above $53 for the first time ever, as shown on the XAG/USD chart.

Bullish sentiment has been driven by political factors, sustained demand from central banks, and the metal’s growing use in modern industries such as renewable energy.

Meanwhile, media reports are adding to the sense of market frenzy, noting:

→ shortages in physical supply;

→ forced liquidation of short positions (the “short squeeze” effect);

→ bold analyst forecasts — with a CNBC survey suggesting silver could double from current levels to reach $100.

Technical Analysis of the XAG/USD Chart

In earlier analysis of the XAG/USD chart, we:

→ identified an upward channel;

→ noted that silver’s rise was slowing around the $48.75 level, though new record highs in gold could spur the “silver bulls”.

That slowdown has proved to be merely a pause before a breakout to fresh 45-year highs. The ascending channel has maintained its slope but widened upward — notably, the current all-time high sits along the upper boundary of this expanded channel.

Key observations:

→ A sharp drop of more than 5% over the past two candles signals strong selling pressure, likely linked to profit-taking after a roughly 17% rise over the past 30 days.

→ Long lower wicks on the recent wide candles (as indicated by the arrow) show active buying interest.

→ The rise in the ATR indicator became evident as the market broke through the key psychological level of $50 per ounce.

The increase in volatility means traders may need to adjust their strategies — it can also signal that a market reversal could be nearing, as extreme price swings often mark the end of prolonged trends.

For now, however, demand remains strong enough to keep the market within its upward channel:

→ bulls are likely to view the $50–50.50 area as key support;

→ bears may look to reassert control if XAG/USD attempts to climb further above $53.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Crypto Market Quickly Met Resistance

