Sample Category Title

FTSE 100 Wave Analysis

FTSE 100: ⬇️ Sell

- FTSE 100 reversed from resistance zone

- Likely to fall to support level 9090.00

FTSE 100 index recently reversed down from the resistance zone between the key resistance level 9330,00 (which stopped the previous wave (3) in the middle of August, as can be seen below) and the upper daily Bollinger Band.

The downward reversal from this resistance zone started the active short-term correction 2.

FTSE 100 index can be expected to fall to the next support level 9090.00, the target for the completion of the wave 2 (low of the previous correction (4)).

EURUSD Wave Analysis

EURUSD: ⬆️ Buy

- EURUSD broke key resistance level 1.1835

- Likely to rise to resistance level 1.2000

EURUSD currency pair recently broke above the key resistance level 1.1835 (which stopped the previous impulse wave (5) at the end of June, as can be seen below).

The breakout of the resistance level 1.1835 was preceded by the breakout of the daily Triangle from July, which accelerated the active impulse wave (3).

Given the clear daily uptrend, EURUSD currency pair can be expected to rise to the next round resistance level 1.2000, target for the completion of the active impulse wave (3).

Gold (XAU/USD) Soars to Breach $3700/oz. FOMC Meeting Next, Will Rally Continue?

Gold prices soar to tap $3700/oz as Fed rate cut bets ramp up. The precious metal continues to benefit from the uncertainty around Fed policy moving forward beyond the September 17 meeting.

The expectations for a rate cut and a dovish Fed moving forward has led to US Dollar weakness and falling US Treasury yields which have aided Gold's rise. The US dollar is getting weaker, with its value falling against other major currencies.

This is because financial markets are now pricing in around 95% probability that the Federal Reserve will cut interest rates by 0.25% and expect a more dovish outlook moving forward.

At the same time, returns on US government bonds are also staying low. This makes assets like gold, which don't pay interest, more attractive to investors because they aren't giving up much in potential earnings by not holding bonds instead

The question for market participants right now is how much further can the gold rally go?

Fed Policy Holds the Key

On Wednesday, the much anticipated Federal Reserve decision will be the main focus for financial markets. It does appear as though a 25bps rate cut has largely been priced in and thus we have seen many analysts talk about the potential of a ‘buy the rumor, sell the fact’ reaction to the rate decision.

With that in mind, markets may be more focused on the dot plot and how the Fed sees the rate outlook moving forward. The calls by the Trump administration as well as a weakening labor market has seen markets price in more aggressive rate cuts over the next 12 months.

A dovish Fed outlook could fuel the Gold rally and push the precious metal toward the $3800/oz handle. A more hawkish outlook or no changes to the dot plot could see the Gold prices finally drop and pullback toward the $3600/oz handle.

Fed Independence Concerns Linger

The Fed meeting is holding its monetary policy meeting at a difficult time. US President Donald Trump is actively trying to influence their decisions, and there are legal challenges against the Fed's leadership which has led to concerns around Fed independence which is also aiding the Gold rally.

Leading up to the meeting, President Trump has been pressuring Fed Chair Jerome Powell on social media to make a bigger interest rate cut than what is expected. Trump believes that a more significant cut is overdue and would greatly help the housing market.

In a related development, a U.S. appeals court stopped an attempt by President Trump to remove Fed Governor Lisa Cook from her position, ruling that his reasons were not legally sufficient. This means Lisa Cook is expected to participate in Wednesday's important vote.

Additionally, Stephen Miran, a key economic advisor to President Trump, was narrowly confirmed by the Senate to join the Federal Reserve Board. Analysts believe that Miran might push for a larger interest rate cut than what most people expect, which keeps the question about how much political influence might affect the Fed's decisions.

Other Factors Supporting Gold Prices

Gold is receiving an extra boost from heightened global tensions, which are pushing investors toward safe-haven assets.

This increase in geopolitical risk is primarily driven by two major developments: an escalation of the conflict between Israel and Hamas, as Israel launched a significant ground offensive in Gaza City on Tuesday, and an intensification of drone and missile strikes by Ukraine on Russian refineries, which is disrupting Russia's energy infrastructure.

