Sample Category Title

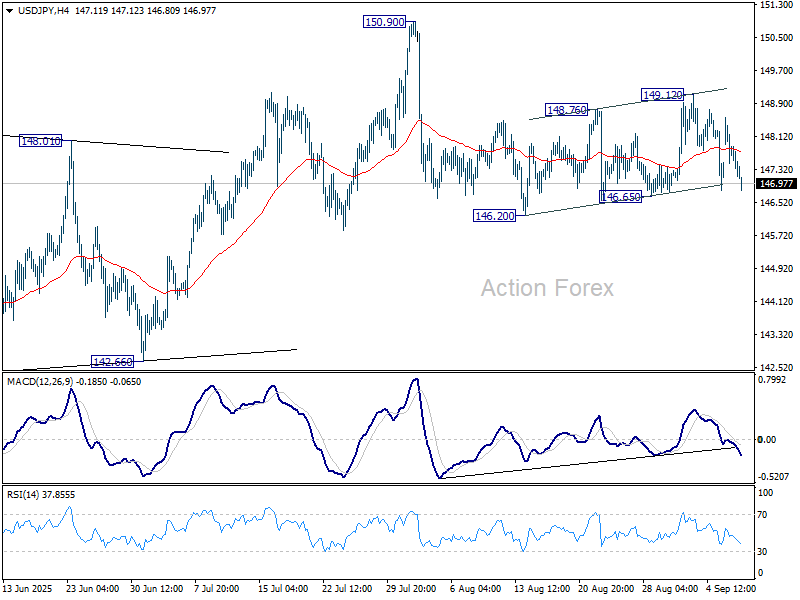

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.05; (P) 147.82; (R1) 148.29; More...

Range trading continues in USD/JPY and intraday bias stays neutral. On the downside, break of 146.65 will suggest that fall from 150.90 is resuming. More importantly, sustained trading below 55 D EMA (now at 147.15) will argue that whole rebound from 139.87 has completed with three waves up to 150.90. Deeper decline should then be seen to 142.66 support next. However, break of 149.12 will turn bias back to the upside for retesting 150.90.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