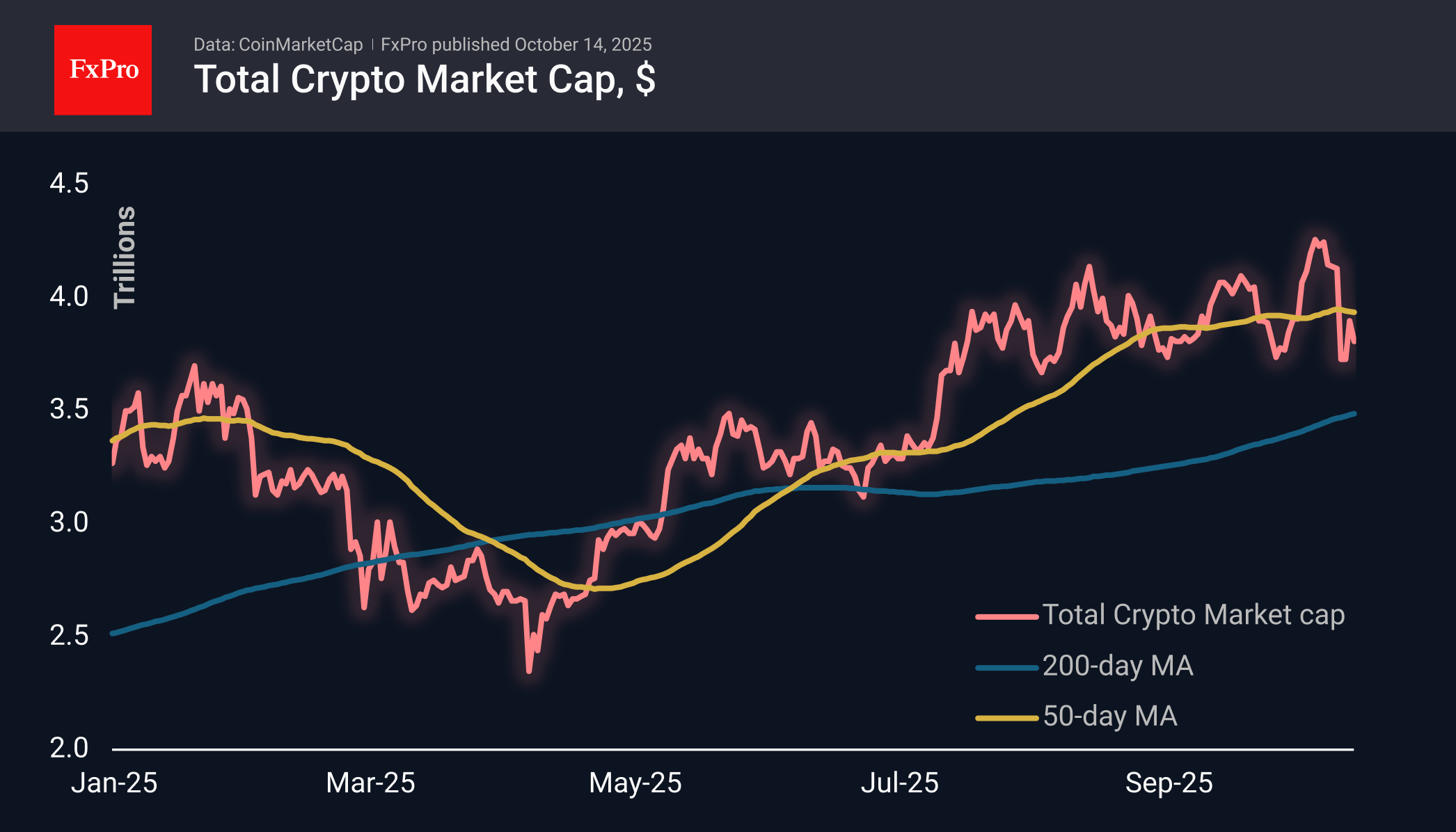

Market Overview

The crypto market capitalisation lost 2.8% over the past day to $3.81 trillion. On Monday, the 50-day moving average acted as local resistance. The recovery rebound did not find a solid foundation, as many investors doubt that the risks of sudden trade conflicts will quickly disappear. BNB recorded a 10% drop, while Zcash lost almost twice as much, retreating after a more than 300% rally in the last 30 days. XRP and Dogecoin are down more than 5%.

