Sample Category Title

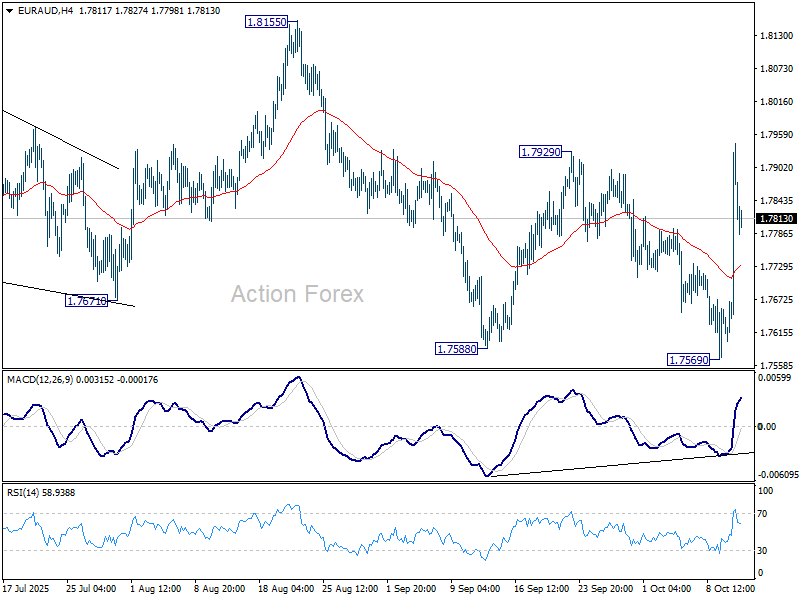

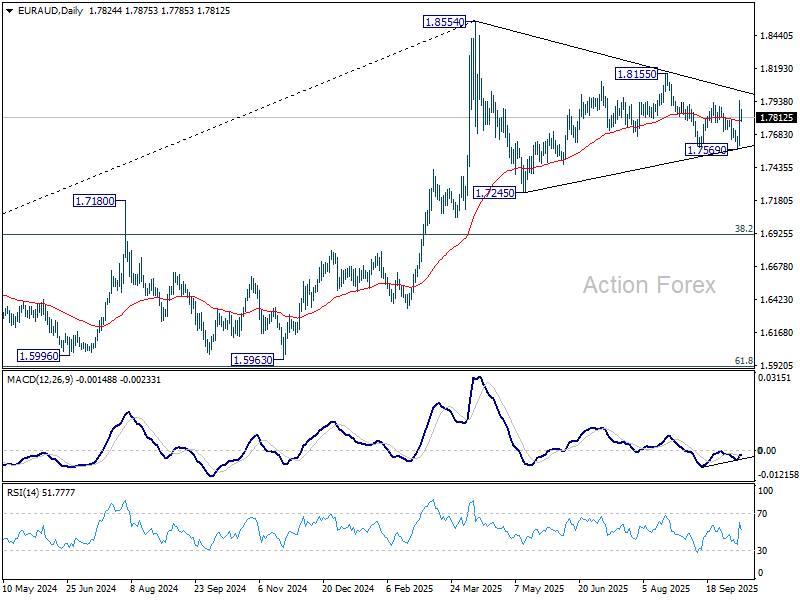

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7711; (P) 1.7837; (R1) 1.8071; More...

Intraday bias in EUR/AUD remains mildly on the upside for the moment. Fall from 1.8155 could have completed at 1.7569 already. Further rise should be seen to 18155 resistance. Firm break there will argue that whole corrective pattern from 1.8554 has also completed and bring retest of this high. On the downside, below 55 4H EMA (now at 1.7730) will turn bias neutral and mix up the outlook.

In the bigger picture, price actions from 1.8554 medium term top are seen as a corrective pattern. Deeper fall could be seen as the pattern extends, but downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Uptrend from 1.4281 is expected to resume at a later stage.