Economic Calendar

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Technical Analysis - Gold (XAU/USD)

From a technical standpoint, Gold broke out of the bull flag pattern on a four-hour timeframe before rallying to its potential target around the $3700/oz handle.

We are seeing a pullback since then with the latest four hour candle closing as a hanging man, which hints at further downside.

Given the rally this week, we could see a bit of a pullback as some market participants may look to take profit ahead of the FOMC meeting.

The period-14 RSI is also in overbought territory. A break back below the 70 level on the RSI usually signals a shift in momentum and could lead to a short-term push lower.

However, we have seen similar attempts at a pullback since the backend of last week and each time buyers returned with conviction to print fresh highs.

Thus there is a possibility that this could continue heading into the US Fed rate decision.

Gold (XAU/USD) Four-Hour Chart, September 16, 2025

Source: TradingView (click to enlarge)

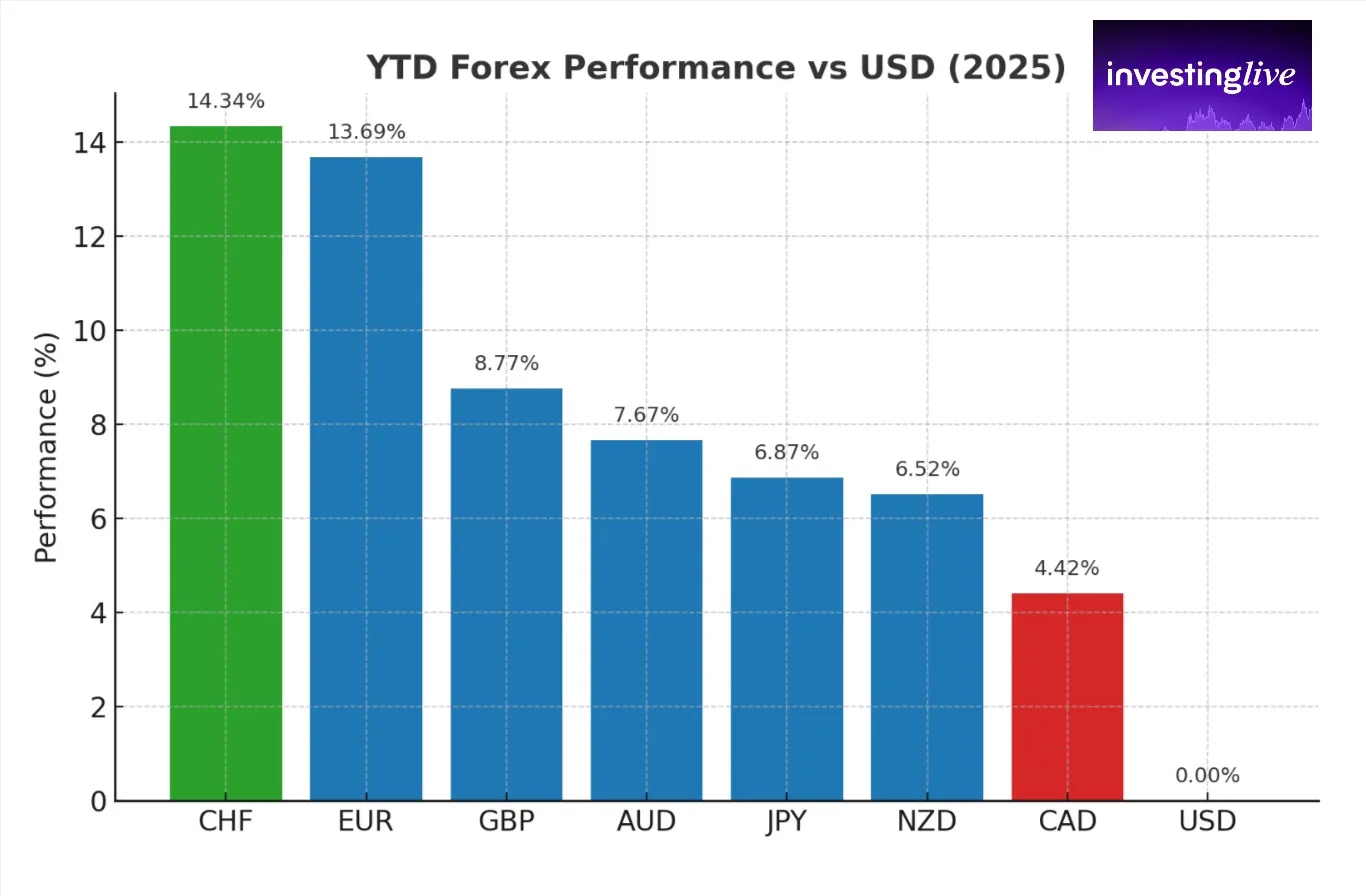

Swiss Franc Leads Majors as US Session Begins and Reclaims 2025 Crown

European currencies are having a fantastic year, with the CHF, the Euro, and GBP achieving their best performance since the early 2000s.

With US President Trump doing everything he can to devalue the US dollar (tariffs, beefs with other countries, menacing the Fed's Independence, and Jerome Powell), and on the other side of the Atlantic, EU countries allying to boost productivity in the years to come, the conditions for such outperformance are optimal.