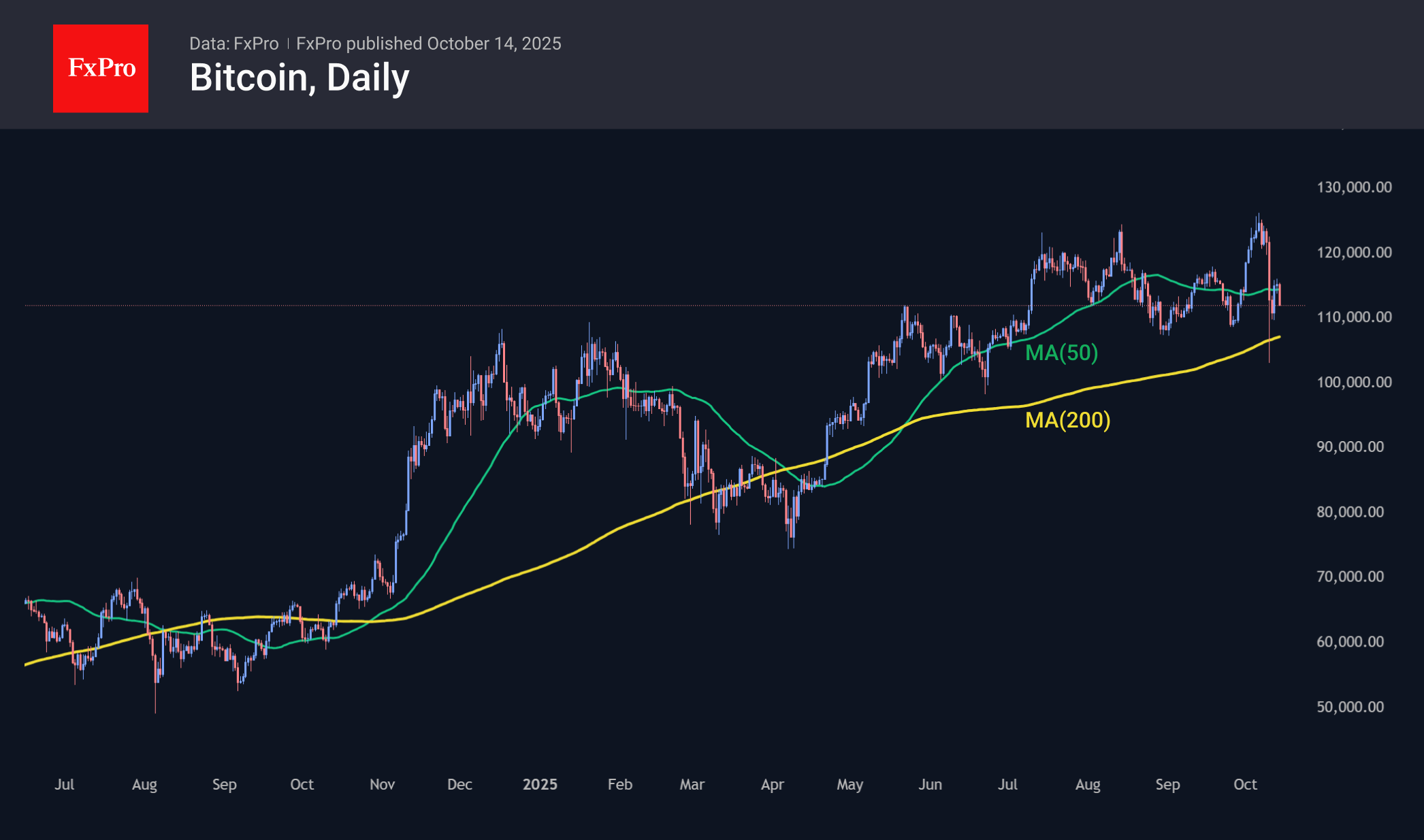

Bitcoin is down nearly 3% in 24 hours, falling below $112K. In July-September, the first cryptocurrency found buyers on dips in the $108-109K range, and the intrigue of the day is whether it will find them now. Like the crypto market, BTCUSD is trading below the 50-day MA but above the 200-day MA. Consolidation below the long average could be a repeat of the situation at the end of 2021, when a bear market started.

News Background

According to CoinShares, global investment in crypto funds rose by $3.169 billion last week, almost half the record inflow of the previous week. Investments in Bitcoin increased by $2.671 billion, in Ethereum by $338 million, in Solana by $93 million, in XRP by $62 million, and in Sui by $2 million.

The correction in the crypto market led to a large-scale liquidation of leveraged positions, which created conditions for a new phase of growth in crypto assets, according to CryptoQuant. The leverage ratio (ELR), which measures the average leverage of traders relative to reserves on exchanges, fell to its lowest level since 2022.

According to Glassnode, funding rates in the cryptocurrency derivatives market have reached their lowest levels since the 2022 bear market, which often creates conditions for growth.

Santiment analysts suggested that negotiations between the US and China on trade tariffs will soon determine the dynamics of the crypto market. Bitcoin could fall below $100,000.

Strategy bought 220 BTC ($27.2 million) last week. The total assets under management reached 640,250 BTC, worth about $73 billion. A week earlier, Strategy refrained from buying because it was unable to raise capital through the sale of shares.

BitMine bought another 202,037 ETH, taking advantage of the price drop. The company’s total reserves reached 3.03 million ETH, or 2.5% of the cryptocurrency’s issuance.

According to Bloomberg, Hong Kong-based China Renaissance Holdings is in talks to raise $600 million to create a fund focused on accumulating BNB. The fund’s shares are planned to be listed on the American stock exchange.

UK Wage Growth Hits 3-Year Lows, Gold Retreats from Highs, FTSE 100 Eyes Gains. US Earnings Season Ahead

Asia Market Wrap - Asian Shares Cautious

Asian stock markets showed mixed results on Tuesday, ultimately struggling to gain ground as optimism about potential US-China trade talks was offset by doubts about whether the two nations could reach a lasting agreement.

Initially, broader Asian indexes saw some gains, but those quickly faded to trade flat. A new front in the trade war opened as the US and China began imposing port fees on shipping firms.

Consequently, markets like Hong Kong's Hang Seng Index dropped 0.4%, and mainland Chinese blue-chip stocks slipped 0.1%.

However, some markets were boosted by company-specific news. Taiwan's market jumped 0.8% after a record performance by chipmaker TSMC, following an announcement that OpenAI would partner with Broadcom to create in-house AI processors.