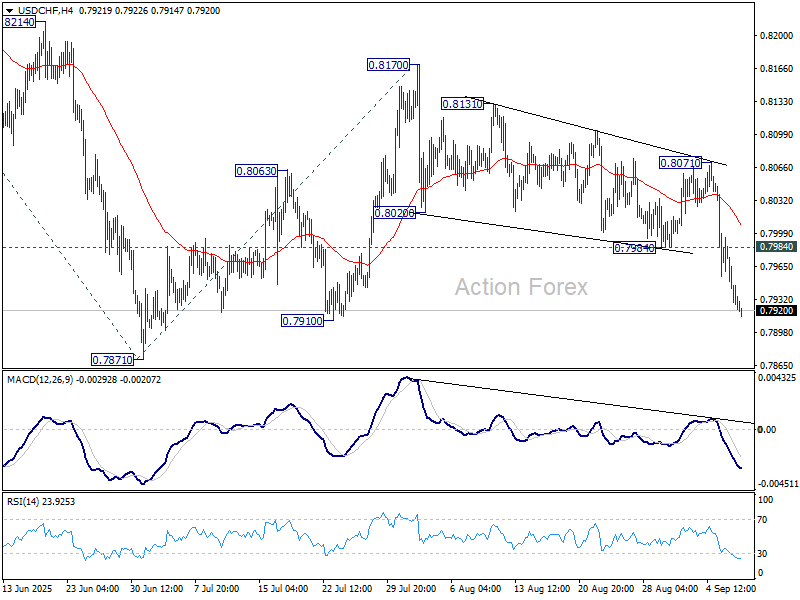

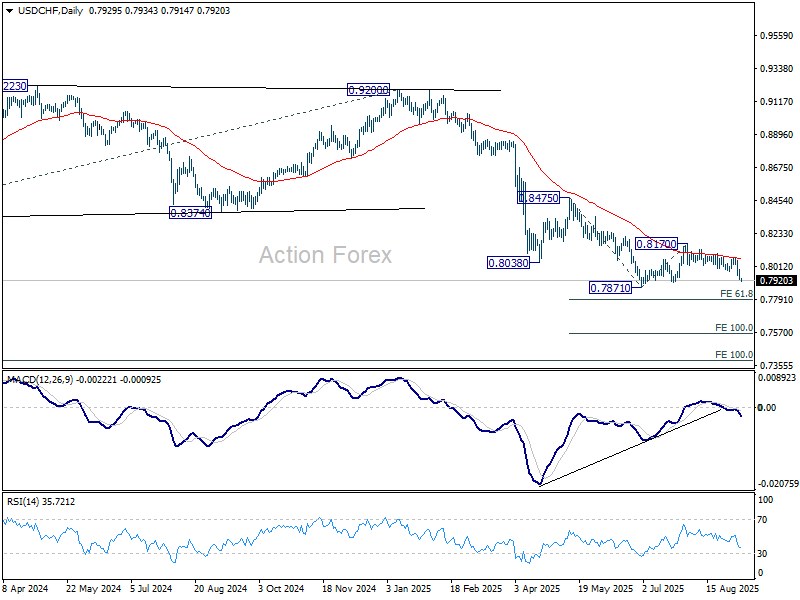

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7908; (P) 0.7952; (R1) 0.7976; More….

USD/CHF's decline is in progress and intraday bias stays on the downside for retesting 0.7871 low. Firm break there will resume larger down trend. Next target is 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797. On the upside, above 0.7984 resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.8071 resistance holds, in case of recovery.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

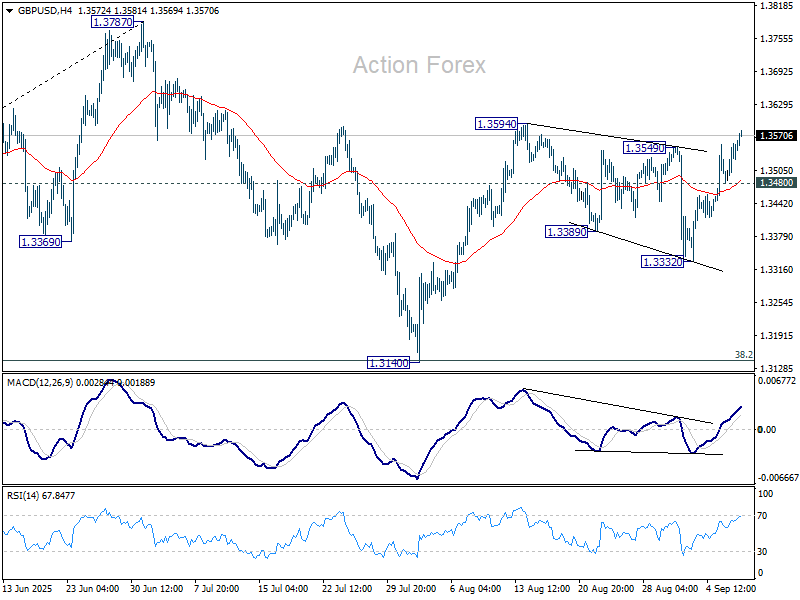

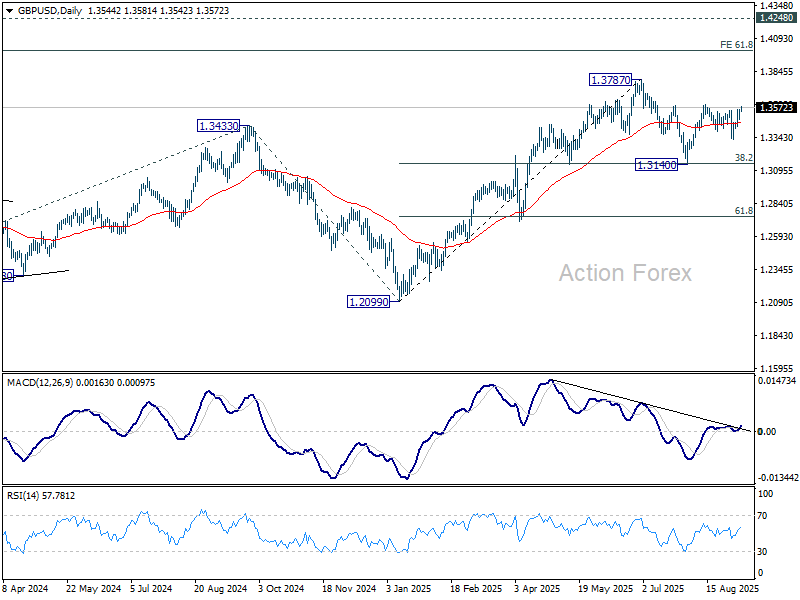

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3499; (P) 1.3528; (R1) 1.3574; More...

Intraday bias in GBP/USD remains on the upside at this point. Firm break of 1.3594 resistance will resume the rally from 1.3140 and target a retest on 1.3787 high. On the downside, below 1.3480 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 1.3332 support holds, in case of retreat.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3132) holds, even in case of deep pullback.