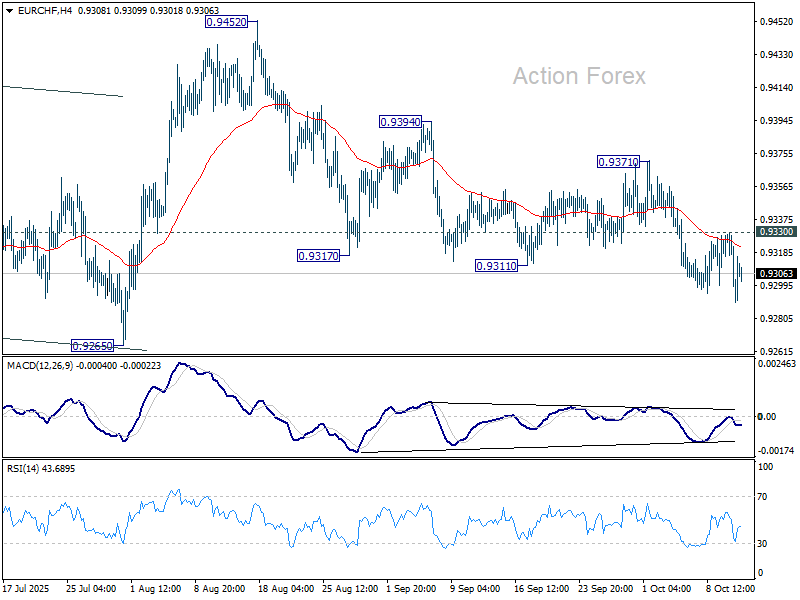

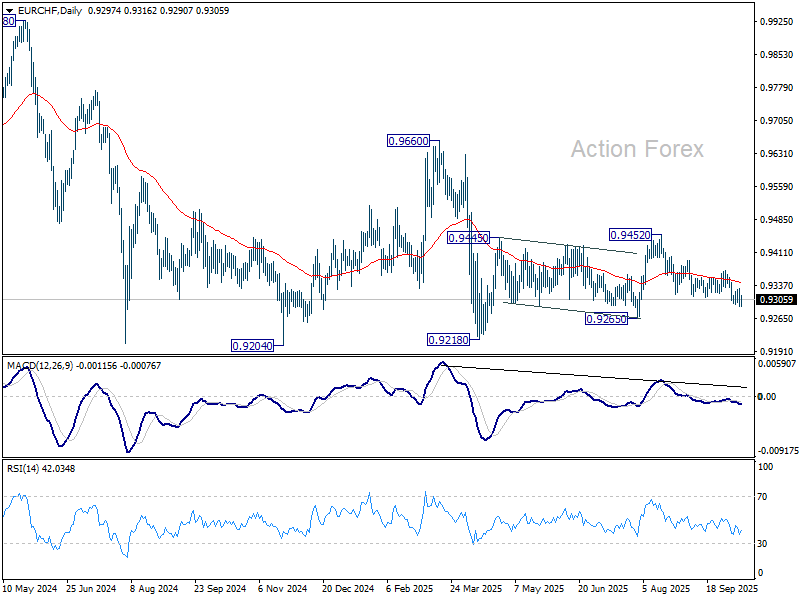

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9272; (P) 0.9303; (R1) 0.9319; More...

Intraday bias in EUR/CHF stays mildly on the downside at this point. Fall from 0.9452 should target 0.9265 support. Firm break there should confirm that whole corrective rebound from 0.9218 has completed at 0.9452, and deeper fall should be seen to 0.9204/18 support zone. For now, risk will stay on the downside as long as 0.9330 resistance holds, in case of recovery.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. Bearishness is reaffirmed by rejection at 55 W EMA (now at 0.9405). Firm break of 0.9204 will confirm down trend resumption. On the upside, break of 0.9452 resistance is needed to be the first sign of bullish reversal, and break of 0.9660 is needed to confirm.

Trump Revives Trade War With New Tariffs on China

In focus today

Today will be light on the data front, with no immediate market movers scheduled.

This week will be light in terms of data releases as the US government shutdown most likely means that the US CPI will not be released on Wednesday and as the other major economies have no tier-1 data scheduled. During the week we will get Chinese credit growth data, which has been strong into the summer but faded somewhat in recent months. We will also look out for the final September inflation print in the euro area and German ZEW, as well as both September CPI and PPI in China. In the UK, we receive the monthly labour market report and August GDP data. In Japan, focus turns to the parliamentary vote on a new PM on Wednesday.

Economic and market news

What happened since Friday

In global trade, US President Donald Trump caught markets (and us) by surprise on Friday as he posted on Truth Social he would impose 100% tariffs on all Chinese goods on top of existing tariffs, see US-China trade - New trade escalation turns focus to Xi-Trump meeting, 13 October. In addition, he threatened to put new export controls "virtually every product they make" and on "all critical software products". The measures were a response to China announcing new export controls on rare earth minerals on Thursday last week. The tariffs would not come into effect until 1 November, though, which leaves time for talks and a possible deal with China when Trump and Chinese president Xi Jinping meet at end of this month at the sidelines of APEC Summit.

Things already seem to have calmed down over the weekend as Trump on Sunday made a new post on Truth Social saying "Don't worry about China, it will all be fine" adding that "Highly respected President Xi just had a bad moment. He doesn't want Depression for his country and neither do I". The USA wants to help China, not hurt it!!". The change in tone suggest that there has been backchannel communication between the US and Chinese side over the weekend that points to a deal being possible at the end of the month and that the tariffs will not come into effect. China's Ministry of Commerce on Sunday released a Q&A on China's recent measures highlighting that "China's export controls are not export bans". While uncertainty has increased, we see a more than 50% chance that a deal will be made between Xi and Trump before the tariffs come into effect.

In the US, the University of Michigan's flash October consumer sentiment survey showed only small changes in consumer sentiment and inflation expectations from last release. September 1-year inflation expectations fell marginally to 4.7% (prior: 4.8%), while the preliminary October 1-year inflation expectations landed at 4.6%.

US President Donald Trump will address the Israeli Knesset on Monday as a fragile Gaza ceasefire enters its fourth day, allowing for the exchange of hostages and prisoners. Trump also leads a peace summit in Egypt, though lingering tensions and unresolved governance issues in Gaza underscore the challenges ahead for lasting stability.

In France, President Emmanuel Macron reappointed Sébastien Lecornu as French prime minister on Friday, only four days after Lecornu resigned from the post. Lecornu has already appointed a government and must now present a 2026 budget today and then likely face a vote of no confidence during the week. His survival depends on at least the tacit support from the Socialists and Republicans. To get the socialist support he will likely present a watered-down version of the previous budget proposals with less strict spending cuts and a possible change to the pension reform. If the parliament fails to pass a budget an emergency bill must be passed. If Lecornu is ousted in a vote of no confidence Macron must appoint a new PM or call for a snap election, which still is a significant risk.