Regarding basic economics, one thing to watch for Europe and Switzerland could be a too-strong currency, which would impair exports in an already-cooling economy (and crippled with 39% tariffs with the US).

In fact, Switzerland has been in deflation since May 2025. While its economy continues to grow slowly, such economic activity is not expected to hold up much given the recent SNB dovishness.

In the current state of geopolitics, participants looking for safety have had enough of a yen that loses too much in Carry due to historically low rates and have come back to the Swissie in search of value amid a less-competitive dollar.

2025 Currency Performance, September 16, 2025 – Source: InvestingLive.com

This nice graph offered by InvestingLive depicts how strong the geographic trends (mentioned through many of our previous pieces) guide Forex performance.

European currencies are leading with the new shift in narrative, followed by APAC (JPY, NZD and AUD) and finally North-American currencies which have struggled quite a lot.

Tomorrow should be interesting as traders really are pre-selling the US Dollar in what seems to be rushed-hedges for a dovish FOMC.

Any hawkishness or even a more neutral than dovish tone, and/or mentioning of tariff uncertainty should lead to consequent mean-reversion for the USD.

More mentions towards labor market weakness and one time tariff price hikes would be confirming the USD down-move.

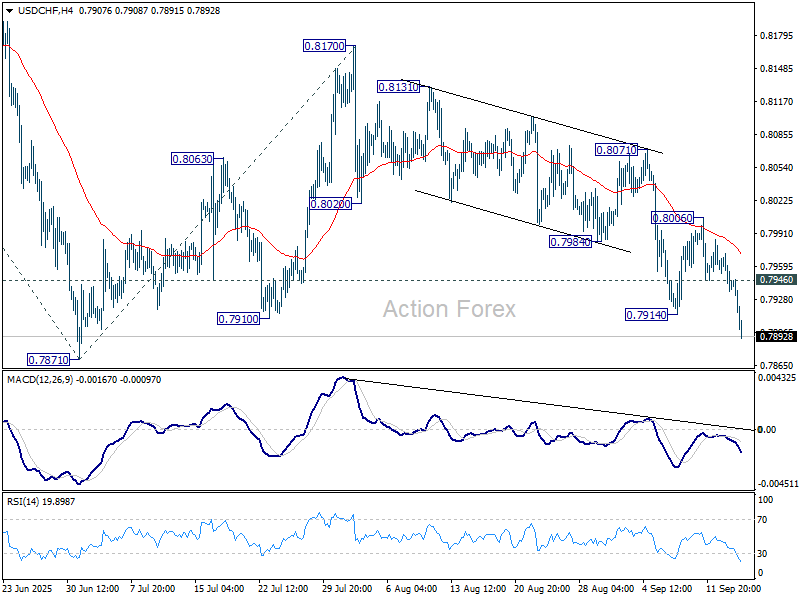

Up about 0.50% as we speak, let's have a look at USDCHF multi-timeframe charts to gain our edge on potential reversal or continuation levels for the pair.