Gold Continues Its Rally

Last night, as widely expected, the French government collapsed after losing a confidence vote. The lower house’s unusual coalition of far-left and far-right deputies rejected the government’s plan to rein in France’s ballooning budget deficit. In his response, the outgoing PM François Bayrou warned: “you can change the government but you can’t change the reality” of rising and more expensive debt. Indeed, France’s 10-year yield, which dipped into negative territory before the pandemic, was trading near 3.6% last week before easing. The spread over German Bunds widened past the 80bp before narrowing again.

The French political deadlock looks set to continue, with both Marine Le Pen and Jean-Luc Mélenchon likely to oppose any successor government. After all, this is the third government change in a year and the fifth PM in less than two years. The question is why French bonds performed relatively well over the past sessions despite the looming collapse. Most likely, the risks were already priced in, and/or investors are betting that France will find a way to finance its deficit before the year-end deadline. Still, as the UK learned under Liz Truss’s mini-budget fiasco, market confidence can evaporate overnight. Today, UK 10-year gilts yield above 4.5% and with unappetizing outlook, leaving little fiscal headroom for Keir Starmer’s government, forcing policy adjustments through higher taxes or lower spending. France could face a similar fate if investors lose faith.

But for now, the market impact seems limited. The Stoxx 600 rose 0.5% yesterday, with the CAC 40 also higher, helped by expectations of lower Fed rates on horizon. European futures point to some downside pressure this morning, but the upbeat sentiment in the euro this morning suggests that the French news are not a big deal - it’s already baked into the market prices. The EURUSD is about to retest the 1.18 psychological resistance and with the French no confidence vote out of the way – with no surprise – the pair could clear resistance and look at the next hurdle: the 1.20 mark.

In the US, investors took weak jobs data as confirmation that the Federal Reserve (Fed) is preparing to cut rates at its next three meetings, with some betting on a 50bp move as early as September. The S&P 500 on Monday consolidated just below record highs, while the 2-year yield fell to its lowest in a year. Still, this week’s inflation data could reinforce or derail those bets. JPMorgan analysts warn of a potential “sell-the-news” reaction to Fed’s upcoming rate cuts and recommend hedging with gold and VIX futures.

Meanwhile Gold continues its rally, supported by central bank buying and demand from investors seeking alternatives to Treasuries. For those who still love Treasuries, softer US yields reduce the opportunity cost of holding gold, reinforcing the golden momentum. The metal is technically overbought, but Goldman Sachs recently noted that if just 1% of privately held Treasuries were reallocated into gold, the price could approach $5,000/oz. Too high? Remember that one Bitcoin is worth more than $111K this morning.

In energy, US crude rebounded yesterday and is extending gains, even after OPEC signaled higher output over the weekend. Many analysts doubt OPEC will engage in a price war: US shale production generally struggles below $60–65/bbl, and several OPEC members are already pumping near maximum capacity. That suggests support for prices in the $60–62pb range, reinforced by a weaker dollar and persistent geopolitical risks, including the no-peace scenario in Ukraine in the near future.

French PM Loses Confidence Vote

In focus today

In the US, the Bureau of Labor Statistics will publish its preliminary estimate of the annual benchmark revisions for Nonfarm Payrolls at 16CET. The revision affects data from April 2024 to March 2025. We expect a negative revision of -400k jobs.

In France, attention turns to President Macron and his reaction to the collapse of the government. The Elysee Palace has announced that Macron will appoint a new prime minister in the coming days, aligning with our baseline scenario. This eliminates the immediate downside risk of a snap election. However, political uncertainty is expected to persist, as a new government will still have a hard time passing a budget, particularly with significant spending cuts.

Economic and market news

What happened yesterday

In France, PM Francois Bayrou lost a confidence vote yesterday after seeking parliamentary support to reduce the country's debt burden. President Emmanuel Macron plans to appoint a new prime minister in the coming days, but no obvious candidate has emerged who could get parliament's backing for a budget. Bayrou warned that the country is "drowning in debt", but opposition parties continued to rebuff his proposals for spending cuts. The market reaction was muted, with the euro and French bond futures little changed as investors had expected Bayrou's downfall.

In Norway, the general election ended with a majority for the 'red-green' side. This implies that the Labour party will continue as a minority government, seeking support mainly on the red-green side. Even if this could prove challenging, we think the effect on financial markets is negligible, as fiscal policy still will be restricted by the fiscal rule (an oil-adjusted budget deficit limited to 3 % of the Petroleum Fund).

In the euro area, the Sentix investor confidence indicator came in lower than expected at -9.2 (prior: -3.7), signalling a rough start to September for consumer sentiment. The report revealed a drop in the Current Situation Index to -18.8 from -13, while the Expectations Index slipped to 0.8 from 6.0.