In China, exports surprised to the upside in September, rising by 8.3% y/y (cons: 6.0%, prior: 4.4) to a seven-month high. In the same period, imports jumped 7.4% y/y (cons: 1.5%, prior: 1.3%). China's trade surplus came in at USD 90.5bn, below expectations of 99.0bn, but higher than the 81.7bn in September the year before.

In Sweden, activity improved in August with GDP rising by 2.4% y/y and 1.1% m/m. Consumption increased as expected, while production in manufacturing and construction also improved. Overall, the data aligns well with our expectations and forecast, albeit slightly exceeding them, which is encouraging for growth in H2.

In Norway, headline inflation came in at 3.6% y/y in September (cons: 3.7%). Core inflation was 3.0% y/y (cons: 3.1%, prior: 3.1%), marking a small downside surprise. The print aligns with the ongoing disinflationary trend, supporting our view that markets may be underestimating the potential for Norges Bank easing in 2026.

Norges Bank announced an important change to their liquidity steering system Friday evening: the introduction of central bank certificates for banks and the public in order to strengthen the attainment of its liquidity policy objectives. Last week, we wrote how we think markets heavily underappreciate the risk of such a radical change to the liquidity set-up.

In Denmark, CPI inflation increased to 2.3% in September from 2.0% in August, in line with our expectations. The move higher is particularly driven by a base effect on energy as a large gasoline price decline in September 2024 exits the inflation measure. Food prices declined only 0.1% mom following the price surge over the summer, which is less than usual for September.

Equities: Risky assets sold off heavily on Friday evening as Trump threatened 'massive' tariffs on China and potentially cancelling the planned meeting with Xi. Equities finished sharply lower (S&P 500 -2.7%, Nasdaq -3.6%, Stoxx 600 -1.3%). Investors sold the most liquid stocks, meaning big tech a sharp -4% lower. This was a 'classic' risk-off session, with falling equities accompanied by falling yields. The US 10y dropped -9bp, gold prices rose (now back above USD 4k again) and oil prices -4% (below USD 60/barrel and lowest since May). Dollar was however not in a 'classic' risk-off, but weakened instead of the typical 'flight to safety' behaviour, as has been the case before in Trump-induced volatility. Rebound appears to start already, with US futures 1-2% higher this morning.

FI and FX: Bond yields rallied on Friday as Trump threatened with new tariffs on China. US Treasuries rallied some 9 to 11bp across the curve from 2Y to 30Y maturities. German yields also rallied some 4-6bp across curve. There was only a modest movement in the USD from 115.7 to 116.1 versus the euro.