USDCHF multi-timeframe analysis ahead of the FOMC

USDCHF Daily chart

USDCHF Daily Chart, September 16, 2026 – Source: TradingView

Despite a strong rebound in the USD in July followed by a monthly consolidation in August, the selling in CHFUSD has started to accelerate since the September NFP release, breaching 0.80 psychological level.

The first time the level was breached in 2025 was in mid-June, when Powell testified. Early July consequently saw a huge reversal higher in the pair.

The breakdown has happened on a few strong bear bars and bears should soon face the 2025 0.7875 Lows support, with prices entering that region.

Daily RSI still has place for movement and is not showing signs of upward tilt – However, one cannot forget that things may change in a flash in tomorrow's FOMC announcement.

USDCHF 4H Chart

USDCHF 4H Chart, September 16, 2026 – Source: TradingView

The ongoing price action is a solid tight bear channel, with traders rushing to exit and hedge their positions before tomorrow's huge trading Session.

Reactions will be interesting as this morning saw another rejection of the 50-period MA at the conjunction of the 2025 downward trendline, which led a huge descent in prices.

USDCHF is now trading around the middle of a freshly formed channel (with the 2025 downtrend) and with oversold RSI conditions, it will be interesting to spot what traders look to do looking forward.

Trading Levels for USDCHF

Daily Resistance Levels

- 0.7970 MA 50

- 0.80 psychological level

- Long-term pivot 0.80 Zone (0.80 to 0.81)

- Main resistance 0.8150 to 0.82 (last highs 0.8165)

- May 2025 highs 0.8475 Resistance Zone

Daily Support Levels

- 0.7890 current daily lows and counting (and middle of downward channel)

- 0.7840 to 0.7875 2025 lows

- 0.77 to 0.7735 August 2011 lows

USDCHF 1H Chart

USDCHF 1H Chart, September 16, 2026 – Source: TradingView

A measured move would place the pair to new lows in 2025 as the imminent selling accelerates after the Retail Sales data.

On the other hand, watch for the way oversold levels – The tight bull channel is expected to hold as long as no bull candle closes above the previous one, so sellers are tightly in control for now.

Watch price action in any close above the 0.7950 short-term pivot zone and any potential acceleration above 0.80. If the current trend continues, look at the 2011 support levels.

Safe Trades and successful trading ahead of the FOMC!

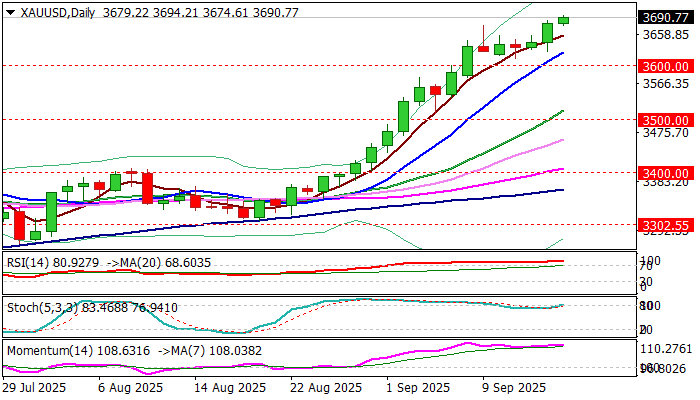

Gold Hits New Record High on Weaker Dollar / Fed Rate Cut Expectation

Gold rose to new record highs in late Monday / early Tuesday trading, as bulls regained traction after a narrow consolidation in past four days.

Fresh weakness of US dollar ahead of Wednesday’s Fed rate decision, in which the central bank is widely expected to cut rate by 25 basis points (there is also a small chance for possible 50 basis points rate cut) provided fresh boost to the yellow metal’s price, in addition to deepening political crisis in the US and some EU countries, as well as signals of worsening geopolitical situation.

With rate cut being almost fully priced in, markets await to hear about Fed’s guidance for the near future, with growing hopes that the central bank will remain in a dovish mode that would provide further support for gold.

