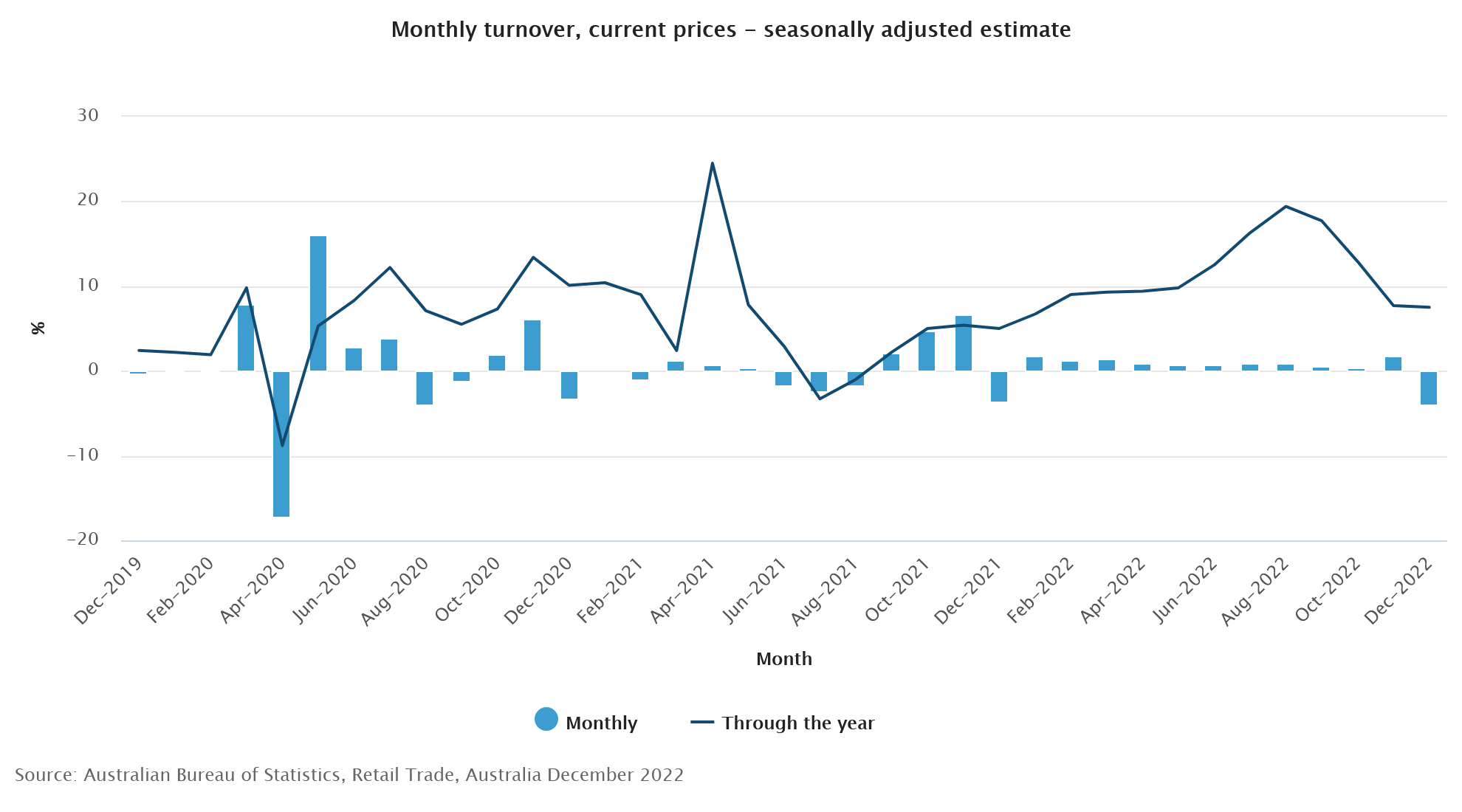

Australia retail sales turnover dropped sharply by -3.9% mom to AUD 34.47m in December, much worse than expectation of -0.3% mom. That’s the first contraction after 11 straight months of growth. Still, sales turnover remained elevated at its sixth highest level on record, and was up 7.5% yoy for the year.

Ben Dorber, ABS head of retail statistics, said: “The large fall in December suggests that retail spending is slowing due to high cost-of-living pressures… The latest Consumer Price Index showed that prices continued to rise strongly in the December quarter. To see the effect of consumer prices on recent turnover growth, it will be important to look at quarterly retail sales volumes which we will release next week.”

China official PMI manufacturing rose to 50.1, non-manufacturing up to 54.4

China official PMI Manufacturing rose from 47.0 to 50.1 in December, slightly below expectation of 50.2. PMI Non-Manufacturing jumped from 41.6 to 54.4, above expectation of 51.0. Both indexes were also back in expansion region.

Senior NBS statistician Zhao Qinghe noted that economic activity returned to expansion amid an improvement in the business operation climate and the situation.

“Meanwhile, many companies in the manufacturing and services sectors still reported a lack of market demand is the major concern for their businesses. The foundation of economic recovery still needs to be further consolidated,” he added.