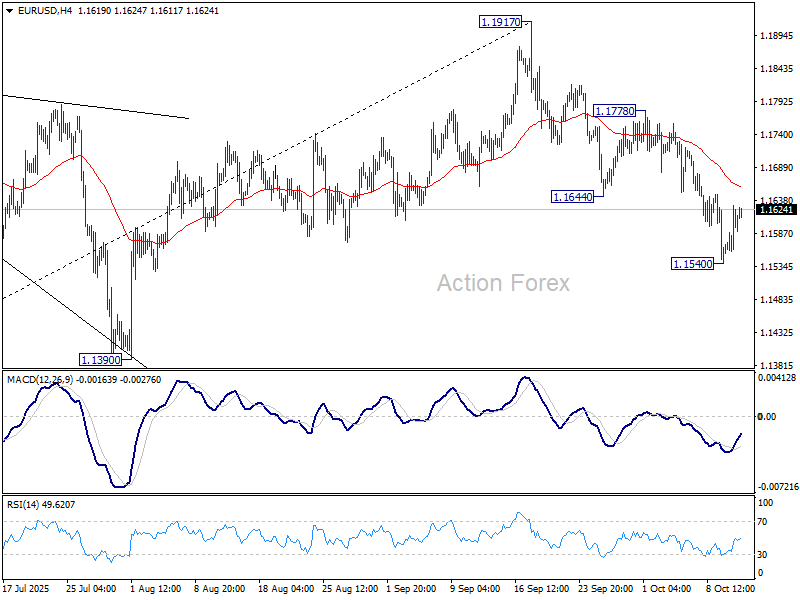

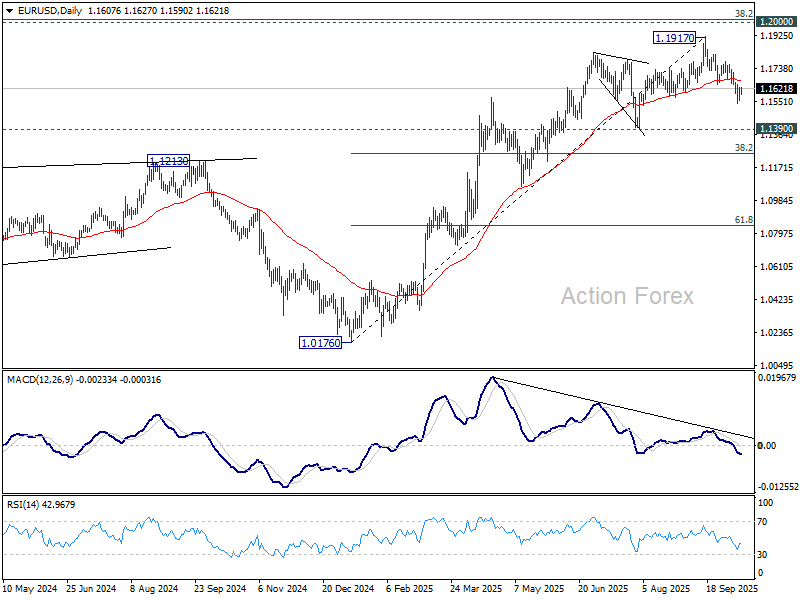

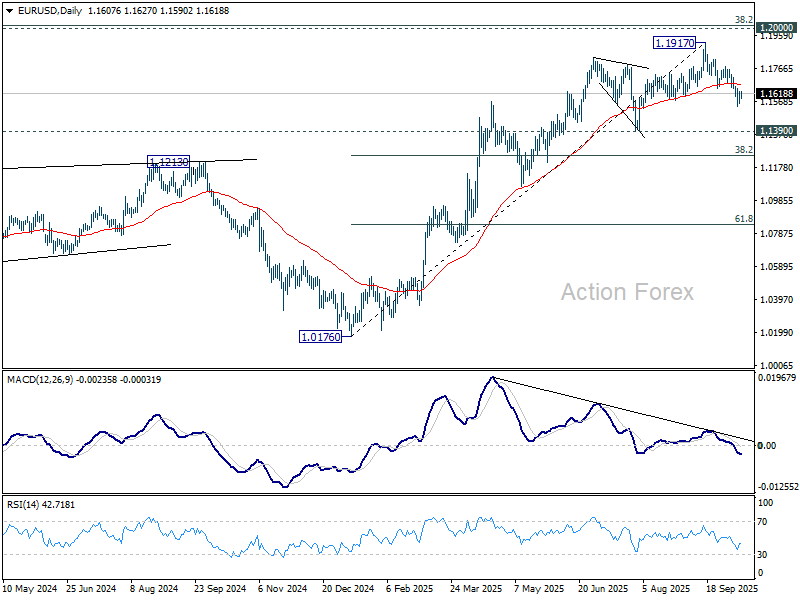

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1573; (P) 1.1601; (R1) 1.1651; More…

Intraday bias in EUR/USD stays neutral and some consolidations could be seen above 1.1540. Deeper decline is expected as long as 1.1778 resistance holds. On the downside, break of 1.1540 will resume the fall form 1.1917 to 1.1390 , or further to 38.2% retracement of 1.0176 to 1.1917 at 1.1252.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top is likely in place at 1.1917, just ahead of 1.2 key psychological level. As long as 55 W EMA (now at 1.1247) holds, the up trend from 0.9534 (2022 low) is still extended to continue. Decisive break of 1.2000 will carry larger bullish implications. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep outlook bearish.

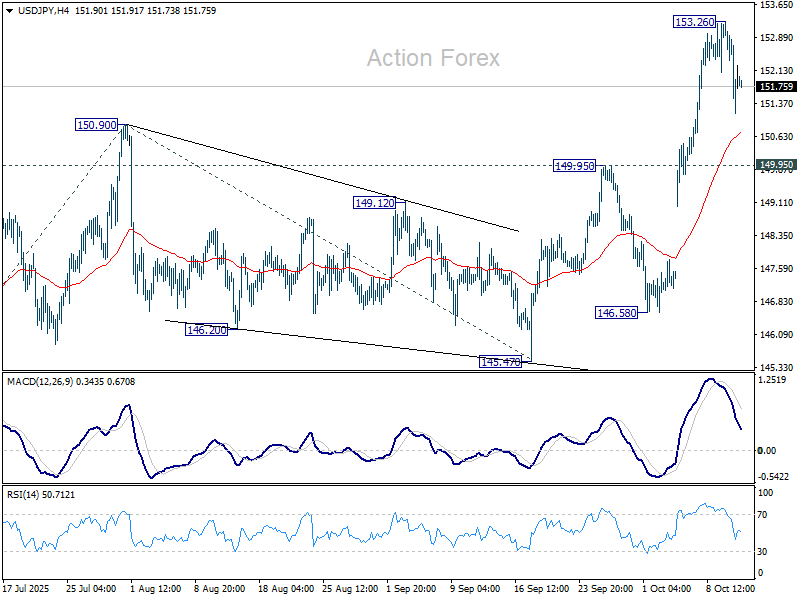

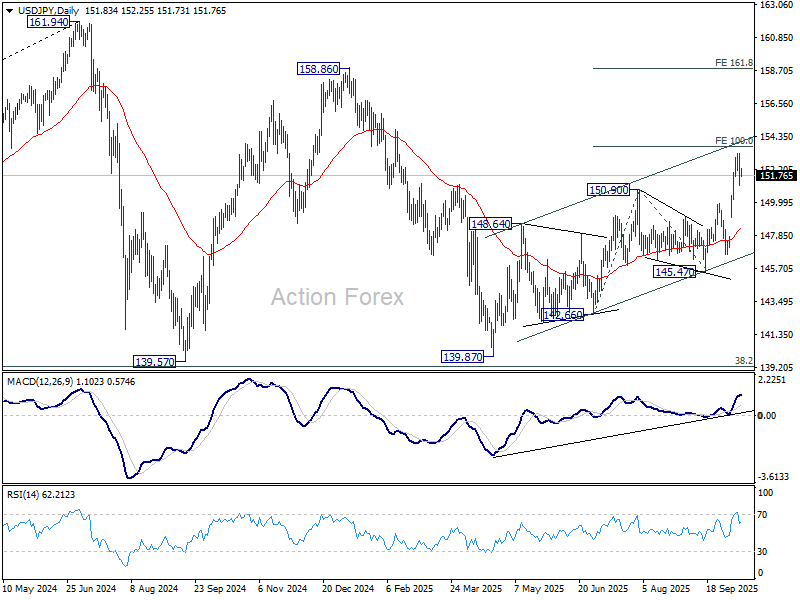

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.47; (P) 151.87; (R1) 152.58; More...