In Denmark, foreign trade data showed a 3.3% rise in exports for July, driven by services and goods produced abroad by Danish companies. At the same time, industrial production, excluding pharma, increased modestly and thus continues to recover along the rest of the European manufacturing sector. The outlook remains positive, supported by expected growth in neighbouring countries. However, US demand will be monitored closely as uncertainties persist around items like medicine and wind turbines, as well as the broader economy.

Equities: Equities were mostly higher yesterday, with the Stoxx 600 closing up 0.5% and the S&P 500 rising 0.2%. Just as Friday, lower bond yields explained the strength in equities. Growth stocks and small caps outperformed, led by sectors such as tech and consumer discretionary. Although absolute moves were mild, this was a risk-on session, with global cyclicals outperforming defensives by 1 p.p.

As our readers know, this goes against our expectation of how yields and their impulse on equities would unfold. The weaker-than-expected labor market explains the divergence. While we remain in the positive camp, expecting higher equities, our call was based on accelerating macro data and rising long-end yields. In the short term, this leaves us wrong on the value trade in the equity space.

FI&FX: While political developments in France - and to a minor extent Norway - have caught the headlines market reactions have thus far been very modest. Instead, the big story for rates and FX market has been the continued decline in yields and the bullish flattening of global curves as the steepener trade has lost steam. In both the US and Norway easing bets are on the rise in a week with key data releases ahead of next week's FOMC and Norges Bank meetings. When it comes to currency moves the rally in US fixed income has weighed on the USD with EUR/USD moving back close to 1.18. EUR/NOK and EUR/SEK remain little changed relative to Friday's close.

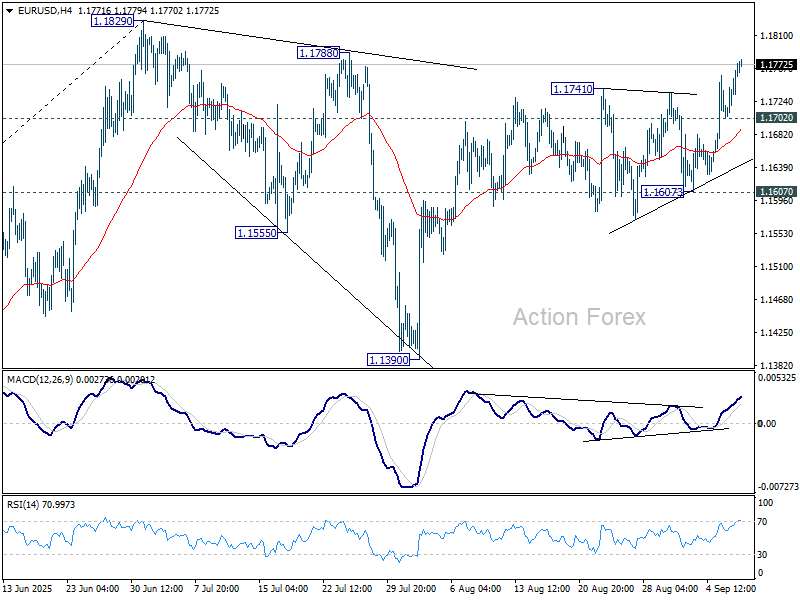

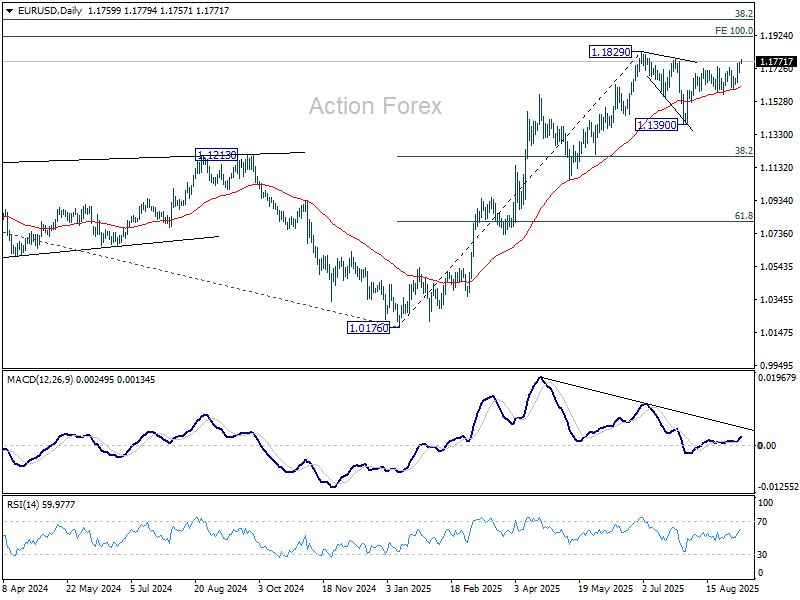

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1723; (P) 1.1745; (R1) 1.1785; More...