Psychological $3700 level is under increased pressure, with break here to expose next target at 3734 (Fibo 138.2% projection).

Bulls so far don’t react on overbought daily studies, but some consolidation / shallow correction should be expected in the near term, if current fundamentals remain unchanged.

Res: 3700; 3734; 3750; 3789

Sup: 3674; 3624; 3600; 3577

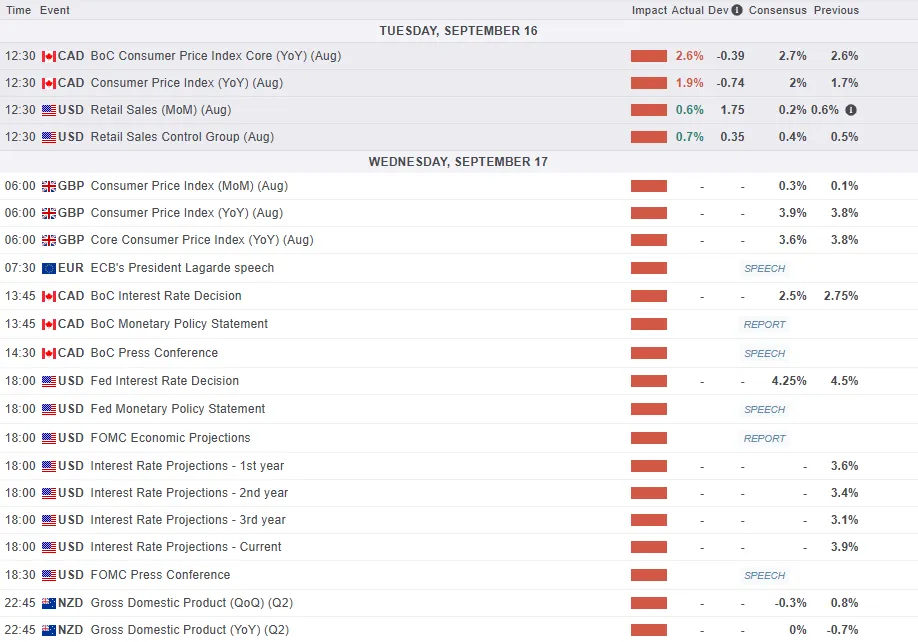

US: Retail Sales Continued to Rise in August

Building on their gain in July, retail and food services sales continued to grow in August, advancing by 0.6% month-on-month (m/m) and matching July's gain. Today's result was stronger than consesus expectations for a 0.2% gain.

Sales of autos & parts as well as sales at the gasoline stations both rose by 0.5% on the month. Sales at the building materials and garden equipment & supplies stores were little changed (+0.1% m/m).

Sales in the "control group", which excludes the three volatile components mentioned above (i.e., autos, gasoline and building supplies) were up by a healthy 0.7%. Online sales led the gains, with sales at non-store retailers rising by 2% on the month. Clothing stores had another good month, with sales rising by 1.0% - a sixth consecutive monthly increase. Sales of sporting goods & hobby items were also higher (+0.8%). Miscellaneous (-1.1%), general merchandise stores (-0.1%), health & personal care stores (-0.1%) and furniture (-0.3%) retailers were the categories where sales were lower.

Sales at bars and restaurants – the only service category in the report – rebounded by 0.7%, following a flat reading in the prior month.

Key Implications

There was not much to complain about in this report. Retail sales continued to rise at a decent clip for the third consecutive month, with above-consensus print for both core and headline numbers. Decent retail sales over the last few of months suggest that consumer spending growth is likely to come in around 2% (annualized) in the third quarter. This is still modest growth, particularly when compared with the 3.5% pace seen in the second half of last year, but better than our initial tracking.

Consumers may have breathed a sigh of relief that their worst inflation fears have not materialized, however, the impact of tariffs continues to show up in core goods prices. Up until recently, businesses have tried to absorb higher costs and shield consumers, but inflation data over the last few months have shown that some of the costs are now being passed on. We expect greater pass through of tariff-related price increases over the coming months. With the labor market downshifting and cost pressures heating up, consumer spending momentum is likely to remain modest through year-end.