Intraday bias in USD/JPY remains neutral for the moment and some more consolidations could be seen. Downside should be contained above 149.95 resistance turned support. Break of 153.26 will target 100% projection of 142.66 to 150.90 from 145.47 at 153.71. Firm break there will pave the way to 161.8% projection at 158.80. However, decisive break of 149.95 will bring deeper pullback to 55 D EMA (now at 148.22) instead.

In the bigger picture, current development suggests that corrective pattern from 161.94 (2024 high) has completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. On the downside, break of 145.47 support will dampen this bullish view and extend the corrective pattern with another falling leg.

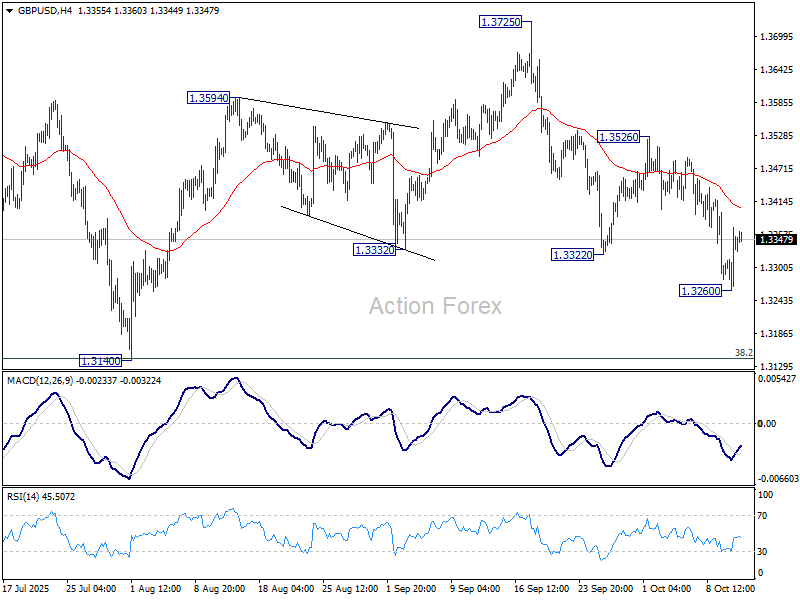

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3290; (P) 1.3329; (R1) 1.3395; More...

Intraday bias in GBP/USD remains neutral and some more consolidations could be seen above 1.3260 temporary low. Overall outlook is unchanged that corrective pattern from 1.3787 is extending. Below 1.3260 will bring deeper decline but strong support should be seen from 1.3140 cluster (38.2% retracement of 1.2099 to 1.3787 at 1.3142) to contain downside. On the upside, break of 1.3526 will bring stronger rally back to retest 1.3728/87 resistance zone.

In the bigger picture, rise from 1.0351 (2022 low) is still seen as a corrective move. Further rally could be seen to 61.8% projection of 1.0351 to 1.3433 (2024 high) from 1.2099 (2025 low) at 1.4004. But strong resistance could emerge from 1.4248 (2021 high) to limit upside. Sustained break of 55 W EMA (now at 1.3173) will argue that a medium term top has already formed and bring deeper fall back to 1.2099.