In South Korea, the Kospi index gained 0.6% after Samsung Electronics reported surprisingly strong predicted operating profits for the third quarter, thanks to solid demand for traditional memory chips.

In contrast, Japan's Nikkei index fell 1.2% as the market reopened after a holiday.

UK Wage Growth Struggles

The rate at which UK workers' regular pay is increasing has slightly slowed down, marking the weakest growth in over three years, primarily due to slower raises in the private sector.

From June to August 2025, the average regular pay (not including bonuses) grew by 4.7% annually, a small drop from the previous period and exactly what market experts expected. This slowdown was entirely concentrated in the private sector, where wage growth fell from 4.7% to a four-year low of 4.4%.

In contrast, public sector wages actually accelerated, hitting 6.0% annual growth, partly because some pay raises were implemented earlier this year than last. Among different industries, the highest pay increases (after the public sector) were seen in wholesaling, retailing, and hospitality (5.9%), while the weakest were in finance and business services (2.9%). When accounting for inflation (meaning the real buying power of the wages), the growth was minimal, slowing to just 0.6%, which is the lowest real-terms gain since 2023.

The data today will only add to expectations of a December rate cut from the Bank of England (BoE).

European Session - European Stocks Struggle

European stock markets declined on Tuesday, reaching a two-week low, as fresh worries about the US-China trade conflict resurfaced and corporate news, specifically from French tire maker Michelin, weighed heavily on the market.

The overall STOXX 600 index fell by 0.6%. Investors were nervous after both the US and China began imposing new port fees on shipping companies, a move that signals an expansion of the trade war despite earlier hopes for talks.

This anxiety hit the miners sector the hardest, which fell by 2%.

The automakers sector also dropped 1.5%, largely due to Michelin, whose stock plunged 9.3% after the company cut its financial outlook for the entire year. Michelin blamed worse-than-expected sales and falling profit margins in the North American market.

Other related companies, like Germany's Continental and Italy's Pirelli, also saw their shares fall.

Bucking the trend, Swedish telecoms firm Ericsson soared 12.4% after it reported stronger-than-expected quarterly profits and downplayed the potential negative effects of the new US tariffs.

On the FX front, the U.S. dollar's strength was brief on Tuesday, as it weakened against many other major currencies.

Both the euro and the British pound (sterling) saw small gains against the dollar. Currencies often seen as a measure of investor risk appetite, the Australian dollar and the New Zealand dollar, both suffered heavy losses, dropping 0.63% and 0.5%, respectively.

In contrast, traditional safe-haven currencies, those investors turn to during times of uncertainty were gaining ground. The Swiss franc rose 0.2%, and the Japanese yen reversed its earlier losses to climb 0.3% against the dollar.