Sunset Market Commentary

Markets

With the upcoming Fed meeting looming – one which should see rates reduced for the first time since December – it would take something material to lure investors from the sidelines back into the market arena. US retail sales tried by coming in better than expected across the board. Headline sales rose 0.6% on a non-inflation adjusted monthly basis while the control group (used in GDP calculations) added 0.7%. Last month’s figures saw a slight upward adjustment as well. But the NY Fed’s services business activity indicator unexpectedly slumped to one of the weakest levels in recent years (-19.4 from 11.7) with weak details, including for the forward-looking gauge. It basically confirmed the message coming from the manufacturing series published yesterday. The mixed bag of data left no permanent marks on rates. The latter eventually turned south in early US dealings with changes varying between -2.7 (2-yr) and -0.2 bps (30-yr). German Bunds underperform, driven by the long end of the curve. The 30-yr rises 2.6 bps. The French spread overtook the Italian one yesterday and that remains the case today. It’s a symbolically important sign of the times. A nervous dollar loses some ground against G10 peers. The greenback on a trade-weighted basis hits a two-month low in the 97 area. EUR/USD rose to fall just short of the July high at 1.1829. The pair is currently trading around 1.1822 and seems eager for a leap higher. A nod from Fed chair Powell could be needed for a sustained break though. The 2-yr tenor hovers near important support at the 2024/2025 lows. In other Fed-related news, the US White House said it’ll appeal Monday’s court decision that affirmed Fed’s Cook can continue do her job with her lawsuit challenging Trump’s move to fire her pending. It seems that, at least for the September meeting, Cook will be able to cast her vote as member of the Board nonetheless. The UK labour market report came in largely as expected. Sterling shrugged and EUR/GBP followed EUR/USD higher. UK assets, including gilts, are now eying tomorrow’s CPI release and Thursday’s BoE annual decision on QT. It is near certain that the £100bn of the last three years will be reduced since it would mean topping up the £50bn passive rundown by the same amount. That could pressure an already jittery gilt market.

News & Views

The Hungarian Statistical office today published Full time employers’ average earnings data. Average gross earnings in July grew by 9.0% Y/Y down from 9.7% in June (-1.5% M/M). Private sector wages declined 1.7% M/M bringing the Y/Y measure to 8.7% from 9.7%. After a strong 3.7% M/M gain in June, public sector wages declined a modest 0.5% M/M still raising the Y/Y measure from 9.5% to 10%. Net earnings increased by 9.4% and real earnings were 4.9% higher compared to the same month last year. The overall outcome of the report was slightly softer than expected. Even so, it doesn’t profoundly change the outlook for MNB policy in the short term as wage growth is still expected to remain elevated. The MNB in its latest inflation report (June 2025) expected whole economy gross wage growth of 9.2% this year, accelerating back to 10.5% next year. Short-term HUF rates held stable today (2-y swap 6.15%). Money markets hardly see any chance the MNB already being able to further reduce the policy rate (6.5%) this year. The forint in the meantime is testing the strongest levels in more than a year (EUR/HUF 390 area).

Canadian CPI declined 0.1% M/M (NSA) raising the Y/Y measure from 1.7% to 1.9%, falling below consensus expectations (2.0% Y/Y). Gasoline prices falling to a lesser extent year over year in August (+1.4% M/M; -12.7% Y/Y) than in July (-16.1%) were an important driver behind the faster growth in headline inflation. Excluding gasoline, the CPI rose 2.4% in August, after increasing 2.5% in each of the previous three months. Moderating the acceleration in the all-items CPI were lower prices for travel tours and fresh fruit compared with July, statistics Cananda comments. Shelter prices rose a modest 0.1% M/M and 2.6% Y/Y (from 3.0%). Core inflation (trim measure) eased slightly to 3.0% from 3.1%. Even as core inflation still holds above the 2% target, softer activity data, including poor labour market data for July and August, are expected to push the Bank of Canada to restart its easing cycle and cut the policy rate tomorrow from 2.75% to 2.5%. The loonie gains modestly today against a broadly weaker US dollar (USD/CAD 1.375).