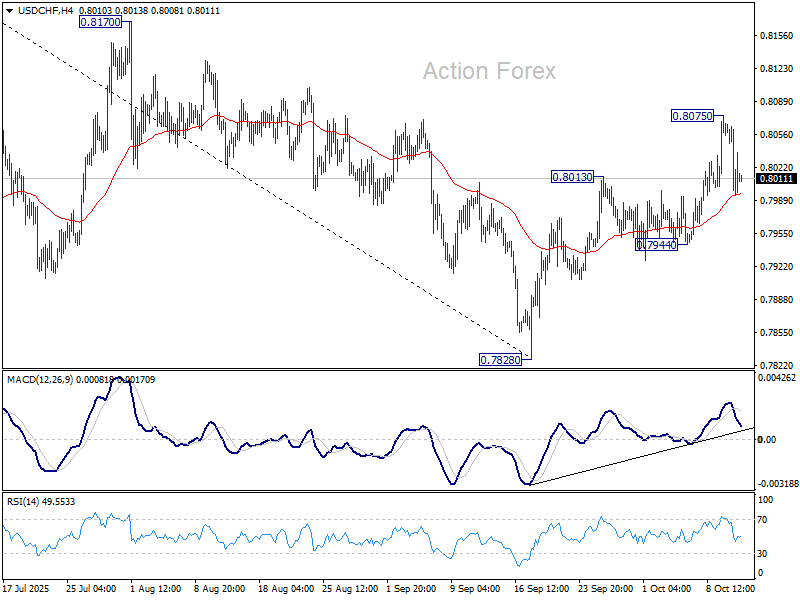

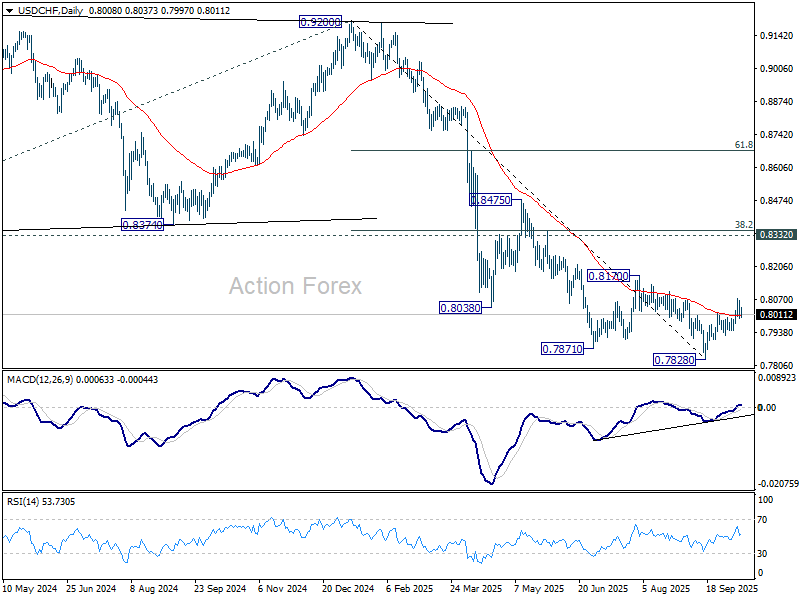

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7963; (P) 0.8019; (R1) 0.8050; More…

Intraday bias in USD/CHF remains neutral and some more consolidations could be seen below 0.8075 temporary top. Price actions from 0.7828 are currently seen as correcting whole fall from 0.9200. Above 0.8075 will target 0.8170 resistance next. On the downside, though, break of 0.7944 support will bring retest of 0.7828 low instead.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).

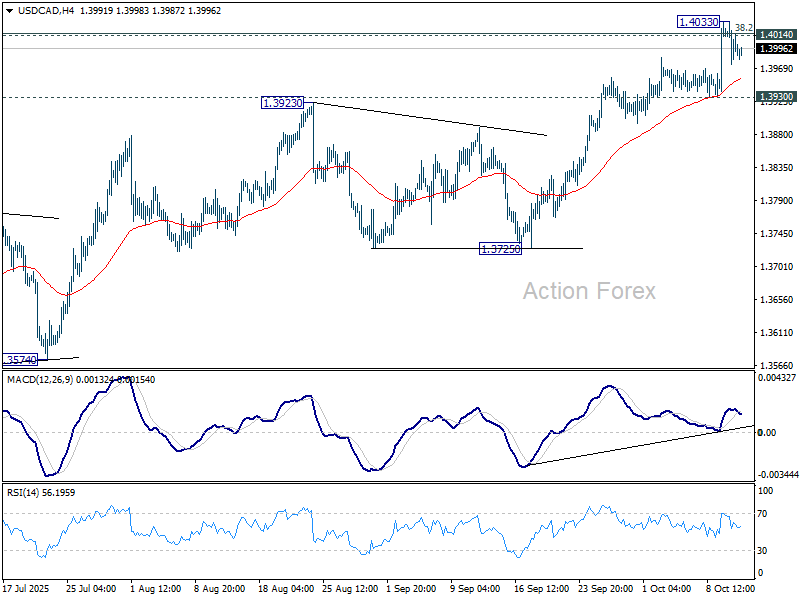

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3975; (P) 1.4004; (R1) 1.4033; More...

Intraday bias in USD/CAD stays neutral for the moment. On the upside, sustained break of 1.4014/7 will suggest that USD/CAD is already reversing the whole fall from 1.4719, and target 61.8% retracement at 1.4312. On the downside, firm break of 1.3930 support will indicate rejection by 1.4014/7 cluster resistance. That would keep the rebound from 1.3538 corrective, and turn bias to the downside for 1.3725 support.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. However sustained trading above 1.4014 will suggest that it's more likely just a correction, and the larger up trend would be in favor to resume through 1.4791 at a later stage.