EUR/USD's rally continues today and intraday bias stays on the upside for retesting 1.1829. Firm break there will resume larger up trend to 1.1916 projection level. On the downside, below 1.1702 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 1.1607 support holds, in case of retreat.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

Greenback on the Brink, France Adds Pressure to Euro

Dollar weakened broadly overnight and selling pressure persisted in Asia on Tuesday, with the greenback on the verge of breaking recent lows against Euro, Swiss Franc, and Aussie. The decline comes amid falling U.S. Treasury yields and growing conviction that the Fed will move toward faster easing.

With no major U.S. releases scheduled today and the Fed in blackout mode ahead of next week’s FOMC, traders are still appearing impatient. Thursday’s CPI looms large, but speculative selling has already picked up, raising the risk that Dollar’s decline becomes self-reinforcing if technical levels give way.

Whether the move extends into a broader selloff remains a key focus. A break of recent lows in multiple pairs could invite further technical selling, especially if Thursday’s CPI shows softening price momentum. While a 50bps Fed cut next week is still unlikely, markets are increasingly pricing a dovish dot plot and statement.

At the same time, Euro is struggling under its own weight. France’s Prime Minister François Bayrou lost a confidence vote on Monday, ending a turbulent nine months in office. His departure makes him the fourth prime minister to collapse under President Emmanuel Macron’s second term, highlighting the persistent instability in French politics.

France now faces yet another stretch of political drift and uncertainty. Macron must quickly find a candidate palatable enough to avoid being brought down immediately, but precedent suggests the process could drag on. This instability has weighed on Euro, particularly against the Swiss franc, with investors turning defensive.

For the week so far, Dollar sits at the bottom of performance table, followed by Loonie and Yen. Yen, however, is rebounding as Nikkei retreats from record high and falling U.S. yields offer support. At the other end, Kiwi leads, followed by Aussie and Swiss franc, with Sterling and Euro mixed in the middle.

In Asia, at the time of writing, Nikkei is down -0.32%. Hong Kong HSI is up 0.64%. China Shanghai SSE is down 0.61%. Singapore Strait Times is down 0.42%. Japan 10-year JGB yield is down 0.004 at 1.564. Overnight, DOW rose 0.25%. S&P 500 rose 0.21%. NASDAQ rose 0.45%. 10-year yield fell -0.040 to 4.460.

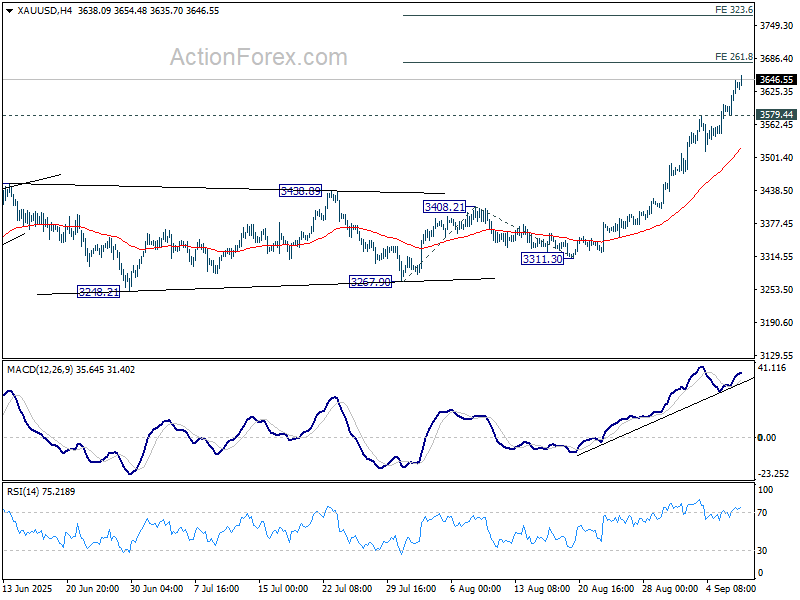

Gold rally may stretch to 3765 if US 10-year yield breaks 4%

The benchmark U.S. 10-year yield extended its recent slide on Monday, dropping to a five-month low. At the same time, Gold surged to another record high, reflecting strong demand for safety and conviction that inflation data due this week could steer the Fed toward faster easing.

