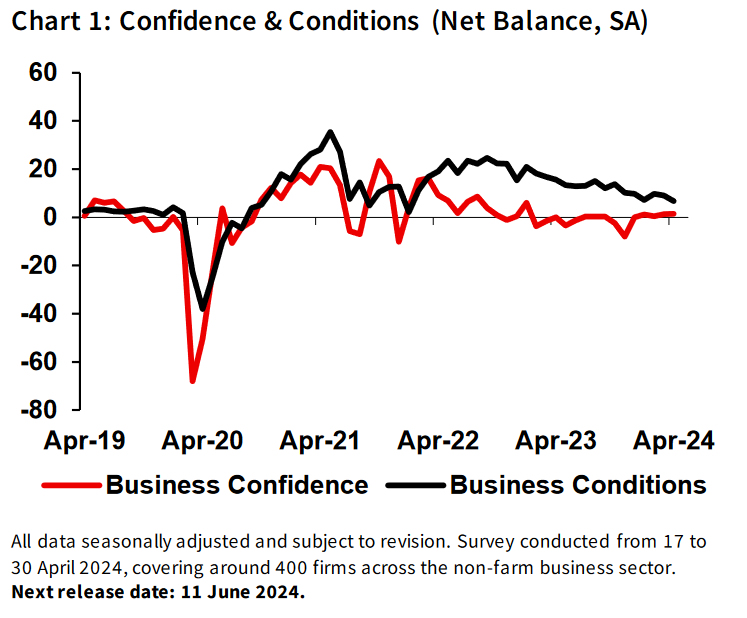

Australia’s NAB Business Confidence held steady at 1 in April. Business Conditions index fell from from 9 to 7. Notably, trading conditions declined from 15 to 12, while profitability was unchanged at 6. A significant reduction was observed in employment conditions, which dropped from 6 to 2.

NAB Chief Economist Alan Oster reflected on these figures: “All three components of business conditions were back at their long-run averages in April.” He described this as a milestone, marking a normalization after the unusually high levels of 2022, “reflecting slowing economic growth.”

Labour cost growth decreased to 1.5% from 1.7%, and purchase cost growth slowed to 1.2% from 1.5%. Meanwhile, product price growth rose slightly to 0.9% from 0.7%. Retail price growth moderated significantly to 0.9% from 1.4%.

Oster noted, “There was some further improvement in the pace of cost growth in April, and a step down in the pace of retail price growth.” He suggested these changes could indicate easing in inflation in the second quarter, though further observation is needed to confirm this trend.

RBNZ survey shows moderating short-term inflation expectations

According to RBNZ Business Expectations Survey for Q2, respondents have lowered their expectations for CPI inflation in both the short-term and medium-term, while their long-term CPI inflation expectations have remained stable.

Specifically, one-year-ahead annual inflation expectations have notably decreased by 49 bps, moving from 3.22% to 2.73%. Two-year-ahead inflation expectations also saw a decline from 2.50% to 2.33%. Five-year-ahead inflation expectations are holding steady at 2.25%. Ten-year-ahead expectations edged up slightly by 3bps, from 2.16% to 2.19%.

Regarding the Official Cash Rate, survey respondents anticipate that it to 5.46% by the end Q2, similar to current rate at 5.50%. Looking further ahead, they forecast a reduction in OCR to 4.79% by the end of Q1 2025, marking a slight increase from last quarter’s prediction of 4.74%. These expectations align with anticipation of approximately three rate cuts by the end of Q1 next year.

Full RBNZ business expectations survey here.