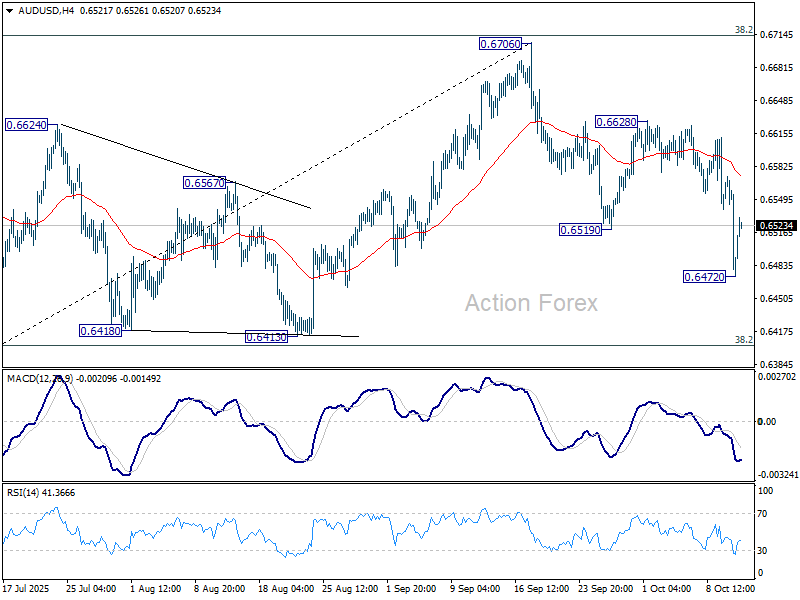

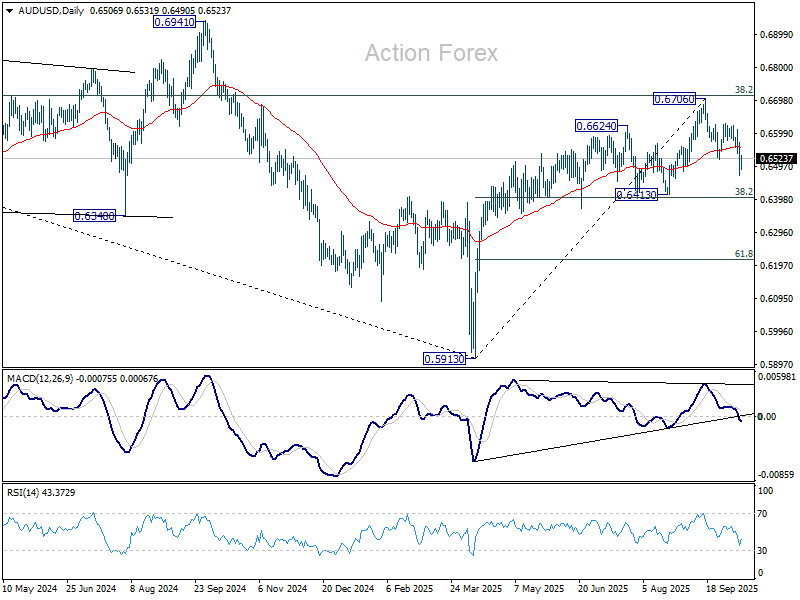

AUD/USD Daily Report

Daily Pivots: (S1) 0.6442; (P) 0.6508; (R1) 0.6542; More...

AUD/USD recovered notably today and intraday bias is turned neutral first. Still, risk will remain on the downside as long as 0.6628 resistance holds. Current development suggests rejection by 0.6713 fibonacci resistance. Below 0.6472 will resume the fall from 0.6706 to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.

U.S.–China War of Words Jolts Asia, Yet U.S. Futures Signal Contained Fallout

Asian equities started the week sharply lower after renewed flare-up in U.S.–China trade tensions, though signs from U.S. futures suggested that sentiment hadn’t worsened materially beyond last Friday’s selloff. Hong Kong’s Hang Seng Index slumped nearly -3.5% by midday, leading regional loss. The declines came after Beijing recently tightened export controls on rare earth minerals, prompting US President Donald Trump to retaliate with a threat of 100% tariffs on all Chinese imports starting November 1.

China’s Ministry of Commerce struck a combative tone over the weekend, saying the country was “not afraid of” a trade war and accusing Washington of a “textbook double standard.” The tit-for-tat rhetoric revived fears of a deeper standoff between the world’s two largest economies, though investors were quick to note that the broader risk mood had not deteriorated further. U.S. stock futures traded higher, signaling that Wall Street was stabilizing after last week’s sharp drop and that the Asian session was largely a delayed reaction rather than fresh panic selling.

Trump appeared to soften his stance on Sunday, posting online that “Don’t worry about China, it will all be fine!” and calling President Xi “highly respected.” He added that neither side wanted a depression, emphasizing that “the U.S.A. wants to help China, not hurt it.” The conciliatory tone contrasted sharply with his tariff threat days earlier and helped reassure investors that negotiations remain possible.

Vice President JD Vance echoed this calibrated approach in an interview with Fox News, saying the U.S. “will negotiate if Beijing is willing to be reasonable,” while reminding that Washington still “holds more cards.” Together, their remarks were interpreted as an attempt to de-escalate market fears without undermining the U.S. negotiating position.

Some observers see this exchange as part of a tactical phase rather than a reversion to the full-scale trade war. Both sides appear to be hardening their rhetoric strategically ahead of a potential Trump–Xi meeting at the APEC summit in South Korea later this month. Such posturing allows both governments to project strength domestically, and is more about negotiation leverage than policy action. For now, traders are watching for signs of follow-through, but few expect immediate disruption to trade flows.

In currencies, risk sentiment remained mixed but orderly. Aussie led gains for the day so far, followed by Kiwi and Loonie. Yen and Swiss Franc weakened while Euro dipped modestly. Sterling and Dollar traded mid-range. Overall, the currency markets are signaling unease, but not alarm.

In Asia, Japan is on holiday. At the time of writing, Hong Kong HSI is down -3.49%. China Shanghai SSE is down -1.17%. Singapore Strait Times is down -1.19%.

China trade in September, exports and imports surge, surplus narrows

China’s trade figures for September delivered a mixed picture. Exports rose 8.3% yoy, well above forecasts of 6.0% and marking the fastest pace in six months. Imports jumped 7.4% yoy, the strongest gain since April 2024 and far exceeding expectations of 1.5%.

However, the details showed signs of strain beneath the surface. Exports of rare earths—a key strategic material—fell -30.9% from August to 4,000 tonnes, the lowest level since February, amid tighter export restrictions. Meanwhile, soybean imports surged to the second-highest level on record, boosted by heavy purchases from South America as buyers avoided U.S. supplies in response to the escalating trade conflict.