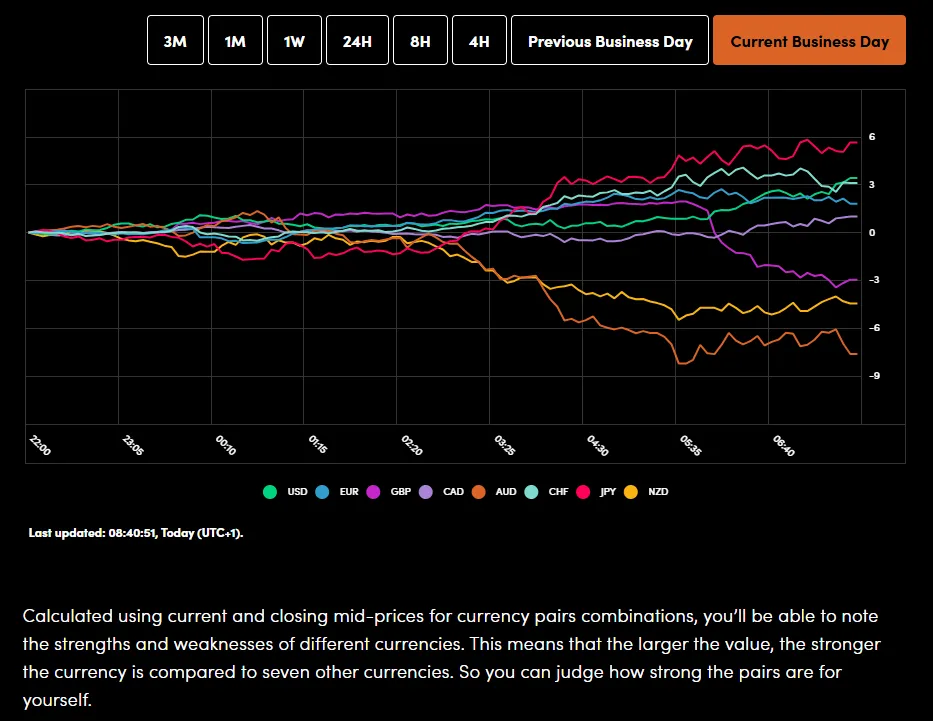

Currency Power Balance

Source: OANDA Labs

Oil prices saw a small increase on Tuesday, while the price of gold continued its record-breaking surge.

Oil gained slightly, with Brent crude rising 0.2% to $63.45 per barrel. This gain came after a report from OPEC (Organization of the Petroleum Exporting Countries) on Monday indicated a key shift in the oil market.

OPEC now expects the world's oil supply to closely match demand next year, mainly because the larger OPEC+ group is increasing production. This is a change from their previous forecast, which had predicted a shortage of oil in 2026.

Meanwhile, Gold showed no signs of slowing down, jumping another 1.1% to a new record of $4,179.00/oz.

Economic Calendar and Final Thoughts

Looking at the economic calendar, the European session will bring ZEW economic sentiment data from the Euro Area and Germany.

Later in the day markets will continue to keep an eye on trade deal development talks between the US and China before earnings season kicks off. We will hear from BlackRock, JPMorgan and Citi Group today before Central Bank speakers take the spotlight.

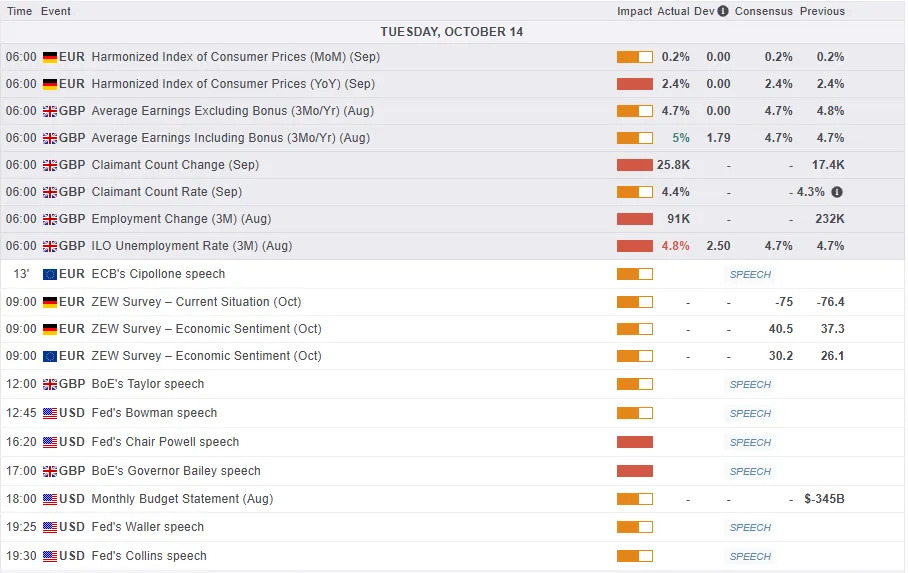

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Day - FTSE 100 Index

From a technical standpoint, the FTSE 100 is trading just above a key support level provided by the 100-day MA around 9392.5.

A hold above this level of support could signal another bullish leg to the upside.

The period-14 RSI is currently below the 50 level which signals bearish momentum. A break back above 50 here could help the FTSE 100 push higher.

Immediate resistance rests around the 9500 handle before the swing high at 9590 comes into focus.

On the downside, support rests at 9392 before the 9357 and 9311 handles become areas of interest.

FTSE 100 Index Four-Hour Chart, October 14. 2025

Source: TradingView.com (click to enlarge)