Markets are squarely focused on the August PPI release on Wednesday, followed by Thursday’s CPI, which will be critical in shaping expectations ahead of next week’s FOMC meeting. Any evidence of cooling inflation risks could soften Fed hawks’ resistance to faster rate cuts. While a 50bps move in September remains unlikely, the statement and dot plot could flag a steeper path of easing.

That possibility is keeping pressure on U.S. yields. Key attention is on the 4% mark for the 10-year yield. A clean break below this psychological level could spur an even deeper slide

Technically, 10-year has already broken through 100% projection of 4.629 to 4.205 from 4.493 at 4.069, with no sign of bottoming yet. It is also pressing against the lower bound of its near-term falling channel. Sustained break there will indicate further acceleration to 138.2% projection at 3.907 next, with prospect of diving to 3.886 support. In any case, outlook will stay bearish as long as 4.188 support turned resistance holds.

Gold, meanwhile, remains in a phase of upward re-acceleration, as indicated by 4H MACD. It's on track to 261.8% projection of 3267.90 to 3408.21 from 3311.30 at 3678.63. Overbought condition as seen in 4H RSI could limit upside there on first attempt. But break of 3579.44 support is needed to indicate temporary topping first.

Meanwhile, if the 10-year yield breaks below 4% in the coming days, Gold’s rally could extend further, eyeing 323.6% projection at 3765.34 before a peak is established. For now, both Treasuries and bullion look unstoppable, with inflation data set to determine the next leg of momentum.

Westpac: Australia consumer optimism elusive, RBA to pause in September

Australia’s Westpac Consumer Sentiment Index dropped -3.1% mom to 95.4 in September, reversing part of last month’s boost from the RBA’s third rate cut. While sentiment remains modestly above July levels and well above the April tariff-driven low, the index has slipped back into “cautiously pessimistic” territory. Westpac said outright optimism remains "elusive", with households still uneasy about the path ahead despite relief from the cost-of-living crisis.

The RBA is expected to keep its cash rate steady at 3.6% when it meets later this month. Westpac noted recent data on inflation and demand came in "somewhat firmer than expected", reinforcing the case for caution. Policymakers are seen waiting for further confirmation that underlying trends remain benign before resuming cuts.

For now, consumer recovery looks sluggish, and Westpac expects "further easing will likely be needed" to sustain momentum. It forecasts another 25bp cut in November and two additional moves in 2026, underscoring the gradual path ahead for both sentiment and policy.

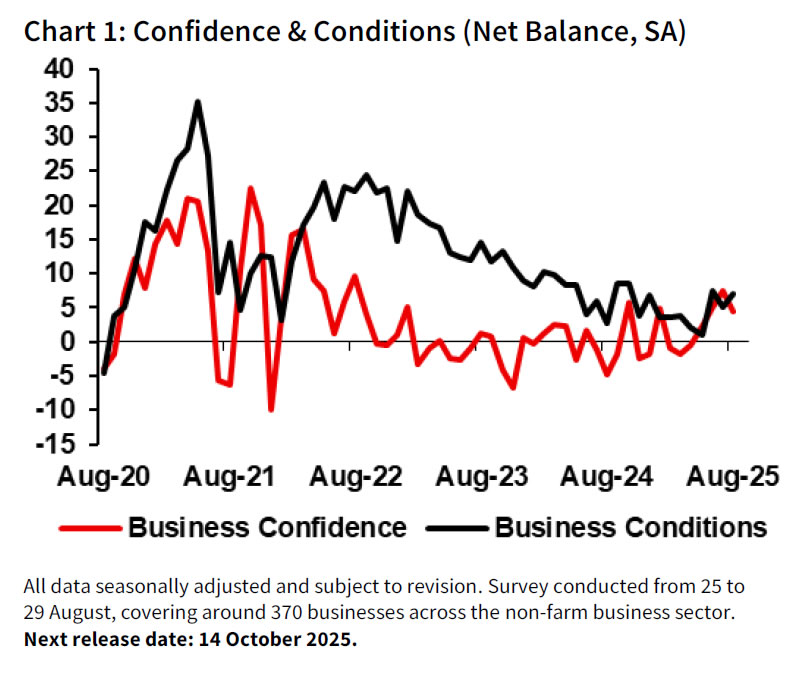

Australia NAB business survey: Confidence falls, costs ease, capacity still tight

Australia’s NAB Business Confidence index slipped from 8 to 4 in August, but conditions showed improvement, rising from 5 to 7. Trading remained steady at 12, while profitability rose from 2 to 4 and employment from 2 to 5. NAB Chief Economist Sally Auld said the results support the view that “the outlook for businesses continues to improve,” with both confidence and conditions now near long-run averages.