Overall, China’s trade surplus narrowed to USD 90.5B from USD 102.3B, undershooting expectations of USD 98.5B. The surplus with the U.S. widened to USD 22.8B, even as total bilateral trade continued to shrink—exports to the U.S. fell nearly -17% in the first three quarters, while imports declined -11.6%. At the same time, trade deficit with Russia expanded to its widest level in six months at USD 2.1B.

NZ BNZ services at 48.3, contracts for 19th month as signs of strain persist

New Zealand’s services sector remained mired in contraction in September, with BNZ Performance of Services Index edging up modestly from 47.6 to 48.3. While the improvement marks a slight lift in momentum, the index has now stayed below the 50-point expansion threshold for 19 consecutive months.

Activity and sales rose to 47.8, and new orders improved to 49.6, but both remained in negative territory. Employment slipped to 47.8, reflecting ongoing caution among firms facing soft sales and squeezed margins.

BNZ reported that 58% of survey comments were negative, only marginally below August’s 59.6%. Respondents cited weak consumer confidence, rising living costs, and reduced discretionary spending as key drags. Many businesses also noted clients delaying projects and contracts amid broader economic uncertainty.

EUR/CAD: Euro pullback and Loonie resilience could amplify downside risks

Canadian Dollar is holding its ground as one of the month’s best-performing currencies so far, supported by surprisingly strong domestic data despite a slump in oil prices. WTI crude’s drop through 60 last week would normally pressure the Loonie, but September’s upbeat employment figures more than offset that drag.

The standout feature of the report was rebound in manufacturing jobs — the sector’s first monthly gain since January — signaling renewed momentum in an area hard-hit by global trade tensions. The improvement was particularly welcome after a weak summer stretch that had driven the BoC’s 25bps rate cut in September.

Markets are now looking to the October 21 CPI report for confirmation. Inflation would probably need to print well below expectations to confirm the case for another cut on October 29. For now, the data flow leans toward a pause.

Technically, EUR/CAD shows early signs of exhaustion after meeting upside target of 61.8% projection 1.4682 to 1.5959 from 1.5598 at 1.6387. Visible bearish divergence on D MACD reinforces the case that upward momentum is fading.

Sustained break below the 55 D EMA (now at 1.6160) should indicate medium term topping at 1.6402. Deeper decline could then be seen to correct whole five-wave rally from 1.4483 (Nov 2024 low), and target 38.2% retracement of 1.4483 to 1.6402 at 1.5669. Nevertheless, strong bounce from 55 D EMA will retain near term bullishness and set up another rally through 1.6402 instead.

Also, it should be noted that cross-currency dynamics point to growing downside risk for EUR/CAD. EUR/USD has failed to break through the key 1.2000 cluster resistance and has since retreated from 1.1917. Deeper pullback or even a shift toward bearish reversal could be underway.

At the same time, USD/CAD is testing strong cluster resistance near 1.4000, where a corrective dip appears likely after months of steady advance.

Should both patterns materialize—Euro weakening against Dollar while Loonie strengthens versus the Greenback—EUR/CAD would accelerate its decline, reinforcing the view that a medium-term top is in place. However, sustained strength in USD/CAD or stabilization in EUR/USD would shift the odds away from this bearish case in EUR/CAD.

UK and Australia take focus as shutdown delays U.S. CPI

It’s set to be a relatively quiet week in terms of data releases. The US calendar is near empty due to ongoing government shutdown. The most notable casualty is September’s CPI report, originally slated for Wednesday, which is now postponed. It's reported that the Bureau of Labor Statistics confirmed that it will “promptly resume” work, with CPI now scheduled for October 24 — nine days later than planned. The timing ensures the Fed will have the data in hand ahead of its October 28–29 policy meeting.

In the UK, labor market and GDP readings will be the main event. Speculation has already grown that the BoE’s easing cycle may be near its end, with policymakers keen to avoid reigniting inflationary pressures amid still-firm labor costs. Stronger wages or activity data this week would strengthen the case for the BoE to hold policy steady in November.

In the Asia-Pacific region, attention turns to Australia, where the RBA’s meeting minutes and September employment report will be closely watched. The November policy meeting remains live, with markets divided over whether another rate cut is warranted. The labor figures will be pivotal in shaping that debate, as resilient household spending has so far kept the RBA cautious about over-stimulating demand. The RBA’s minutes may offer some color on the internal balance of views but are unlikely to reveal new signals ahead of the more decisive Q3 CPI report later this month.

Here are some highlights for the week:

- Monday: New Zealand BNZ services index; China trade balance.

- Tuesday: RBA minutes, NAB business confidence; UK employment; Swiss PPI; German ZEW economic sentiment, CPI final; US NFIB small business index; Canada building permits.

- Wednesday: China CPI, PPI; Eurozone industrial production; Canada manufacturing sales, wholesale sales; US Empire state manufacturing, Fed's Beige Book.

- Thursday: Japan machine orders; Australia employment; Japan tertiary industry index; UK GDP, trade balance; Swiss SECO economic forecasts; Eurozone trade balance; US Philly Fed survey, NAHB housing index.

- Friday: Eurozone CPI final.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6442; (P) 0.6508; (R1) 0.6542; More...

AUD/USD recovered notably today and intraday bias is turned neutral first. Still, risk will remain on the downside as long as 0.6628 resistance holds. Current development suggests rejection by 0.6713 fibonacci resistance. Below 0.6472 will resume the fall from 0.6706 to 0.6413 cluster support (38.2% retracement of 0.5913 to 0.6706 at 0.6403).

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. Outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and pave the way to 0.6941 structural resistance for confirmation.