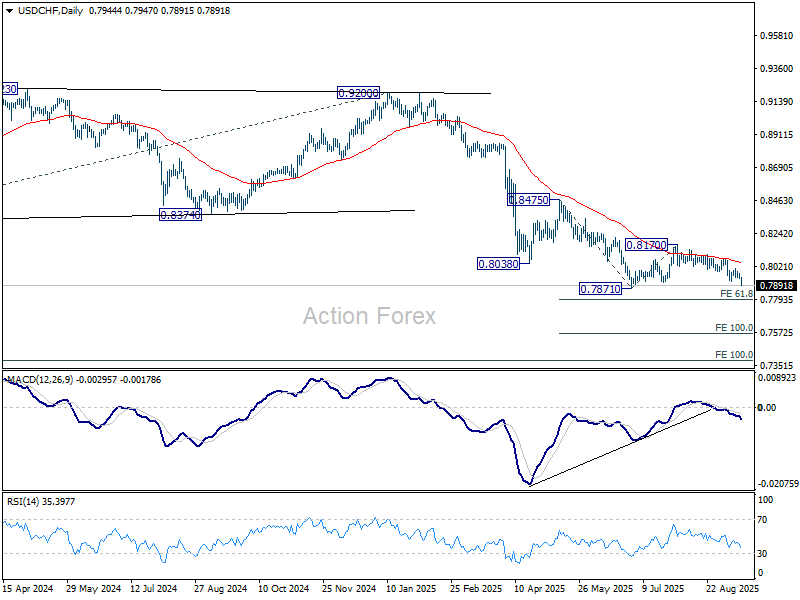

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7931; (P) 0.7953; (R1) 0.7968; More….

Intraday bias in USD/CHF is back on the downside with break of 0.7914 support. Further fall should be seen to retest 0.7871 low. Decisive break there will resume larger down trend to 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797. On the upside, above 0.7946 minor resistance will turn intraday bias neutral again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds.

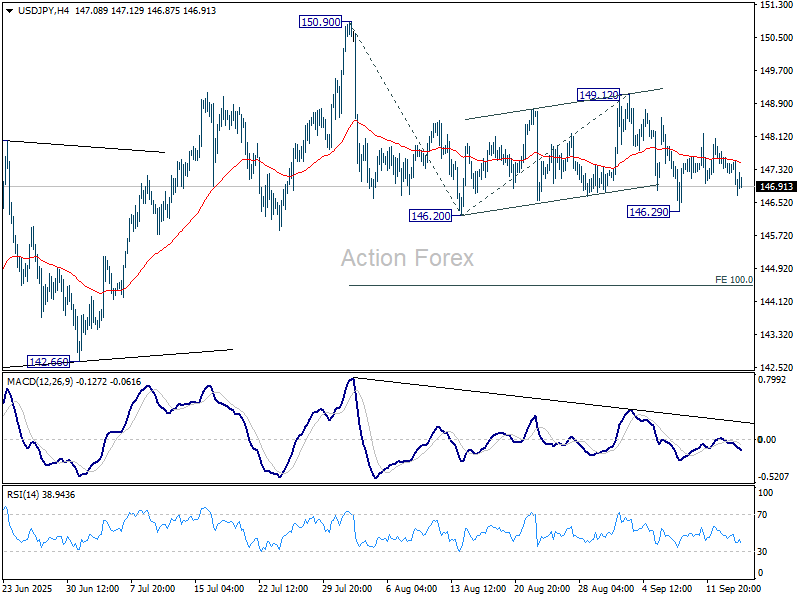

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.15; (P) 147.48; (R1) 147.73; More...

Intraday bias in USD/JPY remains neutral a,d with 149.12 resistance intact, further fall is in favor. On the downside, firm break of 146.29 support will solidify the case that whole rebound from 139.87 has completed with three waves up to 150.90. Deeper decline should then be seen to 100% projection of 150.90 to 146.20 from 149.12 at 144.42.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.