Capacity utilisation rose to 83.1% from 82.5%, staying two percentage points above its long-run norm. Capital expenditure intentions also improved, climbing from 8 to 10. Together, these suggest firms are still operating at high levels of resource use despite broader uncertainties.

At the same time, cost pressures eased further. Purchase cost growth slowed from 1.3% to 1.1%, its lowest since 2021, while labour costs moderated to from 1.9% 1.5% and product price growth dipped to from 0.8% 0.6%. The survey points to an environment of resilient business activity and capacity tightness, but with inflation pressures continuing to recede.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1723; (P) 1.1745; (R1) 1.1785; More...

EUR/USD's rally continues today and intraday bias stays on the upside for retesting 1.1829. Firm break there will resume larger up trend to 1.1916 projection level. On the downside, below 1.1702 minor support will turn intraday bias neutral first. But risk will stay on the upside as long as 1.1607 support holds, in case of retreat.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

Gold rally may stretch to 3765 if US 10-year yield breaks 4%

The benchmark U.S. 10-year yield extended its recent slide on Monday, dropping to a five-month low. At the same time, Gold surged to another record high, reflecting strong demand for safety and conviction that inflation data due this week could steer the Fed toward faster easing.

Markets are squarely focused on the August PPI release on Wednesday, followed by Thursday’s CPI, which will be critical in shaping expectations ahead of next week’s FOMC meeting. Any evidence of cooling inflation risks could soften Fed hawks’ resistance to faster rate cuts. While a 50bps move in September remains unlikely, the statement and dot plot could flag a steeper path of easing.

That possibility is keeping pressure on U.S. yields. Key attention is on the 4% mark for the 10-year yield. A clean break below this psychological level could spur an even deeper slide

Technically, 10-year has already broken through 100% projection of 4.629 to 4.205 from 4.493 at 4.069, with no sign of bottoming yet. It is also pressing against the lower bound of its near-term falling channel. Sustained break there will indicate further acceleration to 138.2% projection at 3.907 next, with prospect of diving to 3.886 support. In any case, outlook will stay bearish as long as 4.188 support turned resistance holds.

Gold, meanwhile, remains in a phase of upward re-acceleration, as indicated by 4H MACD. It's on track to 261.8% projection of 3267.90 to 3408.21 from 3311.30 at 3678.63. Overbought condition as seen in 4H RSI could limit upside there on first attempt. But break of 3579.44 support is needed to indicate temporary topping first.

Meanwhile, if the 10-year yield breaks below 4% in the coming days, Gold’s rally could extend further, eyeing 323.6% projection at 3765.34 before a peak is established. For now, both Treasuries and bullion look unstoppable, with inflation data set to determine the next leg of momentum.

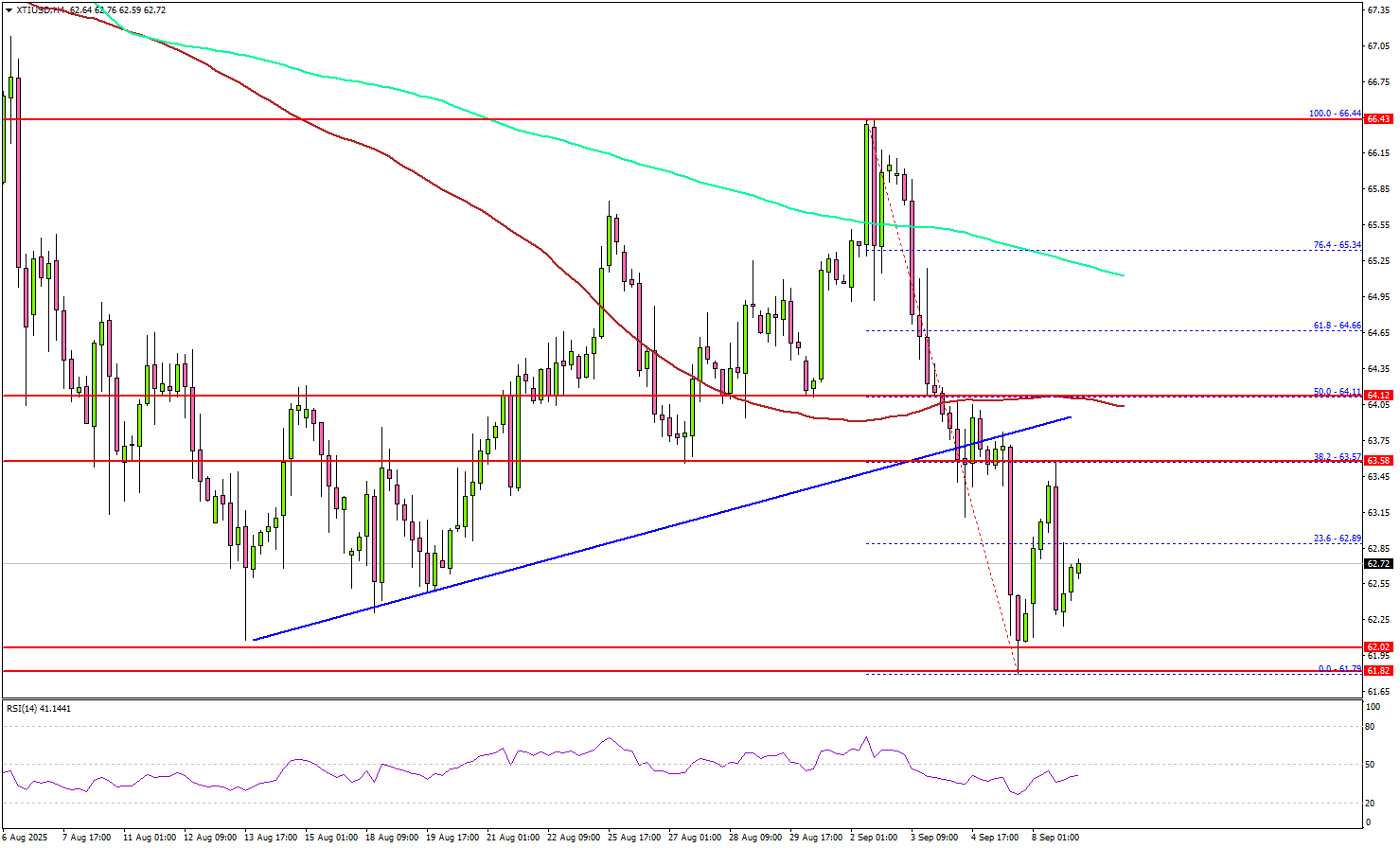

WTI Crude Oil Slide – Key Levels Every Trader Must Watch Now

Key Highlights

- WTI Crude Oil prices started a fresh decline below the $64.20 support.

- The price traded below a key bullish trend line with support at $63.80 on the 4-hour chart.

- Gold rallied further to a new all-time high above $3,640.

- Bitcoin is attempting to recover but upside might be capped near $115,000.

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price failed to stay above $65.50 against the US Dollar. There was a strong bearish reaction below $65.00 and $64.00.

Looking at the 4-hour chart of XTI/USD, the price traded below a key bullish trend line with support at $63.80. There was a close below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

A low was formed at $61.79 before there was a minor recovery wave. However, the bears are still active below $64.00. On the upside, immediate resistance is near the $63.50 level.

The first key hurdle for the bulls could be near the 100 simple moving average (red, 4-hour) at $64.00. A close above $64.00 might send Oil prices toward the 61.8% Fib retracement level of the downward move from the $66.44 swing high to the $61.79 low at $65.35.

Any more gains might call for a test of $66.50 in the near term. On the downside, the first major support sits near the $61.80 zone. The next support could be $60.50. A daily close below $60.50 could open the doors for a larger decline.

In the stated case, the bears might aim for a drop toward $58.00. Any more losses could open the doors for a test of the $50.00 handle.

Looking at Gold, the bulls remained in action, and they pushed the price to a new all-time high above the $3,640 level.

Economic Releases to Watch Today

- NFIB Business Optimism Index for Aug 2025 – Forecast 101.0, versus 100.3 previous.

- Nonfarm Payrolls Benchmark Revision.

Australia NAB business survey: Confidence falls, costs ease, capacity still tight

Australia’s NAB Business Confidence index slipped from 8 to 4 in August, but conditions showed improvement, rising from 5 to 7. Trading remained steady at 12, while profitability rose from 2 to 4 and employment from 2 to 5. NAB Chief Economist Sally Auld said the results support the view that “the outlook for businesses continues to improve,” with both confidence and conditions now near long-run averages.

Capacity utilisation rose to 83.1% from 82.5%, staying two percentage points above its long-run norm. Capital expenditure intentions also improved, climbing from 8 to 10. Together, these suggest firms are still operating at high levels of resource use despite broader uncertainties.

At the same time, cost pressures eased further. Purchase cost growth slowed from 1.3% to 1.1%, its lowest since 2021, while labour costs moderated to from 1.9% 1.5% and product price growth dipped to from 0.8% 0.6%. The survey points to an environment of resilient business activity and capacity tightness, but with inflation pressures continuing to recede.